Fidget Toys Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

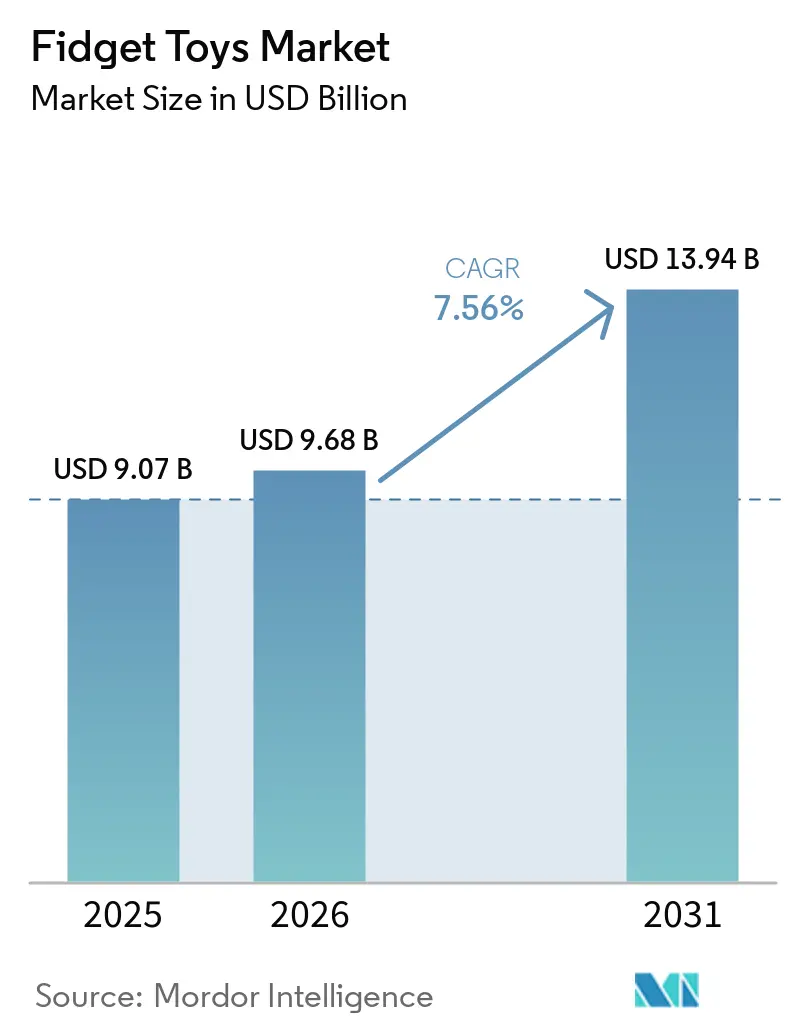

| Market Size (2026) | USD 9.68 Billion |

| Market Size (2031) | USD 13.94 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

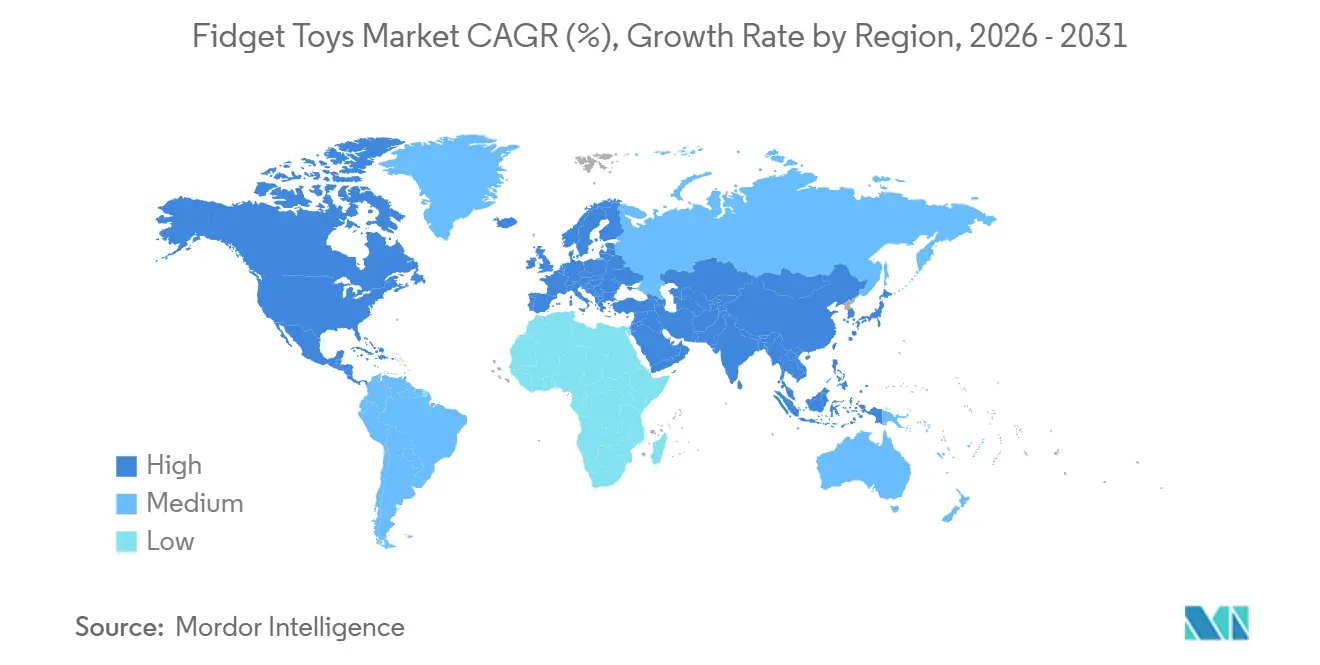

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fidget Toys Market Analysis by Mordor Intelligence

The fidget toys market size is expected to increase from USD 9.07 billion in 2025 to USD 9.68 billion in 2026 and expected to reach USD 13.94 billion by 2031, growing at a CAGR of 7.56% over 2026-2031. The fidget toys market is supported by a broad rise in mental health concerns, with nearly 1.2 billion people worldwide living with a mental disorder as of May 2026, which has widened demand for simple and accessible stress-relief products[1]Source: Institute for Health Metrics and Evaluation, “Global Mental Disorders Have Nearly Doubled Since 1990, Now Affecting 1.2 Billion People Worldwide,” healthdata.org. The category now reaches well beyond children because wellness habits, therapy use, and social media discovery have pulled in office workers, adult collectors, and neurodivergent consumers across income groups. The fidget toys market is also shifting from novelty-led buying toward products that carry a clearer stress-relief or sensory purpose, which is raising the value of therapeutic positioning, safer materials, and repeat purchase channels. Regulatory changes in Europe and China are tightening chemical and safety requirements, which is pushing brands to rethink plastics, formulations, and supplier standards. The fidget toys market remains moderately fragmented, and competition is increasingly shaped by product safety, premium materials, therapeutic credibility, and the ability to respond quickly to viral demand while limiting exposure to counterfeit goods.

Key Report Takeaways

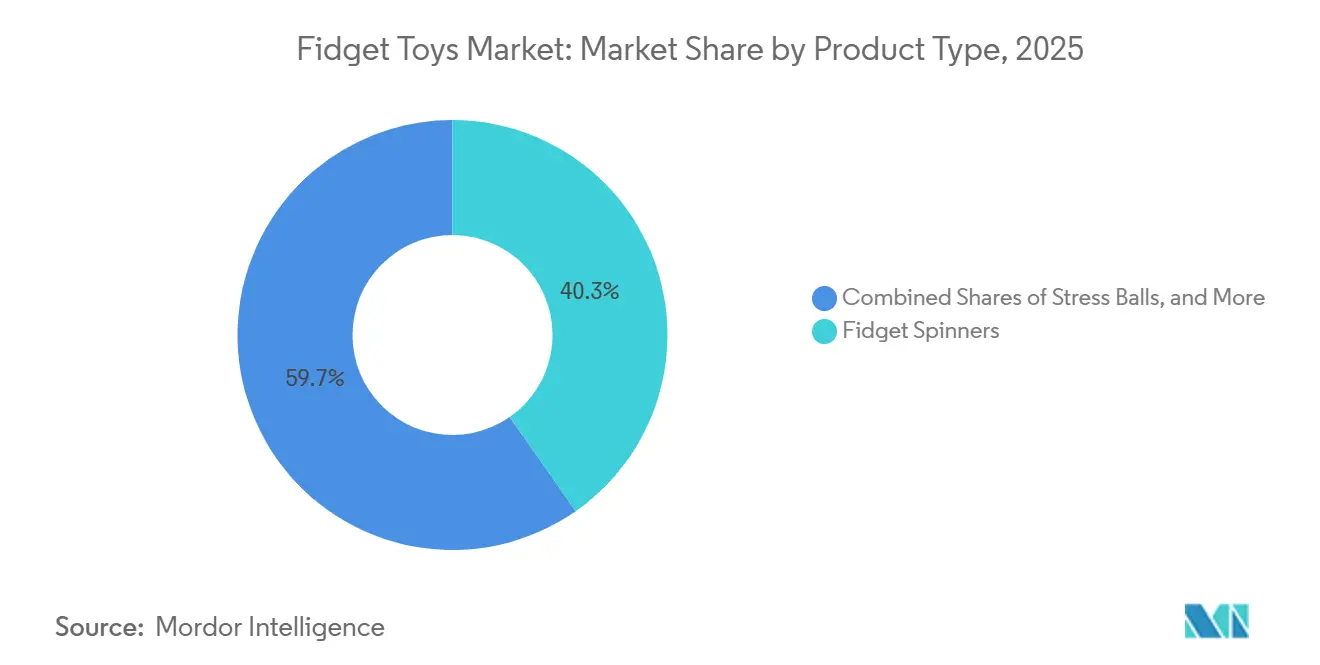

- By product type, fidget spinners led with 40.28% revenue share in 2025, while stress balls are forecast to expand at 9.11% CAGR through 2031.

- By material, plastic held 53.48% share in 2025, while silicone is projected to record the highest CAGR at 8.73% through 2031.

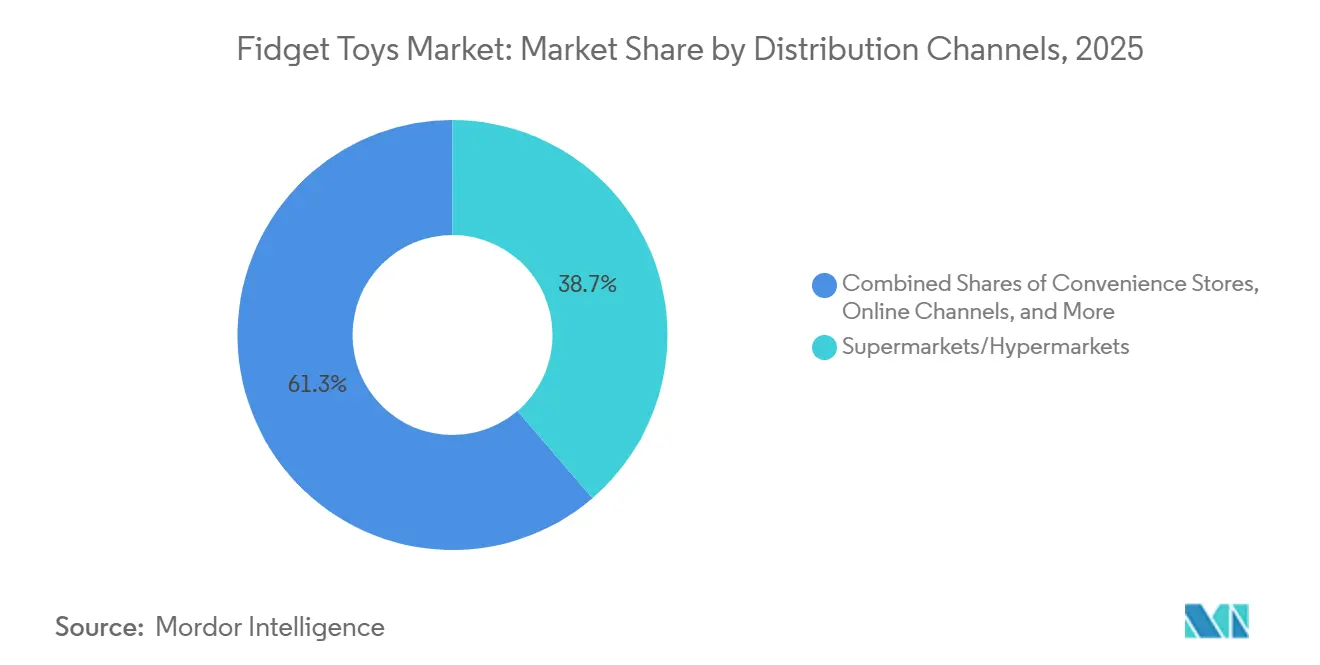

- By distribution channel, supermarkets and hypermarkets accounted for 38.72% of revenue in 2025, while online retail is advancing at 9.03% CAGR through 2031.

- By geography, North America held 41.35% of revenue in 2025, while Asia-Pacific is forecast to grow at 8.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fidget Toys Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Awareness of Stress and Anxiety Management Products | +2.0% | Global, with elevated impact in North America and Western Europe | Medium term (2-4 years) |

| Increasing Adoption of Sensory Toys for ADHD and Autism Support | +1.5% | Global, highest concentration in North America, Europe, and Australia | Long term (≥ 4 years) |

| Strong Influence of Social Media Trends and Viral Product Marketing | +1.2% | North America, Europe, East Asia | Short term (≤ 2 years) |

| Continuous Product Innovation in Designs, Materials, and Functions | +1.0% | Global, with premium innovation starting in North America and extending into Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing Demand for Portable and On-the-Go Entertainment Products | +0.8% | Global, with early gains across urban markets in North America, Europe, and Asia | Short term (≤ 2 years) |

| Rising Consumer Interest in Screen-Free Recreational Activities | +0.7% | North America, Western Europe, Australia, South Korea, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Stress and Anxiety Management Products

The fidget toys market is benefiting from a wider consumer search for low-cost ways to manage daily stress and anxiety. A 2026 global release from IHME stated that nearly 1.2 billion people worldwide now live with a mental disorder, which has made emotional wellness a much larger consumer concern than it was in prior years. A 2026 Lancet analysis also showed that anxiety disorders posted the sharpest rise among major mental disorders in the post-COVID period, reinforcing demand for products tied to sensory relief and self-regulation. This has widened the commercial base of the fidget toys market beyond toy aisles because products are now purchased through pharmacy, school supply, and convenience-led channels. The demand pattern is durable because the category increasingly sits at the intersection of wellness buying, casual play, and practical coping behavior.

Increasing Adoption of Sensory Toys for ADHD and Autism Support

The fidget toys market is also supported by more formal use of sensory products in therapeutic and educational settings. A 2024 study in the Journal of Positive Behavior Interventions found that fidget toy use among elementary students with autism did not harm story detail acquisition during reading tasks, which supports their continued use in structured classroom activity[2]Source: ERIC, “The Impact of Fidget Toys on Story Detail Acquisition and Visual Attention for Elementary Students with Autism,” eric.ed.gov. This kind of clinical backing gives schools, therapists, and parents a clearer reason to treat these products as functional tools rather than passing novelties. The institutional channel matters because it creates repeat purchasing behavior that is less exposed to viral trend cycles than general retail. Brands such as Tangle Creations have strengthened their position by registering sensory tools such as Tangle Therapy and Tangle Relax as FDA medical devices, which helps them stand apart in healthcare and education procurement.

Strong Influence of Social Media Trends and Viral Product Marketing

The fidget toys market now depends heavily on short-cycle digital discovery, especially when new tactile formats move quickly through video platforms and marketplace algorithms. Viral content has become more than a marketing tool because it now shapes launch timing, buying decisions, and retailer expectations around sell-through. The Toy Association reported that the U.S. toy market grew 13% in dollar terms from January through April 2026, and licensed and collectible formats continued to hold a strong position in global toy sales, which supports the link between social buzz and toy spending. In the fidget toys market, products designed for unboxing, texture-focused video, and fast visual appeal can move from niche awareness to broad retail traction within days. This dynamic favors brands that can pair quick design response with dependable inventory and platform-ready merchandising.

Continuous Product Innovation in Designs, Materials, and Functions

The fidget toys market is moving toward more engineered and differentiated products, which is reducing reliance on simple visual novelty alone. Lautie’s Noiz-O launch in early 2026 introduced a linked rotation mechanism that pushed premium spinner design toward greater mechanical sophistication and adult collector appeal. At the same time, the mass end of the fidget toys market is expanding through hybrid products that combine tactile play with collectibles, art activity, or decorative value. This pattern supports higher average selling prices because one product can now serve as a fidget tool, a gift item, and a display object. The commercial advantage is strongest for brands that can innovate in both function and material while staying compliant with tighter global toy safety rules.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Counterfeit and Low-Quality Products | -1.4% | Global, with highest impact in Europe, North America, and online marketplaces | Short term (≤ 2 years) |

| Short Product Life Cycles and Rapidly Changing Consumer Trends | -1.0% | Global, with concentrated impact in North America and East Asia | Short term (≤ 2 years) |

| Regulatory Compliance Challenges for Children's Toy Safety Standards | -0.8% | Europe, the UK, North America, and China | Medium term (2-4 years) |

| Growing Competition from Digital Entertainment and Mobile Gaming | -0.7% | North America, Western Europe, and East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit and Low-Quality Products

The fidget toys market faces a persistent quality problem because counterfeit and unsafe products can enter the category quickly when demand spikes. U.S. authorities seized nearly 1.6 million dangerous or illegal toys at the border in FY2024, up 45% from FY2023, including nearly 102,000 toys with unsafe lead levels. In Europe, Europol’s Operation LUDUS seized 45.6 million counterfeit toys, showing the scale at which unsafe imitation products can spread through retail and online channels[3]Source: Europol, “Cheating the Toy World, Operation LUDUS,” Europol, europol.europa.eu. A 2025 Toy Industries of Europe exercise found that 96% of toys from non-EU marketplace sellers were non-compliant, and 86% carried serious safety risks, which makes trust and certification central to the category. The result is margin pressure for legitimate brands because they must absorb compliance costs while lower-quality sellers ignore them.

Short Product Life Cycles and Rapidly Changing Consumer Trends

The fidget toys market remains exposed to fast swings in consumer attention, and that keeps the revenue life of many product formats short. Fidget spinners still lead the category by share, but they have settled into a mature volume segment rather than a strong growth engine. The commercial gap between a product going viral and the arrival of low-cost copycat versions can be very small, especially for simple plastic and silicone formats. This pushes brands to build stronger narratives around therapy use, collectibility, material quality, or licensed content rather than relying on novelty alone. Companies with broader product portfolios across stress balls, pop-it toys, infinity cubes, and sensory strips are better placed to withstand the rotation of trend-led demand within the fidget toys market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Novelty Fatigue Redirects Volume Toward Therapeutic Formats

Fidget spinners held 40.28% of fidget toys market share in 2025, which kept them as the largest product type by revenue. Their lead still reflects wide shelf presence, easy consumer recognition, and continued use in classrooms and offices. The segment remains important to the fidget toys market because it offers low production complexity and high merchandising visibility. Even so, its growth profile is now more mature than that of newer or more wellness-linked formats.

The fidget toys market size for stress balls is forecast to expand at 9.11% CAGR through 2031, making them the fastest-growing product type in the current mix. Their appeal is broader because they serve as stress-relief tools, low-cost gifts, and therapy-adjacent items at the same time. This gives the segment stronger relevance among parents, school counselors, and mental health practitioners who prefer products with a clearer use case. Pop-it toys remain high volume but lower value, while premium metal, magnetic, and specialty tactile formats are gaining traction with adult buyers and specialty wellness retailers. The product mix in the fidget toys market is therefore shifting from mechanics-led novelty toward formats that carry more functional meaning and better pricing support.

By Material: Regulatory Pressure Accelerates the Shift Away from Commodity Plastics

Plastic accounted for 53.48% of revenue in 2025, which kept it as the dominant material base in the fidget toys market. Its lead is tied to low cost, fast molding speed, and broad compatibility with large-scale production in Asian supply chains. Plastic also supports a wide range of shapes, colors, and textures, which has made it the default material for mainstream and impulse-priced products. That position remains strong in the short term because scale economics still favor mass-market plastic items.

Silicone is projected to grow at 8.73% CAGR through 2031, which makes it the fastest-rising material in the fidget toys market. The shift reflects stronger parent interest in non-toxic materials and the effect of tighter toy safety regulation in Europe and China. Silicone also fits well with squeeze, putty, gel, and soft sensory formats that need both durability and tactile consistency. Metal keeps a premium niche among adult collectors, while wood and other natural materials appeal to buyers looking for lower-tech and sustainability-linked options. Material choice in the fidget toys market is increasingly becoming a brand signal rather than only a manufacturing decision.

By Distribution Channel: Supermarket Dominance Faces a Structural Challenge from Social Commerce

Supermarkets and hypermarkets captured 38.72% share in 2025, which made them the largest distribution route in the fidget toys market. Their position is built on impulse buying, checkout placement, seasonal promotions, and strong alignment with back-to-school traffic. These stores also benefit from high visibility for lower-priced formats that do not require extensive consumer education. The channel remains important because it still drives broad household reach at scale.

Online retail is advancing at 9.03% CAGR through 2031, which makes it the fastest-growing route in the fidget toys market. The shift reflects a direct link between social media discovery, marketplace search, and rapid order fulfillment. Viral content can raise retailer sell-through far above normal weekly levels during short demand spikes, which makes digital channels especially important for fast-moving launches. Convenience stores keep a stable role in school-adjacent and transit-heavy locations, while therapy-linked specialty channels are building a smaller but higher-quality repeat business. Distribution in the fidget toys market is moving toward a model where physical retail drives breadth and online platforms drive speed.

Geography Analysis

North America held 41.35% of the fidget toys market share in 2025, making it the largest regional contributor by revenue. The region’s position is supported by deep retail infrastructure, strong occupational therapy networks, and high spending on toys and related wellness products. The Toy Association reported 13% dollar growth in the U.S. toy market from January through April 2026, which signals favorable demand conditions for tactile and low-tech play formats. The same association also highlighted consumer interest in cozy, tactile, screen-free play, which aligns directly with the value proposition of the fidget toys market.

Asia-Pacific is the fastest-growing region, and the fidget toys market size there is forecast to rise at 8.85% CAGR through 2031. Demand growth is broadening beyond China, even though China remains a key production and consumption center for stress-relief and squeeze formats. India is also an important demand center because its toy sector is expanding, and the domestic manufacturing policy is encouraging more certified local supply within the category. Southeast Asian countries are gaining relevance because e-commerce platforms are widening access to affordable sensory products and impulse-led toy buying. Japan and South Korea follow different paths, with Japan showing stronger premium adult demand and South Korea showing faster social commerce-driven traction.

Europe remains a premium-oriented and compliance-heavy region in the fidget toys market. The EU Toy Safety Regulation 2025/2509 entered into force on January 1, 2026, and it raised the standard for chemical compliance in toys sold into the bloc. That change is likely to direct more demand toward certified and higher-quality brands while making low-cost non-compliant supply less competitive. South America and the Middle East and Africa are still smaller contributors, but they have favorable long-term conditions through urban retail expansion, young populations, and improving awareness of screen-free and sensory play.

Competitive Landscape

The fidget toys market is moderately fragmented, with specialist sensory brands operating alongside large toy companies that are entering through adjacent tactile formats. Competition is strongest in lower price tiers, where plastic and silicone products are easy to copy and quick to launch. This keeps shelf competition high and makes brand trust, product safety, and retail compliance more important than simple novelty. The fragmented structure also means that fast response to trends can matter as much as scale in the fidget toy market.

Some companies are trying to separate themselves through clear strategic moves. Hasbro pre-launched Nano-mals in 2026, bringing interactive fidget-style pets with touch-responsive behavior into the category and signaling that larger toy companies see room in sensory-led hybrid products. Lautie introduced the Noiz-O in early 2026, using a proprietary linked rotation mechanism to push the premium spinner segment toward more engineered tactile performance. Tangle Creations has built a more defensible position in healthcare and education channels through FDA medical device registration for Tangle Therapy and Tangle Relax, which gives it a credibility advantage in institutional sourcing. These moves show that the fidget toys market is no longer competing only on toy aesthetics, because clinical fit, adult appeal, and technical design now shape premium positioning.

Another dividing line in the fidget toys market is the difference between general retail brands and companies targeting adult collectors or therapy-led demand. Premium direct-to-consumer players can command much higher unit prices when material quality and tactile precision are part of the product promise. Mainstream players, by contrast, focus more on reach, licensing, and broad retail placement. Over time, this should keep the market fragmented, but it should also widen the performance gap between brands that offer credible differentiation and those that depend on short-lived trend volume.

Fidget Toys Industry Leaders

LEGO Group

Hasbro Inc.

Mattel Inc.

Spin Master Corp.

ZURU Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hasbro pre-launched Nano-mals, a line of interactive fidget-style pets with over 70 sounds and reactions that respond to petting, feeding, flipping, and shaking. Retail availability is set for August 1, 2026, marking Hasbro's direct entry into the sensory fidget-interactive toy hybrid segment at a consumer price point.

- February 2026: Lautie launched the Noiz-O fidget spinner featuring a proprietary crown-button linked rotation mechanism, where the outer spinner leaf and inner button rotate at varying speeds simultaneously. Early sell-through velocity exceeded any prior Noiz-series drop, according to collector channel data.

- March 2025: Tangle Creations launched its Tangle product line in the Chinese market. By early 2026, cumulative sales exceeded 1 million units, establishing one of the most successful Western sensory fidget brand entries into mainland China in the period.

Global Fidget Toys Market Report Scope

| Fidget Spinners |

| Stress Balls |

| Infinity Cubes |

| Pop-It Toys |

| Others |

| Plastic |

| Metal |

| Silicone |

| Wood |

| Other Materials |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Fidget Spinners | |

| Stress Balls | ||

| Infinity Cubes | ||

| Pop-It Toys | ||

| Others | ||

| By Material | Plastic | |

| Metal | ||

| Silicone | ||

| Wood | ||

| Other Materials | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the fidget toys space?

The fidget toys market was valued at USD 9.07 billion in 2025 and is projected to reach USD 13.94 billion by 2031 at a 7.56% CAGR.

Which product type leads revenue today?

Fidget spinners remain the largest product type, with 40.28% revenue share in 2025.

Which product category is growing the fastest through 2031?

Stress balls are the fastest-growing product type, with a forecast CAGR of 9.11% through 2031.

Why is online retail becoming more important for fidget products?

Online retail is forecast to grow at 9.03% CAGR because viral discovery, marketplace search, and fast fulfillment now move demand more quickly than many physical channels.

Page last updated on: