Superhydrophobic Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

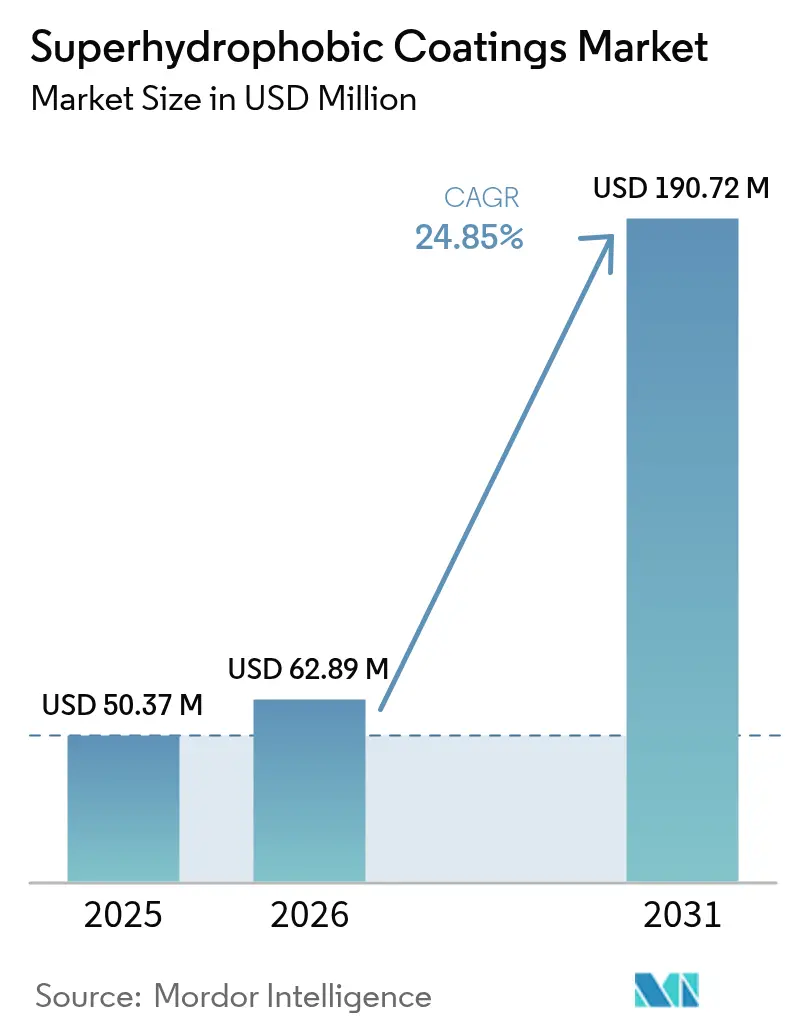

| Market Size (2026) | USD 62.89 Million |

| Market Size (2031) | USD 190.72 Million |

| Growth Rate (2026 - 2031) | 24.85% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Superhydrophobic Coatings Market Analysis by Mordor Intelligence

The Superhydrophobic Coatings Market size is expected to grow from USD 50.37 million in 2025 to USD 62.89 million in 2026 and is forecast to reach USD 190.72 million by 2031 at 24.85% CAGR over 2026-2031. Automotive-led modernization of electric vehicle (EV) battery packs, tightening global restrictions on fluorinated chemistries, and premium applications in augmented-reality head-up displays continue to keep demand momentum high. Manufacturers pursue functional integration, blending anti-wetting, corrosion resistance, and self-cleaning attributes to simplify coating stacks and lower the total cost of ownership. Precision spray-plasma deposition lines, though capital-intensive, deliver the coating uniformity and nanostructured control needed for large-scale deployments. Investment flows favor North America, where automakers combine lifetime paint warranties with aggressive EV rollouts, while European players race to commercialize PFAS-free silica platforms before looming REACH deadlines. Competitive intensity centers on patent portfolios covering PFAS-free nanoparticles and low-temperature plasma processing, elevating intellectual property (IP) as a strategic barrier to entry.

Key Report Takeaways

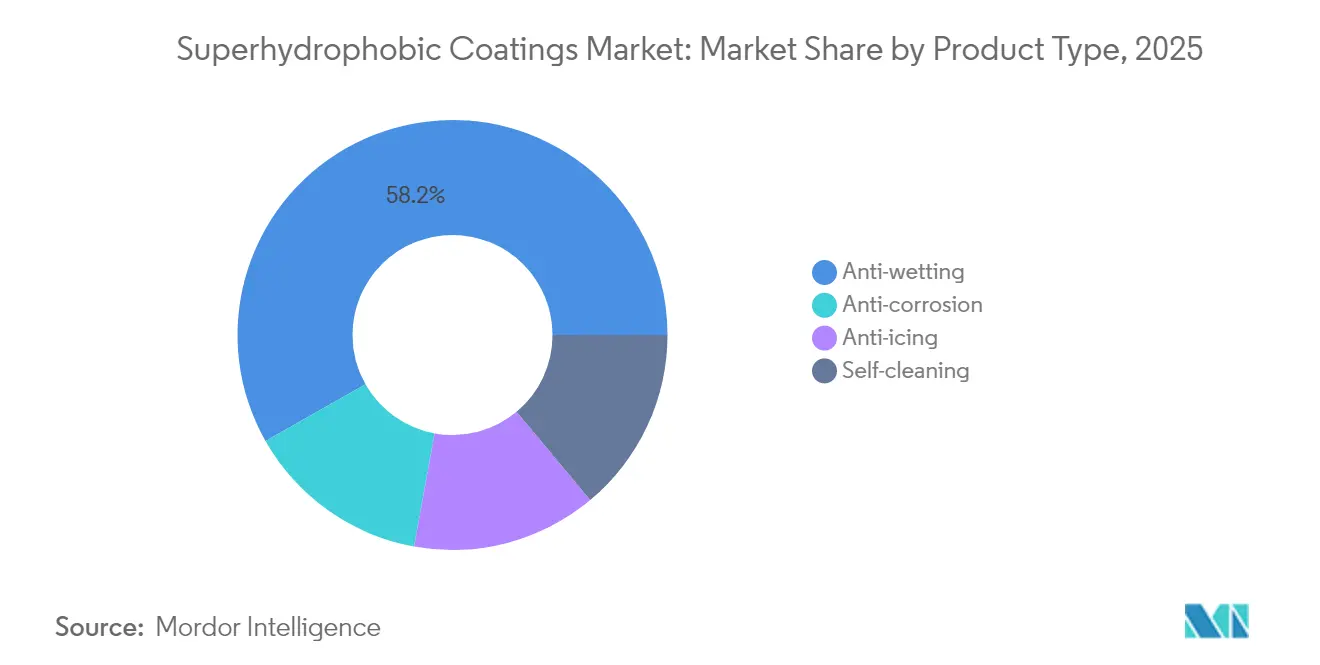

- By product type, anti-wetting captured 58.21% of the superhydrophobic coating market share in 2025 and is projected to expand at a 25.95% CAGR through 2031.

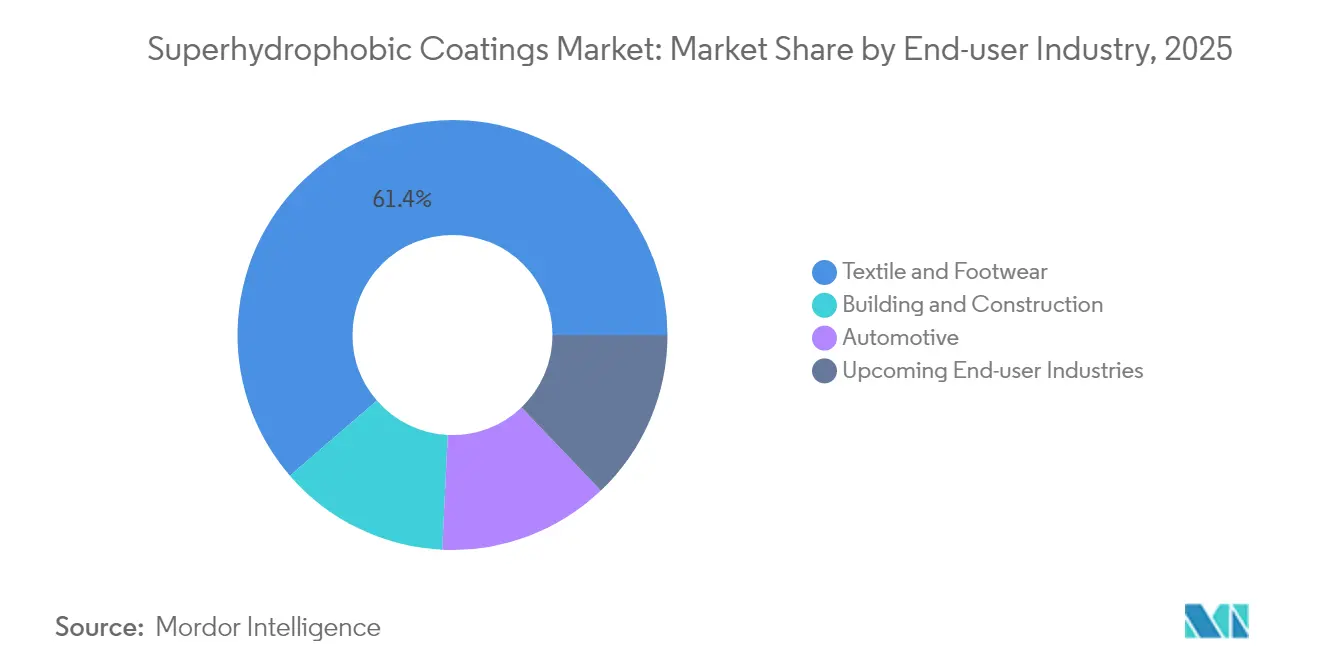

- By end-user industry, textile and footwear accounted for a 61.35% share of the superhydrophobic coating market size in 2025. Upcoming end-user industries are projected to advance at a 25.1% CAGR through 2031.

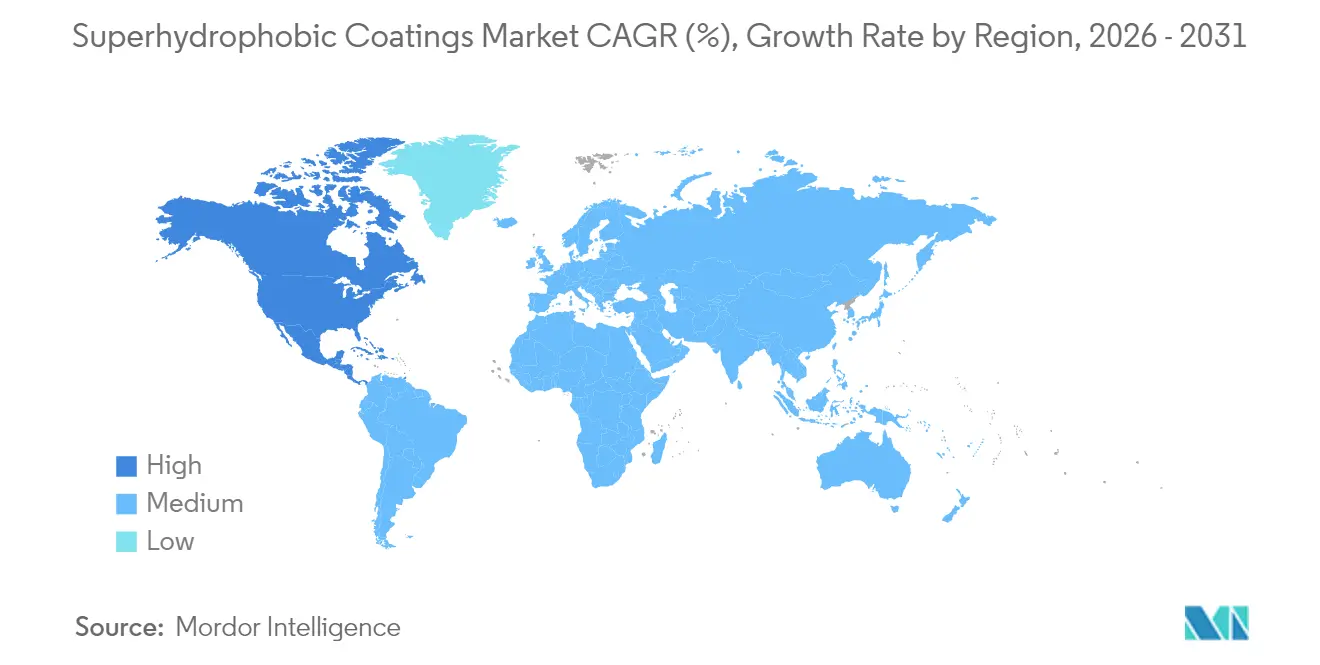

- By geography, North America accounted for 62.60% of the revenue share in 2025 and is projected to grow at a 37.85% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Superhydrophobic Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for corrosion-resistant coatings in EV battery packs | +3.8% | Global, strongest in APAC and North America | Medium term (2-4 years) |

| Rapid replacement of fluorinated chemistries by PFAS-free nano-silica systems | +3.1% | Europe and North America expanding to APAC | Short term (≤ 2 years) |

| Growth of transparent, self-cleaning glass coatings for AR-HUDs | +2.0% | North America and EU | Long term (≥ 4 years) |

| Automotive OEM push for lifetime paint-protection warranties | +2.5% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Standardization of ISO 21207 multi-cycle corrosion test in marine sector | +1.8% | Global, primary in Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Corrosion-Resistant Coatings in EV Battery Packs

EV battery manufacturers integrate nano-structured barriers that lower moisture-related failures, leveraging spray-plasma lines at Tesla and BYD facilities. Suppliers tailor formulations that withstand aggressive thermal cycling and electrochemical stress typical of pouch and cylindrical cell designs. The superhydrophobic coating market benefits from this shift as battery makers lock in long-term supply contracts, prompting coating firms to build dedicated automotive-grade capacity. Growth accelerates as global EV assembly volumes grow annually, reinforcing the scaling advantages of PFAS-free chemistries.

Rapid Replacement of Fluorinated Chemistries by PFAS-Free Nano-Silica Systems

EU REACH proposals targeting C6 fluoropolymers accelerate industry migration to silica-based platforms capable of achieving water contact angles of 150 ° or greater without fluorine[1]European Chemicals Agency, “PFAS Restrictions Under REACH Regulation,” echa.europa.eu. Equipment recalibration for silica particle dispersion incurs near-term expenses, but volume scaling is expected to narrow cost premiums by 2026. Patents related to particle functionalization and low-temperature curing underscore IP’s strategic importance across the superhydrophobic coating market.

Growth of Transparent, Self-Cleaning Glass Coatings for Augmented-Reality HUDs

Premium automakers, including Mercedes-Benz and BMW, utilize transparent nanocoatings that prevent windshields from forming water spots without compromising optical clarity[2]S. Patel, “AR-HUD Coating Breakthrough,” Automotive Engineering International, sae.org . Surface roughness tuning maintains transmission above 95% while sustaining contact angles of 140° or greater, thereby resolving a long-standing performance trade-off. Tight tolerances demand clean-room deposition and in-line spectrophotometry, driving high margins for qualified suppliers. Although unit volumes remain modest, revenue per square meter is three to four times that of conventional anti-wetting coatings, adding leverage to the superhydrophobic coating market size.

Automotive OEM Push for Lifetime Paint-Protection Warranties

Ford extended paint guarantees, mandating coatings that survive accelerated weathering cycles. Superhydrophobic layers serve as sacrificial shields against UV radiation, road salt, and micro-abrasion, thereby reducing warranty claims. OEM bid specifications increasingly call for self-healing matrices that restore hydrophobicity after scratches, prompting resin suppliers to integrate dynamic polymer networks. The shift to high-volume demand reinforces North America’s leadership in the superhydrophobic coating market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of precision spray-plasma lines for mass production | -1.5% | Global, strongest in emerging markets | Short term (≤ 2 years) |

| Pending EU REACH restriction on C6 fluoropolymers increases reformulation risk | -1.0% | Europe, secondary global impact | Medium term (2-4 years) |

| Abrasion-induced performance decay on textile fibers over 50 wash cycles | -1.3% | Global, highest in Asia-Pacific textile hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex of Precision Spray-Plasma Lines for Mass Production

The high cost of plasma units limits capacity expansion for small firms. Uniform coating of large substrates hinges on precise control of gas flow, power density, and substrate temperature, demanding specialized engineers. Alternate sol-gel routes reduce capital needs but sacrifice abrasion resistance, constraining penetration in heavy-duty segments. Consolidation favors incumbents who can amortize equipment across high-volume contracts, thereby sustaining moderate fragmentation in the superhydrophobic coating market.

Pending EU REACH Restriction on C6 Fluoropolymers Increases Reformulation Risk

Draft restrictions inject regulatory uncertainty, slowing capital deployment and delaying customer qualification. Fluoropolymer suppliers curtail output, inducing price volatility that hits formulators reliant on legacy chemistries. Diversified players hedge with silica and bio-based platforms, but single-chemistry firms face margin compression as they rush to replicate performance benchmarks under compressed timelines. The transition reshapes competitive dynamics, advantaging technology owners with wide chemistry toolkits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Anti-Wetting Dominance Across Diverse Applications

The anti-wetting segment held a 58.21% market share in the superhydrophobic coating market in 2025 and is forecasted to deliver the fastest 25.95% CAGR from 2026 to 2031. The lead traces to versatile, silica- and fluorine-free chemistries that span automotive, textile, and architectural domains. Self-cleaning variants capture architectural glass jobs in high-rise façades where maintenance‐free optics lower total building costs. Anti-corrosion subtypes serve oil platforms and chemical tanks, trading higher solids content for extreme chemical resistance. Anti-icing blends stand out in the aerospace industry, where certification costs justify premium pricing.

Convergence blurs historic boundaries as formulators embed multi-functionality within single coats that resist water, salt, and fouling. Plasma-assisted grafting permits nano-scaled roughness without bulk fluorine, easing future compliance. As test protocols evolve, anti-wetting suppliers integrate abrasion modifiers that preserve contact angles of 130° or greater under rotary taber tests, thereby extending service life. Advanced polymer cross-linking and nano-particle dispersion unlock performance synergies that expand the superhydrophobic coating market size across all product categories.

By End-User Industry: Textile Leadership Faces Emerging Competition

Textile and footwear applications represented 61.35% of the superhydrophobic coating market size in 2025. Water-repellent outerwear and stain-proof fashion goods dominate volume. Upcoming End-user Industries collectively clock a 25.1% CAGR, outpacing traditional segments. EV battery enclosures and premium automotive exteriors enhance the automotive industry’s contribution, while wind turbines utilize ice-shedding surfaces to increase winter capacity factors. Electronics OEMs request splash-proof smartphone casings that rely on nano-thin coatings invisible to the end user.

Textile durability remains the primary hurdle, as hydrophobic treatment often decays after frequent laundering. Research focuses on covalent grafting and polymer encapsulation to achieve more than 100 wash cycles without requiring surface retreatment. Upcoming medical and electronics niches, although lower in tonnage, achieve up to six times higher price points, thereby cushioning margins. Regulatory certifications, including ISO 10993 for biocompatibility and IPC surface cleanliness standards, lengthen product introduction cycles but secure longer-term volume stability for qualified vendors in the superhydrophobic coating market.

Geography Analysis

North America accounted for 62.60% of the superhydrophobic coating market share in 2025 and is projected to advance at a 37.85% CAGR from 2026 to 2031. The United States drives uptake through Tesla’s battery pack coating deployments and Ford’s paint protection guarantees. Canada enhances growth with anti-icing solutions for regional jets and wind turbines that operate in severe icing conditions, while Mexico’s vehicle assembly lines specify cost-efficient, PFAS-free nano-silica blends compatible with U.S. OEM standards.

Asia-Pacific registers robust gains in textile production in Vietnam and Bangladesh, plus accelerating EV assembly in India and Thailand. China’s battery gigafactories utilize line-integrated spray-plasma systems, generating high-volume orders that expand the market size for superhydrophobic coatings. Japan and South Korea supply precision plasma equipment and specialty chemicals, reinforcing intra-regional value chains. Electronics brands in Seoul and Tokyo are integrating splash-proof coatings into consumer devices, which boosts average selling prices.

Europe maintains steady growth despite REACH headwinds, with German premium automakers leading the way in PFAS-free technology pilots. The United Kingdom’s aerospace cluster specifies anti-icing coatings for next-generation narrow-body aircraft, while France’s couture houses deploy hydrophobic treatments on luxury textiles to elevate garment longevity. Italy’s architecture firms are adopting self-cleaning glass façades, and Spain is channeling renewable energy subsidies toward blade protection. ISO 21207 marine standards drive early adoption across North Sea shipyards, ensuring durable corrosion protection in harsh saltwater environments.

South America, the Middle-East, and Africa represent emerging demand nodes. Brazil’s offshore drillships require anti-corrosion barriers, and Saudi Arabia’s giga-projects order hydrophobic glass panels that slash cleaning costs across desert climates. Currency swings and tariff policies shape procurement, underscoring the need for localized production partnerships. The competitive field remains dynamic as suppliers balance cost lines against fluctuating exchange rates while scaling PFAS-free chemistries.

Competitive Landscape

The superhydrophobic coating market remains moderately fragmented. Specialty firms such as exploit intellectual property around nanometer-scale surface modification, focusing on electronics and medical device niches where conformal coverage is critical. Vertical integration trends surfaced, with coating vendors acquiring plasma equipment manufacturers to secure process know-how and after-sales revenue. Strategic alliances between chemical formulators and EV battery OEMs lock in volume commitments and accelerate formulation cycles. Startups targeting bio-based chitosan and rosin platforms attract sustainability-focused investors and license their technologies to large chemical houses for global rollout. Equipment suppliers bundle analytics software that tunes plasma parameters in real time, providing process guarantees that reduce scrap rates. As PFAS restrictions tighten, incumbents expedite the retirement of legacy fluorinated lines, freeing capital for PFAS-free scaling and positioning the industry for a decisive shift toward silica and bio-derived solutions within the forecast horizon.

Superhydrophobic Coatings Industry Leaders

UltraTech International Inc.

NEI Corporation

P2i Ltd

Aculon

Nasiol Nano Coating

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Researchers have unveiled a cotton fabric, treated with a fully bio-based, superhydrophobic coating. This innovative technology, which harnesses rosin acid and chitosan nanoparticles, ensures effective oil-water separation without the use of fluorinated compounds, while also boasting durability in challenging conditions.

- February 2025: Researchers have unveiled a PFAS-free superhydrophobic chitosan coating that boasts remarkable water resistance, thereby avoiding the use of harmful chemicals, as evidenced by its application. Analysis through contact angle measurements and drop impact tests validates the chitosan coating's superhydrophobic nature, showcasing an advancing contact angle (θA) of 151° and a receding contact angle (θR) of 136°.

Global Superhydrophobic Coatings Market Report Scope

A superhydrophobic coating is a thin surface layer that repels water and is made from superhydrophobic materials. The superhydrophobic coating has intense applications in the field of self-cleaning, antifogging, antibacterial, and environmental remediation because of its nonwetting behavior.

The superhydrophobic coatings market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into anti-corrosion, anti-icing, self-cleaning, and anti-wetting. Based on the end-user industry, the market is segmented into textile and footwear, automotive, building and construction, and upcoming end-user industries. The report also covers the market sizes and forecasts for the superhydrophobic coatings market in major countries across several regions.

For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Anti-corrosion |

| Anti-icing |

| Self-cleaning |

| Anti-wetting |

| Textile and Footwear |

| Automotive |

| Building and Construction |

| Upcoming End-user Industries |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Turkey | |

| Rest of Middle-East and Africa |

| By Product Type | Anti-corrosion | |

| Anti-icing | ||

| Self-cleaning | ||

| Anti-wetting | ||

| By End-user Industry | Textile and Footwear | |

| Automotive | ||

| Building and Construction | ||

| Upcoming End-user Industries | ||

| By Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the superhydrophobic coating market expected to grow from 2026 to 2031?

Revenue is projected to rise from USD 62.89 million in 2026 to USD 190.72 million in 2031, reflecting a 24.85% CAGR.

Which region holds the largest share of demand for superhydrophobic coatings?

North America led with a 62.60% share in 2025, supported by strong EV battery, aerospace, and premium automotive activities.

What drives the transition away from fluorinated chemistries?

Pending REACH restrictions on C6 fluoropolymers and corporate sustainability goals are pushing rapid adoption of PFAS-free nano-silica systems.

Which product type dominates current sales?

Anti-wetting formulations account for 58.21% revenue and show the fastest growth at a 25.95% CAGR through 2031.

How do superhydrophobic coatings benefit EV battery packs?

They cut moisture-related failures, enhancing thermal runaway prevention and extending battery life in demanding duty cycles.

Page last updated on: