Market Overview

| Study Period | 2021 - 2031 |

|---|---|

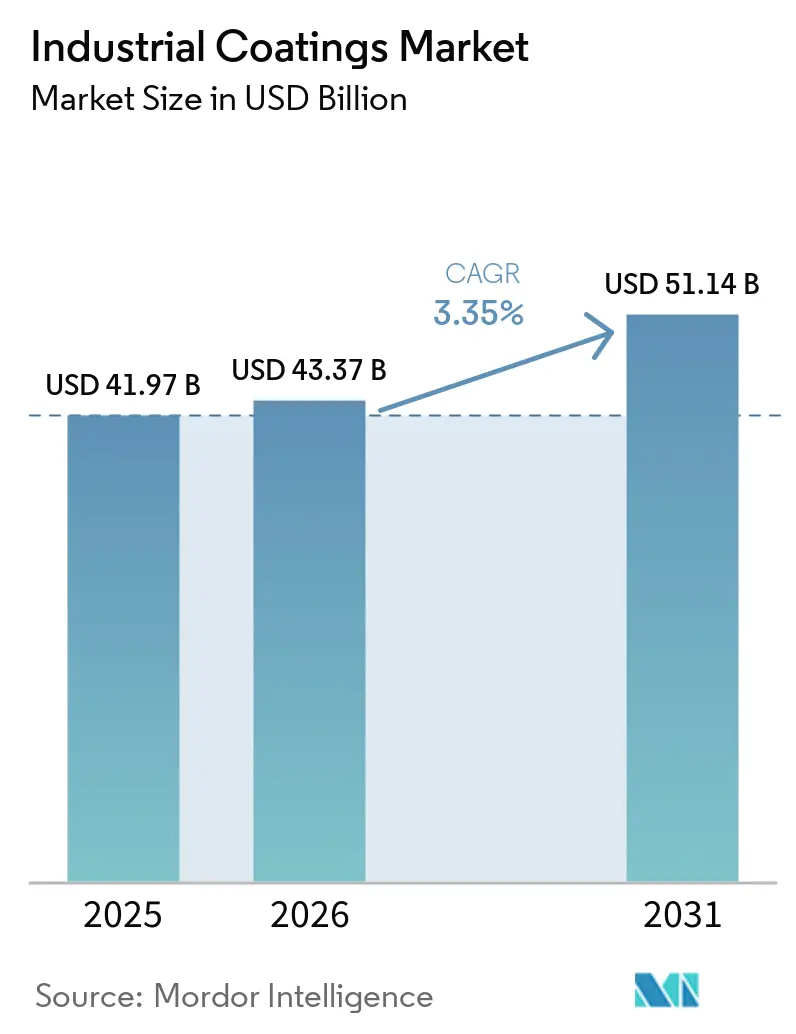

| Market Size (2026) | USD 43.37 Billion |

| Market Size (2031) | USD 51.14 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

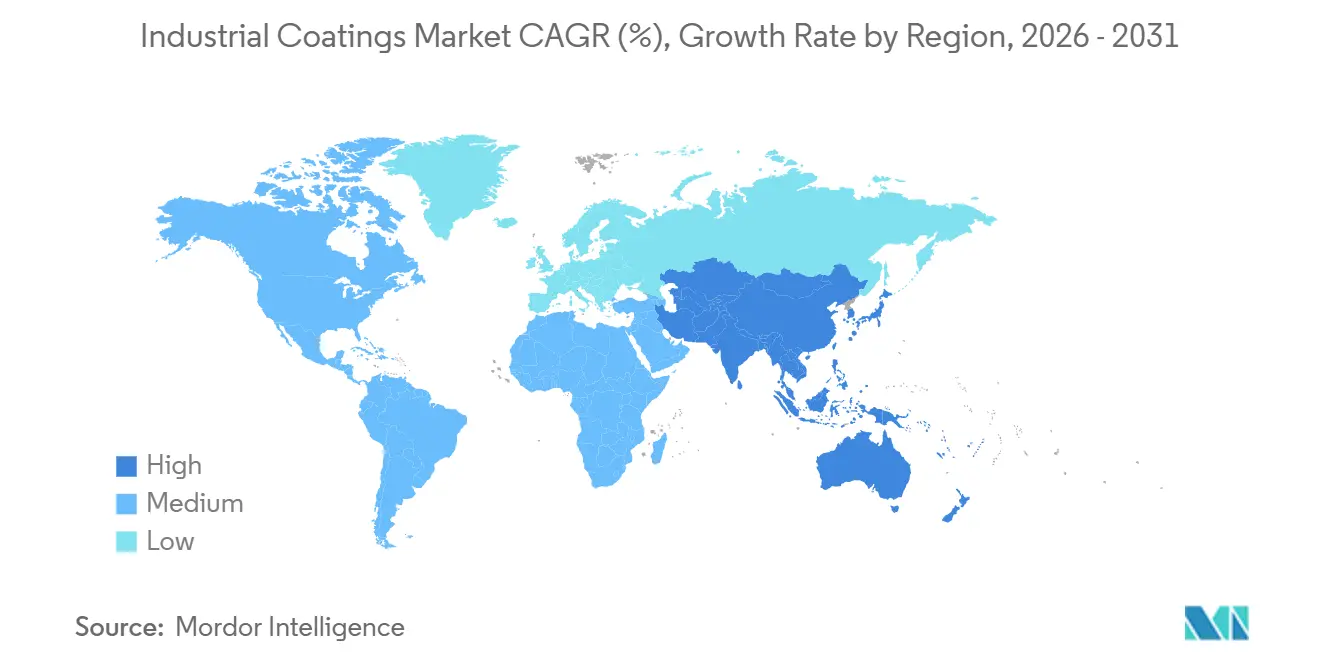

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

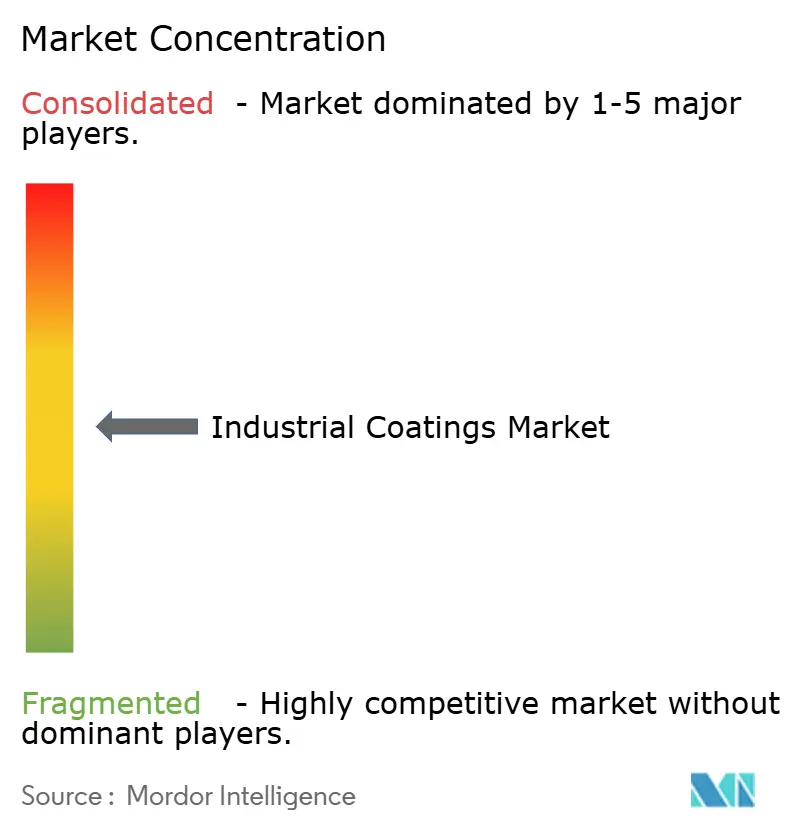

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Coatings Market Analysis by Mordor Intelligence

The Industrial Coatings Market size is expected to grow from USD 41.97 billion in 2025 to USD 43.37 billion in 2026 and is forecast to reach USD 51.14 billion by 2031 at a 3.35% CAGR over 2026-2031. This steady growth accompanies a marked pivot toward water-borne, powder, and ultraviolet-cured chemistries as regulators tighten volatile-organic-compound limits in North America, Europe, and parts of Asia. Epoxy resins retained the largest slice of demand in 2025, yet polyurethane systems are advancing at more than 5% per year as aerospace, wind-energy, and high-build infrastructure applications favor tougher, UV-stable films. Powder coatings continue to gain share in appliances and wheels because they deliver near-zero emissions and almost complete transfer efficiency, while ultraviolet-LED lines lower energy use by roughly 70% in automotive and composite plants. Asia-Pacific consolidated its position as the dominant volume hub, supplying more than half of global consumption and benefiting from sustained capital spending on bridges, petrochemical tanks, and factory build-outs.

Key Report Takeaways

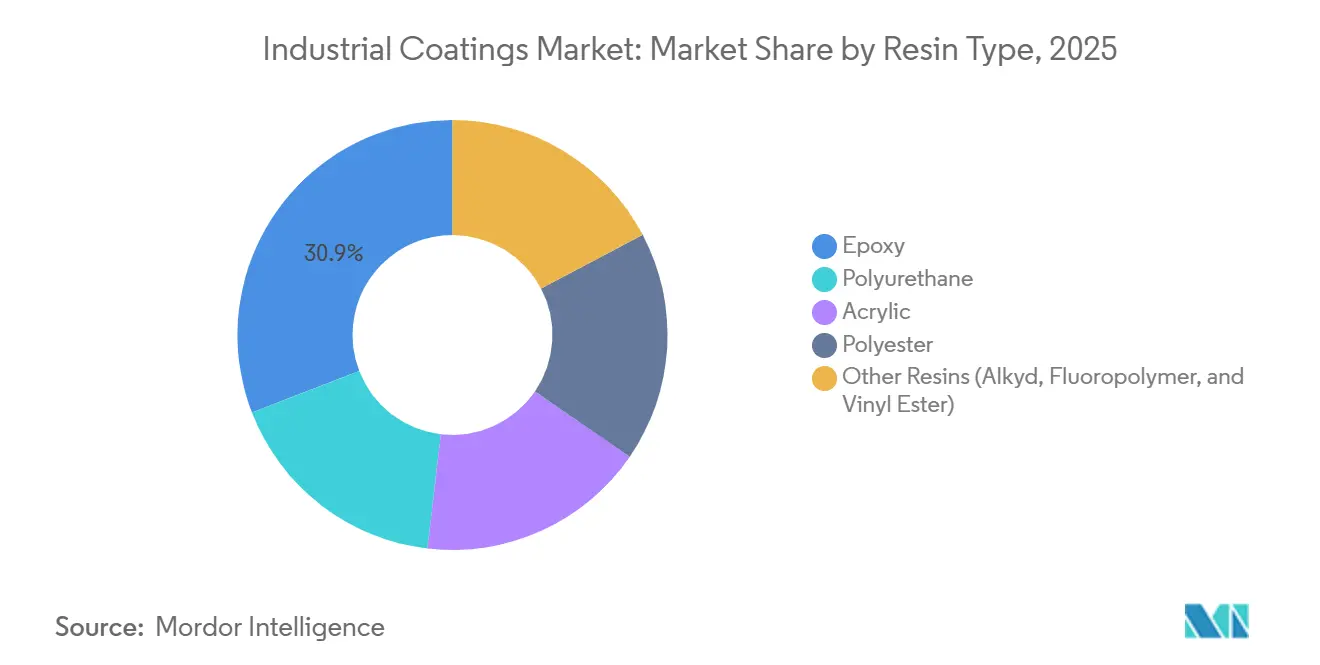

- By resin type, epoxy led with 30.85% of the industrial coatings market share in 2025, while polyurethane is projected to expand at a 5.08% CAGR through 2031.

- By technology, solvent-borne products still accounted for 36.91% of the industrial coatings market size in 2025, but water-borne coatings are registering the fastest adoption, growing at a 4.91% CAGR during the same period.

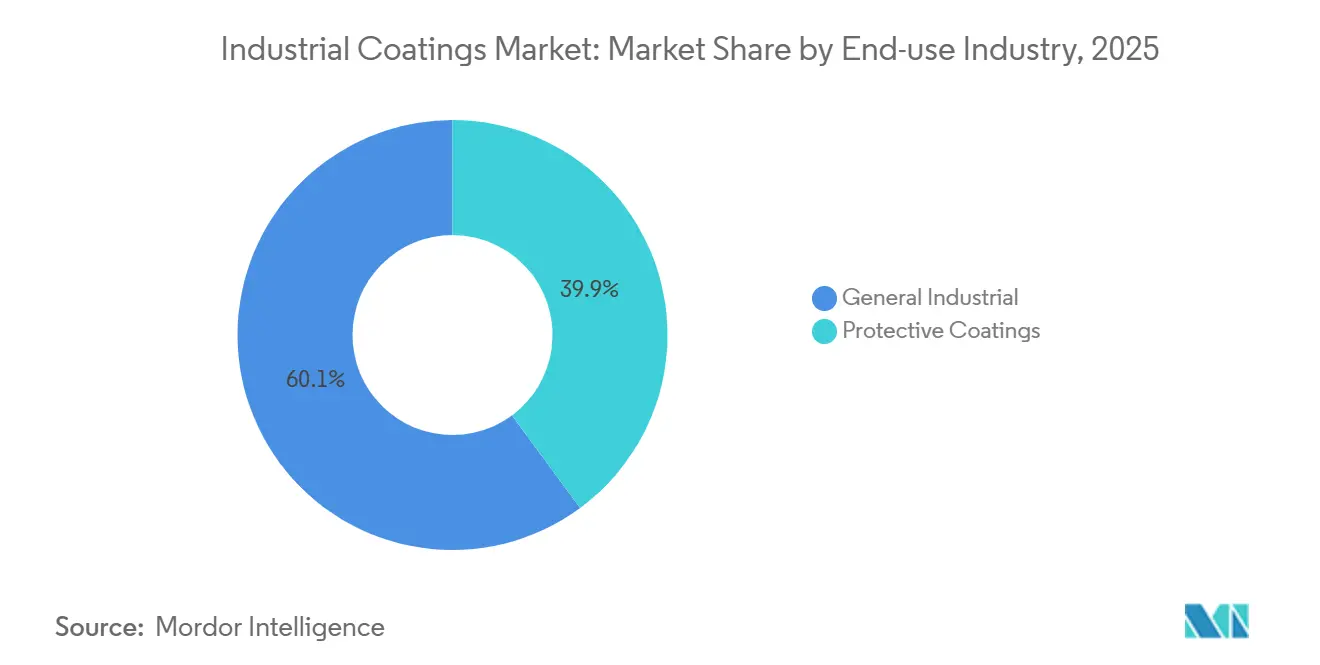

- By end-use industry, general industrial applications captured 60.12% revenue share of the industrial coatings market in 2025, and are forecast to grow at 4.12% CAGR to 2031.

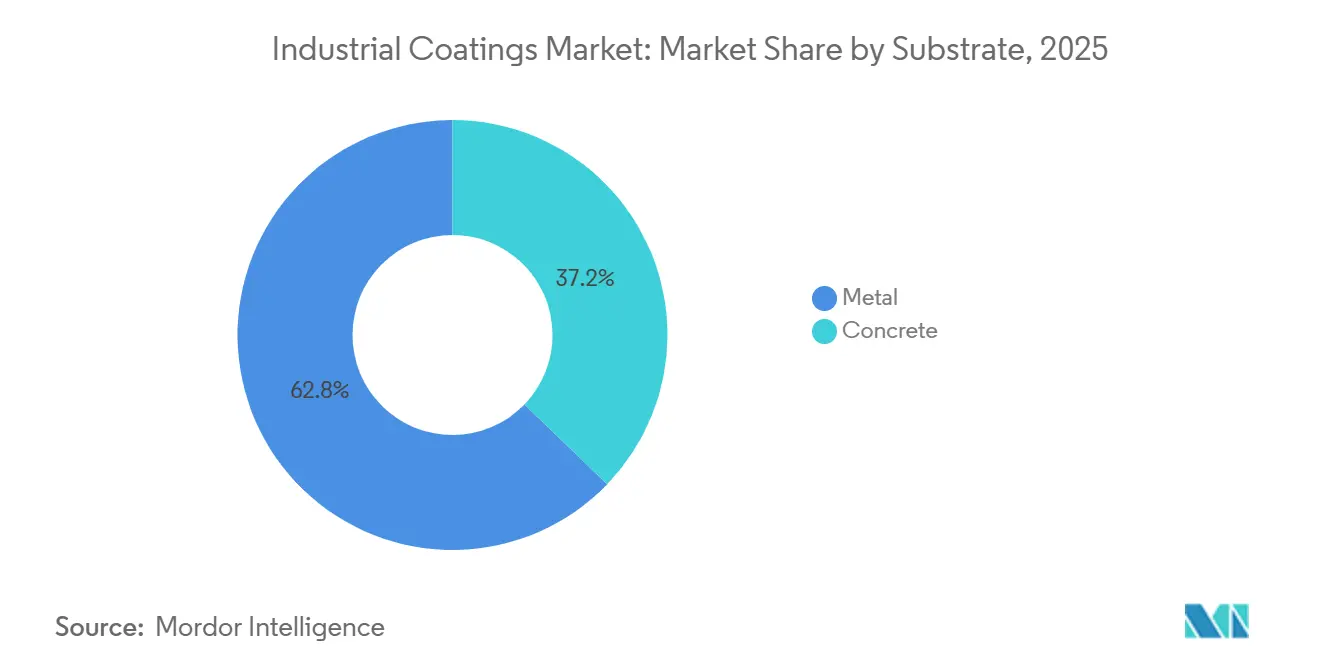

- By substrate, metal led with 62.78% of the industrial coatings market share in 2025, while concrete is projected to expand at a 4.60% CAGR through 2031.

- By region, Asia-Pacific commanded 51.16% of the industrial coatings market in 2025, and the region is projected to advance at a 4.35% CAGR between 2026 and 2031 as investments in infrastructure rehabilitation accelerate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protective-coatings spend on aging oil & gas assets | +0.8% | North Sea, Gulf of Mexico, Middle East | Long term (≥ 4 years) |

| Accelerating APAC industrial build-outs | +1.2% | China, India, Vietnam, Indonesia | Medium term (2-4 years) |

| Environmental mandates for low-VOC chemistries | +0.9% | U.S., EU, China, India | Medium term (2-4 years) |

| UV-LED instant-cure production lines | +0.5% | Germany, South Korea, Japan, Mexico | Short term (≤ 2 years) |

| Sensor-enabled predictive-maintenance films | +0.3% | U.S., EU pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Protective-Coatings Demand for Aging Oil and Gas Assets

Deferred upkeep left roughly 40% of offshore platforms in the North Sea and Gulf of Mexico running past their original corrosion-protection lifespans, triggering large-scale recoating programs. Shell dedicated USD 1.2 billion in 2025 to upgrade 15 U.K. platforms with three-coat glass-flake epoxies that stretch service intervals to 25 years[1]Shell plc, “Annual Report 2025,” shell.com. TotalEnergies allocated USD 800 million for West African subsea pipelines exposed to hydrogen sulfide and chloride attack. Middle-East petrochemical complexes are simultaneously lining storage tanks with high-build polyurethane to satisfy updated API 653 integrity provisions. This multi-billion-dollar backlog keeps the industrial coatings market on a stable upward track as asset owners now prioritize lifecycle economics over first-cost savings. Because the underlying infrastructure is capital-intensive and safety-critical, specification shifts are deliberate, extending revenue visibility for suppliers through the next decade.

Rapid APAC Industrial Expansion Fueling General-Industrial Volumes

China’s 2025 infrastructure stimulus of USD 140 billion funded high-speed rail, metro extensions, and large steel bridges across the Yangtze basin, each requiring multi-layer epoxy or polyurethane defenses. India’s production-linked incentive program secured USD 22 billion in fresh factory spending, with automated spray booths in Gujarat and Tamil Nadu alone consuming an estimated 180,000 metric tons of coatings. Vietnam has become a manufacturing relocation hotspot, where cleanroom electronics plants specify anti-static epoxy floors tested to IEC 61340. Indonesia’s nickel-smelter boom demands silicone films able to resist 600°C furnace conditions. Taken together, the region applies more kilograms of coating per USD of manufacturing value added than any other geography, illustrating a structural edge that lifts the industrial coatings market throughout the forecast horizon.

Environmental Mandates Accelerating Water-Borne and Powder Uptake

Revised US National Emission Standards in early 2025 lowered allowable VOCs in industrial maintenance coatings to 340 g/L, rendering traditional solvent alkyds uneconomic without vapor-recovery systems. California’s South Coast district tightened the bar to 250 g/L while demanding real-time emissions monitoring, spurring a wave of acrylic emulsion and powder investments by multinational suppliers. European makers slashed VOCs below 100 g/L by using renewable propylene-glycol substitutes, matching solvent-borne durability without overshooting cost targets. Because powder coatings emit zero VOCs, Axalta and AkzoNobel each commissioned fresh polyester lines in China and Poland, capturing surge orders in appliances and wheels. Smaller regional formulators either shift into toll manufacturing or exit altogether, pushing the industrial coatings market toward more consolidated, technology-driven players.

UV-LED Instant-Cure Lines Adopted by OEM Factories

More than 200 ultraviolet-LED curing systems were installed in Germany, South Korea, and Japan during 2025, displacing mercury vapor lamps and thermal ovens and trimming energy use by roughly 15 kWh per vehicle body[2]BMW Group, “Sustainability Report 2025,” bmwgroup.com. BMW’s Leipzig plant reported a 68% energy cut and 40% floor-space release after deploying LED clear-coat lines. Hyundai achieved sub-10-second cure times at Ulsan, permitting single-shift operation that shortens takt time and slashes utility bills. Aerospace contractors validated UV-curable polyurethane primers for composite fuselage parts, reducing cycle time from four hours to 90 seconds. LED arrays last over 20,000 hours, eliminating frequent bulb changes and toxic-waste fees, making the switch financially compelling even for mid-sized Mexican and Thai contract shops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and PFAS curbs on solvent systems | -0.6% | U.S., EU, China | Medium term (2-4 years) |

| Titanium-dioxide and epoxy price swings | -0.9% | Global, import-dependent economies | Short term (≤ 2 years) |

| Short supply of micronized aluminum pigments | -0.2% | U.S., EU, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening VOC and PFAS Regulations on Solvent-Borne Systems

A draft European Union restriction seeks to phase out per- and polyfluoroalkyl substances in fluoropolymer films used in chemical reactors and semiconductor tools, pushing formulators toward less proven siloxane or ceramic routes. California extended its 250 g/L VOC ceiling to industrial maintenance categories, forcing fast-dry alkyds either into costly reformulations or retirement. Compliance adds USD 0.30-0.50 per liter in R&D and plant retooling, squeezing mid-tier suppliers without global scale. China’s environment ministry signaled a plan to harmonize VOC limits with EU norms by 2027, potentially sidelining one-quarter of domestic solvent capacity. Collectively, these curbs temper overall industrial coatings market growth during the transition, even as they accelerate uptake of low-emission chemistries.

Titanium-Dioxide and Epoxy-Resin Price Volatility

Titanium-dioxide spot quotes jumped above USD 3,300 per metric ton in late 2025 after hydropower shortages forced idling of Sichuan chloride-process capacity. Because acrylic and polyester films rely on 20-30% TiO₂ for opacity and UV shield, the cost spike pinched margins for coatings sold into cost-sensitive construction and refinish channels. Epoxy-resin prices rose in parallel with bisphenol-A feedstock, which gained 22% year-on-year amid refinery downtime in the US Gulf Coast and Northeast Asia. Protective-coatings suppliers with raw-material index clauses saw 200-300 basis-point margin erosion, while small regional players without hedges slipped into negative cash flow. Although price pressure eased in early 2026, volatility keeps credit risk elevated and could delay capex decisions in the industrial coatings industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Systems Accelerate While Epoxy Retains Core Volume

Epoxy, despite sliding marginally in high-growth niches, still accounted for 30.85% of the industrial coatings market size in 2025, supported by marine, pipeline, and heavy-duty structural jobs that require tenacious adhesion on blasted steel. Acrylic emulsions built incremental share in refinish and light-industrial tasks because they comply with California’s 250 g/L VOC ceiling straight from the drum. Polyester resins, largely in powder form, stayed essential to appliance shells and office furniture, a segment now capturing zero-emission credits in Europe. Hybrid formulations blending epoxy primers with polyurethane topcoats continue to rise because they marry bond strength with weather-fast gloss. Polyurethane demand climbed at a 5.08% CAGR between 2026 and 2031 as aerospace, wind-turbine, and high-durability infrastructure owners specified two-component films for their superior flex-crack resistance and UV holdout.

Suppliers are widening castor oil or palm kernel polyol content to raise renewable carbon share while maintaining mechanical stability. Fluoropolymer volumes flattened as pending PFAS bans and customer hesitancy slowed project validation. Vinyl ester, alkyd, and novolac chemistries remained confined to niche corrosion or fast-drying roles. Altogether, resin diversification both cushions raw-material shocks and broadens the addressable industrial coatings market without sacrificing core epoxy reliability.

By Technology: Water-Borne and Powder Alternatives Gain Traction

Solvent-borne products captured 36.91% of 2025 revenue; their trajectory tilts down as protective-coatings formulations prove water-borne options can now survive splash-zone immersion and 120°C cycling. Powder coatings grew briskly in wheels, radiators, shelving, and small tractors, buoyed by 97-99% transfer efficiency and elimination of hazardous-air-pollutant permitting. Ultraviolet-curable lines progressed from boutique to mainstream once LED arrays reduced heat load and lamp changeouts. Collectively, these shifts push the industrial coatings market toward lower emissions, shorter cure times, and reduced energy footprints while preserving throughput. Water-borne chemistries advanced 4.91% annually through 2031, lifted by North American and European plant upgrades that swapped solvent alkyds for acrylic dispersions under new VOC laws.

Suppliers are layering digital color-match and near-infrared cure additives into their offerings, letting job shops hit exact shades with fewer coats. Electro-deposition remains dominant for automotive bodies, yet next-gen cationic baths now include bio-based co-solvents and F-free surfactants. Thermal-spray metalizing and high-solid novolac epoxies keep niche footholds where 200-μm films in one pass pay for themselves in offshore upkeep costs. As regulatory scrutiny heightens, the technology mix will continue to tip toward water and powder, reinforcing sustainability narratives that echo across the broader industrial coatings market.

By End-Use Industry: General-Industrial Dominates, Protective Segment Ramps Up

General-industrial lines, encompassing machinery, fabricated metal, consumer electronics, and white goods, held 60.12% revenue in 2025 thanks to continuous appliance runs, electronics casings, and agricultural equipment demand. The segment is projected to move at a 4.12% CAGR through 2031 as automation and urbanization fuel durable-goods consumption. Protective coatings requirements for oil, gas, mining, and power assets surged in 2025 when operators earmarked more than USD 2 billion for platform, pipeline, and tank rehabilitation. Midstream energy players increasingly specify glass-flake epoxies and high-build polyurethanes capable of withstanding hydrogen sulfide and 120°C operating temperatures, a practice that expands long-cycle revenue visibility.

Within power, coal and combined-cycle stations in India and Southeast Asia adopted ceramic-filled films to double tube life in flue-gas systems, cutting outages and emissions simultaneously. Mining groups in Australia and Chile lined sag mills and tailings ponds with abrasion-resistant novolacs, containing aggressive slurries and acidic leachates. Infrastructure owners in the Asia-Pacific region deployed ISO 12944 C5-M systems to extend bridge cycles past 15 years even in salt-spray zones. This composite end-use mosaic keeps the industrial coatings market broad and resilient against single-sector slowdowns.

By Substrate: Metal Dominates, Concrete Rising Fast

Metal remained the anchor substrate with a 62.78% share in 2025, reflecting the ubiquity of steel and aluminum in vehicles, aircraft, ships, and capital equipment. Blast-cleaned Sa 2.5 steel paired with zinc-rich primers under epoxy mid-coats and polyurethane topcoats remains the gold standard for marine and petrochemical shells, keeping recurrence business intact. Concrete, however, grew 4.60% per year as desalination projects, wastewater plants, and data centers mandated linings to combat chloride ingress, carbonation, and electrostatic discharge. The Taweelah desalination plant in the United Arab Emirates specified epoxy-modified cementitious layers for tanks facing daily 15-45°C thermal swings.

India’s highway authority ordered acrylic sealers and aliphatic polyurethane tops for 12,000 lane-km of new concrete pavement to deter coastal chloride penetration. Data centers in North America applied anti-static epoxies, satisfying IEC 61340 while tolerating forklift loads and chilled-floor shock. Formulators now market moisture-tolerant primers curing on substrates with up to 8% water content, shaving two-week vapor barrier waits on fast-track builds. As megaprojects worldwide pour more concrete than steel, the industrial coatings market for cementitious surfaces promises above-average expansion.

Geography Analysis

Asia-Pacific dominated the industrial coatings market in 2025 with a 51.16% share and is set to pace forward at a 4.35% CAGR as China, India, Vietnam, and Indonesia underpin structural spending on transport, energy, and manufacturing. China's ambitious 2025 stimulus is channeling funds into high-speed rail spines and new bridges over the Yangtze. These projects are projected to consume significant amounts of epoxy and polyurethane annually. Meanwhile, India's foreign direct investment (FDI) initiative, bolstered by an incentive program, has accelerated the installation of water-borne lines in Gujarat and Tamil Nadu. This advancement has notably reduced both the cycle time and emissions associated with automotive shells and consumer appliances.

In North America and Europe, growth was modest, constrained by mature stock levels and stringent environmental regulations. The U.S. set a VOC limit for industrial maintenance films, leading to increased investments in acrylic-emulsion R&D and heightened capital needs for solvent vapor recovery. In 2025, Germany introduced UV-LED paint lines, achieving energy savings at BMW and Volkswagen facilities. However, the EU's proposal to ban PFAS has cast a shadow of uncertainty over high-performance fluoropolymer sectors, causing delays in some chemical processing rollouts.

Outside of Asia, emerging regions in South America, the Middle East, and Africa present the most significant growth opportunities. Brazil has initiated a tender for highway resurfacing, utilizing acrylic sealers and polyurethane tops tailored for the country's humid tropical cycles. In Saudi Arabia, a water initiative has specified epoxy-modified cementitious linings for concrete reservoirs, addressing chloride loads. South Africa's Transnet has allocated funds for refurbishing coastal rail assets, employing ISO 12944 C5-M epoxies. Concurrently, Nigeria's Dangote refinery utilized protective films during its 2024-25 plant commissioning. Collectively, these endeavors not only diversify revenue streams but also shield the industrial coatings market from regional disruptions.

Competitive Landscape

The Industrial Coatings market is moderately concentrated. Regional challengers in India, China, and Brazil win share by co-locating plants near OEM clusters, shortening delivery windows, and tailoring formulations to local regulations. Asian Paints added a USD 200 million Gujarat plant in 2025 to target water-borne auto and appliance lines, while Hempel and Jotun secure offshore wind and pipeline jobs through marine lineage expertise. Innovation pipelines are thickening around self-healing, antimicrobial, and bio-based resins. These advances ensure the industrial coatings industry will keep evolving alongside sustainability and digital-integration imperatives.

Industrial Coatings Industry Leaders

AkzoNobel N.V.

Axalta Coating Systems

PPG Industries, Inc.

The Sherwin-Williams Company

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: At its Asia-Pacific Innovation Center in Shanghai, Covestro unveiled a suite of locally developed coatings tailored for diverse industries across the Asia Pacific. This newly introduced coatings portfolio is designed for pivotal applications spanning mobility, home and living, infrastructure, renewable energy, and the realms of printing and packaging.

- June 2025: At the AIA Conference on Architecture and Design 2025, PPG presented its architectural metal coatings, designed to deliver superior performance in weathering, design, and durability. This innovation is expected to strengthen PPG's position in the industrial coatings market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial coatings market as factory-made liquid, powder, or UV-cured films deposited on metal or concrete parts in non-architectural settings to protect against corrosion, chemicals, or abrasion while adding functional or safety value across original equipment lines and maintenance yards worldwide.

Scope Exclusions: Decorative wall paints, DIY aerosols, and upstream resin feedstocks are not covered.

Segmentation Overview

- By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Polyester

- Other Resins (Alkyd, Fluoropolymer, and Vinyl Ester)

- By Technology

- Solvent-borne

- Water-borne

- Powder

- UV Technology

- By End-use Industry

- General Industrial

- Protective Coatings

- Oil and Gas

- Mining

- Power

- Infrastructure

- Other Protective Coatings

- By Substrate

- Metal

- Concrete

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Nordics

- Rest of Europe

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Interviews with formulators, Asian OEM buyers, North American distributors, and environment health regulators grounded our assumptions on applied film thickness, workable margins, and the pace at which powder lines displace solvent systems.

Desk Research

We mapped HS-3208/3209 trade flows in UN Comtrade and Eurostat, aligned volumes with output indices from the US Federal Reserve and China's National Bureau of Statistics, and trended resin costs in regional price trackers. Bulletins from the Japan Paint Manufacturers Association, VOC registers issued by ECHA, and patent abstracts mined through Questel clarified technology timelines. Company filings pulled via D & B Hoovers and daily news captured on Dow Jones Factiva flagged capacity moves and selling price shifts. These references are illustrative, not exhaustive.

Market-Sizing & Forecasting

Mordor analysts start with a top-down consumption build: production plus net trade converts to regional volumes that are multiplied by current average selling prices, then sanity checked through selective supplier roll-ups. Key variables in our multivariate regression include global PMI, passenger car assemblies, infrastructure CAPEX, resin to crude spreads, VOC compliance dates, and powder coating penetration. Where job shops are under represented, sales are prorated using labor census ratios before final triangulation.

Data Validation & Update Cycle

Outputs face variance tests against historical bands, peer ratios, and live press signals; anomalies trigger senior review. Reports refresh annually, and large capacity additions or major regulatory shifts prompt an interim update so clients always receive the latest view.

Why Mordor's Industrial Coatings Baseline Earns Trust

Published values often diverge because providers tweak scope, price anchors, or refresh cadence.

Mordor excludes architectural liters, applies metal only trade codes, updates prices quarterly, and converts currencies with IMF averages, yielding a tight and repeatable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 41.97 B (2025) | Mordor Intelligence | - |

| USD 112.04 B (2024) | Global Consultancy A | Decorative paint bundled; single year ASP |

| USD 93.63 B (2024) | Industry Analysis B | Solvents counted; shipment value gross |

| USD 149.72 B (2023) | Trade Journal C | Mixed base currencies; OEM tools merged |

This comparison shows that the focused, regularly refreshed scope adopted by Mordor Intelligence gives decision makers a balanced baseline they can replicate, question, and trust.

Key Questions Answered in the Report

How large is the industrial coatings market in 2026?

The industrial coatings market size stood at USD 43.37 billion in 2026 and is forecast to reach USD 51.14 billion by 2031.

Which resin type is growing fastest in industrial coatings?

Polyurethane systems are expanding at a 5.08% CAGR through 2031 because aerospace, wind-energy, and infrastructure owners prioritize their UV and impact durability.

What region consumes the most industrial coatings?

Asia-Pacific accounts for just over 51% of global revenue share thanks to heavy infrastructure and manufacturing investments across China, India, Vietnam, and Indonesia.

How are environmental rules shaping product demand?

Stricter VOC and emerging PFAS restrictions are shifting share toward water-borne, powder, and UV-cured chemistries that emit fewer hazardous compounds.

Which technology segment is gaining share fastest?

Water-borne and powder coatings jointly outpace solvent varieties, supported by zero- or low-emission profiles and rising regulatory pressure.

Page last updated on: