Compact Camera Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

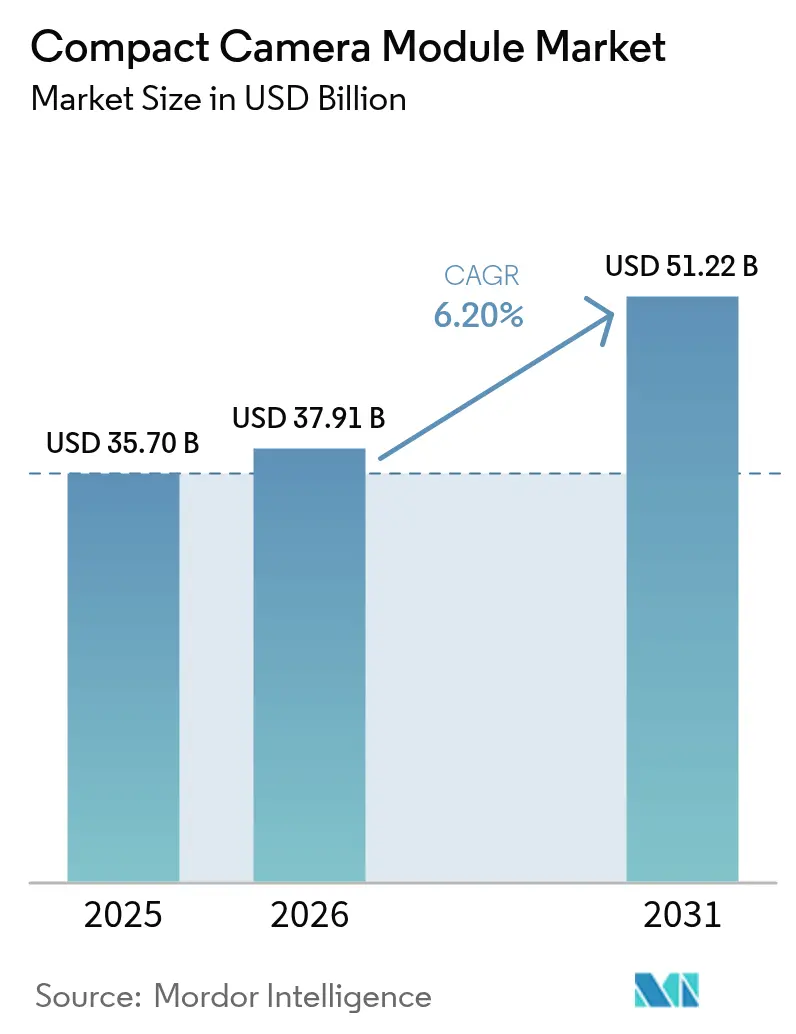

| Market Size (2026) | USD 37.91 Billion |

| Market Size (2031) | USD 51.22 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

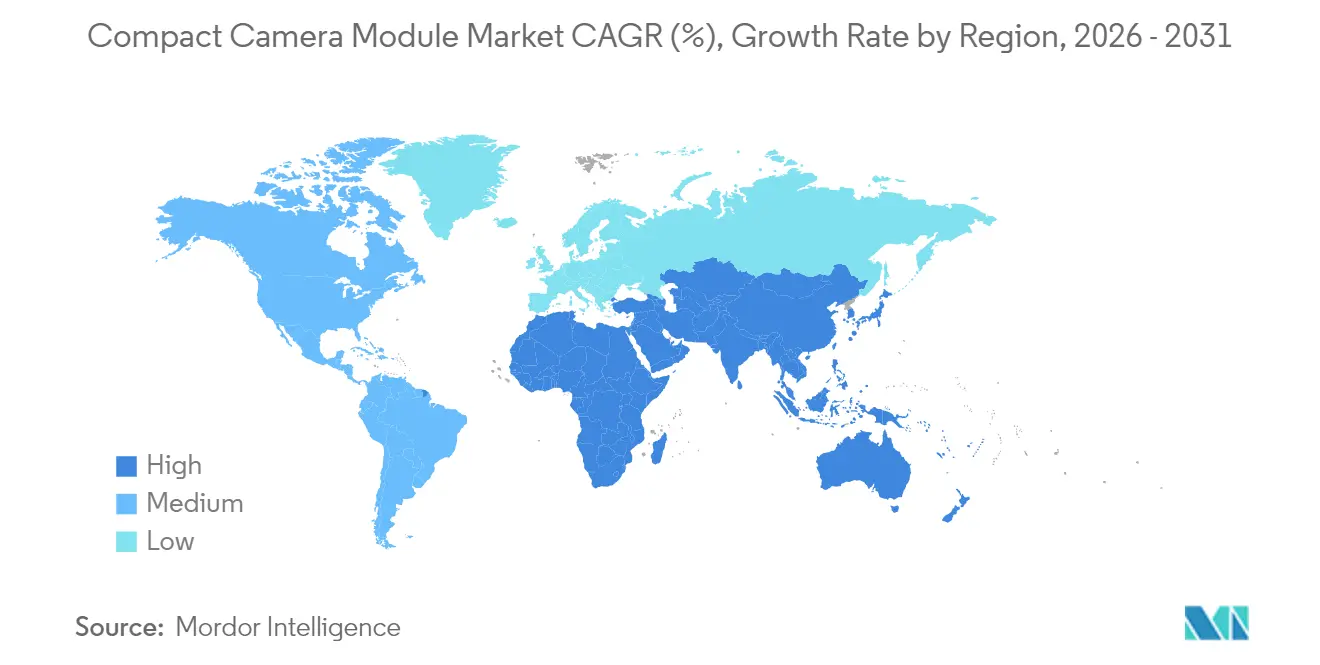

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

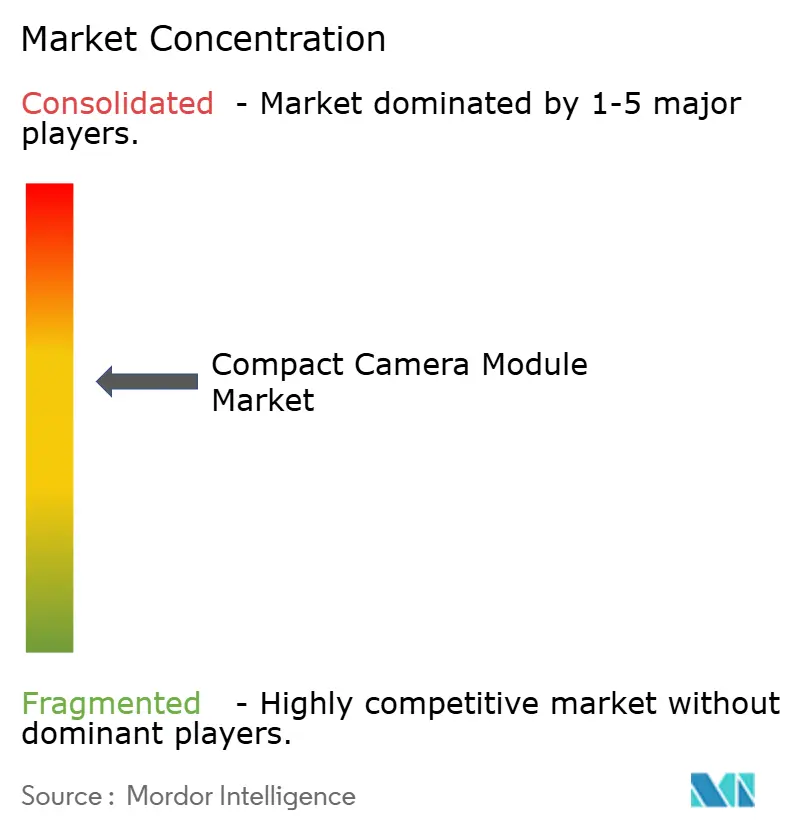

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compact Camera Module Market Analysis by Mordor Intelligence

The compact camera module market size is expected to grow from USD 35.7 billion in 2025 to USD 37.91 billion in 2026 and is forecast to reach USD 51.22 billion by 2031 at 6.20% CAGR over 2026-2031. Growth is being propelled by multi-camera smartphones, regulatory mandates for advanced driver assistance systems (ADAS), and new use cases in extended reality (XR) and industrial automation. Suppliers are shifting from single units to multi-camera arrays that incorporate periscope zoom, under-display sensors, and short-wave infrared (SWIR) capability, elevating both average selling prices and shipment volumes. Asia-Pacific retains the manufacturing hub advantage, while Vietnam’s incentive-backed facilities and Japan’s export controls reshape global supply distribution. Patent litigation, notably around tetraprism zoom lenses, underscores how intellectual property remains a decisive competitive lever. Simultaneously, AI-driven process controls such as LG Innotek’s defect-cutting platform are compressing production costs and improving yield rates, reinforcing competitiveness.

Key Report Takeaways

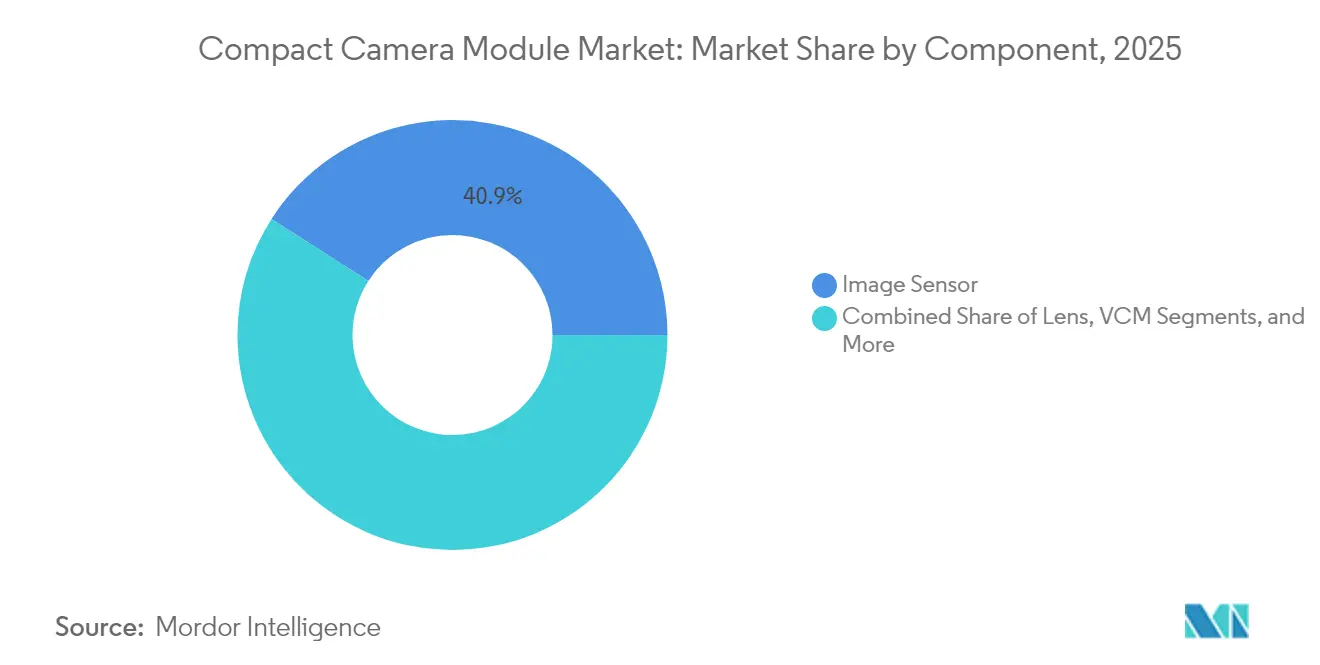

- By component, image sensors led with 40.92% revenue share in 2025, while voice coil motors are expanding at a 7.05% CAGR through 2031.

- By focus type, auto-focus devices held 78.35% of the compact camera module market share in 2025 and are growing at 6.18% CAGR.

- By pixel resolution, the above-48 MP segment is advancing fastest at 7.55% CAGR, whereas the 9–20 MP range retained 38.02% share.

- By application, mobile captured 62.05% of the compact camera module market size in 2025; automotive is projected to grow at 6.55% CAGR to 2031.

- By geography, Asia-Pacific commanded 66.35% revenue share in 2025, while the Middle East & Africa posts the highest 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compact Camera Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-camera smartphones (>50 MP CIS) accelerating demand in China and India | +1.2% | APAC core, global spill-over | Short term (≤ 2 years) |

| ADAS mandates driving surround-view camera installations in EU and United States vehicles | +0.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Industrial and healthcare retrofits with SWIR-enabled CCMs | +0.6% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| XR/AR headsets requiring 6-DOF inside-out tracking cameras | +0.4% | Global, led by North America | Medium term (2-4 years) |

| Adoption of optical under-display selfie modules by Korean OEMs | +0.3% | APAC core, global expansion | Long term (≥ 4 years) |

| Vietnam government incentives for export-oriented CCM assembly | +0.2% | APAC manufacturing shift | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multi-camera smartphones (>50 MP CIS) accelerating demand in China and India

Smartphone makers are standardizing triple and quad-camera setups, multiplying unit demand as each handset now carries three to four compact camera modules instead of a single assembly. Sony’s 50 MP LYT-818 sensor and Samsung’s stacked CIS roadmap intensify competition and compress cost curves, enabling mid-tier devices to adopt high-resolution imaging. Chinese brands use camera specs as primary differentiation, pushing foundries such as SmartSens to scale capacity after USD 225 million Series D funding.

ADAS mandates driving surround-view camera installations in EU and United States vehicles

The EU’s GSR2 rules, effective July 2024, plus forthcoming US FMVSS 127 standards mandate automatic emergency braking and pedestrian detection systems, igniting demand for multi-camera ADAS suites.[1]Autonomous Vehicle International, “New EU safety regulations mandate the use of ADAS,” autonomousvehicleinternational.com Samsung Electro-Mechanics has responded with water-repellent, heated enclosures that secure reliability under harsh conditions. Automotive revenue is projected to outpace the overall compact camera module market at a 13.8% CAGR through 2030.

Industrial and healthcare retrofits with SWIR-enabled CCMs

Sony’s IMX992/993 sensors pair visible and SWIR wavelengths, allowing one module to displace multiple legacy cameras in moisture detection, food inspection, and recycling lines. Colloidal quantum-dot integration via onsemi’s acquisition of SWIR Vision Systems lowers cost barriers, while ams OSRAM’s sub-2.3 mm NanEye modules open endoscopic opportunities. The addressable retrofit market grows as existing machinery upgrades rather than replaces imaging systems entirely.

XR/AR headsets requiring 6-DOF inside-out tracking cameras

Demand for micro-camera arrays able to map depth in real time is rising with the next wave of XR headsets. Meta and Samsung patents describe compact lens barrels, electromagnetic shielding, and distributed Bragg reflectors that underpin lightweight designs. Sony’s 0.44-inch OLED microdisplay sets size benchmarks that indirectly escalate precision needs for companion camera modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Japan-China CIS export controls tightening tier-2 supply | -0.9% | APAC core, global disruption | Short term (≤ 2 years) |

| Low yield in wafer-level optics for 8K video modules | -0.7% | Global manufacturing, APAC hub | Medium term (2-4 years) |

| Patent wars over periscope-zoom actuators | -0.5% | Global, premium smartphones | Long term (≥ 4 years) |

| Copper-driven shortfall in automotive-grade VCSEL coils | -0.3% | Global automotive chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Japan-China CIS export controls tightening tier-2 supply

Tokyo’s updated critical materials list complicates shipments of advanced CMOS components to Chinese plants, forcing companies such as Toppan to relocate certain lines while Vietnamese incentives lure new projects. The transition period creates cost swings and planning uncertainty throughout the compact camera module market supply chain.

Low yield in wafer-level optics for 8K video modules

Hybrid wafer bonding and 3D stacking push defect rates higher as pixel sizes shrink. Process engineers face trade-offs between inspection intensity and production cost, limiting 8K-ready module availability and elevating price premiums. Equipment vendors highlight void formation and film uniformity as persistent bottlenecks that restrict near-term supply elasticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Image Sensors Anchor Revenue, VCMs Lead Growth

Image sensors delivered 40.92% of 2025 revenue, underscoring their role as the value core of the compact camera module market. Sony’s 3D-stacked architecture enables system miniaturization and premium pricing, while Apple’s multivendor strategy injects Samsung into a domain long dominated by Sony. Lens makers pursue hybrid glass-plastic blends to withstand extreme automotive temperatures, and assembly houses confront margin pressure as integration complexity rises.

Voice coil motors (VCMs) for autofocus and optical image stabilization register the quickest 7.05% CAGR, driven by vehicle vibration demands and multi-camera smartphones. The segment’s momentum shows how downstream requirements ripple back to components, reshaping the compact camera module market investment priorities. The supply shift also mitigates single-supplier risk, smoothing delivery to handset and vehicle OEMs.

By Focus Type: Auto-Focus Extends Dominance Amid Feature Creep

Auto-focus modules captured 78.35% in 2025 and continue to gain at 6.18% CAGR, intertwined with premium photography features that require rapid, precise focal adjustment. LG Innotek’s tetraprism lens for iPhone 16 Pro exemplifies how flagship requirements cascade through the focus chain. Periscope-zoom actuator disputes, however, expose vulnerability to intellectual-property breakdowns.

Fixed-focus modules still ship into budget handsets, wearable sensors, and certain industrial devices where simplicity and reliability trump optical flexibility. Yet even in these arenas, algorithmic enhancements such as AI-based denoising elevate baseline performance, indirectly sustaining the compact camera module market momentum.

By Pixel Resolution: Ultra-High Resolution Accelerates Above 48 MP

Sensors above 48 MP advance at 7.55% CAGR, buoyed by Samsung’s ISOCELL HP9 200 MP telephoto device that offers stronger light capture while preserving compactness. As a result, handset OEMs race to market extreme-resolution flagships, creating halo effects across lower tiers.

The 9–20 MP range, still the sweet spot for mainstream balancing of cost and quality, holds 38.02% share. Market dynamics point to gradual migration upward as image pipelines and storage constraints ease. Yet lens diffraction limits and processing overhead may cap pixel escalation, reinforcing differentiation via computational photography rather than sheer counts.

By End-Use Application: Mobile Leadership Faces Automotive Upswing

Smartphones account for 62.05% of the compact camera module market, but growth is moderating as global penetration peaks. Manufacturers seek new revenue in foldable phones and under-display modules while preserving unit volumes.

Automotive modules, advancing at 6.55% CAGR, stand out as the breakout opportunity. Surround-view systems, driver monitoring, and sensor fusion architectures multiply camera counts per vehicle, raising content value per unit. Meanwhile, healthcare mini-modules and industrial SWIR retrofits create specialized niches that reward suppliers able to meet certification and reliability thresholds.

Geography Analysis

Asia-Pacific maintained 66.35% share in 2025 due to integrated supply chains spanning wafer fabrication to final assembly. China spearheads investment in advanced sensors, South Korea innovates in AI-optimized production, and Vietnam scales with incentive-laden facilities that diversify risk away from concentrated coastal Chinese hubs.

North America and Europe form premium application centers. The EU’s GSR2 regulation secures long-term demand for automotive camera arrays, while US firms pioneer XR camera technologies through patent-heavy R&D.

The Middle East and Africa, though starting from a smaller base, exhibit the fastest 7.12% CAGR as smartphone penetration and vehicle safety rules rise. Investment in 5G networks and assembly clusters supports steadily improving ecosystem maturity, signaling incremental contribution to the compact camera module market over the forecast horizon.

Value Chain Analysis

The compact camera module value chain starts with upstream semiconductor and materials inputs, notably CMOS image sensors (Sony, Samsung, OmniVision), optical elements (lens stacks, wafer-level optics, IR-cut filters), and motion components such as voice coil motors for AF/OIS. Midstream players then integrate these parts into miniaturized assemblies through precision alignment, packaging, calibration, and reliability testing, with production largely concentrated across East Asia, including China, South Korea, Taiwan, and increasingly Vietnam as export-oriented assembly footprints expand.

Downstream demand is shaped by smartphone OEMs that pull multi-module arrays at scale and by automotive programs that require higher-grade validation (thermal, vibration, and ingress protection) for ADAS and in-cabin systems. Bottlenecks cluster around advanced sensor substrates, yield management in wafer-level optics for high-resolution and 8K-class modules, and the need for safety-stock buffers at OEM hubs when just-in-time replenishment is disrupted by geopolitics and export controls, including Japan-linked constraints on advanced CMOS component flows into a China-centric supply base.

Competitive Landscape

Industry leadership is shared among a handful of vertically integrated giants that leverage optics know-how and deep patent portfolios. LG Innotek’s AI-enabled defect reduction platform slashes scrap rates by 90%, preserving margin amid pricing pressure.[3]LG Innotek, “LG Innotek solidifying its position as a leader in camera modules through innovative AI processes,” lginnotek.com Samsung Electro-Mechanics exploits material advances to deliver weather-proof automotive modules, leveraging synergies across its electronics divisions.[4]Samsung Electro-Mechanics, “Samsung Electro-Mechanics plans to mass produce ‘Weather Proof’ automotive camera modules,” samsungsem.com

Patent conflicts remain pivotal. Largan’s suit to defend tetra-prism exclusivity with Apple showcases how courtroom outcomes can alter supplier rosters overnight. White-space entrants such as ams OSRAM and onsemi exploit SWIR and medical niches where incumbents lack specialized expertise.

Robotics emerges as a diversification avenue: Samsung and LG aim to capture humanoid robot vision modules, an adjacent arena projected to scale from KRW 40 billion in 2026 to KRW 4.7 trillion by 2029, broadening revenue sources beyond plateauing smartphone volumes.

Compact Camera Module Industry Leaders

Chicony Electronics Co. Ltd

Cowell E Holdings Inc.

Fujifilm Corporation

LG Innotek Co. Ltd

LuxVisions Innovation Limited (Lite-On Technology Corporation)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automotive camera content is expanding beyond mobile, supported by regulatory-driven ADAS adoption and the shift toward in-cabin monitoring. Evidence of productization includes LG Innotek disclosing automotive RGB-IR in-cabin camera modules and showcasing an under-display camera concept for instrument clusters at CES 2026, which indicates camera modules being engineered for concealed, always-on sensing inside vehicles rather than only external perception. This supports whitespace for suppliers able to industrialize high-reliability optics, heated and weather-proof housings, and low-light performance while meeting OEM qualification cycles.

Industrial, healthcare, and security applications provide a second opportunity layer where compactness and spectral capability matter more than smartphone-style cost optimization. SWIR-enabled modules (for example, Sony IMX992/993-class sensing and onsemi capabilities built via SWIR Vision Systems) enable retrofits in inspection, moisture detection, recycling, and medical imaging, while edge AI integration at the module or camera level supports real-time analytics in smart security and fleet management. Across these use cases, vertical integration in optics, actuators, and calibration software, along with IP control in periscope and under-display architectures, remains a key lever for differentiation as assembly capacity shifts within Asia-Pacific (including Vietnam incentive-backed expansion) to reduce single-country concentration risk.

Recent Industry Developments

- May 2026: Chicony Electronics discussed a rebound in first-quarter 2026 performance, citing a shift toward higher-end mixes including imaging-related products. The update reinforces a broader move among ODMs toward value-added vision hardware as differentiation increases in security and industrial endpoints.

- December 2025: LG Innotek announced a next-generation under-display camera for automotive instrument clusters and positioned the concept for visibility at CES 2026. The development supports concealed in-cabin sensing designs and extends the automotive camera module roadmap beyond conventional visible cameras mounted in the cabin.

- December 2024: LG Innotek disclosed its automotive RGB-IR in-cabin camera module initiative as part of scaling its automotive sensing business. RGB-IR architectures strengthen driver and occupant monitoring performance under challenging lighting, raising the technical bar for module suppliers targeting automotive qualification.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from compact camera modules sold for integration into devices, where the module is a packaged camera unit built around an image sensor and optics, and then supplied to OEMs and integrators for end products.

Scope exclusions: standalone digital cameras and replacement retail accessories are excluded unless they are sold as compact modules intended for device integration.

Segmentation Overview

- By Component

- Image Sensor

- Lens

- Camera Module Assembly

- VCM (AF and OIS)

- By Focus Type

- Auto-Focus

- Fixed-Focus

- By Pixel Resolution

- Upto 8 MP

- 9-20 MP

- 21-48 MP

- Above 48 MP

- By End-use Application

- Mobile

- Consumer Electronics (Ex-Mobile)

- Automotive

- Healthcare

- Security and Surveillance

- Industrial

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Southeast Asia

- Rest of Asia-Pacific-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to anchor it in observable electronics and automotive signals before assumptions were applied. For demand context by region, public datasets and official sources such as UN Comtrade trade statistics, International Telecommunication Union device connectivity indicators, World Bank macro series, and OECD industrial output data were reviewed.

On the supply and technology side, we also reviewed US Patent and Trademark Office publications, peer-reviewed imaging and optics journals, and regulator and road safety portals where camera related rules are discussed for vehicles and surveillance use cases. Company annual reports, filings, and investor presentations were reviewed to understand product mix shifts, including autofocus adoption and higher megapixel trends, and to sanity check pricing direction. For added consistency, a paid subscription database was referenced for company financials and news timelines, and another paid patent tool was used to screen camera module filings. The sources listed here are illustrative, and many other public documents and datasets were also consulted for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary inputs were collected from module supply chain participants, device OEM facing roles, component specialists, and downstream buyers who track camera adoption across mobile, consumer electronics, automotive, healthcare, industrial, and security use cases. We covered APAC, EMEA, and the Americas so regional mix, pricing behavior, and demand timing differences could be corrected in the model before final totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 19% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where device build volumes and adoption rates were reconstructed by end use, then translated into module value using typical camera counts per device and blended ASP ranges. To keep the model practical, we focused on repeatable inputs, including smartphone and consumer electronics shipment direction, vehicle camera penetration for ADAS and in cabin monitoring, the mix shift from fixed focus to autofocus, the share of higher pixel resolutions, and the typical lens and VCM content per module.

After the first pass, totals were corroborated using selective bottom-up approximations, including roll ups from sampled supplier revenue disclosures, channel checks on module pricing movements, and simple volume times ASP builds for a few high volume device categories. Where a bottom-up view was incomplete, gaps were handled by applying conservative regional mix shares that were agreed in interviews, then stress tested so no single assumption dominated the outcome.

For forecasting, scenario analysis was used, then tightened with a light multivariate regression on demand drivers that had stable historical behavior, such as device shipments, auto production, and camera penetration per platform. Final growth paths were adjusted only after primary experts confirmed realistic timing for technology shifts like multi camera setups, autofocus take rates, and higher resolution adoption.

Data Validation & Update Cycle

Outputs were checked against independent signals, including shipment direction by device category, regional manufacturing momentum, and the implied ASP trend from the model. Differences were investigated before sign off. When unusually sharp jumps appeared, assumptions were revisited, and follow up questions were sent back to a few respondents to confirm whether the change reflected reality or a scope or timing mismatch.

A multi step internal review is followed so market totals, growth rates, and key drivers remain consistent with the stated definition and coverage. Reports are refreshed annually, and interim updates are made if a material event affects device production, trade flow, or pricing, after which a final analyst pass is completed right before delivery so clients receive the latest updated view.

Mordor Intelligence's Compact Camera Module Market Size Measured Against Other Published Estimates

Published numbers for compact camera modules can vary because the boundary between a camera module, a broader camera components bundle, and even device level imaging value is not always treated the same way across publishers. Differences also come from the chosen base year, whether values are reported as shipment based revenue or installed content value, and how fast pricing is assumed to move as megapixels and autofocus features change.

In this study, the biggest gap drivers are usually scope and the evidence used to keep assumptions realistic. Some estimates fold in adjacent imaging components beyond the module build, or they apply aggressive unit growth without reconciling it to device shipments and regional production signals, which can push the headline number higher than what the demand pool supports.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 37.91 B (2026) | |

| Industry Publisher A | USD 39.41 B (2024) | Uses a different base year and mixes revenue with output reporting in parts of the analysis, which can shift implied ASPs when unit assumptions are carried into value forecasts. |

| Global Consultancy B | USD 66.20 B (2023) | Applies a much broader value pool that appears to capture more imaging content around the module, and the growth path is set at a higher level that is less tightly reconciled to device shipment direction. |

Device shipment direction, camera penetration per end use, and the implied ASP trend are the checks that keep Mordor Intelligence's estimate tied to the compact module demand pool, which is why the spread narrows once scope and pricing logic are aligned. Overall, the benchmark table shows that year selection and what is counted as module value explain most of the difference, and our approach stays traceable because each step maps back to clear volumes, mixes, and price assumptions.

Key Questions Answered in the Report

What is the current size of the compact camera module market?

The market is valued at USD 37.91 billion in 2026 and is projected to reach USD 51.22 billion by 2031.

Which region holds the largest share of the compact camera module market?

Asia-Pacific commands 66.35% of global revenue, owing to its integrated manufacturing ecosystem.

What are the fastest-growing application areas for compact camera modules?

Automotive ADAS systems lead growth at a 6.55% CAGR, followed by industrial and healthcare SWIR retrofits.

How are export controls affecting supply chains?

Japan’s tighter CIS export rules are prompting suppliers to diversify toward Vietnam and other Southeast Asian hubs, introducing short-term cost volatility.

What technology trend will shape future design priorities?

The shift toward multi-camera arrays with periscope zoom, under-display sensors, and SWIR functionality is redefining module architectures and supplier roadmaps.

Page last updated on: