Self-Healing Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

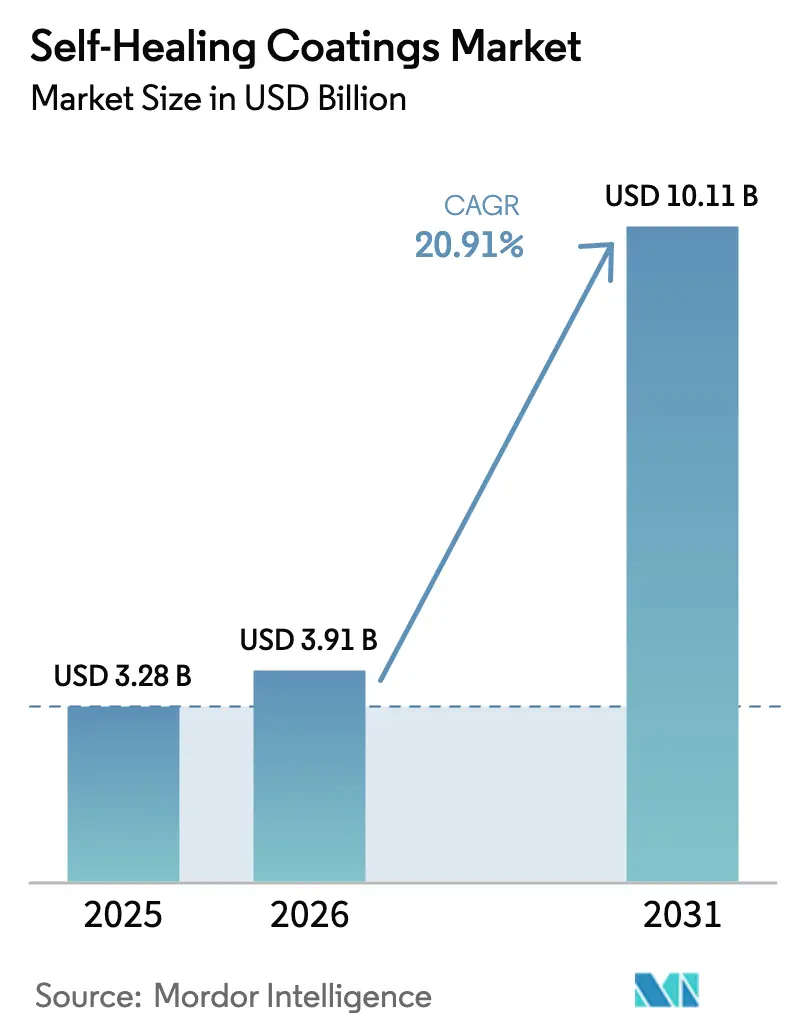

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 10.11 Billion |

| Growth Rate (2025 - 2030) | 20.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Healing Coatings Market Analysis by Mordor Intelligence

The Self-Healing Coatings Market size is expected to increase from USD 3.28 billion in 2025 to USD 3.91 billion in 2026 and reach USD 10.11 billion by 2031, growing at a CAGR of 20.91% over 2026-2031. OEMs and infrastructure owners are now prioritizing materials with long-lasting durability over frequent repaint cycles. This strategic pivot has expanded project scopes and boosted average order values. Extrinsic capsule technology, with its seamless integration into existing polyurethane and epoxy chemistries through a minor process tweak, leads in revenue share. Meanwhile, intrinsic reversible-bond systems, as synthesis costs have decreased, have transitioned from pilot scales to commercial production. Construction agencies in Europe, North America, and the Asia-Pacific are now issuing tenders emphasizing self-healing specifications. This push is expanding volume growth beyond the once-niche markets of aerospace and electronics. In tandem, coating formulators are embedding IoT sensors to monitor healing events in real-time. This advancement not only creates new data streams but also quickens procurement cycles and justifies premium pricing.

Key Report Takeaways

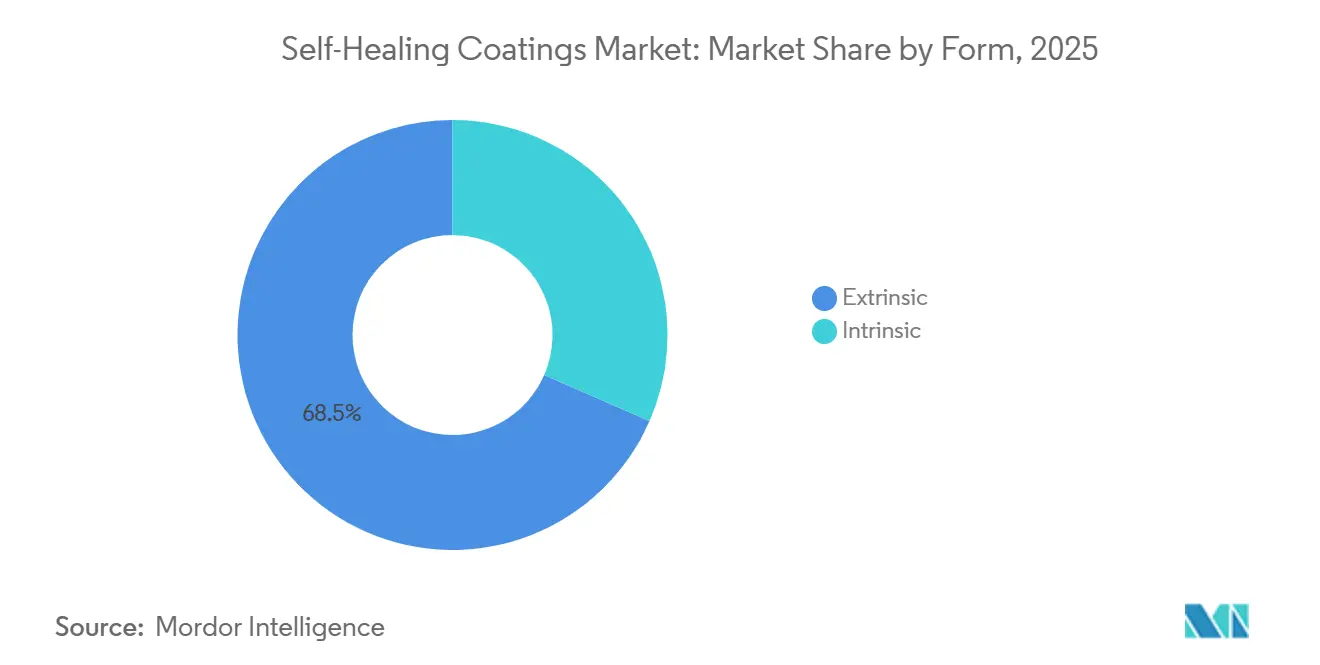

- By form, extrinsic formulations captured 68.45% of 2025 revenue, whereas intrinsic chemistries are advancing at a 21.17% CAGR through 2031.

- By material type, polymers held 44.31% of revenue in 2025 and remain the fastest-growing material category at a 21.42% CAGR through 2031.

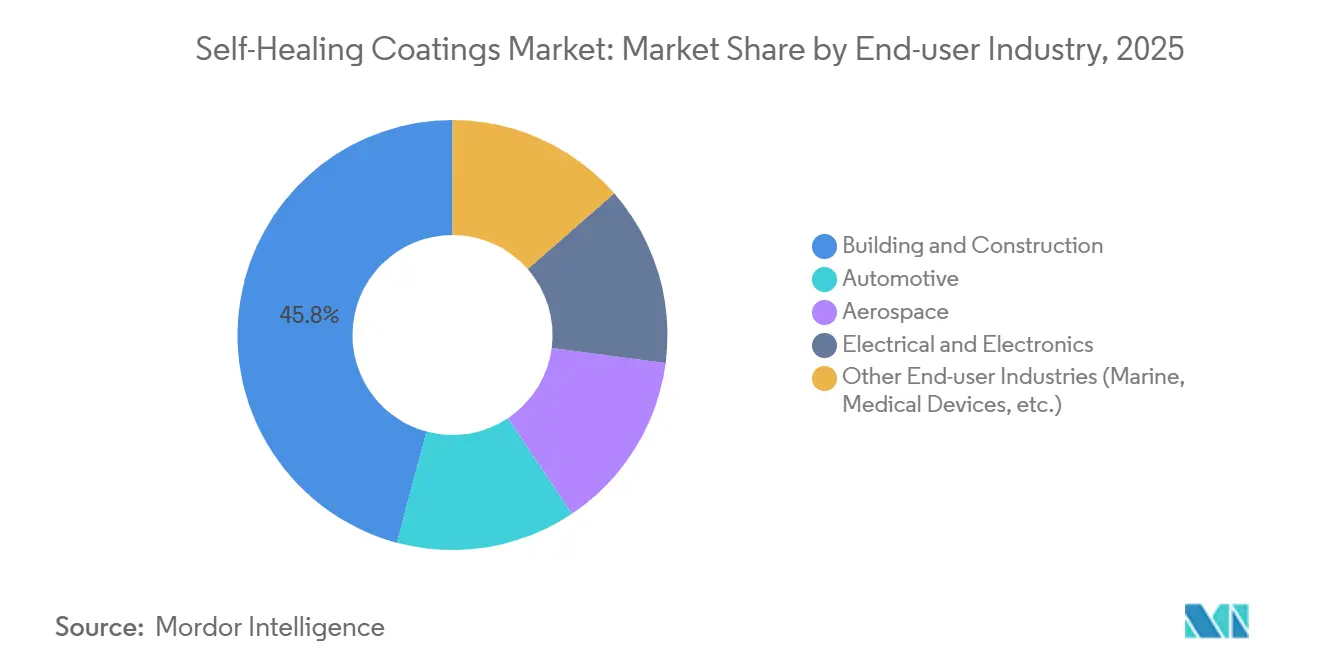

- By end-user industry, building and construction led with a 45.82% share in 2025, while electrical and electronics is projected to expand at a 22.25% CAGR to 2031.

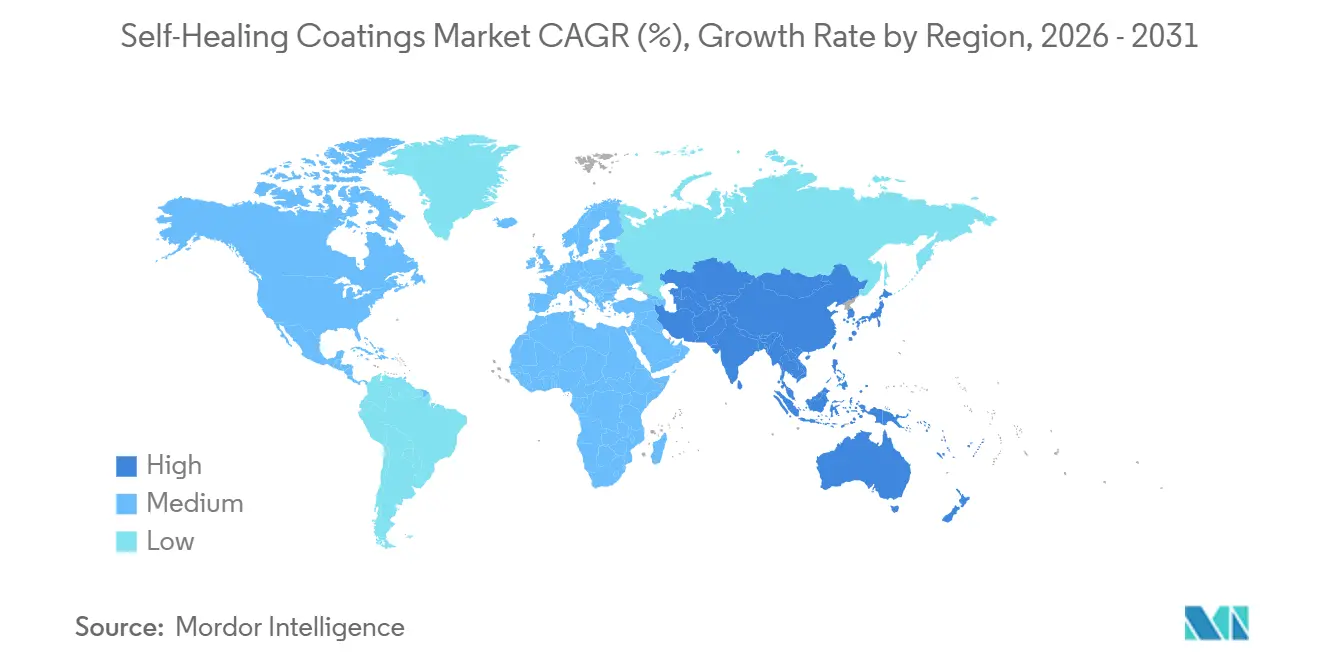

- By geography, Europe accounted for 48.91% of 2025 sales; Asia-Pacific is forecast to post the highest regional CAGR of 24.64% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Self-Healing Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in micro-capsule technology scale-up projects | +4.50% | Global | Medium term (2-4 years) |

| Increasing refurbishment demand from aging infrastructure in Asia and Europe | +5.20% | Asia-Pacific and Europe | Long term (≥4 years) |

| OEM push for lifetime corrosion warranty in EV platforms | +3.80% | Global, concentrated in North America, Europe, China | Medium term (2-4 years) |

| Mandatory anti-fouling norms driving marine adoption | +2.10% | Global, coastal regions and major shipping routes | Short term (≤2 years) |

| AI-enabled in-situ coating health monitoring unlocking service models | +2.90% | North America and Europe, early pilots in Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Micro-Capsule Technology Scale-Up Projects

In 2025, operations began for multi-ton capsule reactors, significantly reducing unit costs and bringing healing coatings closer to the price range of premium epoxies. Formulators, now utilizing capsule diameters averaging under 10 µm, achieved a significant advancement in automotive clearcoats by attaining high packing density without any film haze. Offshore wind towers, featuring dual-shell architectures, successfully passed rigorous salt-spray tests, confirming their durability in the field. The ability to co-extrude capsules using standard spray equipment enabled contractors to avoid substantial capital expenditures, smoothing the transition to trial adoption. In response to these advancements, tier-one resin suppliers introduced capsule masterbatch offerings that seamlessly integrate into current mixing lines, further accelerating global adoption.

Increasing Refurbishment Demand from Aging Infrastructure in Asia and Europe

Public agencies, addressing aging infrastructure from the 1960s, such as bridge decks, tunnels, and rail viaducts, are now prioritizing rehabilitation over complete overhauls to conserve capital. In 2025, Horizon Europe allocated a significant amount of funding to resilience projects, emphasizing self-healing coatings to extend recoating intervals. China's transport ministry is implementing polymer overlays that autonomously seal minor cracks, aiming to reduce lifecycle costs across its extensive expressway network. Concurrently, India's National Infrastructure Pipeline has allocated substantial funds for retrofitting railway bridges, incorporating coatings that extend inspection intervals. As extreme weather intensifies freeze-thaw cycles, asset owners increasingly view self-healing technology as a safeguard against unexpected closures.

OEM Push for Lifetime Corrosion Warranty in EV Platforms

Leading automakers, including Tesla, Volkswagen, and General Motors, are now offering extended corrosion warranties on their latest EV models. This initiative has increased scrutiny on paint suppliers to validate their products' healing efficacy under accelerated salt-fog conditions. Following this trend, BYD introduced a warranty across its entire range, prompting Chinese tier-one suppliers to ensure their capsule-infused primers meet rigorous standards. Battery enclosures, particularly at their aluminum-steel joints, are susceptible to galvanic corrosion. However, self-healing coatings that release inhibitors on demand present a cost-effective protective measure. With warranty claims directly influencing OEM profits, procurement teams are increasingly willing to invest in materials that promise reduced long-term service costs. This strategic shift is firmly embedding self-healing specifications into upcoming EV platforms, with a forecast horizon extending from 2026 to 2031.

Mandatory Anti-Fouling Norms Driving Marine Adoption

In a pivotal regulatory action, the International Maritime Organization banned organotin and imposed restrictions on copper release rates[1]International Maritime Organization, “AFS Convention,” imo.org . This has steered maritime fleets toward biocide-free fouling-release topcoats. Ships treated with capsule-infused silicone and fluoropolymer coatings can restore their low surface energy when scratched. This breakthrough enables vessels to maintain smooth hulls for longer durations, translating to decreased fuel consumption on North Sea routes. The European Maritime Safety Agency has endorsed self-healing systems for vessels operating in marine protected zones. Early adopters of this technology report saving an entire dry-dock cycle every decade. Such advantages resonate deeply with shipowners striving to meet the stringent carbon-intensity benchmarks set by the International Maritime Organization.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premium versus legacy coatings | -3.20% | Global, acute in price-sensitive emerging markets | Short term (≤2 years) |

| Qualification hurdles in aerospace supply chain | -1.40% | North America and Europe, concentrated in commercial aviation | Medium term (2-4 years) |

| Nanocapsule raw-material toxicity debates | -0.90% | Europe and North America, regulatory scrutiny under REACH and TSCA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Qualification Hurdles in Aerospace Supply Chain

Small innovators face challenges in funding the additional costs associated with Nadcap accreditation and MIL-PRF-85285 compliance for each new primer program. Regulators have not yet standardized healing metrics, resulting in tailored reviews for each application and extended approval timelines. A change in formulation requires the recertification of downstream assemblies, delaying the rollout of even previously approved coatings. Until industry consortia establish unified test standards, aerospace adoption will remain limited to non-critical components, such as ground equipment and interior panels.

Nanocapsule Raw-Material Toxicity Debates

Polyurea-formaldehyde capsules release trace amounts of formaldehyde during curing. The European Chemicals Agency has requested additional ecotoxicity data on particles smaller than 100 nm[2]European Chemicals Agency, “Understanding REACH,” echa.europa.eu . Meanwhile, the United States Environmental Protection Agency's requirement for extensive pre-manufacture notices on new nanomaterials can significantly delay product launches. Environmental advocates warn that weathered coatings could release microplastics into waterways, prompting cities to consider excluding specific capsule systems from public tenders. While formulators are experimenting with chitosan and alginate shells, these alternatives have a shorter shelf life and softer mechanical properties, creating challenges for logistics and performance assurances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Capsule Economics Favor Extrinsic Dominance

In 2025, extrinsic systems accounted for 68.45% of the revenue, supported by rigorous quality-control measures that maintain capsule size and wall integrity on a large scale. The market share of extrinsic products in the self-healing coatings market is bolstered by their proven ability to seal over 80% of cracks in defects smaller than 100 micrometers. Intrinsic variants are experiencing a robust growth rate of 21.17% CAGR during the forecast period of 2026-2031, driven by the rapid transition of Diels-Alder linkages and hydrogen-bond networks from laboratory settings to practical applications.

Extrinsic capsules are predominantly utilized in marine and bridge structures, where impacts, though infrequent, carry significant consequences. In contrast, intrinsic chemistries excel in electronic housings, which endure constant micro-abrasion. Supply chains are now integrating both approaches, offering hybrid formulations that first seal through capsule rupture and subsequently utilize reversible bonds. With ISO committees developing healing test methods, specifiers are expected to benefit from clearer benchmarks, potentially steering the self-healing coatings market towards multi-cycle intrinsic systems.

By Material Type: Polymer Versatility Drives Leadership

Polymers accounted for 44.31% of the material revenue in 2025 and are projected to grow at a rate of 21.42% during the forecast period of 2026-2031. This growth is primarily attributed to the adaptability of polyurethane and epoxy matrices, which seamlessly integrate both capsules and dynamic crosslinks. The versatility of polymers enables a single SKU to serve the automotive, construction, and electronics sectors, thereby expanding the market reach. Metals and alloys, while occupying a specialized niche, rely on sacrificial oxidation rather than self-repair. In contrast, concrete systems utilize bacterial calcite precipitation, achieving notable restoration of compressive strength.

Polythioctic-acid resins, which heal at ambient temperatures through disulfide exchange, not only reduce reliance on energy-intensive cure ovens but also lower emissions at production plants. Concrete additives, previously limited to bridges, are now being utilized in residential basements in seismic zones. This trend positions the polymer segment to align with broader building codes, reinforcing its dominance in the self-healing coatings market through 2031.

By End-User Industry: Construction Anchors, Electronics Accelerates

The building and construction sector contributed 45.82% to 2025 sales, driven by the extensive surface-area requirements of bridges, tunnels, and parking structures. Even a modest penetration in these areas results in significant volumes, anchoring the self-healing coatings market. The electrical and electronics sector is projected to expand at a 22.25% CAGR during the forecast period of 2026-2031, propelled by the increasing adoption of conformal coatings by data-center operators and semiconductor fabs. These coatings effectively seal delamination and prevent moisture ingress.

In the automotive sector, the focus is on electric vehicle underbodies and battery-pack enclosures, where capsule primers play a critical role in reducing warranty corrosion claims. The aerospace sector, historically conservative, is now specifying intrinsic polyurethane clears for cargo-bay liners and cabin panels, enabling self-repair of scratches during service. Meanwhile, the marine industry is transitioning from copper-based anti-fouling paints to advanced silicone systems. These innovative systems not only self-heal upon damage but also extend dry-dock cycles. Collectively, these developments are diversifying revenue streams and mitigating cyclic risks for suppliers in the self-healing coatings market.

Geography Analysis

Europe, buoyed by Green Deal funding and Horizon Europe pilots, commanded 48.91% of 2025 revenue, underscoring a push for coatings that extend maintenance intervals to 20 years. In 2024, Germany allocated funds for retrofitting Autobahn bridges, mandating self-healing primers. The United Kingdom's Network Rail adopted concrete overlays, successfully reducing track-closure hours. France, meanwhile, endorsed polyurethane topcoats for high-speed catenary masts, slashing maintenance costs within 18 months. Nordic nations are now utilizing capsule systems that release inhibitors during freeze-thaw cycles. Mediterranean ports are transitioning crane structures to self-repairing silicone. These initiatives are consistently driving demand in the region.

Asia-Pacific, led by China's Belt and Road Initiative, is on track for a 24.64% CAGR through the forecast period of 2026-2031. In 2025, China integrated self-healing clauses into expressway tenders covering thousands of kilometers. India's railway-bridge fund is pushing for coatings that prolong inspection intervals. Japan's transport ministry is advocating self-healing protection for quake-prone piers. South Korea is embedding sensor-equipped coatings in smart-city transit hubs, funneling maintenance data into municipal dashboards. Suppliers across the region are boosting capsule production, addressing price disparities, and accelerating local adoption. This momentum is set to elevate the self-healing coatings market in emerging Asian nations.

North America is witnessing a surge in adoption, driven by the United States bridge bill, which recognizes self-healing coatings as an eligible expense. In Canada, cold-weather standards are sparking interest in low-Tg polyurethane clears, ensuring flexibility in frigid conditions. Concurrently, Mexico's automotive sector is shifting from e-coat tanks to capsule primers. Brazil is trialing silicone-based hull systems on pre-salt offshore rigs, targeting reduced downtime. In the Middle-East, mega-projects like NEOM are selecting coatings resistant to sandstorm abrasion. South Africa's mining industry is testing intrinsic epoxies on ore chutes. These varied projects are expanding the geographic revenue landscape of the self-healing coatings market.

Competitive Landscape

The self-healing coatings market is moderately fragmented. In 2026, BASF launched a capsule facility, targeting the European EV warranty extension market. PPG entered a partnership with a United States aerospace OEM, with aspirations for FAA-approved primer qualifications by 2028. Meanwhile, agile innovators such as Autonomic Materials, NEI Corporation, and GVD Corporation are establishing niches with vascular networks and nanocomposite films. While they adeptly fill gaps left by larger entities, they lack the scale for significant infrastructure contracts. Investors are rallying behind start-ups that blend bio-based capsules with AI monitoring, resonating with sustainability objectives and data-driven service agreements.

Patent filings in 2025 highlighted breakthroughs in dual-trigger systems, leveraging both thermal and mechanical stimuli, alongside hybrid designs merging capsules with reversible bonds. With ISO 4628 yet to define healing metrics, buyers are relying on supplier data, complicating competitive narratives. Independent laboratories are developing certification standards, and the endorsement of any specific standard could transform procurement dynamics. The fusion of material science, digital monitoring, and performance assurances emphasizes that the genuine competitive advantage lies in achieving verifiable multi-cycle healing at scale, rather than merely being the first to unveil a new chemistry.

Self-Healing Coatings Industry Leaders

Akzo Nobel N.V.

3M

BASF

PPG Industries Inc.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: TPU researchers have developed "self-healing" coatings designed for fusion reactor components. This advancement is expected to significantly enhance the operational lifespan of reactor equipment. The study, conducted under the state assignment "Science" No. FSWW-2023–0005, has been published in the Journal of Materials Science.

- October 2025: Researchers at MISIS University, in partnership with Chinese scientists, have developed a "self-healing" protective coating for niobium alloy products used in the energy and chemical industries. This coating significantly enhances wear and heat resistance compared to untreated niobium substrates.

Global Self-Healing Coatings Market Report Scope

Self-healing coatings are the type of coatings that have the innate potential to mend suffered damage on their own or with an external stimulus.

The self-healing coatings market is segmented by form, material type, end-user industry, and geography. By form, the market is segmented into extrinsic and intrinsic. By material type, the market is segmented into polymers, metals and alloys, concrete and cementitious, and ceramics and glass. By end-user industry, the market is segmented into building and construction, automotive, aerospace, electrical and electronics, and other end-user industries. The report also covers the market size and forecasts for self-healing coatings in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Extrinsic |

| Intrinsic |

| Polymers |

| Metals and Alloys |

| Concrete and Cementitious |

| Ceramics and Glass |

| Building and Construction |

| Automotive |

| Aerospace |

| Electrical and Electronics |

| Other End-user Industries (Marine, Medical Devices, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Form | Extrinsic | |

| Intrinsic | ||

| By Material Type | Polymers | |

| Metals and Alloys | ||

| Concrete and Cementitious | ||

| Ceramics and Glass | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Aerospace | ||

| Electrical and Electronics | ||

| Other End-user Industries (Marine, Medical Devices, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the self-healing coatings market?

The self-healing coatings market reached USD 3.91 billion in 2026 and is projected to hit USD 10.11 billion by 2031 at a 20.91% CAGR.

Which segment holds the largest self-healing coatings market share?

Extrinsic capsule formulations led with 68.45% of 2025 revenue.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to post a 24.64% CAGR, outpacing all other regions.

How are electric-vehicle warranties influencing adoption?

OEM commitments to 12-year corrosion coverage are driving capsule-filled primers into new EV platforms.

Are standardized healing tests available?

Not yet; ISO committees are drafting methods, and current approvals rely on proprietary supplier data.

Page last updated on: