Educational Toys Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 78.48 Billion |

| Market Size (2031) | USD 118.08 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

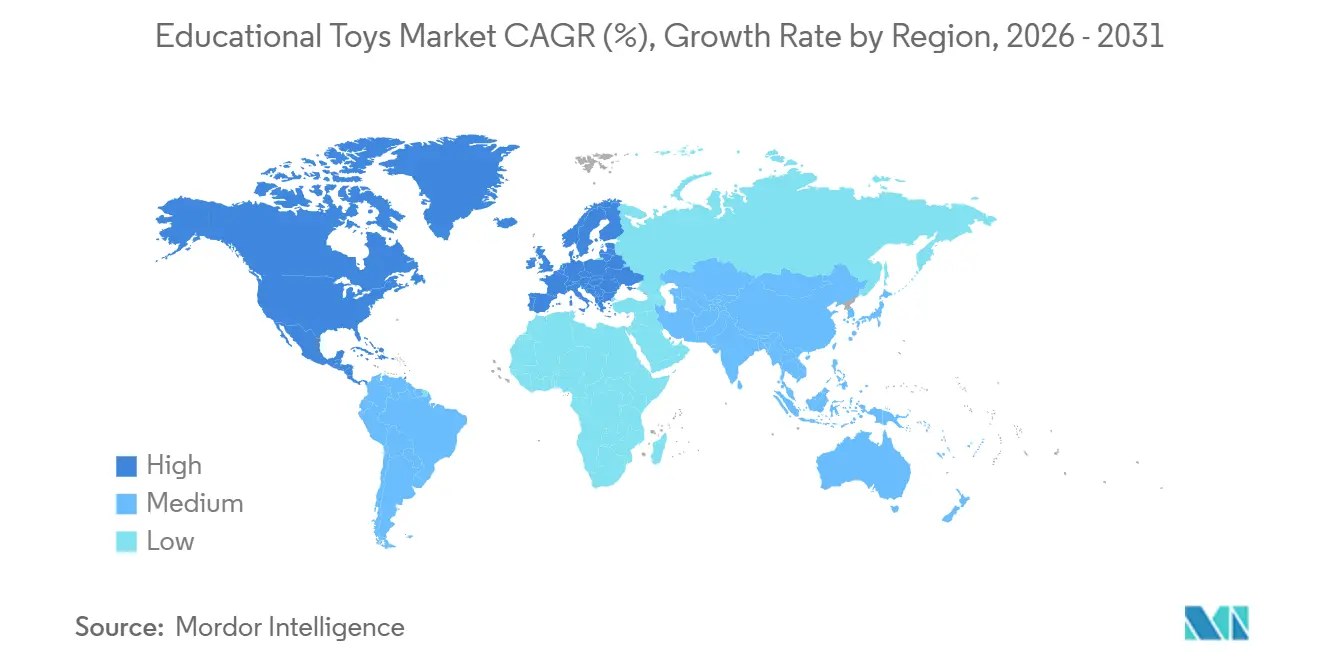

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

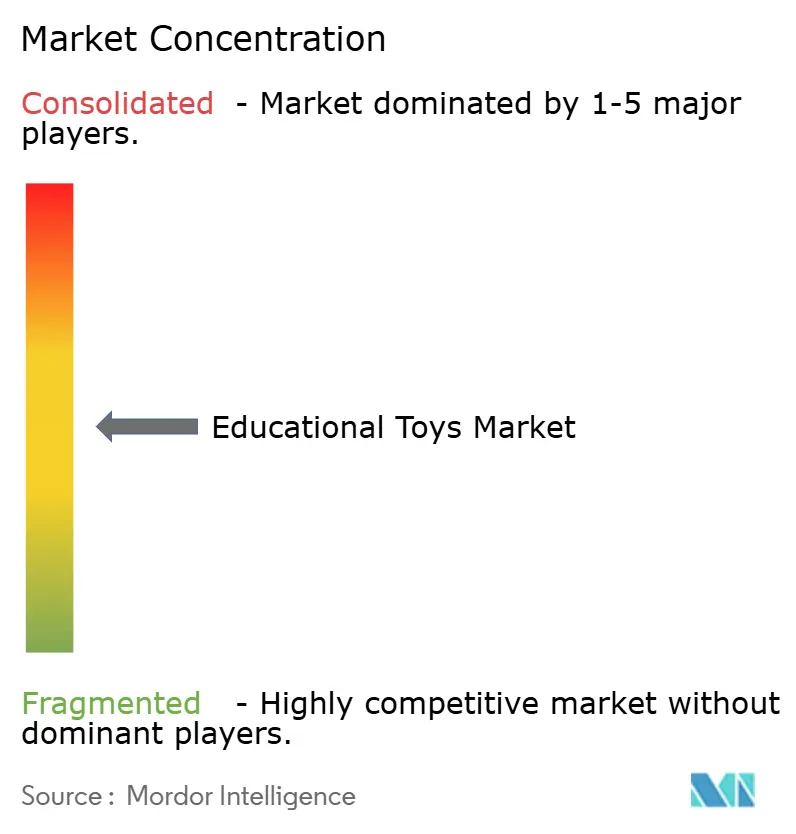

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Educational Toys Market Analysis by Mordor Intelligence

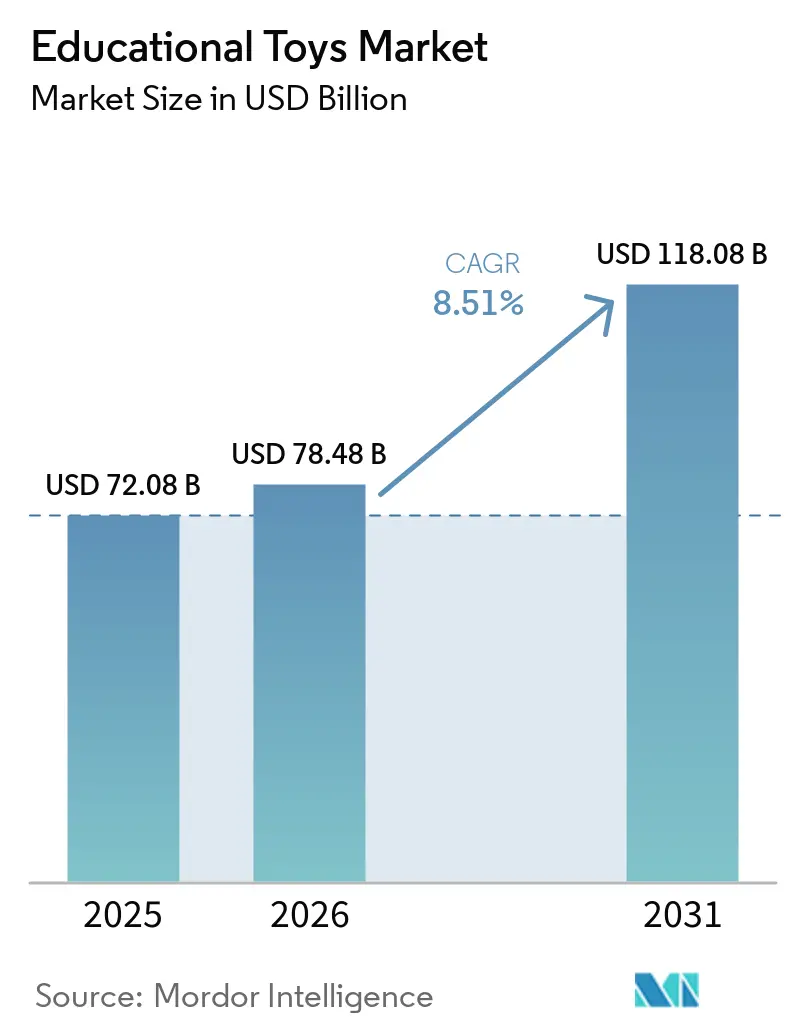

The educational toys market size is expected to grow from USD 72.08 billion in 2025 to USD 78.48 billion in 2026 and is forecast to reach USD 118.08 billion by 2031 at 8.51% CAGR over 2026-2031. Demand in the educational toys market is increasing as caregivers prioritize products that actively support the development of cognitive, motor, and socio-emotional skills, moving away from passive entertainment toward evidence-based play experiences. Advances in large-scale neuroimaging have established connections between early brain development, from infancy to preschool, and later reading proficiency. This has led manufacturers to design products aligned with critical developmental stages rather than broad age categories. Institutional purchasing in the educational toys market is also driving growth, with schools incorporating coding, robotics, and social-emotional learning into curricula and acquiring toys equipped with pre-designed lessons, teacher dashboards, and tools for tracking outcomes.

Key Report Takeaways

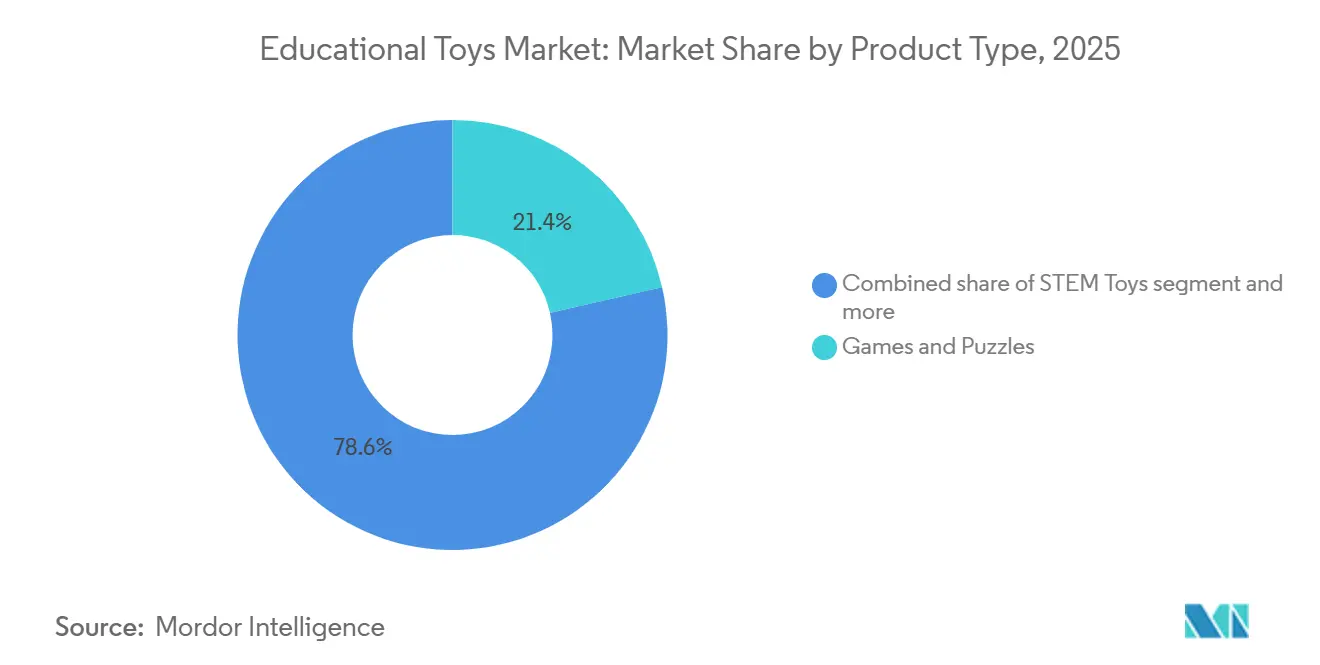

- By product type, Games and Puzzles led with 21.43% of the educational toys market share in 2025, whereas STEM Toys are forecast to expand at an 9.92% CAGR through 2031.

- By technology integration, Non-Electronic Traditional Toys commanded 56.11% of the educational toys market size in 2025, while Smart Toys with AI and IoT are projected to register an 11.43% CAGR to 2031.

- By age group, the 5-8 Years cohort held 55.13% of the educational toys market size in 2025; the 0-4 Years segment will advance at an 11.12% CAGR over 2026-2031.

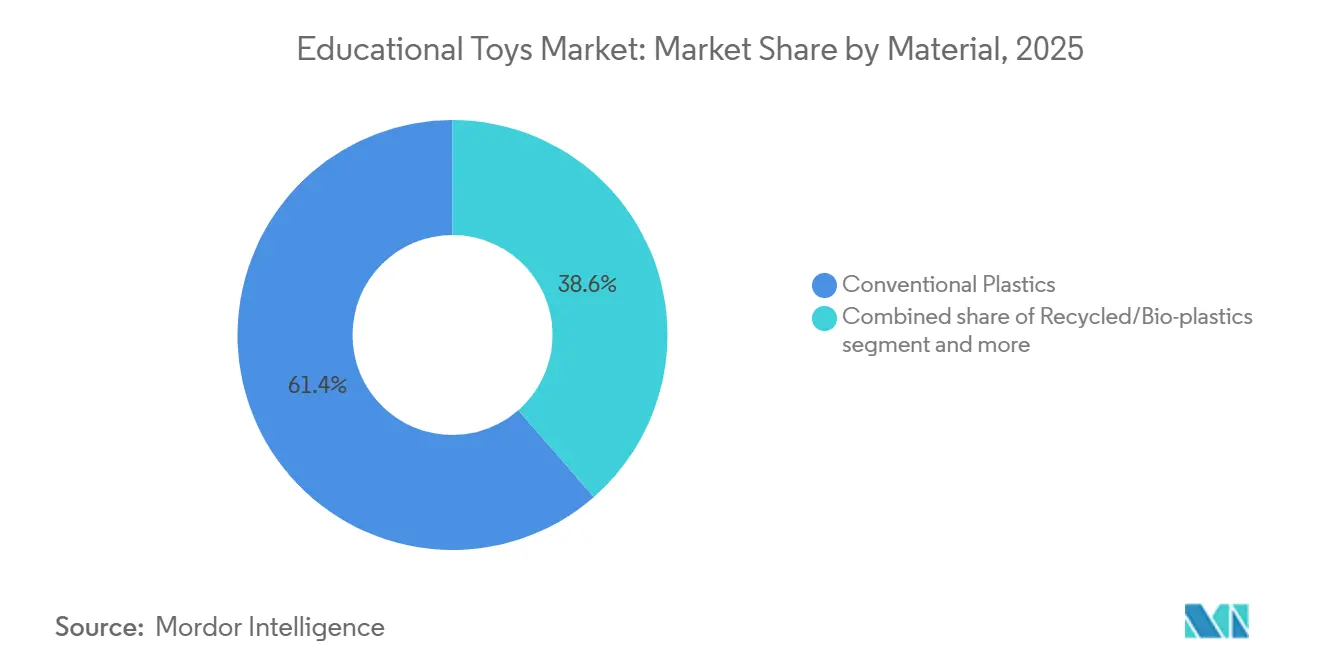

- By material, Conventional Plastics captured 61.43% of educational toys market share in 2025, with Recycled and Bio-plastics expected to grow at a 12.02% CAGR.

- By distribution channel, Supermarkets and Hypermarkets accounted for 28.33% of the educational toys market size in 2025; Online Retail Stores are poised to post a 12.41% CAGR to 2031.

- By geography, Europe led with 37.82% revenue share in 2025, whereas Asia-Pacific is forecast to log the fastest regional CAGR at 11.71% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Educational Toys Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of early childhood brain development and neuroplasticity | +1.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Growing emphasis on STEM/STEAM education in schools and curricula | +2.1% | Global, Asia-Pacific core with spillover to North America and Europe | Long term (≥ 4 years) |

| Expansion of digital-integrated learning driving hybrid educational toys | +1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Increasing focus on social-emotional learning (SEL) and emotional intelligence in kids | +1.2% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Strong push for inclusive and special-needs-oriented toys | +0.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Certification and endorsement of toys by educators, psychologists, and pediatricians boosting credibility | +1.0% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising awareness of early childhood brain development and neuroplasticity

Longitudinal neuroimaging studies in the educational toys market have significantly influenced product development timelines and marketing strategies. Research conducted in 2025 demonstrated that individual differences in brain trajectory features such as volumetric measures, cortical surface measures, and white-matter measures from infancy to school age directly predicted preschool phonological processing [1]Source: Proceedings of the National Academy of Sciences, “Longitudinal Trajectories of Brain Development from Infancy to School Age and Their Relationship with Literacy Development,” pnas.org. This, in turn, mediated early elementary decoding and word reading. This causal relationship supports the commercial focus on toys targeting the 0-4 age group, a period when the neural substrates of literacy are most adaptable. In the educational toys market, manufacturers are addressing this by incorporating developmental milestones into product labeling and collaborating with pediatric associations to validate their claims. Additionally, the neurobiology of play has been extensively studied. Rodent models indicate that play activates the prefrontal cortex, amygdala, striatum, and ascending dopamine and opioid systems, with neonatal tactile handling enhancing later play motivation. Applying these findings, companies are developing toys that encourage caregiver-mediated playful interactions, sensorimotor exploration, and symbolic play scenarios, features that have been shown to support motor, language, and executive function development across various age groups.

Growing emphasis on STEM/STEAM education in schools and curricula

Curriculum integration in the educational toys market has shifted from being aspirational to a requirement in many jurisdictions, creating a stable institutional market. In 2026, LEGO Education introduced its Computer Science and Artificial Intelligence Kit for grades 6-8. The kit includes 30 standards-aligned lessons across six units, featuring built-in formative assessments and a safe artificial intelligence design that ensures all processing occurs locally without collecting student data. Its institutional adoption model bypasses traditional retail channels and enables multi-year purchasing agreements. The kit combines hands-on LEGO construction with a Coding Canvas application and an optional Python package, addressing the challenge of balancing age-appropriate content with sufficient complexity to maintain student engagement as their skills develop. Schools are increasingly prioritizing vendors that offer teacher training, lesson libraries, and progress-tracking dashboards, effectively delegating curriculum development to educational product providers.

Expansion of digital-integrated learning driving hybrid educational toys

In the educational toys market, hybrid toys that combine physical interaction with digital feedback are gaining market share from both traditional analog toys and screen-based products. LEGO's SMART Play platform, introduced at the Consumer Electronics Show (CES) in January 2026, integrates custom chips smaller than a standard LEGO stud into traditional LEGO bricks. These chips include sensors, accelerometers, light and sound detectors, and miniature speakers, enabling real-time responsive behaviors without the need for screens. The initial release features three Star Wars-themed sets, incorporating SMART Bricks, Tags, and Minifigures that generate context-aware sounds such as engine roars, lightsaber hums, and The Imperial March based on physical play actions. This innovation addresses parental concerns about excessive screen time while meeting children's expectations for interactive play experiences. Studies indicate that engaging with real, multifunctional toys reduces screen-time-related behavioral issues more effectively than developing executive function skills. Hybrid toys leverage this finding by providing novelty and interactive feedback without fostering the passive consumption habits associated with digital apps.

Increasing focus on social-emotional learning (SEL) and emotional intelligence in kids

Social and Emotional Learning (SEL) competencies, such as emotion recognition, social skills, and self-regulation, are increasingly being integrated into early childhood curricula, driving demand for toys designed to support these skills. Manufacturers are incorporating these insights into product features, including cooperative building sets that encourage turn-taking, role-play toys that simulate social scenarios, and games with explicit emotion-labeling mechanics. The Battery for the Evaluation of Learning and Development in Infancy (BELADI) play-based assessment battery, validated in Spain in 2024, has operationalized socioemotional dimensions such as social skills, aggressiveness, disconnection, and anxiety within playful contexts. This demonstrates that toys can function both as educational tools and as assessment instruments. This intersection of play and measurement creates opportunities for data-driven product development and evidence-based marketing strategies. However, it also raises concerns regarding privacy and ethical considerations related to behavioral tracking in young children.

Restrains Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulty in measuring and demonstrating tangible learning outcomes from educational toys | -0.8% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Safety and choking-hazard concerns leading to stricter parental filters on small-part toys | -1.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| High competition from free digital games and apps that offer similar educational claims | -1.5% | Global, most acute in North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Challenges in designing toys that are both age-appropriate and not too complex | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Difficulty in measuring and demonstrating tangible learning outcomes from educational toys

The lack of standardized and scalable assessment frameworks in the educational toys market hampers manufacturers' ability to validate educational claims and justify premium pricing. Although play-based assessment tools like BELADI (Behavioral and Emotional Learning Assessment for Development and Intervention) have shown acceptable psychometric properties with content validity coefficients ranging from 0.88 to 0.92 and internal consistency alphas between 0.76 and 0.89 across psychomotor, cognitive, and socioemotional domains, these tools are primarily limited to research settings and are not suitable for commercial product validation. A 2024 review of 157 studies on digital device usage and childhood cognitive development highlighted methodological inconsistencies, varied outcome measures, and mixed neuroimaging results, making it difficult to establish definitive effect-size estimates. This lack of clarity enables competitors to make unverified claims, undermining trust and commoditizing the market. Manufacturers pursuing rigorous longitudinal trials face extended timelines and high costs with uncertain commercial returns, while those relying on anecdotal evidence risk regulatory scrutiny and reputational harm if their claims are contested.

Safety and choking-hazard concerns leading to stricter parental filters on small-part toys

Regulatory enforcement in the educational toys market is becoming more stringent, significantly impacting design flexibility and market access. In January 2026, the Consumer Product Safety Commission (CPSC) recalled 49,410 units of pull-string teething toys due to choking hazards, 9,300 fidget magnet balls for ingestion risks, and 3,500 multifunction pounding games for containing detachable high-powered magnets [2]Source: United States Consumer Product Safety Commission, “AiTuiTui Pull String Teething Toys Recalled Due to Risk of Serious Injury or Death from Choking; Violate Mandatory Standard for Toys,” cpsc.gov. These recalls highlight violations of mandatory American Society for Testing and Materials (ASTM) F963 standards and federal small-parts regulations (16 Code of Federal Regulations 1501), which prohibit items that fit within a small-parts cylinder or detach during use and abuse tests for children under the age of three. Compliance necessitates extensive testing, including impact drops, torque, tension, and compression, with force criteria varying by age group. This increases development costs and extends time to market. Parental risk aversion is further heightened by the rapid spread of recall notices on social media, leading retailers to implement additional screening measures and insurers to demand higher coverage limits. The Consumer Product Safety Commission estimates that approximately 2,400 magnet ingestion cases were treated in United States emergency departments between 2017 and 2021, with 8 deaths reported globally from 2005 to 2021, creating ongoing liability risks for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: STEM Toys Lead Innovation Velocity

In the educational toys market, STEM (science, technology, engineering, and mathematics) toys are projected to grow at a compound annual growth rate (CAGR) of 9.92% from 2026 to 2031, marking the fastest growth rate among product types. This growth is attributed to increased institutional adoption and a growing emphasis by parents on equipping children with future-ready skills. Games and puzzles held a 21.43% market share in 2025, highlighting their adaptability across various age groups and settings, including homes, classrooms, and waiting areas. Their low-tech nature also makes them resilient in regions with unreliable electricity or internet connectivity. Building and construction toys remain a cornerstone of the category due to their enduring appeal, which stems from open-ended play and compatibility across product generations. For instance, LEGO's January 2026 launch of SMART Play, featuring sensors and synthesizers integrated into standard bricks to provide context-aware sounds without screens, illustrates how established players are incorporating digital interactivity into traditional designs.

Arts and crafts toys, encompassing language, literacy, artistic, and creative products, benefit from the integration of maker education and design thinking into school curricula. A 2025 case study demonstrated the effectiveness of a modular 3D letter-building set, co-designed with kindergarten teachers, in enhancing letter-form recognition, spatial awareness, and fine motor skills. Role-play toys, particularly those focused on professions, support social-emotional learning and career exploration. Pretend play scenarios associated with these toys help children symbolically process experiences and reduce frustration during transitions. Other product types, such as musical instruments, outdoor exploration kits, and sensory toys, cater to niche developmental needs and therapeutic applications. Instrumented toys, emerging from research labs, are increasingly being used to measure infant cognitive flexibility through embedded sensors.

By Technology Integration: Screen-Free Smart Toys Disrupt Traditional Dichotomy

The smart toys segment in the educational toys market, incorporating artificial intelligence (AI) and Internet of Things (IoT) technologies, is projected to grow at a compound annual growth rate (CAGR) of 11.43% from 2026 to 2031, marking the fastest growth among technology tiers. This growth is driven by manufacturers integrating sensors, machine learning, and wireless connectivity into physical play objects. In contrast, non-electronic traditional toys accounted for a 56.11% market share in 2025. This segment remains strong due to parental concerns about excessive screen time, regulatory uncertainties surrounding data privacy, and the tactile, multi-sensory engagement offered by analog materials. While appropriately designed digital content can enhance visuospatial skills and executive functions, excessive passive screen time has been linked to reduced sustained attention, sleep disturbances, and impaired social-cognitive development. Meanwhile, electronic and interactive toys occupy a middle tier, featuring battery-powered lights, sounds, and simple feedback loops without internet connectivity or data collection. These toys appeal to caregivers seeking novelty without the risks associated with data privacy.

The smart toys segment is evolving into two distinct architectures: cloud-connected devices and edge-computing designs. Cloud-connected devices enable adaptive learning and remote updates but raise concerns about data privacy. On the other hand, edge-computing designs process data locally, preserving user anonymity. An example of the latter is LEGO's SMART Play platform, where all AI-based computer vision processing occurs locally, ensuring that no images or personal data are stored or shared. Similarly, Miko Mini, an AI-powered conversational robot designed for children aged 5-10, emphasizes safety by being Children's Online Privacy Protection Act (COPPA)-compliant, offering enhanced encryption, parental controls, and ensuring no identifiable voice recordings are stored. These design choices reflect regulatory pressures such as COPPA in the United States and General Data Protection Regulation (GDPR) in Europe, as well as parental skepticism regarding algorithmic manipulation of children.

By Age Group: Early Years Segment Captures Neuroplasticity Premium

The 0-4 Years segment in the educational toys market is projected to grow at a compound annual growth rate (CAGR) of 11.12% from 2026 to 2031, making it the fastest-growing age cohort. This growth is supported by neuroscientific evidence highlighting the benefits of early intervention. The 5-8 Years cohort held a 55.13% market share in 2025, driven by its alignment with the start of formal schooling, heightened caregiver focus on academic preparedness, and the developmental stage where children can engage with complex toys while benefiting from play-based learning. Longitudinal magnetic resonance imaging (MRI) studies published in 2025 revealed that brain development features such as volumetric, cortical surface, and white-matter measures from infancy to school age directly influenced preschool phonological processing. This, in turn, impacted early elementary decoding and word reading. This causal relationship supports premium pricing for toys designed to target critical periods of neuroplasticity, particularly those that enhance phonological awareness, symbolic play, and caregiver-mediated interaction.

The 9-11 Years and 12+ Years segments face challenges due to digital alternatives, including smartphones, gaming consoles, and social media, as well as the perception that physical toys are more suitable for younger children. However, STEM kits, robotics platforms, and advanced building sets continue to perform well by positioning themselves as tools for skill development rather than traditional toys. For example, LEGO Education's Computer Science and Artificial Intelligence (AI) Kit for grades 6-8 remains a notable offering in this space.

By Material: Bio-Plastics Gain Share Amid Sustainability Mandates

In the educational toys market, recycled and bio-plastics are expected to grow at a compound annual growth rate (CAGR) of 12.02% from 2026 to 2031, emerging as the fastest-growing material type. This growth is primarily driven by increasing regulatory pressures and shifting consumer preferences toward sustainability. In comparison, conventional plastics held a 61.43% market share in 2025, supported by their cost advantages, design flexibility, and well-established supply chains. However, conventional plastics are increasingly scrutinized due to concerns over microplastic pollution, endocrine-disrupting additives, and challenges related to end-of-life disposal.

Wood and paper-based toys appeal to eco-conscious consumers and align with Montessori educational philosophies that prioritize natural materials. Despite their attractiveness, these materials face limitations such as higher costs, lower durability, and reduced design complexity compared to injection-molded plastics. Other material types, including textiles, metals, and hybrid composites, are utilized in niche applications, such as sensory toys for children with special needs and outdoor exploration kits.

By Distribution Channel: E-Commerce Gains Share via Personalization and Subscription

In the educational toys market, online retail stores are expected to grow at a compound annual growth rate (CAGR) of 12.41% from 2026 to 2031, making them the fastest-growing distribution channel. This growth is driven by factors such as personalization engines, subscription models, and direct-to-consumer strategies that eliminate the need for traditional shelf space. In 2025, supermarkets and hypermarkets accounted for a 28.33% market share, benefiting from high foot traffic, impulse purchasing, and the ability for customers to physically inspect products before buying. This is particularly important for tactile toys and items requiring complex assembly.

Specialty stores offer curated product assortments, knowledgeable staff, and experiential retail formats, including in-store play areas and workshops. However, they face challenges such as margin pressures due to e-commerce price transparency and the fixed costs associated with maintaining physical locations. Other distribution channels, including direct sales, catalogs, and institutional procurement, cater to niche markets such as schools, daycares, and therapy centers. The growth of e-commerce is driven by algorithmic recommendation engines that promote complementary products, subscription boxes that simplify purchasing and enhance customer lifetime value, and user-generated reviews that act as substitutes for in-store product inspections. Amazon's significant role in online toy sales presents both opportunities and risks. While the platform provides access to global demand and a robust fulfillment infrastructure, it also commoditizes products through price-comparison tools and exposes manufacturers to risks such as counterfeit goods and knock-offs. In January 2026, the Consumer Product Safety Commission (CPSC) issued recalls for several products sold exclusively on Amazon and Temu, including magnetic building sets and pull-string teething toys.

Geography Analysis

Europe accounted for 37.82% of the educational toys market share in 2025, driven by high per-capita income, strong educational infrastructure, stringent safety regulations, and a cultural focus on play-based learning. Key markets such as Germany, the United Kingdom, France, and Spain drive demand in the region. Germany's emphasis on quality standards and the United Kingdom's early-years curriculum are supporting growth in the premium segment. Sustainability preferences are particularly strong in Northern Europe, where consumers prioritize recycled materials, Forest Stewardship Council (FSC)-certified wood, and carbon-neutral manufacturing. This trend creates opportunities for brands like PlanToys and Green Toys. However, economic challenges, including inflation, rising energy costs, and fiscal austerity, are limiting discretionary spending. Mid-tier brands face pressure to demonstrate clear educational value or risk being replaced by lower-cost alternatives. The region's regulatory framework, including Conformité Européenne (CE) marking, European Norm (EN) 71 toy safety standards, and Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) restrictions, imposes compliance costs that favor established players with dedicated regulatory teams.

In the educational toys market, the Asia-Pacific region is projected to grow at a compound annual growth rate (CAGR) of 11.71% from 2026 to 2031, making it the fastest-growing market. This growth is driven by the expanding middle class in China and India, government mandates for Science, Technology, Engineering, and Mathematics (STEM) education, and increasing parental investment in early education. In China, education reforms that emphasize creativity and problem-solving over rote memorization are boosting demand for open-ended construction toys and STEM kits. In India, the growing educational technology (edtech) ecosystem is fostering hybrid toy-app bundles that combine physical interaction with digital feedback. While Japan's aging population and low birth rate limit volume growth, high per-capita spending and a cultural appreciation for craftsmanship sustain demand for premium, design-focused products. Emerging markets such as Indonesia, Thailand, and Singapore are benefiting from rising disposable incomes and greater awareness of early childhood development. However, price sensitivity and fragmented retail landscapes require localized go-to-market strategies. The region's manufacturing base, concentrated in China, Vietnam, and Thailand, offers cost advantages but is exposed to geopolitical risks, tariff fluctuations, and rising labor costs.

North America, South America, and the Middle East and Africa collectively account for the remaining educational toys market share. North America benefits from high consumer spending, a well-established e-commerce infrastructure, and institutional procurement by schools and daycares. However, the region faces challenges such as market saturation and competition from free digital applications. In the United States, Consumer Product Safety Commission (CPSC) enforcement and American Society for Testing and Materials (ASTM) F963 compliance requirements create regulatory barriers that protect established players while increasing entry challenges for new entrants [3]Source: Federal Register, “Safety Standard Mandating ASTM F963 for Toys,” federalregister.gov. Mexico's proximity to U.S. manufacturing and distribution networks positions it as a nearshoring destination amid tariff uncertainties. South America, led by Brazil and Argentina, shows growth potential due to urbanization and expanding middle classes. However, macroeconomic volatility and currency fluctuations complicate pricing strategies and margin management. The Middle East and Africa, with key markets such as the United Arab Emirates, Saudi Arabia, South Africa, and Turkey, represent emerging opportunities. These markets exhibit high growth potential but face challenges such as limited consumer data and underdeveloped distribution infrastructure. Establishing a presence in these regions requires patient capital and localized partnerships.

Competitive Landscape

The educational toys market is moderately fragmented, with global incumbents coexisting alongside emerging entrants. Established companies in the educational toys market, like LEGO, Mattel, and Hasbro, leverage their brand equity, retail networks, and intellectual property portfolios to maintain market share. Meanwhile, digitally native brands and STEM-focused (Science, Technology, Engineering, and Mathematics) specialists capitalize on opportunities in subscription models, institutional sales, and sensor-embedded smart toys. Key strategies include vertical integration into content and curriculum development, horizontal expansion through licensing partnerships (e.g., LEGO's collaborations with Star Wars and Pokémon, and Mattel's partnership with OpenAI announced in 2025), and mergers and acquisitions to enhance digital capabilities. For instance, Mattel's USD 318 million acquisition of full ownership of Mattel163 in February 2026 added expertise in mobile game development, publishing, and digital customer acquisition to its portfolio.

Technology remains a critical competitive area. LEGO's SMART Play platform incorporates over 20 patented sensor and synthesizer technologies into its bricks, creating a proprietary ecosystem that enhances user engagement and raises barriers to imitation. Emerging disruptors, such as Shifu Technologies and Ozobot, focus on STEM-oriented products and bypass traditional retail channels by utilizing direct-to-consumer e-commerce and institutional sales to schools. Ozobot, for example, offers dual coding pathways with screen-free color codes and block-based programming targeting children aged 4-5 and above, with a reported reach of over 1.7 million students.

Opportunities also exist in inclusive and special-needs-oriented toys. Products with clinically validated efficacy, such as LEGO-based therapy, which has shown improvements in executive function for children with autism spectrum disorder (ASD), can command premium pricing and gain traction in institutional markets. Sustainability is another area of growth. Brands that demonstrate credible efforts in recycled-material sourcing, carbon-neutral manufacturing, and circular-economy models (e.g., take-back programs and modular repairability) can differentiate themselves in eco-conscious segments. However, consumer willingness to pay a premium for such features varies across regions and income levels. Compliance with safety standards, including ASTM F963 (American Society for Testing and Materials), CPSC (Consumer Product Safety Commission) regulations, and international standards like ISO 8124, is essential. Recent product recalls highlight that safety lapses can lead to immediate market exclusion and significant reputational damage.

Educational Toys Industry Leaders

LEGO Group

Mattel Inc.

VTech Holdings Ltd.

Hasbro Inc.

Spin Master Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Wondery introduced a unique line of toys and consumer products inspired by the top-ranked science podcast for children and their parents, Wow in the World. The Wondery Kids & Wow in the World toy line features products that reinterpret classic toys and play patterns, providing children and their parents with a new way to interact and engage.

- September 2024: Hape expanded its sustainable product portfolio by introducing new educational toys made from bamboo and recycled plastics. This initiative aligns with global environmental regulations and addresses the increasing parental demand for environmentally friendly products.

- July 2024: Osmo introduced subscription-based educational kits that integrate physical manipulatives with interactive digital games, aimed at early childhood development through play-based and experiential learning.

- February 2024: LeapFrog collaborated with Walmart to develop exclusive STEM-focused educational toy bundles. These bundles integrate physical toys with digital learning content and are available through Walmart's extensive supermarket network and online platforms.

Global Educational Toys Market Report Scope

The educational toys market includes toys designed to enhance children's cognitive, motor, and creative skills through interactive play. The market is segmented by product type, technology integration, age group, material, distribution channel, and geography. By product type, the market includes building and construction toys, games and puzzles, arts and crafts such as language, literacy, artistic, and creative toys, role play toys focusing on professions, STEM (Science, Technology, Engineering, and Mathematics) toys, and other product types. By technology integration, the market is divided into non-electronic traditional toys, electronic and interactive toys, and smart toys with artificial intelligence (AI) and Internet of Things (IoT). By age group, the market caters to children aged 0 to 4 years, 5 to 8 years, 9 to 11 years, and 12 years and above. By material, the market includes conventional plastics, recycled and bio-plastics, wood and paper-based materials, and other material types. By distribution channel, the market is segmented into supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the above mentioned segments.

| Building and Construction |

| Games and Puzzles |

| Arts and Crafts (Language, Literacy, Artisitic and Creative Toys) |

| Role Play (Profession Focused) |

| STEM Toys |

| Other Product Types |

| Non-Electronic Traditional Toys |

| Electronic/Interactive Toys |

| Smart Toys with AI/IoT |

| 0-4 Years |

| 5-8 Years |

| 9-11 Years |

| 12+ Years |

| Conventional Plastics |

| Recycled/Bio-plastics |

| Wood and Paper-based |

| Other Material Types |

| Supermarkets and Hypermarkets |

| Speciality Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Building and Construction | |

| Games and Puzzles | ||

| Arts and Crafts (Language, Literacy, Artisitic and Creative Toys) | ||

| Role Play (Profession Focused) | ||

| STEM Toys | ||

| Other Product Types | ||

| By Technology Integration | Non-Electronic Traditional Toys | |

| Electronic/Interactive Toys | ||

| Smart Toys with AI/IoT | ||

| By Age Group | 0-4 Years | |

| 5-8 Years | ||

| 9-11 Years | ||

| 12+ Years | ||

| By Material | Conventional Plastics | |

| Recycled/Bio-plastics | ||

| Wood and Paper-based | ||

| Other Material Types | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Speciality Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the educational toys market in 2026?

It is valued at USD 78.48 billion in 2026, on track to reach USD 118.08 billion by 2031.

Which product segment is expanding the fastest?

STEM Toys are projected to grow at a 9.92% CAGR between 2026 and 2031.

Why is Asia-Pacific the fastest-growing region?

Middle-class expansion, STEM mandates in China and India, and rising parental spend push the region to an 11.71% CAGR.

What drives the shift toward smart, sensor-enabled toys?

Parents want interactive feedback without added screen time, while edge-AI hardware meets privacy rules and enriches play value.

How are sustainability trends affecting materials?

Regulatory pressure and eco-conscious consumers lift bio-plastics, expected to post a 12.02% CAGR through 2031.

Page last updated on: