Content Recommendation Engine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

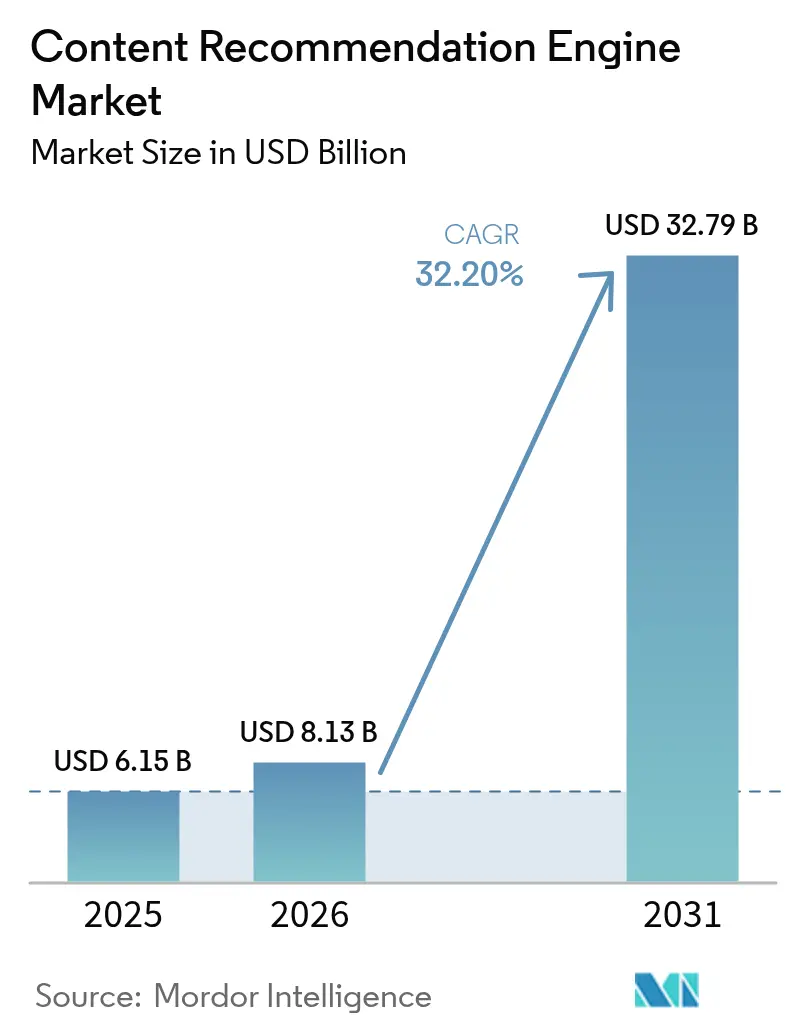

| Market Size (2026) | USD 8.13 Billion |

| Market Size (2031) | USD 32.79 Billion |

| Growth Rate (2026 - 2031) | 32.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Recommendation Engine Market Analysis by Mordor Intelligence

The Content Recommendation Engine Market size is expected to grow from USD 6.15 billion in 2025 to USD 8.13 billion in 2026 and is forecast to reach USD 32.79 billion by 2031 at 32.20% CAGR over 2026-2031. This rapid scale-up reflects the move from passive search toward always-on personalization that shapes what users watch, read, and buy. Surging streaming libraries, wider edge-AI deployment, and stricter privacy rules together create a new baseline for real-time relevance across devices. Major digital platforms now treat recommendation quality as a core revenue lever, and enterprises in retail, media, and finance are racing to match that standard. At the same time, rising compute efficiency, availability of pre-trained models, and lower entry costs allow small businesses to deploy the same caliber of personalization as global leaders.

Key Report Takeaways

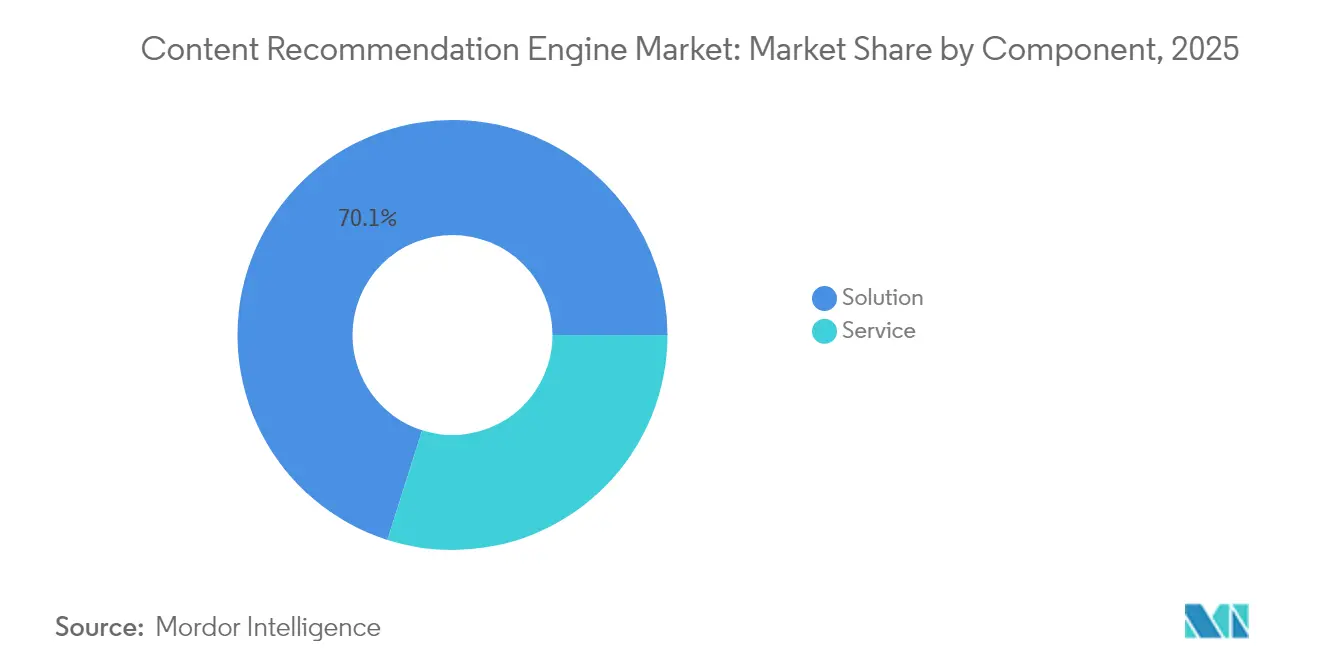

- By component, solutions led with 70.10% of content recommendation engine market share in 2025; services are projected to expand at a 34.39% CAGR through 2031.

- By deployment mode, cloud infrastructure accounted for 80.65 % of the content recommendation engine market size in 2025, while edge-integrated deployments post a 33.98 % CAGR to 2031.

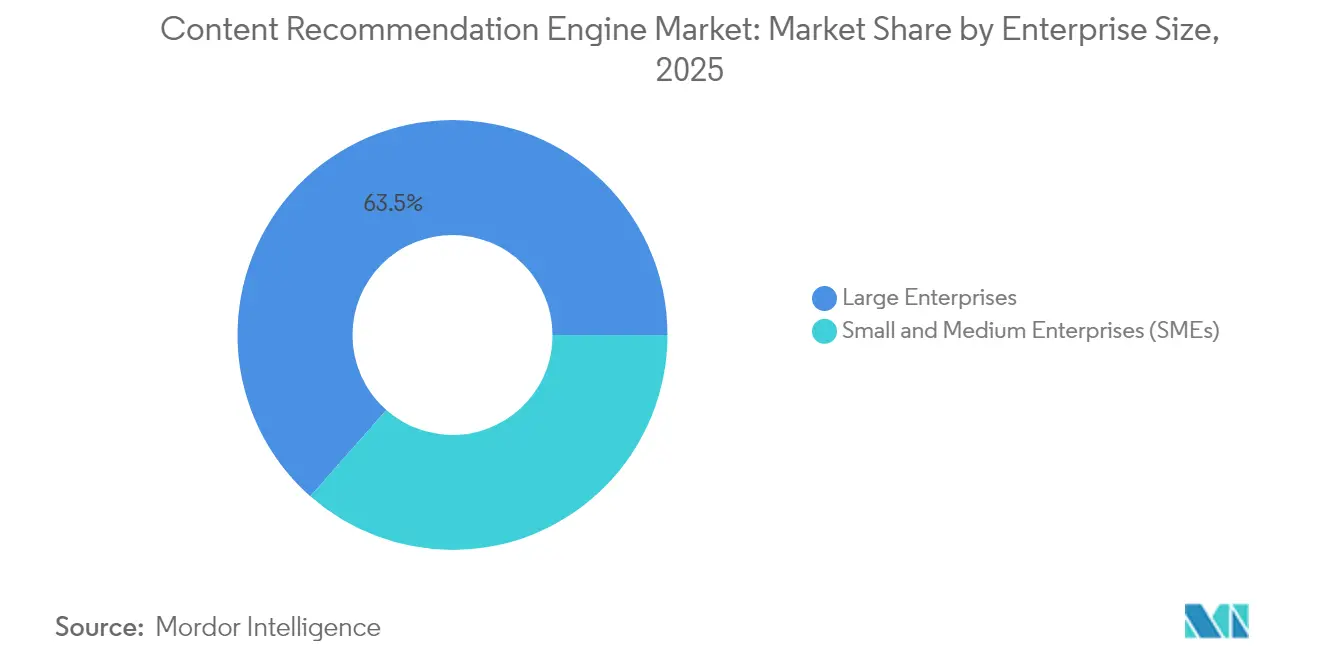

- By enterprise size, large enterprises held 63.50 % share of the content recommendation engine market in 2025; small and medium enterprises recorded the highest 34.59 % CAGR through 2031.

- By personalisation approach, content-based filtering captured 53.90 % of the content recommendation engine market in 2025; hybrid filtering advances at a 34.94 % CAGR through 2031.

- By end-user industry, e-commerce and retail commanded 35.20 % of the content recommendation engine market size in 2025; BFSI is the fastest-growing segment at a 34.01 % CAGR to 2031.

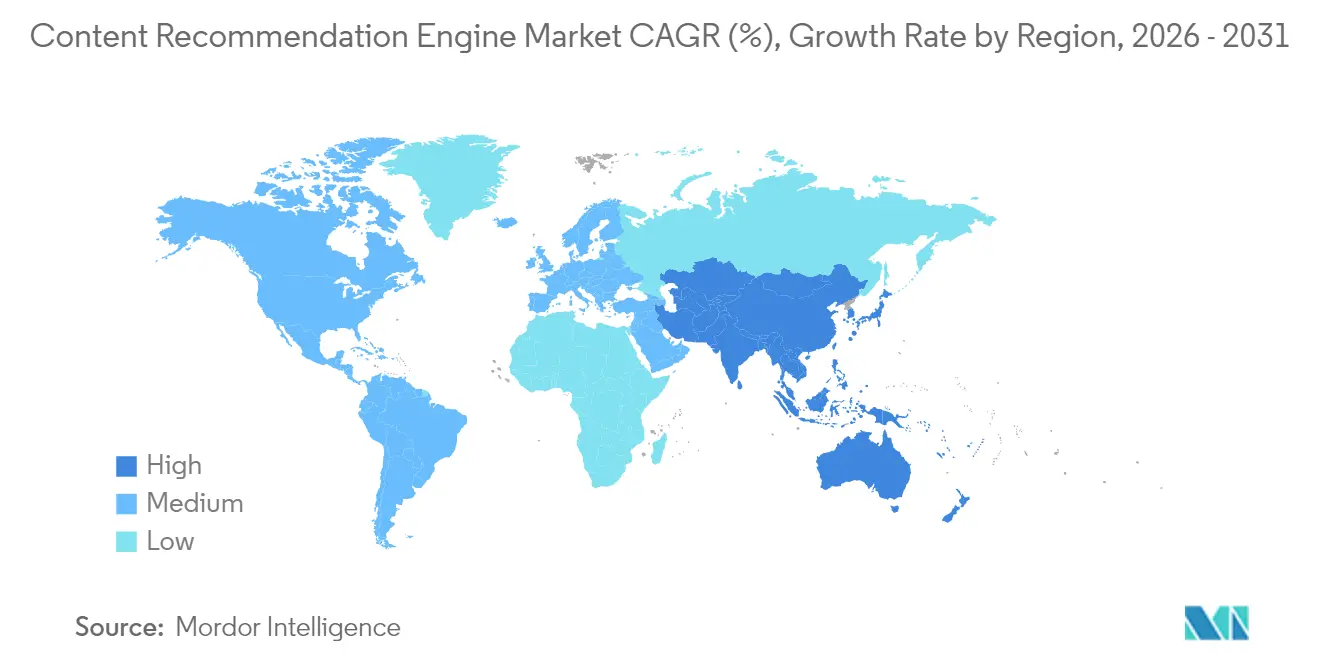

- By geography, North America led with 38.20 % revenue share in 2025, whereas Asia-Pacific delivered the strongest 35.41 % CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Recommendation Engine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising streaming-content volumes | +8.2% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Growing demand for hyper-personalised UX | +7.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Cookieless first-party data strategies | +6.8% | Global, regulatory-driven in EU and California | Short term (≤ 2 years) |

| Edge-AI inference for real-time recommendations | +5.9% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Integration with headless CMS and commerce stacks | +4.1% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Multilingual content expansion in emerging markets | +3.7% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Streaming-Content Volumes Drive Infrastructure Scaling

Record levels of video, audio, and article uploads have created petabyte-scale interaction logs that traditional collaborative filtering alone cannot handle. Netflix’s shift to foundation models illustrates how growing libraries require architectures that fuse multimodal item metadata with real-time engagement signals. [1]Netflix Technology Blog, “Foundation Model for Personalized Recommendation,” netflixtechblog.com Cloud and edge operators are responding with heavy capital spending; Amazon announced more than USD 100 billion in 2025 data-center investments to meet AI workload demand. Vendors able to process thumbnail images, audio waveforms, and transcripts in one model are gaining enterprise interest, particularly from streaming newcomers that cannot afford multi-system complexity.

Growing Demand for Hyper-Personalised UX Transforms User Expectations

Modern consumers expect the next item to feel curated just for them within milliseconds. Hospitality studies show that 61% of hotel guests are willing to pay extra for custom experiences, with AI recommendations delivering nearly USD 40 million in incremental revenue for early adopters. [2]Hospitality Net, “AI in Hospitality: Creating Personalized Customer Experience,” hospitalitynet.org Startups such as Shaped have raised fresh funds to offer self-service recommendation platforms that let smaller firms launch without large engineering teams. Across sectors, real-time micro-segmentation, dynamic pricing, and adaptive interfaces are converging, making hyper-personalisation a board-level priority.

Cookieless First-Party Data Strategies Reshape Tracking Methodologies

The phase-out of third-party cookies and the enforcement of GDPR and CPRA have compelled brands to build first-party data lakes and server-side event pipelines. Companies now deploy consent managers and privacy-enhancing computation while using attribution models that rely on anonymous IDs rather than cross-site tags. Recommendation algorithms that apply federated learning techniques have gained traction because they update models in the browser or on the device, thus avoiding sensitive data transfer. Firms mastering cookieless personalisation report higher opt-in rates and stronger trust scores with regulators.

Edge-AI Inference for Real-Time Recommendations Enables Low-Latency Processing

Delivering suggestions at the network edge cuts round-trip latency and bandwidth. Mobile inference benchmarks show up to 4.3× speed gains versus cloud-only routes. Telecommunications operators have begun collocating recommendation micro-services at 5G base stations so that videos, news cards, or product tiles are ranked locally. The same approach improves battery life on wearables and connected cars, where bandwidth is limited and privacy concerns are high. Vendors integrating on-device vector databases with central model training report higher click-through rates in pilot programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulations (GDPR, CPRA etc.) | -4.8% | Global, strictest in EU and California | Short term (≤ 2 years) |

| Cold-start and sparse-data limitations | -3.2% | Global, acute in emerging markets | Medium term (2-4 years) |

| Algorithmic bias and echo-chamber concerns | -2.7% | Global, regulatory focus in EU and US | Long term (≥ 4 years) |

| Escalating compute-energy costs for deep models | -2.1% | Global, critical in energy-constrained regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations Create Compliance Complexity

GDPR and CPRA require explicit consent, transparent logic, and deletion rights, exposing firms to multimillion-euro fines for failures. [3]Legal Nodes, “ChatGPT Privacy Risks for Business,” legalnodes.com Eight additional U.S. state laws take effect in 2025, each with separate notice and opt-out clauses. Providers must now bake privacy into model design, employ differential privacy, and retain audit records. Compliance tools add cost, and stricter permissions can limit data variety, reducing algorithm accuracy when poorly managed.

Cold-Start and Sparse-Data Limitations Constrain Personalisation Effectiveness

When a new user, region, or product launches, interaction history is minimal, making predictions harder. Hybrid methods that blend content features with collaborative indicators help, but require steady feature engineering and hardware overhead. Research into large language models for recommendation hints at solving part of the cold-start by tapping pretrained knowledge. Yet smaller enterprises may lack the resources to fine-tune such models, slowing time-to-value in new markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expansion Outpaces Solution Dominance

Solutions retained 70.10 % of revenue in 2025 as firms purchased turnkey engines to power search, video rows, and product carousels. The content recommendation engine market size attached to services, however, is projected to multiply at a 34.39 % CAGR to 2031 as organizations seek data-engineering help, model tuning, and integration safeguards. Vendors now bundle advisory, A/B testing, and ongoing performance reviews, converting one-time software deals into recurring engagements.

Service demand also stems from architectural shifts toward headless commerce and composable tech stacks that require custom connectors. Implementation partners connect recommendation APIs to CMS, inventory systems, and analytics tools, ensuring unified profiles and real-time feedback loops. A rise in self-serve platforms has not replaced professional services; instead, it expands the pie by reducing entry barriers and then upselling optimization packages once volume scales.

By Deployment Mode: Cloud Dominance and Edge Convergence

Cloud-hosted engines delivered 80.65 % of the content recommendation engine market share in 2025, benefiting from elastic scaling and access to specialized GPUs. The content recommendation engine market size connected to edge-assisted architectures is now growing 33.98 % annually, signalling convergence rather than replacement. Enterprises train large models centrally but push compressed inference graphs to mobile apps, set-top boxes, and in-store kiosks for instantaneous advice.

Public-cloud providers embed recommendation APIs alongside storage, streaming, and security services to lock in customers. At the same time, hybrid deployments meeting data-sovereignty rules keep sensitive behavior logs within national borders while still syncing anonymous embeddings to the cloud for periodic retraining. The twin-track model is becoming standard in sectors such as media and automotive, where latency and privacy both carry revenue impact.

By Enterprise Size: SME Adoption Accelerates

Large enterprises held 63.50 % of revenue in 2025, yet the small-and-medium segment is expanding at a brisk 34.59 % CAGR. Lower total cost of ownership, pay-as-you-go licensing, and ready-made connectors for commerce platforms let SMEs replicate advanced personalisation once exclusive to global brands. Template workflows for product grids, news feeds, and in-app banners reduce data-science overhead.

Cloud marketplaces further ease access, allowing SMEs to procure a recommendation module alongside hosting and security in one subscription. Many smaller firms now run A/B tests with automated significance testing that surfaces winning models without manual SQL queries. As data maturity improves, SMEs upgrade to multi-model routing and experiment orchestration, reinforcing vendor stickiness and expanding lifetime value for providers.

By Personalisation Approach: Hybrid Filtering Gains Momentum

Content-based techniques, which rely on product attributes and metadata, generated 53.90 % of segment revenue in 2025. Hybrid filtering—combining collaborative behavior with rich content vectors—now records a 34.94 % CAGR, eroding single-method dominance. Hybrid setups mitigate cold-start risk while preserving discovery serendipity, and they align well with privacy demands because initial predictions can be made on client-side content data alone.

Advances in multimodal embeddings allow text, image, and audio cues to sit within shared latent spaces, improving cross-domain suggestions such as recommending a podcast based on a film taste. Large-language-model encoders add semantic nuance beyond keyword overlap, pushing click-through gains even with smaller interaction logs. Vendors are shipping configuration wizards that let non-technical users define the blend ratio among algorithms, reducing reliance on hard-coded rules.

By End-User Industry: BFSI Growth Challenges E-Commerce Leadership

E-commerce and retail continued to lead with 35.20 % revenue share in 2025, underlining the direct link between personalised merchandising and basket size. Banking, financial services, and insurance are projected to rise at a 34.01 % CAGR to 2031, as lenders and insurers deploy next-best-product engines for cards, loans, and policies. Recommendation modules now power robo-advisors, helping investors choose funds based on risk appetite and saving goals.

Media, entertainment, and gaming remain strong adopters, enriching watch lists and in-game item stores. Hospitality, propelled by success stories such as personalised room upgrades and activity suggestions, is scaling deployment across global hotel chains. Cross-industry knowledge transfer is accelerating: Retail media networks borrow financial services risk-scoring techniques to improve relevance, while BFSI firms adopt e-commerce A/B frameworks to shorten iteration cycles.

Geography Analysis

North America held 38.20 % revenue share in 2025, anchored by mature streaming platforms, high-speed broadband, and robust venture funding. Cloud hyperscalers headquartered in the region bundle recommendation APIs into larger software suites, reinforcing stickiness across industries. Regulatory clarity and strong developer ecosystems accelerate experimentation, but growth is tapering as saturation rises and competitive pricing pressures margins.

Asia-Pacific delivers the fastest 35.41 % CAGR to 2031, supported by mobile-first consumption, expanding 5G coverage, and demand for multilingual recommendations across vast cultural landscapes. Regional governments invest heavily in AI infrastructure and data-center capacity, catalyzing local startups that tailor algorithms to language nuances and urban-rural content gaps. Companies such as DeepSeek reached nine-digit user bases within days of launch, underscoring the appetite for personalised discovery tools. Edge computing investments by telecom carriers help overcome cross-border data-transfer rules, keeping inference near users while updating models centrally.

Europe exhibits steady adoption, tempered by strict privacy oversight that slows rollout but spurs innovation in privacy-preserving computation. Vendors test federated learning pilots to satisfy GDPR yet deliver accuracy on par with global peers. South America and the Middle East and Africa remain emerging opportunity zones. Cloud data-center openings, combined with lightweight SDKs optimised for lower bandwidth, are narrowing the gap, positioning these regions as the next wave of accelerators for the content recommendation engine market.

Competitive Landscape

The content recommendation engine market features a blend of hyperscale cloud providers, independent software vendors, and niche AI specialists. Market leaders leverage integrated stacks that cover data ingestion, model training, A/B testing, and delivery. Amazon Web Services, for instance, reported USD 29.3 billion in Q1 2025 cloud revenue, with recommendation APIs cited among high-growth workloads. Google and Microsoft offer similar toolchains that shorten deployment cycles and lock clients into proprietary ecosystems.

Specialised vendors differentiate through domain focus, lighter footprint, or privacy-centric architectures. Dynamic Yield tailors algorithms to retail merchandising, while Taboola and Outbrain focus on publisher monetisation. Startups such as Argoid AI, now acquired by Amagi, integrate recommendation engines with broadcast workflows to support FAST channel curation. The result is growing consolidation as large players buy niche innovators to expand vertical reach.

Competitive advantage increasingly hinges on three capabilities: real-time inference under 50 milliseconds, multimodal embedding fusion, and regulatory compliance that provides audit trail transparency. Companies that master energy-efficient model deployment also gain cost leverage as AI data-center electricity demand is projected to hit 9 % of the U.S. grid by 2030. [4]American Council for an Energy-Efficient Economy, “Future-Proof AI Data Centers,” aceee.org White-space remains in healthcare and education, where specialised vocabularies and ethical constraints require tailored solutions.

Content Recommendation Engine Industry Leaders

Amazon Web Services (Amazon.com Inc.)

Google LLC (Recommendations AI)

Adobe Inc. (Adobe Target)

Dynamic Yield Ltd.

Taboola Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amagi acquired Argoid AI to enhance AI-driven content planning for OTT platforms.

- June 2025: JINS expanded its multilingual interactive retail assistant, JINS AI, after positive pilot feedback.

- May 2025: Amazon estimated a USD 700 million profit contribution from AI assistant Rufus in 2025, tied to richer product recommendations.

- May 2025: Kikusui Sake Brewery rolled out ‘Nihonshu AI Navigation’ for personalised sake selection.

- April 2025: Adobe rolled out Experience Platform Agent Orchestrator, citing a 50 % revenue uplift from AI agent integration.

- April 2025: ELEMENTS introduced ‘Coordware’, enabling AI-generated content and recommendations for fashion e-commerce.

- March 2025: Kaizen Platform launched ‘Kaizen Personalize Agent’ to unify search, notification, and recommendation flows across web and LINE apps.

- March 2025: Dai Nippon Printing launched ‘Persona Insight’ to create virtual consumer personas powered by generative AI.

- February 2025: Qloo raised USD 25 million to advance cultural-taste-driven entertainment recommendations.

- December 2024: Mediagenix acquired Spideo to deepen AI-driven discovery in media workflows.

Global Content Recommendation Engine Market Report Scope

The content recommendation engine collects and analyzes data that is based on users' behavior, and it assists in offering personalized and relevant content or product recommendations. The end-user for the market is Media, Entertainment & Gaming, E-Commerce and Retail, and others.

| Solution |

| Service |

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Content-based Filtering |

| Collaborative Filtering |

| Hybrid Filtering |

| Media, Entertainment, and Gaming |

| E-commerce and Retail |

| BFSI |

| Hospitality |

| IT and Telecommunication |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solution | ||

| Service | |||

| By Deployment Mode | Cloud | ||

| On-premises | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Personalisation Approach | Content-based Filtering | ||

| Collaborative Filtering | |||

| Hybrid Filtering | |||

| By End-user Industry | Media, Entertainment, and Gaming | ||

| E-commerce and Retail | |||

| BFSI | |||

| Hospitality | |||

| IT and Telecommunication | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the content recommendation engine market?

The content recommendation engine market is worth USD 8.13 billion in 2026 and is set to reach USD 32.79 billion by 2031.

Which region grows fastest over the next five years?

Asia-Pacific records the highest growth, with a 35.41 % CAGR expected through 2031, driven by mobile-first users and rising AI investments.

Which segment expands the quickest within deployment modes?

Edge-integrated architectures, while still a minority, are growing at 33.98 % annually as enterprises push inference closer to users for latency gains.

Why are services gaining share against standalone solutions?

Enterprises need integration, data engineering, and ongoing optimisation, causing services to expand at a 34.39 % CAGR even though solutions still hold the largest revenue base.

How do privacy regulations affect recommendation deployment?

Rules like GDPR and CPRA mandate explicit consent and transparency, pushing firms toward federated learning and on-device processing to maintain personalisation without breaching compliance.

Which end-user industry shows the highest growth rate?

Banking, financial services, and insurance is the fastest-growing vertical, expected to rise at a 34.01 % CAGR as firms deploy next-best-product engines and personalised offers.

Page last updated on: