Critical Care Antiarrhythmic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

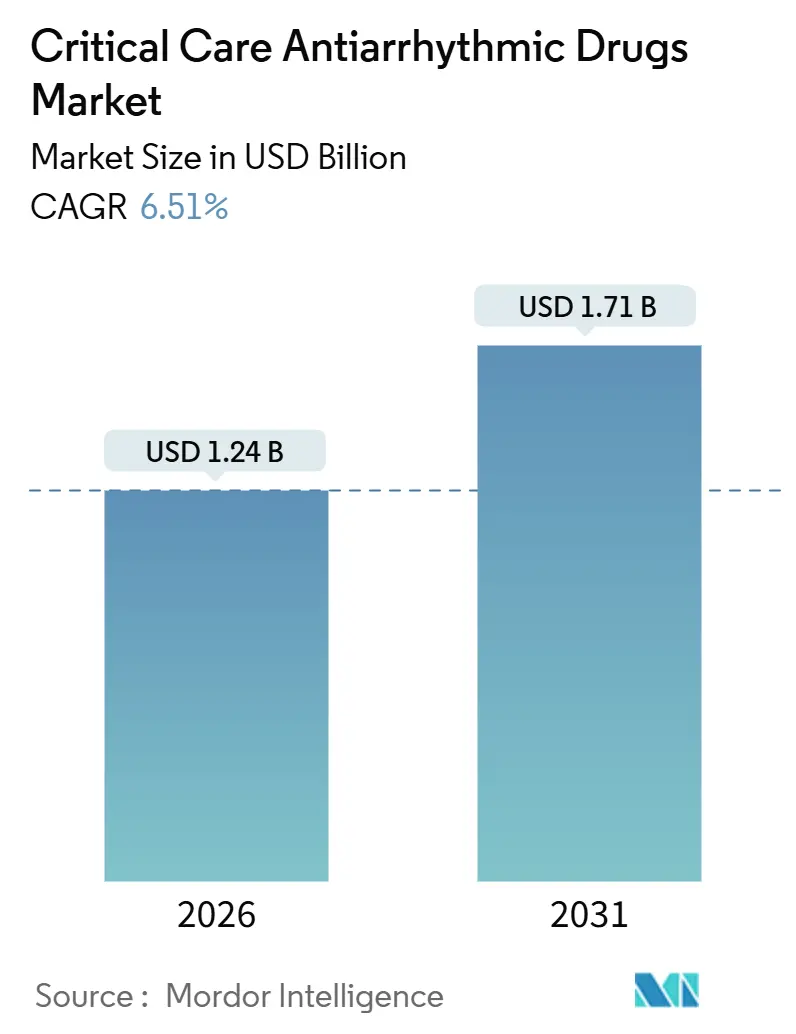

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

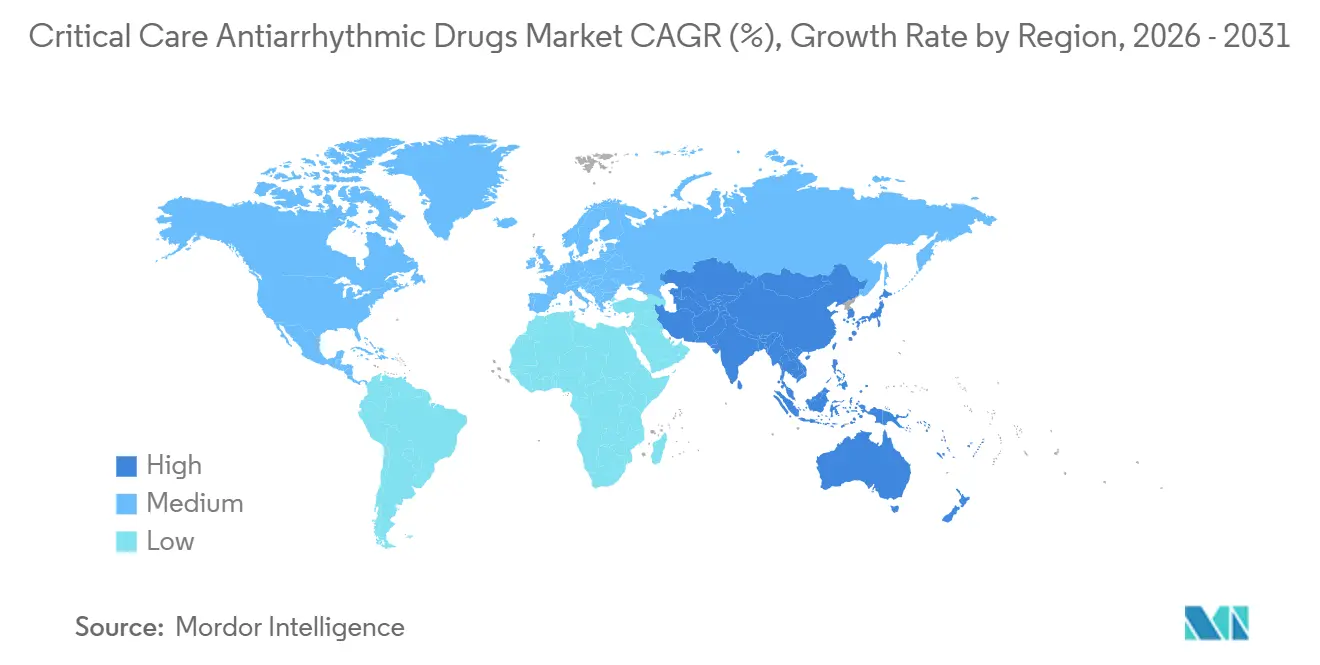

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Critical Care Antiarrhythmic Drugs Market Analysis by Mordor Intelligence

The Critical Care Antiarrhythmic Drugs Market size is estimated at USD 1.24 billion in 2026, and is expected to reach USD 1.71 billion by 2031, at a CAGR of 6.51% during the forecast period (2026-2031).

The increasing global burden of arrhythmia, coupled with higher critical-care bed density and the adoption of smart infusion pumps to reduce dosing errors, is driving market growth. Expansion initiatives in China, Saudi Arabia, and Egypt are significantly increasing the installed base of continuous electrocardiographic monitors. Concurrently, updated guidelines from the American Heart Association and the European Society of Cardiology continue to position beta blockers and amiodarone as key components of intensive-care treatment protocols. Baxter’s Novum IQ smart pump, with a 97% drug-library compliance rate—well above the industry average—highlights the rapid integration of error-prevention software in healthcare facilities. Furthermore, Milestone Pharmaceuticals’ self-administered etripamil nasal spray signals a potential shift in managing certain supraventricular tachycardia cases outside emergency departments, which could reshape channel dynamics over the forecast period.

Key Report Takeaways

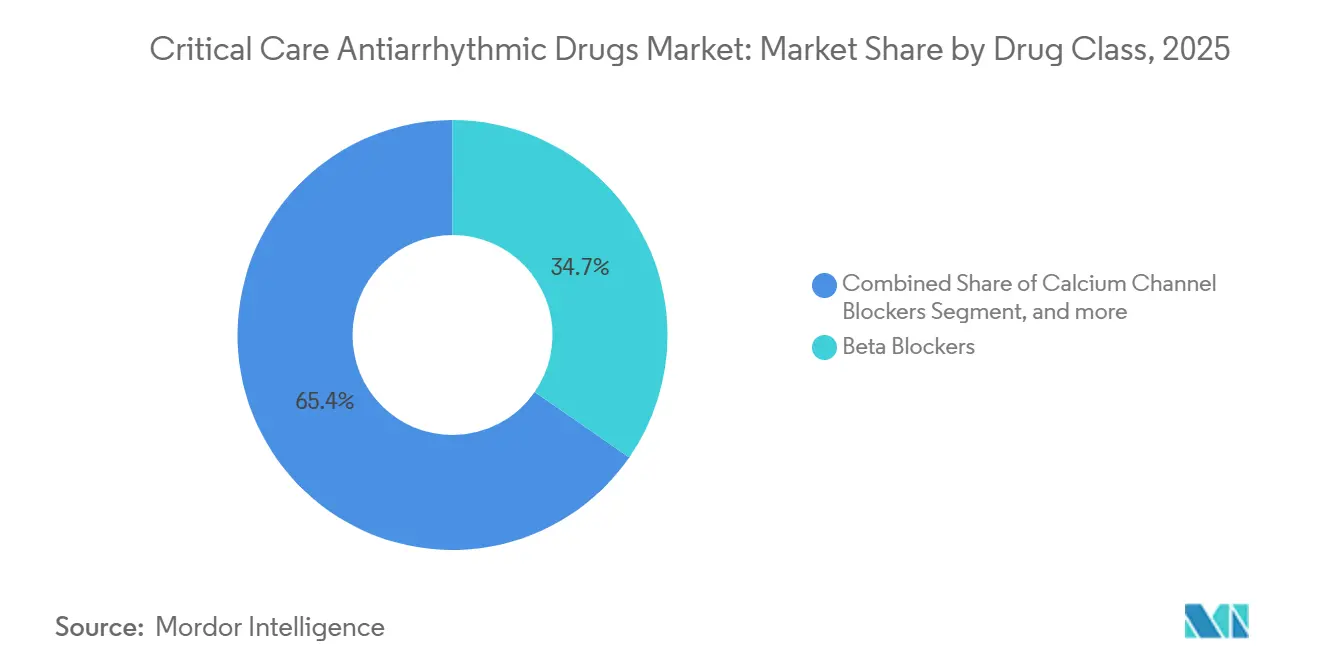

- By drug class, beta blockers led with 34.65% of the critical care antiarrhythmic drugs market share in 2025, while potassium channel blockers are forecast to grow at an 8.65% CAGR to 2031.

- By disease type, supraventricular arrhythmias accounted for 52.45% of the critical care antiarrhythmic drugs market size in 2025, whereas ventricular arrhythmias are expected to advance at an 8.76% CAGR through 2031.

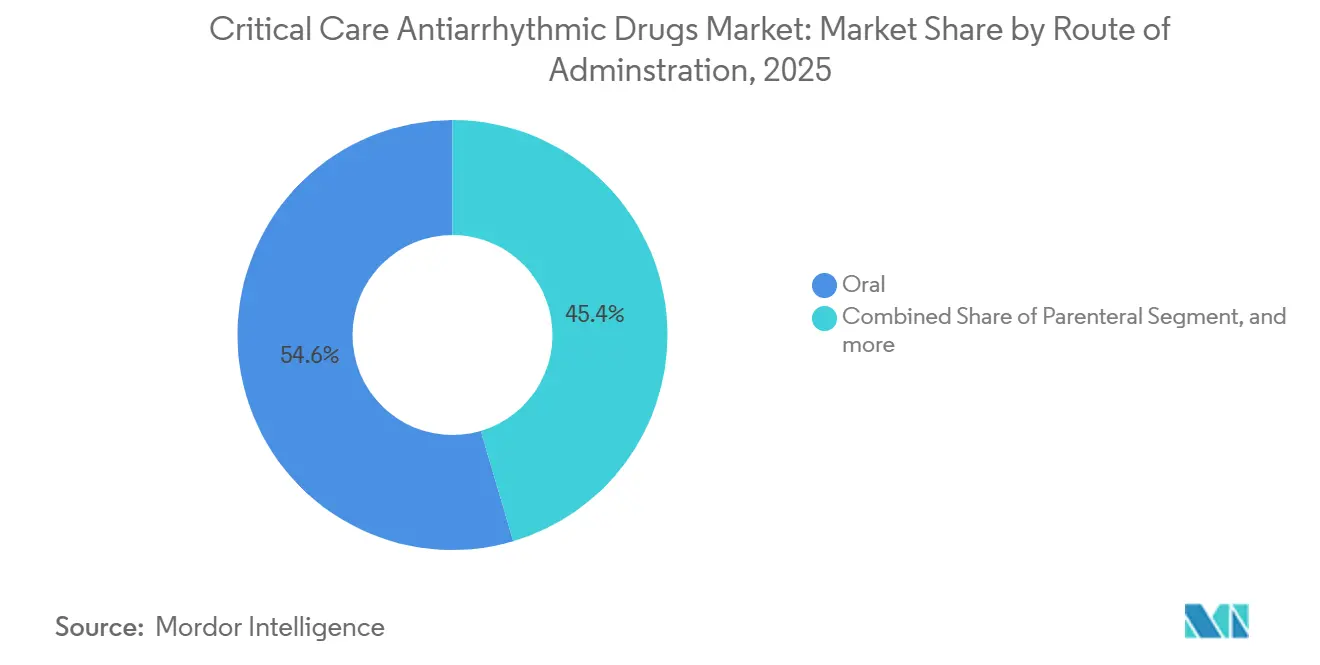

- By route of administration, oral formulations held 54.56% share of the critical care antiarrhythmic drugs market size in 2025, and parenteral products are expanding at a 9.21% CAGR through 2031.

- By distribution channel, hospital pharmacies captured 62.45% of the critical care antiarrhythmic drugs market in 2025, and online pharmacies recorded the fastest growth at a 9.65% CAGR through 2031.

- By geography, North America commanded 42.56% share of the critical care antiarrhythmic drugs market size in 2025 and Asia-Pacific is projected to register a 7.54% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Critical Care Antiarrhythmic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Cardiovascular Disease Burden | +1.8% | Worldwide, prominent in North America, Europe, China | Long term (≥ 4 years) |

| Expansion of Critical Care Infrastructure | +1.5% | China, India, Saudi Arabia, broader MEA and South America spill-over | Medium term (2-4 years) |

| Aging Population and Comorbidities | +1.2% | North America, Western Europe, Japan, South Korea | Long term (≥ 4 years) |

| Technological Advancements in Drug Delivery and Monitoring | +0.9% | North America, European Union, early GCC and Australia uptake | Short term (≤ 2 years) |

| Increasing ICU Admissions for Cardiac Conditions | +0.7% | Global, focused in tertiary centers with cardiac ICUs | Medium term (2-4 years) |

| Supportive Clinical Guidelines and Protocols | +0.4% | Global, led by ACC/AHA, ESC and national societies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Cardiovascular Disease Burden

Atrial fibrillation and flutter prevalence rose 137% between 1990 and 2021, reaching 52.55 million people worldwide, and Europe alone recorded 957,812 new atrial fibrillation cases in 2021[1]Robert Bonow, “ACC/AHA 2025 guideline for acute coronary syndromes,” American Heart Association, ahajournals.org. The United States prevalence stood at 3.89% during 2019-2023, translating into 4.83 million patients, while arrhythmia-related mortality climbed to 19.4 per 100,000 in 2021. This epidemiological swell, coupled with a 30.2% crude case fatality rate in ICU bloodstream infections, keeps both parenteral and oral antiarrhythmic demand on an upward path. Forecast models suggest atrial fibrillation mortality will reach 12.3 per 100,000 by 2040, reinforcing sustained consumption of rate- and rhythm-control therapies.

Expansion of Critical Care Infrastructure

China’s May 2024 directive targets 15 ICU beds per 100,000 residents by the end of 2025, while Saudi Arabia added a 28-bed cardiac ICU, and Egypt aims to lift hospital-bed density from 12 to 30 per 10,000 by 2030. The United States expects ICU days to rise by 14% between 2025 and 2035, thereby expanding the installed base for smart infusion pumps and telemetry capable of safely dosing amiodarone, lidocaine, and esmolol. These investments expand the immediate addressable market for critical care antiarrhythmic drug therapies, especially intravenous formulations.

Aging Population and Comorbidities

The mean atrial fibrillation patient age in the United States reached 76 years during 2019-2023, and prevalence doubles with every decade after 50. Heart failure, hypertension, and chronic kidney disease add complexity, so 80.64% of U.S. patients receive rate control and 31.02% receive rhythm control. Japan and Western Europe—both aging rapidly—report similar multimorbidity patterns that tilt prescribers toward established agents with predictable pharmacokinetics, reinforcing sales momentum for amiodarone and beta blockers.

Technological Advancements in Drug Delivery and Monitoring

Baxter’s Novum IQ large-volume pump achieved 97% drug-library compliance just one month after installation, beating the industry average of 84%. The FDA’s strengthened infusion-pump guidance and ISMP standards encourage hospitals to adopt hard dose limits, automated secondary infusion management, and interoperability with electronic health records. In Saudi Arabia, early-alert sepsis systems now integrate real-time vitals, cutting response times for arrhythmia episodes. Continuous QTc monitoring mandated in the AHA’s 2025 standards further cements the purchase of advanced telemetry capable of detecting torsades de pointes risk with dofetilide or sotalol.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Drug Reactions and Safety Concerns | −0.8% | North America and European Union | Short term (≤ 2 years) |

| Stringent Regulatory and Approval Requirements | −0.6% | United States, EU, Japan | Medium term (2-4 years) |

| Competition from Device-Based Rhythm Management | −0.5% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Cost Pressures and Reimbursement Limitations | −0.4% | Global, most intense in public-payer systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Drug Reactions and Safety Concerns

AHA’s 2025 electrocardiographic monitoring statement obliges QTc tracking for dofetilide, sotalol, flecainide, and propafenone to curb torsades de pointes risk. Amiodarone continues to trigger pulmonary, thyroid, and hepatic adverse events, calling for repeated lab and imaging checks. Manual pump programming errors or low-flow inaccuracies can still produce overdoses, despite the march toward smart pumps. The cumulative safety burden limits uptake in facilities with scarce continuous monitoring, nudging some prescribers toward agents with shorter half-lives.

Stringent Regulatory and Approval Requirements

The FDA’s infusion-pump life-cycle guidance asks for rigorous safety-assurance documentation, stretching review timelines and raising costs[2]U.S. Food and Drug Administration, “Infusion pump total product life-cycle guidance,” FDA, fda.gov. Egypt’s new Drug Authority and value-based procurement rules similarly prolong approvals. Absence of explicit dosing parameters during cardiopulmonary bypass creates legal uncertainty, deterring rapid label expansions. Collectively, these hurdles slow the entry of innovative formulations, reinforcing incumbent dominance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Beta Blockers Retain the Lead While Potassium Blockers Accelerate

Beta blockers captured 34.65% of 2025 sales, buoyed by 80.64% rate-control usage among U.S. atrial fibrillation patients and perioperative recommendations from cardiothoracic societies. This entrenched profile provides a stable revenue base for the critical care antiarrhythmic drugs market. Potassium channel blockers, led by amiodarone and dofetilide, will log an 8.65% CAGR to 2031 as clinicians seek rhythm-control options for refractory cases. Calcium channel blockers remain a second-line choice for narrow-complex tachycardias, while sodium channel blockers such as lidocaine and procainamide preserve relevance in shock-refractory ventricular fibrillation. The “other” segment, including adenosine and digoxin, serves niche indications but maintains formulary presence due to guideline support in specific tachyarrhythmia algorithms.

A steady pipeline sustains therapeutic diversity. Lupin’s generic dronedarone lowers average selling prices, while Novartis’ Phase 2 study of PKN605 illustrates long-range innovation. Smart pump integration favors agents with well-defined infusion protocols, a factor that helps beta blockers and amiodarone hold share. Yet patent expiries and global generic capacity keep competitive tension high, making differentiated safety or delivery profiles critical for future entrants in the critical care antiarrhythmic drugs market.

By Disease Type: Supraventricular Arrhythmias Dominate, Ventricular Growth Outpaces

Supraventricular arrhythmias represented 52.45% of 2025 demand, propelled by escalating atrial fibrillation prevalence and new self-administration options such as etripamil. The critical care antiarrhythmic drugs market for supraventricular disorders will continue to expand due to an aging population and guideline-driven adoption of rhythm-control therapies. Ventricular arrhythmias, though smaller today, are on an 8.76% CAGR upswing, linked to guideline mandates for post-myocardial-infarction beta-blocker therapy and persistent out-of-hospital cardiac arrest incidence. Arrhythmia-related mortality trends further justify aggressive treatment strategies, supporting durable volume growth across both segments.

ICU sepsis episodes often precipitate new-onset atrial fibrillation, keeping intravenous beta-blocker and calcium-channel-blocker demand high. Device therapies continue to siphon off certain refractory cases, yet acute episodes and resource-limited regions still rely heavily on pharmacologic options, preserving market breadth across disease categories.

By Route of Administration: Oral Products Dominate but Intravenous Lines Gain Momentum

Oral formulations accounted for 54.56% of 2025 sales, as chronic maintenance therapy remains widespread. Nonetheless, the heightened adoption of loading doses and continuous infusions in critical-care units is expected to drive a 9.21% CAGR for parenteral formats through 2031. Baxter’s ready-to-use injectables and Novum IQ platform underscore hospital preference for premixed, error-reducing solutions that shorten nurse preparation time. Meanwhile, the first-in-class nasal spray, etripamil, opens the door to alternative routes, albeit from a small base, signaling potential diversification in delivery options within the critical care antiarrhythmic drugs market.

Pharmacokinetic challenges during cardiopulmonary bypass and the need for dose precision empower smart pump developers, driving a tighter link between device and drug sales. Reimbursement favoring generics may limit branded intravenous uptake, but safety-feature investments can still tilt buying decisions toward premium systems that minimize medication errors.

By Distribution Channel: Hospitals Rule, Digital Dispensing Rises

Hospital pharmacies supplied 62.45% of 2025 volumes, reflecting the need for real-time ECG monitoring during initiation of drugs such as amiodarone and dofetilide. Intensive-care bed growth in China and Saudi Arabia will sustain hospital dominance, yet the online channel is projected to clock a 9.65% CAGR through 2031. Generic launches encourage mail-order platforms to offer lower prices for maintenance prescriptions, a trend supported by expanding e-traceability in markets like Egypt. Retail chains retain their place for chronic refills but face erosion as payers steer beneficiaries to lower-cost digital options, especially for stable atrial fibrillation patients.

Mandatory in-person monitoring for certain agents limits the spillover of high-risk prescriptions to online pharmacies, so growth will concentrate on drugs with wide therapeutic indices and limited laboratory requirements. Hospitals are countering channel leakage by coupling drug procurement with device contracts and using integrated dosing software as a retention tool in the critical care antiarrhythmic drugs market.

Geography Analysis

North America generated 42.56% of 2025 revenue. A projected 14% rise in ICU days by 2035, paired with 4.83 million atrial fibrillation patients, maintains solid baseline consumption. CMS reimbursement rules now favor generics, compressing unit prices but keeping patient access high. Milestone’s nasal spray provides the first self-administered option in the region, with market uptake hinging on commercial payer coverage. Canada and Mexico contribute smaller but steady volumes through regulatory harmonization and cross-border supply chains that support generic inflows.

Europe remains the second-largest region, underpinned by 957,812 incident atrial fibrillation cases and uniform ESC guidelines that sustain rhythm-control therapy. Workforce shortages, particularly a forecast 4,200 critical-care nurse gap in the United Kingdom, pressure budgets and strengthen generic bargaining power. Western European payers leverage centralized tenders to secure low prices, while Eastern Europe records the fastest unit growth as critical-care capacity expands from a low base.

Asia-Pacific posts the quickest aggregate expansion at a 7.54% CAGR to 2031. China’s ICU-bed mandate, Japan’s aging population, India’s growing generic production, and Australia’s comprehensive reimbursement pathway collectively expand the critical care antiarrhythmic drugs market in the region. South Korea, Indonesia, and Vietnam represent emerging pockets, balancing rising cardiac admissions against affordability constraints that tilt preferences toward digoxin or generic amiodarone.

The Middle East and Africa show uneven progress. Saudi Arabia leads infrastructure spending with new cardiac ICUs and electronic early-warning systems, while Egypt targets a 30-per-10,000 bed ratio by 2030. However, many sub-Saharan countries remain limited by budget and workforce shortfalls, leaving penetration low. South America, led by Brazil, benefits from blended public-private pay systems and an established manufacturing base, yet currency volatility continues to challenge price stability.

Competitive Landscape

The critical care antiarrhythmic drugs market is moderately fragmented. Baxter, Fresenius Kabi, and Hikma dominate the injectable shelves through bundled device-and-drug offerings. Baxter’s 2024 rollout of six ready-to-use injectables paired with Novum IQ infusion pumps illustrates a defense built on safety software and service contracts. Fresenius Kabi leverages broad intensive-care portfolios to negotiate volume-based discounts, while Hikma expands its U.S. footprint via generic ephedrine and other cardiovascular injectables.

Generic challengers intensify price pressure. Lupin’s 2024 dronedarone approval introduced immediate erosion for the once-premium brand. Indian peers such as Aurobindo and Sun Pharma scale global supply chains that feed formulary decisions in both mature and emerging markets. Meanwhile, Milestone Pharmaceuticals captured mindshare with etripamil, the first nasal-spray calcium-channel blocker, positioning itself to disrupt emergency department protocols. Novartis’ mid-stage pipeline asset hints at longer-term brand-name entrants, although regulatory timelines extend beyond 2031.

Hospitals increasingly demand interoperability between electronic health records and infusion devices, favoring vendors that offer full-service agreements and real-time analytics. This bundling erects switching barriers: once a facility standardizes on a pump platform, rival drug suppliers must integrate to win share. Opportunities for newcomers, therefore, concentrate on artificial-intelligence-enabled dosing algorithms, fixed-dose combination products that simplify polypharmacy, and point-of-care pharmacogenomics that tailor drug choice to individual torsades risk.

Critical Care Antiarrhythmic Drugs Industry Leaders

Pfizer Inc.

Novartis AG

Sanofi S.A.

Baxter International Inc.

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Milestone Pharmaceuticals received FDA approval for etripamil nasal spray (Cardamyst) for adult paroxysmal supraventricular tachycardia, introducing the first self-administered calcium-channel blocker.

- December 2025: Novartis began a Phase 2 randomized trial of PKN605 for atrial fibrillation, signaling sustained investment in novel rhythm-control mechanisms

- September 2024: BD, one of the leading global medical technology companies, acquired Edwards Lifesciences' Critical Care product group, which will be renamed as BD Advanced Patient Monitoring.

Global Critical Care Antiarrhythmic Drugs Market Report Scope

As per the scope of the report, critical care antiarrhythmic drugs are medications used in emergency and intensive care settings to manage and restore normal heart rhythm in patients experiencing life-threatening arrhythmias. They help stabilize the cardiac electrical activity and prevent complications such as stroke or cardiac arrest. These drugs are administered under close medical supervision due to their potent effects and potential side effects.

The Critical Care Antiarrhythmic Drugs Market is Segmented by Drug Class (Beta Blockers, Calcium Channel Blockers, Sodium Channel Blockers, Potassium Channel Blockers, and Others), Disease Type (Supraventricular Arrhythmias, Ventricular Arrhythmias, and Others), Route Of Administration (Oral, Parenteral, and Other Route Of Administrations), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Beta Blockers |

| Calcium Channel Blockers |

| Sodium Channel Blockers |

| Potassium Channel Blockers |

| Other Drug Classes |

| Supraventricular Arrhythmias |

| Ventricular Arrhythmias |

| Other Disease Type |

| Oral |

| Parenteral |

| Other Route Of Administrations |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Class | Beta Blockers | |

| Calcium Channel Blockers | ||

| Sodium Channel Blockers | ||

| Potassium Channel Blockers | ||

| Other Drug Classes | ||

| By Disease Type | Supraventricular Arrhythmias | |

| Ventricular Arrhythmias | ||

| Other Disease Type | ||

| By Route Of Administration | Oral | |

| Parenteral | ||

| Other Route Of Administrations | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the critical care antiarrhythmic drugs market?

The market was valued at USD 1.24 billion in 2025 and is projected to reach USD 1.71 billion by 2031.

Which drug class holds the largest share in hospital critical-care settings?

Beta blockers lead with 34.65% share because of their dual rate-control and post-infarction prophylactic roles.

How fast is the Asia-Pacific region expanding?

Asia-Pacific is expected to post a 7.54% CAGR through 2031, the fastest among all regions.

What factor is driving intravenous formulation growth?

Adoption of smart infusion pumps and wider use of loading doses in ICUs are pushing parenteral products at a 9.21% CAGR.

Which new product may shift supraventricular tachycardia care away from emergency rooms?

FDA-approved etripamil nasal spray lets patients self-terminate episodes, potentially reducing hospital visits.

Are smart pumps influencing procurement decisions?

Yes, hospitals increasingly favor suppliers offering infusion devices with embedded safety software and drug-library integration.

Page last updated on: