Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.28 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 5.84 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Travel Retail Market Analysis by Mordor Intelligence

The Thailand Travel Retail Market size was valued at USD 3.28 billion in 2025 and is estimated to grow from USD 3.62 billion in 2026 to reach USD 5.84 billion by 2031, at a CAGR of 10.02% during the forecast period (2026-2031).

The upturn is supported by passenger recovery across Airports of Thailand’s network and by targeted policy measures that keep Thailand competitive among regional tourism hubs. The August 2024 closure of all inbound duty-free shops redirected spend toward departure-side stores and downtown formats, which concentrates volume in core locations where operators can drive higher-value conversion. Visa-policy liberalization for priority origin markets, including the mutual visa-free regime with China from March 2024, is widening the pool of free independent travelers who exhibit a stronger propensity to buy premium goods at airports. Chinese arrivals remained below pre-pandemic benchmarks in 2025, which shifts sales mix toward long-haul and high-value cohorts while pressuring operators to improve basket size through curated assortments and omnichannel pre-order.

Key Report Takeaways

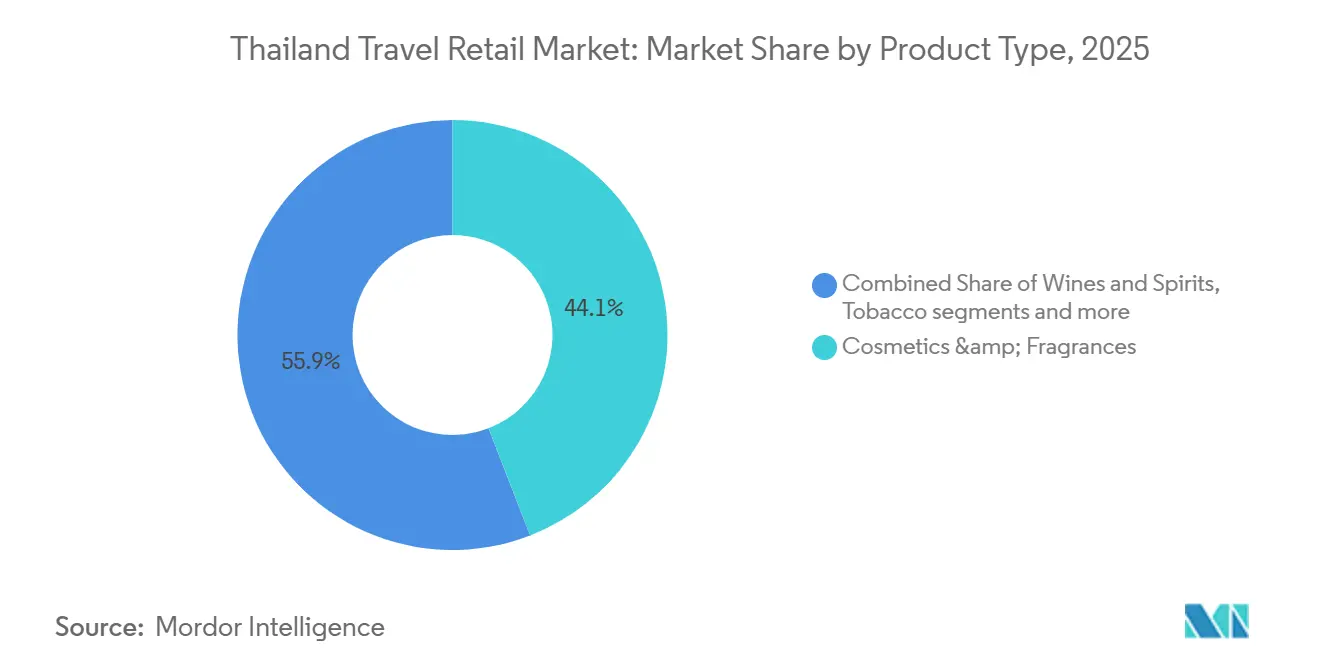

- By product type, Cosmetics & Fragrances led with 44.12% in 2025, while Wines & Spirits is forecast to expand at a 9.11% CAGR through 2031.

- By distribution channel, Airports held a 65.42% share in 2025, while Airports are projected to post the highest CAGR at 9.18%.

- By geography, Central Thailand accounted for a 60.25% share in 2025, while Northern Thailand is projected to grow at a 9.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Travel Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism rebound post-pandemic & tourist-visa liberalisation | +2.1% | Global, with concentration in Northeast Asia, South Asia, and Eastern Europe | Medium term (2-4 years) |

| Airport capacity expansion (Suvarnabhumi East, Don Mueang T3, Phuket) | +1.8% | Central Thailand, Southern Thailand, Northern Thailand, with spill-over to regional hubs | Long term (≥ 4 years) |

| Premium beauty & personal-care boom among inbound visitors | +1.4% | Asia-Pacific core with spill-over from Middle East visitors in Phuket | Medium term (2-4 years) |

| Luxury tax and wine duty reforms stimulate duty-free spending | +1.2% | National, with particular strength in Bangkok, Phuket, and Chiang Mai | Short term (≤ 2 years) |

| Cancellation of arrival duty-free shifts spent on departures/downtown | +0.8% | National, concentrated in major airports and selected downtown flagships | Short term (≤ 2 years) |

| Omnichannel pre-order & e-wallet integration lifts conversion rates | +0.9% | Global, with early gains in Bangkok, Phuket, and Chiang Mai; strongest among Chinese travelers using cross-border QR payments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound Post-Pandemic & Tourist-Visa Liberalisation

Thailand’s visa policies have been a clear tailwind since 2024, including the mutual visa-free arrangement with China that took effect in March 2024 and broader visa measures to support source-market recovery. Total international arrivals in 2025 remained in a stabilized range, with changes in source-market mix that elevate the share of long-haul and high-spending visitors for the Thailand travel retail market. The performance of the Thailand travel retail market is increasingly tied to dwell time and ticket size, which tend to be higher for independent travelers planning pre-orders and luxury purchases[1]Tourism Authority of Thailand, “Tourism Statistics 2024–2025,” Tourism Authority of Thailand, tourismthailand.org. Digital payment readiness, including cross-border QR interoperability, reduces frictions at checkout and helps the Thailand travel retail market convert intent into transactions more consistently.

Airport Capacity Expansion (Suvarnabhumi East, Don Mueang T3, Phuket)

Airports of Thailand is executing a multi-year capacity program that raises long-run passenger throughput and the platform’s ability to capture non-aeronautical revenue, with upgrades at Bangkok’s dual-airport system and in Phuket backed by defined timelines. Non-aeronautical revenue already accounts for a material share of AOT’s total revenue, reinforcing the strategic role of commercial yield management in the Thailand travel retail market. Expansion phases occasionally require flow redesigns and space reconfiguration, but the long-term effect is to enlarge airside commercial canvases and staff productivity per square meter for the Thailand travel retail market[2]Airports of Thailand, “Annual Report 2024,” Airports of Thailand, aot.co.th. The August 2024 policy closure of inbound duty-free consolidated spend at departures and in selected downtown hubs that emphasize curated experiences and pre-order pickup. Infrastructure improvements, paired with optimized concessions, strengthen the tie between passenger growth and retail receipts, which should accrue to the Thailand travel retail market over the forecast horizon.

Premium Beauty & Personal-Care Boom Among Inbound Visitors

The T-Beauty phenomenon, where Thai cosmetics captured 97.62% of Thailand's beauty imports into China and Bangkok Cosmoprof 2025 attracted 23,000+ visitors (+20% year-on-year), has elevated Thailand from a sourcing backwater to a must-stock destination for international travelers, yet this shift's travel retail implications extend far beyond stocking Mistine and Cathy Doll[3]IMPACT Exhibition and Convention Center, “Event Highlights,” IMPACT / ICE Bangkok, icebangkok.com . Regulatory oversight by Thailand’s Food and Drug Administration assures product authenticity and compliance, which sustains trust at the point of sale for the Thailand travel retail market. Digital payments and loyalty tie-ins help move beauty shoppers from browsing to basket confirmation, which supports margin mix through premium lines for the Thailand travel retail market. These operational and regulatory pillars strengthen conversion and repeat purchases in a category that already leads overall travel retail demand in Thailand.

Luxury-Tax and Wine-Duty Reforms Stimulate Duty-Free Spending

Wine import duty elimination and excise adjustments implemented in early 2024 altered Thailand’s price architecture and encouraged broader participation in the category. The reforms expand the addressable base for wines and premium spirits while inviting duty-free operators to differentiate through exclusive allocations, limited releases, and pre-order commitments. As price parity narrows with domestic retail, airport operators are emphasizing assortment uniqueness, giftability, and traveler services to sustain category leadership within the Thailand travel retail market[4]King Power International Group, “Official Site,” King Power, kingpower.com. Duty-free allowances on liquor remain relevant to purchase planning, and integration of pre-order windows with flight itineraries supports considered, higher-value purchases. Category momentum, coupled with service design and inventory privileges, points to the continued relevance of wines and spirits in the Thailand travel retail market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on volatile Chinese tourist flows | -1.6% | National, with acute impact in Bangkok, Phuket, and Pattaya | Medium term (2-4 years) |

| High concession fees & minimum-guarantee burdens | -1.3% | National, concentrated at AOT gateways where major concessions are operated. | Long term (≥ 4 years) |

| King Power liquidity crisis/contract renegotiation risk | -1.0% | National, systemic exposure given the concentration of airport duty-free operations | Medium term (2-4 years) |

| E-commerce price transparency erodes price advantage | -1.1% | National, mitigated by the January 2026 removal of low-value duty exemptions. | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Volatile Chinese Tourist Flows

The recovery of Chinese visitors remained uneven in 2025 despite visa facilitation, which keeps the outlook sensitive for operators exposed to this cohort. Segment volatility affects airport locations with merchandise mixes that historically skewed toward Chinese tour-group preferences. Operators have accelerated diversification across other source markets, which changes category priorities and language capabilities at frontline counters for the Thailand travel retail market. The mix shift increases the weight of long-haul travelers who buy premium categories, but it requires sustained investment in service design to stabilize conversion over time. Policy efforts remain supportive, yet demand-side caution reinforces the need for omnichannel and loyalty levers to balance the revenue base of the Thailand travel retail market.

High Concession Fees & Minimum-Guarantee Burdens

Thailand’s airport concessions operate under revenue-sharing and minimum-guarantee frameworks that require operators to balance fixed commitments with variable demand. As non-aeronautical income rises in importance for airport operators, commercial terms are structured to protect the public landlord, which compresses margin flexibility for retailers during slowdowns in the Thailand travel retail market. Contract revisions have focused on continuity and yield protection while aligning timelines with major infrastructure projects. This environment benefits operators with sufficient capital, technology, and loyalty infrastructure, and it raises entry barriers for new players considering Thailand’s large hubs. The aggregate effect is to strengthen the incentive for superior execution while limiting price-based competition in the Thailand travel retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cosmetics Dominance Meets Spirits Revival

Cosmetics & Fragrances commanded 44.12% of Thailand's travel retail market share in 2025, and this leadership reflects consistent buyer interest in premium beauty, curated sets, and travel-exclusive lines. The category benefits from pre-trip discovery and event-led visibility, which positions operators to capture demand through pre-order, collection timing, and loyalty benefits. Beauty, authenticity, and safety regulation under Thailand’s Food and Drug Administration help preserve confidence at the point of sale, which underpins conversion in high-velocity airport environments. Wines & Spirits is the fastest-growing product group with a projected 9.11% CAGR through 2031, supported by 2024 tax reforms that broadened category participation and encouraged premium trading-up. Duty-free operators are leaning into exclusivity, limited releases, and concierge service to keep the Thailand travel retail market competitive, where domestic prices have moved closer to duty-free levels.

The wider luxury ecosystem is reinforcing high-aspiration purchasing through experiential concepts, visible in watch and jewelry showcases within flagship locations that add traffic and dwell to neighboring categories. Curated horology and fine jewelry help anchor premium positioning for the Thailand travel retail market, and they complement beauty and spirits in multi-category baskets. Tobacco remains managed by a tight regulatory regime and enforcement against prohibited products, which preserves clarity for compliant retail operations. Food & Confectionery maintains steady traveler appeal through gifting and impulse formats, and operators use seasonal assortments to support conversion among family and group travelers. Taken together, the breadth of assortment, exclusivity, and compliance underpin product strength and help sustain a premium mix within the Thailand travel retail market.

By Distribution Channel: Airports Reign, Downtown Retreats

Airports accounted for 65.42% of sales in 2025 and are projected to post a 9.18% CAGR, reaffirming their primacy as the most efficient channel for scale, conversion, and logistics in the Thailand travel retail market. Airports of Thailand’s sustained investment in capacity and the rising share of non-aeronautical revenue underscore the strategic importance of commercial yield across the network. In-flight duty-free on national carriers complements airside retail by adding pre-order windows and on-seat delivery that can capture specific segments, such as fragrance and gifting. Digital payments and secure checkout processes reduce friction and support larger basket values, especially for pre-committed purchases. These factors keep airport formats central to shopper journeys and sustain channel expansion in the Thailand travel retail market.

Downtown duty-free has evolved toward flagship and experiential concepts that serve urban residents and free independent travelers with curated zones and assisted pickup for airport-bound items. The August 2024 end of inbound duty-free activity steered residual purchase intent to departure-side and downtown units, which reinforced the shift toward premium experiences and pre-order conversion. Airlines are introducing subscription and loyalty constructs that keep frequent travelers in branded ecosystems while reinforcing ancillary spending touchpoints. Airport e-commerce integration and click-to-collect programs have extended the shopping window, which aligns with omnichannel strategies now standard in the Thailand travel retail market. The cumulative effect is a more deliberate shopper journey that privileges convenience, authenticity, and exclusivity over pure price comparison in Thailand’s travel retail.

Geography Analysis

Central Thailand is the commercial core of the Thailand travel retail market, led by Bangkok’s dual-airport system and strong luxury retail infrastructure, and it accounted for a 60.25% share in 2025. International passenger recovery has been firm, with Airports of Thailand reporting surging throughput that supports the base for airside retail. Departure-side concentration after the policy shift on inbound duty-free has benefited Bangkok gateways, where curated formats and pre-order collection are easiest to scale. Supporting systems, including duty-free e-commerce touchpoints and loyalty integration, are densest in Central Thailand, which magnifies its lead within the Thailand travel retail market. These advantages position the region to sustain growth as capacity expansions continue.

Northern Thailand is the fastest-growing region at a projected 9.63% CAGR through 2031, with Chiang Mai’s expansion plan a key enabler of future capacity. Infrastructure roadmaps anticipate significant upgrades that align with cultural and experiential travel patterns that favor this region. The visitor mix tends to skew toward independent travelers who prefer longer stays and curated purchases, which fits well with pre-order models for the Thailand travel retail market. Northern gateways also serve as diversification valves for national networks where Bangkok faces peak constraints. Consistent policy support for regional tourism development improves the medium-term outlook for retail growth at airports in the North.

Southern Thailand remains a pivotal luxury and resort corridor, with Phuket Airport on a defined upgrade path to raise installed capacity and improve service levels. The mix of long-haul visitors and premium resort traffic supports watches, jewelry, spirits, and beauty categories within the Thailand travel retail market. Airfield and terminal improvements in the South are expected to convert into higher non-aeronautical yields as airside layouts are optimized for retail. Forward infrastructure planning in Eastern Economic Corridor nodes adds optionality for the regional dispersion of passenger flows. Collectively, these geographic dynamics reinforce the concentration of value in Central Thailand, the velocity advantage in the North, and the premium mix in the South across the Thailand travel retail market.

Competitive Landscape

Airport concessions in Thailand are highly concentrated, with a single incumbent operating across major AOT-managed gateways and shaping category execution and loyalty integration for the Thailand travel retail market. Post-pandemic renegotiations aimed to balance continuity with higher yield capture for the public landlord, and they aligned contract windows with long-horizon infrastructure plans. The concentration of airside operations rewards scale players that can sustain capital, inventory, and technology requirements while meeting service standards. This structure is a core context for strategic moves by incumbents and partners in the Thailand travel retail market. Partnership models that combine global loyalty ecosystems with local retail footprints have become central to value creation.

Operators are investing in experiential downtown formats that complement airport stores, with flagship concepts that organize high-value categories into curated zones and provide assisted airport collection for restricted items. The role of omnichannel has expanded from basic pre-order to journey-wide engagement, which integrates product discovery, price transparency, loyalty rewards, and pickup logistics for the Thailand travel retail market. In-flight duty-free on national carriers remains a relevant extension for select categories, and it provides additional pre-order and delivery options around long-haul schedules. Airline subscription and lounge programs create recurring engagement points that can influence incidental purchases. Together, these tactics improve conversion along a traveler’s path and reinforce ecosystem stickiness in Thailand’s travel retail.

Global partners are strengthening technology utility across borders, including mobile app features, local currency pricing, and connectivity improvements for Chinese travelers who expect seamless digital journeys. Airport-side digitization and compliance fundamentals, including payment security and data protection standards, remain table stakes as baskets shift to higher-value categories in the Thailand travel retail market. Operators are also aligning with regulatory and customs frameworks on allowances and labeling, which assures a consistent traveler experience at exit points. Capacity upgrades and longer concession horizons support the business case for sustained investment in brand boutiques and exclusive allocations. The overarching pattern is a consolidation of capability around scale, loyalty, compliance, and experiential formats in the Thailand travel retail market.

Thailand Travel Retail Industry Leaders

King Power International Group

Airports of Thailand PLC

Central Pattana

Lotte Duty Free

The Shilla Duty Free

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Airports of Thailand Public Company Limited (AOT) approved amended duty-free concession conditions with King Power Duty Free at Suvarnabhumi, Don Mueang, Phuket, Chiang Mai, and Hat Yai airports to continue operations and align contracts with current business realities rather than terminate them.

- November 2025: King Power City Boutique opened at One Bangkok’s Parade Zone, Thailand’s first city-boutique duty-free and lifestyle retail concept spanning 5,248 m² on two floors, featuring curated zones for luxury goods, spirits, watches, and Thai makers under an experiential shopping model.

- September 2025: Avolta and King Power International Group launch the “Club Avolta X Power Pass” loyalty partnership, creating a borderless loyalty experience that offers reciprocal benefits across Avolta’s global travel-retail network and King Power’s duty-free and travel-related ecosystem in Thailand.

- July 2024: The Thai government implemented a policy eliminating inbound duty-free shops at major international airports (including Suvarnabhumi, Don Mueang, Phuket, Chiang Mai, Hat Yai, U-Tapao, Samui, and Krabi), reclaiming approximately 2,250 m² of space and redirecting tourist spending to domestic retail channels.

Thailand Travel Retail Market Report Scope

Travel retail is a specialized area of the retail market that serves tourists and other travelers. It can be characterized as the sale of goods and services to travelers leaving, arriving at, or passing through an airport, seaport, railway station, or other travel-related facilities.

The market is segmented by product type and by distribution channel. By product type, the market is sub-segmented into beauty and personal care, wines and spirits, tobacco, eatables, fashion accessories, and hard luxury, and other product types, and by distribution channel, the market is sub-segmented into airports, airlines, ferries, and other distribution channels.

The report offers the market sizes and forecasts in value (USD) for all the above segments.

By Product Type

| Fashion & Accessories |

| Jewelry & Watches |

| Wines & Spirits |

| Food & Confectionery |

| Cosmetics & Fragrances |

| Tobacco |

| Other Product Types (Stationery, Electronics, etc.) |

By Distribution Channel

| Airports |

| Airlines |

| Ferries |

| Other Channels (Railway Stations, Border Shops, Downtown) |

By Geography

| Central Thailand |

| Northern Thailand |

| Northeastern Thailand (Isan) |

| Eastern Thailand |

| Western Thailand |

| Southern Thailand |

| By Product Type | Fashion & Accessories |

| Jewelry & Watches | |

| Wines & Spirits | |

| Food & Confectionery | |

| Cosmetics & Fragrances | |

| Tobacco | |

| Other Product Types (Stationery, Electronics, etc.) | |

| By Distribution Channel | Airports |

| Airlines | |

| Ferries | |

| Other Channels (Railway Stations, Border Shops, Downtown) | |

| By Geography | Central Thailand |

| Northern Thailand | |

| Northeastern Thailand (Isan) | |

| Eastern Thailand | |

| Western Thailand | |

| Southern Thailand |

Key Questions Answered in the Report

What is the current size and growth outlook for the Thailand travel retail market?

The Thailand travel retail market size was USD 3.62 billion in 2026 and is projected to reach USD 5.84 billion by 2031 at a CAGR of 10.02%.

Which product categories lead sales in Thailand’s airport and duty-free ecosystem?

Cosmetics & Fragrances lead the mix, and Wines & Spirits is the fastest-growing category on the back of 2024 tax reforms and premiumization.

How important are airports as a channel in Thailand’s travel retail?

Airports accounted for 65.42% of 2025 sales and are projected to post the highest channel CAGR, supported by capacity upgrades and a non-aeronautical revenue focus.

What policy shifts are shaping traveler purchases in Thailand?

The mutual visa-free regime with China, the August 2024 closure of inbound duty-free, and the January 2026 end of low-value duty exemptions are key drivers of channel dynamics and pricing.

Which regions within Thailand are poised for the fastest growth?

Northern Thailand is projected to grow the fastest through 2031 as capacity plans and experiential tourism patterns align, while Central Thailand remains the largest base.

Page last updated on: