Collagen Dressings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

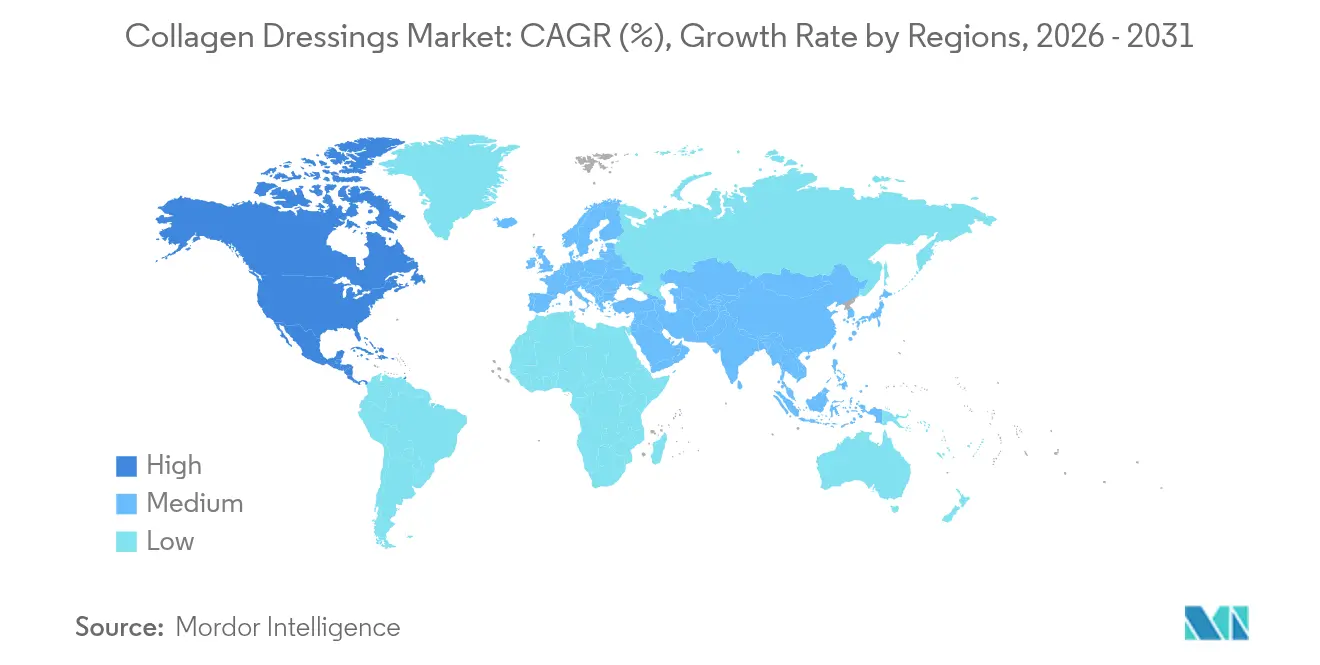

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

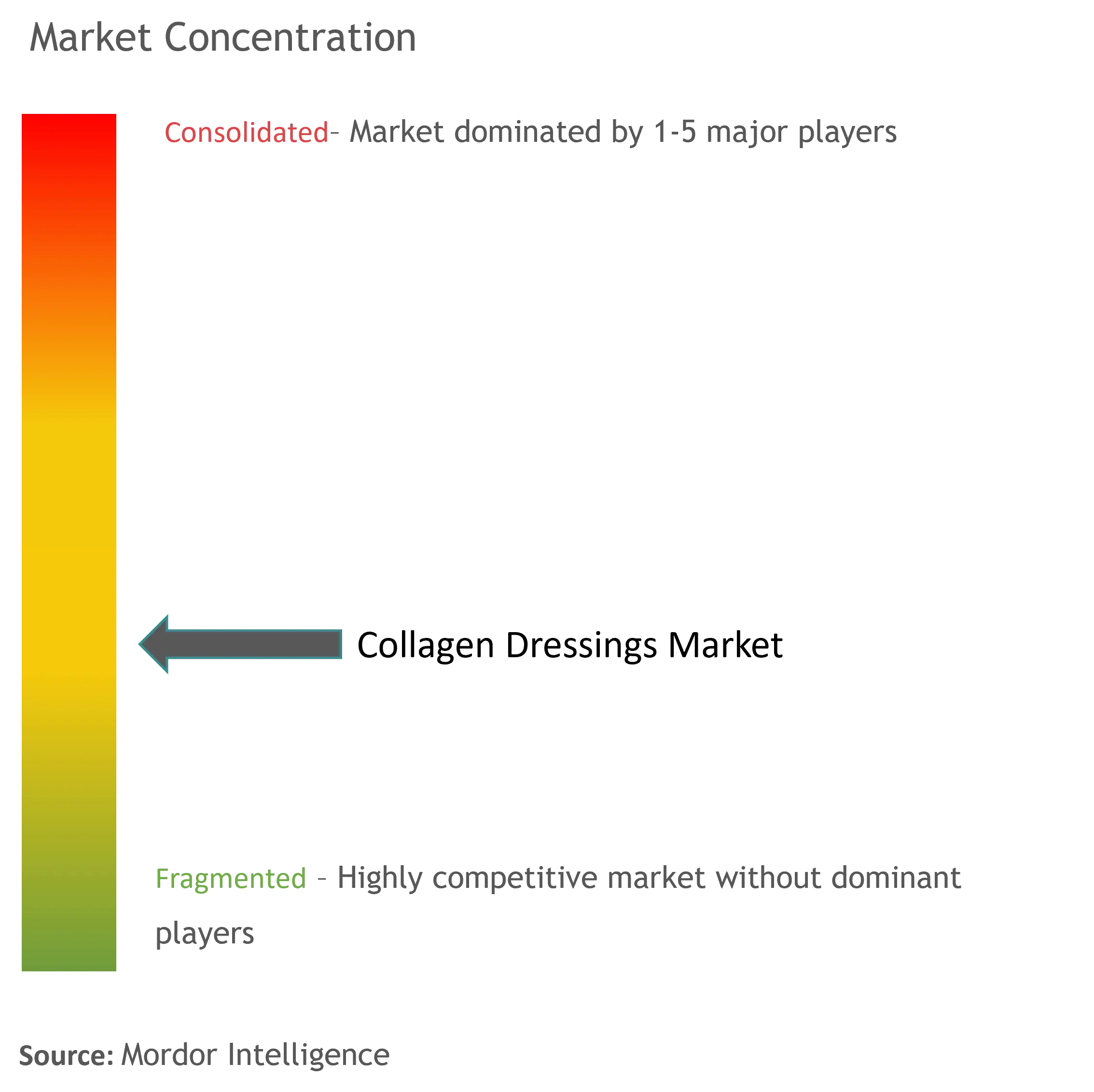

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Collagen Dressings Market Analysis by Mordor Intelligence

The collagen dressings market size was valued at USD 1.25 billion in 2025 and estimated to grow from USD 1.32 billion in 2026 to reach USD 1.68 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). Demand momentum stems from a rising global caseload of acute and chronic wounds, larger surgical volumes, and a growing preference for bioactive wound care solutions that shorten healing time and minimize complications. Market expansion is tempered by supply‐chain and regulatory cross-currents, including stricter evidence expectations for diabetic foot ulcer care and a pending United States Food and Drug Administration (FDA) wound-dressing reclassification proposal that could reshape compliance costs. Intensifying research around recombinant and plant-based materials promises to ease sourcing constraints while lowering immunogenic risk, and smart-sensor integration is linking dressings to wider digital-health ecosystems. Competitive intensity is therefore shifting toward firms that combine material science, data analytics, and strong clinical dossiers, enabling them to capture share in the collagen dressings market.

Key Report Takeaways

- By source, bovine collagen held 41.25% of collagen dressings market share in 2025 while equine collagen is projected to advance at a 5.61% CAGR through 2031.

- By form, gel formats led with 27.80% revenue contribution in 2025; sheet formats are expected to expand at 5.72% CAGR to 2031.

- By application, acute wounds commanded 60.90% share of collagen dressings market size in 2025 and chronic wounds are set to grow at a 5.66% CAGR to 2031.

- By end user, hospitals remained the primary channel in 2025, whereas ambulatory surgical centers are forecast to post the fastest growth at 5.68% CAGR to 2031.

- North America dominated with 41.10% share of collagen dressings market size in 2025; Asia-Pacific is the fastest-growing region at 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Collagen Dressings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of acute & chronic wounds | +1.2% | Global, with concentration in aging populations of North America and Europe | Medium term (2-4 years) |

| R&D & technological advancements in collagen dressings | +0.8% | North America & EU leading innovation, APAC adoption following | Long term (≥ 4 years) |

| Growing number of surgical procedures worldwide | +0.9% | Global, with emerging markets in APAC showing highest growth | Short term (≤ 2 years) |

| Increasing prevalence of diabetes-linked chronic ulcers | +0.7% | Global, particularly acute in developing nations with rising diabetes rates | Medium term (2-4 years) |

| Recombinant & plant-based collagen reducing immunogenicity | +0.4% | Developed markets initially, expanding to global adoption | Long term (≥ 4 years) |

| Smart sensor–integrated collagen dressings enabling remote monitoring | +0.3% | North America and EU early adopters, gradual APAC penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Acute & Chronic Wounds

Global lifestyle and demographic shifts are pushing wound prevalence higher. Diabetes affects more than 537 million adults worldwide and 44.4% of them show peripheral neuropathy, a major risk factor for chronic ulcers [1]Taylor & Francis, “Peripheral Neuropathy in Diabetes: Global Prevalence,” Nature, nature.com. Health systems have responded by assembling dedicated wound-care teams; one Korean tertiary facility treated 180,872 wound cases between 2018-2022 while achieving high patient-satisfaction scores. Economic pressure is mounting: in Australia chronic wounds add USD 2 billion-USD 4 billion in annual outlays. Such demand pulls advanced solutions into mainstream formularies and elevates collagen dressings market penetration. Home-care uptake is intensifying after Medicare introduced caregiver training reimbursement in 2025, encouraging wider at-home treatment.

R&D and Technological Advances in Collagen Dressings

Bioengineering is addressing the limitations of animal-derived collagen. Evonik’s VECOLLAN recombinant platform eliminates animal-borne pathogens and batch variability through fermentation-based production [2]Evonik Industries AG, “VECOLLAN – Recombinant Collagen Platform,” corporate.evonik.com. Carnegie Mellon’s FRESH 3D bioprinting technique fabricates vascularized tissue entirely from collagen, paving the way for next-generation personalized grafts. Smart bandages embedding bioelectric sensors have delivered 99.75% closure versus 94.00% for standard care in controlled trials. Such innovations can lift treatment outcomes and safeguard supply, propelling the long-term trajectory of the collagen dressings market.

Growing Number of Surgical Procedures Worldwide

Elective and emergency surgeries are rising alongside deeper penetration of advanced operating facilities in emerging nations. Updated 2024 CDC surgical-site-infection guidelines endorse negative-pressure approaches for select procedures, implicitly nudging hospitals toward bioactive dressings. Solventum’s V.A.C. Peel and Place Dressing cuts application time by 61% and cost by 41%while sustaining a seven-day wear window, illustrating how efficiency imperatives foster adoption [3]Solventum, “V.A.C. Peel and Place Dressing Launch,” solventum.com. As post-operative care migrates to outpatient settings, demand concentrates on dressings that pair ease of use with extended protection, keeping the collagen dressings market on a growth path.

Increasing Prevalence of Diabetes-Linked Chronic Ulcers

Diabetic foot ulcers (DFUs) pose a clinical and economic burden, costing the United Kingdom’s National Health Service USD 7,800 per case annually. The International Working Group on the Diabetic Foot’s 2023 guideline cautions against routine collagen use due to low-certainty evidence, compelling firms to fortify clinical data. At the same time, the American Heart Association’s 2024 statement promotes multidisciplinary DFU care, opening space for collagen systems that integrate vascular and metabolic considerations. Companies able to link superior outcomes to solid evidence stand to widen share across the collagen dressings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternate advanced wound dressings | -0.6% | Global, with mature markets showing higher substitution rates | Short term (≤ 2 years) |

| High cost of next-generation collagen dressings | -0.4% | Emerging markets primarily, cost-sensitive healthcare systems | Medium term (2-4 years) |

| Stringent animal-sourcing & regulatory hurdles | -0.3% | EU and North America leading regulatory tightening | Medium term (2-4 years) |

| Supply bottlenecks for medical-grade bovine collagen | -0.2% | Global, with US domestic sourcing particularly constrained | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Alternate Advanced Wound Dressings

Amniotic membrane-derived products such as AMNIODERM+ achieved 95.5% wound-size reduction in diabetic ulcer trials, setting high performance bars for competing modalities. Negative-pressure systems continue to gain traction after studies showed enhanced closure rates over traditional options. Hydrocolloid and alginate dressings hold cost advantages for routine care, while antimicrobial coatings tackle infection control gaps. The FDA’s 2024 proposal to reclassify antimicrobial dressings may increase compliance costs for those technologies, creating mixed competitive effects but generally keeping pricing pressure on the collagen dressings market.

High Cost of Next-Generation Collagen Dressings

Recombinant collagen platforms need specialized bioreactors, pushing unit costs beyond traditional bovine equivalents, which constrains adoption in resource-limited settings. United States supply satisfies only 30-40% of domestic demand, causing price fluctuations that ripple through hospital procurement cycles. Reimbursement structures require clear clinical justification for high-priced products, and administrative burden slows uptake. Manufacturers must therefore demonstrate cost-per-quality-adjusted-life-year superiority, a hurdle that tempers the near-term expansion of the collagen dressings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Bovine Dominance Faces Innovation Pressure

Bovine-derived materials captured 41.25% collagen dressings market share in 2025 on the back of decades-long clinical familiarity and scalable rendering infrastructure. However, only 30-40% of United States demand is met domestically, creating exposure to global supply shocks. Equine collagen is gaining ground at a 5.61% CAGR, supported by superior biocompatibility and a lower immunogenic profile. Porcine options provide cost advantages and structural similarity to human collagen, while marine sources offer thermal stability beneficial in tropical regions. Recombinant human collagen is emerging as a disruptive force; Evonik’s fermentation-based VECOLLAN promises consistent purity and potentially leaner quality-assurance footprints. Plant biotechnologies are advancing as sustainability requirements rise across European tenders. Taken together, the source landscape is moving toward diversified and traceable supply, giving manufacturers that invest early a chance to lock in strategic positions within the collagen dressings market.

Growing ethical concerns over animal welfare and strict European sustainability mandates are catalyzing the shift toward recombinant and plant-based alternatives. PlantForm Corporation’s synthetic biology route to bioidentical human collagen exemplifies the shift toward engineered solutions that dovetail with circular-economy policies. Yet raw-material cost, scalability, and regulatory clarity remain development hurdles. Firms able to offer end-to-end traceability and stable pricing will meet hospital procurement criteria more easily, a requirement likely to influence future collagen dressings market size. Over the forecast period, multi-source strategies that blend animal, recombinant, and plant inputs are expected to cushion companies against supply disruptions and regulatory shocks while boosting clinician confidence.

By Form: Gel Leadership Challenged by Sheet Innovation

Gel products claimed 27.80% revenue in 2025 due to their ability to conform to irregular surfaces and fill undermining tissue spaces. Sheets, however, are projected to outpace all other forms at 5.72% CAGR to 2031 as hospitals prefer standardized dosing, reduced fiber shedding, and longer wear times. Powder and particulate formats serve niche deep-cavity applications, whereas foams handle high-exudate wounds but face higher manufacturing complexity. Composite sheets embedding silver ions or growth factors bring multipronged therapeutic effects that appeal to trauma centers seeking antibiotic stewardship.

Advances in freeze-drying and electrospinning now allow sheet dressings to retain structure for up to seven days, lowering nursing time. Multi-layer laminates can modulate moisture and oxygen tension, thereby improving granulation. As outpatient surgery volumes grow, devices that require fewer dressing changes resonate with both providers and patients, bolstering collagen dressings market size growth. Manufacturers with cross-format capability can shift production toward fast-growing segments when margins tighten, securing resilience in a competitive environment.

By Application: Acute Dominance with Chronic Acceleration

Acute indications accounted for 60.90% of collagen dressings market size in 2025, reflecting standardized post-surgical protocols and the urgency of traumatic wound care. Chronic ulcers, spanning diabetic, venous, and pressure ulcers, form the market’s fastest-expanding subset at 5.66% CAGR, underpinned by an aging population and escalating diabetes prevalence. In burns, collagen matrices act as temporary skin substitutes that reduce pain and fluid loss, while surgical wounds benefit from the material’s hemostatic and scaffold properties. DFUs illustrate the tension between guideline skepticism and real-world need: clinicians still look for bioactive dressings that foster rapid closure despite current evidence gaps.

Health-economic models suggest that shortening chronic-wound closure time by even one week can save USD 1,200 per patient in avoided nursing visits. This fiscal incentive propels payers toward covering premium collagen combinations that offer antimicrobial or growth-factor benefits. Personalized wound management platforms are emerging, in which clinicians select formulations based on wound etiology and biomarker feedback, reinforcing segmentation inside the collagen dressings market. As electronic health records integrate wound photos and sensor data, the line between treatment and monitoring blurs, creating demand for dressings that double as data-collection devices.

By End User: Hospital Shift Toward Outpatient Models

Hospitals and specialty clinics remained the largest buyers in 2025 thanks to control over complex post-operative care. Nonetheless, ambulatory surgical centers and home-care settings now report the quickest uptake due to reimbursement models rewarding early discharge. The 2025 caregiver training codes under Medicare have already led to a measurable rise in advanced dressings dispensed directly to households. Long-term care institutions value extended-wear sheets that reduce labor; military and disaster-response teams prioritize products with ambient-temperature stability and rapid hemostasis.

The distributed-care trend changes purchasing criteria: safety, simple instructions, and digital readouts trump marginal improvements in absorption. Suppliers bundling dressings with telehealth dashboards can offer physicians remote visibility into healing progress, cementing differentiation in a crowded collagen dressings market. Vendors able to service multi-site networks gain leverage in pricing negotiations, as integrated delivery networks increasingly prefer single-source contracts to streamline inventory and training.

Geography Analysis

North America held 41.10% of collagen dressings market size in 2025 due to robust reimbursement systems, high surgical volumes, and early adoption of digital wound-care technologies. The FDA’s proposed reclassification of antimicrobial dressings may shift competitive dynamics, potentially easing comparative hurdles for plain collagen products while raising the bar for blended antimicrobial formats. Domestic bovine collagen scarcity keeps input costs volatile, but strong venture funding for recombinant routes offers buffers against future shocks. Regional research clusters in Pittsburgh and Boston continue to spin out innovations such as 3D bioprinted collagen vascular grafts.

Asia-Pacific is projected to grow at 5.12% CAGR through 2031, the fastest among all regions. Rising medical tourism in Thailand and India further boosts advanced-dressing demand, with hospitals targeting international accreditation standards that require evidence-backed products. Cost-sensitive payers drive interest in marine and plant-derived collagen as local fisheries and agritech ventures scale supply.

Europe represents a mature yet innovation-oriented zone where stringent animal-welfare rules and carbon-footprint targets steer procurement toward traceable sources. Germany and the Nordic countries are trialing “green” purchasing frameworks that score suppliers on life-cycle analysis. Recombinant and vegan collagens such as NovaColl rolled out by Brenntag and Cambrium cater to this strategic shift. While budget constraints encourage tendering for low-price options, clinical-outcome guarantees increasingly appear in contracts, suiting vendors able to supply both efficacy data and sustainability credentials. Taken together, regional nuances create targeted opportunities for diversified players across the collagen dressings market.

Competitive Landscape

The collagen dressings market features moderate fragmentation, with diversified device conglomerates coexisting alongside focused biotech innovators. Organogenesis lifted Advanced Wound Care revenue in 2024 after securing additional 510(k) clearances including PuraPly Micronized Wound Matrix.

Strategically, incumbents are doubling down on vertical integration of raw-material supply to ward off shortages, while partnering with sensor and software firms to embed connectivity. Evonik’s fermentation platform collaboration roadmap illustrates a push to own proprietary sources that bypass animal supply. Coloplast’s USD 1.3 billion acquisition of Kerecis in 2023 provided fish-skin collagen technology that complements its European footprint and sustainability agenda. Emerging challengers target niche clinical unmet needs with recombinant, plant-based, or smart dressings that gather wound-environment data. Although smaller companies often depend on contract manufacturing, the rise of modular bioreactors lowers entry barriers by reducing capex.

Price competition remains fierce in commoditized gel and powder lines, yet premiumization is evident in composite sheets that promise infection control, pain reduction, and remote monitoring. Suppliers differentiating through clinical-outcome evidence and economic-value dossiers win preferred-supplier status within integrated delivery networks. Over the forecast term, competitive advantage hinges on aligning R&D pipelines with regulatory trends and payer expectations, ensuring sustained expansion in the collagen dressings market.

Collagen Dressings Industry Leaders

3M

Smith+Nephew

McKesson Medical-Surgical Inc.

DermaRite Industries, LLC.

Convatec Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Yokohama National University unveiled a 3D-printing method that creates collagen tissues with multi-directional fiber alignment, enabling grafts with near-native mechanical properties.

- January 2025: Brenntag partnered with Cambrium to introduce NovaColl vegan collagen across Europe and the United Kingdom, using precision fermentation to produce skin-identical micro-molecular collagen GCI Magazine.

- January 2024: Sanara MedTech Inc. entered an exclusive license agreement with Tufts University to develop and commercialize patented technology covering 18 unique collagen peptides.

- July 2023: Coloplast Corp. agreed to acquire Kerecis, a fish-skin-based wound-care company, for USD 1.3 billion to widen its advanced wound-care portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the collagen dressings market as all sterile wound-management products whose primary structural component is purified collagen (bovine, porcine, equine, avian, marine, recombinant, or plant) presented in sheets, gels, powders, foams, or composite matrices that remain in situ to modulate exudate and accelerate granulation tissue formation. According to Mordor Intelligence, products used strictly as topical cosmetic masks or oral nutraceuticals are excluded.

Scope Exclusion: Temporary hemostatic sponges and collagen-coated sutures are outside this report.

Segmentation Overview

- By Source

- Bovine

- Porcine

- Avian

- Marine

- Recombinant Human Collagen

- Plant-based Collagen

- By Form

- Gel

- Powder

- Sheet

- Paste

- Foam

- Particulate/Granule

- Combination & Composite Formats

- By Application

- Acute Wounds

- Surgical & Traumatic Wounds

- Burns (Partial & Full Thickness)

- Chronic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Acute Wounds

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home-Care Settings

- Long-Term Care Facilities

- Military & Field Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple hours of semi-structured interviews with hospital wound-care nurses, procurement heads at group purchasing organizations in North America, Europe, and Asia-Pacific, and product managers at regional manufacturers helped us stress-test usage rates, average selling prices, and reimbursement shifts that secondary material alone could not clarify.

Desk Research

Mordor analysts began with publicly available wound-care surveillance from agencies such as the US Centers for Medicare & Medicaid Services, Eurostat, and Japan's MHLW, followed by chronic-wound prevalence data from the International Diabetes Federation and WHO. Trade-flow statistics from UN Comtrade, patent families retrieved via Questel, and product utilization tallies from the Norway Road Federation (for pressure-injury incidence proxies) strengthened the demand pool. We then reviewed clinical-trial registries, peer-reviewed journals, and 10-K filings that disclose sales of advanced dressings, cross-checking unit volumes against shipment tallies in Volza. These sources built the factual spine. D&B Hoovers and Dow Jones Factiva filled financial gaps. This list is illustrative, not exhaustive, and many additional references informed validation.

Market-Sizing & Forecasting

A top-down incidence model converts treated chronic and acute wound cases into addressable demand, using prevalence trends, surgical procedure counts, burn admissions, and average number of dressings per patient episode. These outputs are corroborated through selective supplier roll-ups and sampled ASP × volume checks. Key variables like diabetic foot-ulcer prevalence, hospital inpatient days, bovine collagen price indices, and antimicrobial adoption rates drive scenario inputs. Multivariate regression with lagged macro-health indicators projects 2026-2030 growth; gap years are linearly interpolated when bottom-up evidence is thin.

Data Validation & Update Cycle

Before sign-off, we rerun variance screens, peer review anomalies, and reconcile currency conversions. Models refresh every twelve months, with mid-cycle tweaks triggered by major regulatory or recall events. A final analyst pass occurs just before client delivery so users receive the latest view.

Why Mordor's Collagen Dressings Baseline Commands Reliability

Published estimates often differ because firms pick uneven product mixes, inflate clinician uptake, or backcast from broad wound-care totals. Our disciplined definition, annual refresh cadence, and variable-level cross-checks keep numbers reproducible.

Key gap drivers include rival studies bundling topical hemostats, assuming uniform ASP escalation, or anchoring forecasts to single-region prevalence trends that ignore emerging-market acceleration and currency effects.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.26 B (2025) | Mordor Intelligence | - |

| USD 2.21 B (2024) | Global Consultancy A | Bundles hemostatic sponges and bioengineered skin substitutes, inflating base value |

| USD 0.72 B (2025) | Industry Journal B | Uses static ASPs and omits outpatient home-care volumes, compressing market total |

Taken together, the comparison shows that Mordor's figures sit between aggressive and conservative peers because our scope, variable selection, and yearly validation steps create a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

How big is the Collagen Dressings Market?

The Collagen Dressings Market size is expected to reach USD 1.32 billion in 2026 and grow at a CAGR of 4.92% to reach USD 1.68 billion by 2031.

Who are the key players in Collagen Dressings Market?

3M, Smith+Nephew, McKesson Medical-Surgical Inc., DermaRite Industries, LLC. and Convatec Group PLC are the major companies operating in the Collagen Dressings Market.

Which is the fastest growing region in Collagen Dressings Market?

Asia-Pacific is forecast to grow at 5.12% CAGR through 2031 due to expanding wound-care infrastructure and rising chronic disease prevalence.

Which region has the biggest share in Collagen Dressings Market?

In 2025, the North America accounts for the largest market share in Collagen Dressings Market.

Which source segment dominates the collagen dressings market?

Bovine collagen leads with 41.25% share, although equine and recombinant sources are gaining ground.

Page last updated on: