Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The High-Resolution Industrial Camera Market Report is Segmented by Spectrum (Visible RGB, Infrared, X-Ray, and Multispectral), Frame Rate (250-1000, 1001-10000, 10001-30000, and More), Application (Precision Measurement, Quality Inspection, Robotics Automation, Surveillance, and Scientific R&D), End-Use Industry (Electronics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

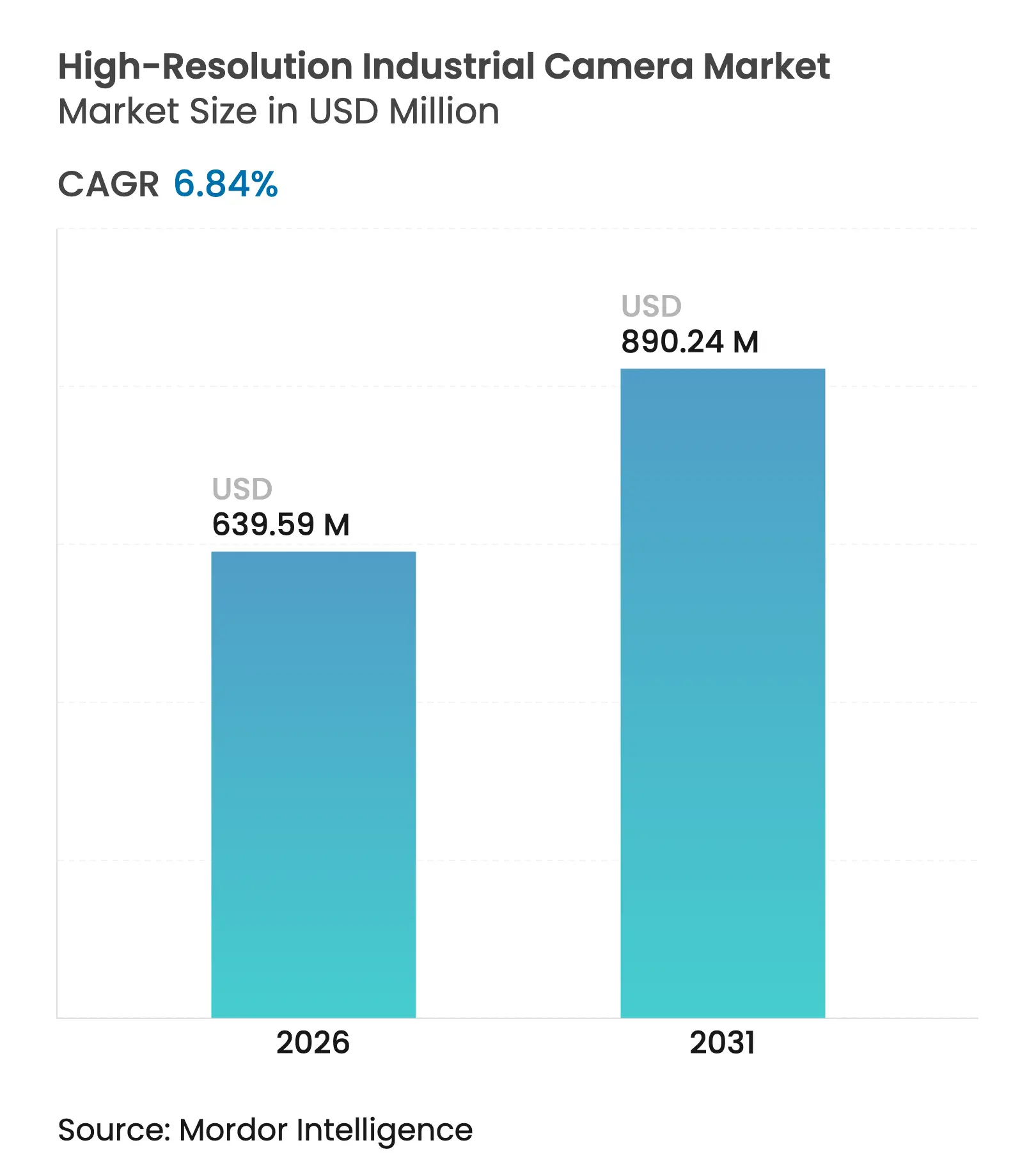

| Market Size (2026) | USD 639.59 Million |

| Market Size (2031) | USD 890.24 Million |

| Growth Rate (2026 - 2031) | 6.84 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

High-resolution industrial camera market size in 2026 is estimated at USD 639.59 million, growing from 2025 value of USD 598.64 million with 2031 projections showing USD 890.24 million, growing at 6.84% CAGR over 2026-2031. The market is expanding steadily as manufacturers worldwide integrate advanced vision systems into their production lines. Analysts tracking the space see mid-single-digit annual growth through the end of the decade, supported by rising investments in quality automation, semiconductor miniaturization, and edge-based artificial intelligence workloads. Adoption has accelerated in facilities that require microscopic inspection, such as wafer fabrication plants and printed-circuit-board assembly lines because visual accuracy now determines both output yield and brand reputation. Suppliers able to combine imaging hardware with proprietary algorithms are capturing the lion’s share of new orders, while interface innovations such as CoaXPress-over-Fiber remove distance limits that once curbed factory-floor flexibility.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing need for zero-defect manufacturing Growing need for zero-defect manufacturing | 2.10% | Global, with concentration in APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:2.10% | Geographic Relevance:Global, with concentration in APAC | Impact Timeline:Medium term (2-4 years) |

Cost-down of high-speed CMOS global-shutter sensors Cost-down of high-speed CMOS global-shutter sensors | 1.80% | Global | Short term (≤ 2 years) | |||

Expansion of advanced robotics in harsh environments Expansion of advanced robotics in harsh environments | 1.50% | North America and Europe, with emerging adoption in APAC | Medium term (2-4 years) | |||

Surge in on-edge AI inference demanding higher image quality Surge in on-edge AI inference demanding higher image quality | 1.20% | North America, Europe, advanced APAC economies | Long term (≥ 4 years) | |||

Regulatory push for in-cabin driver monitoring Regulatory push for in-cabin driver monitoring | 0.80% | Europe, North America, Japan | Medium term (2-4 years) | |||

MandA race for proprietary prism/quad-linear IP MandA race for proprietary prism/quad-linear IP | 0.50% | Global, with concentration in North America and Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing need for zero-defect manufacturing

High-volume producers have tightened tolerance windows to micrometer levels that human inspectors cannot reliably detect. McKinsey reported that factories introducing vision-based quality gates cut defect escapes by up to 90% and lifted throughput by 30%. Pairing high-resolution sensors with AI classifiers slashes false positives, while early-stage wafer screening in semiconductor lines can save USD 500,000–1 million per production run.

Expansion of advanced robotics in harsh environments

Vision-guided robots now operate inside foundries, chemical plants and decommissioning sites where heat, dust and vibration would disable unprotected optics. Teledyne’s Bumblebee X camera, presented in 2025, demonstrates dual-path processing that lets robots retain sub-millimeter accuracy under variable lighting. Field data from the Association for Advancing Automation shows such systems lowering injury frequency by 35% while extending equipment life through predictive maintenance.[1]Association for Advancing Automation, “The Critical Role of Machine Vision Systems,” automate.org

Cost-down of high-speed CMOS global-shutter sensors

The price of a 5-megapixel industrial camera fell below USD 1,000 in 2024, compared with more than USD 10,000 for a 1.4-megapixel unit three decades earlier. Affordable global-shutter technology eliminates motion blur at line speeds above 10 m/s, opening vision adoption to small and medium enterprises in textiles, food packaging, and pharmaceuticals.

Surge in on-edge AI inference demanding higher image quality

Edge devices equipped with neural processing units need richer visual data to reach cloud-level classification accuracy. The 2025 Edge AI Report documented 99.8% defect-detection precision when inspection systems captured high-resolution inputs, while reducing bandwidth by 95% versus cloud-centric workflows. Integrated processing inside the camera module also removes latency, which is critical for millisecond-scale adjustments in robotic guidance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile semiconductor supply chain raising BOM costs Volatile semiconductor supply chain raising BOM costs | -1.20% | Global, with severe impact in North America and Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.20% | Geographic Relevance:Global, with severe impact in North America and Europe | Impact Timeline:Short term (≤ 2 years) |

Export-control tightening on vision gear to China Export-control tightening on vision gear to China | -0.90% | China, with ripple effects in global supply chains | Medium term (2-4 years) | |||

Data-pipe bandwidth bottlenecks above 25 Gbps Data-pipe bandwidth bottlenecks above 25 Gbps | -0.80% | Global | Medium term (2-4 years) | |||

Short replacement cycles in smart-factory CAPEX budgets Short replacement cycles in smart-factory CAPEX budgets | -0.50% | North America, Europe, advanced APAC economies | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile semiconductor supply chain raising BOM costs

Export restrictions on germanium and gallium lifted specialty-optics prices by up to 75%, and lead times for advanced image sensors breached 40 weeks in 2024. Producers now lock in multi-quarter component contracts or pre-buy silicon to shield margins, but higher working capital needs pressure smaller vendors.

Data-pipe bandwidth bottlenecks above 25 Gbps

Ultra-high-resolution streams overwhelm legacy links. IEEE’s ISAAC project highlighted the push for 25 Gbps standards to carry uncompressed imagery.[2]IEEE 802.3 ISAAC, “Need for 25 Gbps Links,” ieee802.org Designers otherwise juggle frame rate, bit depth, and resolution compromises that dilute defect-detection fidelity in semiconductor and high-speed packaging lines.

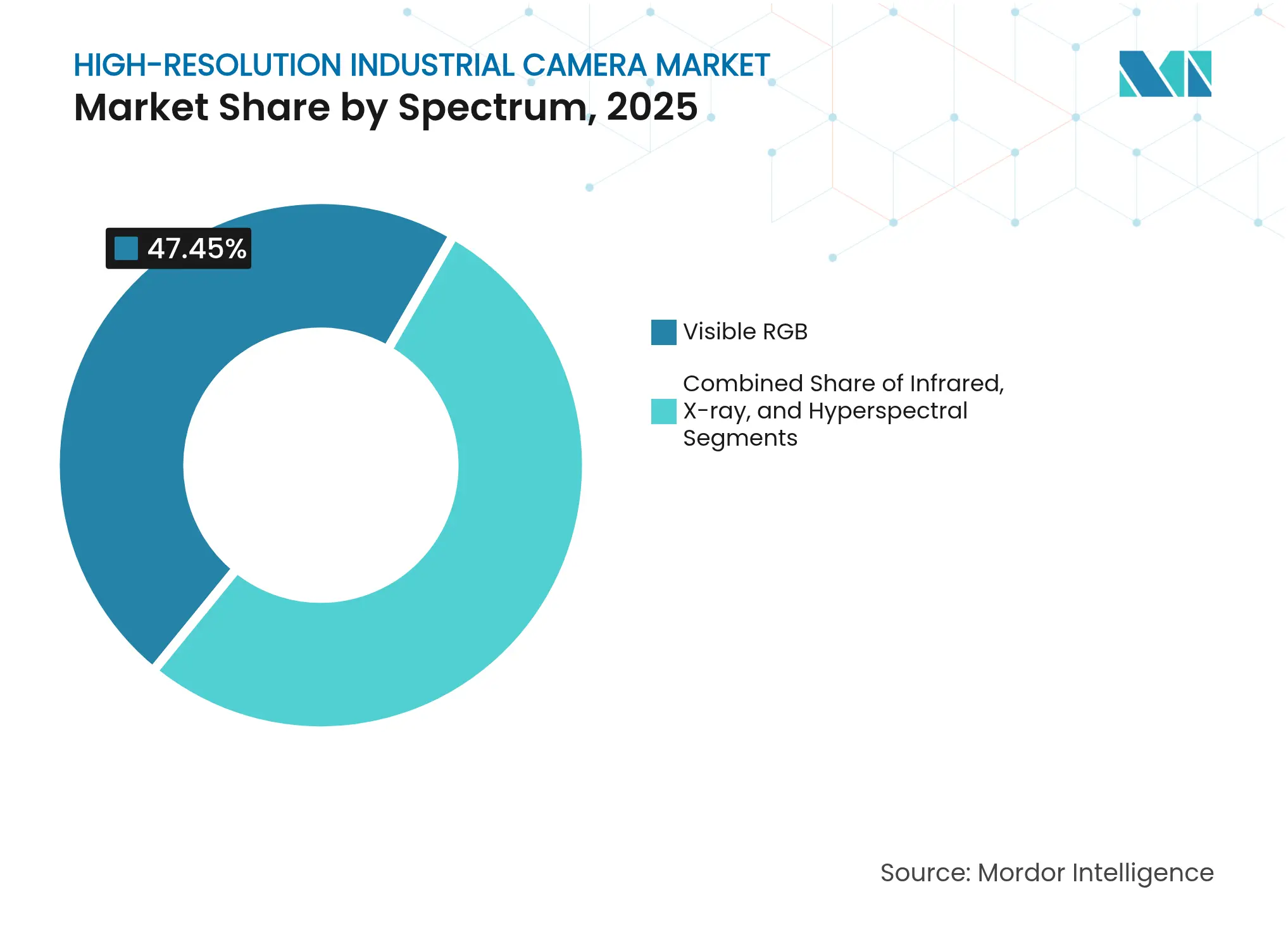

By Spectrum: Infrared Imaging Unlocks Hidden Defects

Visible-light units still anchor the high-resolution industrial camera market because of their cost-efficiency and compatibility with standard lighting. Recent gains in color-linearity and dynamic-range tuning improve surface-finish inspection for automotive coatings and consumer-electronics housings. Short-wave-infrared models, however, are scaling fastest as falling indium gallium arsenide sensor prices reveal moisture ingress, silicon subsurface cracks, and bruise patterns in harvested produce. Multispectral platforms that merge RGB with near-infrared or ultraviolet bands now achieve simultaneous capture, with solutions such as Chromasens’ allPIXA neo-line-scan array offering synchronized RGB + NIR imaging for accelerated conveyor inspection.

Hyperspectral designs spanning 250 - 2,500 nm provide full material fingerprinting for food authenticity and pharmaceutical-tablet coating uniformity. Photonics industry data notes more than 30 contiguous spectral bands in recent line-scan releases. Early adopters report cutbacks in chemical-testing costs and reduced product recalls, positioning multispectral platforms for broader factory deployment once acquisition costs fall further.

Note: Segment shares of all individual segments available upon report purchase

By Frame Rate: Ultra-High-Speed Captures Crucial Microseconds

Frame-rate requirements diverge sharply by task. Cameras rated between 250 and 1,000 fps form the backbone of the high-resolution industrial camera market, giving sufficient temporal acuity for pick-and-place verification and conveyor fault logging without generating unmanageable data volumes. Above this tier, 1,001-10,000 fps instruments capture fluid-dynamics turbulence in inkjet nozzle research, while 10,001-30,000 fps units help visualize explosive bolt separation in aerospace tests.

At the frontier, models exceeding 50,000 fps chronicle micro-fracture propagation and airbag deployment sequences. The i-SPEED 5 family demonstrates 13 Gpixels/s throughput and optional electromechanical shutters for remote calibration, mitigating the illumination challenge posed by microsecond exposure times. Research labs now couple such high-speed streams with FPGA-based compression blocks to contain storage footprints.

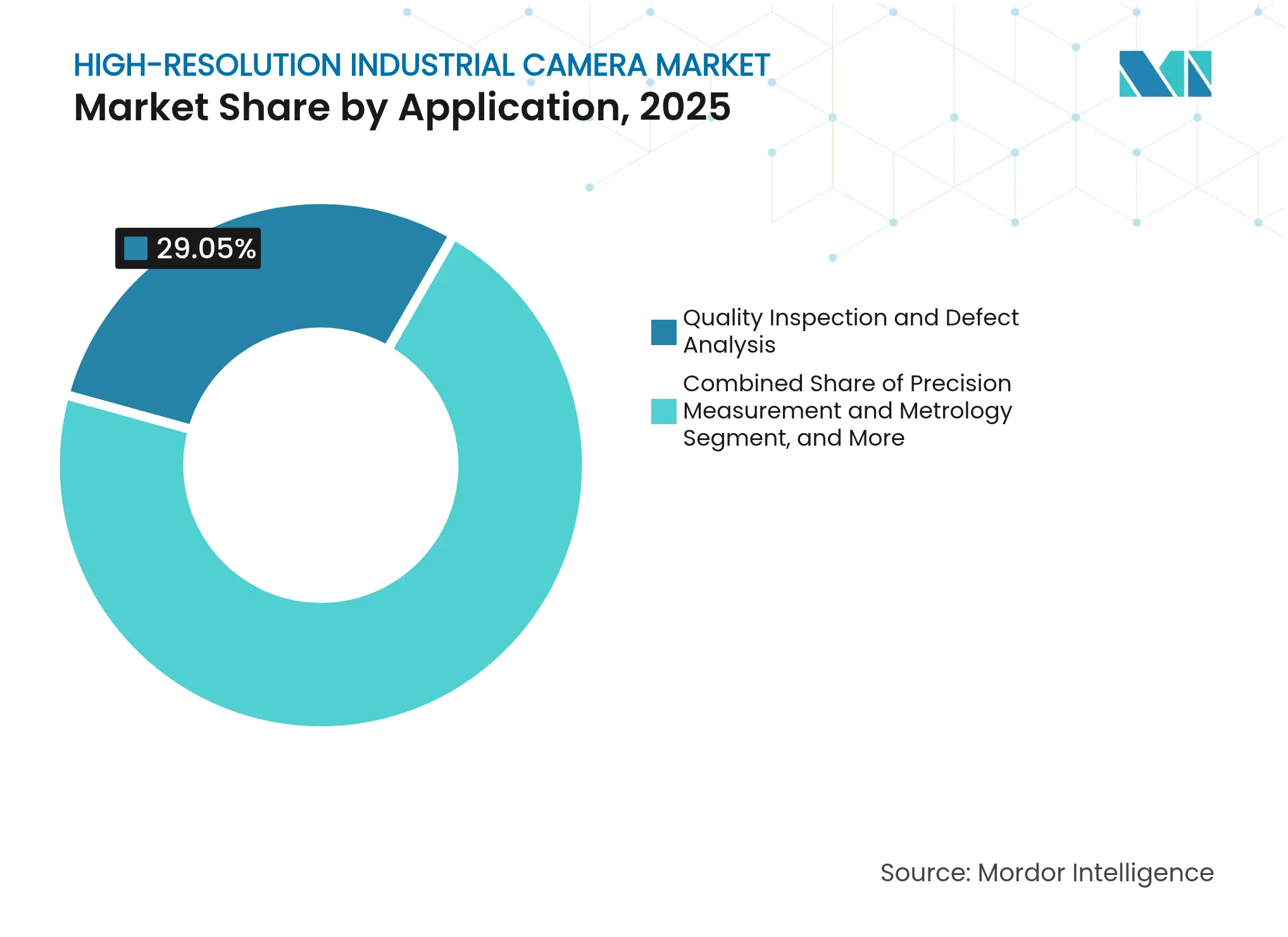

By Application: Robotics Automation Drives Future Growth

Automated optical inspection lines remain the single largest usage cluster within the high-resolution industrial camera market. Inline vision gates compare each product against a golden template and trigger reject diverters in under 30 milliseconds. In contrast, robotics-and-factory-automation installations represent the highest expansion rate as cobots receive vision upgrades that enable bin-picking and fine-pitch screw insertion.

Precision metrology stations use calibrated telecentric optics to achieve micron-level dimensional consistency, replacing contact probes and shrinking cycle times. Surveillance setups inside process plants add analytics such as anomaly detection and PPE compliance, reflecting a convergence between security and manufacturing safety objectives. Academic and corporate R&D groups push technological limits, evidenced by the University of Arizona’s terapixel-per-second demonstrator and the OASIS wall that stitches 298.44 MP streams for immersive analytics.

Note: Segment shares of all individual segments available upon report purchase

By End-use Industry: Medical Systems Accelerate Adoption

Front-end semiconductor fabrication lines and surface-mount assembly plants are still the largest buyers in the high-resolution industrial camera industry. Wafer-level defect mapping, solder-paste height measurement, and die-bond alignment cannot tolerate pixelation or smear; products such as JAI’s Spark-series 189 fps global-shutter models serve this need. Hospitals and device makers now constitute the fastest-growing customer set as minimally invasive surgery, ophthalmology, and high-content cell screening demand precise color rendition and sub-cellular resolution.

Automotive assemblers employ vision stations for body-in-white seam quality and paint-shop particle analysis, while in-cabin driver-monitoring cameras address regulatory mandates for fatigue detection. Aerospace technicians deploy borescope-like high-resolution probes to spot rivet flaws in hard-to-reach fuselage sections. Food-and-beverage producers increasingly adopt hyperspectral inspection to flag foreign objects and classify raw material freshness without destructive sampling.

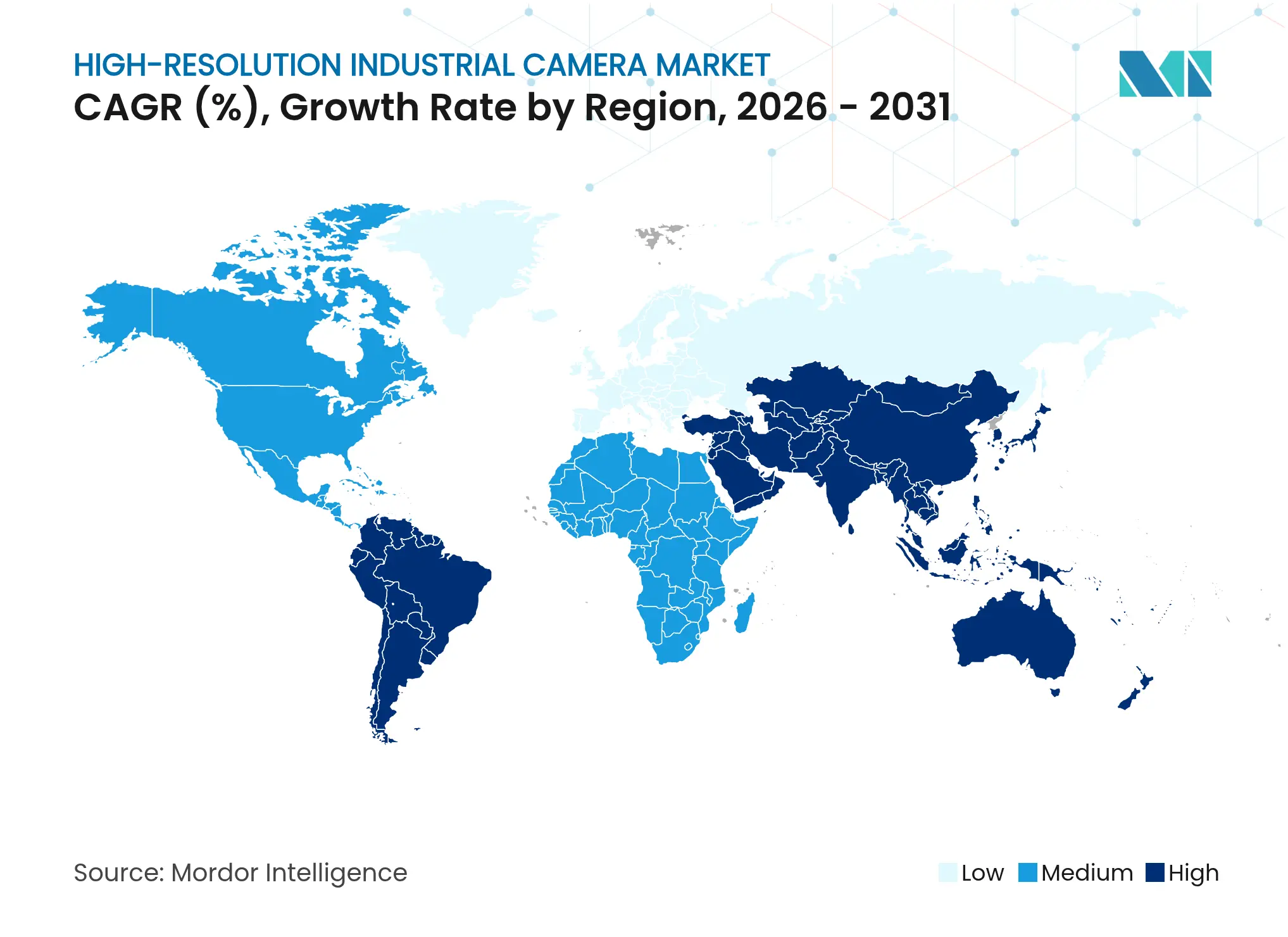

Asia–Pacific commands the largest installed base of high-resolution industrial cameras, reflecting its role as the world’s electronics manufacturing hub. China’s extensive surface-mount technology lines, combined with Japanese and South Korean automotive and display-panel facilities, sustain year-round demand for board-level and line-scan imagers. Regional suppliers benefit from local semiconductor fabs that shorten optics-and-sensor lead times. Yet export-control tightening has prompted Chinese OEMs to develop indigenous solutions, a shift that could reshape long-term sourcing patterns.

The Middle East and Africa, while starting from a lower penetration point, show the most vigorous percentage growth in the high-resolution industrial camera market. Government-backed industrial parks in the United Arab Emirates and Saudi Arabia are specifying advanced machine vision for metals processing, 3D-printed aerospace components, and pharmaceutical packaging lines. Regional integrators partner with European optics firms to bridge skill gaps, although high capital-equipment costs remain a hurdle for small suppliers.

North America and Europe represent mature yet technologically advanced territories where niche, high-performance cameras find receptive buyers. Pharmaceutical clean-rooms, food traceability loops, and advanced automotive crash labs sustain continuous upgrades. Regulatory frameworks on traceability and corporate sustainability accelerate the adoption of vision systems that document each production stage. Local vendors focus on software differentiation, embedding AI algorithms that learn defect libraries without external training datasets.

Market Concentration

Competition in the high-resolution industrial camera market is moderate, with a cluster of multinational incumbents-Cognex, Keyence, Teledyne, Omron and Basler-occupying the upper tier. They bundle cameras with proprietary vision-tool libraries, creating lock-in at the factory-automation system level. Mid-range pricing pressure comes from agile Chinese manufacturers that exploit domestic sensor supply and lower overheads, compelling incumbents to defend margins through feature innovation and service contracts.

Vertical integration is a key theme: vendors are designing custom image signal processors that accelerate convolutional neural networks within the camera body, reducing reliance on host PCs. Acquisitions of filter-fabrication houses and optics specialists provide control over spectral-imaging roadmaps, while firmware updates deliver evolving classification models to installed bases. White-space opportunities lie in multi-spectral and harsh-environment niches; Photron’s FASTCAM Mini CX, for example, pairs high-light-sensitivity ISO 5,000 color operation with HD video for aerospace bolt separation analysis.

Regulation also shapes rivalry. The United States Bureau of Industry and Security eased license rules for lower-risk, high-throughput cameras in early 2025, simplifying exports to allied markets but tightening scrutiny on shipments to certain regions.[4]Justin Kiff, “Revisions to License Requirements for Specific Cameras,” federalregister.gov Vendors now craft regional SKUs compliant with diverse control lists, adding complexity yet opening protected market segments for local partners.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The high-resolution industrial camera market is growing due to increasing demand for precision and automation across industries like manufacturing, automotive, and electronics. Key players such as Basler AG, Teledyne Technologies, and Sony Corporation are driving innovation with advanced imaging technologies. As industries adopt smart factory solutions, the need for high-quality inspection, defect detection, and process optimization is fueling market expansion.

The high-resolution industrial camera market is segmented by spectrum (visible RGB, infrared, x-ray), frame rate (250 to 1,000 FPS, 1,001 to 10,000 FPS, 10,001 to 30,000 FPS, 30,001 to 50,000 FPS, above 50,000 FPS), application (precision measurement, quality inspection, robotics and automation, surveillance, and other applications), end-use industry (electronics and semiconductor, automotive and transportation, medical and life sciences, aerospace and defense, and other end-use industries), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East And Africa). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.