Thermo Compression Forming Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

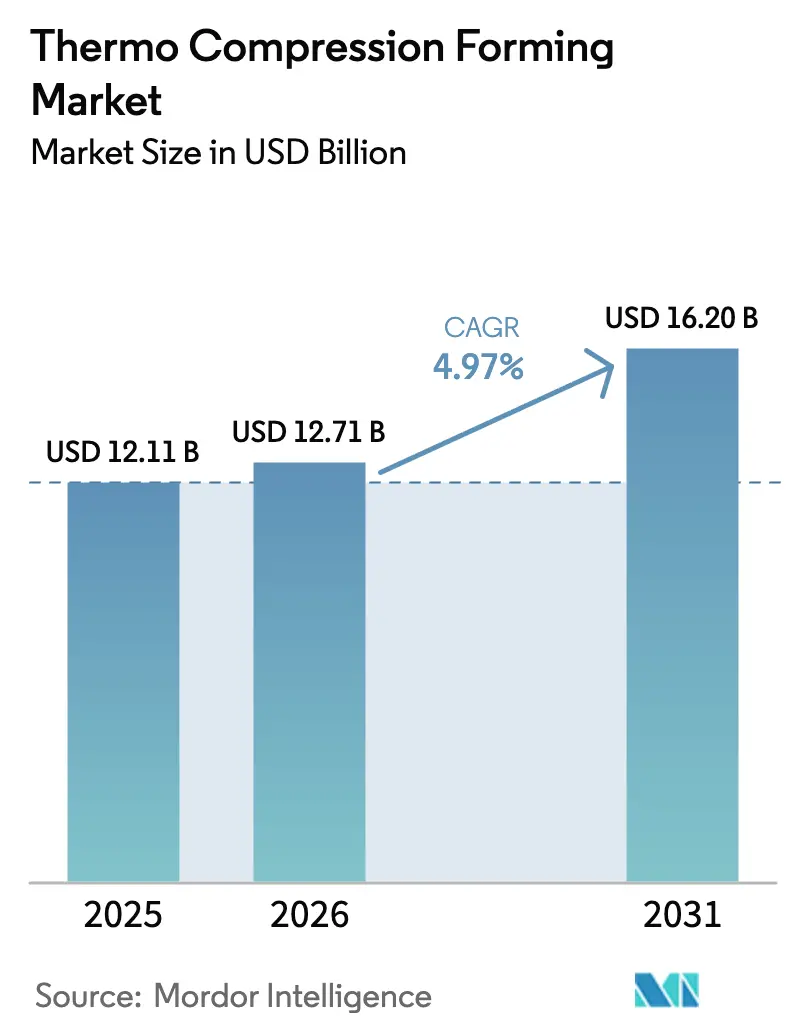

| Market Size (2026) | USD 12.71 Billion |

| Market Size (2031) | USD 16.20 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

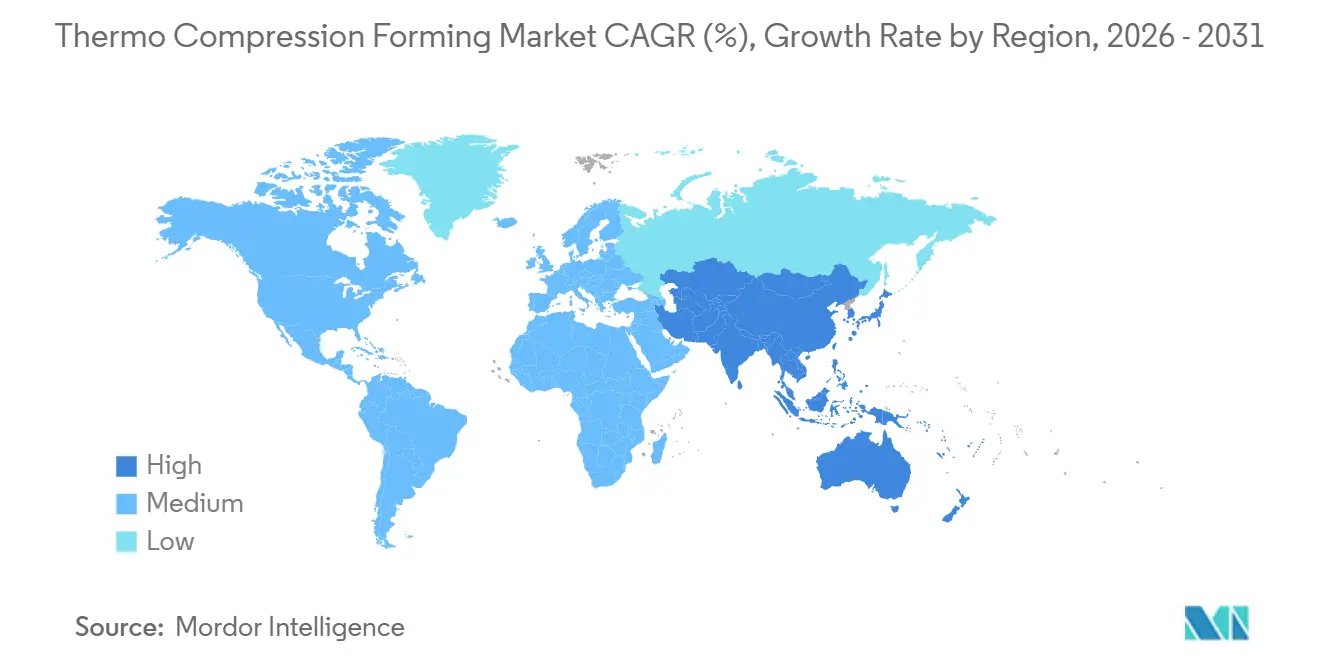

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermo Compression Forming Market Analysis by Mordor Intelligence

The Thermo Compression Forming Market size is projected to expand from USD 12.11 billion in 2025 and USD 12.71 billion in 2026 to USD 16.20 billion by 2031, registering a CAGR of 4.97% between 2026 to 2031. This growth comes as semiconductor backend steps closer to final assembly lines, supply-chain resilience becomes a boardroom mandate, and artificial-intelligence process control enters mainstream operations. Mounting demand for lightweight yet durable packaging, the migration of high-bandwidth-memory and chiplet architectures into series production, and rapid adoption of servo-hydraulic presses capable of 10,000 kN are expanding the installed base of equipment. At the same time, converters and equipment OEMs are embedding machine-learning analytics that flag dimensional drift milliseconds before a defect arises, trimming scrap rates below 0.5% and shortening design-for-manufacturability cycles. Sustainability pressures, especially in Europe and North America, favor bio-based polylactic acid, cellulose, and recycled PET sheet that can be re-extruded without significant molecular-weight loss, stimulating material-science partnerships between resin producers and converters.

Key Report Takeaways

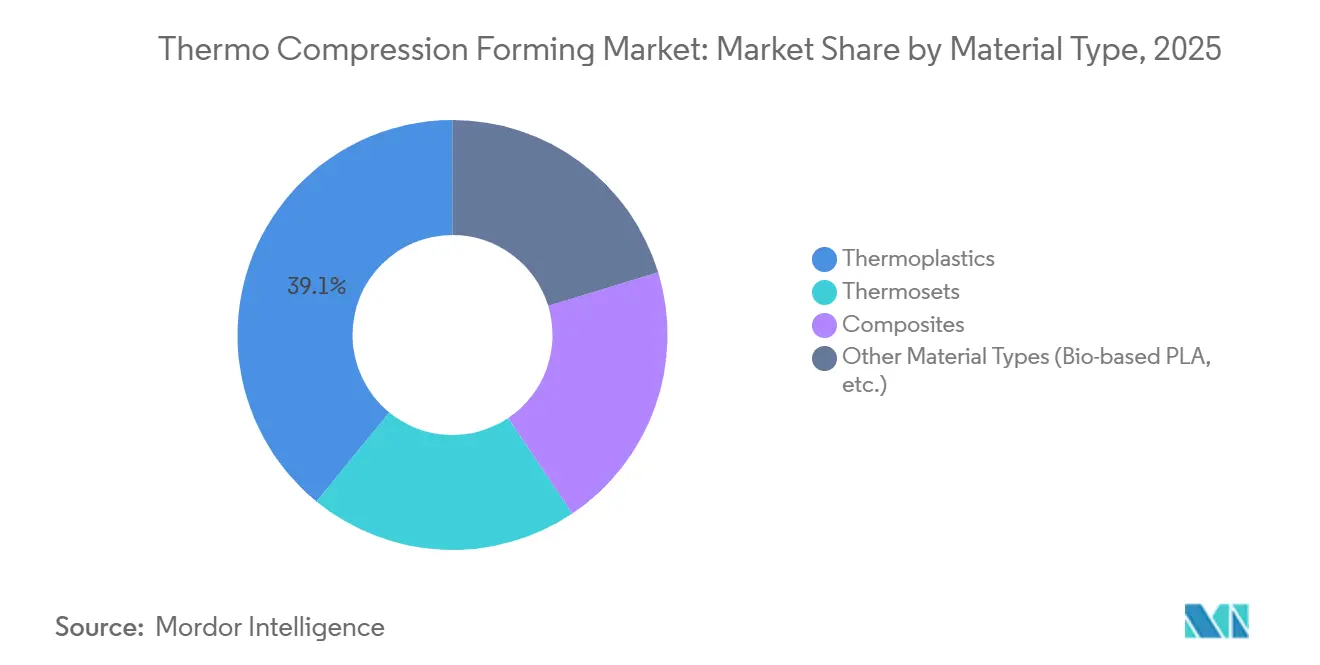

- By material type, thermoplastics led with 39.11% of the thermo compression forming market share in 2025, while other material types are forecast to expand at a 5.51% CAGR through 2031.

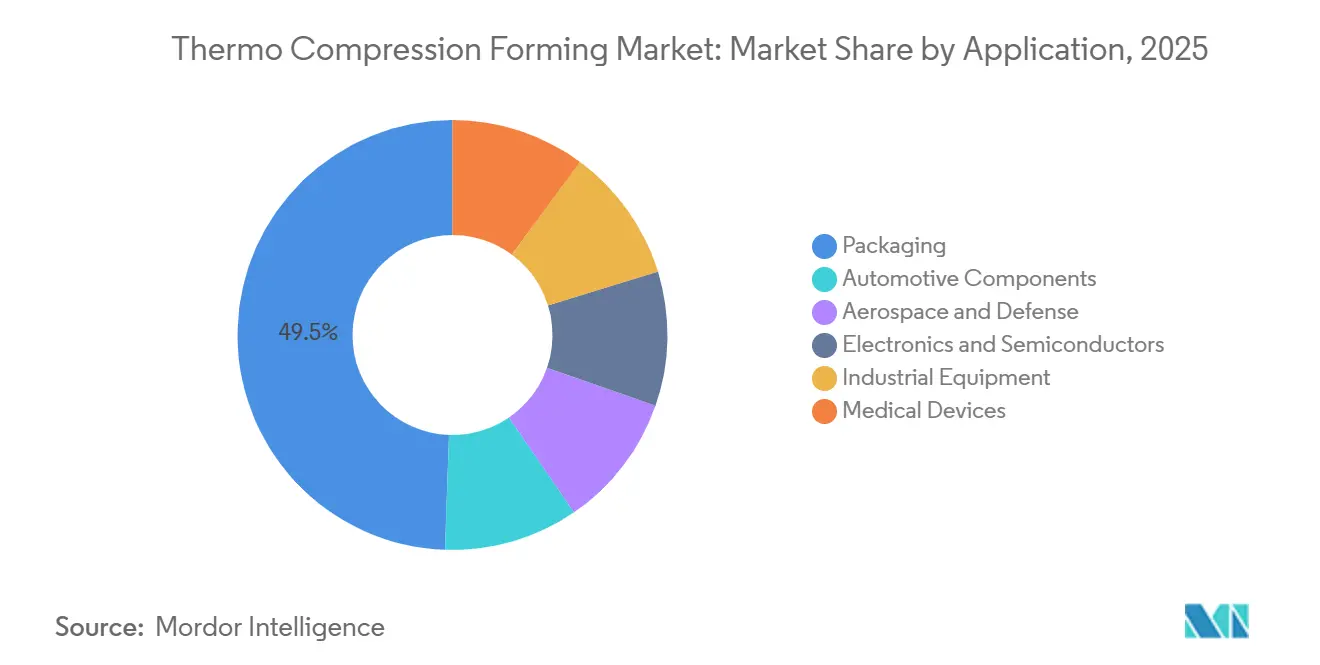

- By application, packaging contributed 49.45% of the thermo compression forming market share in 2025; the medical devices segment is advancing at a 5.96% CAGR through 2031.

- By geography, Asia-Pacific accounted for 45.24% of the thermo compression forming market share in 2025 and is set to grow at a 5.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thermo Compression Forming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Lightweight and Durable Packaging Solutions | +0.9% | Global, with concentration in North America and Europe for food-service and pharmaceutical applications | Medium term (2–4 years) |

| Increased Use in Electronics Assembly and Semiconductor Packaging | +1.4% | Asia-Pacific core (Taiwan, South Korea, China), spill-over to North America via CHIPS Act reshoring | Long term (≥ 4 years) |

| Supply-side Incentives for Reshoring Semiconductor Backend | +0.8% | United States (CHIPS Act), European Union (EU Chips Act), Japan (Economic Security Promotion Act) | Medium term (2–4 years) |

| In-line AI-driven Quality Analytics Enabling Zero-defect Forming | +0.6% | Global, early adoption in Germany, Japan, and United States for medical-device and automotive Tier 1 suppliers | Short term (≤ 2 years) |

| Ultra-fast-cycle Servo-hydraulic Presses More Than 10,000 kN Cutting Takt Time 40% | +0.7% | Global, with highest penetration in Asia-Pacific electronics assembly and European automotive clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Lightweight and Durable Packaging Solutions

Consumer-goods and pharmaceutical brands now specify thermoformed trays that match the barrier and drop-test credentials of injection-molded containers while trimming material mass 20-30%. Europe’s Packaging and Packaging Waste Regulation sets a 2030 deadline for recyclability or compostability, prompting converters to run wall sections below 0.5 mm without puncture failures[1]European Commission, “Packaging and Packaging Waste Regulation Proposal,” europa.eu. Nefab’s 2025 Tennessee hub re-grinds and re-extrudes scrap into new roll stock, letting OEMs log recycled-content metrics that feed ESG audits. Food-service chains further pull demand by switching to EN 13432-certified PLA clamshells that disintegrate in 90 days inside industrial composters, sparing landfill fees in California and Québec.

Increased Use in Electronics Assembly and Semiconductor Packaging

Heterogeneous integration relies on copper-to-copper hybrid bonds formed at 200-400 °C with ±1-2 µm alignment. SK Hynix earmarked KRW 19 trillion (USD 13 billion) for its P&T7 advanced-packaging fab to deliver 12-layer HBM3 stacks by 2027. ASE Technology’s 2026 USD 7 billion outlay will triple CoWoS-class capacity to 25,000 wafers per month and embed micro-fluidic channels for 120 kW AI racks. TOPPAN’s new flip-chip substrate line bonds 5 µm indium bumps for SWIR sensor arrays, confirming that Moore’s Law leverage now comes from minimizing interconnect latency rather than shrinking transistor gates.

Supply-side Incentives for Reshoring Semiconductor Backend

The United States CHIPS and Science Act dedicates USD 52.7 billion for domestic capacity, funneling USD 2 billion to Amkor’s Peoria backend site that will start thermo-compression operations in 2027. Europe’s Chips Act seeks 20% global output share by 2030, and Japan’s subsidies offset up to 50% of backend CapEx, catalyzing equipment suppliers to co-locate process-transfer labs near customer fabs. These incentives raise orders for modular bonders re-configurable for varied die sizes, shrinking the payback period for low-volume defense and medical lines.

In-line AI-Driven Quality Analytics Enabling Zero-defect Forming

Machine learning that samples 1,200 process data points per cycle now anticipates dimensional drift 30 ms before it manifests. KIEFEL’s SpeedGuard slashed medical-tray scrap from 3% to less than 0.5%, supplying OEMs that demand Cpk more than 1.67 on critical dimensions. WM Thermoforming’s Empower vision suite rejects micro-cracked blister packs at line-speed, a prerequisite for FDA serialization compliance. Simulated forming windows cut validation loops from 12 weeks to 4 weeks, an advantage when device lifecycles shrink to months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dimensional Drift in Ultra-thin Laminate Stacks | -0.5% | Global, acute in aerospace and automotive composite applications in North America and Europe | Medium term (2–4 years) |

| Competition from Low-pressure Thermo-form and Injection-compression | -0.4% | Global, with highest substitution risk in packaging and consumer-goods segments | Short term (≤ 2 years) |

| Scarcity of Heat-resistant Recyclable Composite Feedstock | -0.3% | Global, most severe in Europe due to stringent end-of-life regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dimensional Drift in Ultra-thin Laminate Stacks

Carbon-fiber laminates below 1.5 mm spring back more than 3° when formed above 180 °C because asymmetric ply orientation amplifies CTE mismatch. Laser-assisted forming tempers the outer surface to 250 °C while holding the core at 180 °C, but station retrofits run USD 200,000-400,000 and thus stay niche in aerospace stringers. Hexcel’s 40-minute-cure prepregs hit ±0.5 mm tolerances, yet designers must co-bond stiffeners that blunt the weight-saving rationale. In battery boxes, uneven pressure lifts fiber-volume fraction variability 5 points, a latent delamination trigger during thermal cycling.

Competition from Low-pressure Thermo-form and Injection-compression

Injection-compression injects melt into a partly open cavity, then compresses to net shape, reaching tolerances rivaling thermo compression forming at 20-30% lower clamp tonnage. Although tooling is pricier, consistent cavity filling lessens warpage, a win in instrument panels with molded-in ducts. Vacuum thermoforming at less than 0.5 MPa meanwhile undercuts capital costs for disposable trays, creaming share where aesthetics trump precision. Customers switching cite faster mold changes and easy insert-molding, hard to duplicate in compression without secondary steps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Thermoplastics Dominate, Bio-based Grades Surge

Thermoplastics captured 39.11% of the thermo compression forming market share in 2025 on the back of cycle-time compatibility and closed-loop scrap re-melt. Polypropylene, PET, and polycarbonate lead food, automotive, and electronics, while ABS serves housings demanding impact toughness. Other material types, including bio-based PLA, climb at a 5.51% CAGR through 2031, riding municipal bans on single-use plastics and new PLA grades that hold 100 °C hot-fill[2]European Bioplastics, “PLA Heat-Resistance Advancements,” europeanbioplastics.org .

Converters now blend recycled PET with barrier EVOH and structural PLA, forming multilayers that extend chilled-food shelf life from 7 to 10 days without oxygen pick-up. KIEFEL’s NATUREFORMER shapes cellulose into fresh-produce trays that home-compost in 12 weeks. Composite thermoplastics add carbon or glass fiber to meet electric-vehicle battery-tray rigidity, yet dimensional-drift and recycled-fiber scarcity temper uptake. Thermosets, while niche, remain irreplaceable where continuous 150 °C exposure demands phenolic flash-burn resistance.

Momentum will favor lines that swap tools quickly between PP and PLA sheets, integrate inline crystallinity measurement, and log life-cycle data to feed packaging EPR compliance. Firms that master barrier-layer co-extrusion and low-tension sheet feeding will ride the mix shift toward multilayer bio-based films.

By Application: Packaging Leads, Medical Devices Accelerate

Packaging commanded 49.45% of the thermo compression forming market size in 2025, with blister packs, clamshells, and ready-meal trays driving volume thanks to low tool cost and 500,000-cycle mold life. Pharma blister cards now route serialized QR codes, dovetailing with EU Falsified Medicines rules and U.S. DSCSA to authenticate dose packs at the dispenser.

Medical devices application is expected to grow at a 5.96% CAGR through 2031 as implantable OEMs outsource sterile-barrier systems validated under ISO 11607. UFP Technologies’ 2025 buyout of UNIPEC and TPI adds tight-tolerance battery shields and robotic-surgery drapes, bundling molding, assembly, and clean-room packout under ISO 13485. Automotive liners, under-body shields, and interior trim lean on large-format presses to cut assemblies from five metal stampings to one composite shot, shaving 15% vehicle mass. Aerospace panels claim carbon-fiber thermoplastics for weldable stringers that sidestep aluminum fatigue holes. Electronics trays insist on ±0.1 mm pockets to safeguard fragile dies, anchoring a premium niche for anti-static, ultra-flat carriers.

Geography Analysis

Asia-Pacific held 45.24% of 2025 revenue and will post a 5.84% CAGR to 2031 as Taiwan and South Korea scale advanced packaging and China continues electronics assembly. ASE’s USD 7 billion 2026 outlay adds Penang capacity, diversifying away from Taiwan and underpinning regional thermo-compression machine demand. Japan’s TOPPAN and Nissha invest in flip-chip substrates that call for sub-40 µm copper-pillar bonding, while China’s EV surge exceeds 8 million units, fueling battery-tray orders for servo-hydraulic presses.

North America’s share revives under CHIPS Act subsidies. Amkor’s Peoria plant, slated for 2027, will run thermo-compression for mission-critical aerospace chips, securing supply chains against geopolitical shocks. Nefab’s Tennessee hub meets auto OEM recycled-content targets, and Mexico’s medical device corridor leverages proximity to U.S. OEMs and lower labor costs.

Europe’s Packaging Waste Regulation steers converters into compostable PLA and cellulose trays. Germany, France, and the U.K. target EV lightweighting, using carbon-fiber compression molding to stretch range. Nordic grocers push PLA dairy cups, supported by robust composting infrastructure. Policy and high energy prices encourage equipment retrofits with energy-recovery hydraulics. The Middle-East and Africa build first-wave pharma-pack plants, yet recycling deficits hinder circular-economy adoption.

Competitive Landscape

The thermo compression forming market features low concentration. The five largest players held roughly 28% of 2025 revenue, but converter space remains atomized across thousands of regional firms. Competitive edge is transitioning from press tonnage to data fidelity; converters guaranteeing Cpk more than 1.67 through AI-assisted parameter control win aerospace and medical bids that pay 30-50% premiums. KIEFEL’s Speedformer line embeds SpeedGuard analytics and computer vision, moving the vendor model toward performance-based service contracts that monetize uptime rather than one-time hardware sales.

Niche players exploit white spaces. UFP Technologies, fresh off UNIPEC and TPI deals, now supplies ISO 13485-certified, tight-tolerance thermoformed battery shields and injection-molded surgical drapes under one roof, cutting lead times for Class III implants. Equipment makers court such specialists with modular platen kits and quick-change tooling that flex across medical, packaging, and EV programs. Sustainability also shapes rivalry: lines able to form cellulose, PLA, and recycled PET without deep retrofits offer value when EPR fees penalize virgin plastic.

Thermo Compression Forming Industry Leaders

Amcor plc

UFP Technologies, Inc.

FLEXTECH

FRIMO Innovative Technologies

KIEFEL GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: UFP Technologies, Inc. expanded its medical device manufacturing capabilities by acquiring Universal Plastics & Engineering Company (UNIPEC) and Techno Plastics Industries (TPI). This development positively impacted the thermo-compression forming market by enhancing production capabilities and innovation.

- February 2025: At JEC World 2025, FRIMO Innovative Technologies highlighted its Automated Wet Compression Molding (WCM) technology to address the demand for efficient composite manufacturing. The system impregnated dry continuous fiber fabrics with reactive resin outside the press before consolidation, utilizing fast-curing resin systems that significantly outpaced traditional Resin Transfer Molding (RTM) in speed.

Global Thermo Compression Forming Market Report Scope

Thermo compression forming is a manufacturing process that involves shaping preheated thermoplastic sheets or composite materials between two matched molds using heat and mechanical pressure. This process produces durable, high-strength components, commonly utilized in the automotive and aerospace industries for lightweighting, as it combines shaping and curing in a single step.

The Thermo Compression Forming Market is segmented by material type, application, and geography. By material type, the market is segmented into thermoplastics, thermosets, composites, and other material types (e.g., bio-based PLA). By application, the market is segmented into packaging (food and beverage, pharmaceutical, consumer goods), automotive components, aerospace and defense, electronics and semiconductors, industrial equipment, and medical devices. The report also covers the market size and forecasts for thermo compression forming in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Thermoplastics |

| Thermosets |

| Composites |

| Other Material Types (Bio-based PLA, etc.) |

| Packaging | Food and Beverage |

| Pharmaceutical | |

| Consumer Goods | |

| Automotive Components | |

| Aerospace and Defense | |

| Electronics and Semiconductors | |

| Industrial Equipment | |

| Medical Devices |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Thermoplastics | |

| Thermosets | ||

| Composites | ||

| Other Material Types (Bio-based PLA, etc.) | ||

| By Application | Packaging | Food and Beverage |

| Pharmaceutical | ||

| Consumer Goods | ||

| Automotive Components | ||

| Aerospace and Defense | ||

| Electronics and Semiconductors | ||

| Industrial Equipment | ||

| Medical Devices | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the thermo compression forming market?

The thermo compression forming market size stands at USD 12.71 billion in 2026 and is forecast to reach USD 16.20 billion by 2031.

Which material type dominated in 2025?

Thermoplastics delivered 39.11% of 2025 revenue thanks to rapid cycle times and easy in-house recycling of trim scrap.

Why is Asia-Pacific growing fastest through 2031?

Taiwan, South Korea, and China are tripling advanced-packaging lines for AI accelerators, pushing Asia-Pacific thermo compression forming revenue at a 5.84% CAGR to 2031.

Why are medical device applications growing fastest through 2031?

ISO 11607 sterile-barrier mandates and demand for tight-tolerance battery shields drive medical devices applications at a 5.96% CAGR through 2031.

Page last updated on: