Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

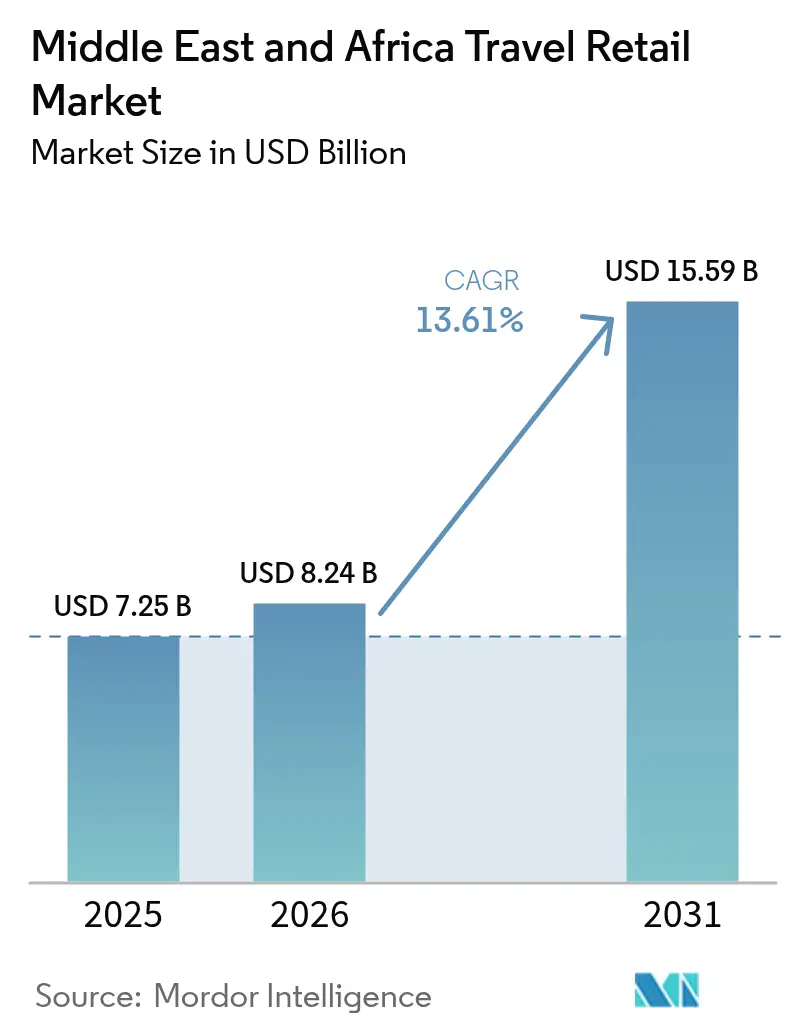

| Base Year Market Size (2025) | USD 7.25 Billion |

| Market Size (2026) | USD 8.24 Billion |

| Market Size (2031) | USD 15.59 Billion |

| Growth Rate (2026 - 2031) | 13.61% CAGR |

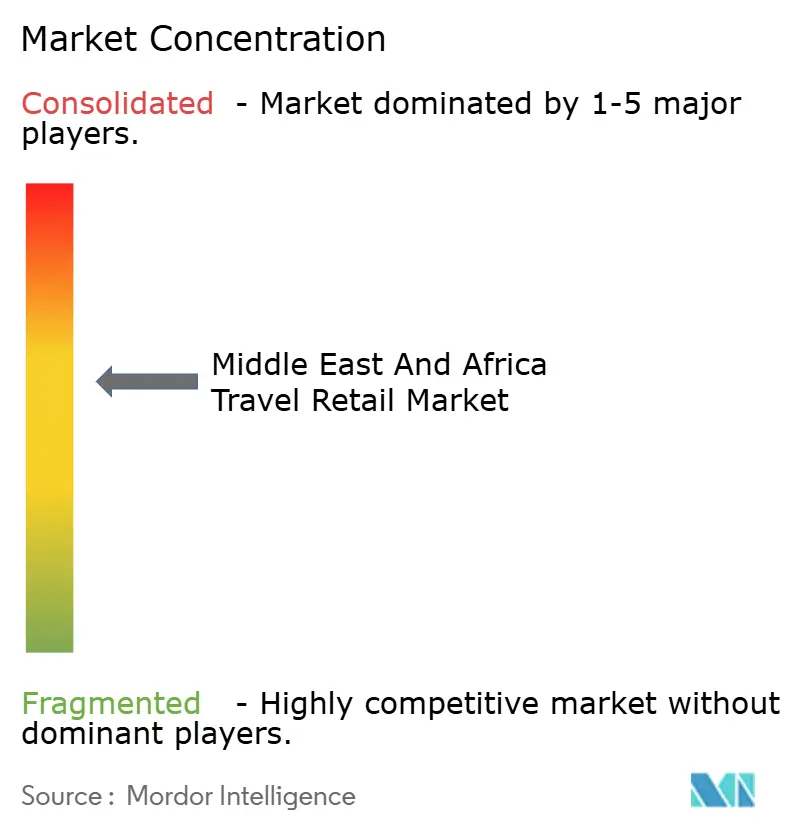

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Travel Retail Market Analysis by Mordor Intelligence

The Middle East and Africa travel retail market size was valued at USD 7.25 billion in 2025 and estimated to grow from USD 8.24 billion in 2026 to reach USD 15.59 billion by 2031, at a CAGR of 13.61% during the forecast period (2026-2031). Investment in airport capacity across the Gulf is widening retail footprints and improving dwell-time economics, which supports higher conversion and average transaction value in the Middle East and Africa travel retail market. New concourses and gates at major hubs like Hamad International Airport add premium storefronts, curated concepts, and more square meters per passenger, which improves category visibility and exclusivity. Policy support is also strong, as Saudi Arabia’s 2025 arrivals reached 122 million under Vision 2030, which reinforces demand for retail at both primary and secondary airports [1]Saudi Press Agency, “Saudi Arabia Welcomes 122 Million Visitors in 2025,” Saudi Press Agency, spa.gov.sa. Trade integration is rising, with intra-African trade growing in 2024, which increases cross-border corporate travel and supports a deeper duty-free assortment at African gateways. Digital payment rails and mobile pre-order partnerships are streamlining checkout across the Middle East and Africa travel retail market, reducing friction for travelers who prefer wallet-based or alternative payment options.

Key Report Takeaways

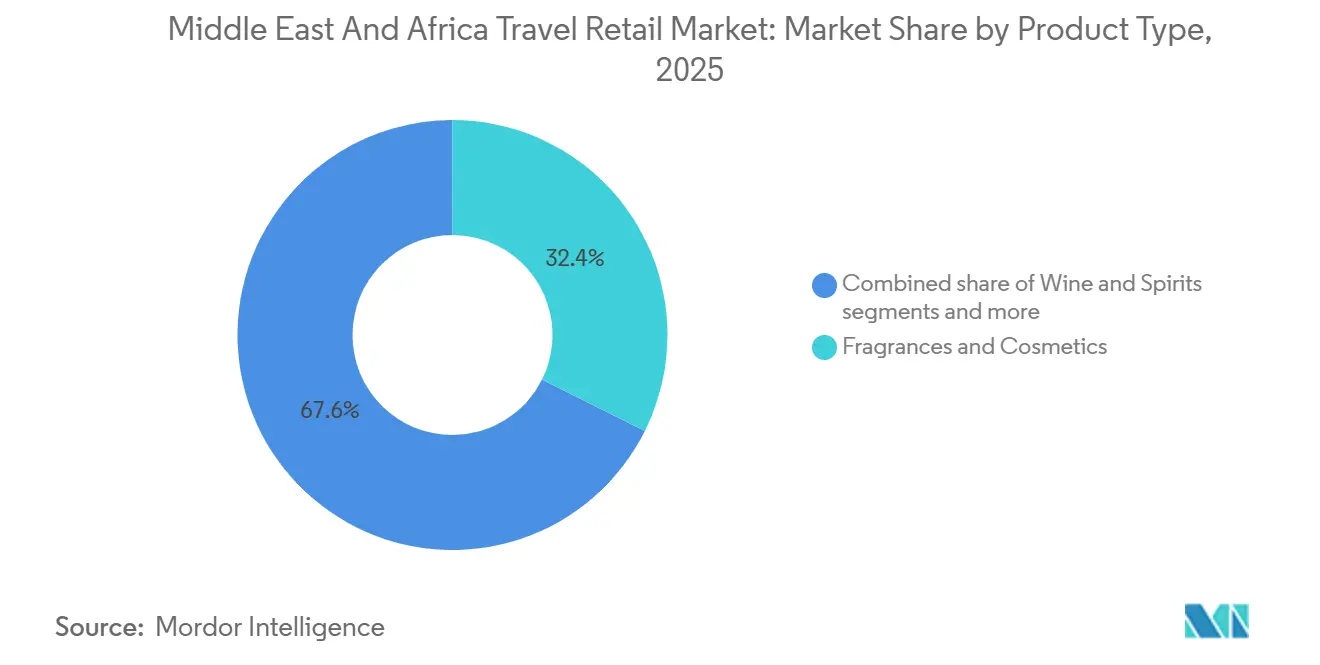

- By product type, Fragrances and Cosmetics led the Middle East and Africa travel retail market with 32.36% of the market share in 2025, while Food and Confectionery is projected to expand at a 13.36% CAGR to 2031.

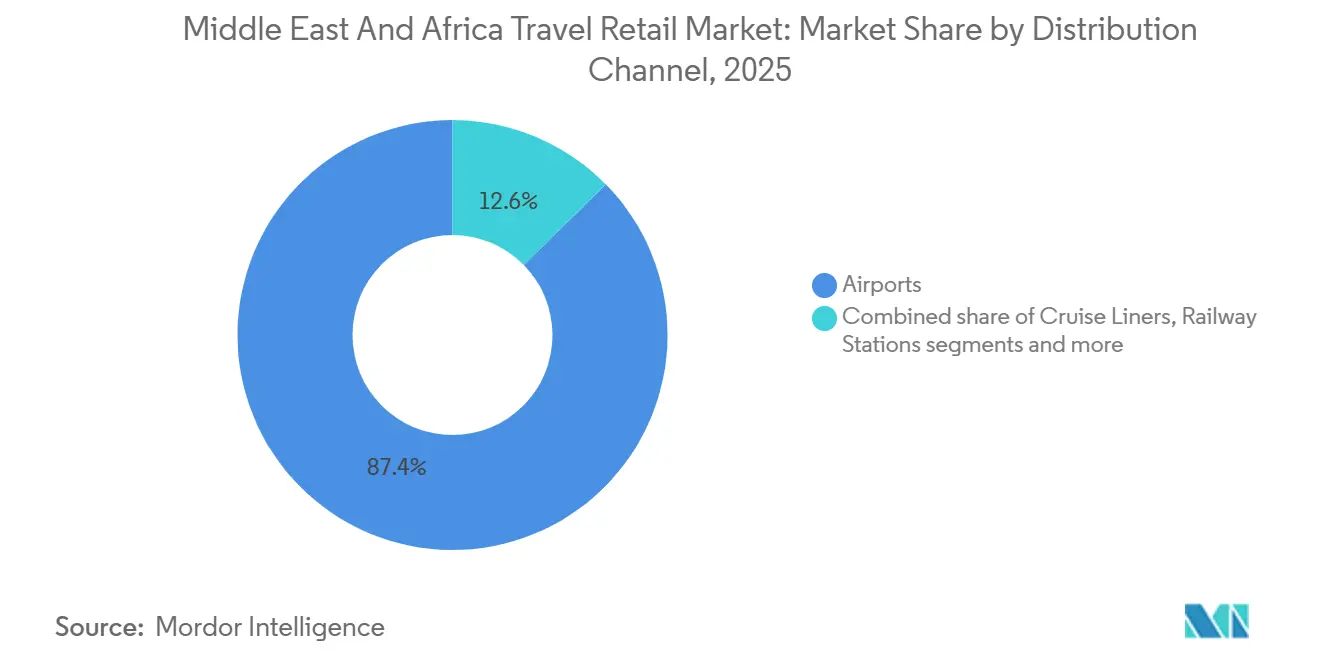

- By distribution channel, Airports held 87.36% of the Middle East and Africa travel retail market share in 2025, while Cruise Liners recorded the highest projected CAGR at 17.76% through 2031.

- By traveler demographics, Leisure Travelers accounted for 47.38% of the Middle East and Africa travel retail market share in 2025, while Medical and Wellness Tourists are advancing at a 15.25% CAGR through 2031.

- By geography, GCC countries represented 42.76% of the Middle East and Africa travel retail market share in 2025, while Sub-Saharan Africa is projected to grow at a 14.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of airport capacities across GCC hubs | +3.2% | GCC core (Saudi Arabia, UAE, Qatar), spill-over to secondary hubs (Oman, Bahrain) | Medium term (2-4 years) |

| Increasing outbound leisure spending by MEA residents | +2.1% | GCC countries, South Africa, Nigeria | Short term (≤ 2 years) |

| Tourism diversification policies like Saudi Vision 2030 | +2.8% | Saudi Arabia, UAE, Qatar, Egypt | Medium term (2-4 years) |

| Pilgrimage traffic boosts Saudi Arabia's secondary airports | +1.5% | Saudi Arabia (Madinah, Tabuk, Jeddah) | Short term (≤ 2 years) |

| AFCFTA driving growth in intra-African business travel | +1.9% | Sub-Saharan Africa (ECOWAS, SADC, EAC regions) | Long term (≥ 4 years) |

| Mobile pre-orders and e-wallets transform duty-free ecosystems | +1.7% | GCC countries, South Africa, Nigeria, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Airport Capacities Across GCC Hubs

Saudi Arabia is executing multi-airport capacity upgrades, and regulators are outlining new infrastructure programs that increase airside throughput while aligning with ICAO compliance standards, thereby expanding leasable commercial space for duty-free use at terminal and concourse levels. In the UAE, Zayed International Airport completed major capacity works in 2024, and the terminal transformation increased potential footfall for high-margin categories, which supports stronger flows in the Middle East and Africa travel retail market. Hamad International Airport opened Concourses D and E in March 2025, raising annual capacity beyond 65 million and adding 2,700 square meters of retail space operated by the airport’s commercial arm, thereby improving category breadth and visibility [2]Qatar Airways Group, “Hamad International Airport Unveils State-of-the-Art Concourses D and E,” Qatar Airways, qatarairways.com. These additions help hubs manage peak flows from transfer waves and pilgrimage seasons, reducing crowding in legacy floor plans and supporting longer dwell times per passenger, which encourages browsing and impulse purchases. As regional networks scale, spillover benefits reach secondary airports in Oman and Bahrain, which attract new routes and incremental gates that can support smaller but growing retail formats in the Middle East and Africa travel retail market. Greater terminal capacity also creates space for experiential concepts and value-tier corners, enabling operators to balance premiumization with accessible price points as volumes grow.

Increasing Outbound Leisure Spending by MEA Residents

Saudi Arabia recorded USD 79.94 billion (SAR 300 billion) in resident travel-related spending in 2025, and the broader lift in trip frequency and international itineraries raises the conversion potential for giftable categories and exclusive launches across the Middle East and Africa travel retail market. South Africa’s Tourism Satellite Account reported higher outbound expenditures in 2024, underscoring pent-up demand and a growing willingness to spend on travel-linked consumption baskets. Nigerian remittances exceeded USD 20 billion in 2024, and this income effect supports Gulf-bound shopping stopovers, which raise duty-free footfall on long-haul departures and returns. Major Gulf hubs reported strong passenger throughput in 2025, and transfer-heavy flight banks align with higher browsing propensity, which benefits beauty and confectionery. Loyalty ecosystems are growing as global operators scale membership programs that add targeted promotions and price transparency, boosting basket size among frequent travelers. Aviation and customs regulators in South Africa and Nigeria set duty-free operating policies and compliance rules that sustain orderly concession growth as passenger volumes expand.

Tourism Diversification Policies Like Saudi Vision 2030

Saudi Arabia targets 150 million visitors by 2030, and the current trajectory includes rapid hotel pipeline growth, improved visa processing efficiency, and support for pilgrimage and leisure flows that increase retail potential across multiple airport tiers. The Nusuk platform streamlined the Umrah booking process and scaled digital adoption, improving travel readiness and visit frequency, in turn raising airside retail traffic. Hajj and Umrah targets are elevating predictable seasonal peaks, and those windows allow duty-free operators to plan inventory and staffing more effectively at Jeddah and Madinah, thereby enhancing service levels and conversion. Egypt’s 2024 tourism receipts improved, and the UAE maintained high hotel occupancy in 2025, both of which sustained passenger uplift and helped stabilize retail replenishment cycles in the Middle East and the Africa travel retail market. Qatar’s cultural tourism assets added steady museum traffic in 2024, and the airport’s commercial strategy continues to introduce unique retail concepts that complement core categories. Cruise is also included in diversification programs, with new Red Sea port developments and the launch of Saudi Arabia’s first cruise ship retail footprint, which opens a new channel for growth.

Pilgrimage Traffic Boosting Saudi Arabia's Secondary Airports

Madinah’s and Tabuk’s airports are scaling capacity and commercial planning in line with rising pilgrimage and NEOM-linked traffic, which raises the relevance of localized assortments and culturally resonant brands at those gateways. Jeddah’s commercial footprint expanded in late 2024 under a major retail build-out, and the presence of a large-format duty-free operation is now anchoring the airport’s sales ramp, which tightens the link between predictable pilgrimage flows and retail throughput. National regulators continue to align infrastructure and safety standards with ICAO requirements, and these frameworks underpin terminal upgrades that include more retail and food-and-beverage units. Predictable calendar spikes from Hajj and Umrah allow operators to pre-position inventory for value and premium segments, reducing out-of-stock risk and improving conversion during peak days in the Middle East and Africa travel retail market. VAT refund protocols for eligible foreign tourists and clear customs rules improve purchase confidence and perceived value, thereby strengthening category resilience during peak travel periods. The expansion of retail at secondary gateways broadens access to international assortments for regional travelers, reducing channel leakage to city-side stores and supporting growth in the Middle East and Africa travel retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political instability continues to impact parts of Africa | -1.4% | Sudan, Sahel (Mali, Burkina Faso, Niger), East Africa fragility zones | Medium term (2-4 years) |

| Oil-price volatility reduces spending across GCC countries | -1.1% | GCC countries (Bahrain, Oman, Saudi Arabia) | Short term (≤ 2 years) |

| Stricter duty-free allowances and tobacco rules implemented | -0.8% | Global, with stricter enforcement in North America, Europe, affecting MEA transit passengers. | Long term (≥ 4 years) |

| Underdeveloped infrastructure limits cruise terminal growth | -0.6% | East Africa (Kenya, Tanzania), West Africa (Ghana, Senegal) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Political Instability Continues to Impact Parts of Africa

Conflict in Sudan displaced millions of people, and the situation continues to disrupt air connectivity by limiting commercial operations at key gateways, which constrains duty-free revenue opportunities linked to those passenger flows. The International Monetary Fund reported a sharp GDP contraction in Sudan in 2024, underscoring the macroeconomic shock that has reduced discretionary spending and complicated retail operations in the region. Security incidents in parts of the Sahel remain a headwind, and elevated travel advisories limit visitor numbers and airline capacity allocations that would otherwise support store traffic. Regional air traffic in East Africa is recovering at varying rates, and Addis Ababa’s gateway is still below 2019 levels, which is slowing retail normalization at connected hubs. International operators active in Southern Africa emphasize local partnerships and agile formats to hedge risk while maintaining service levels in variable conditions. Mediation frameworks led by the African Union and regional economic communities continue to work toward conflict de-escalation, which would create a more supportive backdrop for air travel and retail in the long term.

Stricter Duty-Free Allowances and Tobacco Rules Implemented

The United States FDA is advancing a rulemaking process to reduce nicotine in combusted cigarettes, and eventual implementation would influence demand patterns among transiting passengers who shop for tobacco during United States-linked itineraries. Canada continues to enforce detailed allowances with specific stamp requirements on tobacco, which adds operational complexity for retailers who manage inventory separation by destination [3]Canada Border Services Agency, Duty & Taxes: Traveler Information,” CBSA, cbsa-asfc.gc.ca. United Kingdom rules require robust age verification for tobacco purchases, and the process steps can add time at checkout, a balance operators must balance with staffing and automation. European tax harmonization discussions remain active, and changes to ceilings or minimums would cascade into assortment and pricing strategies for the Middle East and Africa travel retail market. Public health frameworks under the WHO FCTC encourage stronger controls across member states, and national laws in the UAE and South Africa have tightened regulations on vaping and tobacco, reducing impulse purchases in certain travel zones. Operators are responding by elevating beauty, confectionery, and hybrid retail-dining offerings to diversify revenue away from categories facing tighter rules, aligning with portfolio shifts reported by major global concessionaires.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premiumization Meets Affordable Indulgence

Fragrances and Cosmetics captured 32.36% in 2025, and Food and Confectionery is projected to be the fastest-growing line at a 13.36% CAGR through 2031, positioning beauty as the core anchor while affordable indulgence scales breadth across the Middle East and Africa travel retail market. The depth of beauty assortments and frequent exclusive sets support higher conversion among transfer passengers who are sensitive to availability and price advantage at hub airports in the Middle East and Africa travel retail market. Food and confectionery’s growth outlook ties to an expanding mix of localized SKUs and curated gifts, which appeal to both the leisure and visiting-friends-and-relatives segment profiles that value compact formats. Operator strategy is shifting toward hybrid experiences, such as beauty lounges and curated pop-ups, which boost trial and repeat purchases in premium beauty. Category resilience is buttressed by retail expansions at large hubs where new square meters improve sightlines for core brands and provide room for localized novelties.

The Middle East and Africa travel retail industry is also diversifying into cruise-led formats that carry premium beauty and confectionery assortments in compact footprints, which improve category reach beyond airports. Large-format openings at Saudi gateways add anchoring space for fashion, jewelry, and watches that complement beauty-led traffic, and these adjacencies sustain higher overall basket sizes as passengers browse across categories. Product safety and quality frameworks in cosmetics and food remain a backbone, and compliance with Gulf and African standards keeps supply chains aligned with cross-border rules for cosmetics and food handling. Operators continue to calibrate the mix between hero SKUs and seasonal assortments, which helps manage inventory risk during oil-price swings and macroeconomic variability. This balance supports sustained category momentum within the Middle East and Africa travel retail market as network growth introduces new passenger cohorts across hub and secondary airports.

By Distribution Channel: Airport Dominance with Cruise Upside

Airports commanded 87.36% of revenue in 2025, supported by consistent passenger concentration at GCC hubs and steady expansion of terminal capacity, and this share anchors the channel’s role in the Middle East and Africa travel retail market. Cruise liners are the fastest-growing channel at a 17.76% projected CAGR through 2031, and new port infrastructure and the launch of Saudi cruise operations introduce incremental spaces where compact but premium assortments can thrive. Airport formats benefit from high transfer ratios at Gulf hubs and expanding retail footprints that add exposure for premium beauty, jewelry, and gift confectionery, which drive higher penetration and repeat buys. Additional square meters in new and refurbished terminals increase the number of storefronts, enabling brand clustering and stronger category zoning that improve wayfinding and speed purchasing. Airport-owned retailers also leverage vertical integration to optimize product flow and promotional calendars, which supports a consistent experience across concourses in the Middle East and Africa travel retail market.

The Middle East and Africa travel retail industry is using the cruise channel as a testing ground for localized concepts that resonate with Gulf and Red Sea itineraries, thereby diversifying channel exposure and extending the shopping window beyond airport dwell times. Gulf cruise terminals with integrated promenades offer duty-free products that complement onboard retail, supporting blended spending patterns among passengers who value both shipside and shore-side assortments. In Africa, cruise retail remains nascent, with terminals lacking dedicated space, and future tender frameworks that add bonded retail zones could lift channel contribution over time. Across channels, payment innovations and pre-orders are standardizing the shopper journey, reducing friction and improving capture rates as passengers move through multiple touchpoints from booking to boarding. Airport expansion programs and cruise-port build-outs collectively expand the physical canvas for retail, which underpins multi-year growth in the Middle East and Africa travel retail market.

By Traveler Demographics: Leisure Leads, Wellness Accelerates

Leisure Travelers represented 47.38% of spend in 2025, while Medical and Wellness Tourists are projected to expand at a 15.25% CAGR through 2031, and this split guides assortment planning and price laddering across hubs in the Middle East and Africa travel retail market. Saudi Arabia’s 2025 visitor base and the UAE’s strong hotel occupancy in 2025 reflected steady leisure demand, which correlates with category performance in beauty, gifts, and souvenirs. Business travel remains important as AfCFTA policies and route openings improve connectivity, and spending patterns include targeted luxury and premium electronics, which support a healthy base even with fewer trips per traveler. Passenger cohorts linked to visiting friends and relatives continue to grow, which raises appetite for value-led confectionery and small electronics that pack well and complement gifting. Wellness-focused passengers route through Gulf hubs for care or follow-up visits, which often yield longer dwell times and broader retail missions that combine self-care, gifting, and travel essentials.

The Middle East and Africa travel retail industry is using data-led targeting to tailor promotions to each cohort, improving conversion by aligning offers with mission types and time of day. Leisure and VFR segments respond to bundles and exclusives that deliver visible value, supporting confectionery growth without diluting brand equity. Business travelers value speed and proximity to premium lounges and fast-track corridors, which influence location strategy for luxury boutiques. Wellness travelers seek clean beauty and functional products, and curated storefronts near medical tourism corridors can increase penetration among this cohort. Aligning these micro-strategies with event calendars and route banks supports sustained growth in the Middle East and Africa travel retail market as passenger mixes evolve through 2031.

Geography Analysis

GCC countries accounted for 42.76% of revenue in 2025, and Sub-Saharan Africa posted the steepest projected growth at a 14.65% CAGR through 2031, underscoring the region’s split between scale today and velocity ahead in the Middle East and Africa travel retail market. GCC economies provide the largest current base for the Middle East and Africa travel retail market, and this position reflects both high passenger density and sustained investment in terminal space that lifts the commercial envelope per traveler. Airport expansions in Saudi Arabia and the UAE continue to add gates and concourses, which increase storefront availability for luxury and value-led products that drive penetration across multiple demographics. Saudi Arabia’s tourism policies and visa simplification efforts add another tailwind, which builds predictable peaks around pilgrimage and recurring city events that concentrate retail demand. Qatar’s concourse development added a substantial retail area in 2025, which supports premium beauty, fashion, and specialty formats that target transfer segments and high-yield origin-destination travelers. These dynamics create a robust foundation for the Middle East and Africa travel retail market, with GCC hubs serving as platforms for experiential retail concepts adaptable across the region.

Sub-Saharan Africa shows the fastest projected trajectory in the Middle East and Africa travel retail market, and underlying drivers include stronger intra-African trade, improved payment interoperability, and better air-service agreements that add new routes. Country-level growth is supported by reform momentum and selective investments by global concessionaires, who are deepening partnerships at leading airports, thereby raising assortment quality and improving store presentation. Customs harmonization and standards recognition under AfCFTA protocols reduce delays for bonded shipments, which enhances resilience in supply chains servicing African hubs. West African and East African gateways that modernize commercial areas will capture a larger share of spend as connecting traffic rises, bringing new cohort mixes with a higher propensity to purchase clean beauty, confectionery, and travel essentials. Continued route expansion and better terminal layouts will support the maturation of the Middle East and Africa travel retail market across African subregions through the forecast period.

North African markets form a connective corridor that benefits from both GCC linkages and European proximity, and recent concession wins in Tunisia illustrate how operators are leaning into this bridge position to tighten procurement and widen localized assortments. Morocco’s terminal development pipeline and cruise terminal projects in Casablanca are designed to support higher throughput and more integrated retail footprints, which increases the potential for both cruise and airport retail. Gulf cruise capacity and Dubai Harbour’s multi-ship terminal model add a complementary geography-led growth lever, which may pull more international cruise itineraries into the broader Middle East and Africa travel retail market over time. Together, these developments help distribute growth beyond a handful of anchor hubs and spread retail capability across more city pairs and travel corridors. The net effect is a more balanced geography mix within the Middle East and Africa travel retail market as investments move in tandem with air and sea passenger growth.

Competitive Landscape

Global operators and airport-owned retailers shape the competitive dynamics of the Middle East and Africa travel retail market, and the field balances strong incumbents with expansion-minded challengers. A leading global operator reported USD 17.06 billion (CHF 13.47 billion) in 2024 turnover following its merger integration, and it expanded further in North Africa, announcing 15 store concessions in Tunisia in early 2025, extending its footprint across the Mediterranean gateway network. Another global player increased exposure to Saudi Arabia and consolidated capabilities in Europe through a 2025 acquisition, which strengthens group-wide procurement and supplier terms that can benefit Middle East operations. Airport-owned retailers in the Gulf leverage vertical integration to align terminal design, traffic management, and retail strategy, thereby gaining an execution edge in new concourse openings and supporting premium shop-in-shop formats.

Joint-venture models are prevalent at large North African and Southern African gateways, and one European family-owned retailer highlighted that the Middle East and Africa accounted for a third of group turnover in 2024, supported by major openings in Saudi Arabia and long-standing partnerships in South Africa. Across the Middle East and Africa travel retail market, operators are investing in data, loyalty, and automation to boost labor productivity and improve campaign precision during peak transfer periods. Payment innovation underpins execution, with wallet integrations and crypto acceptance rolled out in select Gulf stores to reduce checkout friction and appeal to tech-forward cohorts. Regulatory settings for payments and biometrics are maturing under telecom and financial authorities, stabilizing the environment for the deployment of digital features across terminals. This digitalization tilt is strengthening the resilience of the Middle East and Africa travel retail market as operators optimize pricing, mix, and promotions by time and zone.

Macroeconomic and policy factors shape strategy across subregions, and operators adjust playbooks as oil prices fluctuate and regulatory conditions evolve. Fiscal surpluses in Qatar and the UAE supported consistent investment in terminal retail, enabling on-time delivery of commercial space during major capacity expansions. In Saudi Arabia, aviation and customs authorities are coordinating infrastructure and compliance frameworks that facilitate the scale-up of commercial offerings at primary and secondary airports. The competitive set remains dynamic as new domestic entrants in Saudi Arabia seek to capture a greater share of retail value within national ecosystems, introducing fresh models into the Middle East and Africa travel retail market. The next phase will likely blend premiumization, localization, and omnichannel features, as operators elevate experiences while protecting value tiers in response to oil-cycle sensitivity and varying consumer confidence across markets.

Middle East And Africa Travel Retail Industry Leaders

Lagardère Travel Retail

The Shilla Duty Free

Dubai Duty Free

Qatar Duty Free

Dufry AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Port of NEOM installed automated cranes in anticipation of its 2026 opening, aiming to enhance trade links and boost passenger and retail flows. This infrastructure investment supports Saudi Arabia's Red Sea cruise-port pipeline and positions NEOM as a multimodal logistics and tourism gateway.

- May 2025: Lagardère Travel Retail acquired a 70% stake in the Amsterdam Schiphol Duty Free business, taking over more than 20 stores covering perfumes, cosmetics, sunglasses, liquor, tobacco, and confectionery. While Schiphol is European, this acquisition strengthens Lagardère's global procurement leverage, benefiting its Middle East Africa operations through enhanced supplier terms.

- March 2025: Qatar Airways, Hamad International Airport, and Qatar Duty Free unveiled Concourses D and E, increasing annual passenger capacity to over 65 million and adding 2,700 square meters of retail space. The expansion introduced 10-plus new outlets, including the 100-square-meter Pop Mart boutique, the first in the Middle East Africa region, and reinforced Hamad International Airport's Skytrax 2024 ranking as the World's Best Airport.

- March 2025: Saudi Arabia's Public Investment Fund launched Al Waha, the kingdom's first domestically owned duty-free retailer, signaling Vision 2030's intent to capture retail revenues historically claimed by international operators and align with the USD 79.94 billion (SAR 300.00 billion) domestic tourism-spending target.

Middle East And Africa Travel Retail Market Report Scope

Travel retail in the Middle East and Africa refers to the formal sale of duty-free and duty-paid goods to international travelers within controlled environments, such as airports, seaports, and border crossings.

The Middle East and Africa travel retail market report is segmented by product type (fashion and accessories, wine and spirits, tobacco, food and confectionary, fragrances and cosmetics, other product types), distribution channel (airports, cruise liners, railway stations, other distribution channels), traveler demographics (business travelers, leisure travelers, visiting friends & relatives, medical & wellness tourists, student travelers), and geography (United Arab Emirates, Saudi Arabia, South Africa, Nigeria, Rest of Middle East and Africa). The market forecasts are provided in terms of value (USD).

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionary |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends & Relatives (VFR) |

| Medical & Wellness Tourists |

| Student Travelers |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| South Africa |

| Nigeria |

| Rest of Middle East And Africa |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionary | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends & Relatives (VFR) | |

| Medical & Wellness Tourists | |

| Student Travelers | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

Key Questions Answered in the Report

What is the current size and growth outlook for the Middle East and Africa travel retail market in 2026?

The Middle East and Africa travel retail market size is USD 8.24 billion in 2026 and is projected to reach USD 13.87 billion by 2031 at a 13.87% CAGR, supported by capacity expansion and policy-led tourism growth.

Which product category leads the Middle East and Africa travel retail market in 2026?

Fragrances and Cosmetics lead by revenue, with 32.36% share in 2025, while Food and Confectionery have the fastest projected growth to 2031, aided by curated gifting and localized SKUs.

What channels are driving growth in the Middle East and Africa travel retail market?

Airports dominate with 87.36% share in 2025 due to high passenger concentration and expanding concourses, while Cruise Liners show the fastest projected CAGR through 2031 as new terminals and Gulf cruise capacity come online.

Which geographies are most important for the Middle East and Africa travel retail market?

GCC countries account for the largest share at 42.76% in 2025, given their hub airports and high dwell times, while Sub-Saharan Africa is the fastest-growing region due to trade integration, visa openness, and payments interoperability.

What are the main risks facing the Middle East and Africa travel retail market?

Key risks include political instability in select African subregions, oil-price volatility that can temper GCC spending, and stricter tobacco regulations that raise compliance costs, though operators are mitigating these through portfolio diversification and payment innovation.

Which strategic moves defined 2025 in the Middle East and Africa travel retail market?

Notable moves included Avolta’s 15-store entry into Tunisia, Lagardère’s acquisition of a 70% stake in Amsterdam Schiphol Duty Free to boost procurement leverage, and Qatar’s new concourses that added 2,700 square meters of retail.

Page last updated on: