Construction Toy Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.34 Billion |

| Market Size (2031) | USD 17.13 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

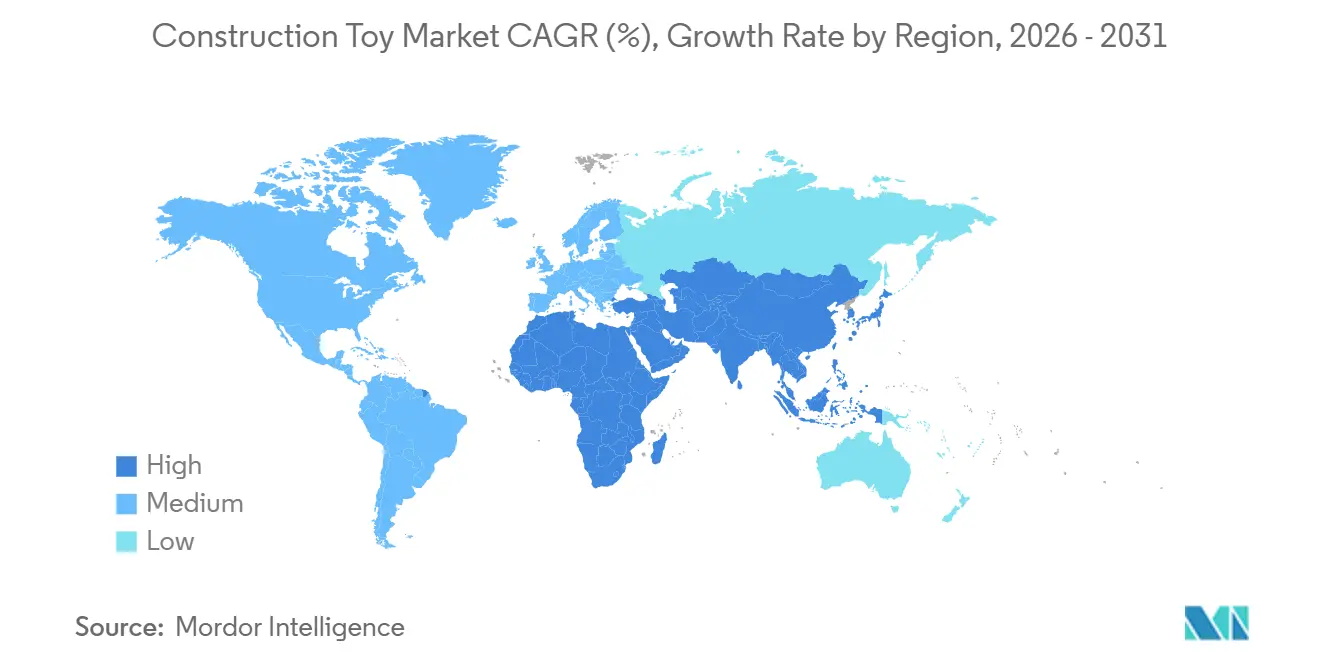

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

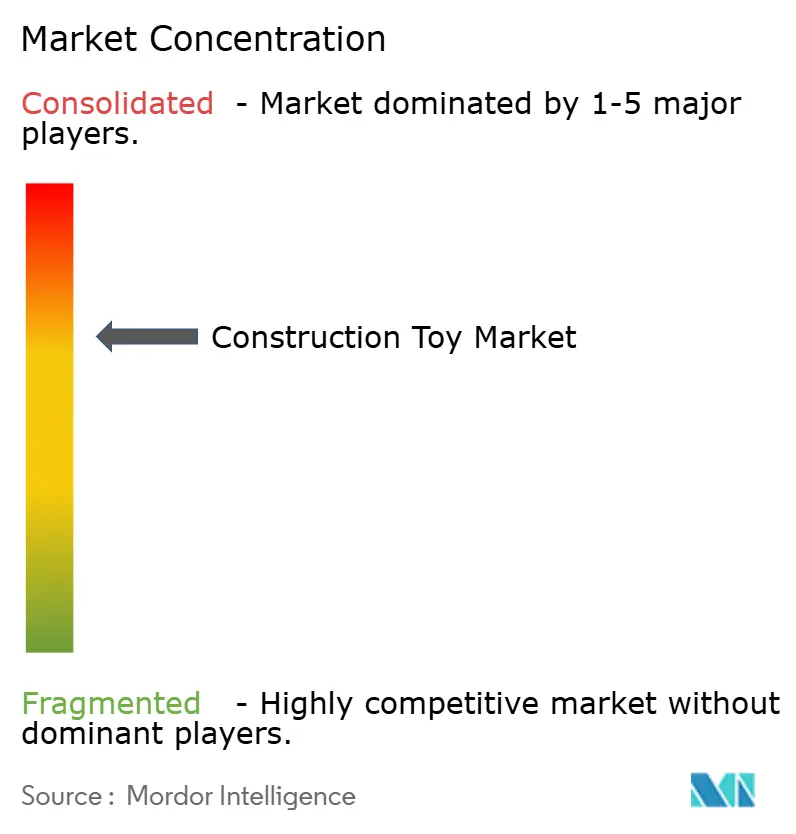

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Construction Toy Market Analysis by Mordor Intelligence

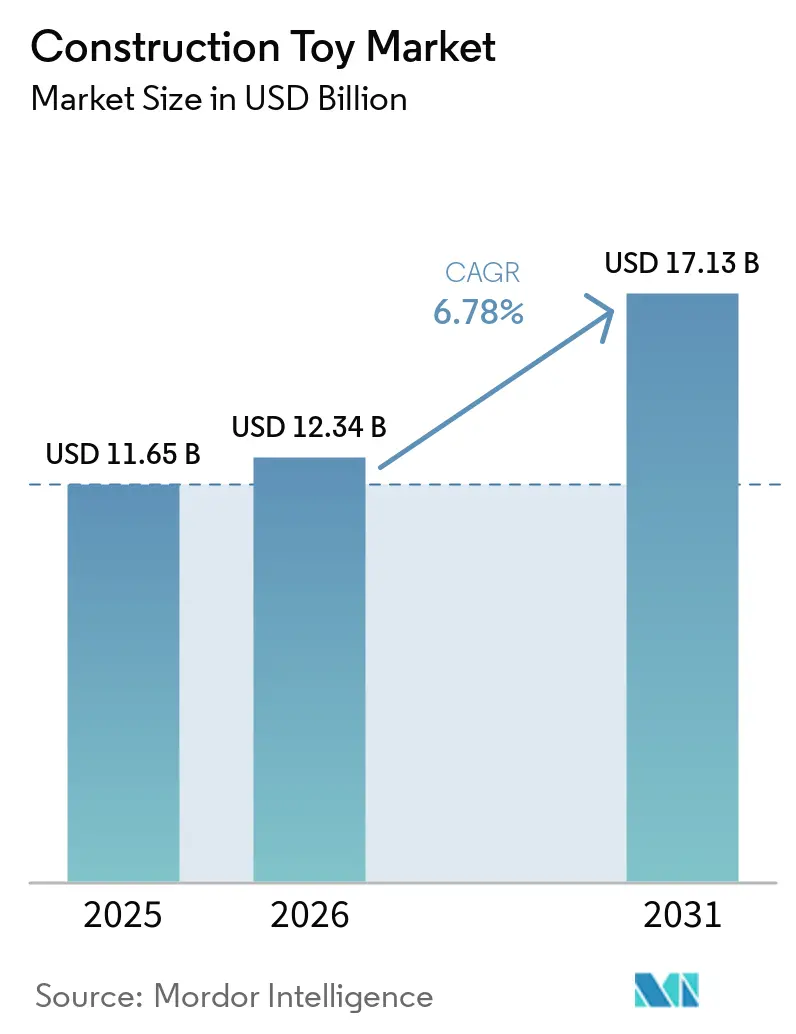

The construction toy market was valued at USD 11.65 billion in 2025 and is expected to reach USD 12.34 billion in 2026, with projections estimating growth to USD 17.13 billion by 2031, at a CAGR of 6.78% during the 2026–2031 forecast period. This growth is driven by the increasing demand for toys that combine entertainment with creativity, problem-solving, and skill development. The rising awareness of play-based learning has further fueled the demand for products that promote cognitive development, imagination, and practical learning experiences. Additionally, the market is benefiting from ongoing product innovation, including advanced building mechanisms, interactive features, smart functionalities, and intricate designs that enhance engagement beyond traditional play.

Key Report Takeaways

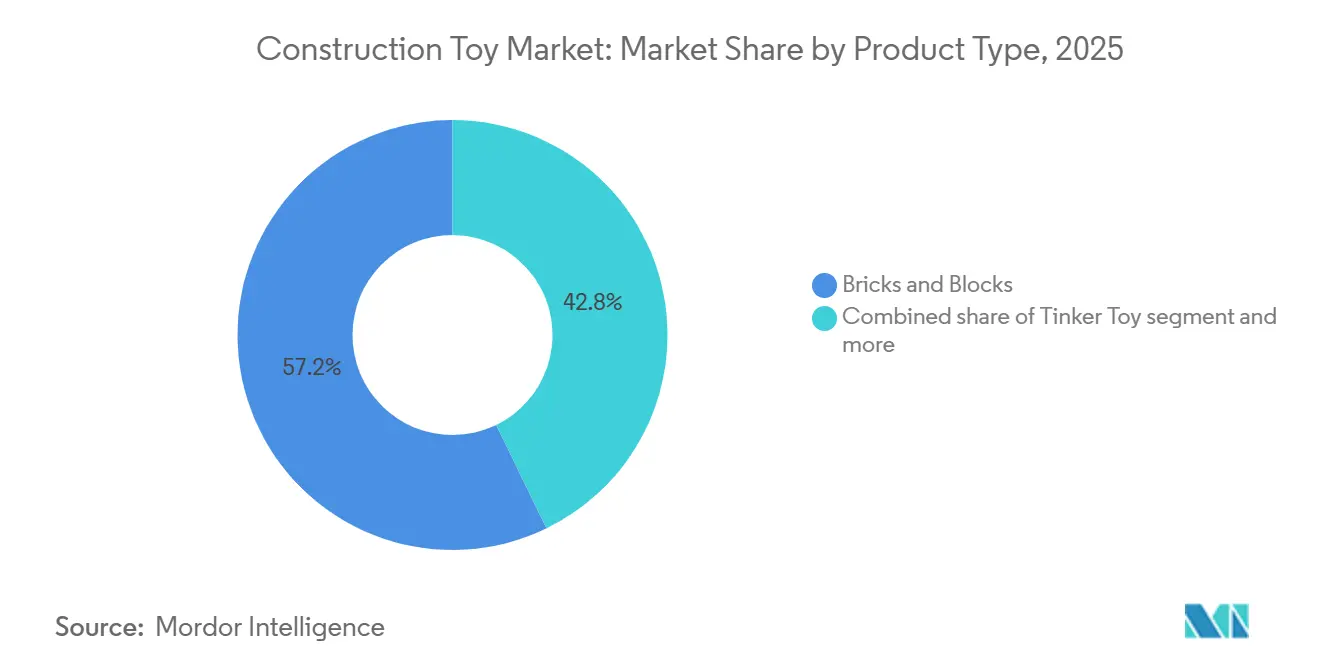

- By product type, bricks and blocks held 57.21% of the construction toy market share in 2025, while tinker toy is forecast to expand at 7.39% through 2031.

- By material, polymer accounted for 36.53% of the construction toy market size in 2025, while wood is projected to grow at 7.93% through 2031.

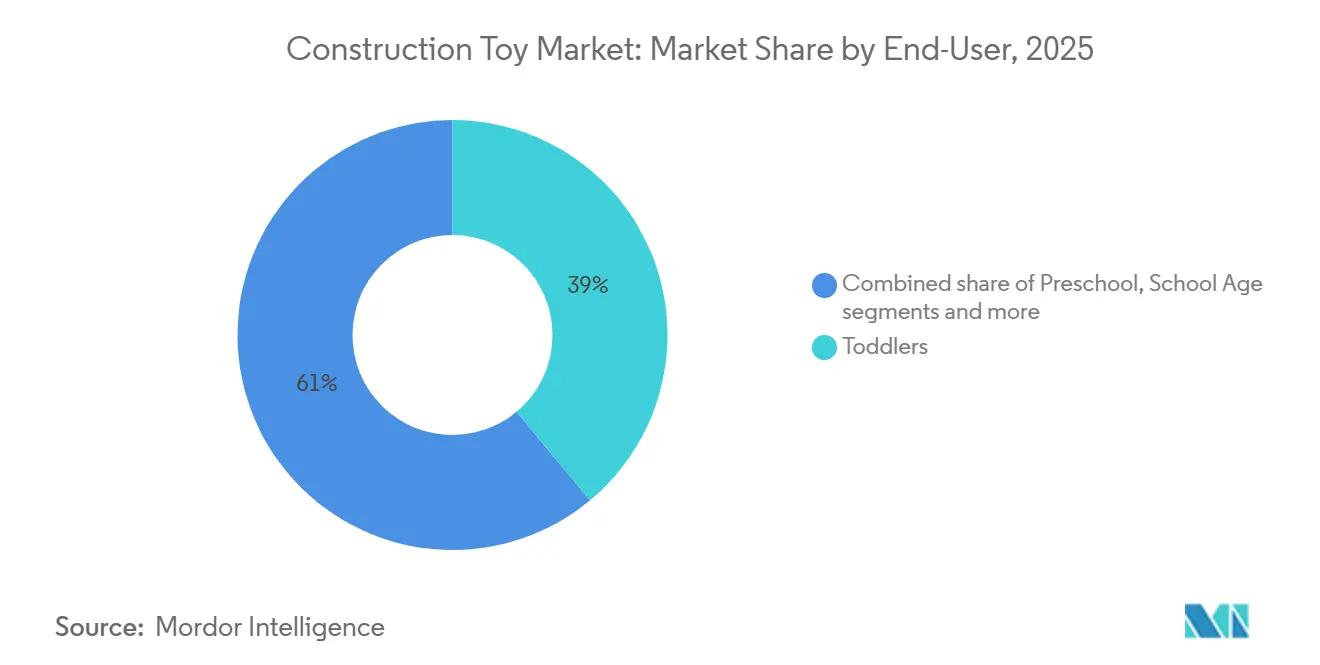

- By end-user, toddlers led with 38.95% share in 2025, while teenagers are expected to record the highest CAGR of 7.31% through 2031.

- By distribution channel, supermarkets and hypermarkets held 41.23% share in 2025, while online retail stores are projected to advance at 8.45% through 2031.

- By geography, North America accounted for 34.33% share in 2025, while Asia-Pacific is forecast to grow at 7.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Construction Toy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on STEM-based learning and educational toys | +1.9% | Global, particularly strong in North America, Western Europe, and East Asia | Medium term (2–4 years) |

| Focus on cognitive development and skill-based play | +1.1% | Global, with concentrated impact in North America and Asia-Pacific | Medium term (2–4 years) |

| Increasing integration of technology and interactive features | +1.0% | North America, Western Europe, Japan, South Korea | Medium term (2–4 years) |

| Preference for screen-free and hands-on activities | +0.7% | North America and Europe, spill-over to urban Asia-Pacific and Middle-East and Africa | Short term (≤ 2 years) |

| Adoption of construction toys in schools and learning centers | +0.8% | North America, Europe, China, India, Southeast Asia | Long term (≥ 4 years) |

| Demand for sustainable and eco-friendly construction toys | +0.6% | Western Europe and North America core, growing in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing emphasis on STEM-based learning and educational toys

The increasing focus on STEM-based learning and educational toys is driving growth in the construction toy market. Parents, educators, and learning institutions are recognizing the value of hands-on play in fostering essential skills. Construction toys offer interactive learning opportunities by introducing children to fundamental concepts in science, engineering, mathematics, design, and problem-solving through building activities. Unlike traditional toys that primarily provide entertainment, construction sets encourage experimentation, logical thinking, spatial awareness, and creativity by enabling users to plan, assemble, test, and refine their creations. The growing adoption of activity-based learning methods has boosted the demand for toys that integrate education with engagement, positioning construction toys as a key tool for early skill development.

Focus on cognitive development and skill-based play

The increasing emphasis on cognitive development and skill-based play reflects a growing consumer preference for toys that offer meaningful engagement beyond mere entertainment. Construction toys play a significant role in fostering problem-solving abilities, spatial reasoning, creativity, concentration, patience, and decision-making skills. These toys enable users to design, assemble, and refine their creations through hands-on activities. They also promote progressive learning, allowing users to advance from simple structures to more complex builds, thereby enhancing planning and logical thinking over time. Additionally, the recognition of play as a means for creativity, relaxation, and personal development is driving interest in these toys among a wider audience. According to The Toy Association, 81% of parents in 2025 included a toy or game for themselves in their holiday shopping lists, up from 72% in the previous year [1]Source: The Toy Association, "Toy and Play Trends", toyassociation.org. This trend highlights the growing appeal of toys as tools for engagement, creativity, and skill-building across various age groups.

Increasing integration of technology and interactive features

The integration of technology and interactive features is driving growth in the construction toy market by transforming traditional building activities into more engaging and skill-enhancing experiences. The inclusion of smart components, sensors, robotics, coding capabilities, app connectivity, and interactive elements enables users to create models that move, respond, and perform specific actions, thereby increasing the play value of these toys. These technological advancements promote experimentation, logical thinking, and technical skill development by merging physical assembly with digital interaction. For example, The LEGO Group introduced LEGO SMART Play technology at Toy Fair 2026, featuring the LEGO SMART Brick, highlighting the industry's shift toward connected and intelligent building systems. Such innovations enhance user engagement by incorporating programmable functions and immersive experiences, while also extending the lifecycle of construction toys beyond traditional building activities, contributing to sustained market growth.

Preference for screen-free and hands-on activities

The increasing preference for screen-free, hands-on activities is driving growth in the construction toy market. Parents and caregivers are seeking alternatives that promote active participation, creativity, and real-world interaction. Concerns about the effects of prolonged digital device usage have heightened demand for toys that offer immersive offline experiences while fostering attention span, imagination, and independent thinking. Construction toys provide a tactile play environment where users physically manipulate components, experiment with designs, and solve problems through trial and error, resulting in deeper engagement compared to passive entertainment. The ability to build, rebuild, and customize structures supports extended play sessions while enhancing patience, focus, and fine motor skills. As families emphasize balanced recreational activities that combine enjoyment with developmental benefits, construction toys are increasingly recognized as valuable tools for creative, hands-on learning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from digital entertainment and gaming platforms | -0.9% | Global, most acute in North America, East Asia, and Western Europe | Short term (≤ 2 years) |

| Concerns related to small components and choking hazards | -0.5% | Global, with regulatory pressure concentrated in North America, Europe, and Australia | Medium term (2–4 years) |

| Product recalls due to quality and safety issues | -0.4% | Global, particularly relevant for brands manufacturing in lower-cost regions | Medium term (2–4 years) |

| Availability of counterfeit and low-quality construction toys | -0.6% | Asia-Pacific core, spill-over to Middle-East and Africa and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from digital entertainment and gaming platforms

The growth of the construction toy market is being restrained by increasing competition from digital entertainment and gaming platforms. Children and teenagers are spending more time on smartphones, video games, streaming platforms, and other digital activities. Interactive digital content provides instant entertainment, regular updates, social connectivity, and immersive experiences, which can diminish interest in traditional hands-on play. Construction toys, which require time, patience, concentration, and physical assembly, face challenges in appealing to users accustomed to fast-paced digital engagement. The rising availability of mobile games, virtual building platforms, and online entertainment options has further intensified competition for recreational time and attention. Moreover, the shift in play habits toward digital-first experiences may reduce the frequency of physical toy usage. As a result, construction toy manufacturers are focusing on innovation, incorporating interactive features and hybrid play models to sustain consumer interest.

Concerns related to small components and choking hazards

Concerns regarding small components and choking hazards are limiting the growth of the construction toy market. Many building sets include small, detachable pieces, necessitating careful age classification and safety considerations. Construction toys rely on connectors, blocks, rods, and miniature components to create intricate structures, but these elements can pose risks for younger users if swallowed or misused. Such safety concerns significantly influence purchasing decisions, particularly for products aimed at younger age groups, where safety is a primary consideration for parents and caregivers. Manufacturers are required to adhere to strict regulations concerning component size, material safety, labeling, and product testing, which complicates the development of innovative yet child-safe products. Additionally, safety issues, product recalls, or non-compliance with toy safety standards can erode consumer trust and damage brand reputation. Consequently, balancing detailed construction experiences with stringent safety requirements remains a critical challenge for market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bricks and Blocks Command the Premium Shelf

Bricks and blocks accounted for a 57.21% market share in the construction toy market in 2025, driven by their ability to provide flexible, open-ended building experiences that promote repeated use and long-term engagement. Unlike fixed-pattern toys, bricks and blocks enable users to create, dismantle, and rebuild various structures, enhancing their play value and extending the product lifecycle. This segment benefits from features such as interlocking designs, durability, compatibility across different sets, and ease of use for various skill levels. The hands-on assembly process fosters creativity, spatial reasoning, concentration, and planning skills, making these toys a preferred choice for developmental play. Continuous advancements in brick designs, including improved fitting mechanisms, enhanced colors, diverse shapes, lightweight structures, and specialized pieces, have expanded building possibilities and enhanced the user experience.

The Tinker Toy segment is projected to grow at the fastest CAGR of 7.39% during 2026–2031, driven by its emphasis on mechanical building, structural experimentation, and hands-on engineering-focused play. The growth of this segment is supported by the rod-and-connector systems that allow users to create movable, three-dimensional structures, demonstrating basic engineering principles such as balance, rotation, joints, and framework design. Unlike traditional stacking-based construction toys, Tinker Toys encourage trial-and-error building methods, enabling users to explore component interactions and strengthen design thinking and problem-solving skills. The ability to construct functional models, including towers, vehicles, machines, and moving structures, enhances engagement by offering a more realistic and interactive building experience.

By Material: Polymer Leads, but Wood Signals the Institutional Premium

The polymer segment maintained its leading position with a 36.53% market share in 2025, attributed to its adaptability, durability, and suitability for precise construction toy designs. Polymer materials enable manufacturers to produce lightweight components with consistent shapes, accurate fitting systems, smooth edges, and strong interlocking capabilities, which are critical for repeated assembly and disassembly. The material's flexibility supports the creation of a wide range of colors, textures, sizes, and specialized components while ensuring strength and long product lifecycles. Additionally, advancements in molding techniques have enhanced the quality of polymer-based pieces by achieving tighter tolerances, improved surface finishes, and better structural performance.

The wood segment is expected to be the fastest-growing material category, with a projected CAGR of 7.93% during 2026–2031. This growth is driven by the rising preference for natural, durable, and sensory-rich construction play materials. Wooden construction toys offer a unique tactile experience through their texture, weight, and organic feel, fostering a stronger connection with hands-on building activities compared to synthetic alternatives. The segment's expansion is further supported by advancements in wood processing technologies, which enable smoother finishes, precise shaping, safer edges, and more detailed construction components while maintaining material strength. Wood's high durability and ability to endure long-term use make it ideal for repeated assembly, stacking, and creative building activities.

By End-User: Toddlers Anchor Volume, Teenagers Redefine Value

The toddlers segment maintained the largest end-user share at 38.95% in 2025, driven by the significant role of construction toys in fostering early-stage developmental learning and foundational skill-building. According to the Office for National Statistics (UK), the population of children aged 0 to 4 years reached 3.57 million in 2024, underscoring a substantial early childhood consumer base that supports demand for development-focused toys [2]Source: Office for National Statistics (UK), "Population of young children (aged 0-4) in the United Kingdom", ons.gov.uk. Construction toys for toddlers are increasingly popular due to their ability to promote sensory exploration, object recognition, shape identification, color learning, and basic problem-solving during critical growth stages. Features such as larger, easy-to-handle pieces with rounded edges, lightweight structures, and simple connection mechanisms make these toys suitable for early learners, while also enhancing grip strength and hand coordination.

The teenagers segment is expected to be the fastest-growing end-user category, with a projected CAGR of 7.31% through 2031. This growth is driven by increasing demand for advanced, skill-oriented, and challenge-based construction experiences. Teenagers are showing greater interest in complex building systems that involve detailed assembly, mechanical functions, design precision, and problem-solving tasks, marking a shift from simple play to hobby-based creation. The segment’s expansion is further supported by rising interest in engineering concepts, robotics, coding integration, and project-based activities that enable users to experiment with functional designs and innovative structures. Construction toys for teenagers often feature higher difficulty levels, a wider variety of components, and longer completion times, providing a sense of accomplishment and encouraging sustained engagement.

By Distribution Channel: Supermarkets Hold Volume, Online Channels Capture Growth

The supermarkets and hypermarkets segment accounted for a significant 41.23% market share in 2025. This dominance is attributed to the strong influence of in-store product discovery, immediate purchase decisions, and high consumer interaction with construction toys prior to purchase. The segment benefits from dedicated toy sections, well-organized shelf arrangements, promotional displays, and seasonal merchandising strategies that enhance product visibility and encourage impulse buying. Physical retail formats enable consumers to assess key product attributes such as package size, design complexity, component variety, and age suitability, which are critical factors in construction toy selection. Additionally, the availability of diverse product ranges within a single retail environment facilitates easy comparison and supports purchases catering to varied user preferences and skill levels.

The online retail stores segment is anticipated to be the fastest-growing distribution channel, with a projected CAGR of 8.45% through 2031. This growth is driven by the increasing preference for digital toy discovery, convenient purchasing options, and access to a wider variety of construction toy collections. Online platforms allow consumers to explore an extensive range of building sets, compare complexity levels, review component details, and select products based on age suitability and skill requirements. Features such as detailed product descriptions, demonstration videos, user reviews, and build previews enhance purchase confidence, particularly for construction toys where design features and assembly experience are key considerations. Furthermore, digital channels cater to the demand for specialized and limited-edition construction sets, which may not be prominently available in physical retail stores.

Geography Analysis

North America accounted for a 34.33% share of the construction toy market in 2025, driven by the strong adoption of skill-based, educational, and advanced building toys. This growth is supported by well-established product quality and safety standards. The implementation of the ASTM F963-23 compliance mandate, effective in 2024, has enhanced safety requirements across the United States toy industry, emphasizing material testing, mechanical safety, and quality assurance processes [3]Source: Consumer Product Safety Commission, "Toy Safety Business Guidance", cpsc.gov. These stricter standards have encouraged the production of safer, higher-quality construction toys, benefiting manufacturers with established compliance capabilities. Additionally, the region’s growth is bolstered by demand for innovative building experiences, including complex model sets, engineering-focused designs, and collectible construction formats that promote longer engagement and repeat purchases.

Asia-Pacific is projected to be the fastest-growing region, with a CAGR of 7.96% through 2031. This growth is driven by increasing adoption of educational play concepts, STEM-focused learning approaches, and greater awareness of early childhood development through interactive toys. The rising availability of diverse construction toy formats through expanding retail networks and digital platforms has improved product accessibility across the region. The market is also benefiting from growing demand for creative learning tools, technology-integrated construction sets, and products that combine entertainment with practical skill development. Greater exposure to global toy trends and evolving preferences for structured, problem-solving activities are further accelerating the region’s growth outlook.

Europe continues to gain traction in the construction toy market, supported by a strong focus on sustainable materials, product safety, and learning-oriented play experiences. Demand for durable, eco-conscious, and high-quality construction toys is increasing as consumers prioritize long-lasting and responsibly designed products. South America and the Middle East and Africa are emerging markets for construction toys, driven by expanding toy accessibility, increasing adoption of international toy trends, the growth of organized retail channels, and rising interest in creative and educational play products. Improvements in product availability, digital purchasing channels, and broader awareness of the developmental benefits of construction toys are expected to support steady growth across these regions.

Competitive Landscape

The construction toy market is highly consolidated, dominated by key players such as The LEGO Group, Mattel, Inc., Spin Master Corp., Hasbro, Inc., and Bandai Namco Holdings Inc. These companies maintain strong market positions through extensive product portfolios, established brand recognition, and ongoing innovation. Leading manufacturers are expanding their product ranges by introducing more complex designs, interactive building experiences, and products that integrate creativity with learning. Significant investments in design capabilities, advanced manufacturing processes, and consumer engagement strategies enable these companies to sustain competitive advantages and foster customer loyalty.

Technology integration has become a critical competitive strategy, with companies developing construction toys that offer enhanced functionality, such as digital connectivity, robotics, coding elements, augmented experiences, and interactive features. Manufacturers are blending traditional hands-on building activities with modern digital experiences to boost engagement and extend product usage. Advances in precision engineering, modular designs, customization options, and sophisticated assembly systems are helping companies differentiate their offerings and meet the demand for more advanced construction experiences across diverse user groups.

Sustainability has emerged as a key focus area within the competitive landscape. Companies are increasingly adopting eco-friendly materials, recyclable components, bio-based plastics, and sustainable packaging solutions. Leading brands are investing in responsible sourcing practices and material innovation to minimize environmental impact while maintaining product durability and performance. Additionally, strategic partnerships, licensed collaborations, product launches, and the expansion of digital retail capabilities are shaping competition, enabling companies to strengthen their market presence and adapt to changing consumer expectations.

Construction Toy Industry Leaders

-

The LEGO Group

-

Mattel, Inc.

-

Spin Master Corp.

-

Hasbro, Inc.

-

Bandai Namco Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Legend of Toys, a direct-to-consumer toy startup, secured INR 21 crore in a pre-Series A funding round. The round saw participation from notable investors including Singularity Early Opportunities Fund, Veltis Capital, Enzia Ventures, DeVC, Atrium Angels, and Stride.

- April 2026: Funskool India Ltd. has unveiled Blazetrix, its latest toy range. The inaugural lineup features three unique construction-themed vehicles: Buzz Claw, Core Crush, and Iron Hook.

- January 2025: Jazwares has unveiled its latest construction toy brand, BLDR. With BLDR, children and collectors alike can engage in imaginative play, building, and creativity within the expansive BLDR constructable system.

Global Construction Toy Market Report Scope

Construction toys are playthings that allow children to build, create, and design objects. The construction toy market is segmented by product type, material, end-user, distribution channel, and geography. Based on product type, the market is segmented into bricks and blocks, tinker toy, model construction kits, and others. Based on material, the market is segmented into wood, polymer, metal, and others. Based on end-user, the market is segmented into toddlers, preschool, school age, and teenagers. Based on distribution channel, the market is segmented into supermarkets and hypermarkets, online retail stores, specialty toy stores, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecast have been done based on the value (in USD million).

| Bricks and Blocks |

| Tinker Toy |

| Model Construction Kits |

| Others |

| Wood |

| Polymer |

| Metal |

| Others |

| Toddlers |

| Preschool |

| School Age |

| Teenagers |

| Supermarkets and Hypermarkets |

| Online Retail Stores |

| Specialty Toy Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bricks and Blocks | |

| Tinker Toy | ||

| Model Construction Kits | ||

| Others | ||

| By Material | Wood | |

| Polymer | ||

| Metal | ||

| Others | ||

| By End-User | Toddlers | |

| Preschool | ||

| School Age | ||

| Teenagers | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Online Retail Stores | ||

| Specialty Toy Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the construction toy market by 2031?

The construction toy market is forecast to reach USD 17.13 billion by 2031, rising from USD 12.34 billion in 2026 at a 6.8% CAGR.

Which product category leads revenue in construction toys?

Bricks and blocks led the category with 57.21% share in 2025, supported by strong brand familiarity, broad theme coverage, and repeat purchase potential.

Which material type is growing the fastest in this category?

Wood is projected to record the fastest growth at 7.93% through 2031, helped by school demand and parent preference for non-plastic positioning.

Which buyer group matters most for current demand?

Toddlers were the largest end-user group in 2025 with 38.95% share, because early learning, safety, and gifting needs keep this segment steady in volume terms.

Page last updated on: