Polyaspartic Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

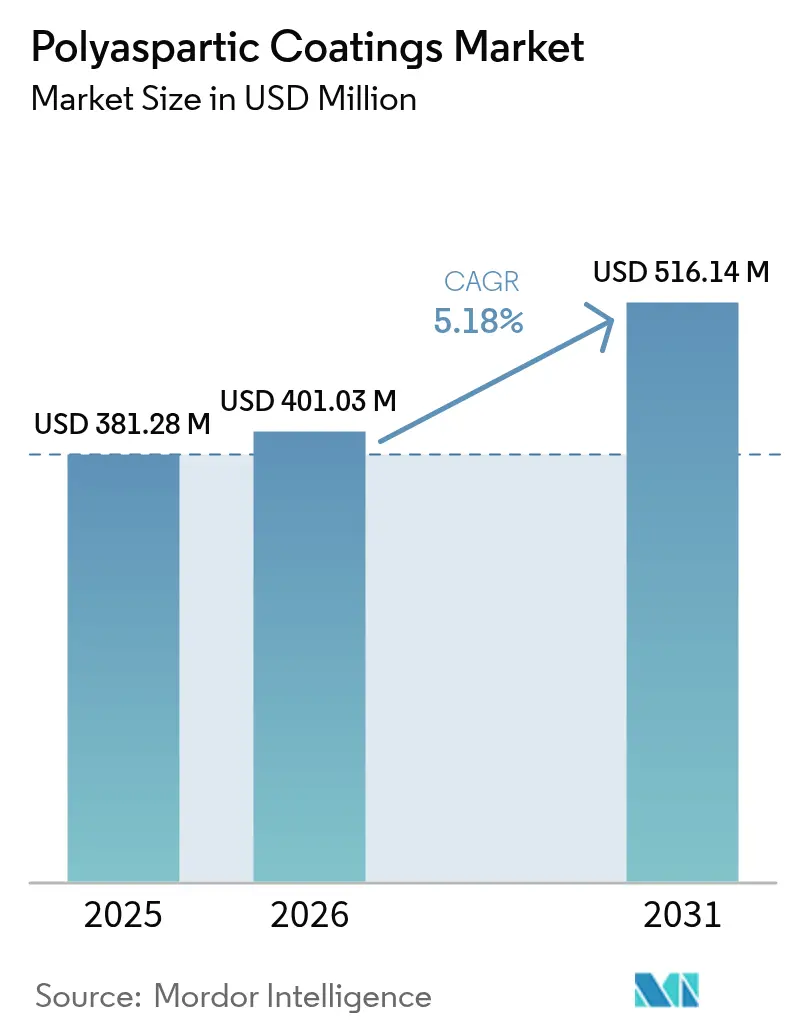

| Market Size (2026) | USD 401.03 Million |

| Market Size (2031) | USD 516.14 Million |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyaspartic Coatings Market Analysis by Mordor Intelligence

The Polyaspartic Coatings Market size was valued at USD 381.28 million in 2025 and estimated to grow from USD 401.03 million in 2026 to reach USD 516.14 million by 2031, at a CAGR of 5.18% during the forecast period (2026-2031). Demand is expanding as builders, manufacturers, and asset owners search for fast-curing, low-VOC systems that reduce downtime, meet tightening air-quality rules, and prolong service life. Flooring contractors rely on the technology’s one-day return-to-service to mitigate skilled-labor shortages, while infrastructure owners specify it to limit traffic closures on decks and ramps. Water-borne chemistries are narrowing the performance gap with solvent-borne systems and are scaling faster because they simplify regulatory compliance. Asia leads global consumption with a 45% share, propelled by high‐volume construction in China and India and by regional supply chains that shorten lead times for fast-moving projects.

Key Report Takeaways

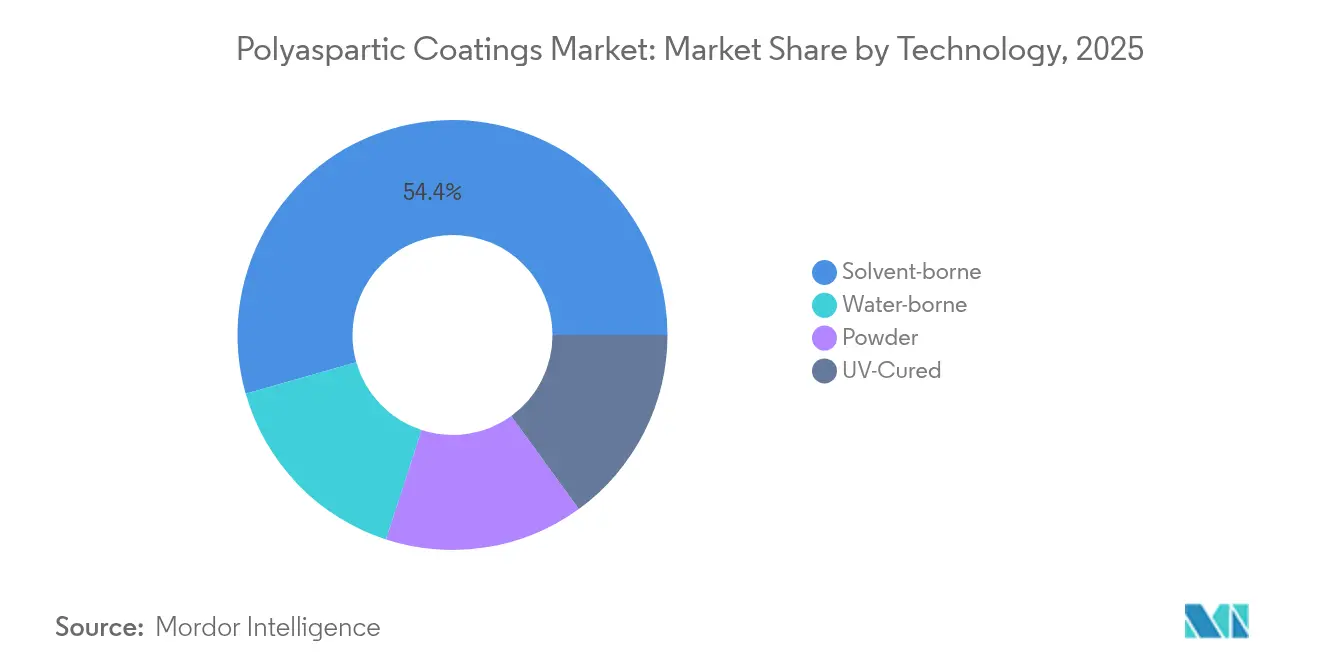

- By technology, solvent-borne grades held 54.40% of the polyaspartic coatings market share in 2025, while water-borne grades are projected to post the fastest 5.78% CAGR through 2031.

- By type, pure polyaspartic systems commanded 69.20% of the polyaspartic coatings market size in 2025; hybrid systems are expected to expand at a 6.14% CAGR to 2031.

- By application, flooring captured 59.20% revenue share in 2025 and is forecast to advance at a 6.42% CAGR during 2026-2031.

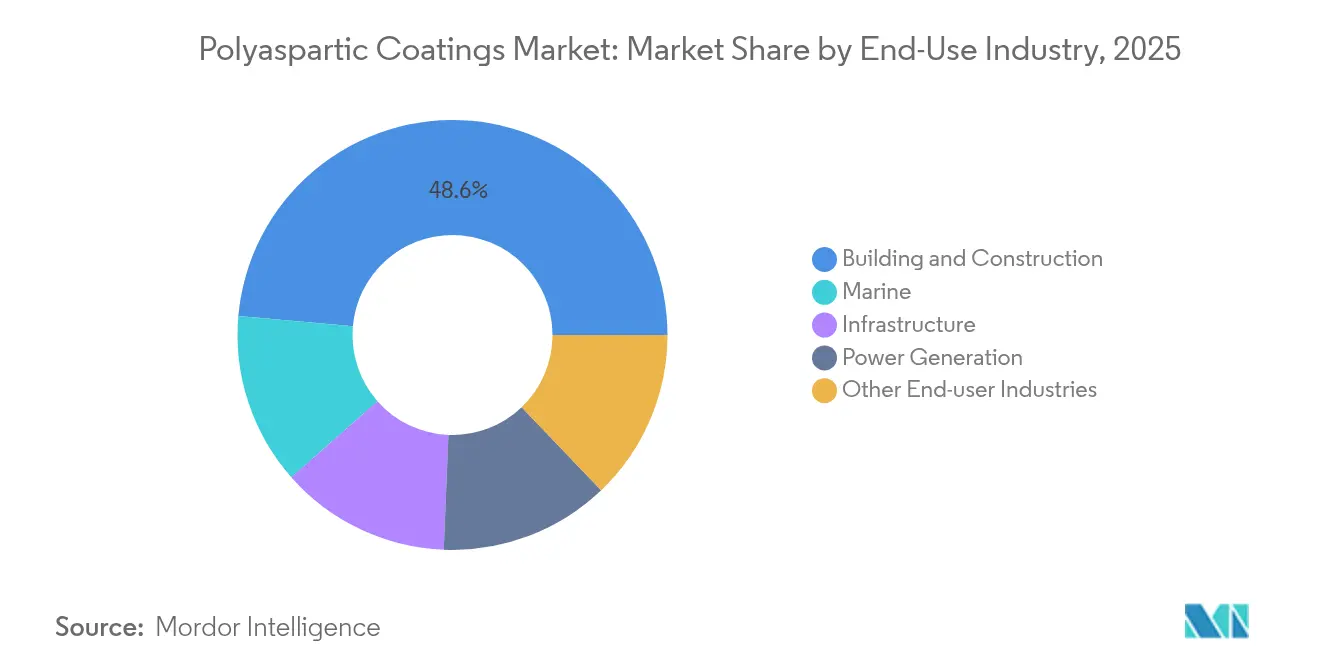

- By end-use industry, building & construction led with 48.60% of the polyaspartic coatings market size in 2025, and are expected to expand at a 5.69% CAGR to 2031.

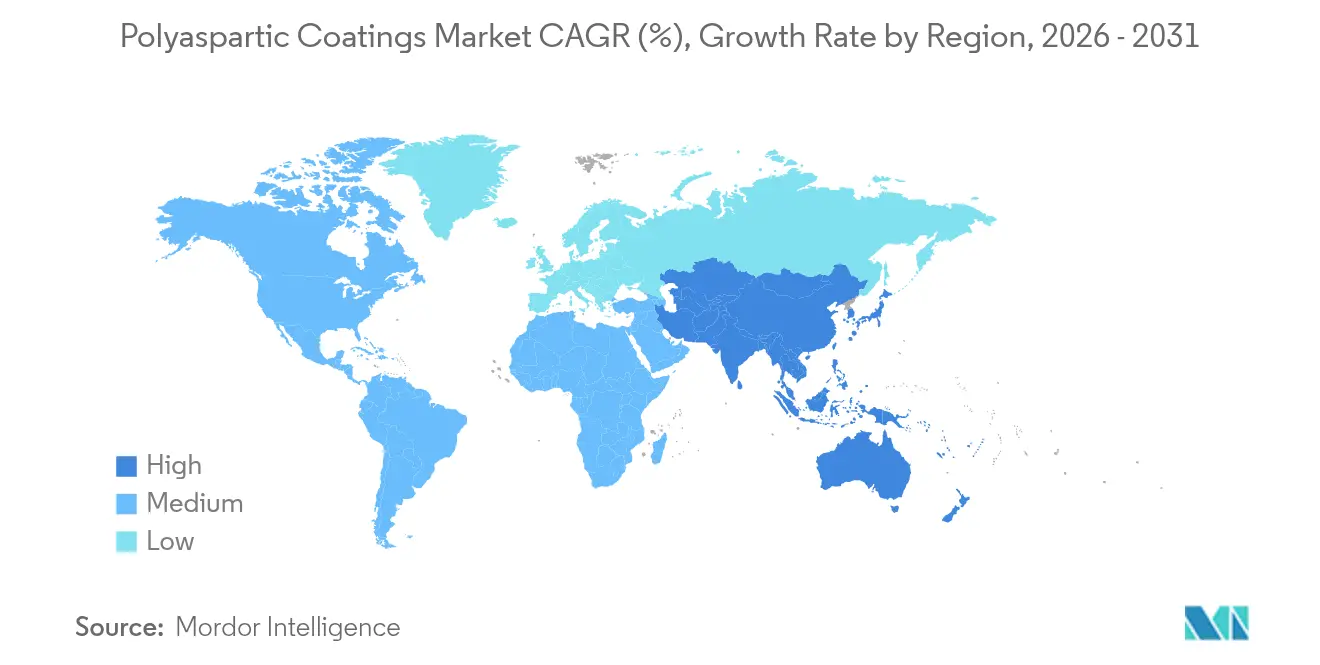

- By geography, Asia accounted for 44.70% of global revenue in 2025, and the region is projected to grow at a leading 6.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyaspartic Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green-Building Certification Mandates in Europe Accelerating Adoption of Low-VOC Polyaspartic Systems | +1.20% | Europe, spillover to North America & developed APAC | Medium term (2-4 years) |

| Rapidly Increasing Demand from the Building and Construction Industry | +1.80% | Global, especially North America & Asia | Short term (≤2 years) |

| Rising Infrastructure Development in Emerging Economies | +0.90% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Superior Performance over Traditional Coatings | +0.70% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Green-Building Certification Mandates in Europe

Europe’s new decarbonization rules cap VOC content in construction products and reward low-emission coatings within BREEAM, DGNB, and EU Ecolabel schemes. Polyaspartic suppliers that document ISO-compliant emissions secure specification advantages because developers use certifications as marketing assets to command rent premiums. Laboratories such as Fraunhofer WKI provide third-party testing, shortening time to proof. The resulting pull-through boosts orders for water-borne and bio-content grades, prompting formulators to accelerate scale-up at European plants. Multinationals re-label existing solvent-based lines with greener chemistries to defend share, while regional specialists partner with resin producers to launch ready-to-spray kits.

Rapidly Increasing Demand from Building and Construction Industry

Builders embrace polyaspartic flooring because it cuts project schedules by one to two days over epoxy, enabling contractors to complete more square footage annually with fixed crews. Owners gain 15-plus-year service life in heavy-traffic retail and logistics centers, reducing lifetime maintenance costs even when initial material prices run 30-50% higher. Labor scarcity intensifies adoption: single-day systems free scarce applicators for the next job sooner. Architectural firms integrate polyaspartic topcoats into decorative concrete designs to meet both aesthetic and durability targets, expanding use cases from warehouses to shopping malls and stadium concourses.

Rising Infrastructure Development in Emerging Economies

Indonesia's paint production has experienced significant growth, driven by public-works investments emphasizing quick-return protective coatings. In India, highways and metro stations adopt rapid-cure systems that reopen lanes overnight to avoid daytime congestion. Bridge-deck waterproofing benefits from the chemistry’s UV stability and elongation, which mitigate cracking in hot-humid climates. The influx of foreign direct investment into regional manufacturing zones further lifts demand for factory flooring that withstands chemicals and forklift abrasion.

Superior Performance over Traditional Coatings

Polyaspartic technology pairs ultraviolet resistance, low odor, and high solids in a single formulation that cures in under two hours at 20 °C, outperforming epoxy and traditional polyurethane in hot-tire pickup, moisture tolerance, and gloss retention. Systems such as Covestro’s Pasquick platform slash application steps by allowing thicker single-coat builds, which eliminates primer stages and cuts VOC emissions by 30%[1]Covestro, “Pasquick® Technology,” solutions.covestro.com . Asset owners in food processing and pharmaceutical plants value the resulting hygiene and chemical resistance, extending the technology’s reach beyond parking decks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Compared to Alternatives | -1.30% | Global, acute in developing markets | Medium term (2-4 years) |

| Feedstock Price Volatility in Asia-Pacific | -0.80% | Asia-Pacific with global supply ripple | Short term (≤2 years) |

| Limited Awareness in Developing Markets | -0.50% | Emerging economies in Asia, Africa, Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Cost Compared to Alternatives

Pure polyaspartic coatings cost 30-50% more than comparable epoxy, constraining penetration in price-sensitive housing segments. The premium reflects higher amine ester feedstock prices and tighter processing tolerances. Contractors without lifecycle-cost models default to cheaper systems despite shorter service life. Suppliers answer with hybrid lines that blend acrylic or polyurethane resins to shave 15-20% off list prices while retaining fast cure and UV resistance, planting a migration path toward pure grades as experience deepens.

Feedstock Price Volatility in Asia-Pacific

Propylene prices in parts of Asia climbed in early 2025, pushing isocyanate and polyol costs higher and squeezing margins for coatings producers lacking scale hedges. Nippon Paint’s decision to lift finished-goods prices to 9% from January 2025 highlights the downstream impact. Smaller regional formulators risk order deferrals when they pass on surcharges, while integrated multinationals leverage global procurement to blunt volatility. Some producers lengthen contract tenors with propylene suppliers or increase inventory buffers, but working-capital demands rise accordingly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Formulations Move Into the Mainstream

Solvent-borne grades held a 54.40% revenue share in 2025; however, water-borne products are forecast to register a 5.78% CAGR, the highest among technology categories, as regulators impose lower VOC ceilings. Water-based dispersants such as Lubrizol’s Solsperse W60 improve pigment stability, delivering color consistency once achievable only with solvent carriers. Producers also introduce bio-content amines to cut carbon footprints. In Asia, municipal green-building codes adopt European VOC limits, accelerating specification even in economies without federal mandates. Large contractors appreciate water clean-up and lower odor, which reduces containment costs on occupied sites, turning the polyaspartic coatings market into a preferred solution in hospitals and schools.

Continuous resin research has narrowed mechanical-property gaps between water-borne and solvent-borne systems. Covestro’s INSQIN polyurethane reduces process-water use by 95% and CO₂ emissions by 45% compared with legacy solvent routes. These gains enable coating suppliers to promote environmental key-performance indicators alongside cure speed and hardness. As a result, the polyaspartic coatings market sees tiered product ladders: entry water-borne hybrids for cost-sensitive interiors, mid-tier universal systems for commercial flooring, and premium exterior water-borne pure grades for façade cladding.

By Type: Hybrid Systems Extend Value Down-Market

Pure formulations generated 69.20% of 2025 sales, yet hybrid systems are projected to grow at 6.14% CAGR as applicators seek balanced performance and price. Products such as Advanced Polymer Coatings’ TriFLEX DTM merge polyurethane flexibility with polyaspartic UV durability to create a direct-to-metal coating that withstands salt spray and color fade. Hybrids often lengthen open time to ease large-area application in warm climates, resolving a common complaint about rapid pure-grade gel.

A second hybrid wave blends polyaspartic with polysiloxane to improve heat resistance in flue-gas stacks and offshore structures. Material scientists leverage oligomer design to tune cure profiles, enabling use of standard airless pumps instead of plural-component rigs, thus broadening contractor acceptance. Because hybrids cut raw-material cost per gallon by double-digit percentages, the polyaspartic coatings industry positions them as step-up options from epoxy, easing buyers into the premium category without sticker shock.

By Application: Flooring Dominates Yet Diversification Accelerates

Flooring retained 59.20% of global demand in 2025 and is set to log a 6.42% CAGR on the strength of retail remodels, fulfillment centers, and healthcare expansions. ArmorPoxy’s 85%-solids polyaspartic floor allows light traffic within six hours and vehicular traffic within forty-eight hours, keeping hospitals and grocery stores open overnight during upgrades. In the polyaspartic coatings market size for flooring, hybrid systems carve share where odor sensitivity is paramount, such as pharmaceutical cleanrooms.

Beyond floors, moisture-barrier membranes for podium decks and green roofs capture attention because polyaspartic sheets resist hydrolysis better than epoxy. Ghostshield’s Polyaspartic 930 topcoat provides 93% solids with high gloss and abrasion resistance, making it a candidate for aircraft hangars and petrochemical terminals. Anti-corrosive topcoats for heavy-equipment cabs and rail cars add another growth node, aided by new pigments that maintain color after 2,000 hours of Q-UV exposure.

By End-Use Industry: Building & Construction Shapes Future Specifications

Building & construction accounted for 48.60% of 2025 consumption and will remain the anchor vertical at a 5.69% CAGR. Contractors favor fast-track decks in multifamily towers where rental revenue starts sooner. Architects pursuing WELL and LEED credits specify low-odor, low-VOC polyaspartic sealers to safeguard occupant health, reinforcing demand in corporate interiors.

Marine maintenance crews adopt polyaspartic hull coatings to replace solvent-rich polyurethanes that yellow under tropical sun. Power-generation plants use the chemistry on turbine hall floors because it withstands hydraulic-fluid spills and cleans easily, boosting safety. Sika’s 2024 acquisition of Kwik Bond Polymers illustrates how infrastructure refurbishment specialists integrate polyaspartic solutions to penetrate bridge and runway rehabilitation niches. Automotive line operators test anti-chip topcoats to cut bake-oven dwell times. As more case studies validate lifecycle savings, the polyaspartic coatings market secures recurring orders across multiple asset classes.

Geography Analysis

Asia-Pacific generated 44.70% of global revenue in 2025 and is tracking a 6.48% CAGR through 2031 as megacities invest in transit, data centers, and smart manufacturing clusters. China’s shift to renovation over greenfield builds sustains demand for rapid-cure deck refurbishment, while India’s Smart Cities Mission channels public funds into pedestrian bridges and metro stations that specify low-maintenance coatings. Indonesia and Vietnam emerge as second-tier hotspots, aided by local suppliers scaling blended hybrids that lower import dependence.

North America's value is driven by warehouse automation, expansions in cold-storage capacity, and the USD 1.2 trillion federal infrastructure program enacted in 2022. Bridge owners exploit the chemistry’s overnight return-to-service to minimize lane closures; state departments of transportation incorporate it into asset-management guidelines. Commercial real-estate owners schedule overnight floor recoats to sidestep business interruptions, which sustains aftermarket demand even during new-build slowdowns. High adoption of contractor certification programs accelerates the polyaspartic coatings market across Canada and the United States.

Europe’s stringent air-quality statutes and mature green-building certification ecosystem create a stable platform for water-borne adoption. Germany anchors regional volume through industrial floor upgrades, while Scandinavia deploys polyaspartic membranes on timber structures to lengthen maintenance cycles in harsh freeze–thaw climates. Southern Europe experiments with cool-roof formulations that combine polyaspartic binders with infrared-reflective pigments to curb building energy use. Eastern European countries, encouraged by EU cohesion funds, specify rapid-cure bridge coatings to compress tight construction seasons, bolstering market penetration.

Regulatory Landscape

Polyaspartic coatings are shaped primarily by chemical-substance and air-emissions compliance, pushing formulators toward low-VOC, high-solids, and water-borne systems for building and infrastructure uses. In the European Union, REACH (EC 1907/2006) governs registration and restrictions, with Annex XIV (authorisation) and Annex XVII (restrictions) serving as key checkpoints for raw materials used in industrial coatings and surface treatment systems.

In May 2026, the EU added N-methyl-2-pyrrolidone (NMP), N,N-dimethylformamide (DMF), and specified benzotriazole derivatives to REACH Annex XVII restrictions for industrial coatings and related surface treatment uses, increasing the need for supplier declarations and SVHC screening documentation in procurement. In the United States, the EPA regulates chemical substances under TSCA, where many coating polymers can qualify for the polymer exemption under 40 C.F.R. 723.250 if criteria are met, while specific Significant New Use Rules (SNURs) also apply to certain chemistries (including PFAS-related rules) relevant to surface-coating supply chains.

Value Chain Analysis

The value chain starts with petrochemical feedstocks and specialty intermediates used to manufacture polyaspartic ester resins (amine-functional) and compatible isocyanates (commonly HDI/HMDI) that form the two-component coating backbone. Critical intermediates and chain extenders, such as methylenebis(2-methylcyclohexylamine) (MACM), can influence cost, lead times, and formulation latitude, making upstream purity and supply continuity important for consistent cure profile and appearance.

Resin producers and major coating formulators convert these inputs into pure and hybrid polyaspartic systems, then move product through chemical distributors and regional applicator channels (industrial flooring contractors, waterproofing installers, and protective-coating service providers). Standards and qualification frameworks influence downstream adoption and specification, including AMPP-based testing and inspector practices for protective coatings, and China-focused product standards such as T/CWA 204-2021 for polyaspartic acid ester waterproof coatings. Bottlenecks frequently sit at formulation control (viscosity and reactivity balance for fast cure) and at contractor capability, where application training and access to suitable spray/mix equipment can determine whether projects can reliably achieve one-day return-to-service performance.

Competitive Landscape

Global supply is highly consolidated. BASF, PPG, Sherwin-Williams, and Akzo Nobel leverage integrated resin production and expansive distributor networks to defend volume leadership. Covestro focuses on raw-material innovation, raising bio-based acrylate capacity in Foshan in late 2024 to support its Desmophen CQ NH line with 25% renewable content.

Mid-size specialists differentiate through application-specific chemistry. LATICRETE markets SPARTACOTE FLEX XPL Clinical Plus, a silver-ion-enhanced floor system that inhibits bacterial growth in hospitals. ArmorPoxy tailors ultra-high-solids kits for DIY garages, using e-commerce channels to bypass retail mark-ups. ALTANA invests in additive R&D to supply rheology modifiers that enhance flow at lower VOCs.

Strategic deals reshape portfolios: PPG bought VersaFlex in 2024 to deepen polyurea and polyaspartic capabilities and announced further divestments in architectural coatings to free capital for specialty segments[3]PPG, “Agreement to sell architectural coatings business,” investor.ppg.com . Sika’s acquisition of Kwik Bond equips it with turn-key polymer concrete solutions for bridge decks. Japan’s Nippon Paint, confronting raw-material inflation, passes price increases and accelerates captive resin production to hedge volatility. Across the polyaspartic coatings market, firms with scale, proprietary resin back-integration, and advanced technical-service teams are best positioned to withstand cost swings and to capture premium specification wins.

Polyaspartic Coatings Industry Leaders

Akzo Nobel N.V.

BASF SE

PPG Industries Inc.

The Sherwin-Williams Company

Covestro AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening where owners and contractors value rapid return-to-service alongside lower-VOC compliance, particularly in commercial and industrial flooring (the largest application) and in infrastructure maintenance windows where lane closures are constrained. Regulatory and certification pull-through supports this shift: Europe-focused green-building schemes and tightening VOC ceilings in construction products are accelerating interest in water-borne and documented low-emission systems, reinforcing demand for third-party emissions testing and certification-ready product lines.

Opportunities also track upstream capacity and vertical integration moves that improve supply security for key precursors and resins, helping formulators meet short project lead times in fast-moving construction markets. For example, Zhuhai Feiyang completed an expansion in April 2024 that added 26,000 tons per year of polyaspartic material capacity and 20,000 tons per year of diethyl maleate capacity, alongside an upgraded innovation center, strengthening availability of core inputs and development support for new grades. Technology whitespace includes cure-control approaches and new chemistries (latent catalysts for longer working time, silicone-modified backbones for durability tuning, and bio-based resin variants) that broaden applicability beyond interior floors into exterior protective, UV-cured, and specialty membrane uses where contractors need a larger application window without giving up fast commissioning.

Recent Industry Developments

- May 2026: BASF introduced Efka PX 4720, a dispersing agent positioned for radiation-curing coating systems, including polyaspartic and UV-curable formulations, at American Coatings Show 2026. The launch targets formulators working to improve pigment wetting and stability while maintaining fast cure and high-solids performance in advanced polyaspartic systems.

- June 2025: Sherwin-Williams expanded deployment of Accelera One polyaspartic flooring system across multiple regional facilities, enabling faster installation timelines and broader contractor adoption.

- November 2024: Covestro increased production of Desmophen CQ NH polyaspartic resins at its Foshan, China facility, supporting grades with at least 25% bio-based content. The capacity move strengthens availability of lower-carbon resin options for formulators supplying fast-curing, durable coatings into Asia-led construction demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of polyaspartic coating materials sold for protective and decorative use on common substrates, where demand is tied to fast cure, chemical resistance, and durability needs across building and industrial environments.

Scope exclusions: We exclude upstream raw monomers, application labor services, and general-purpose polyurethane or epoxy coatings that are not sold as polyaspartic systems.

Segmentation Overview

- By Technology

- Solvent-borne

- Water-borne

- Powder

- UV-Cured

- By Type

- Pure Polyaspartic Coatings

- Hybrid Polyaspartic

- By Application

- Flooring

- Waterproofing and Moisture-Barrier

- Anti-Corrosive Top-Coat

- By End-Use Industry

- Building and Construction

- Marine

- Infrastructure

- Power Generation

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle east and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping how polyaspartic coatings are produced and where they are consumed, and then it is used to build a clean set of assumptions before interviews begin. Public sources used for this include US EPA VOC guidance, ECHA chemical dossiers, USITC trade data for coatings and resins, OECD and national statistics offices for construction and industrial output indicators, and peer-reviewed journals covering polyurea and coatings performance.

We also review annual reports, investor presentations, product technical data sheets, and credible industry press to understand typical use cases like flooring, infrastructure protection, and equipment coatings. Where available, a paid subscription is used for company financials and news screening, and another paid tool is used to scan patents and track technology signals like curing chemistry and low-VOC formulation activity. These examples are not exhaustive, and many other public and paid sources were also checked to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to confirm what is actually being bought and applied, and then to pressure-test pricing, channel mix, and replacement cycles that are not visible in public data. We spoke with a mix of formulators, distributors, applicators, and large end users across key consuming regions, so our assumptions on adoption in flooring and protective coatings stayed realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 18% | Managers: 51% | Americas: 22% |

Market-Sizing & Forecasting

Sizing uses a top-down build that reconstructs demand from coatings consumption signals and end-use activity, followed by product-level adoption assumptions for polyaspartic systems in the mix. In practice, we start from construction and industrial maintenance spending indicators, then translate that into coating demand using area-based application intensity, typical dry film thickness patterns, and repaint or refurbishment cycles that reflect how projects are usually sequenced.

To keep results grounded, selective bottom-up checks are applied, such as sampled price per kilogram by region, distributor channel checks on volume movement, and supplier revenue exposure cross-checks where disclosures exist. Key inputs that are watched closely include VOC-driven shifts toward low-emission formulations, flooring and infrastructure project starts, industrial downtime tolerance (which drives fast return-to-service demand), and resin pricing direction that affects blended selling prices. Forecasts are run using scenario analysis supported by expert views on construction activity and industrial capex, and gaps in the bottom-up checks are handled through conservative interpolation based on comparable substrate and application patterns.

Data Validation & Update Cycle

Outputs are validated through multiple passes that look for variance against independent signals, such as construction output direction, coatings demand indicators, and observable pricing moves in resin and formulated coatings. When a number looks off, the model is reopened, assumptions are rechecked, and targeted follow-ups are triggered with interviewees to confirm whether the change is real or caused by a definition mismatch.

Before sign-off, another analyst reviews calculations and logic, and edge cases like currency timing, unusually high price inflation, or sudden demand shocks are tested. The report is refreshed each year, with interim updates if a material event changes demand, regulation, or supply, and a final pre-delivery check is completed so clients receive the latest view.

Mordor Intelligence's Polyaspartic Coatings Market Size Compared With Other Published Estimates

Published numbers for polyaspartic coatings do not always line up, and the gaps usually come from what each publisher counts, the base year chosen, and how pricing is carried forward in the forecast. Even when the same terms are used, some studies are effectively tracking a narrower flooring-led demand pool, while others include adjacent fast-cure polyurea or protective coating chemistries.

End-use activity signals like construction output direction and industrial maintenance intensity, combined with primary feedback on regional price bands and adoption by application, are the checks that keep Mordor Intelligence tied to a repeatable demand pool for polyaspartic coatings. Differences also come from how fast curing and low-VOC shifts are translated into penetration rates, whether currency conversion is done on annual averages or spot timing, and how recently the assumptions were revalidated after resin price swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.40 B (2026) | |

| Industry Data Publisher A | USD 0.40 B (2024) | Uses a 2024 base year and a shorter forecast window, and the scope description leans on broad segmentation labels that can blend adjacent fast-cure coating types, which can shift totals when definitions are tightened. |

| Research Publisher B | USD 0.38 B (2024) | Anchors the model on a single base year value and a headline CAGR, with limited visibility on how blended pricing and regional adoption are updated after feedstock-driven price changes. |

The spread in the table is mostly explained by base-year choice and how strictly the product boundary is applied, and then by the pricing and penetration logic used to move from history to forecast. By keeping assumptions traceable to practical demand indicators and interview-checked price ranges, we end up with a number that can be replicated and stress-tested without relying on hidden steps.

Key Questions Answered in the Report

1. What is the current polyaspartic coatings market size?

The market is valued at USD 401.03 million in 2026.

2. What growth rate is expected for the polyaspartic coatings industry through 2031?

A forecast CAGR of 5.18 % is projected for 2026-2031.

3. Which region holds the largest polyaspartic coatings market share?

Asia-Pacific leads with about 44.70% share in 2025.

4. Why are water-borne polyaspartic coatings gaining traction?

They meet stricter environmental regulations while closing the performance gap with solvent-borne systems.

5. What application segment generates the most demand?

Flooring represents roughly 59.20% of total demand due to rapid installation and long service life.

6. How do polyaspartic coatings compare to epoxy alternatives in lifecycle cost?

Although initial prices are higher, longer intervals between recoats and reduced downtime often lower total ownership costs over time.

Page last updated on: