Pulmonary Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

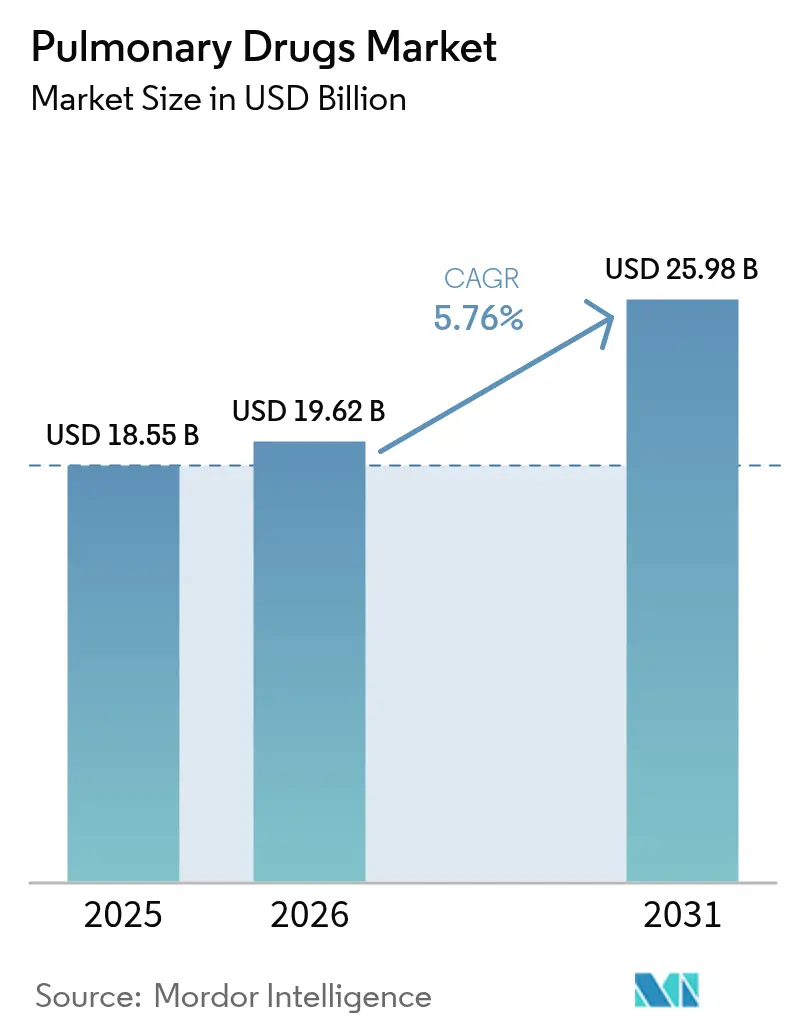

| Market Size (2026) | USD 19.62 Billion |

| Market Size (2031) | USD 25.98 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulmonary Drugs Market Analysis by Mordor Intelligence

The pulmonary drugs market size was valued at USD 18.55 billion in 2025 and estimated to grow from USD 19.62 billion in 2026 to reach USD 25.98 billion by 2031, at a CAGR of 5.76% during the forecast period (2026-2031). Rising respiratory disease prevalence, an aging global population, and steady innovation in inhaled and biologic therapies are the main engines of growth. Demand also tracks worsening air quality, with the World Health Organization reporting that nearly the entire world lives in areas exceeding particulate-matter limits[1]World Health Organization, “Ambient Air Pollution: A Global Assessment,” who.int. At the same time, patient adherence technologies and eco-friendly propellants broaden product appeal, while patent expirations spur both generic competition and life-cycle management strategies. North America leads revenue generation, but Asia-Pacific shows stronger momentum as healthcare access expands and urban pollution intensifies.

Key Report Takeaways

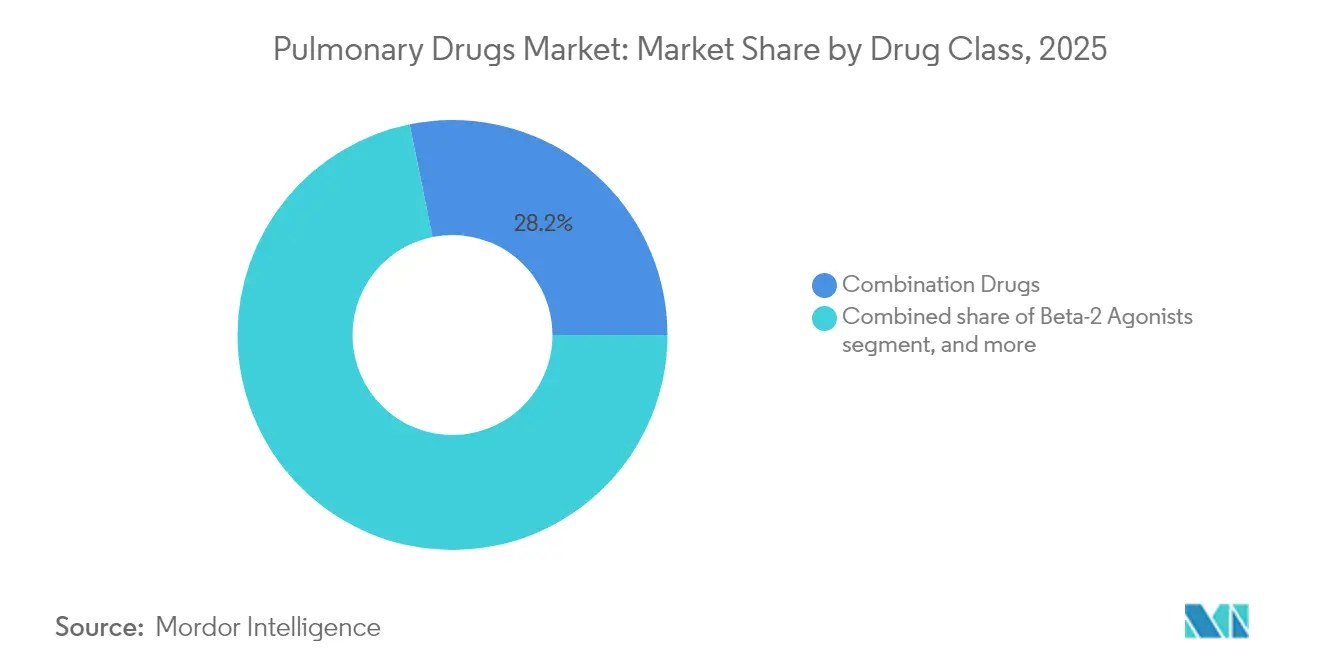

- By drug class, combination drugs led with 28.20% of pulmonary drugs market share in 2025; monoclonal antibodies are expected to grow at a 7.42% CAGR through 2031.

- By indication, asthma accounted for 42.18% share of the pulmonary drugs market size in 2025, while allergic rhinitis is projected to advance at an 8.84% CAGR between 2026-2031.

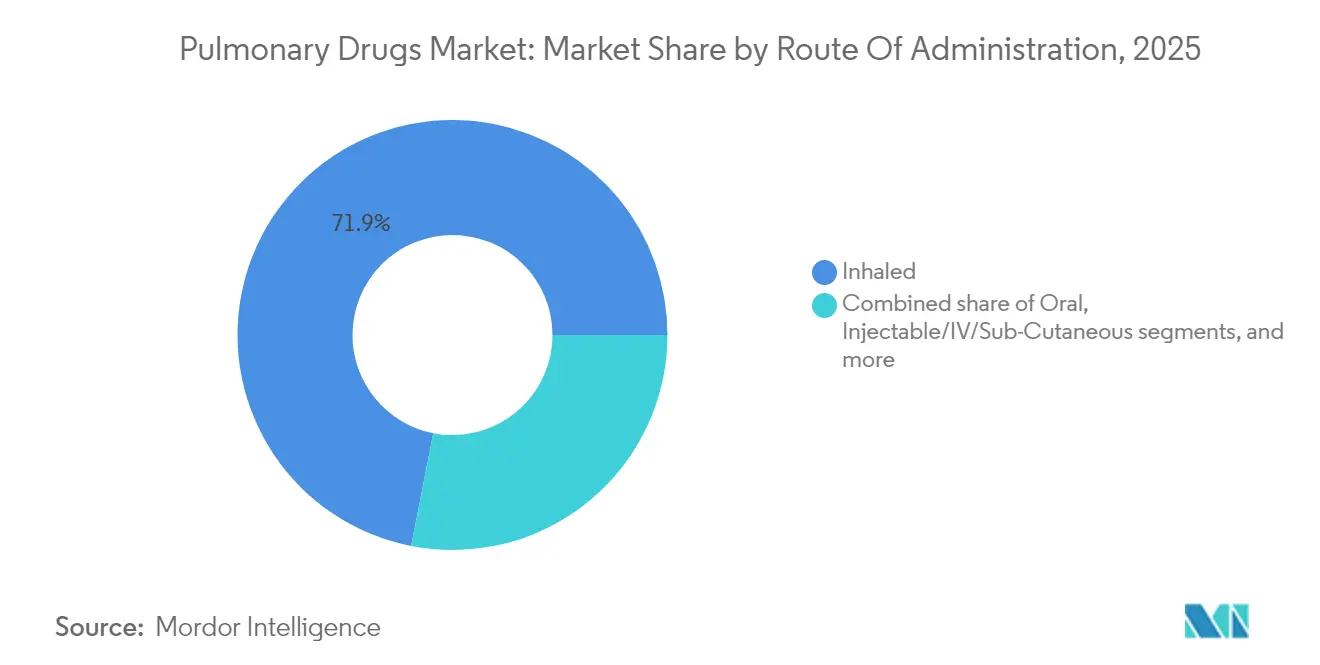

- By route of administration, inhaled formats controlled 71.92% of the pulmonary drugs market size in 2025; intranasal products are forecast to expand at an 8.63% CAGR.

- By distribution channel, retail pharmacies held 47.88% revenue share in 2025; “other channels” (online, specialty, direct-to-patient) show the fastest CAGR at 8.39%.

- By geography, North America captured 38.11% pulmonary drugs market share in 2025, while Asia-Pacific is growing at 6.46% CAGR through the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pulmonary Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of respiratory diseases | +1.8% | Global, strongest in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Growing Burden Of Respiratory Diseases | +1.2% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Aging Global Population | +0.9% | North America and Europe | Medium term (2-4 years) |

| Technological Advancements In Inhalation Therapies | +0.8% | Emerging industrial hubs in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Increasing Environmental Risk Factors | +1.1% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Respiratory Diseases

Air pollution drives mounting morbidity and mortality, causing 4.2 million deaths each year worldwide and accounting for one-quarter of COPD fatalities. Emerging economies feel the heaviest impact because industrial activity often outpaces regulatory oversight. Economic costs accumulate through lost productivity and greater hospital utilization, heightening the need for chronic pharmacologic management. COPD prevalence reached 12.5 million cases in the United States by 2020, with marked variation by race and age[2]American Lung Association, “COPD Trends in the United States,” lung.org. The resulting demand fuels sustained expansion of the pulmonary drugs market as payers prioritize preventive care and exacerbation reduction.

Aging Global Population

Older adults exhibit diminished lung elasticity and weaker immune response, making them prone to chronic respiratory conditions. In the United States, 51.4% of adults live with multiple chronic illnesses, and respiratory disease often overlaps cardiovascular and metabolic disorders[3]Centers for Disease Control and Prevention, “National Center for Health Statistics Multiple Chronic Conditions,” cdc.gov. That comorbidity pattern encourages use of fixed-dose combination inhalers that limit pill burden and simplify regimens. Developed regions already experience rapid population aging, but emerging countries are following close behind, enlarging the future patient pool. This demographic wave underpins long-run volume growth for the pulmonary drugs market.

Technological Advancements in Inhalation Therapies

Smart inhalers with integrated sensors, such as Adherium’s FDA-cleared platform, allow clinicians to track adherence and tailor interventions in real time. Device makers are also redesigning propellants: one new formulation cuts global-warming potential by 99.9%, aligning with stricter environmental mandates. Connectivity features appeal to remote-care models, and data collected from connected devices feed predictive analytics that anticipate exacerbations. While reimbursement pathways remain uncertain in some markets, early adopters demonstrate improved outcomes and lower emergency visits, validating the technology’s clinical value.

Rising Adoption of Biologic Therapies

Monoclonal antibodies such as mepolizumab (approved for COPD in 2025) target underlying inflammatory pathways rather than providing symptomatic relief alone gsk.com. Dupilumab’s earlier approval for COPD broadened the precedent, prompting payers to cover high-cost injectables for select patient subgroups. Patent coverage for most respiratory biologics extends beyond 2030, supporting steady revenue streams. Biosimilars will eventually pressure prices, but complex manufacturing and the need for inhalation-specific delivery devices should delay widespread competition, translating to robust medium-term growth for the pulmonary drugs market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Framework | -0.7% | North America and Europe | Medium term (2-4 years) |

| Adverse Effects And Safety Concerns | -0.5% | Global | Short–medium term (≤ 4 years) |

| Escalating Pricing And Reimbursement Pressures | -0.9% | United States, Europe, parts of Asia-Pacific | Medium term (2-4 years) |

| Patent Expiry And Generic Competition | -1.1% | Primarily developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework

Heightened pharmacovigilance has lengthened review cycles. The FDA recently attached Guillain-Barré warnings to RSV vaccines, signaling more conservative risk-benefit thresholds for respiratory products. Manufacturing audits also intensified; quality citations against multiple active-ingredient plants caused temporary production halts. While such vigilance protects patients, it increases development cost and can slow product launches, particularly affecting smaller innovators and emerging-market manufacturers. Larger firms may benefit from lower competitive entry, but their compliance spending continues to rise.

Patent Expiry and Generic Competition

The 2025 expiration of fluticasone propionate inhaler patents invites numerous abbreviated filings, echoing the erosion experienced by Advair after its protections lapsed. Complex device engineering still limits quick substitution, yet successful generic entries can slash branded revenue within months. Innovators deploy life-cycle tactics such as new propellants, digital sensors, and expanded indications, yet payers scrutinize incremental benefits. The near-term wave of expirations weighs on the pulmonary drugs industry outlook even as new biologics partially offset lost sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Combination Therapies Retain the Sales Lead

Combination inhalers generated 28.20% of pulmonary drugs market size in 2025, reinforcing clinician preference for multi-mechanism control of airflow limitation. Triple-therapy products like Breztri met Phase III asthma endpoints in 2025, signalling broader label opportunities and deeper formulary penetration. Beta-2 agonists and anticholinergics continue as backbone components inside these fixed-dose platforms, sustaining mature revenue bases. Monoclonal antibodies, though currently smaller in volume, clock a 7.42% CAGR, propelled by approvals in eosinophilic COPD and severe asthma. Corticosteroid monotherapies face modest growth as safety concerns shift interest toward targeted biologics. Anti-leukotrienes and antihistamines preserve niche use in pediatric and allergy-linked cases, while pipeline agents targeting novel inflammatory mediators foreshadow future competitive cycles. The diverse therapeutic arsenal underscores why the pulmonary drugs market remains competitive yet opportunity-rich.

Combination-therapy dominance also shapes manufacturing investment as firms upgrade fill-finish lines to accommodate dual canisters and triple-moiety dry-powder blends. Branded leaders hedge against generic erosion by bundling device innovations such as dose counters and adherence trackers. Meanwhile, monoclonal antibody producers scale up single-use bioreactors to reduce batch contamination risk and comply with evolving good-manufacturing-practice rules. The strategic mix of small-molecule inhalers and injectable biologics leaves purchasers juggling formulary rebates, which in turn shifts contracting power toward wholesalers well versed in complex negotiation.

By Indication: Asthma Prevails While Allergic Rhinitis Gains Pace

Asthma contributed 42.18% of pulmonary drugs market share in 2025 due to its high prevalence and guideline-mandated long-term controller therapy. Biologics addressing Type 2 inflammation build on this base, offering step-up options for uncontrolled disease. COPD remains sizeable but still sees high unmet need for disease-modifying interventions, a gap partially closed by the 2024 approval of ensifentrine. Allergic rhinitis advances fastest at an 8.84% CAGR, supported by combo nasal sprays that merge antihistaminic and corticosteroid activity for rapid symptom relief. Pulmonary arterial hypertension commands premium pricing despite fewer patients, making it disproportionately lucrative. Cystic fibrosis treatments benefit from orphan incentives, though the overall pulmonary drugs market size in that subsegment stays limited by population. Emerging indications such as idiopathic pulmonary fibrosis inch forward as research unravels fibrosis-driving pathways, attracting early-stage venture funding.

Geographic treatment patterns differ: asthma biologic uptake climbs steadily in the United States and Germany, while COPD triple inhaler adoption outpaces elsewhere due to hospital-driven protocols. In Asia-Pacific, rhinitis therapy growth rides rising urban allergen exposure. Such regional nuances push manufacturers to tailor educational campaigns, reimbursement dossiers, and supply chains, reflecting the nuanced segmentation landscape inside the pulmonary drugs market.

By Route of Administration: Inhaled Platforms Stay Dominant Amid Nasal Momentum

Inhaled products accounted for 71.92% of pulmonary drugs market size in 2025 because they deliver medicine directly to disease sites and are familiar to prescribers. Dry-powder inhalers and metered-dose inhalers vie on simplicity, inspiratory flow requirements, and environmental footprint. Regulatory support for lower-GWP propellants is accelerating device refresh cycles, prompting branded suppliers to relaunch legacy molecules in greener formats. Intranasal delivery, with an 8.63% CAGR, garners attention after the 2025 approval of an epinephrine nasal spray for pediatric anaphylaxis. Needle-free and quick-onset characteristics appeal to patients, while payers weigh cost offset from avoided emergency visits.

Oral formulations maintain relevance for systemic effects when airway deposition is not critical or when patients cannot coordinate inhaler techniques. Injectable biologics grow in tandem with asthma and COPD antibody indications, though administration shifts toward at-home subcutaneous options to minimize clinic visits. Nascent modalities such as transdermal patches and pulmonary-delivered gene therapies remain inside the “other routes” bucket, where preclinical successes could redefine delivery norms. Patient-centric design and device training programs increasingly influence formulary inclusion, emphasizing convenience alongside efficacy within the broad pulmonary drugs market.

By Distribution Channel: Retail Pharmacy Leads During Digital Transition

Retail outlets dispensed 47.88% of 2025 sales as chronic users rely on neighborhood pharmacists for refills and counseling. Medication therapy management programs drive adherence, lowering exacerbation rates and reinforcing channel loyalty. Specialty pharmacies, although smaller, rise rapidly on the back of biologic adoption, offering cold-chain logistics and nurse-run injection training. Hospitals focus on acute exacerbation therapy and initiation of complex agents, then often transition patients to retail or specialty settings for maintenance. “Other channels” such as online pharmacies and direct-to-consumer delivery achieve an 8.39% CAGR, propelled by telehealth growth, mail-order convenience, and price transparency.

Consolidation among pharmacy benefit managers continues to reshape bargaining power. Digital ordering portals integrate with electronic health records, automating prior authorizations and accelerating fulfillment. As omnichannel models mature, manufacturers must align trade terms across brick-and-mortar and e-commerce while preventing parallel trade, safeguarding both volume and pricing integrity across the pulmonary drugs market.

Geography Analysis

North America retained 38.11% of 2025 revenue, buoyed by high biologic uptake and favorable reimbursement structures. U.S. Medicare redesigns for 2025 introduce negotiated ceiling prices, increasing payer leverage yet promising broader affordability once drugs qualify for negotiation. Canadian provinces expand biologic coverage, though tendering keeps net prices under pressure. The region also drives device innovation, with several FDA-de novo clearances for smart inhalers shaping clinical expectations.

Europe remains a core market characterized by universal coverage and stringent cost-effectiveness rules. Germany, the United Kingdom, and France collectively command the largest slice of regional spending, underpinned by aging demographics and strong environmental policies aimed at cutting particulate emissions. Pan-EU initiatives streamline approval pathways, easing multi-country launches and shortening time-to-market. However, reference-pricing frameworks limit high list prices, directing manufacturers toward outcomes-based contracts, particularly for biologics.

Asia-Pacific records the fastest 6.46% CAGR through 2031. Rapid urbanization and coal-heavy power generation worsen air-quality metrics, expanding the patient pool. China invests in local production of inhaled generics to curb import dependence, although premium biologics still rely on multinational supply. India’s domestic industry scales up dry-powder inhaler output, supporting both export and local demand. Japanese guidelines widen indications for triple therapy, spurring prescription growth, while Australia funds remote-monitoring pilots to serve rural COPD patients. Southeast Asian countries improve reimbursement, yet affordability remains a hurdle, leaving room for tiered-pricing strategies across the pulmonary drugs market.

Competitive Landscape

Large multinationals dominate the mid-to-high price tiers, leveraging patent portfolios, salesforces, and regulatory experience. AstraZeneca targets USD 80 billion companywide revenue by 2030, with respiratory therapies as a core pillar, underpinned by Breztri, Fasenra, and a late-stage IL-33 antibody. GSK expands its biologic footprint after acquiring Aiolos Bio, complementing the strong uptake of Trelegy inhaler and Nucala injectable. Sanofi bolsters rare disease depth through its Inhibrx deal, positioning recombinant alpha-1 antitrypsin for pivotal trials. These acquisitions illustrate the reliance on bolt-on deals to fill pipeline gaps.

Smart-device partnerships emerge as a differentiator. GSK collaborates with Propeller Health for connected inhalers, while smaller digital startups offer analytics dashboards to flag non-adherence. Yet commercialization hurdles remain: Teva withdrew its Digihaler line in 2024, citing low uptake despite positive feedback on clinical utility. Patent cliffs trigger defensive strategies. Innovators re-patent device mechanisms, pursue pediatric extensions, and invest in greener propellants to justify new codes. Generic challengers concentrate on off-patent corticosteroids and dual bronchodilators, but device replication complexity prolongs market entry.

Regional manufacturers compete on cost leadership, supplying branded generics in emerging markets. Indian contract development organisations gain share in dry-powder formulations, while Chinese firms partner with Western companies for antibody fill-finish work. Mid-size biotechs focus on niche pathways such as neutrophil elastase inhibition and T-cell checkpoint modulation, aiming for orphan designations that expedite review. Venture funding stays healthy, partly because the pulmonary drugs market offers multiple subsegments with distinct risk-return profiles, balancing monoclonal scale-up cost against the simpler economics of fixed-dose bronchodilators.

Pulmonary Drugs Industry Leaders

GlaxoSmithKline plc

AstraZeneca plc

Boehringer Ingelheim GmbH

Novartis AG

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AstraZeneca reported positive KALOS and LOGOS Phase III data for Breztri in asthma, supporting label expansion beyond COPD.

- May 2025: GSK secured FDA approval for Nucala (mepolizumab) in COPD, marking the first anti-IL-5 biologic for this indication.

- March 2025: FDA approved Neffy epinephrine nasal spray for severe allergic reactions in children aged 4+, the first needle-free epinephrine option.

- February 2025: GSK acquired Aiolos Bio for USD 1.4 billion, adding a long-acting anti-TSLP antibody to its respiratory pipeline.

- January 2025: Sanofi finalized a USD 2.2 billion acquisition of Inhibrx, gaining INBRX-101 for alpha-1 antitrypsin deficiency.

- September 2024: Molex agreed to purchase Vectura Group to extend inhalation drug-delivery capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pulmonary drugs market as prescription and over-the-counter pharmaceutical agents that act directly on the airways or lung parenchyma to prevent, control, or reverse disorders such as asthma, chronic obstructive pulmonary disease, pulmonary fibrosis, pulmonary arterial hypertension, cystic fibrosis, and acute respiratory infections. Drugs delivered by inhalation, oral, or parenteral routes are included, provided their primary clinical objective is pulmonary.

Scope Exclusion: vaccines, diagnostic agents, and stand-alone delivery devices are outside this assessment.

Segmentation Overview

- By Drug Class

- Beta-2 Agonists

- Anticholinergic Agents

- Oral & Inhaled Corticosteroids

- Anti-Leukotrienes

- Antihistamines

- Monoclonal Antibodies

- Combination Drugs

- Other Drug Classess

- By Indication

- Asthma

- COPD

- Allergic Rhinitis

- Pulmonary Arterial Hypertension

- Cystic Fibrosis

- Other Indications

- By Route of Administration

- Inhaled

- Oral

- Injectable/IV/Sub-Cutaneous

- Intranasal

- Other Route of Administrations

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviewed pulmonologists, hospital pharmacy heads, payers, and supply-chain managers across North America, Europe, and Asia-Pacific. The discussions helped validate treatment mix shifts (for example, rising biologic penetration), typical patient days on therapy, channel mark-ups, and forthcoming patent cliffs, allowing us to fine-tune desk-research assumptions.

Desk Research

We began by mapping the universe of approved and pipeline respiratory drugs using open datasets from sources such as the World Health Organization, the U.S. Food and Drug Administration's Orange Book, ClinicalTrials.gov, UN demographic statistics, and air-quality dashboards from the U.S. EPA and the European Environment Agency. Annual utilization signals were then linked to pricing clues drawn from listed reimbursement schedules, company 10-K filings, and hospital procurement portals. According to Mordor Intelligence analysts, subscription databases like D&B Hoovers and Dow Jones Factiva provided targeted financials and news that anchored company-level benchmarks. The sources cited above illustrate, not exhaust, our secondary evidence pool used for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down demand pool was first constructed from diagnosed prevalence of key respiratory diseases, therapy adoption rates, and average annual treatment cost per patient. Results were corroborated with selective bottom-up roll-ups of sampled manufacturer revenues and channel checks, which are then adjusted for double counting. Variables that most influence the model include asthma and COPD prevalence growth, biologic share of new prescriptions, smart-inhaler uptake, average selling price erosion post-generic entry, and regional reimbursement changes. Multivariate regression combined with scenario analysis projects these drivers through 2030, while gaps in bottom-up evidence are bridged with conservative ratio estimates agreed upon in expert calls.

Data Validation & Update Cycle

Outputs pass three layers of variance checks, peer review, and senior-analyst sign-off. Models refresh every year, with interim updates triggered by material regulatory approvals, safety withdrawals, or macro shocks. A quick validation sweep is completed just before report release so clients receive the freshest view.

Why Mordor's Pulmonary Drugs Baseline Commands Dependability

Published numbers often diverge because firms select different therapy baskets, pricing assumptions, and refresh timings. We acknowledge that reality upfront and then show how disciplined variable selection and annual recalibration anchor our baseline.

Key gap drivers include whether inhalation devices are bundled with drugs, the breadth of disease inclusion (some services add oncology agents), and whether list or net prices are applied. Mordor restricts scope to therapeutics targeting pulmonary pathologies only, applies net-of-rebate pricing proxies, and reconciles volumes with real-world prevalence, which together temper over-estimation risk.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.55 B (2025) | Mordor Intelligence | - |

| USD 56.98 B (2025) | Global Consultancy A | Bundles delivery devices and broader respiratory care drugs; relies on high-level manufacturer revenue splits without patient prevalence checks |

| USD 61.10 B (2023) | Industry Magazine B | Includes oncology and biologic immunotherapies for lung cancer; older base year and no net-price adjustments |

| USD 53.24 B (2023) | Data Services C | Focuses on delivery systems plus drugs, uses shipment values and applies uniform growth multipliers |

Taken together, the comparison shows that when non-pulmonary products or gross pricing slip in, market values swell quickly. By anchoring inputs to disease-specific prevalence, validated therapy mix, and net economics, Mordor Intelligence offers decision-makers a balanced, transparent baseline they can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current value of the pulmonary drugs market?

The pulmonary drugs market is valued at USD 19.62 billion in 2026.

How fast is the pulmonary drugs market expected to grow?

The market is projected to expand at a 5.76% CAGR, reaching USD 25.98 billion by 2031.

Which drug class holds the largest pulmonary drugs market share?

Combination inhalers lead with 28.20% share as of 2025.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to grow at a 6.46% CAGR, outpacing other regions.

Why are biologics gaining traction in respiratory care?

Monoclonal antibodies provide targeted inflammation control and have secured recent approvals for severe asthma and COPD, driving a 7.42% CAGR for this segment.

How are smart inhalers influencing patient outcomes?

Connected inhalers track real-time adherence, enable data-driven interventions, and have demonstrated reduced exacerbation rates in early adopter programs.

Page last updated on: