Antidiuretic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

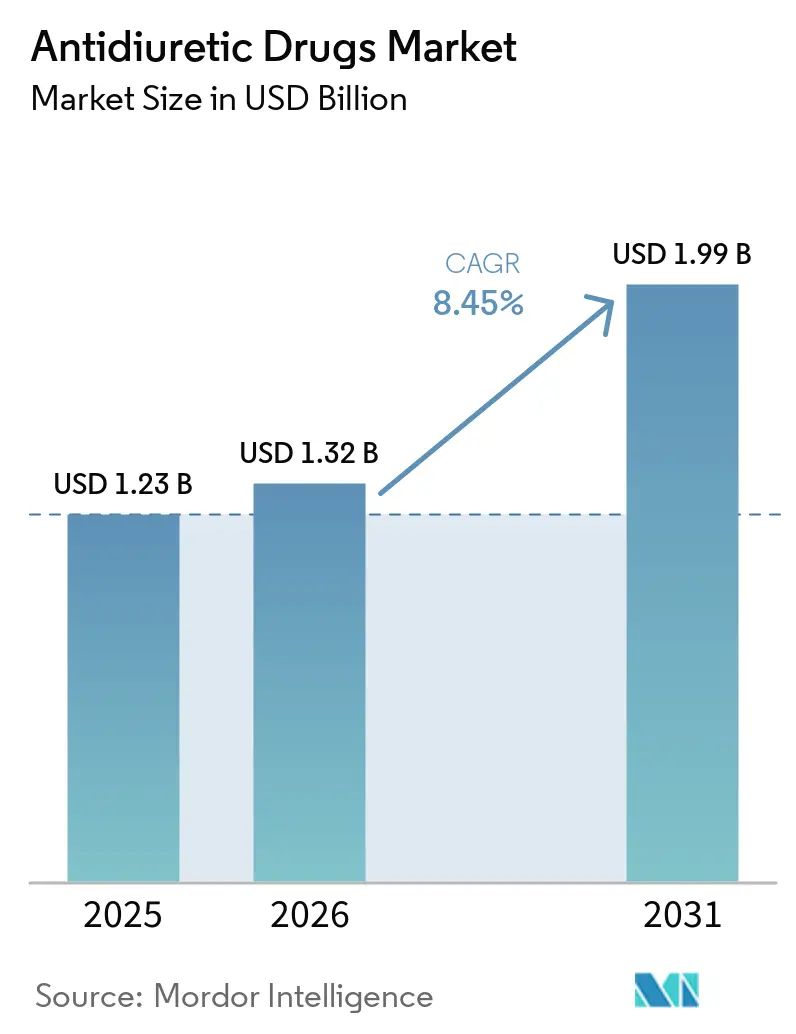

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antidiuretic Drugs Market Analysis by Mordor Intelligence

The Antidiuretic Drugs Market size is projected to be USD 1.23 billion in 2025, USD 1.32 billion in 2026, and reach USD 1.99 billion by 2031, growing at a CAGR of 8.45% from 2026 to 2031.

The antidiuretic drugs market is moving beyond its earlier dependence on hospital-led vasopressin demand and is building a broader base in chronic outpatient care. A tighter diagnostic pathway after the shift to arginine vasopressin deficiency is helping the antidiuretic drugs market identify patients earlier and start therapy with less delay in routine practice. Aging-related nocturia is widening the treated population and is giving the antidiuretic drugs market a steadier demand profile that extends well past rare endocrine care alone. Patent expiry and generic entry are lowering treatment costs in several mature markets, which is supporting volume expansion even as branded margins come under pressure in the antidiuretic drugs market. This leaves the antidiuretic drugs market open to companies that can balance low-cost supply, route-specific convenience, strong monitoring support, and reliable hospital availability.

Key Report Takeaways

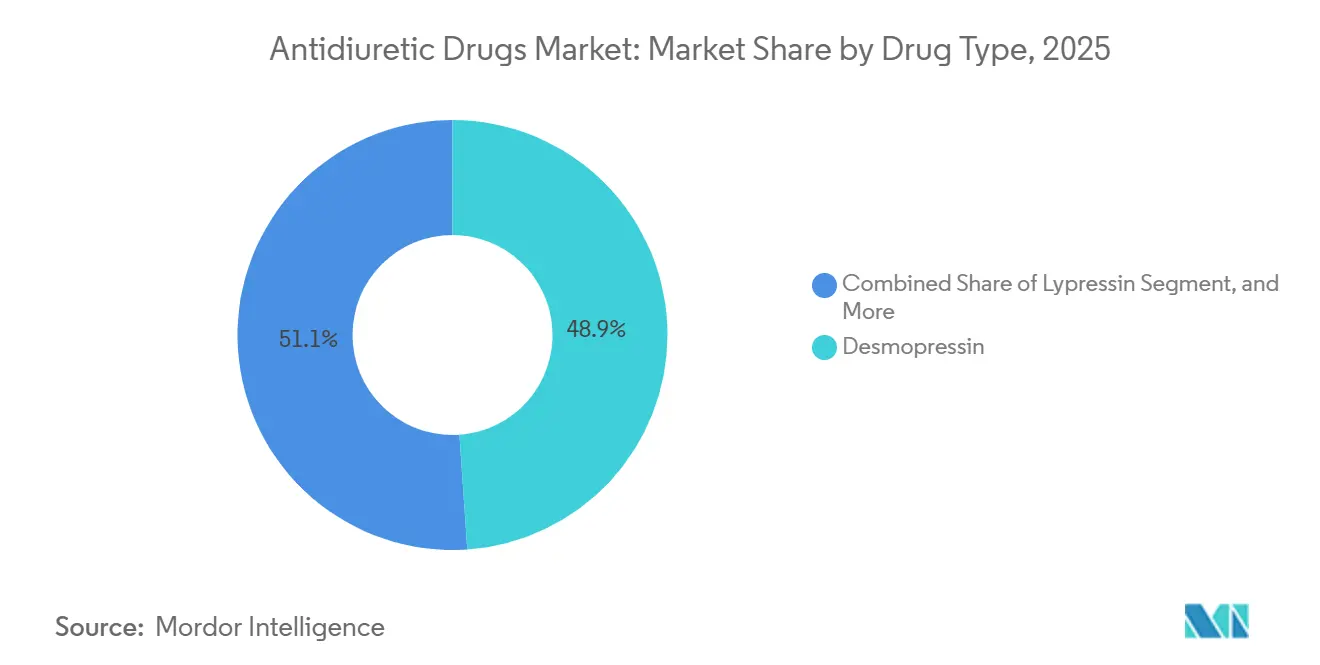

- By drug type, desmopressin held 48.9% of the market in 2025, and lypressin is projected to expand at 8.8% CAGR through 2031.

- By route of administration, oral formulations accounted for 39.6% of the antidiuretic drugs market size in 2025, and injectable formulations are projected to grow at 8.5% CAGR through 2031.

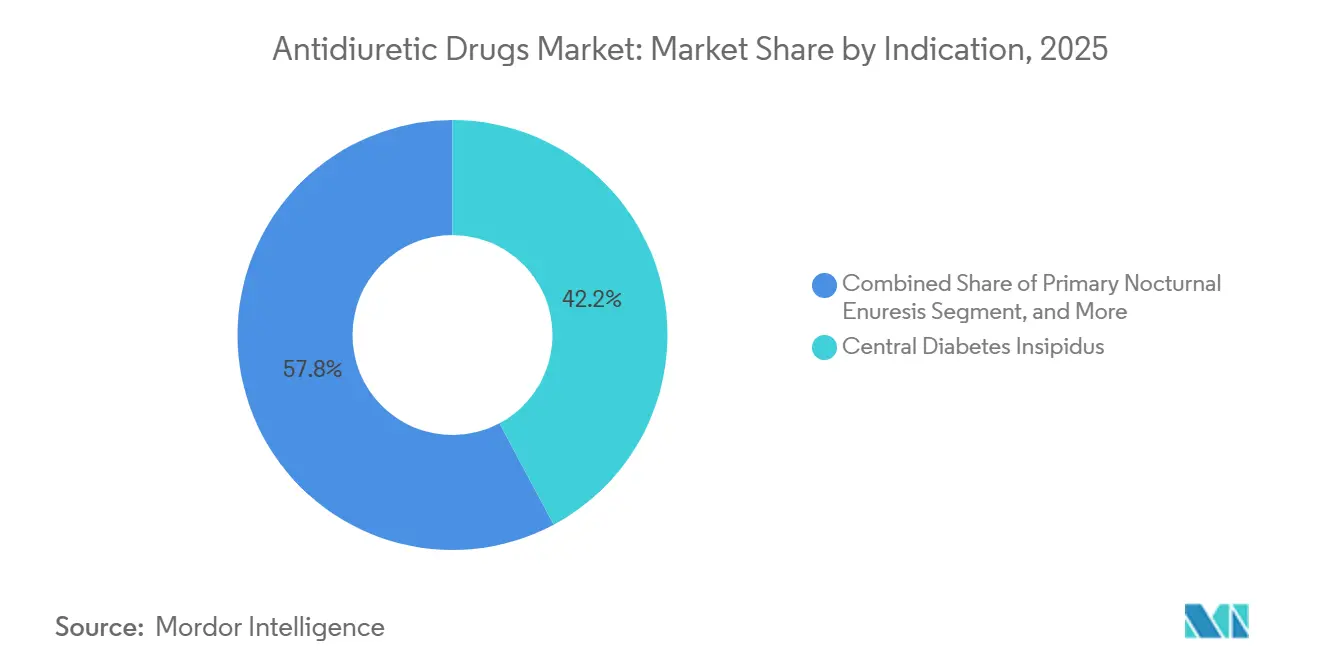

- By indication, central diabetes insipidus represented 42.2% of the market in 2025, and nocturia and nocturnal polyuria are projected to grow at 9.5% CAGR through 2031.

- By end user, hospitals held 44.3% of the market in 2025, and homecare settings are projected to expand at 10.8% CAGR through 2031.

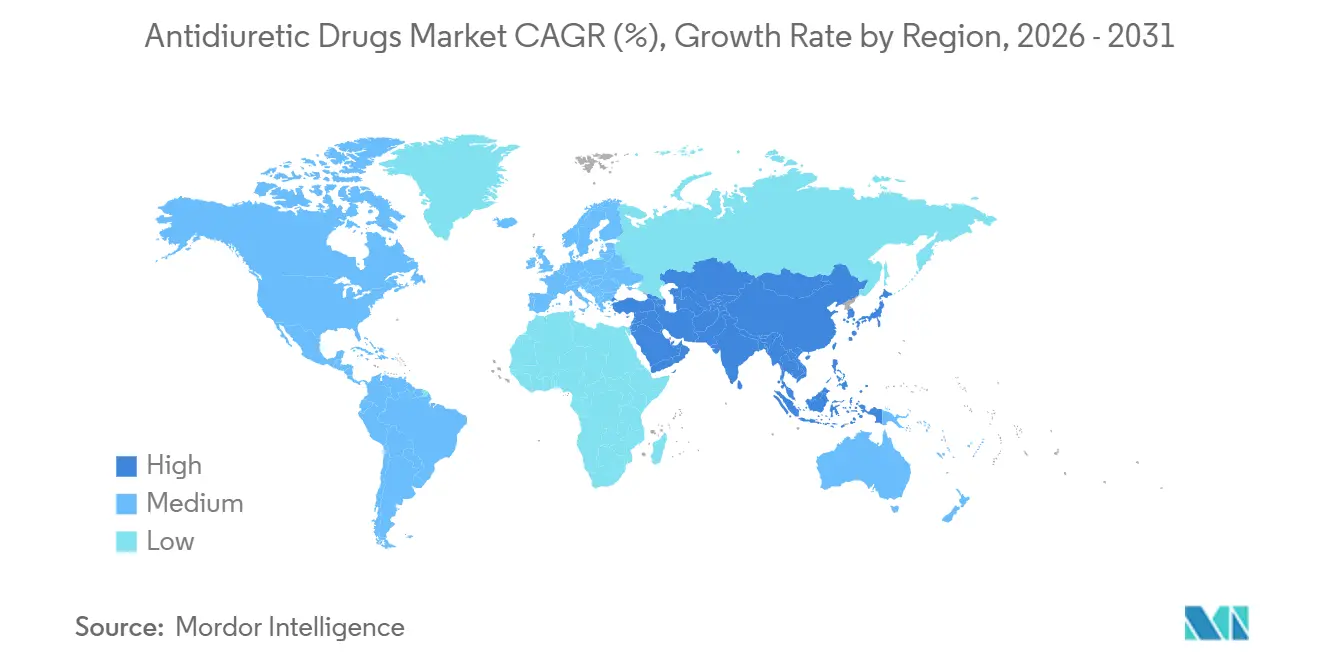

- By geography, North America held 38.4% of antidiuretic drugs market share in 2025, and Asia-Pacific is projected to grow at 9.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antidiuretic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Diagnosis Of AVP-Deficiency Disorders | +2.5% | Global, with early gains in North America, EU, and Japan | Medium term (2-4 years) |

| Aging-Linked Nocturia Burden | +1.8% | Global, APAC core including Japan, South Korea, and Australia, with spillover to MEA | Long term (≥ 4 years) |

| Generic Launches Expanding Access | +1.5% | North America and EU, with emerging market spillover to India and Southeast Asia | Short term (≤ 2 years) |

| Septic Shock Guideline Support For Vasopressin | +1.2% | Global, with highest impact in North America, EU, and APAC ICU infrastructure | Medium term (2-4 years) |

| Post-Pituitary Surgery AVP-Deficiency Case Capture | +0.8% | North America and EU, with early gains in China and Japan | Medium term (2-4 years) |

| Copeptin-Led Diagnostic Upgrade | +0.5% | EU and North America, with early-stage adoption in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Diagnosis Of AVP-Deficiency Disorders

Higher diagnosis is expanding the treatable pool in the antidiuretic drugs market. The change in clinical language from central diabetes insipidus to arginine vasopressin deficiency has sharpened diagnostic focus and reduced confusion in endocrine practice, which is improving case recognition in regular care pathways.[1]Cihan Atila, Irina Chifu, Juliana B. Drummond, et al., “A Novel Diagnostic Score for Diagnosing Arginine Vasopressin Deficiency (Central Diabetes Insipidus) or Primary Polydipsia with Basal Laboratory and Clinical Parameters,” The Lancet Diabetes & Endocrinology, thelancet.com A 2025 study in The Lancet Diabetes & Endocrinology developed and validated a basal clinical probability score that combined plasma sodium, osmolality, copeptin, and symptom features, and it diagnosed AVP-D in 75% of patients without dynamic stimulation testing. AVP-D remains a low-prevalence condition, yet real-world case capture is still below epidemiological expectations, so each upgrade in diagnostic protocol can directly widen the treated base for desmopressin use in the antidiuretic drugs market. Faster diagnosis also changes the care path because patients can move to treatment earlier, which increases treated patient-days over a full year. This helps the antidiuretic drugs market build growth from better identification, not only from a rise in disease prevalence.

Aging-Linked Nocturia Burden

Aging-linked nocturia is a major source of expansion for the antidiuretic drugs market. A 2024 review in Tzu Chi Medical Journal reported that nocturia prevalence exceeds 50% in adults older than 80, which shows how strongly demand is tied to population aging.[2]Tien-Lin Chang and Hann-Chorng Kuo, “Nocturia, Nocturnal Polyuria, and Nocturnal Enuresis in Adults: What We Know and What We Do Not Know,” Tzu Chi Medical Journal, pmc.ncbi.nlm.nih.gov The same review noted that direct healthcare costs tied to nocturia-related falls and injuries in the United States reached USD 1.5 billion annually, which keeps the condition visible to health systems and prescribers. This demand driver is stronger than a simple volume effect because older populations generate a repeat need for monitoring, follow-up, and long-term therapy decisions around nocturnal polyuria. As Japan and South Korea continue to age, primary care and urology settings are likely to record more formal nocturia diagnoses instead of treating the condition as an unstructured quality-of-life complaint. That shift gives the antidiuretic drugs market a broader referral base and a steadier prescription flow outside specialist endocrine centers.

Generic Launches Expanding Access

Generic launches are widening access across the antidiuretic drugs market. Aurobindo Pharma received final FDA approval in March 2024 for desmopressin acetate tablets in 0.1 mg and 0.2 mg strengths, and the products were approved as AB-rated generic equivalents to DDAVP Tablets. Lower-priced generic entry is expanding outpatient use in insured markets because payers and pharmacies can move patients toward less expensive chronic therapy options with limited disruption. Ferring reported that Minirin sales declined 6% at constant exchange rates in 2024, and the company linked part of that decline to generic entry in Western Europe and Canada.[3]Ferring Pharmaceuticals, “Annual Report 2024,” Ferring Pharmaceuticals, ferring.com This creates a two-way commercial effect in the antidiuretic drugs market because lower prices can bring more patients into therapy even when legacy branded products lose pricing power. The result is a market that is becoming more volume-driven, especially in segments where long-term maintenance use matters more than brand distinction alone.

Septic Shock Guideline Support For Vasopressin

Guideline support is reinforcing vasopressin demand on the hospital side of the antidiuretic drugs market. The Surviving Sepsis Campaign updated its international sepsis guidance in March 2026 and recommended adding vasopressin to norepinephrine for adults with septic shock who are receiving escalating catecholamine doses. The same guideline recommended against terlipressin for septic shock, which further strengthened vasopressin’s role as the main non-catecholaminergic adjunct in this setting. Japan’s sepsis guideline framework also supported vasopressin as a second-line vasopressor, which gives this demand driver relevance outside North America and Europe. Once hospitals update formularies and ICU protocols around these recommendations, procurement becomes more stable and less dependent on individual physician preference. That gives the antidiuretic drugs market a durable institutional demand layer even as the outpatient desmopressin business grows faster.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyponatremia Monitoring Burden And Boxed Warnings | -1.2% | Global, with highest impact in North America and EU where pharmacovigilance standards are strictest | Short term (≤ 2 years) |

| Limited Affordability In Chronic-Use Markets | -0.8% | South Asia, Southeast Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Vasopressin Injection Shortages And Back-Order Risk | -0.5% | North America, with limited spillover to EU | Short term (≤ 2 years) |

| Route-Specific Adherence And Administration Frictions | -0.4% | Global, most pronounced in pediatric and elderly cohorts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyponatremia Monitoring Burden And Boxed Warnings

Hyponatremia monitoring remains the clearest brake on the antidiuretic drugs market. The FDA boxed warning for desmopressin acetate requires serum sodium to be normal before treatment starts, then checked within 7 days, at around 1 month, and periodically after that. The label also calls for closer observation in people aged 65 or older and in patients whose clinical profile raises sodium-related risk, which makes routine prescribing more cautious in older populations. This is a meaningful commercial issue because the same elderly patients who carry higher safety concerns also represent the most active nocturia population. Prescribers therefore face a clear tradeoff between symptom relief and the follow-up burden that safe treatment requires. Until monitoring becomes easier or confidence improves in lower-risk patient selection, this safety framework will keep part of the antidiuretic drugs market from converting awareness into prescriptions.

Vasopressin Injection Shortages And Back-Order Risk

Supply fragility is still disrupting parts of the antidiuretic drugs market. The U.S. Pharmacopeia placed vasopressin injection on its 2024-2025 Vulnerable Medicines List as an essential injectable with elevated shortage risk, which underscores the product’s supply sensitivity. ASHP continued to list desmopressin acetate nasal spray as an active shortage in May 2026, showing that route-specific access issues remain unresolved in the U.S. supply chain. The FDA’s calendar year 2024 shortage report also showed that even with lower overall new shortages, vasopressin injection still remained on the active list. These conditions make supply reliability a competitive variable in its own right, not just an operational concern. Manufacturers with multiple production sites, stronger inventory planning, and broader formulation coverage are therefore better positioned in the antidiuretic drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Desmopressin Leads On Breadth While Lypressin Expands From A Small Base

Desmopressin accounted for 48.91% of the market in 2025 and remained the clear leader by drug type. That lead reflects its use across AVP-D, primary nocturnal enuresis, nocturia, nocturnal polyuria, and selected bleeding-related settings, which gives it a wider clinical base than competing classes. It also remains the best-established chronic therapy option in the antidiuretic drugs market because endocrinology and urology pathways are already built around it. Its V2 receptor selectivity keeps the therapeutic focus on antidiuretic action without the pressor effect seen with native vasopressin, which supports its long-standing role in routine care. The class still benefits from broad familiarity among specialists, general practitioners, and hospital teams, and that familiarity reduces switching pressure when new products arrive.

Lypressin is projected to grow at 8.84% CAGR through 2031, which makes it the fastest-growing drug type in this antidiuretic drugs market. Its growth is coming from a small base, yet it is gaining attention in narrower patient cohorts where nasal delivery and tolerability considerations shape treatment choice more heavily. Vasopressin continues to command meaningful hospital revenue because septic shock protocols still support its use in critical care and keep institutional purchasing active. Terlipressin now faces a more limited role in this specific therapeutic setting after the 2026 international sepsis guidance recommended against it for septic shock. The rest of the category remains small, but the user-supplied evidence shows that the antidiuretic drugs industry is not standing still and is still open to niche reformulation strategies. Eton’s desmopressin oral solution program, which reached FDA filing acceptance in 2025, shows how companies are still trying to defend focused subsegments even as the core tablet business faces generic pressure.

By Route Of Administration: Oral Formats Stay Largest While Injectables Gain Ground In Hospitals

Oral formulations held 39.57% of the antidiuretic drugs market size in 2025, which kept this route in the leading position. That leadership came from the practical fit of tablets and sublingual products in chronic AVP-D and nocturia management, where long-term adherence matters more than acute administration speed. Oral use also matches the shift of the antidiuretic drugs market toward home-based and outpatient care because it removes the need for regular clinical supervision in stable patients. The waterless convenience of oral disintegrating formats has been especially useful in older populations, where nighttime dosing patterns and fluid timing matter. This route, therefore, keeps the commercial center of gravity tied to convenience, patient routine, and refill continuity.

Injectables are projected to expand at 8.52% CAGR through 2031, making them the fastest-growing route in the antidiuretic drugs market. The main reason is stronger hospital demand for vasopressin products that can fit ICU protocols and procurement cycles with lower preparation burden. Ready-to-use presentations are particularly attractive because they reduce compounding steps, help lower medication error risk, and fit high-volume critical care settings more smoothly. Intranasal desmopressin remains clinically important for selected patients, but supply restoration has taken time after the earlier global recall tied to packaging tightness issues. Ferring said it submitted a variation to European regulators in November 2024 and planned a U.S. submission in Q2 2025 as part of that restoration process. Subcutaneous and intramuscular presentations remain smaller in commercial terms, yet they still matter in perioperative care and ICU transitions where route flexibility is clinically necessary.

By Indication: Central DI Anchors Revenue While Nocturia Builds The Fastest Growth Path

Central diabetes insipidus held 42.17% of the market in 2025 and remained the leading indication. This segment stays large because most AVP-D patients require sustained desmopressin replacement, which gives the antidiuretic drugs market durable long-run treatment demand. Clinical guidance from the Society for Endocrinology and Japanese guideline bodies continues to place desmopressin at the center of AVP-D treatment pathways, which supports consistent prescribing behavior. Post-pituitary surgery cases add another important stream of demand because transient AVP-D remains common in structured neurosurgical pathways. That mix of lifelong disease management and post-surgical case capture keeps this indication at the revenue core of the antidiuretic drugs market.

Nocturia and nocturnal polyuria are projected to grow at 9.51% CAGR through 2031, which makes them the fastest-growing indications. The growth rate reflects a broader change in practice because frequency-volume charts are making it easier to identify desmopressin-eligible patients in routine urology and general practice settings. A review in Tzu Chi Medical Journal found that desmopressin reduced nocturia frequency in 43% to 66.7% of responsive patients, which supports continued use in carefully selected populations. The same review reported that nighttime urine volume in elderly patients with severe nocturnal polyuria fell from 956 mL to 523 mL after 1 month, which helps explain why this indication is expanding faster than the rest of the antidiuretic drugs market. Hemophilia A, von Willebrand disease type 1, vasodilatory shock, and temporary postoperative polyuria remain relevant, but they contribute less to total value because treatment duration or eligible patient count is more limited in each case.

By End User: Hospitals Still Lead But Homecare Is Becoming Strategically More Important

Hospitals accounted for 44.29% of the market in 2025 and remained the largest end-user group. Their lead comes from vasopressin procurement in septic shock and from parenteral desmopressin use in postoperative care and bleeding-related settings. Hospital demand also carries weight because formulary alignment can lock in recurring institutional purchasing for critical care products. Specialty clinics form the next important layer, since endocrinology, urology, and hematology services often initiate treatment and guide titration decisions. This means acute care still anchors revenue today even as the antidiuretic drugs market becomes more distributed across outpatient channels.

Homecare settings are projected to expand at 10.76% CAGR through 2031, which is the fastest rate among end users. Oral and sublingual desmopressin make this shift possible because stable patients can manage chronic treatment without the same degree of direct supervision required in specialist clinics. Japan’s PMDA revised desmopressin nasal spray prescribing information in June 2025 and reinforced self-management guidance that included home fluid restriction instructions. Once patients stabilize on therapy, refill continuity is often better in homecare than in appointment-dependent settings, which can extend treatment persistence. That is why homecare is becoming a real volume multiplier inside the antidiuretic drugs market, even though hospitals still generate the largest share today.

Geography Analysis

North America held 38.43% of the market in 2025, which made it the largest regional base. The United States remains the core revenue center because it combines advanced ICU infrastructure, strong AVP-D diagnostic capacity, and active generic approvals across both oral and injectable products. The FDA’s calendar year 2024 shortage report recorded 15 new drug shortages, the lowest level in a decade, yet vasopressin injection still remained on the active shortage list. That combination of strong demand and uneven supply creates a market where availability can matter as much as price for hospital customers. Canada followed a similar pattern and authorized the temporary importation of U.S.-authorized vasopressin injection in March 2026 to address a domestic supply shortfall for critical care patients. These events show that North America remains the most commercially important part of the antidiuretic drugs market, but also one of the most operationally sensitive.

Europe is the second-largest regional cluster in the antidiuretic drugs market and remains shaped by generic desmopressin competition and strict post-marketing surveillance. Ferring reported that Minirin sales declined 6% at constant exchange rates in 2024, partly because of generic entry in Western Europe and Canada. Germany and the UK stand out as high-value markets because they combine mature endocrine care with strong ICU vasopressin utilization. The Society for Endocrinology’s clinical guidance has helped standardize inpatient AVP-D management and has supported more consistent prescribing and monitoring across NHS practice.

Asia-Pacific is projected to grow at 9.85% CAGR through 2031, making it the fastest-growing region in the antidiuretic drugs market. The region is benefiting from population aging, wider insurance access in parts of the region, and a stronger regional manufacturing base for generic medicines. Japan remains the most advanced country market in Asia-Pacific because aging is deepest there, and clinical guidance formally supports desmopressin as standard treatment for central DI. In January 2025, Kissei announced that its domestic sales partnership with Ferring for Minirin Melt and desmopressin preparations in Japan would end on March 31, 2025, after which Ferring would assume sole promotion responsibility. China and India are still earlier in penetration terms, but hospital expansion and rising healthcare spending are widening the treated pool over time. The Middle East, Africa, and South America remain smaller regional positions, yet critical care investment and broader reimbursement for rare endocrine disorders should keep incremental demand moving upward across the antidiuretic drugs market.

Competitive Landscape

The antidiuretic drugs market remains moderately fragmented, with Ferring Pharmaceuticals still holding the broadest branded desmopressin presence across key regions and indications. Competition is becoming sharper because generic-focused manufacturers such as Gland Pharma, Aurobindo, Amphastar, Fresenius Kabi, and Caplin Steriles are pushing more aggressively into hospital injectables and oral dosage forms. Ferring reported that Minirin sales declined 6% at constant exchange rates in 2024, and the company linked part of that pressure to generic entry in Western Europe and Canada. This means the antidiuretic drugs market is not centered on one dominant supplier, even though Ferring still leads in brand recognition and portfolio depth. Companies that can pair reliable supply with route-specific convenience are likely to defend margins more effectively than companies that depend only on older branded assets.

Aurobindo made one important strategic move when it secured FDA approval in March 2024 for AB-rated generic desmopressin acetate tablets in 0.1 mg and 0.2 mg strengths, which strengthened price competition in oral therapy. Caplin Steriles made another move when desmopressin acetate injection began U.S. marketing in March 2026 through ANDA219981, adding another generic option in the injectable segment. Ferring made a channel-control move in Japan after the Kissei partnership ended, and it assumed sole promotion responsibility from April 2025. Ferring also continued work to restore nasal spray availability after its earlier recall by submitting a regulatory variation in Europe in November 2024. Together, these actions show that competition in the antidiuretic drugs market is being shaped by route access, lifecycle management, and commercial control of local distribution.

Diagnostic innovation is also influencing competition because better AVP-D identification shortens the path to treatment and supports earlier prescription flow. The companies best placed to benefit are those that can align drug supply with the change in diagnostic practice rather than waiting for hospital demand alone. Manufacturing quality rules still matter because current good manufacturing practice requirements create a practical barrier for weaker suppliers trying to enter a sensitive therapeutic category. This is why integrated production, multiple manufacturing sites, and a mix of oral, nasal, and injectable capabilities continue to shape relative strength inside the antidiuretic drugs market.

Antidiuretic Drugs Industry Leaders

Amneal Pharmaceuticals, Inc.

Baxter International Inc.

Ferring Pharmaceuticals

Sun Pharmaceutical Industries Ltd.

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Surviving Sepsis Campaign published its 2026 International Guidelines for Management of Sepsis and Septic Shock, retaining vasopressin as the recommended adjunct to norepinephrine for septic shock management and explicitly recommending against terlipressin for this indication. With 129 total statements and 23-country panel representation, this update directly influences hospital vasopressin procurement protocols globally.

- February 2026: Caplin Steriles Limited commenced marketing of desmopressin acetate injection (ANDA219981), a 4 mcg/mL sterile solution, in the United States, the product’s marketing start date per DailyMed labeling. This product, manufactured in India, adds a new generic competitor to the injectable desmopressin segment.

- July 2025: The FDA accepted Eton Pharmaceuticals’ NDA for ET-600 (Desmopressin Oral Solution) and assigned a PDUFA target action date of February 25, 2026. The product was designed as the sole oral liquid option for pediatric central diabetes insipidus patients, with patent protection through 2044.

- January 2025: Kissei Pharmaceutical announced the termination of its domestic sales partnership with Ferring Pharmaceuticals for Minirin Melt and desmopressin preparations in Japan, effective March 31, 2025. From April 2025, Ferring assumed sole promotion responsibility, indicating a strategic decision to invest more directly in the Japanese antidiuretic market.

Global Antidiuretic Drugs Market Report Scope

The antidiuretic drugs market refers to the global pharmaceutical industry segment focused on manufacturing and selling medications that help control fluid balance in the body. By mimicking the natural hormone vasopressin, these drugs reduce urination and promote water reabsorption in the kidneys to manage conditions like diabetes insipidus and nocturnal enuresis.

The Antidiuretic Drugs Market is segmented across multiple dimensions to capture its diverse applications and delivery methods. By drug type, it includes Desmopressin, Vasopressin, Terlipressin, Lypressin, and other related agents. In terms of route of administration, the market spans oral, intranasal, injectable, IV, and SC/IM formulations. The indications covered include Central Diabetes Insipidus (DI), Primary Nocturnal Enuresis (PNE), Nocturia, Hemophilia A, Vasodilatory Shock, and other conditions. By end user, the market is segmented into hospitals, specialty clinics, and homecare. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America, with forecasts provided in terms of value (USD).

| Desmopressin |

| Vasopressin |

| Terlipressin |

| Lypressin |

| Other Drug Type |

| Oral | Tablets |

| Oral lyophilisates / sublingual tablets | |

| Intranasal | Metered nasal sprays |

| Nasal solutions / drops | |

| Injectable | |

| Intravenous | |

| Subcutaneous / intramuscular |

| Central Diabetes Insipidus |

| Primary Nocturnal Enuresis |

| Nocturia / Nocturnal Polyuria |

| Hemophilia A and von Willebrand Disease Type 1 |

| Vasodilatory Shock |

| Temporary Postoperative Polyuria / Polydipsia |

| Hospitals |

| Specialty Clinics |

| Endocrinology Clinics |

| Urology Clinics |

| Hematology Clinics |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Desmopressin | |

| Vasopressin | ||

| Terlipressin | ||

| Lypressin | ||

| Other Drug Type | ||

| By Route of Administration | Oral | Tablets |

| Oral lyophilisates / sublingual tablets | ||

| Intranasal | Metered nasal sprays | |

| Nasal solutions / drops | ||

| Injectable | ||

| Intravenous | ||

| Subcutaneous / intramuscular | ||

| By Indication | Central Diabetes Insipidus | |

| Primary Nocturnal Enuresis | ||

| Nocturia / Nocturnal Polyuria | ||

| Hemophilia A and von Willebrand Disease Type 1 | ||

| Vasodilatory Shock | ||

| Temporary Postoperative Polyuria / Polydipsia | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Endocrinology Clinics | ||

| Urology Clinics | ||

| Hematology Clinics | ||

| Homecare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antidiuretic drugs market through 2031?

The antidiuretic drugs market is forecast to reach USD 1.99 billion by 2031, up from USD 1.23 billion in 2025, with a 8.45% CAGR from 2026 to 2031.

Which drug type leads current revenue?

Desmopressin led with 48.91% of 2025 revenue because it spans AVP-D, nocturia, nocturnal polyuria, and selected bleeding-related use cases.

Which indication is expanding fastest?

Nocturia and nocturnal polyuria are projected to grow at 9.51% CAGR through 2031 as screening improves and treatment use expands in aging populations.

Why does North America remain the largest regional opportunity?

North America held 38.43% of 2025 revenue because it combines advanced ICU demand, stronger diagnostic capacity, and active generic competition across oral and injectable products.

What is driving growth of the the antidiuretic drugs market?

Growth is being supported by earlier AVP-D diagnosis, rising nocturia burden in older adults, broader generic access, and stronger hospital use of vasopressin under sepsis guidelines.

Page last updated on: