Composite Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

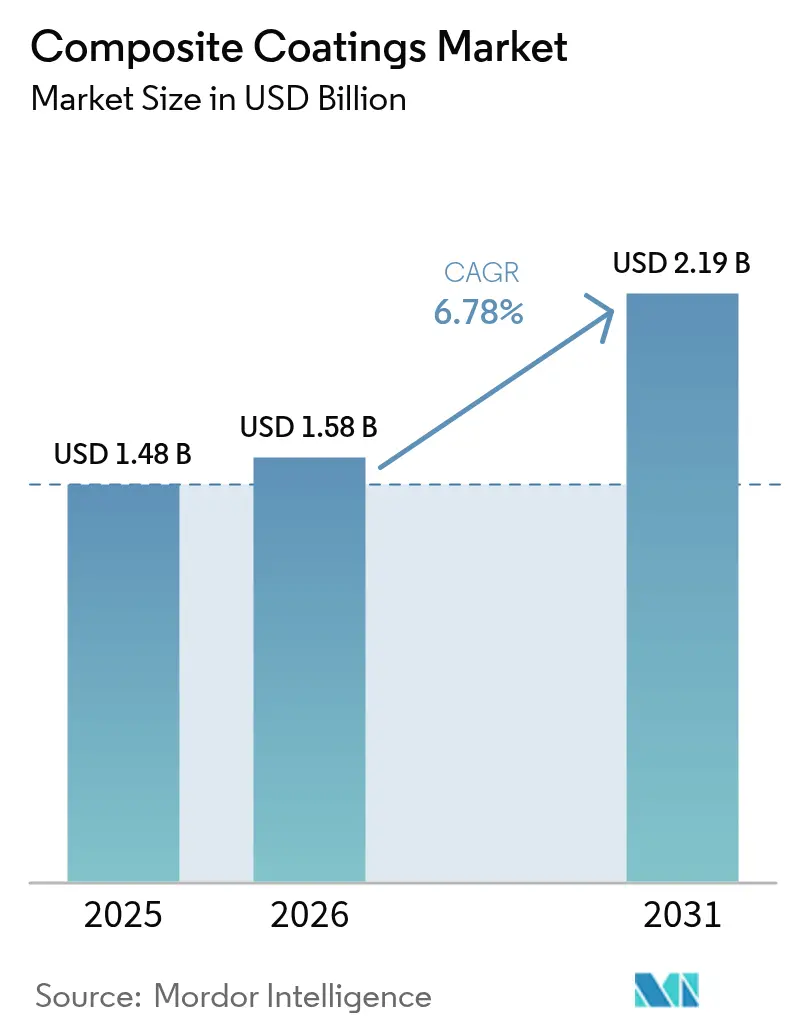

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

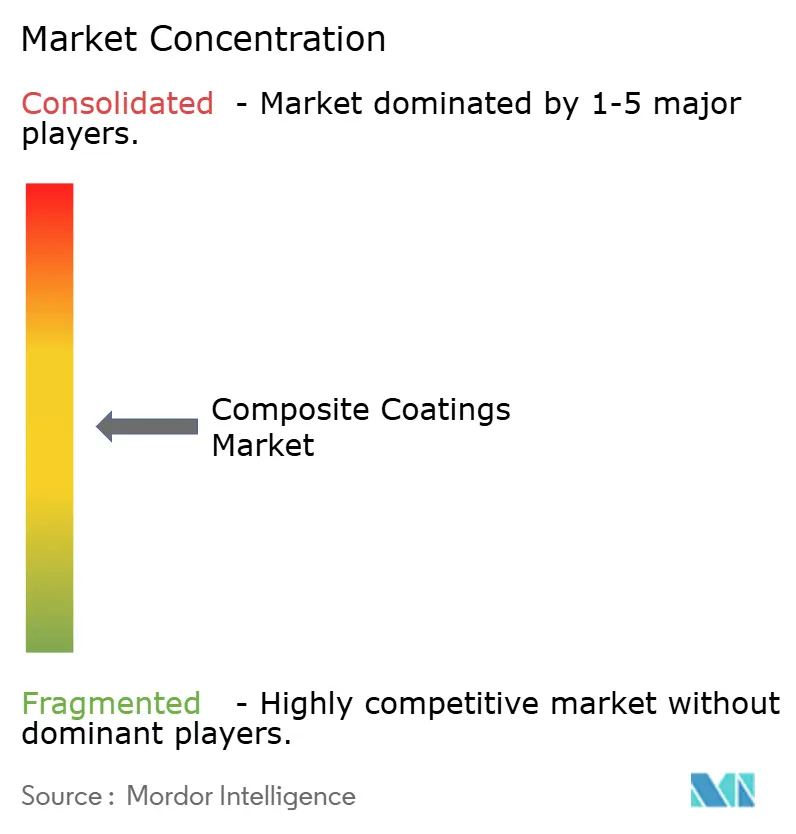

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composite Coatings Market Analysis by Mordor Intelligence

The Composite Coatings market size is expected to grow from USD 1.48 billion in 2025 to USD 1.58 billion in 2026 and is forecast to reach USD 2.19 billion by 2031 at 6.78% CAGR over 2026-2031. Continuous adoption of multilayer technologies that marry corrosion resistance, wear tolerance, and functional surface attributes positions the composite coatings market for sustained expansion. Accelerating offshore oil and gas developments, widening uptake of lightweight transportation parts, and stricter OEM lifetime specifications are collectively lifting demand. Innovation momentum in fluoropolymer, nano-structured, and bio-based chemistries is unlocking fresh, higher-margin use cases. Meanwhile, regional manufacturing shifts and large-scale renewable-energy projects are intensifying competition among established formulators and specialized newcomers.

Key Report Takeaways

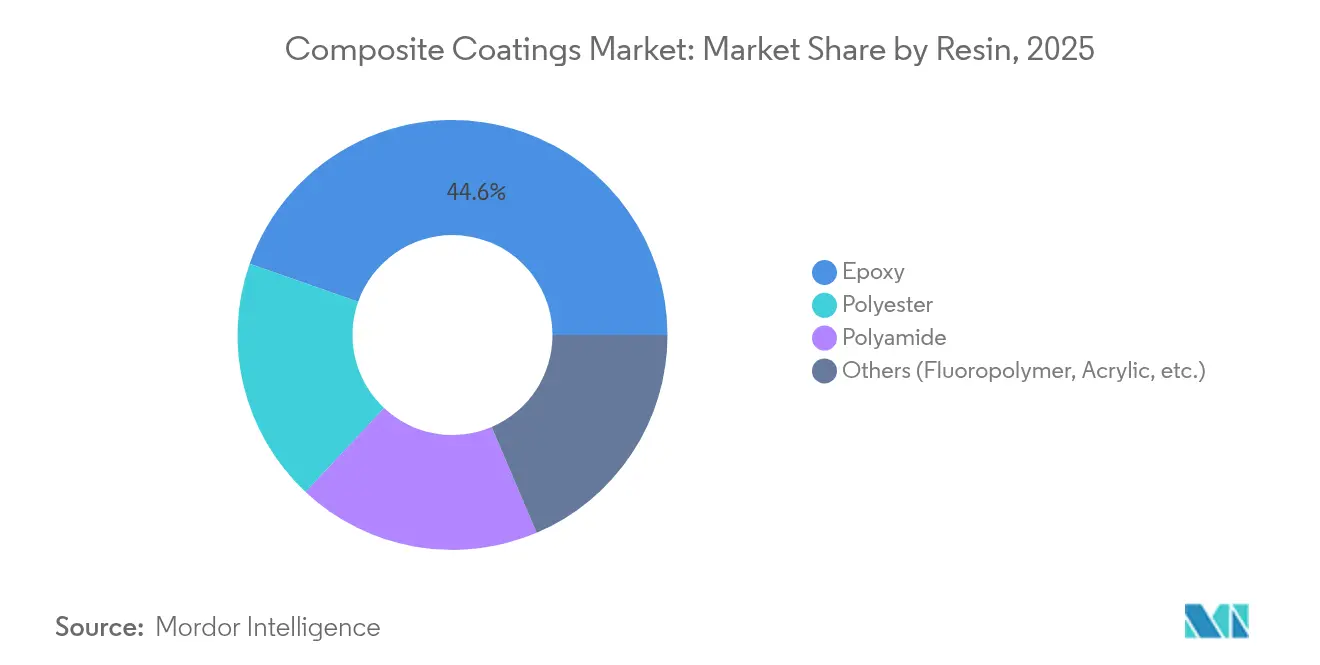

- By resin type, epoxy led with 44.62% composite coatings market share in 2025, whereas the “other resins” bucket that includes next-generation fluoropolymers and bio-based systems is projected to advance at an 8.22% CAGR to 2031.

- By application technique, electroless plating accounted for 29.78% revenue share of the composite coatings market size in 2025; laser-melt injection is forecast to expand at an 8.35% CAGR through 2031.

- By end-user industry, oil and gas held 29.10% of the composite coatings market in 2025, while the other industries group is expected to log the fastest 7.62% CAGR to 2031.

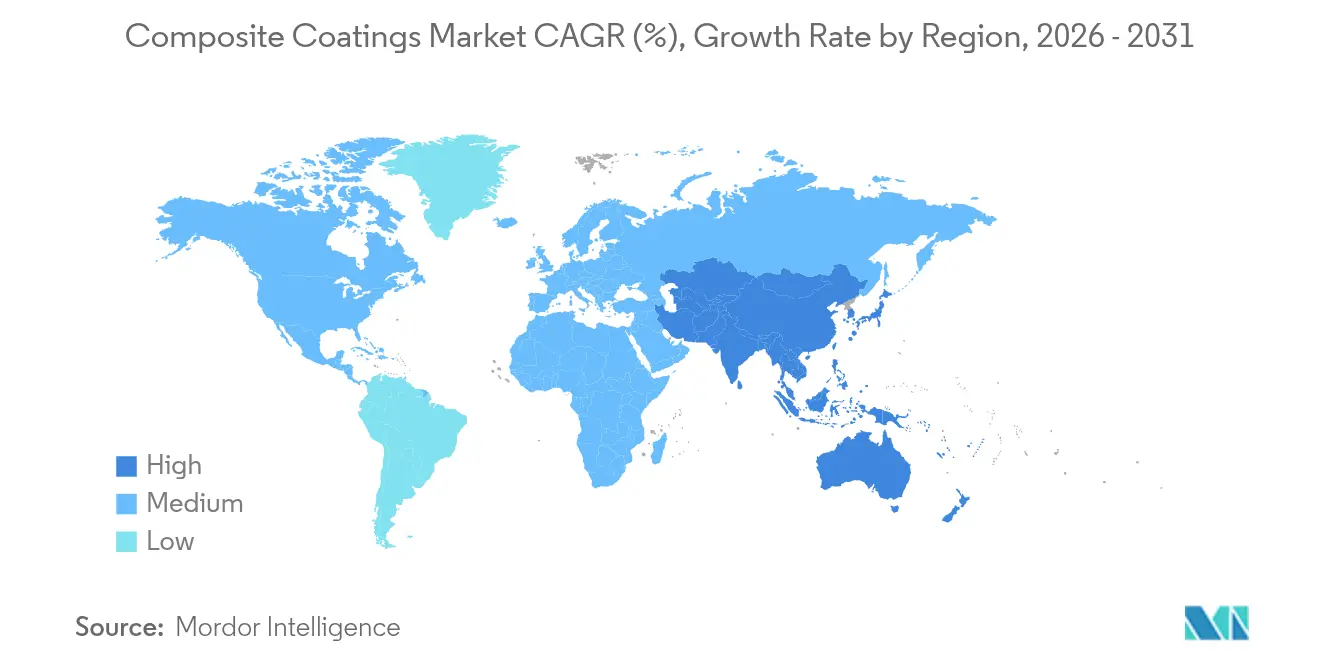

- By geography, Asia-Pacific secured 44.35% of the composite coatings market size in 2025 and is also pacing ahead with a 7.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Composite Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in oil and gas exploration activities | 1.8% | Global, with a concentration in the Middle East, North Sea, and Asia-Pacific offshore fields | Medium term (2-4 years) |

| Rising demand for lightweight, corrosion-resistant structures in transportation | 1.5% | North America and Europe for automotive, Global for aerospace | Long term (≥ 4 years) |

| Shift toward high-performance functional surfaces for renewable-energy hardware | 1.2% | Global, with early adoption in Europe and Asia-Pacific wind markets | Long term (≥ 4 years) |

| OEM mandates for extended coating life and reduced maintenance cycles | 0.9% | Global, with stringent requirements in developed markets | Medium term (2-4 years) |

| Nano-structured composite topcoats enabling anti-biofouling for offshore wind | 0.6% | Europe, Asia-Pacific coastal regions, and emerging in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Oil and Gas Exploration Activities

Deep-water and ultra-deep-water projects are elevating specifications for high-build, glass-flake-reinforced epoxy systems that tolerate temperature swings, hydrostatic pressure, and saline attack. Major offshore operators in Saudi Arabia, the North Sea, and the Gulf of Mexico are extending maintenance cycles toward 10 to 15 years by switching to composite barriers that inhibit cathodic disbondment and under-film corrosion. Uniform coating integrity on risers, wellheads, and topside equipment lowers the total cost of ownership despite higher upfront spend. Rising rig counts and asset-life extension programs, therefore, inject consistent volume growth into the composite coatings market.

Rising Demand for Lightweight, Corrosion-Resistant Structures in Transportation

Automakers pursuing range gains for electric vehicles are replacing steel battery enclosures with aluminum and composite housings that need thin yet resilient protection. Laser-textured primers combined with nanoparticle-filled topcoats elevate wear resistance and paint adhesion on carbon-fiber substrates, supporting weight reductions without compromising durability. In aerospace, self-healing epoxy chemistries incorporating micro-encapsulated agents flag early corrosion onset and autonomously repair micro-scratches, enabling predictive maintenance and shorter aircraft turnaround times.

Shift Toward High-Performance Functional Surfaces for Renewable-Energy Hardware

Offshore wind blades now carry nano-structured coatings that shed water, ice, and salt, thereby preserving aerodynamic profiles over 25-year service lives[1]European Coatings Journal, “Nano-Patterned Anti-Fouling Films for Offshore Wind,” european-coatings.com. Graphene-reinforced epoxies are likewise improving thermal conductivity of solar inverters and transmission components, limiting hotspots and boosting power throughput. The composite coatings market is therefore branching from purely protective functions toward surfaces that actively enhance asset performance.

OEM Mandates for Extended Coating Life and Reduced Maintenance Cycles

Industrial equipment suppliers are shifting warranty models from time-based to performance-based, rewarding coating systems that verify integrity via embedded sensors. Formulators are responding with ceramic-sphere-modified epoxies and low-VOC polyamides that lengthen inspection intervals to 10–15 years while complying with EPA’s aerosol-coating limits effective 2027. These dual compliance-plus-performance goals are channeling premium volumes into the composite coatings market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High processing and capital costs | -0.8% | Global, particularly impacting emerging markets and SMEs | Short term (≤ 2 years) |

| Limited repairability and recyclability versus conventional paints | -0.7% | Europe and North America due to stringent environmental regulations | Medium term (2-4 years) |

| Inconsistent global standards for multilayer composite coatings | -0.6% | Global, with particular challenges in cross-border trade and certification | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Processing and Capital Costs

Sophisticated spray booths, inert-gas curing zones, and laser-injection units raise capital outlays, delaying payback for smaller converters. In January, the prices of epoxy resins rose in Europe amid tight supply, whereas surplus inventory pushed Asian prices lower, illustrating volatility that squeezes margins. Until supply chains stabilize and equipment costs decline, some purchasers will default to lower-performing legacy coatings.

Limited Repairability and Recyclability Versus Conventional Paints

Mechanical stripping of multi-layer composites is labor-intensive and produces hazardous debris, challenging strict European waste directives. Although bio-based epoxies derived from lignin and cardanol lower life-cycle emissions, post-cure recyclability remains nascent. The EPA’s tightening VOC ceiling is hastening waterborne adoption, yet performance parity with solvent systems is not universal, restraining rapid displacement in heavy-duty settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Epoxy Dominance Faces Bio-Based Disruption

Epoxy maintained a 44.62% composite coatings market share in 2025, underscoring unmatched adhesion and chemical resistance for drilling platforms, aerospace structures, and transportation components. Fast-curing formulations with glass flake or ceramic microsphere fillers reinforce barrier paths, extending maintenance cycles. The composite coatings market size for epoxy systems is projected to grow steadily alongside offshore investments and fleet electrification requirements.

Parallel momentum is building around fluoropolymers and emerging bio-epoxies, whose 8.22% CAGR highlights an industry pivot toward sustainability mandates and extreme weatherability. Manufacturers like Sicomin are moving the market toward GreenPoxy lines incorporating waste glycerol and plant oils without diluting mechanical performance.

By Technique: Electroless Plating Leads While Laser Technologies Surge

Electroless nickel-phosphorus and nickel-boron baths covered 29.78% of the composite coatings market in 2025. The approach blankets intricate geometries uniformly, avoids porosity inherent in air spraying, and coats internal passages of valves and pump housings critical to oil and gas uptime. High-phosphorus variants combine toughness with 1,000-hour salt-spray resistance, safeguarding substrates where field repair is cost-prohibitive. The composite coatings market size for electroless plating is expected to increase as process chemistry shifts toward low-PFOS catalysts that satisfy tightening environmental rules.

Laser-melt injection is advancing at an 8.35% CAGR, powered by automotive and aerospace quests for localized hard-facing and rapid prototyping accuracy. The technique fuses alloy or ceramic powders into metal surfaces, realizing dense, metallurgically bonded layers with minimal heat-affected distortion.

By End-User Industry: Oil and Gas Leadership Amid Diversification

Oil and gas operators consumed 29.10% of the composite coatings market demand in 2025, anchored by ongoing asset-life extension in North Sea rigs and Middle East expansion programs. High-thickness epoxy glass-flake linings on separators, subsea pipelines, and splash-zone decks slash corrosion repair costs. The segment will remain volume-heavy, yet growth tempo moderates as renewable-energy buildout accelerates.

Aerospace, defense, and new-energy hardware collectively falling under the other end-user industries segment represent the quickest-moving opportunity set, with a 7.62% CAGR anticipated to 2031 as smart, lightweight, and self-diagnostic coatings achieve qualification.

Geography Analysis

Asia-Pacific retained a dominant 44.35% share of the composite coatings market in 2025 and is projected to compound at 7.31% through 2031. Massive Chinese port expansions, Indian highway corridors, and Southeast Asian petrochemical complexes collectively fuel the consumption of high-build protective formulations. Offshore wind farms off Guangdong and Tamil Nadu further call for anti-biofouling and erosion-resistant systems.

North America commands substantial adoption driven by rigorous OSHA and EPA statutes that reward low-VOC, high-solids chemistries. The Gulf of Mexico’s deep-water rigs, Canada’s oil-sands upgraders, and the United States Navy’s fleet refurbishment pipeline together underpin steady requisition of ceramic-filled epoxies and zinc-rich primers.

Europe’s Green Deal blueprint is steering demand toward bio-derived and recyclable formulations. German automotive producers and UK aerospace plants are early adopters of self-healing clear coats that broadcast integrity status via fluorescence or embedded RFID. Offshore wind foundations across the North Sea rely on nano-structured foul-release films aligned with IMO environmental conventions.

Regulatory Landscape

Composite coatings are increasingly shaped by air-emissions and chemical-substance controls that affect resin selection, additives, and application processes. In the United States, the EPA finalized National VOC Emission Standards for Aerosol Coatings in January 2025 under the Clean Air Act, updating product-weighted reactivity limits and test methods that influence formulation choices for certain composite-coating delivery formats.

In Europe, REACH continues to be a central compliance framework for specialty chemistries used in high-performance multilayer systems. Commission Regulation (EU) 2026/1168 updated REACH Annex XVII in May 2026 to introduce new restrictions on synthetic polymer microparticles, reinforcing the need for portfolio reviews of functional fillers and performance additives that can appear in composite coating stacks and related surface-treatment systems.

Value Chain Analysis

The value chain runs from upstream petrochemical and specialty-chemical inputs (epoxy and curing agents, fluoropolymers, polyamides, pigments, corrosion inhibitors, and functional fillers such as ceramics, glass flake, and nano-additives) through formulation, compounding, and conversion into application-ready systems (spray-applied linings, powder coatings, electroless plating baths, and laser-melt injection consumables). Downstream, coatings are qualified and applied by OEMs and specialist applicators to oil and gas equipment, marine assets, infrastructure, and transportation components, with performance verification anchored in corrosion testing, salt-spray exposure, and increasingly tighter chemical-compliance documentation.

Supply availability and lead times are being influenced by regionalization and capacity moves as companies reduce exposure to shipping disruption and regulatory-driven material substitutions. Recent examples cited in industry channels include localization steps by major coatings suppliers and adjacent players, such as Sherwin-Williams expanding a facility in Vilnius, Lithuania for regional production and Jotun doubling capacity at its Sharjah, UAE plant, alongside efforts to shorten resin supply lead times through local production arrangements in the Middle East. On the innovation and specialty-additive side, Graphene Manufacturing Group (GMG) reported June 2026 sales for its graphene-enhanced THERMAL-XR coating and commissioned a dedicated blending plant, illustrating how performance-additive supply is being supported with dedicated processing to meet industrial demand.

Competitive Landscape

The composite coatings market is moderately fragmented. AkzoNobel, PPG Industries, and Sherwin-Williams leverage global plant footprints, tier-one raw-material agreements, and multi-industry technical service teams to secure repeat contracts. Technological alliances dominate the strategic canvas. Recent tie-ups pair coating formulators with sensor integrators, enabling data-rich films that relay temperature, strain, or pH through thin embedded circuitry. Players that align digital workflow, sustainable raw materials, and global service reach will secure share gains as customers consolidate vendor lists to lower interface complexity and meet audit requirements.

Composite Coatings Industry Leaders

The Sherwin-Williams Company

Akzo Nobel N.V.

PPG Industries, Inc.

RPM International Inc.

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated where asset owners are paying for longer maintenance cycles, thinner high-performance layers, and compliance-ready formulations across offshore energy, marine, and heavy industry. One whitespace area sits at the intersection of regulatory pressure and performance, where formulators redesign composite systems to reduce VOC and remove or limit ingredients facing broader group-based restrictions (for example, microplastics controls under EU REACH Annex XVII updates in May 2026). This is shifting demand toward alternative filler architectures, reformulated dispersions, and application methods that preserve barrier performance while simplifying compliance documentation across global supply chains.

A second opportunity is the commercialization bridge from laboratory-proven nanocomposite and hybrid functional layers into scalable industrial systems for thermal management and high-temperature durability. In 2026, multiple peer-reviewed studies highlighted advances that improve dispersion stability and thermal or oxidation resistance, including a covalent silane-bridging approach for graphene-oxide integration in epoxy matrices (RSC Advances, May 2026) and high-temperature oxidation-resistant composite coatings that reduced mass loss after extended exposure at 1400 C (MDPI Coatings, January 2026). These proof points support product-development pipelines for turbine, aero-engine, and other industrial high-heat hardware where coating functionality extends beyond corrosion protection into thermal shielding and multi-mechanism durability.

Recent Industry Developments

- July 2026: The Sherwin-Williams Company inaugurated the Morikis Global Technology Center in Brecksville, Ohio, a 600,000-square-foot R&D facility focused on advancing coatings innovation. The added research and process-engineering capacity strengthens Sherwin-Williams ability to accelerate formulation development and scale-up across industrial and transportation-adjacent coating platforms relevant to composite-protection requirements.

- June 2026: The Sherwin-Williams Company introduced OneCure, a dust-on-dust powder coating system that enables primer and topcoat to cure together in a single bake. By compressing cure steps into one thermal cycle, the launch targets throughput and energy-efficiency improvements for coated components where multilayer performance and cycle time are key production constraints.

- January 2026: PPG and partners including BMW Group, BCOMP Ltd, SGL Technologies, and Cobra Advanced Composites were recognized with a JEC Innovation Award for a natural fiber composite substrate coated using a PPG multilayer coating system intended to replace traditional carbon fiber in automotive composite applications. The project highlights how coating-layer engineering is being used to make alternative lightweight substrates viable for demanding end-use environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue earned from coatings applied on composite substrates to protect, repair, or enhance performance in industrial and transportation uses, counted at the point of sale of the coating material and application service where relevant.

Scope exclusions: Decorative paints for non-composite surfaces and unrelated metal-only coating systems are excluded from this sizing.

Segmentation Overview

- By Resin

- Epoxy

- Polyester

- Polyamide

- Others (Fluoropolymer, Acrylic, etc.)

- By Technique

- Electroless Plating

- Laser-Melt Injection

- Brazing

- Other Techniques (Sol-Gel and Dip-Coating, etc.)

- By End-User Industry

- Oil and Gas

- Marine

- Automotive and Transportation

- Infrastructure

- Other End-user Industries (Aerospace and Defense, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a clean fact base around where composite coatings are consumed and what drives usage changes across regions. Public sources such as US Census construction and manufacturing data, US International Trade Commission trade statistics, the European Chemicals Agency regulatory updates, and International Energy Agency mobility indicators were reviewed to understand demand signals that indirectly pull coating volumes.

We also used sources such as peer reviewed journals on surface engineering and corrosion protection, patent databases to track technology intensity, and association websites covering composites and protective coatings to ground typical applications and adoption barriers. Company filings, investor presentations, and reputable press were then used to sanity check capacity additions, product positioning, and price movement themes. In addition, a paid subscription for company financials and a shipment level import export database were referenced selectively to validate scale and trade flows. These sources are illustrative only, and many other public materials were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with coating formulators, composite part manufacturers, applicators, and procurement teams in end user industries, so that assumptions from desk research could be confirmed and gaps could be closed. For a global market, inputs were balanced across APAC, EMEA, and the Americas, and discussions were also used to align typical coating thickness, recoat cycles, and pricing behavior by application.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 45% |

| Mid tier: 59% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 15% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down demand pool build that links composite part output and usage intensity to coating consumption, and then converts volumes into value using region and application level pricing ranges. When the demand is reconstructed this way, the biggest practical inputs are composite production activity, aerospace and automotive build rates, maintenance and repair cycles in marine and wind, typical coating thickness and coverage per square meter, and observed raw material led price movements.

Results were then corroborated with selective bottom-up approximations, including supplier and distributor channel checks, sampled project level consumption norms, and ASP times volume cross checks for a few high visibility applications. Where direct visibility is limited (for example, small job shops and in-house coating lines), we apply penetration rates and utilization assumptions that were reviewed in primary discussions, and then adjust the totals only when multiple signals move in the same direction.

For forecasting, scenario analysis was used so that volume growth and pricing can be flexed separately, which matters in coatings when resin and additive costs move faster than end demand. The forward view was anchored to expert consensus on airframe deliveries, renewable installations, industrial production, and repaint intervals, and then smoothed so short-term spikes do not overstate the long-run trend.

Data Validation & Update Cycle

Validation is done through repeated triangulation between modeled outputs and independent indicators, and then through variance checks at regional and application levels. If an implied coating intensity looks too high versus typical coverage rates, or if pricing drifts away from what interviews suggest is achievable, the model is revisited and assumptions are tightened.

Before sign-off, the work goes through multi-step analyst review so that arithmetic, units, and conversion logic are consistent across years. Reports are refreshed annually, and interim updates are triggered when major supply disruptions, regulation shifts, or sharp raw material changes are observed. Right before delivery, a final analyst pass is completed so the numbers reflect the latest public data and primary feedback.

Mordor Intelligence's Composite Coatings Market Sizing Compared With Other Published Estimates

Published composite coatings market values can look different even when they describe the same coating consumption theme, because the boundaries and conversion logic are not always aligned. In practice, the gaps usually come from how each study treats application services versus materials, what it counts as a composite substrate use case, and which year and currency timing is used.

Import and export signals for key coating chemistries, together with build rate checks in aerospace and industrial production markers, are used to keep Mordor Intelligence's estimate tied to a realistic demand pool instead of a broad protective coatings umbrella. Differences also show up when some estimates start from a single prior-year number and extend it with a fixed CAGR, rather than rechecking coverage rates, repaint cycles, and price progression by region as conditions change.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.48 B (2025) | |

| Industry Publisher A | USD 0.96 B (2024) | Uses an earlier base year and reports the value in US$ million with a narrower producer-defined scope, which can undercount downstream application activity and later-year pricing uplift. |

| Global Consultancy B | USD 1.39 B (2025) | Relies more heavily on stated headline growth to 2031 and can differ on what is counted as composite coating techniques and end uses, which shifts the included demand pool and the implied price ranges. |

The spread in the table mainly comes from base-year choice, what is treated as in-scope composite coating demand, and how prices are carried forward from the starting point. By keeping inputs traceable to observable activity indicators and then validating the implied coverage and pricing through industry feedback, we end up with a balanced number that can be repeated and updated in a practical way.

Key Questions Answered in the Report

What is the current value of the composite coatings market?

The composite coatings market size stands at USD 1.58 billion in 2026 and is projected to reach USD 2.19 billion by 2031.

Which resin type dominates composite coatings demand?

Epoxy resins lead with 44.62% composite coatings market share due to superior adhesion and chemical resistance.

Which application technique is growing fastest?

Laser-melt injection is set to post an 8.35% CAGR between 2026 and 2031, driven by precision requirements in aerospace and automotive parts.

Why is Asia-Pacific the largest regional market?

Massive infrastructure spending, offshore energy projects, and expansive manufacturing bases in China, India, and Southeast Asia give Asia-Pacific a 44.35% share in 2025 and the fastest 7.31% CAGR outlook.

How are sustainability regulations influencing product development?

Tightening VOC rules and circular-economy directives are accelerating bio-based resin adoption and driving innovation in recyclable, low-emission composite coatings.

Page last updated on: