Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

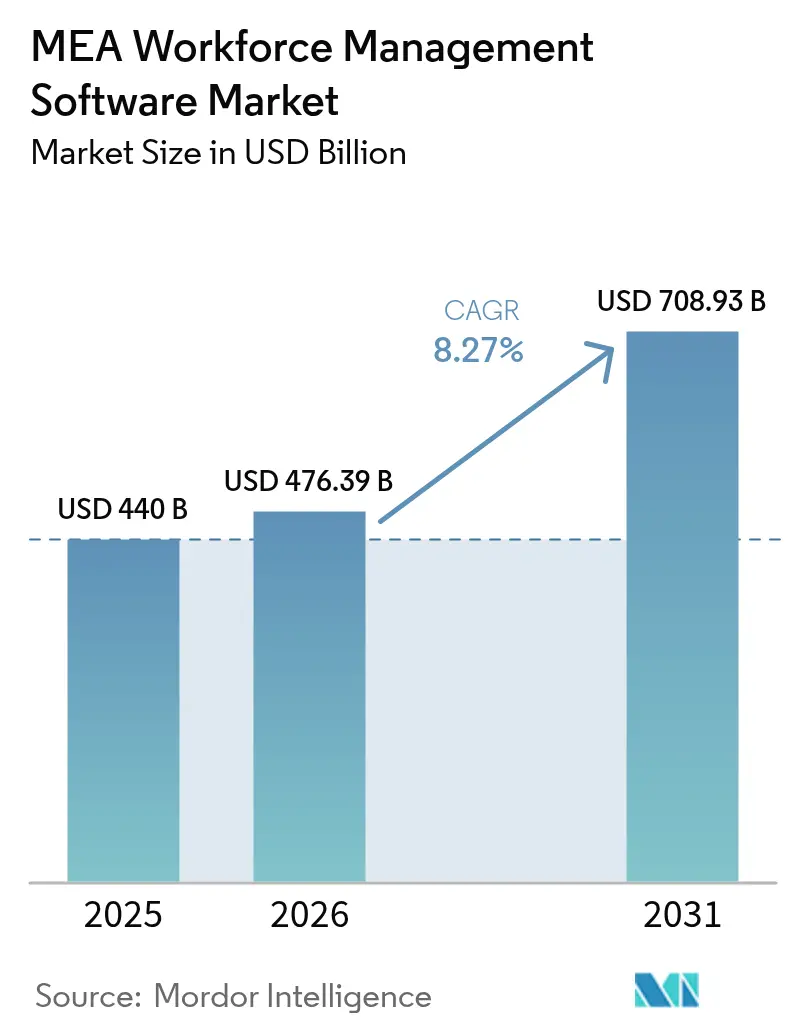

| Base Year Market Size (2025) | USD 440 Billion |

| Market Size (2026) | USD 476.39 Billion |

| Market Size (2031) | USD 708.93 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEA Workforce Management Software Market Analysis by Mordor Intelligence

The MEA Workforce Management Software market size is expected to grow from USD 440 million in 2025 to USD 476.39 million in 2026 and is forecast to reach USD 708.93 million by 2031 at 8.27% CAGR over 2026-2031. Demand is accelerating as public-sector digital initiatives such as Saudi Arabia’s Vision 2030 and the UAE’s Industry 4.0 programme expand the addressable base of employers seeking cloud-ready scheduling, attendance, and analytics tools. Cloud deployment already underpins two-thirds of all installations, a share strengthened by vendors’ performance gains after shifting to hyperscale infrastructure. Regulatory pressure to automate overtime tracking, the emergence of AI-powered optimisation suites, and the region’s large deskless workforce further lift adoption, while mega-projects such as NEOM add sizable new user pools that require sophisticated orchestration.

Key Report Takeaways

- By solution type, Time & Attendance Management led with 33.62% revenue share in 2025, whereas Workforce Analytics is forecast to expand at a 9.31% CAGR to 2031.

- By deployment mode, Cloud captured 65.25% of the MEA Workforce Management Software market share in 2025 and is advancing at a 10.02% CAGR through 2031.

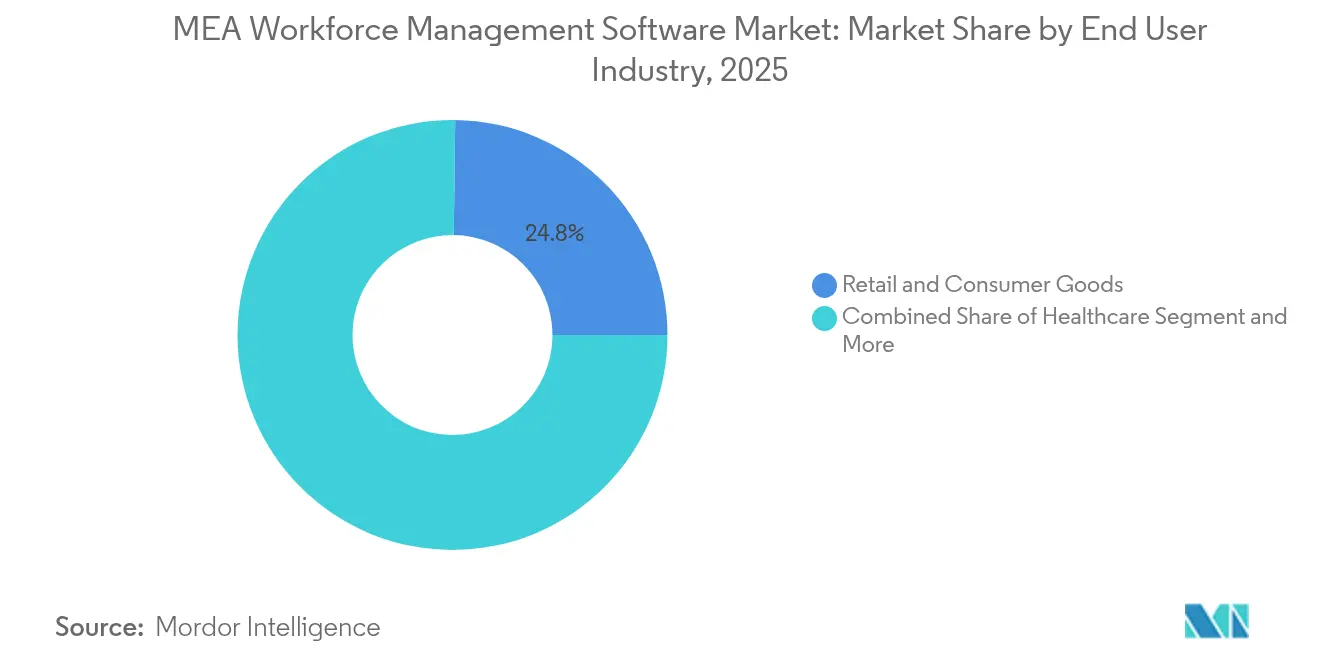

- By end-user industry, Retail & Consumer Goods dominated with 24.80% of the MEA Workforce Management Software market size in 2025, while Healthcare posts the fastest 8.43% CAGR to 2031.

- By organisation size, Large Enterprises held 56.65% share of the MEA Workforce Management Software market size in 2025, whereas Medium Enterprises recorded the highest 8.97% CAGR.

- By geography, Saudi Arabia commanded 30.70% of the MEA Workforce Management Software market size in 2025; Nigeria is projected to deliver a 8.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

MEA Workforce Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based WFM adoption surge | +2.1% | UAE, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Regulatory overtime-tracking mandates | +1.8% | MENA core, Sub-Saharan Africa | Short term (≤ 2 years) |

| Mobile-first WFM via smartphone ubiquity | +1.5% | Nigeria, Egypt, Kenya | Short term (≤ 2 years) |

| Labor-cost optimisation amid diversification | +1.3% | Saudi Arabia, UAE, Nigeria, South Africa | Medium term (2-4 years) |

| Gig and quick-commerce workforce expansion | +1.0% | Urban UAE, Saudi Arabia, Egypt | Medium term (2-4 years) |

| Mega-project workforce orchestration needs | +0.9% | Saudi Arabia, UAE, Qatar, Oman | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud Infrastructure Modernization Accelerates WFM Adoption

Cloud deployment already underpins most new projects, and its 65.70% share reflects employers’ preference for rapid scalability, automated updates, and cross-border availability. The Saudi National Skills Platform adds momentum by embedding cloud architecture in state-backed skilling programmes. WorkForce Software’s migration from Azure to Oracle Cloud yielded a 40% performance gain, illustrating the operational upside.[1]Oracle, “WorkForce Software moves from Azure to Oracle Cloud,” oracle.com Compliance is another catalyst: the UAE’s employee-monitoring framework favours SaaS suites that provide audit trails and consent management by default. Mega-projects such as NEOM, whose headcount can swing by tens of thousands within months, underline why elastic capacity is critical.

Regulatory Compliance Mandates Drive Time-Tracking Sophistication

Time and Attendance Management retains its lead because overtime rules differ markedly across MEA jurisdictions. The International Labour Office’s guidelines push enterprises to deploy configurable systems capable of country-level rule sets.[2]International Labour Office, “Overtime,” ilo.org SAP SuccessFactors’ 2024 release added Microsoft Teams punch-in and automated payroll-cycle alignment to address this complexity. Africa-wide labour-law changes slated for 2025, including Zambia’s pending overtime legislation, heighten demand for compliant digital tracking. Transaction volumes on Saudi Arabia’s Qiwa platform underscore the scale of regulatory automation already in play, with 126 million transactions processed in 2023.

Mobile-First Solutions Capitalize on Smartphone Penetration

Deskless workers form the majority of the regional labour force, making mobile access non-negotiable. WorkForce Software’s SAP Deskless Worker Experience add-on delivers intuitive interfaces for field personnel in sectors such as manufacturing and logistics. Nigerian vendors SeamlessHR and peopleHum also stress mobile usability to reach the country’s large informal segment. The World Bank counts hundreds of regional gig platforms serving SMEs, reinforcing the strategic importance of smartphone-centric scheduling, pay and task modules.

AI-Powered Analytics Transform Workforce Optimisation

Workforce Analytics is the fastest-growing solution category as employers pivot from reactive scheduling to predictive optimisation. UKG’s Bryte AI Agents automate promotion pathways and compliance checks, demonstrating value beyond traditional WFM boundaries. NICE’s CXone Mpower combines AI routing with performance analytics to orchestrate human and virtual agents end-to-end. Blue Yonder clients report double-digit labour-cost savings after embedding predictive models in shift design. Venture-funded startups such as Queen.ai add further momentum by building autonomous optimisation tools for e-commerce fulfilment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration cost and complexity | -1.2% | MEA-wide SMEs | Medium term (2-4 years) |

| Shortage of WFM analytics talent | -0.8% | Nigeria, Egypt, Morocco | Long term (≥ 4 years) |

| Data-residency barriers to cloud rollout | -0.6% | MENA core | Short term (≤ 2 years) |

| Cultural push-back on real-time tracking | -0.4% | Traditional sectors across MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Creates Implementation Barriers

Two-thirds of MEA SMEs struggle to integrate WFM suites with legacy HR and payroll stacks, extending project timelines and elevating total cost of ownership.[3]CloudPay, “Global Payroll Efficiency Index,” cloudpay.com SAP SuccessFactors can charge implementation fees equal to the first year’s subscription, amplifying budget hurdles for mid-market buyers. Yet successful roll-outs signal quantifiable returns: Visa’s consolidated HCM environment cut payroll processing costs materially, illustrating payback potential.

Cultural Resistance to Real-Time Monitoring Persists

Privacy sensitivities can slow adoption in family-owned enterprises and sectors where employee surveillance is viewed skeptically. The UAE mandates explicit consent for monitoring, pushing vendors to design transparency-first features. Human-centric alternatives such as Aware360’s Aware4Duty verify fitness for duty without invasive oversight. ATOSS demonstrates the commercial viability of people-first scheduling, posting USD 27.9 million revenue while serving 15,000 clients worldwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Analytics Drive Next-Generation Intelligence

Time and Attendance Management retained 33.62% of overall revenue in 2025 as organisations prioritised compliance under divergent overtime statutes across MEA. Workforce Analytics, while smaller, is expanding at 9.31% CAGR on the back of AI-driven forecasting and prescriptive insights. The Promotion Agent inside UKG Bryte trims manual HR workflows, illustrating practical AI value. SAP SuccessFactors embeds predictive goal suggestions and skills validation to elevate performance management. As enterprises graduate from punch clocks to analytics dashboards, the MEA Workforce Management Software market repeatedly absorbs add-on modules that stretch far beyond basic scheduling.

Increasing demand for fatigue and field-service optimisation tools is visible in safety-critical industries. Pulsar Informatics’ Fleet Insight offers fatigue risk scoring for aviation operators, meeting regulatory flight-duty constraints. The MEA Workforce Management Software market therefore exhibits a clear shift toward unified suites that integrate compliance, wellbeing and data-driven forecasting.

By Deployment Mode: Cloud Dominance Accelerates Digital Transformation

Cloud captured 65.25% share in 2025 and is on a 10.02% CAGR trajectory, reflecting a decisive pivot away from on-premise upkeep. WorkForce Software’s move to Oracle Cloud lifted system performance by 40%, providing a benchmark for ROI discussions. Enterprises with stringent sovereignty mandates turn to Workday-on-AWS deployments that house data within local jurisdictions yet retain SaaS agility. Hybrid roll-outs remain relevant where corporate groups operate both in regulated petro-states and lightly regulated markets, underscoring the MEA Workforce Management Software market’s need for architectural flexibility.

Continuum Global Solutions’ switch to NICE IEX cloud suite achieved 99.5% uptime and broader self-service adoption, underscoring operational benefits that now outweigh migration pain points for many adopters. As hyperscale data-centre footprints expand in MENA, infrastructural concerns recede, reinforcing cloud’s leadership.

By End-User Industry: Healthcare Leads Digital Adoption Surge

Retail and Consumer Goods held 24.80% revenue share in 2025, reflecting the sector’s intricate peak-season scheduling across malls and e-commerce fulfilment. Healthcare, though smaller, is registering an 8.43% CAGR as hospitals formalise post-pandemic staffing protocols. Frankfurt University Hospital’s deployment of ATOSS illustrates specialist modules that balance staff preferences with patient safety. Manufacturing gains traction via Saudi Arabia’s Industry 4.0 incentives, where sensor-integrated production lines require synchronised labour allocation.

Logistics adoption rises alongside regional e-commerce expansion. Amazon’s new Abu Dhabi delivery station created hundreds of tech-enabled jobs, all requiring dynamic roster management. Energy and Utilities value fatigue-risk mitigation, and mining enterprises in South Africa adopt Pal Solutions to trim payroll expenses by up to 40% through automation.

By Organization Size: Medium Enterprises Drive Market Expansion

Large Enterprises commanded 56.65% of 2025 spending, yet Medium Enterprises chart the steepest growth at 8.97% CAGR as SaaS pricing lowers entry barriers. UKG’s tiered portfolio combines flagship suites with UKG Ready for smaller entities, capturing demand across company sizes. Dayforce Partner Exchange gives mid-market buyers vetted plug-ins and service partners, shortening integration cycles. The MEA Workforce Management Software market consequently benefits from a cascading effect: as large enterprises standardise digital workflows, peers in the supply chain follow suit to stay competitive.

Small Enterprises in Nigeria and Egypt increasingly trial low-cost, mobile-centric tools such as peopleHum, signaling long-term upside once compliance mandates extend into the informal sector. The World Bank’s estimate of hundreds of regional gig platforms validates the micro-enterprise opportunity, foreshadowing incremental volume for cloud vendors.

Geography Analysis

Saudi Arabia remains the largest spender, accounting for 30.70% of the MEA Workforce Management Software market size in 2025. Government-backed platforms such as Qiwa serve more than 10 million users and automate 135 HR services ranging from contract verification to visa issuance. The NEOM build-out alone shifts workforce counts from 140,000 to a targeted 200,000 within a year, reinforcing demand for high-throughput orchestration. Add Vision 2030 incentives for smart factories and the Kingdom presents a consistent growth engine for vendors.

Nigeria posts the fastest 8.88% CAGR, underpinned by indigenous platforms that bundle core HR, payroll and analytics into mobile-first packages. SeamlessHR’s traction among mid-size firms illustrates how local language support and naira pricing reduce adoption friction. Employer-of-record providers such as Playroll make it easier for foreign organisations to hire Nigerian talent compliantly, indirectly boosting software penetration.

The UAE sustains premium per-user spending through continuous logistics and service-sector expansion. Amazon’s Abu Dhabi mega-station highlights the country’s role as a regional fulfilment hub, where cloud-native scheduling ensures next-day delivery standards. South Africa shows rising cloud payroll adoption as cross-border compliance complicates on-premise upkeep; PaySpace leverages local legislation libraries to win multi-country clients. Egypt gains momentum from International Labour Organisation programmes aimed at equipping youth and refugees for platform work, necessitating scalable rostering solutions.

Competitive Landscape

The vendor arena exhibits moderate concentration: global majors dominate enterprise roll-outs, yet regional specialists secure niche wins through localisation. UKG leads in breadth, booking USD 4.4 billion FY 2023 revenue, roughly 45% of which is tied to workforce management. Continuous product renewal—evident in the Bryte AI Agents suite—cements its strategic edge. SAP SuccessFactors leverages embedded AI across modules, while WorkForce Software differentiates via performance gains from Oracle Cloud migration.

Acquisition-driven capability stacking reshapes the field. Ceridian’s purchase of eloomi enriches Dayforce with learning-experience features, aligning with demand for integrated skilling paths. IBM’s planned acquisition of Applications Software Technology augments Oracle Cloud delivery depth for public-sector clients. Regional champions such as MenaITech capitalise on Arabic interfaces and local labour-law engines, while Pal Solutions targets mining verticals with cost-cutting HCM automation.

Innovation awards underline competitive heat: NICE’s CXone Mpower Orchestrator swept Enterprise Connect 2025 accolades for end-to-end AI automation. Start-ups such as Qeen.ai secure eight-figure funding rounds to build autonomous scheduling for e-commerce micro-fulfilment. Taken together, the MEA Workforce Management Software market rewards both scale and specialisation, encouraging alliances that fuse global AI capabilities with granular localisation.

MEA Workforce Management Software Industry Leaders

Active Ops Management International LLP

ADP LLC

Atoss Software AG

Blue Yonder Group Inc.

Ceridian HCM Inc. (Dayforce)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UKG unveiled Bryte AI Agents within the UKG Pro suite, introducing Promotion and Continuous Compliance Agents to automate HR workflows while maintaining human oversight.

- January 2025: IBM announced intent to acquire Applications Software Technology LLC, expanding Oracle Cloud Application expertise for regulated-sector clients.

- January 2025: Blue Yonder introduced Integrated Demand and Supply Planning modules that apply machine learning to balance cost and service in real time.

- November 2024: NICE launched CXone Mpower SmartSpeak, enabling real-time multilingual service across nearly 100 languages.

MEA Workforce Management Software Market Report Scope

Workforce management software enables organizations to centralize resource usage data and better plan future utilization. It allows companies to create custom workflows to be more efficient in their decision-making processes and protect data integrity. To manage several aspects of the workforce for better productivity, the market software solutions include workforce forecast and scheduling, time and attendance management, task management, HR management, and other solutions, including workforce analytics.

The Middle East and African Workforce Management Software Market is segmented by type the market is segment into workforce scheduling and workforce analytics, time and attendance management, performance and goal management, and absence and leave management, by deployment mode the market is segment into on-premise, cloud, by end-user vertical the market is segment into BFSI, consumer goods and retail, automotive, energy and utilities, healthcare, and manufacturing, by country the market is segment into United Arab Emirates, Saudi Arabia, South Africa, rest of Middle East and Africa. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Solution Type

| Workforce Scheduling and Analytics |

| Time and Attendance Management |

| Performance and Goal Management |

| Absence and Leave Management |

| Fatigue, Task and Field Service WFM |

By Deployment Mode

| On-Premise |

| Cloud |

By End-user Industry

| BFSI |

| Retail and Consumer Goods |

| Healthcare |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Hospitality |

| Other Industries |

By Organisation Size

| Large Enterprises (?1 000 staff) |

| Medium Enterprises (250-999) |

| Small Enterprises (<250) |

By Country

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Egypt |

| Rest of Middle East and Africa |

| By Solution Type | Workforce Scheduling and Analytics |

| Time and Attendance Management | |

| Performance and Goal Management | |

| Absence and Leave Management | |

| Fatigue, Task and Field Service WFM | |

| By Deployment Mode | On-Premise |

| Cloud | |

| By End-user Industry | BFSI |

| Retail and Consumer Goods | |

| Healthcare | |

| Manufacturing | |

| Energy and Utilities | |

| Transportation and Logistics | |

| Hospitality | |

| Other Industries | |

| By Organisation Size | Large Enterprises (?1 000 staff) |

| Medium Enterprises (250-999) | |

| Small Enterprises (<250) | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the MEA Workforce Management Software market?

The market is valued at USD 476.39 million in 2026 and is set to grow to USD 708.93 million by 2031.

Which country leads spending on workforce management solutions in MEA?

Saudi Arabia leads with 30.70% of regional spending, buoyed by government digital platforms and mega-projects.

Why is cloud deployment preferred in the region?

Cloud offers scalability, built-in compliance and performance gains—as evidenced by a 40% speed uplift after WorkForce Software shifted to Oracle Cloud.

Which solution segment is expanding fastest?

Workforce Analytics is growing at 9.31% CAGR due to AI-driven forecasting and prescriptive insights.

How are medium-sized enterprises influencing demand?

Medium Enterprises show a 8.97% CAGR, propelled by SaaS pricing models and ecosystem platforms that reduce integration hurdles.

Page last updated on: