Soft Toys Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.88 Billion |

| Market Size (2031) | USD 22.12 Billion |

| Growth Rate (2025 - 2030) | 8.25% CAGR |

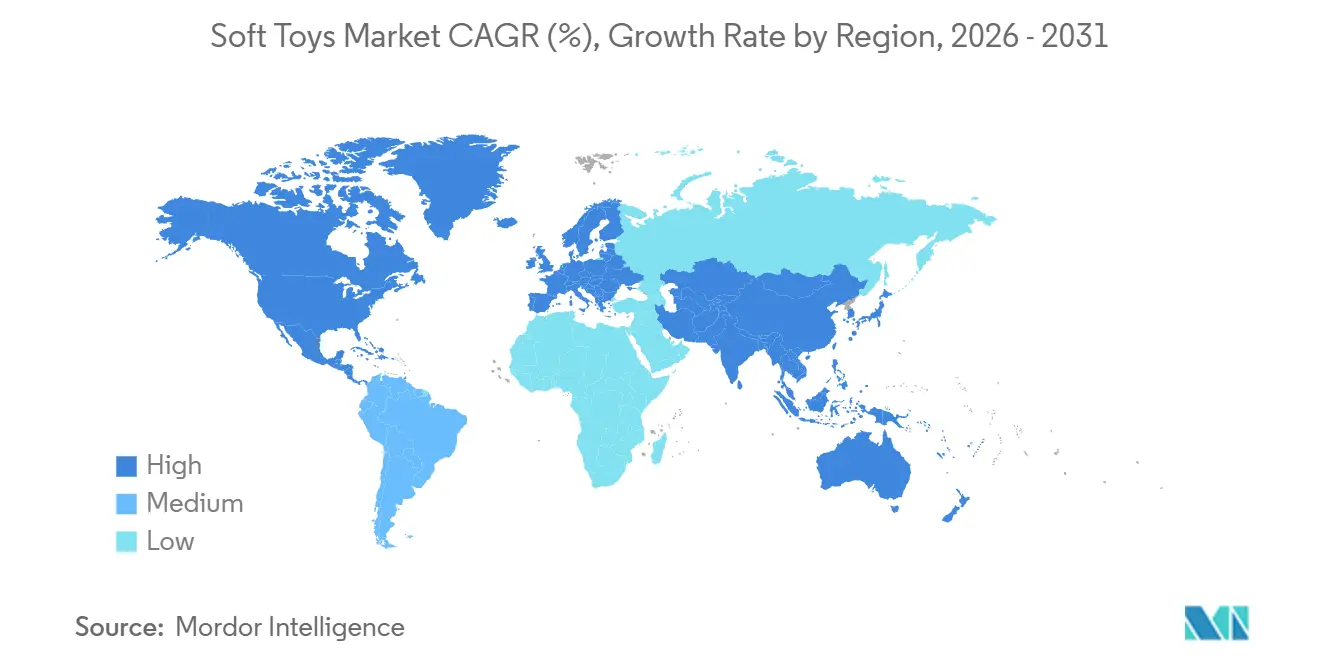

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

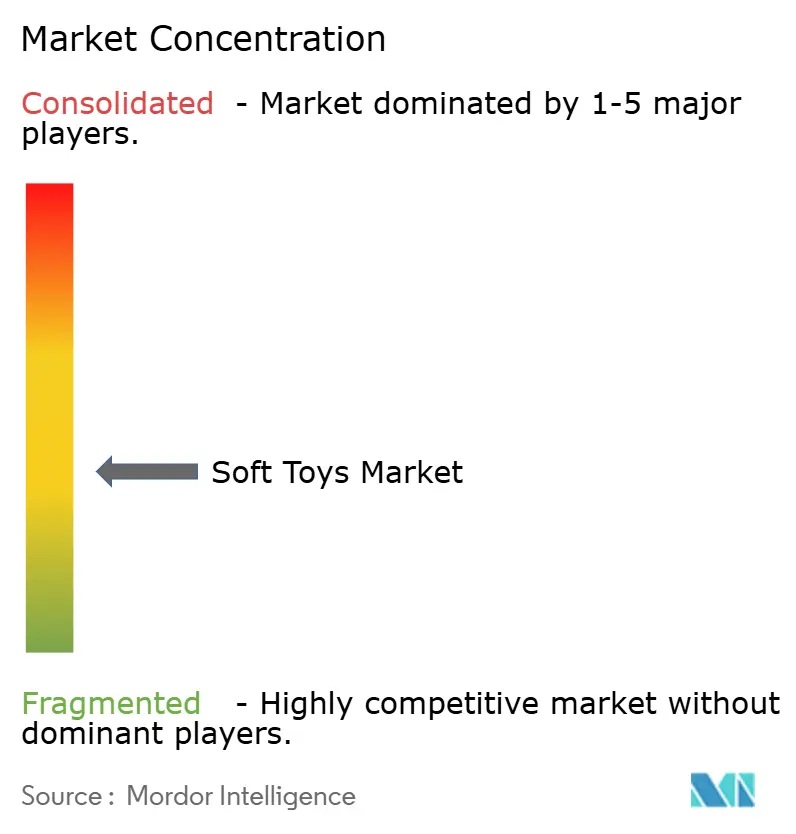

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soft Toys Market Analysis by Mordor Intelligence

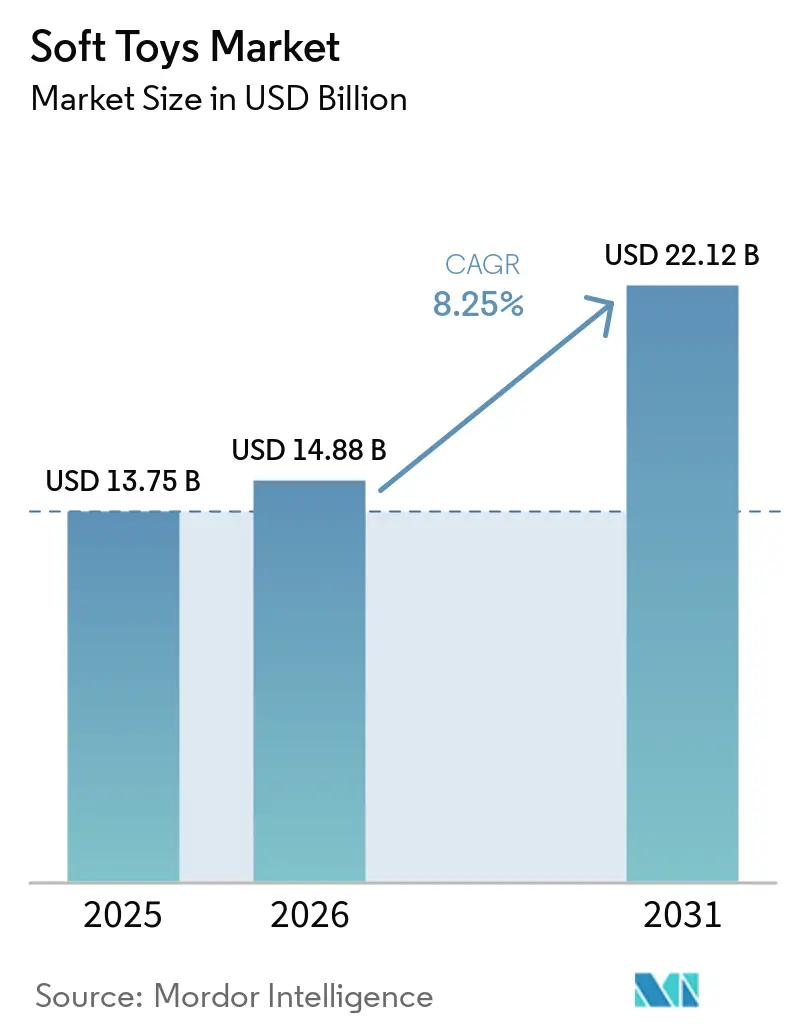

The soft toys market size was valued at USD 13.75 billion in 2025 and is estimated to grow from USD 14.88 billion in 2026 to reach USD 22.12 billion by 2031, at a CAGR of 8.25% during the forecast period (2026-2031). Licensed characters, interactive electronics, and eco-friendly materials are transforming product development strategies. Adults now represent a growing and influential segment of buyers, encouraging the launch of premium products priced above twenty-five dollars in the United States currency. At the same time, sustainability regulations in regions such as Europe and North America are driving a transition toward the adoption of recycled polyester and organic cotton in manufacturing processes. Furthermore, e-commerce flash sales, blind boxes, and product launches led by social media influencers are significantly increasing impulse purchasing behavior among consumers. However, the challenges of counterfeiting and the implementation of stricter safety regulations continue to create substantial cost burdens, particularly for smaller brands that do not have access to in-house testing facilities.

Key Report Takeaways

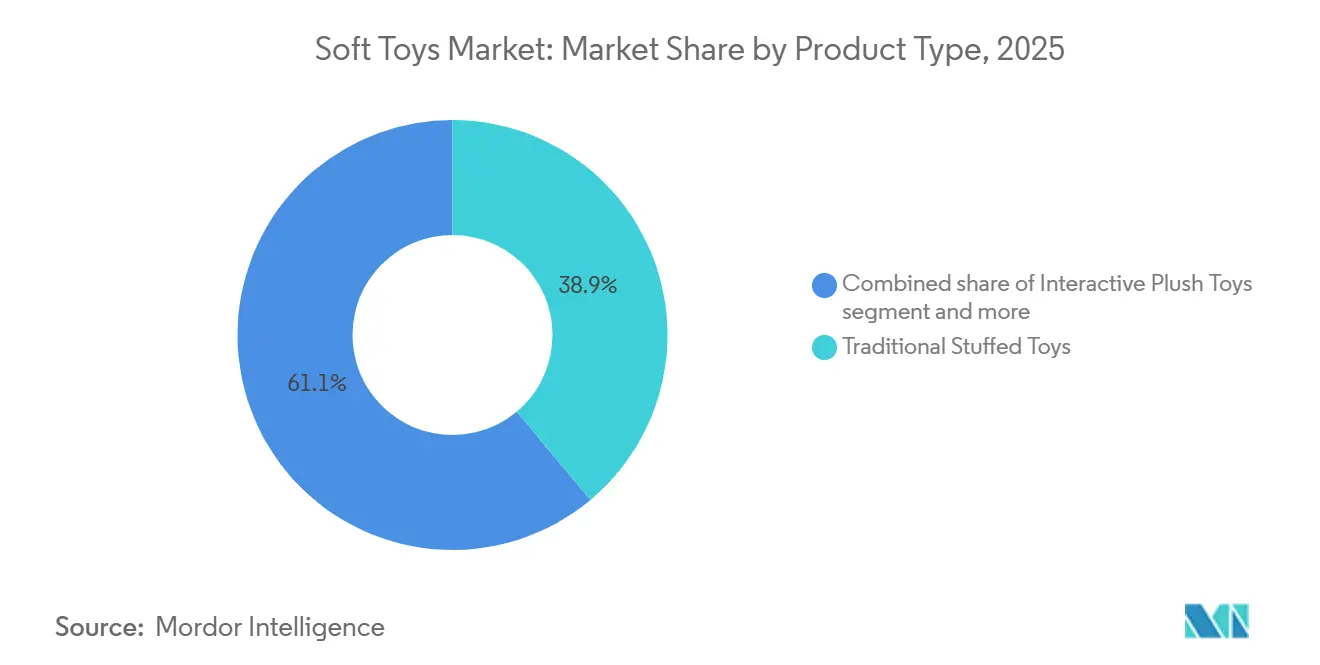

- By product type, traditional stuffed toys held 38.91% of 2025 revenue, while interactive plush is advancing at a 9.82% CAGR through 2031.

- By age, the 0-3 years cohort commanded 37.02% of 2025 demand; the 3-6 years segment is projected to expand at a 9.77% CAGR over 2026-2031.

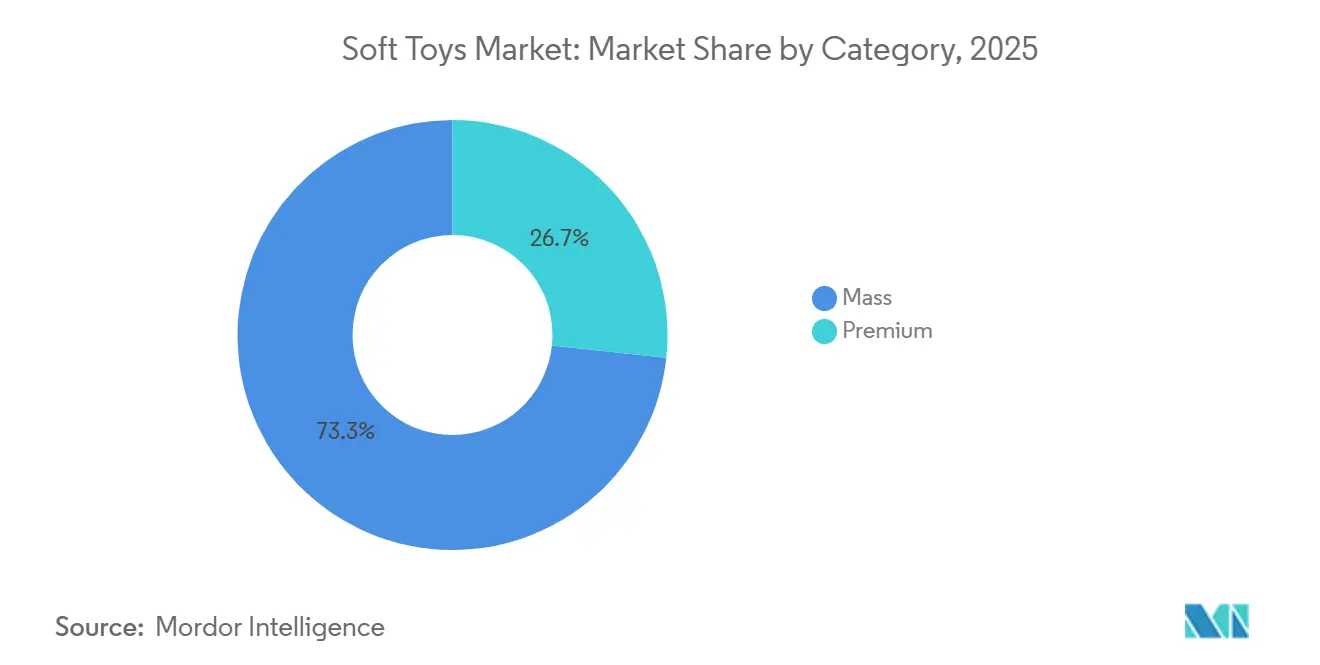

- By category, mass products captured 73.32% of 2025 sales, yet premium lines are forecast to grow at a 10.21% CAGR.

- By distribution channel, specialty stores accounted for 33.22% of 2025 turnover, whereas online retail is rising at a 10.66% CAGR.

- By geography, North America led with 33.73% of 2025 revenue, while Asia-Pacific is set to record the fastest 10.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soft Toys Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Popularity of licensed characters from movies, TV, and games boosting demand for themed plush | +1.8% | Global, with North America and Asia-Pacific leading | Medium term (2-4 years) |

| Demand for educational plush toys supporting cognitive, sensory, and emotional development | +1.2% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Interactive features like AI, voice recognition, and sensors in screen-free phygital toys | +1.5% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Sustainability push using eco-friendly materials such as recycled polyester and organic cotton | +1.0% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Personalization through customizable and on-demand manufacturing options | +0.9% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| E-commerce growth enabling wider access, blind boxes, and limited-edition drops | +1.4% | Global, with Asia-Pacific and North America leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Popularity of licensed characters from movies, TV, and games boosting demand for themed plush

Hasbro renewed its multi-year partnership with Disney in April 2025, securing the rights to produce Star Wars and Marvel plush products, including the Spidey and His Amazing Friends preschool lines. In 2024, Jazwares signed agreements with 125 licensees for Squishmallows and added the FIFA World Cup 2026 to its portfolio. Licensed products are increasingly aligned with theatrical releases to optimize cross-platform revenue. For example, Grogu plush variants from The Mandalorian franchise are priced between USD 32.99 and USD 54.99, illustrating how strong character recognition enables manufacturers to command premium pricing, even in mass-market channels. Disney's 2026 strategy aims to engage 500 licensees and incorporate tech-enabled experiences ahead of the release of Frozen 3 in 2027. This approach highlights how intellectual property holders are leveraging plush products as ongoing revenue streams rather than one-time merchandising opportunities. The growing focus on licensing is consolidating market power among companies with strong studio relationships, leaving independent brands to differentiate themselves through design innovation rather than franchise recognition.

Demand for educational plush toys supporting cognitive, sensory, and emotional development

Therapeutic weighted plush toys, such as those offered by brands like Turbobo, are increasingly used in schools to support sensory regulation for children with autism spectrum disorder. This shift reflects a move from traditional comfort toys to evidence-based developmental tools. Montessori-aligned plush toys emphasize hands-on learning through tactile interaction, while Science, Technology, Engineering, and Mathematics (STEM)-themed products, like the Mary Jackson Interactive Plush, incorporate historical narratives for preschool-aged children. Parents are placing greater importance on cognitive benefits, often prioritizing educational value when selecting toys [1]Source: The Toy Association, “Toy Fair® Brings The Love And Top Toy Trends For 2026,” toyassociation.org. This rising demand is prompting manufacturers to collaborate with child psychologists and occupational therapists during the product development process. The infant-to-toddler age group is particularly responsive to developmental claims, as caregivers seek products that enhance fine motor skills and emotional recognition. However, the educational plush toy segment faces challenges due to exaggerated claims, as regulatory bodies such as the Federal Trade Commission have yet to establish standardized testing protocols to validate cognitive benefit assertions.

Interactive features like AI, voice recognition, and sensors in screen-free phygital toys

China's artificial intelligence toy market is witnessing significant growth, driven by products such as the Ebloma Artificial Intelligence Bear and Toypals Generative Pre-trained Transformer-4 Bear, which incorporate features like voice recognition and emotion sensing. FoloToy has shipped a substantial number of units, while Haivivi's BubblePal has scaled production to a significant volume per month by early 2025, reflecting rapid adoption among tech-savvy parents seeking screen-free alternatives. However, manufacturers report high return rates and a common "two-week wall," where children lose interest after the initial novelty fades. This highlights a challenge in balancing technological complexity with sustained engagement. Interactive plush toys are projected to grow at a steady compound annual growth rate through the next decade. However, this growth depends on addressing key issues such as battery life limitations, app connectivity challenges, and multilingual accuracy, which currently restrict adoption outside English-speaking markets. The long-term success of this segment will rely on manufacturers shifting from gimmick-based features to creating adaptive play experiences that align with a child's developmental needs over time.

Sustainability push using eco-friendly materials such as recycled polyester and organic cotton

Most stuffed toy companies now use recycled polyester for cushioning, while a considerable number of manufacturers incorporate recycled plastic in a portion of their product lines. This shift highlights both consumer preferences and regulatory requirements. Bon Ton Toys has transitioned to fully recycled filling, and Franck and Fischer's Pure Earth Collection utilizes organic cotton certified under the Global Organic Textile Standard and OEKO-TEX frameworks. Additionally, an increasing number of consumers are willing to pay extra for eco-friendly toys, and many parents emphasize sustainability even if it leads to higher costs. Mattel has pledged to use entirely recycled, recyclable, or bio-based materials by the year 2030. Moreover, a significant share of leading toy brands has implemented take-back programs, collectively recovering large quantities of plastic in 2023. However, regulatory challenges remain, as certain states in the United States, such as Massachusetts and Ohio, restrict the use of recycled materials in plush toys due to contamination concerns. This regulatory inconsistency complicates global supply chains and requires manufacturers to maintain separate production lines for different markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent safety regulations requiring rigorous testing and certifications | -0.8% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Proliferation of counterfeit products eroding trust and posing safety risks | -0.6% | Global, with Asia-Pacific and Europe most affected | Short term (≤ 2 years) |

| Supply chain disruptions affecting raw material availability and delivery | -0.5% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Environmental concerns over plastic-derived synthetics and non-biodegradable waste | -0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent safety regulations requiring rigorous testing and certifications

The European Committee for Standardization published EN71-1:2026 in February 2026, introducing new requirements for food-imitating toys, materials, ventilation, neck straps, and glued components, which require manufacturers to redesign existing product lines. In the United States, the American Society for Testing and Materials (ASTM) F963-23 became mandatory on April 20, 2024, tightening regulations on phthalate limits, battery accessibility, and heavy metal thresholds. Furthermore, the Consumer Product Safety Commission's water beads rule, effective March 12, 2026, enforces a 5.0mm funnel test and a 325-microgram acrylamide limit [2]Source: United States Consumer Product Safety Commission, “Toy Safety Business Guidance,” cpsc.gov. Testing costs for simple plush toys range from USD 250 to USD 450 per sample, with a turnaround time of 5-7 days. Third-party certification requirements add administrative overhead, which disproportionately affects small manufacturers. The Consumer Product Safety Commission issued 498 Notices of Violation through June 2025, with 89% targeting Chinese exporters, highlighting increased enforcement alongside growing regulatory complexity. Compliance frameworks such as International Organization for Standardization (ISO) 8124, OEKO-TEX, and the Global Recycled Standard are becoming de facto market entry barriers. These frameworks are concentrating production among vertically integrated firms capable of investing in testing infrastructure, while smaller, artisanal producers face challenges due to limited capital for laboratory partnerships.

Proliferation of counterfeit products eroding trust and posing safety risks

Counterfeit toys continue to pose a significant challenge globally. In the European Union, authorities seized 16.6 million packages valued at EUR 36.8 million during enforcement sweeps [3]Source: Organisation for Economic Co-operation and Development, “Global Trade in Fake Goods,” oecd.org. Similarly, in the United Kingdom, authorities confiscated 259,812 toys worth approximately GBP 3.5 million between January and August 2025, with 90% of these being fake Labubu dolls that failed flammability and choking hazard tests. In the United States, Customs and Border Protection seized counterfeit goods worth USD 776,562 in Norfolk alone, including 12,191 plush toys. Furthermore, 75% of seized counterfeit products failed safety tests, and 46% of consumers who purchased fake products reported safety-related issues. China remains the leading source of counterfeit goods, accounting for 45% of global seizures. The increasing prevalence of cross-border electronic commerce (e-commerce) platforms has enabled counterfeiters to exploit jurisdictional gaps and platform anonymity. Intellectual property enforcement remains fragmented, requiring brand owners to pursue legal actions across multiple jurisdictions. The reputational damage caused by a single counterfeit-related injury can undermine years of brand-building efforts, particularly for premium brands like Jellycat, which rely heavily on perceived quality differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Interactive Plush Outpaces Legacy Categories

Interactive plush toys are expected to grow at a compound annual growth rate (CAGR) of 9.82 percent through 2031. This growth is primarily driven by the integration of artificial intelligence (AI) and voice recognition features, which provide screen-free, physical-digital (phygital) experiences. However, traditional stuffed toys are projected to account for 38.91 percent of the market share in 2025, mainly due to their affordability and widespread appeal across various age groups. In China, the artificial intelligence toy market includes products such as VTech's Cora Smart Cub and Toypals' Generative Pre-trained Transformer 4 (GPT-4) Bear, which offer features like emotion sensing and app connectivity. Despite these advancements, manufacturers report return rates of 30 percent to 40 percent, as the novelty effect often diminishes within two weeks.

Traditional stuffed toys remain a dominant segment in the market due to their simplicity and practicality. These toys do not require batteries and pose minimal choking hazards for infants, making them a popular choice for impulse gifting. However, growth in this segment is slowing as parents increasingly favor toys with educational and interactive features. In contrast, interactive plush toys face challenges such as limited battery life, multilingual accuracy issues, and app connectivity problems, which hinder their adoption in non-English-speaking markets.

By Age: Early Childhood Dominates, Preschool Accelerates

The 0-3 years segment accounted for 37.02% of the market share in 2025, driven by pediatric development research that emphasizes the connection between tactile play and cognitive milestones. Additionally, there is a growing parental demand for sensory toys designed to enhance fine motor skills in young children. The 3-6 years segment is projected to grow at a compound annual growth rate (CAGR) of 9.77%, supported by the increasing popularity of educational plush toys aligned with Science, Technology, Engineering, and Mathematics (STEM) principles, as well as Montessori-inspired products. Therapeutic weighted plush toys from Turbobo are being utilized in over 350 schools to assist with sensory regulation for children diagnosed with autism spectrum disorder. This trend highlights a significant shift in the 0-3 years segment, moving from traditional comfort toys to tools that are backed by evidence and designed to support developmental milestones.

The 6-12 years segment is encountering competition from digital entertainment platforms and video games. However, collectible plush toys such as Squishmallows, which achieved sales of 485 million units in 2024, continue to maintain their relevance. These products tap into social dynamics where ownership of such items signifies belonging to a peer group. Among adults, 81% of parents included toys for themselves in their holiday shopping lists in 2025. This shift in consumer behavior is compelling manufacturers to rethink their strategies, including redesigning packaging, refining messaging, and adjusting distribution approaches to effectively cater to adult consumers without presenting the products in a way that feels infantilizing.

By Category: Premium Segment Captures Collector Premiums

The mass category accounted for 73.32% of the 2025 market share, catering to price-sensitive parents and impulse gifting occasions. However, the premium segment is growing at a compound annual growth rate (CAGR) of 10.21% through 2031, driven by adult collectors, nostalgia-driven buyers, and affluent parents who value design sophistication and limited-edition exclusivity. Jellycat reported increased revenue, with United States sales rising in the first half of 2024. This highlights that premium positioning can deliver significant profit margins when combined with direct-to-consumer distribution strategies and influencer marketing campaigns. Build-A-Bear Workshop announced a substantial increase in the share of adult online sales, with total fiscal revenue nearing half a billion dollars. This demonstrates how experiential retail and personalized offerings can sustain premium pricing even in highly competitive markets. Rare Labubu editions were auctioned for significant amounts in Beijing during 2025, while retired Jellycat designs are being sold for hundreds of dollars on secondary markets. This has fostered a resale economy that enhances perceived value and creates urgency for initial purchases.

Mass-market products rely on volume-driven economics and retail partnerships with supermarkets and hypermarkets, where shelf space allocation depends on rapid inventory turnover and promotional support. However, this model is encountering challenges as e-commerce redirects consumer traffic toward specialty stores and direct-to-consumer channels that prioritize curation over product variety. Premium brands are increasingly utilizing social media platforms such as Instagram and TikTok to promote aspirational lifestyles associated with plush ownership. Notably, a significant portion of Generation Z consumers uses toys as a form of therapy, with many willing to spend over twenty-five dollars per item. This indicates that positioning products around emotional wellness can enhance pricing power and consumer appeal.

By Distribution Channel: Online Retail Disrupts Specialty Dominance

Specialty stores accounted for 33.22% of the distribution share in 2025, driven by curated product assortments and knowledgeable staff who assist parents in selecting age-appropriate and educational items. However, online retail channels are expanding at a compound annual growth rate (CAGR) of 10.66% through 2031. Platforms such as TikTok Shop, Amazon, and direct-to-consumer websites are facilitating discovery-led commerce and blind-box drops, effectively converting impulse buyers within seconds. TikTok Shop's algorithm prioritizes sales-oriented content and visual demonstrations, with products priced between EUR 15 and EUR 30 achieving the highest conversion rates.

Additionally, an eco-friendly toy startup tripled its international customer base within six months by utilizing influencer partnerships that bypass traditional retail gatekeepers. While supermarkets and hypermarkets cater to convenience-driven purchases and last-minute gifting needs, their market share is declining as consumers increasingly favor online channels offering broader selections, user reviews, and doorstep delivery. Other distribution channels, such as pop-up stores and experiential retail concepts like Build-A-Bear workshops, differentiate themselves through customization and entertainment value, though their geographic reach remains limited compared to digital platforms.

Geography Analysis

North America captured 33.73% of the 2025 market share, supported by a strong gifting culture, high disposable incomes, and a well-established specialty retail infrastructure that enables premium product positioning. Build-A-Bear reported a significant increase in adult online sales share, rising from under 20% to 40%, while Jellycat's United States sales grew by 41% in the first half of 2024. These trends highlight the growing influence of the "kidult" segment, which is driving growth beyond traditional pediatric demographics. The United States Consumer Product Safety Commission (CPSC) issued 498 Notices of Violation through June 2025, with 89% targeting Chinese exporters. This reflects stricter regulatory enforcement, creating compliance challenges that favor manufacturers with domestic integration.

The Asia-Pacific market is projected to grow at a compound annual growth rate (CAGR) of 10.32% through 2031, driven by rising middle-class incomes in China, India, and Southeast Asia, along with manufacturing cost advantages that enable competitive export pricing. The increasing popularity of blind-box collectibles, such as Labubu, which contributed over 18% of Pop Mart's global blind-box revenue in 2025, is further fueling growth. India's market, while still developing, is gaining momentum as urbanization and the rise of nuclear families boost demand for developmental toys. Additionally, countries like Indonesia, Thailand, and Vietnam are emerging as key manufacturing hubs, offering cost-effective production capacity for global brands.

Europe is balancing strict sustainability mandates with premium consumer preferences. Parents are increasingly opting for eco-friendly toys, while the European Committee for Standardization (CEN) introduced EN71-1:2026 in February 2026. This regulation enforces new requirements for food-imitating toys and glued components, prompting manufacturers to redesign existing product lines. Germany, the United Kingdom, France, and the Netherlands lead in per-capita toy spending, with specialty retailers and department stores focusing on curated assortments that highlight certifications such as the Global Organic Textile Standard (GOTS) and OEKO-TEX for organic cotton and recycled polyester products. On the other hand, Southern European markets like Italy, Spain, and Poland show higher price sensitivity, favoring mass-market products. However, growth in these regions is limited by lower birth rates and economic challenges that reduce discretionary spending. The European Union's Green Claims Directive requires scientific evidence to substantiate environmental marketing claims, raising the bar for sustainability standards and exposing companies engaging in greenwashing to regulatory penalties.

Competitive Landscape

The global soft toys market is moderately fragmented, with no single player holding a dominant share. The market features a mix of regional specialists, licensed-product manufacturers, and premium direct-to-consumer brands operating across overlapping price tiers and distribution channels. In April 2025, Hasbro extended its partnership with Disney to retain the plush rights for Star Wars and Marvel, while Mattel acquired the global Teenage Mutant Ninja Turtles toy license in February 2026 for a 2027 launch. These developments highlight the importance of intellectual property control as a key competitive factor for major players. Jazwares sold 485 million Squishmallows units in 2024 and secured 125 licensing agreements, including partnerships with Fédération Internationale de Football Association (FIFA) World Cup 2026 and Netflix's KPop Demon Hunters, leveraging licensing to drive cross-category revenue streams.

Smaller disruptors, such as Jellycat, which reported GBP 333 million in revenue in 2024, are bypassing traditional retail channels through direct-to-consumer models and influencer marketing. These strategies help cultivate aspirational lifestyles centered around premium plush ownership. Additionally, white-space opportunities exist in therapeutic plush for special-needs education. For example, Turbobo's weighted plush products are used in over 350 schools but remain under-marketed to occupational therapists and pediatric clinics.

Customization platforms like Budsies and Bespoke Plush enable small businesses and influencers to create branded merchandise without requiring significant inventory investments. However, their combined market share remains minimal compared to mass-market leaders, indicating that personalization is still a niche segment rather than a mainstream category. Technology adoption is also creating a divide in the market. Vertically integrated firms like Mattel and Hasbro are investing in proprietary electronics for interactive plush toys, while smaller brands focus on design differentiation within traditional categories. This divergence is concentrating research and development spending among larger firms, which can absorb 30 to 40 percent return rates during product iteration cycles.

Soft Toys Industry Leaders

Mattel Inc.

Hasbro Inc.

Ty Inc.

Jazwares LLC

Spin Master Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: LEGO Group invested USD 366 million to build a 2,000,000-square-foot warehouse at the Crosspointe Business Centre site in Prince George's County. Furthermore, a 1.7 million-square-foot facility at Meadowville Technology Park is planned to open in 2027.

- May 2025: Ultra Soft Toys introduced its exclusive Mother’s Day collection, designed to provide comfort and emotional support for expectant and new mothers. Launched in time for Mother’s Day celebrations, this carefully curated range includes oversized, ultra-soft plush toys aimed at offering relaxation, joy, and reassurance to women navigating the journey of motherhood.

- February 2025: Hasbro and Mattel introduced a collaborative PLAY-DOH Barbie line, merging Play-Doh's creative play elements with Barbie's well-known fashion themes. The collection includes playsets and tools designed for creating and designing Barbie outfits using Play-Doh compound.

Global Soft Toys Market Report Scope

The soft toys market refers to plush, fabric-based stuffed toys such as teddy bears, dolls, animals, and character figures. These toys are filled with soft materials like polyester or cotton and are primarily designed for children. They aim to foster emotional bonding, enhance sensory development, and encourage imaginative play through activities such as cuddling and role-playing. The market is segmented by product type, including cartoon toys, traditional stuffed toys, interactive plush toys, and other product types; by age group, covering 0 to 3 years, 3 to 6 years, 6 to 12 years, and 12 years and above; by category, divided into mass and premium; by distribution channel, which includes supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels; and by geography, encompassing North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Cartoon Toys |

| Traditional Stuffed Toys |

| Interactive Plush Toys |

| Other Product Types |

| 0–3 Years |

| 3–6 Years |

| 6–12 Years |

| 12+ Years |

| Mass |

| Premium |

| Supermarkets and Hypermarkets |

| Speciality Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cartoon Toys | |

| Traditional Stuffed Toys | ||

| Interactive Plush Toys | ||

| Other Product Types | ||

| By Age | 0–3 Years | |

| 3–6 Years | ||

| 6–12 Years | ||

| 12+ Years | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Speciality Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the soft toys market?

The soft toys market size stood at USD 13.75 billion in 2025 and is forecast to reach USD 22.12 billion by 2031.

How fast is online retail growing within soft-toy sales?

Online channels are expanding at a 10.66% CAGR, driven by influencer-led flash sales and blind-box drops.

Which product type is growing the quickest?

Interactive plush, featuring AI and sensor arrays, is advancing at a 9.82% CAGR through 2031.

Why are premium plush lines gaining traction?

Adult collectors and nostalgia buyers support a 10.21% CAGR for premium plush, with limited editions often reselling above MSRP.

Which region will lead future growth?

Asia-Pacific is projected to post the fastest regional CAGR at 10.32% through 2031, thanks to rising disposable incomes and strong demand for blind-box collectibles.

Page last updated on: