Content Moderation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

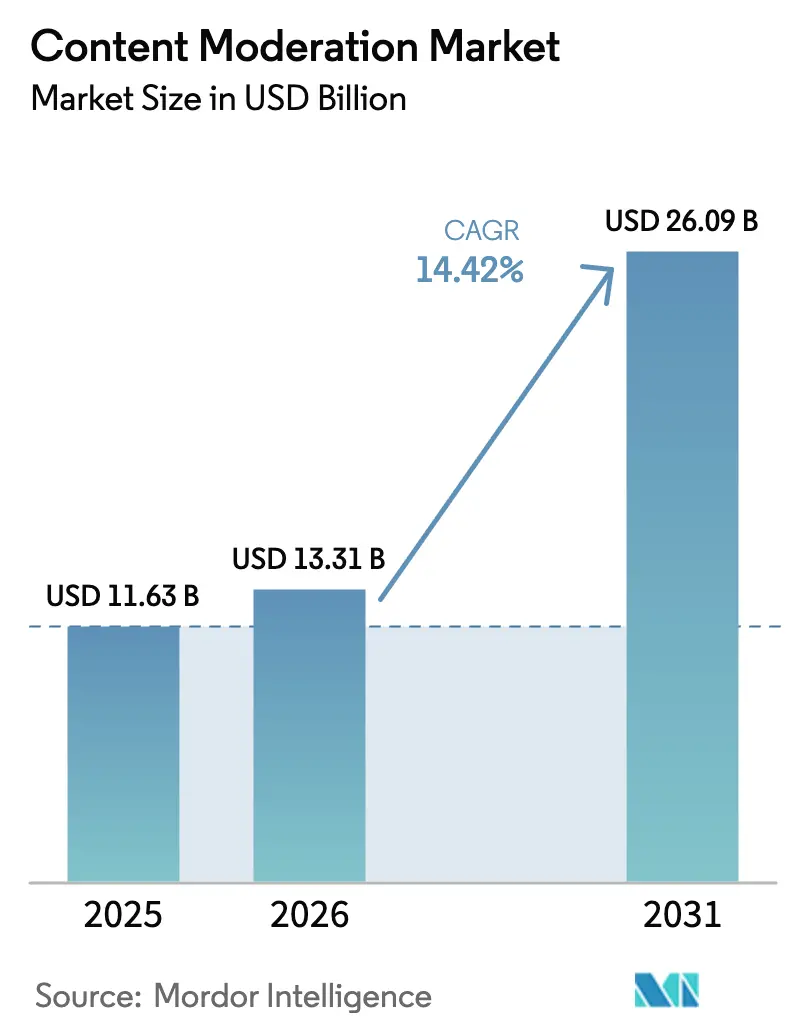

| Market Size (2026) | USD 13.31 Billion |

| Market Size (2031) | USD 26.09 Billion |

| Growth Rate (2026 - 2031) | 14.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Moderation Market Analysis by Mordor Intelligence

The content moderation market size is expected to grow from USD 11.63 billion in 2025 to USD 13.31 billion in 2026 and is forecast to reach USD 26.09 billion by 2031 at 14.42% CAGR over 2026-2031. This expansion reflects the steep rise in user-generated content (UGC), more demanding regulatory frameworks, and advertisers’ insistence on brand-safe environments. Mandates under the EU Digital Services Act (DSA) and the UK Online Safety Act (OSA) are forcing platforms to shift from reactive takedown models to continuous risk-assessment regimes, driving steady budget reallocations toward automated and human-in-the-loop screening systems. Short-form video, live-stream, and voice chat are adding billions of assets per day, intensifying the need for real-time artificial intelligence (AI) that can scale without sacrificing context sensitivity. Consolidation among technology vendors is creating platform-agnostic suites that unify text, image, video, and voice moderation while embedding audit reporting for compliance. Established providers with global footprints and multilingual workforces continue to benefit as brands seek partners that can manage rising costs, regulatory exposure, and psychological risks to human moderators.

Key Report Takeaways

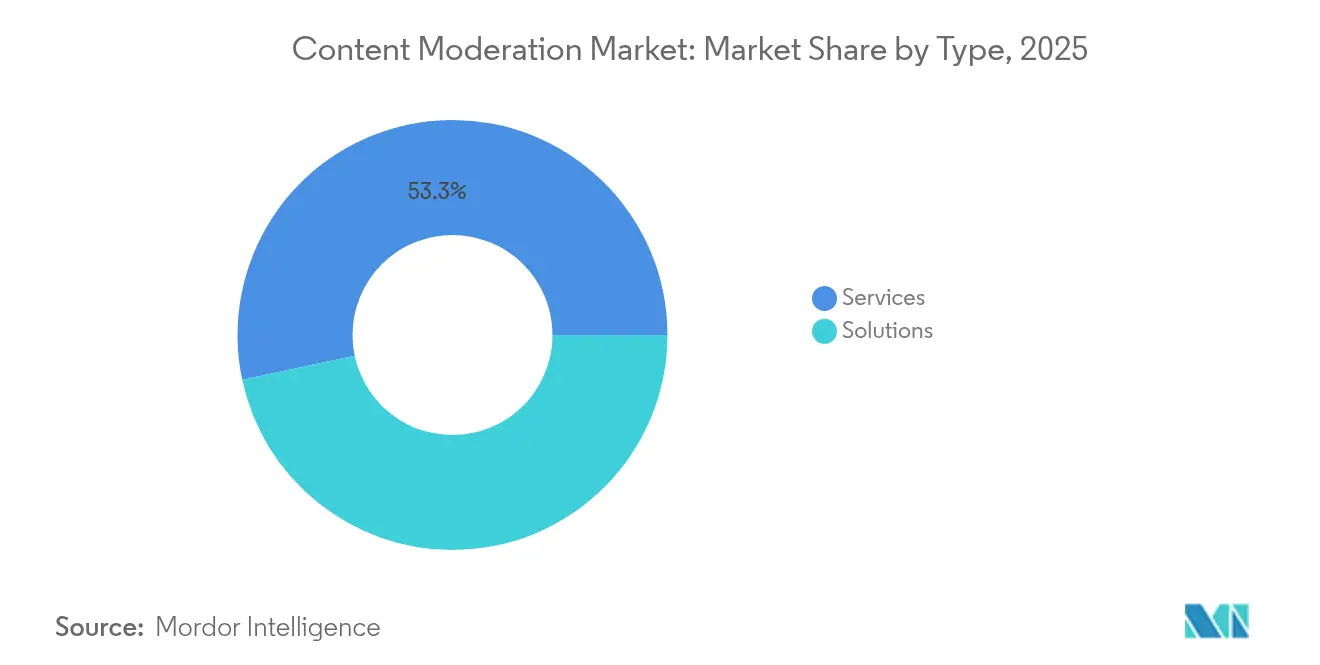

- By type, Services led with 53.34% of content moderation market share in 2025; Solutions are set to expand at a 15.85% CAGR to 2031.

- By deployment, Cloud accounted for 67.88% of the content moderation market size in 2025 and is projected to grow at 16.1% through 2031.

- By content format, Image held 46.12% revenue in 2025, while Live-stream/Voice is advancing at an 18.12% CAGR through 2031.

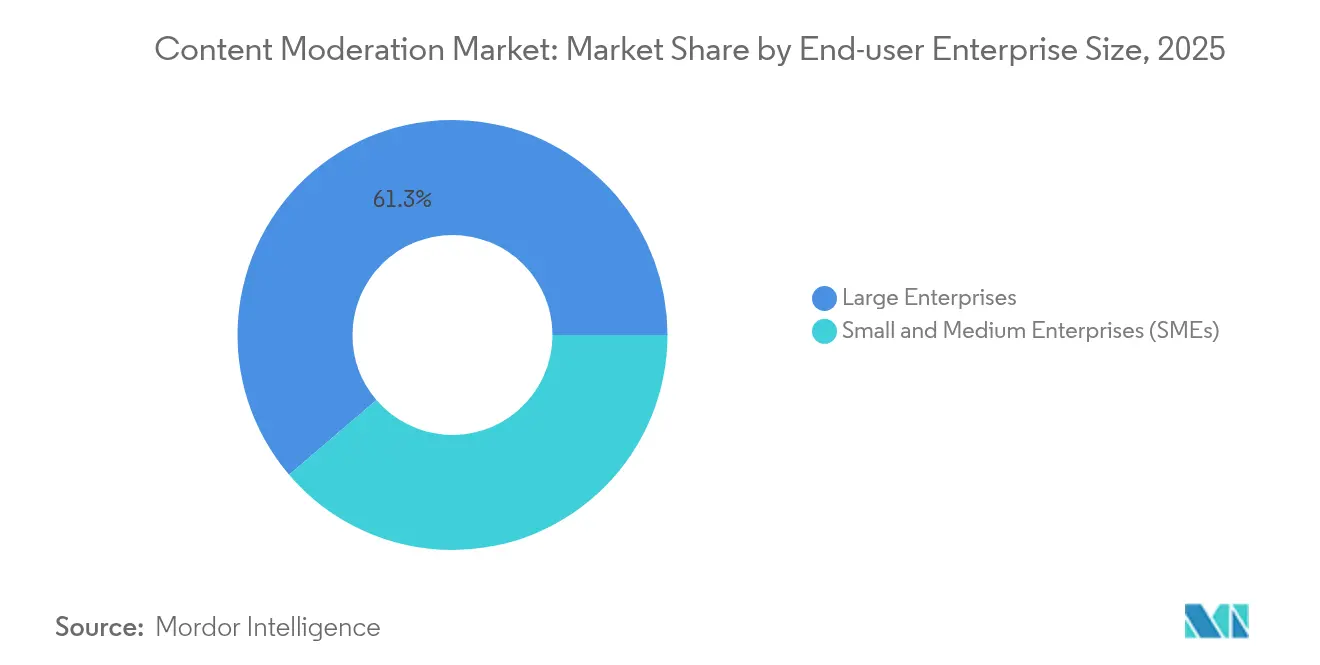

- By enterprise size, Large Enterprises captured 61.25% of the content moderation market size in 2025; Small and Medium Enterprises (SMEs) will post the fastest 14.62% CAGR to 2031.

- By end-user industry, Social Media and Communities commanded 48.93% of the market in 2025, whereas Gaming and Esports Platforms are on track for a 16.95% CAGR to 2031.

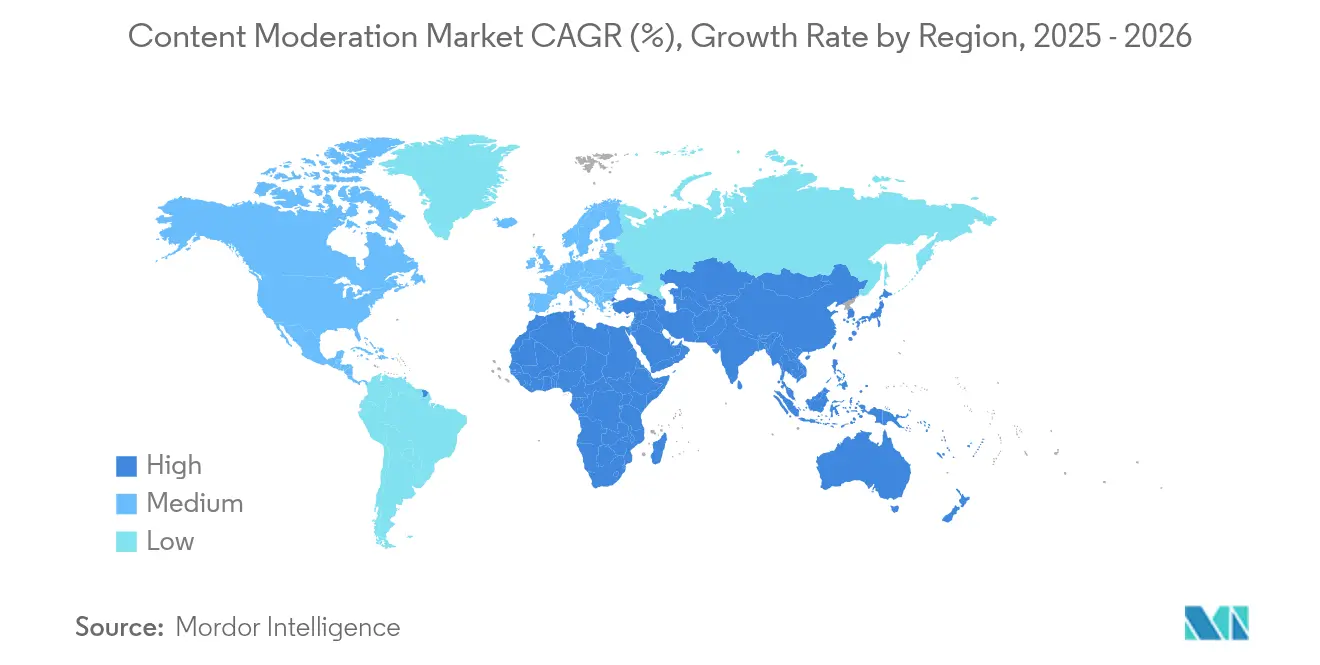

- By geography, North America dominated with 40.75% market share in 2025; Asia-Pacific is poised for an 17.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Moderation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in short-form video UGC | 3.2% | Global, with Asia-Pacific and North America leading | Short term (≤ 2 years) |

| Heightened brand-safety spending by advertisers | 2.8% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Global roll-out of digital-service regulations (EU DSA, UK OSA, etc.) | 4.1% | EU and UK core, spillover to other regions | Medium term (2-4 years) |

| Real-time AI voice-chat moderation demand from online gaming | 2.3% | Global, with North America and Asia-Pacific focus | Short term (≤ 2 years) |

| Transformer-based multimodal models slash per-asset screening cost | 1.8% | Global | Long term (≥ 4 years) |

| Commercialisation of edge-based moderation for AR/VR platforms | 0.5% | North America and EU early adoption | Long term (≥ 4 years) |

| Explosive growth in short-form video UGC | 3.2% | Global, with Asia-Pacific and North America leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive growth in short-form video UGC

Short-form video applications now process millions of uploads per hour, overwhelming traditional review queues. TikTok’s own data show worker headcount in its Pakistan hub rising 315% between 2021 and 2023 as the platform sought to contain a 15% harmful-content exposure rate for teen viewers. Hybrid workflows that pair computer vision with trained reviewers have become standard, yet high creator competition pressures platforms to ease posting friction, sustaining capital flows into real-time detection.

Heightened brand-safety spending by advertisers

After repeated adjacency scandals, 68% of surveyed consumers say they permanently drop trust in brands whose ads appear next to extremist or hateful content.[1]Interactive Advertising Bureau, “2025 Brand Safety and Suitability Survey,” iab.com Brands have responded by directing larger digital budgets toward contextual targeting tools that score page-level risk before bid submission. Even with some marketers challenging the efficacy of stringent blocks, demand for third-party verification remains resilient, fuelling double-digit revenue gains among specialist vendors that can certify low false-positive rates.

Global roll-out of digital-service regulations

The DSA became fully enforceable in February 2024, obliging Very Large Online Platforms to run yearly risk audits and face fines up to 6% of worldwide turnover.[2]European Commission, “The Digital Services Act,” europa.eu The UK followed with OSA enforcement in March 2025, cementing a regulatory template that Australia, Japan, and Brazil are adapting. Large providers have thus prioritised moderation budgets over user-growth incentives, favouring suppliers versed in legal disclosure, incident logging, and transparency report generation.

Real-time AI voice-chat moderation in online gaming

Modulate’s ToxMod has analysed more than 160 million hours of voice traffic, enabling 80 million enforcement actions and cutting toxicity exposure in Call of Duty titles by 25%.[3]Modulate, “ToxMod Processes 160 Million Hours of Voice,” modulate.ai Success metrics tied to player retention are convincing publishers to embed voice filters at the engine level. New entrants such as GGWP are layering semantic context onto speech-to-text pipelines, enabling millisecond-level decisions that satisfy gamers’ low latency expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating moderator mental-health costs | -1.9% | Global, acute in outsourcing hubs | Medium term (2-4 years) |

| Model bias and false-positive brand risk | -1.2% | Global | Short term (≤ 2 years) |

| Data-sovereignty rules limiting cross-border review centres | -0.8% | EU, China, Russia, expanding globally | Long term (≥ 4 years) |

| Adversarial AI attacks that poison classifier accuracy | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating moderator mental-health costs

More than 140 Facebook contractors in Kenya were diagnosed with severe PTSD in late 2024, triggering lawsuits that raised global awareness of psychological harm among review workers. Studies indicate that one in four moderators develops moderate-to-severe distress, driving higher turnover, retraining expense, and reputational risk. Platforms are therefore underwriting expanded counselling programs and accelerating AI substitution for the most graphic categories to reduce human exposure.

Model bias and false-positive brand risk

Audits of large language and vision models show a pattern of over-removal for non-English content and slower remedial action on harmful material in low-resource languages. Such bias distorts public discourse and erodes trust, while false positives can suppress legitimate speech or mis-flag brand messaging. Continual model retraining with region-specific datasets and multilingual reviewers remains essential but resource-intensive, slowing net automation gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Dominate Through Specialized Expertise

Services held 53.34% of content moderation market share in 2025, underscoring enterprises’ reliance on partners that pair multilingual reviewers with proprietary AI. The segment grew at a steady 12–13% annual pace from 2020–2024 and is expected to maintain double-digit momentum because regulatory audits increasingly require documented human oversight. Many buyers select vendors such as TELUS International or Wipro for “follow-the-sun” staffing models that guarantee 24/7 coverage across jurisdictions. Concurrently, Solutions providers expanded at a faster 15.85% CAGR, capturing workloads suited to pure automation. The divergence illustrates an evolutionary shift: as transformer-based image-to-text models mature, solution vendors now offer turnkey APIs capable of flagging hate symbols, extremist insignia, and nuanced context in seconds. Cost differentials narrow when throughput exceeds millions of assets daily, pushing platforms to hybrid contracting that blends subscription software with managed review seats.

The converging model is visible in alliances like Keywords Studios partnering with Spectrum Labs to embed toxicity classifiers in live-ops pipelines, enabling simultaneous scaling of human and machine resources. Compliance questions also favour managed service operators that can issue audit-ready dashboards. Major bid proposals increasingly specify minimum human-review thresholds for under-represented languages, ensuring the services line continues to set volume baselines while solution revenue accelerates. This interplay keeps both streams critical to the broader content moderation market.

By Deployment: Cloud Infrastructure Enables Global Scale

Cloud deployments encompassed 67.88% of content moderation market size in 2025 as hyperscale availability zones offered elastic compute for sudden viral surges. Content platforms can burst from baseline to peak traffic exceeding 3× normal volume when trends explode, and cloud orchestration absorbs this load without procuring on-premise hardware. The shift also simplifies global policy updates: a single model push propagates simultaneously to every region, supporting consistent enforcement. Latency-sensitive formats such as live-stream require sub-300 millisecond round trips, pressuring vendors to distribute inference nodes closer to end users through edge extensions of the major clouds.

On-premise retains niche relevance where data cannot leave sovereign borders—particularly in government portals, digital health, or children’s education apps. Hybrid patterns therefore emerge: sensitive personally identifiable information is redacted locally, while de-identified media flows to cloud for classifier runs. Edge computing is the next frontier, marrying near-device inference with centralised governance. Start-ups that can containerise moderation micro-services for deployment on telco networks, game consoles, or AR headsets stand to unlock new usage tiers, sustaining cloud-adjacent revenue streams across the content moderation market.

By Content Format: Live-Stream Voice Drives Innovation

Image moderation captured the largest 46.12% revenue share in 2025, reflecting the historic dominance of photo-centric social networks and mature convolutional neural network techniques. Nevertheless, live-stream and voice content is the breakout category, forecast at an 18.12% CAGR as social audio rooms, multiplayer games, and metaverse events proliferate. Live formats leave reviewers minimal reaction time; real-time inference must detect hate speech, grooming, or self-harm cues mid-session. Vendors such as Modulate and GGWP deploy low-latency speech-to-intent pipelines that parse acoustic tone, semantics, and speaker metadata in under 150 milliseconds, then pass suspect snippets for human triage.

Video remains technically demanding because violations can occur across audio and visual frames asynchronously. Transformer models pooling temporal and spatial features have reduced frame-by-frame cost, yet heavy compute still encourages a two-pass design in which a coarse scan screens probable violations before a fine-grained review. Text moderation meanwhile faces evasion tactics like “algospeak” and QR-encoded slurs, making multimodal correlation crucial. Together these dynamics reinforce customer preference for suites capable of stitching insights across media channels, supporting sustained growth in every sub-format inside the content moderation market.

By End-user Enterprise Size: SMEs Embrace Automated Solutions

Large enterprises accounted for 61.25% of content moderation market size in 2025 owing to their complex compliance needs, global user bases, and liability exposure. They typically run internal policy teams and contract multiple service partners, with cross-functional dashboards that tally takedowns, appeals, and regulator inquiries. However, SMEs represent the fastest expansion at 14.62% CAGR because API-based services lower adoption barriers. Providers like WebPurify let developers add profanity filters with a few lines of code and pay only per asset processed. Such pricing is vital in emerging economies where platform revenues remain modest yet user numbers soar.

SMEs also tap software marketplaces of major clouds, selecting pre-trained models that update automatically. As a result, small marketplaces, niche forums, and indie game studios introduce content filters earlier in their growth cycle, improving trust well before regulators intervene. Over the forecast horizon, SME demand for bundled analytics—flag aging, reviewer productivity, and policy heat maps—will accelerate subscription tiers, deepening their footprint in the content moderation market.

By End-user Industry: Gaming Platforms Lead Innovation

Social Media and Communities commanded 48.93% of revenue in 2025, a natural outcome of their vast daily post volume. Yet Gaming and Esports platforms will post the highest 16.95% CAGR, converting safety gains directly into player retention and in-game monetisation. Multiplayer titles that deploy proactive voice filters report double-digit drops in churn, translating moderation budgets into tangible financial benefit. Meanwhile, e-commerce operators embed content checks to verify seller listings, detect counterfeit goods, and police user reviews. OTT media services moderate viewer comments to curb toxicity without throttling engagement. Governments are also onboarding moderation for digital hearings and citizen portals, though procurement cycles elongate timelines.

Gaming’s innovation spill-over is evident in the adoption of sentiment analysis models that adjust toxicity thresholds by match tempo or player rank, reducing false positives. In turn, social platforms refine teen-safety settings using insights piloted in games. Cross-industry fertilisation thus reinforces tech development, ensuring every vertical benefits from breakthroughs authenticated within the content moderation market.

Geography Analysis

North America held a 40.75% revenue share in 2025 and is projected to post a 13.85% CAGR to 2031. United States platforms such as Meta, Google, and TikTok channel heavy RandD budgets into generative AI that both creates and polices content, sustaining local demand for advanced trust-and-safety tooling. Canada leverages talent density around Toronto’s AI cluster to host compliance teams serving multilingual markets, while Mexico’s bilingual workforce increasingly anchors Spanish-language review operations for the hemisphere. Federal and state privacy bills continue to shape investment, but harmonisation remains limited, obliging providers to map policies to a patchwork of rules, especially for children’s content and political advertising.

Asia-Pacific is the growth engine, set to expand at 17.62% CAGR through 2031. India combines a vast domestic user base with cost-competitive service centres, enabling global platforms to scale reviewer pools quickly. Pakistan, the Philippines, and Malaysia perform similar roles, each adding linguistic specialities that feed multi-hub delivery models. China’s closed ecosystem nurtures domestic providers aligned with local censorship codes, while Japan and South Korea push technological boundaries in voice and AR/VR moderation tied to advanced gaming markets. Southeast Asian nations such as Indonesia and Vietnam are witnessing an explosion of local social apps, making cultural nuance and dialect coverage critical.

Europe commands middling growth of 13.35% CAGR, yet it shoulders outsized influence through the DSA’s precedent-setting rules. The region fosters providers expert in audit-ready reporting, risk scoring, and third-party oversight. Germany drives robust demand for hate-speech detection keyed to strict domestic laws, whereas France emphasises child-safety guarantees. Post-Brexit, the UK’s OSA layers additional documentary proof obligations, favouring vendors with London-based compliance consultancies. Meanwhile, the Middle East and Africa are early in adoption curves: internet penetration rises rapidly, but political fragmentation and bandwidth limitations constrain immediate scale ups. Local start-ups often partner with global vendors, exchanging cultural knowledge for technology access, gradually integrating these regions into the wider content moderation market.

Competitive Landscape

The market remains moderately concentrated, with the top five providers together estimated below 50% share. ActiveFence exemplifies consolidation, reaching a USD 500 million valuation after acquiring Spectrum Labs and Rewire to build an end-to-end suite that spans threat intelligence, classifier libraries, and regulatory dashboards. Service majors such as TELUS International, Cognizant, and Accenture compete on geographic breadth and vertical expertise, offering thousands of reviewers fluent in 100+ languages and certified across ISO privacy standards. Technology-first players like Modulate specialise in narrow but growing niches—real-time voice—as open-source transformer advances lower barriers in text and image.

Hybrid delivery is the definitive differentiator: vendors bundle model-as-a-service APIs with optional human verification queues, charging premium rates for high-risk categories such as self-harm or extremist propaganda. Edge-deployment roadmaps, vital for AR/VR moderation, are emerging as deal-breakers in next-generation platform RFPs. Compliance automation adds another front: dashboards that auto-populate DSA transparency reports or generate UK OSA risk assessments spare clients from expensive internal builds. Investment continues to flow: Musubi closed a USD 5 million seed round in February 2025, asserting 10× lower error versus human-only review and serving early adopters like Grindr. Overall, the tempo of MandA and venture funding signals sustained belief in high-growth potential across the content moderation market.

Content Moderation Industry Leaders

Genpact, Ltd.

Accenture plc

Wipro Limited

Cognizant

TELUS International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Musubi raised USD 5 million in seed funding led by J2 Ventures to extend its AI platform that claims 10× lower error than human reviewers.

- January 2025: IntouchCX acquired WebPurify, adding automated image and video filters to its customer-experience portfolio.

- December 2024: More than 140 Facebook moderators in Kenya sued Meta and Samasource after diagnoses of severe PTSD linked to graphic content exposure.

- October 2024: Modulate upgraded ToxMod with prosocial detection and text analysis after processing 160 million hours of voice data and enabling 80 million enforcement events.

Global Content Moderation Market Report Scope

Content moderation is the process of reviewing and monitoring user-generated content on online platforms to ensure that it meets certain standards and guidelines. This includes removing inappropriate or offensive content and enforcing community guidelines and terms of service.

The content moderation market is segmented by type (solution, services), by deployment (cloud, on-premises), by content (image, text, video), by enterprises (SMEs, large enterprises), by end-user (IT and telecom, retail, healthcare, government, media and entertainment, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| Cloud |

| On-Premises |

| Image |

| Text |

| Video |

| Live-stream / Voice |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Social Media and Communities |

| Gaming and Esports Platforms |

| E-commerce and Marketplaces |

| Media and Entertainment OTT |

| Telecom and ISPs |

| Government and Public Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Solutions | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| By Content Format | Image | ||

| Text | |||

| Video | |||

| Live-stream / Voice | |||

| By End-user Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-user Industry | Social Media and Communities | ||

| Gaming and Esports Platforms | |||

| E-commerce and Marketplaces | |||

| Media and Entertainment OTT | |||

| Telecom and ISPs | |||

| Government and Public Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the content moderation market by 2031?

The market is forecast to reach USD 26.09 billion by 2031, growing at a 14.42% CAGR.

Which segment is expanding fastest within the content moderation market?

Live-stream and voice moderation is the quickest-growing content format, advancing at an 18.12% CAGR through 2031.

How are new regulations influencing content moderation spending?

The EU DSA and UK OSA mandate annual audits, risk reports, and heavy fines, prompting platforms to raise moderation budgets and adopt hybrid AI-human solutions.

Why is Asia-Pacific considered the growth engine for content moderation?

The region pairs rapid platform adoption with cost-efficient moderation hubs across India, Pakistan, and the Philippines, fuelling an 17.62% CAGR.

What challenges do human moderators face?

High exposure to violent or graphic material results in elevated PTSD rates, leading to legal action, higher turnover, and increased mental-health support costs.

Page last updated on: