Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

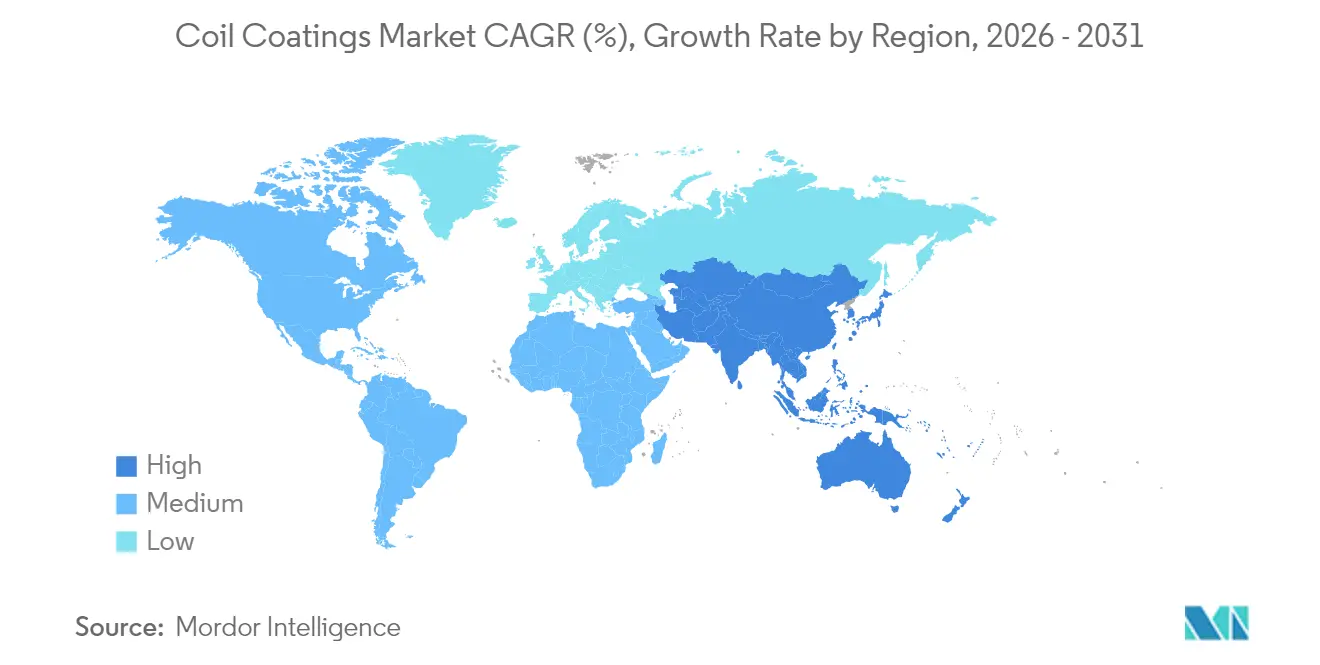

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coil Coatings Market Analysis by Mordor Intelligence

The Coil Coatings market size is expected to grow from USD 3.63 billion in 2025 to USD 3.75 billion in 2026 and is forecast to reach USD 4.41 billion by 2031 at 3.28% CAGR over 2026-2031. Steady construction spending, an upswing in appliance production, and tightening environmental rules anchor this trajectory, even as substrate competition and raw-material volatility moderate headline growth. Demand concentrates in roll-formed steel and aluminum sheets because pre-finishing offers faster installation, uniform quality, and lower lifetime cost than post-fabrication painting. Investments aimed at modular buildings, solar metal framing, and premium home appliances lift volumes in mature regions, while Asia-Pacific’s large manufacturing base keeps the coil coatings market firmly centered in the region. Across segments, polyester chemistries dominate, PVDF (Polyvinylidene Fluoride) gathers momentum in high-end exteriors, and the shift to PFAS-free fluoropolymers is reshaping innovation pipelines.

Key Report Takeaways

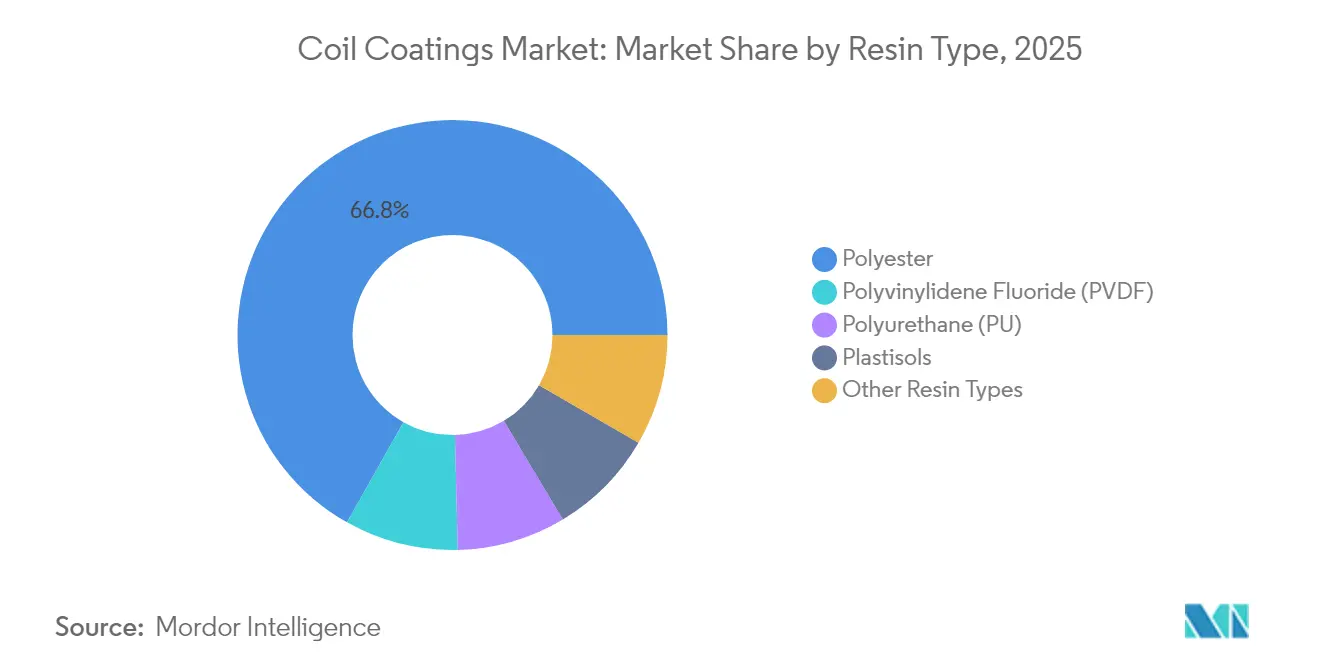

- By resin type, polyester held 66.84% of the Coil Coatings market share in 2025; PVDF is projected to deliver a 3.63% CAGR through 2031.

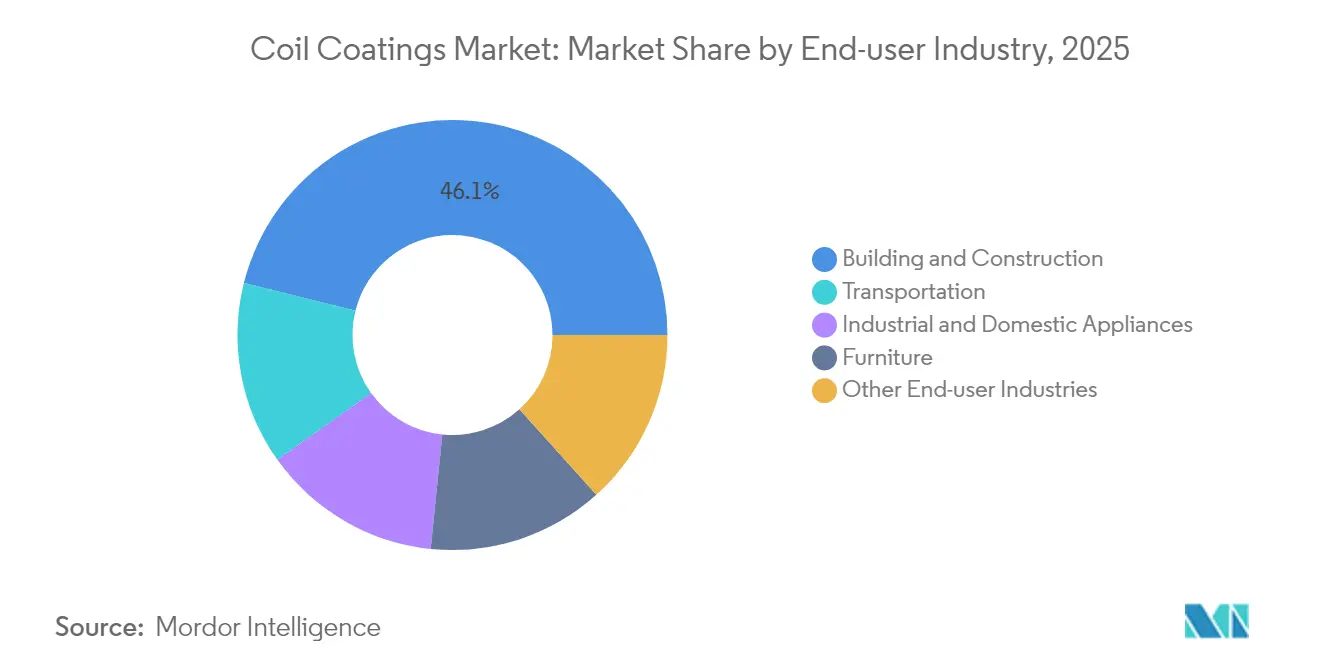

- By end-user industry, building and construction captured 46.12% of the Coil Coatings market size in 2025, while transportation is forecast to expand at a 3.52% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 49.88% of the coil coatings market size in 2025 and is advancing at a 3.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coil Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction Steel Demand Upswing | +0.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Energy-efficient Appliances Expansion | +0.6% | Global, concentrated in APAC manufacturing hubs | Long term (≥ 4 years) |

| Stricter VOC and Carbon Regulations | +0.5% | North America & EU primary, expanding to APAC | Short term (≤ 2 years) |

| Shift toward High-Durability Exterior Panels | +0.4% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Agrivoltaic Metal Framing Boom | +0.3% | Global, early adoption in EU, US, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Steel Demand Upswing

Recovering construction steel orders drive greater use of pre-coated coil because builders can eliminate on-site painting delays, mitigate weather risks, and lower labor costs. The World Steel Association signals a 2025 rebound in global steel demand, with non-residential and infrastructure spending pushing volumes in the United States, China, and India[1]World Steel Association, “Short Range Outlook 2025,” worldsteel.org. Governments channel stimulus into bridges, schools, and renewable-energy projects, favoring corrosion-resistant coil-coated panels. Modular construction firms increasingly specify factory-finished sheets to standardize quality and compress project timelines. Polyester and PVDF coatings with 20- to 30-year warranties support this momentum by lowering total maintenance expense. These factors underpin a significant share of future coil coatings market growth.

Energy-efficient Appliances Expansion

Appliance OEMs (original equipment manufacturers) specify coil coatings to satisfy thermal performance and design demands. Heat-pump outdoor units require finishes that survive freeze-thaw cycles while retaining heat-transfer efficiency, a need highlighted by the United States Department of Energy’s incentive programs. Korean manufacturers Samsung and LG are scaling premium built-in product lines worth USD 64.5 billion globally, with color-matched, scratch-resistant coatings acting as brand differentiators. Engineers must ensure chemical compatibility as refrigeration moves to low-GWP (Global Warming Potential) refrigerants; advanced polyester-silicone hybrids provide the necessary barrier. Luxury real-estate trends toward integrated kitchens elevate aesthetic expectations, pressuring suppliers to offer deep-hue, high-gloss coil options. These dynamics create durable demand pockets inside the coil coatings market.

Stricter VOC and Carbon Regulations

Regulators tighten allowable solvent emissions, forcing plants to adopt waterborne, high-solids, or powder formulations. The U.S. EPA National Emission Standards for Hazardous Air Pollutants (NESHAP) cut permissible VOC levels for coil coating lines, prompting capital upgrades and formulation revisions. In Europe, Best Available Techniques documents set a benchmark of 0.73–0.84 g/m² VOC output for continuous lines, catalyzing investments in regenerative thermal oxidizers and new coating chemistries. Manufacturers with low-VOC portfolios gain procurement preference from OEMs looking to decarbonize scope 3 footprints. Powder coil coating, though currently limited by curing-temperature constraints, is gaining R&D attention because it could eliminate solvent use. Therefore, Compliance pressure underpins risk mitigation and fresh sales opportunities across the coil coatings market.

Shift toward High-Durability Exterior Panels

Climate resilience priorities escalate performance specs for façades and roofs, lifting PVDF demand thanks to its UV and color-retention superiority. Cool-roof formulations incorporating infrared-reflective pigments reduce building energy loads, aligning with green-building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method). Architects increasingly request metallic and pearlescent finishes, stimulating advances in mica-based pigment systems that withstand thermal cycling without chalking. Regions prone to hurricanes or wildfires adopt impact-resistant and non-combustible metal panels, requiring robust topcoats compliant with ASTM E84 and FM 4473 standards. The result is a steady mix shift toward high-performance chemistries that sustain premium price points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Titanium Dioxide and Resin Prices | -0.4% | Global, with supply chain concentrated in China | Short term (≤ 2 years) |

| Plastic and Composite Material Substitution | -0.3% | North America & EU leading, spreading to APAC | Medium term (2-4 years) |

| PFAS-free Fluoropolymer Reformulations | -0.2% | Global, regulatory-driven in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Titanium Dioxide and Resin Prices

Titanium dioxide (TiO₂) markets experienced rapid price oscillations throughout 2024 as Chinese output cuts, power shortages, and environmental inspections collided with uneven demand from coatings, plastics, and paper. Because white and pastel coil colors rely heavily on TiO₂, quarter-to-quarter swings erode margins or trigger pass-through clauses that unsettle customers. Polyesters and acrylic resins follow upstream petrochemical cycles, so feedstock disruptions in Asia can ripple across global supply chains within weeks. Producers hedge by expanding multi-sourcing, raising safety stocks, or blending alternative pigments, yet these tactics inflate working capital and complicate formulation stability.

Plastic and Composite Material Substitution

In certain façades, vehicle body panels, and consumer goods, engineered plastics challenge coated metal based on weight savings and design flexibility. Danish firm Primo A/S supplies composite cladding profiles that tout corrosion immunity and point-of-sale customization. DuPont’s Zytel and Delrin families enable metal replacement in automotive brackets and housings, delivering mass reduction critical to electric-vehicle range goals[2]DuPont, “Engineering Polymers for Lightweighting,” dupont.com. Although high material cost and recycling hurdles limit polymer encroachment to niche or luxury segments, every incremental substitution trims the serviceable tonnage for the coil coatings industry over the mid-term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyester Dominance Faces PVDF Challenge

Polyester chemistries represented 66.84% of 2025 revenue thanks to low unit cost, broad color gamut, and compatibility with a spectrum of primers and backers. Recent investments in high-solids and weather-resistant hybrids strengthen their foothold in mid-range building and appliance programs. The coil coatings market size for polyester products eclipses USD 2.43 billion today, underpinning line utilization across Asia’s contract coaters. Although smaller in volume, PVDF grades post a 3.63% CAGR to 2031 as architects prioritize 30-year warranties and deep-tone aesthetics in large commercial façades. The coil coatings market share grabbed by PVDF is further fueled by cool-roof codes in hot climates that specify minimum solar-reflectance values.

Transitioning to PFAS-free fluoropolymers has initiated an intense R&D (research and development) race. NOF Metal Coatings Group unveiled pilot batches that match traditional weathering metrics, signaling viable pathways to regulation-proof premium topcoats. Sherwin-Williams’ RadGuard radiation-cure line illustrates another innovation vector: UV-triggered polymerization that trims natural-gas usage and raises line speed, appealing to coaters eager to curb carbon footprints. As customers judge bids not only on cost but also on embodied carbon and recyclability, resin suppliers with credible environmental data stand to gain wallet share across the coil coatings market.

By End-user Industry: Construction Leadership Amid Transportation Growth

Building and construction applications accounted for 46.12% of 2025 billings, covering roofing, siding, rainwater systems, and façade elements. Demand pivots around speed-to-site advantages—pre-coated sheets arrive ready to install—slashing labor and weather delays. Government infrastructure packages in the United States, Canada, and India keep pipeline visibility strong through 2027. Meanwhile, although only a mid-single-digit slice now, transportation advances at a 3.52% CAGR as automakers substitute painted blanks with coil-coated aluminum, streamlining stamping, and eliminating primer ovens. The coil coatings market size linked to EV battery casings and lightweight commercial trailers is gaining strategic importance for tier-one suppliers.

Electrification raises thermal-management and corrosion-resistance bars, prompting specification of silicone-modified polyesters and zinc-rich primers. The United States Department of Energy funds pilot lines exploring integrated insulation layers that could embed dielectric properties directly into coil-coated battery boxes. Appliance replacement cycles continue to deliver steady, margin-friendly volumes, particularly in premium stainless-look and matte finishes that replicate powder-coated aesthetics. Furniture and miscellaneous sectors remain specialized but profitable, tapping low-gloss polyurethanes for abrasion-resistant storage cabinets and signage.

Geography Analysis

Asia-Pacific held 49.88% of global revenue in 2025 and is on track for a 3.73% CAGR to 2031 despite pockets of steel oversupply. China’s stimulus-backed rail and EV charging buildout cushions domestic demand, while export-oriented coil lines feed appliance clusters across ASEAN. Japan leverages long-term supply deals with ocean-going shipyards and home-grown appliance majors to sustain premium PVDF demand, whereas South Korea’s appliance giants outsource additional tonnage to Vietnamese toll coaters to optimize logistics for export markets. India’s smart-city schemes and rural electrification spur orders for galvanized roofing and agrivoltaic structures, though price sensitivity favors local polyester formulations.

North America remains technology-focused, emphasizing regulatory compliance and durability over sheer growth. The coil coatings market size in the United States benefits from a remodeling boom and tax incentives for energy-efficient roofs. Stricter VOC caps from the South Coast Air Quality Management District accelerate high-solids adoption and drive capital upgrades among West Coast lines. Canada’s colder climate elevates insulation panels coated with flexible polyurethanes designed to withstand freeze-thaw cycles, while Mexico’s proximity to United States OEMs secures appliance backlog stability under USMCA (United States-Mexico-Canada Agreement) trade provisions.

Europe’s mature landscape values sustainability badges and traceability. Carbon-border adjustments and extended producer-responsibility schemes push mills and coaters to document cradle-to-gate emissions, rewarding suppliers with verified EPDs. Germany’s refurbishment grants promote cool-roof retrofits that favor PVDF, France’s agrivoltaic subsidies accelerate demand for corrosion-resistant framing, and the Nordics continue to specify matte polyesters for standing-seam metal roofs in residential constructions. South America and the Middle East & Africa contribute modest volumes but outsize potential; Brazil’s coastal resorts mandate anti-salt-spray coatings, while Gulf logistics hubs commission color-fast warehouse cladding amid extreme UV exposure. The overall geography spread insulates the coil coatings market against single-region shocks.

Regulatory Landscape

Coil coating producers work under tightening air-emissions and chemical-restriction regimes that influence resin and solvent selection. In the United States, the EPA regulates the surface coating of metal coil under NESHAP (40 CFR Part 63, Subpart SSSS, as updated on the eCFR through March 18, 2026). Facilities either meet MACT-based requirements or comply via alternative organic HAP emission limits using technologies such as incineration or solvent recovery, with monitoring and recordkeeping expectations.

In Europe, REACH restrictions continue to widen the compliance perimeter for industrial coatings and surface treatment chemistries. As of May 8, 2026, REACH Annex XVII listed 79 restricted substance entries, and in May 2026 the EU moved to restrict substances including N-methyl-2-pyrrolidone (NMP), N,N-dimethylformamide (DMF), and certain benzotriazole derivatives relevant to industrial coatings value chains. This reinforces reformulation toward lower-risk systems and more rigorous supplier declarations for both coatings and coated metal products.

Value Chain Analysis

The coil coatings value chain begins with upstream feedstocks (polyester, acrylic, and fluoropolymer resins; pigments such as titanium dioxide; solvents and additives), then moves through paint manufacturers and toll/formulation partners to coil coaters and integrated metal producers operating continuous lines (cleaning, pretreatment, primer/topcoat application, and thermal curing). Downstream, coated steel and aluminum feed roll formers and fabricators serving building products, appliances, transportation, and furniture, where specification and warranty requirements lock in qualified coating systems and pretreatment packages. Industry standards and test methods, including the EN 10169/EN 1396 and EN 13523 series in Europe and ASTM methods such as D3794, help support qualification and comparability across suppliers.

Because coil lines run continuously, the midstream is sensitive to energy and utilities availability, in addition to coating raw-material volatility. In March 2026, Indian coated-steel participants sought government intervention to address propane and industrial gas shortages tied to West Asia logistics disruptions, and at least one downstream coating unit (Enlight Metals, Pune) reported an extended stoppage due to propane unavailability, highlighting how fuel constraints can quickly translate into throughput losses. Strategic collaborations also steer technology direction, including partnerships between coating formulators and steel producers focused on decarbonization and faster-curing approaches, alongside investments in new or upgraded color-coating lines supported by equipment suppliers such as John Cockerill.

Competitive Landscape

The Coil Coatings market is fragmented. Supply security and technical service are decisive tender criteria. Major OEMs mandate on-site audits, accelerated weathering tests, and digital color formulation libraries. Smaller entrants without global field-service teams struggle to break specification locks. Nevertheless, white-space opportunities persist in PFAS-free fluoropolymers, high-recycled-content backers, and radiation-cure platforms that halve energy draw. Partnerships with line-equipment makers and chemical pretreatment specialists can unlock turnkey packages for emerging-market coaters eyeing compliance parity, reinforcing competitive moats for integrated suppliers inside the coil coatings market.

Coil Coatings Industry Leaders

Beckers Group

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Axalta Coating Systems, LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is compliance-ready and lower-footprint chemistries that help coil coaters and OEMs respond to tighter VOC and chemical controls without undermining durability warranties. Reformulation activity around PFAS-free pathways for premium exterior performance, alongside lead-free and chromate-free primer systems, aligns with evolving REACH restrictions and air-emissions limits. This supports demand for suppliers that can provide verified performance data, accelerated weathering packages, and audit-ready documentation for global OEM qualification.

Capacity localization and process productivity upgrades also present opportunities, particularly where fast lead times and regional supply security affect construction panels and appliances. In March 2026, Sherwin-Williams completed a major expansion at its Bowling Green, Kentucky coil coatings plant, increasing capacity by 60% versus 2025 levels and adding automation and larger-batch capability for SMP and polyester systems, reflecting ongoing investment in higher-throughput, regionally supplied products. In India, Jindal India Limited commissioned a new high-speed continuous color coating line in May 2026 as part of a USD 155 million capex program, adding processing flexibility across multiple coating types and strengthening the case for locally available coil-coating formulations, pretreatments, and technical service aligned to nearby steel and fabrication ecosystems.

Recent Industry Developments

- June 2026: Beckers Group, through its Berger-Becker Coatings joint venture, inaugurated a renewable resin manufacturing plant in Nagpur, India, with commercial production scheduled for Q3 2026 and initial capacity of 9,000 metric tons per year. The move brings more resin supply closer to key coil-coating and pre-painted metal demand centers and supports lower-footprint formulation pipelines tied to sustainability and compliance requirements.

- May 2026: Sherwin-Williams and Nippon Paint Group confirmed a joint proposal to acquire AkzoNobel, which was rejected by AkzoNobel's Board. Even without completion, the attempted deal underscored ongoing strategic pressure to broaden global coatings footprints, reinforcing competitive focus on scale, technology depth, and regional manufacturing access across coil and adjacent industrial coatings.

- September 2024: Beckers Group opened its FutureLab in Liverpool, United Kingdom, to accelerate development of next-generation coil coatings. By effectively doubling long-term development capacity, the facility supports faster iteration in sustainable chemistries and performance upgrades needed for demanding building-envelope and appliance specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The coil coatings market covers liquid coating systems applied on continuous, automated coil coating lines, where steel or aluminum coil or sheet is coated and then formed into finished, pre-painted parts sold to downstream manufacturers.

Scope exclusions: It does not include post-fabrication metal painting at job sites, or coatings not applied as part of a coil line process.

Segmentation Overview

- By Resin Type

- Polyester

- Polyvinylidene Fluoride (PVDF)

- Polyurethane (PU)

- Plastisols

- Other Resin Types

- By End-user Industry

- Building and Construction

- Industrial and Domestic Appliances

- Transportation

- Furniture

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base behind demand drivers and to set practical ranges for key model inputs. We referenced public sources such as UN Comtrade trade statistics, USGS and other national mineral and materials statistics, US Census Bureau construction and manufacturing indicators, Eurostat industrial production series, and standards and technical notes from groups such as ASTM and ISO.

Along with that, we reviewed company annual reports, investor presentations, association websites, and coverage in business press to track capacity changes, resin and pigment trends, and downstream end-use signals. For hard-to-find company-level financial splits and patent activity, paid subscriptions for company financials and patent databases were used to cross-check what could be validated from public disclosures. These desk research sources are illustrative, and additional references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was carried out through expert interviews and structured surveys with a mix of coating formulators, coil coaters, distributors, and downstream users from construction, appliances, and transportation. We included respondents across major consuming regions so the desk assumptions on resin mix, typical pricing movement, and end-use adoption could be tested, then adjusted when observed market behavior differed from the initial model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 46% |

| Mid tier: 60% | Functional/Unit leaders: 41% | EMEA: 36% |

| Smaller Players: 15% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build, where the demand pool is reconstructed from coated metal consumption in key end uses, and then filtered through coil coating penetration and typical coating usage on steel and aluminum coil. After this market shape is formed, we corroborate it using selective bottom-up checks such as sampled supplier revenue visibility, channel feedback on average selling price ranges, and volume-by-price sanity checks by resin type, so totals can be corrected where needed.

Inputs used in the model include building and construction activity (especially roofing and cladding), appliances production trends, transportation output, steel and aluminum coil availability, and observable shifts in resin preference such as polyester versus PVDF in premium exterior uses. Pricing assumptions are handled by tracking raw material direction (resins and key additives), mix movement across resin types, and currency timing for converting local values to USD. Forecasts rely mainly on scenario analysis, where baseline growth paths for construction and manufacturing are combined with expert-agreed adoption changes, and then stress-tested for upside and downside cases.

Where bottom-up points are not available for a country or a smaller end-use pocket, gaps are handled by using regional proxy ratios tied to industrial output and trade exposure, then validated through follow-up calls until assumptions sit within realistic ranges.

Data Validation & Update Cycle

Validation is done through triangulation across the demand build, supplier-side checks, and independent signals such as industrial production and trade flows for coated metal and related inputs. When outputs looked inconsistent, we traced the variance back to a small set of drivers, then rechecked those drivers and corrected inputs before final totals were locked.

Each estimate goes through multi-step analyst reviews where assumptions, conversion factors, and year-on-year movements are compared against expected market behavior. Reports are refreshed annually, with interim updates added when material events occur, such as sharp raw material swings or major capacity changes. Before delivery, a final pass is completed so the latest market movements are reflected in the final numbers clients receive.

Mordor Intelligence's Coil Coatings Market Estimate Compared With Other Published Estimates

Published market sizes for coil coatings can vary because firms do not always count the same coating scope, they may use different base years, and they often apply different price and currency timing when converting to USD. Even when the same end-use labels are used, the way steel versus aluminum coil applications are handled can shift the total.

A common gap driver is whether adjacent categories, like broader industrial metal coatings or post-fabrication painting, are included in the coil line coating total. Differences also come from how resin mix is treated, since PVDF-heavy assumptions tend to lift value, and from how quickly prices are expected to normalize after raw material changes. Finally, refresh cadence matters, because models that do not re-check recent construction and appliance output can hold an older growth path for too long.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.75 B (2026) | |

| Industry Publisher A | USD 5.80 B (2025) | This figure is higher mainly because it uses a wider segment frame that explicitly splits the market into product layers like primers and backing coats and may capture broader coating activity around coil applications, which can pull in revenue outside a strict coil-line-only count. |

| Global Publisher B | USD 5.86 B (2025) | This estimate follows a consumption-value approach and uses a faster near-term growth curve, which can raise totals if resale exclusions and end-use allocation are not aligned with coil coating line throughput and resin-mix realities in each region. |

The table shows that the spread is mostly explained by what is counted as coil-line coatings versus adjacent metal coating revenues, and by how pricing and growth are carried forward from the base year. By keeping the count tied to coil-applied coatings on steel and aluminum and rechecking resin mix and end-use signals before finalizing, the reported total stays more traceable to repeatable steps, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the Coil Coatings market in 2026?

The coil coatings market size stands at USD 3.75 billion in 2026.

What is the expected CAGR for coil-applied finishes through 2031?

Revenue is projected to advance at a 3.28% CAGR over 2026-2031.

Which resin dominates sales today?

Polyester formulations hold 66.84% share owing to cost efficiency and versatile performance.

Why is PVDF gaining momentum?

PVDF grows fastest at 3.63% CAGR because it meets long-term color-retention and cool-roof requirements in commercial façades.

Which region leads demand?

Asia-Pacific leads with 49.88% of global revenue thanks to its large appliance, automotive, and construction base.

Page last updated on: