Glass Flake Coating Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.27 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Flake Coating Market Analysis by Mordor Intelligence

The Glass Flake Coating Market size is expected to grow from USD 1.74 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at 4.52% CAGR over 2026-2031. Adoption accelerates as asset owners shift from lowest-bid procurement toward life-cycle cost modeling, recognizing that dense lamellar barriers defer maintenance and extend overall asset life. Oil and gas pipeline integrity programs, offshore wind foundation deployment, and chemical plant debottlenecking jointly underpin robust demand, while epoxy formulation advances reduce cure schedules and open new ambient-temperature application windows. Supply chains remain exposed to resin price swings, yet vertical integration and long-term offtake agreements by leading suppliers shield project timelines. Regional specialists that can satisfy ISO 17025 laboratory accreditation and ISO 12944-9 fingerprinting carve defensible niches alongside multinational incumbents.

Key Report Takeaways

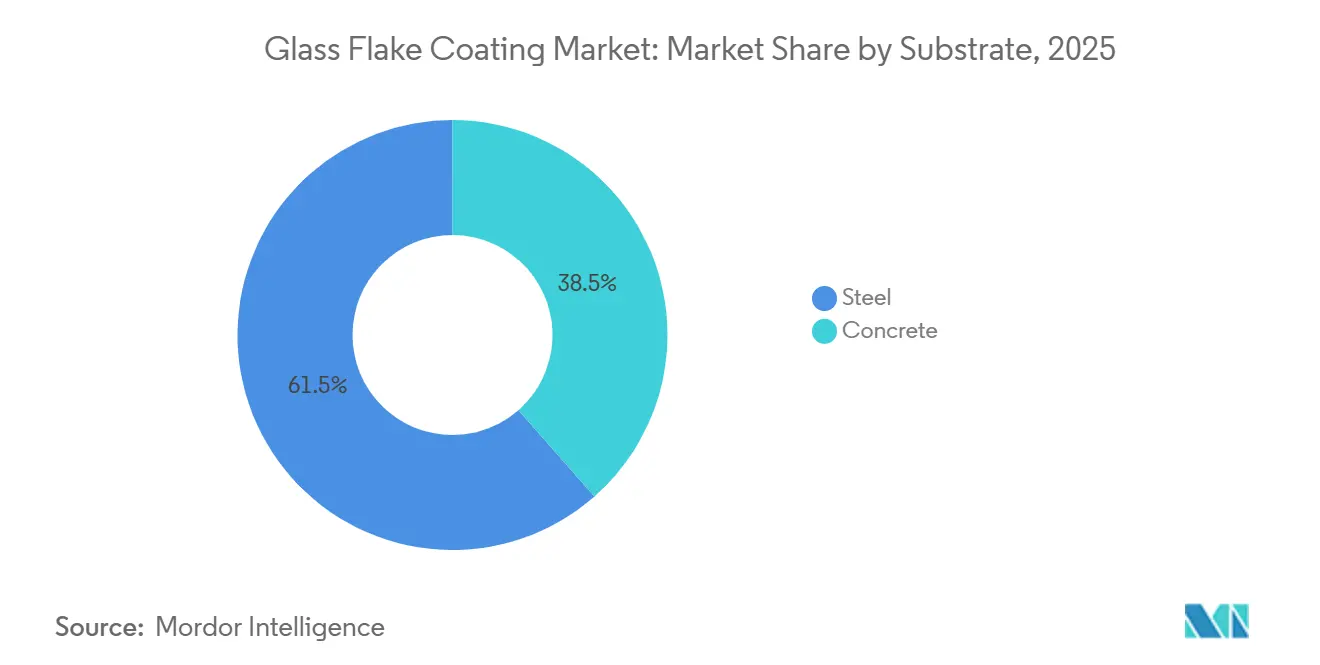

- By substrate, steel accounted for 61.47% of the glass flake coating market share in 2025; concrete is expanding at a 5.82% CAGR through 2031.

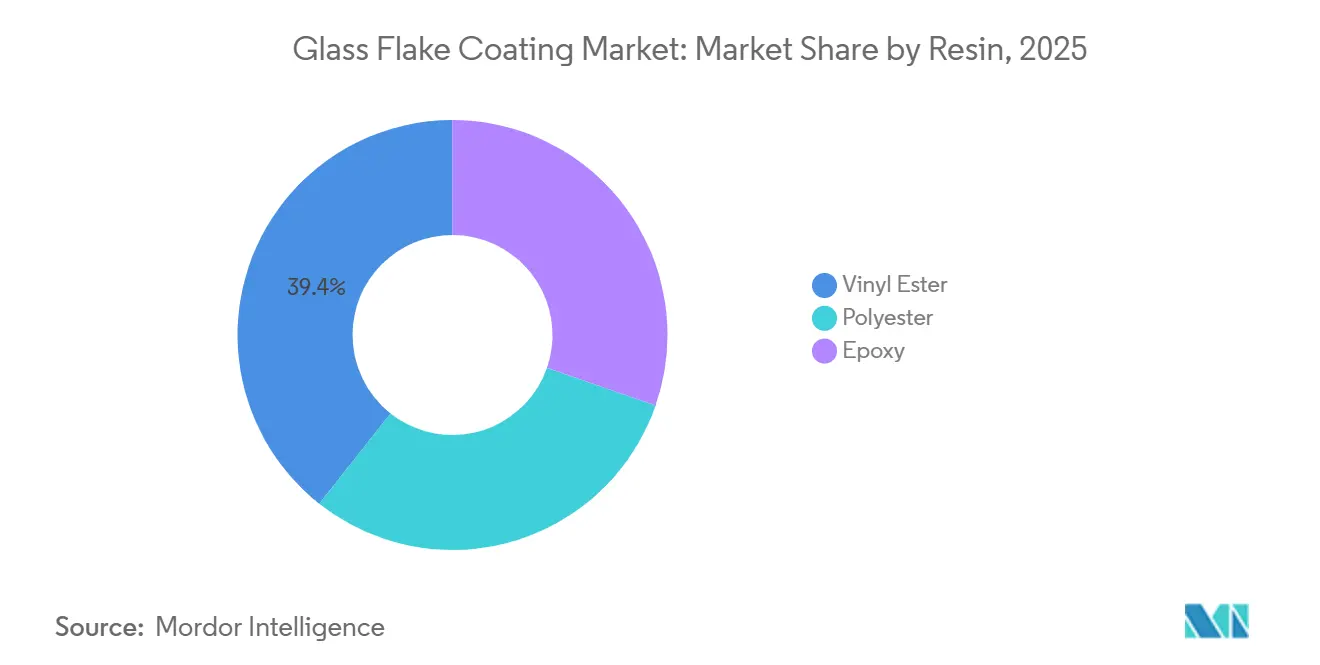

- By resin, vinyl ester held 39.36% share in 2025, while epoxy is growing at the fastest 5.94% CAGR through 2031.

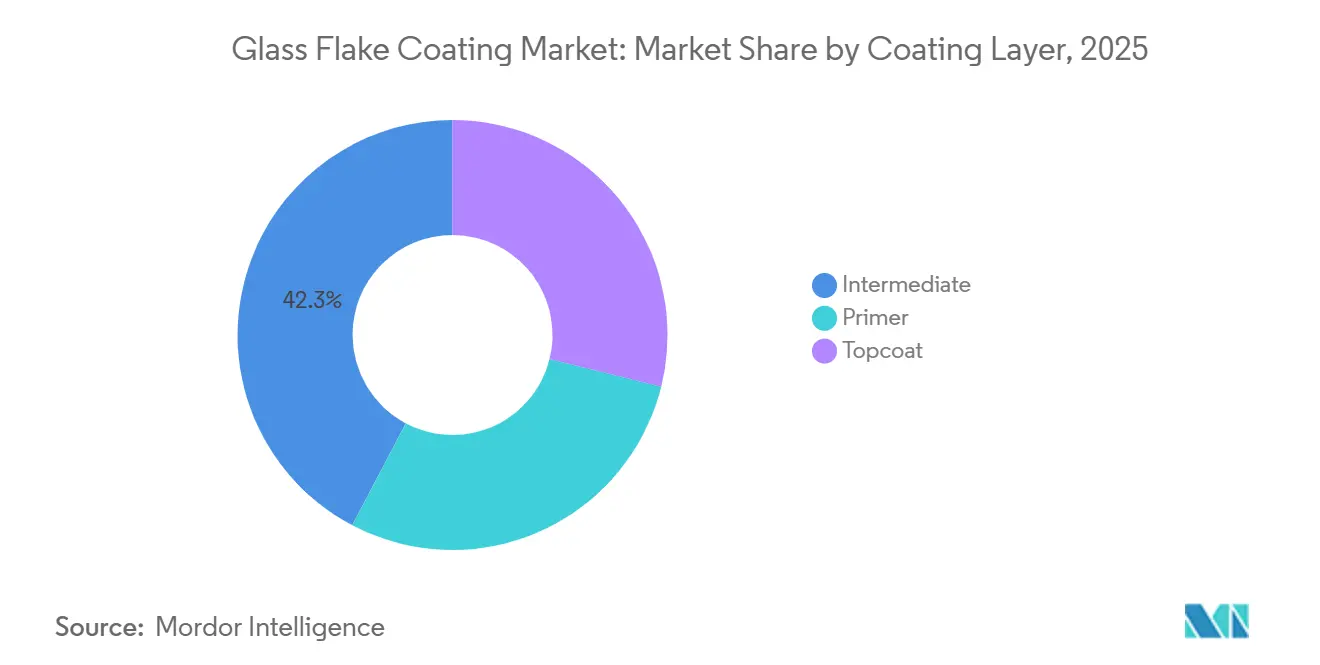

- By coating layer, intermediate coats led with 42.28% of the glass flake coating market size in 2025; topcoat is projected to rise at a 5.88% CAGR through 2031.

- By end-user industry, oil and gas commanded 37.54% share in 2025, whereas chemical processing is forecast to post the highest 5.97% CAGR to 2031.

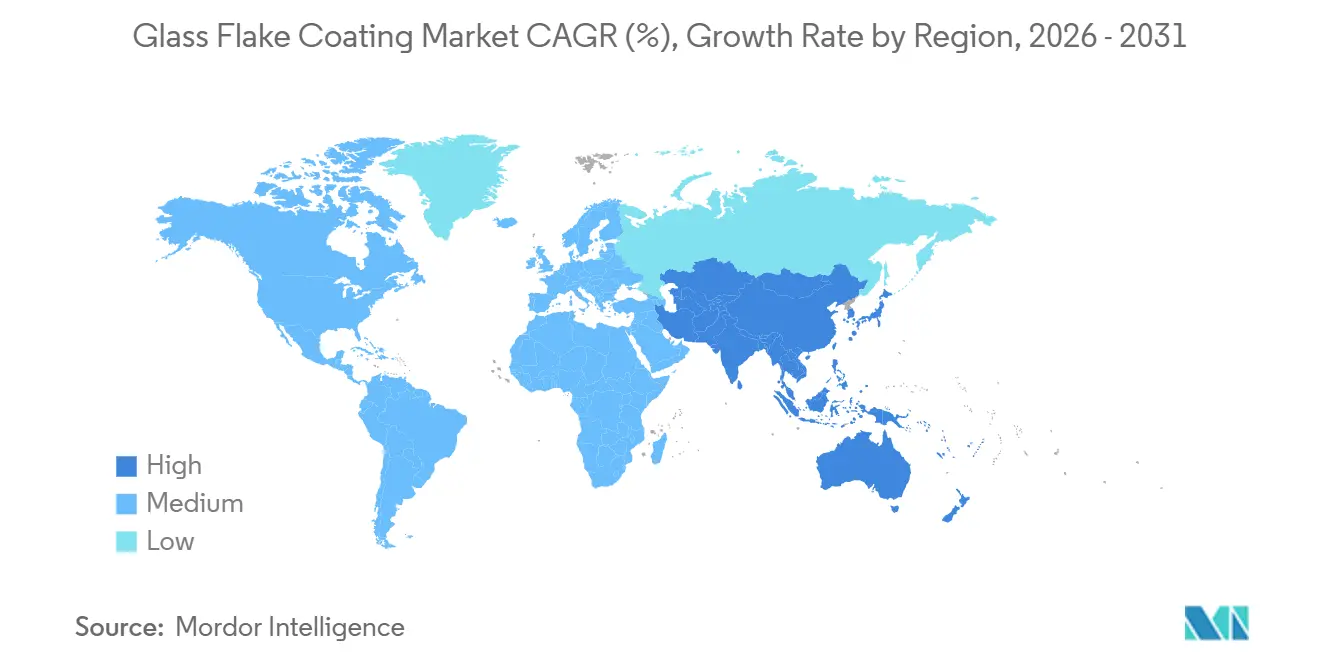

- By geography, Asia-Pacific commanded 46.31% share in 2025 and is forecast to post the highest 5.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Glass Flake Coating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Oil and Gas Pipeline Maintenance Activities | +1.2% | Global, with concentration in North America, Middle East, and Asia-Pacific | Medium term (2-4 years) |

| Severe Corrosion Challenges in Marine Infrastructure | +1.4% | Global, particularly Europe (offshore wind), Asia-Pacific (shipbuilding), and Middle East (offshore platforms) | Long term (≥ 4 years) |

| Rising Demand for High-Performance Coatings in Chemical Processing | +0.9% | Global, with early adoption in North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stringent Environmental Regulations Driving Long-Life Protective Systems | +0.7% | North America and Europe (EPA VOC limits, ISO 12944), cascading to Asia-Pacific | Long term (≥ 4 years) |

| Shift Toward Life-Cycle Cost Modeling in Asset-Intensive Sectors | +0.8% | Global, led by Europe (offshore wind), North America (infrastructure), and Middle East (oil & gas) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Oil and Gas Pipeline Maintenance Activities

Pipeline operators are extending service life rather than replacing assets, elevating glass flake systems from premium options to baseline specifications under IOGP S-715, which prescribes 1,000 µm total dry film thickness and cyclic aging validation[1]International Association of Oil & Gas Producers, “Specification S-715,” iogp.org . Energy Institute guidelines reinforce mandatory condition surveys and certified inspector oversight, adding a services multiplier to material demand. PHMSA enforcement in North America now links integrity digs to coating upgrades, particularly at girth welds where fusion-bonded epoxy is impractical. Qualification barriers rise as applicators must hold NACE or FROSIO Level III credentials and ISO 9001 systems, consolidating work among experienced contractors. As a result, the glass flake coating market benefits from specification-driven pull rather than discretionary spend.

Severe Corrosion Challenges in Marine Infrastructure

IMO PSPC mandates a 15-year ballast-tank coating life with zero blistering and a minimum 5 MPa adhesion threshold, benchmarks consistently met by multi-layer glass flake epoxy packages. A three-coat, 1,400 µm scheme surpassed thermal-sprayed aluminum under Arctic cyclic freeze testing, underscoring resilience in low temperatures. Jotun's Baltoflake polyester delivers 30-plus maintenance-free years in splash zones, and a DNV study pegged life-cycle cost savings at 50% relative to conventional epoxies. Offshore wind expansion adds thousands of monopiles and transition pieces that must meet ISO 24656 Type V glass-flake criteria, converting corrosion control into a material program line item. These dynamics lock glass flake solutions into vessel, jack-up, and foundation specifications worldwide.

Rising Demand for High-Performance Coatings in Chemical Processing

Plant managers leverage glass flake linings to tolerate hotter, more aggressive feeds without expensive alloy upgrades, cutting capital outlay by up to 50% on large reactors. Products such as Belzona 1523 allow continuous immersion at 140 °C, pushing barrier capability into territory once reserved for specialty metals. Advanced Polymer Coatings’ ChemLINE 784 competes by touting 85% volume solids and resistance to 98% sulfuric acid, intensifying R&D around cure speed and field repairability. Predictive integrity programs that quantify avoided shutdowns justify the upfront premium, embedding glass flake coatings within plant debottlenecking capital projects.

Stringent Environmental Regulations Driving Long-Life Protective Systems

The U.S. EPA caps industrial maintenance coating VOCs at 450 g/L, with exceedance fees discouraging solvent-rich formulas. High-solids glass flake epoxies meet limits but pose sprayability challenges that suppliers mitigate through exempt solvents and in-line heating rigs. EU directives link corporate carbon disclosure to product selection, giving low-VOC, long-life systems a compliance edge. ISO 12944 revisions introduce ≥ 25-year durability bands and integrate sustainability metrics, rewarding vertically integrated producers that disclose embodied carbon footprints. Consequently, environmental policy both narrows formulation latitude and elevates technical differentiation opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Raw-Material and Resin Prices | -0.6% | Global, with acute impact in Asia-Pacific (resin production hubs) and Europe (energy-intensive manufacturing) | Short term (≤ 2 years) |

| Volatile Oil Prices Delaying CAPEX Cycles | -0.5% | Global, concentrated in Middle East, North America (shale), and offshore regions | Short term (≤ 2 years) |

| Application Complexity Requiring Skilled Workforce | -0.3% | Global, with acute shortages in North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Raw-Material and Resin Prices

Unsaturated polyester resin prices in China moved downward by 100-200 CNY per t in early 2024, but epoxy prices in the United States swung 14% month-over-month due to bisphenol-A outages and port congestion, compressing gross margins and complicating bid validity windows. Large vendors hedge through multi-year supply contracts, yet regional players pass volatility downstream, eroding competitiveness on fixed-price tenders. Energy-intensive glass flake production adds another variable, tying cost curves to LNG and electricity prices across Europe.

Volatile Oil Prices Delaying CAPEX Cycles

Brent falling below USD 70/bbl in late 2024 postponed multiple Gulf Coast petrochemical expansions and North Sea platform overhauls, deferring coating demand by 6-12 months[2]U.S. Energy Information Administration, “Petroleum & Other Liquids,” eia.gov . During downturns, owners revert to lowest-price procurement, temporarily favoring standard epoxies. Suppliers with multi-market factories, such as PPG’s USD 300 million Tennessee plant, absorb the shock by redeploying capacity to automotive or construction volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate: Steel Dominance Reflects Infrastructure Legacy

Steel contributed 61.47% of the glass flake coating market size in 2025 on the strength of global pipeline networks, offshore platforms, tanker hulls, and process vessels. Lamellar flakes orient parallel to steel substrates, delivering diffusion paths up to 20 times longer than neat resin and meeting NORSOK M-501 splash-zone performance levels. Contractors and inspectors are trained almost exclusively on steel protocols, reinforcing the substrate’s hegemony. Coupling specifications with qualified workforce availability makes steel’s dominance self-reinforcing over the forecast period.

Concrete trails but advances at a 5.82% CAGR as Asia-Pacific infrastructure owners adopt glass flake epoxies to arrest chloride ingress in bridges and wastewater assets. ACI PRC-515.2-13 lists vinyl ester and epoxy coatings for high-acid environments, provided surface moisture and profile are tightly controlled. The higher porosity of concrete necessitates vapor-permeable primers or embedded scrims to mitigate blister risk, favoring turnkey suppliers that bundle surface preparation, primer, and overcoat warranties.

By Resin: Vinyl Ester Incumbency Versus Epoxy Innovation

Vinyl ester retained 39.36% of the glass flake coating market share in 2025, supported by decades of splash-zone field performance under IOGP and IMO rules. Pre-approved formulations and known cathodic-disbondment behavior reduce owner risk in seawater immersion. However, epoxy is outpacing at a 5.94% CAGR through 2031 thanks to high cross-link densities and ambient cures that narrow historical performance gaps. Epoxies also bond better to marginally prepared steel, expanding retrofit suitability. Polyester remains confined to cost-sensitive construction applications, where 10-15-year service life suffices.

By Coating Layer: Intermediate Coats Drive System Thickness

Intermediate captured 42.28% of the glass flake coating market size in 2025 because IMO PSPC and NORSOK M-501 demand total dry film thickness of 1,000 µm or more. These mid-layers embed glass flakes to provide impermeability and mechanical strength, while primers focus on adhesion and topcoats on UV resistance. Topcoats nonetheless post a 5.88% CAGR as offshore wind and bridge projects specify color-stable polyurethane or polysiloxane finishes to reduce survey frequency. System suppliers that integrate all three layers under a single warranty capture specification preference.

By End-user Industry: Oil and Gas Sets Performance Benchmarks

Oil and gas dominated with a 37.54% share in 2025, and its rigorous qualification regimes cascade into marine, chemical, and infrastructure procurement. Field data collected under API 579 fitness-for-service assessments continually validate long-term barrier performance, reinforcing reliance on glass flake packages. Chemical processing, rising at a 5.97% CAGR, deploys glass flake linings to handle hot acids and solvents without exotic alloy retrofits, exemplified by ChemLINE 784 and Protecto-Coat EPG installations. Marine adoption remains tethered to IMO compliance, but offshore wind is emerging as a parallel volume driver.

Geography Analysis

Asia-Pacific commanded 46.31% of the glass flake coating market in 2025 and will expand at a 5.63% CAGR, led by Chinese pipeline buildouts, Indian refinery upgrades, and Southeast Asian LNG terminals that cluster in high-chloride coastal zones. Multinational suppliers leverage Singapore-based training centers and ISO 17025 labs to navigate fragmented ASEAN regulations, securing bulk orders ahead of local challengers. North America's demand is supported by PHMSA-driven pipeline integrity digs and federally funded bridge preservation that embed life-cycle cost methodology. The new PPG Tennessee facility, operational in 2026, provides regional buffer stock that reduces lead time for Gulf Coast turnarounds.

Europe is seeing growth, with ScotWind and INTOG foundations alone adding an addressable demand of more than 2,000 monopiles through 2035. The CoaST program's waterborne advances aim at lowering carbon footprints and application complexity, aligning with EU Green Deal objectives. South America and the Middle East and Africa show upside from Brazilian pre-salt FPSOs and Saudi refinery upgrades, constrained by skilled labor shortages and inconsistent standard enforcement.

Competitive Landscape

The top five suppliers - Jotun, Hempel, PPG, Sherwin-Williams, and AkzoNobel - collectively control roughly 65% of global revenue, signalling moderate fragmentation that leaves space for niche specialists. Type approval for IMO and NORSOK systems raises entry barriers, yet regional firms with ISO 17025 labs and certified applicator networks - such as Chugoku Marine Paints and KCC - win local projects by offering agile technical support. Strategic thrusts concentrate on vertical integration; AkzoNobel's industrial excellence roadmap targets EUR 250 million in profit through supply-chain optimization by 2027. Digital twins like Jotun HullSkater and AkzoNobel Aerofleet capture application data, enabling predictive maintenance contracts that convert coatings into service revenues. Disruptive research explores graphene or ceramic platelet fillers promising equal barrier performance at lower density, but the absence of multi-decade field history slows specification acceptance.

Glass Flake Coating Industry Leaders

Akzo Nobel N.V.

PPG Industries, Inc.

Jotun A/S

The Sherwin-Williams Company

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Indian Department of Heavy Industry issued a significant tender for internal glass flake epoxy coating for welded joints. It indicated a strong demand for glass flake coating in infrastructure maintenance.

- December 2024: Akzo Nobel N.V. published a study that presented research on glass flake coatings. The study emphasized that protective coatings with a higher concentration of lamellar glass flake were highly effective in providing long-term protection for offshore structures.

Global Glass Flake Coating Market Report Scope

A glass flake coating is a protective layer composed of thin, flat glass flakes embedded in a resin binder, such as epoxy or vinyl ester. This structure forms a dense, overlapping barrier that significantly reduces the permeation of moisture, gases, and chemicals. It provides enhanced corrosion resistance, hardness, and abrasion resistance, making it suitable for industrial, marine, and chemical applications.

The glass flake coatings market is segmented by substrate, resin, coating layer, end-user industry, and geography. By substrate, the market is segmented into steel and concrete. By resin, the market is segmented into vinyl ester, polyester, and epoxy. By coating layer, the market is segmented into intermediate, primer, and topcoat. By end-user industry, the market is segmented into oil and gas, marine, chemical processing, industrial, construction, and other end-user industries. The report also covers the market size and forecasts for glass flake coatings in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Steel |

| Concrete |

| Vinyl Ester |

| Polyester |

| Epoxy |

| Intermediate |

| Primer |

| Topcoat |

| Oil and Gas |

| Marine |

| Chemical Processing |

| Industrial |

| Construction |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Substrate | Steel | |

| Concrete | ||

| By Resin | Vinyl Ester | |

| Polyester | ||

| Epoxy | ||

| By Coating Layer | Intermediate | |

| Primer | ||

| Topcoat | ||

| By End-user Industry | Oil and Gas | |

| Marine | ||

| Chemical Processing | ||

| Industrial | ||

| Construction | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the glass flake coating market expected to grow through 2031?

The market is projected to expand at a 4.52% CAGR, moving from USD 1.82 billion in 2026 to USD 2.27 billion by 2031.

Which end-user industry segment drives specifications in this space?

Oil and gas leads specifications, holding 37.54% revenue share in 2025 and influencing standards like IOGP S-715 and NORSOK M-501.

Why are epoxies gaining share against vinyl esters?

New high-crosslink epoxies cure at ambient temperatures, approach vinyl ester impermeability, and are projected to post a 5.94% CAGR through 2031, the fastest among resins.

What geographic region offers the highest growth potential?

Asia-Pacific combines 46.31% share with a 5.63% CAGR, buoyed by pipelines, refineries, and offshore wind builds in China, India, and ASEAN.

Page last updated on: