Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

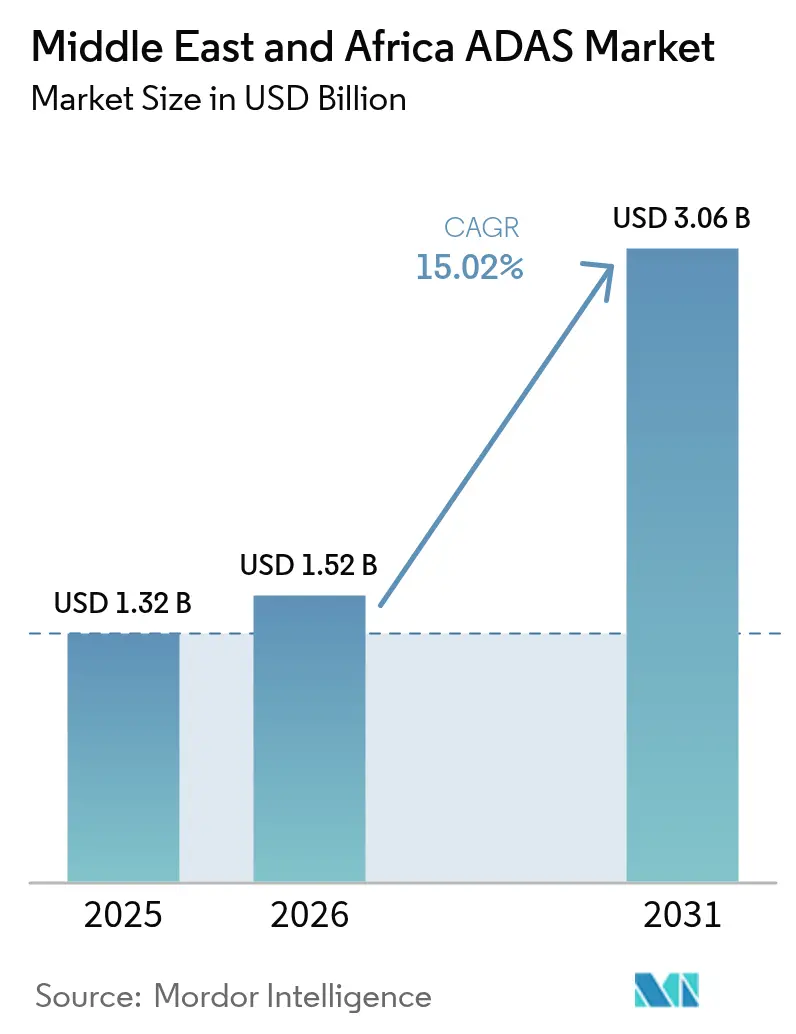

| Base Year Market Size (2025) | USD 1.32 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 15.02% CAGR |

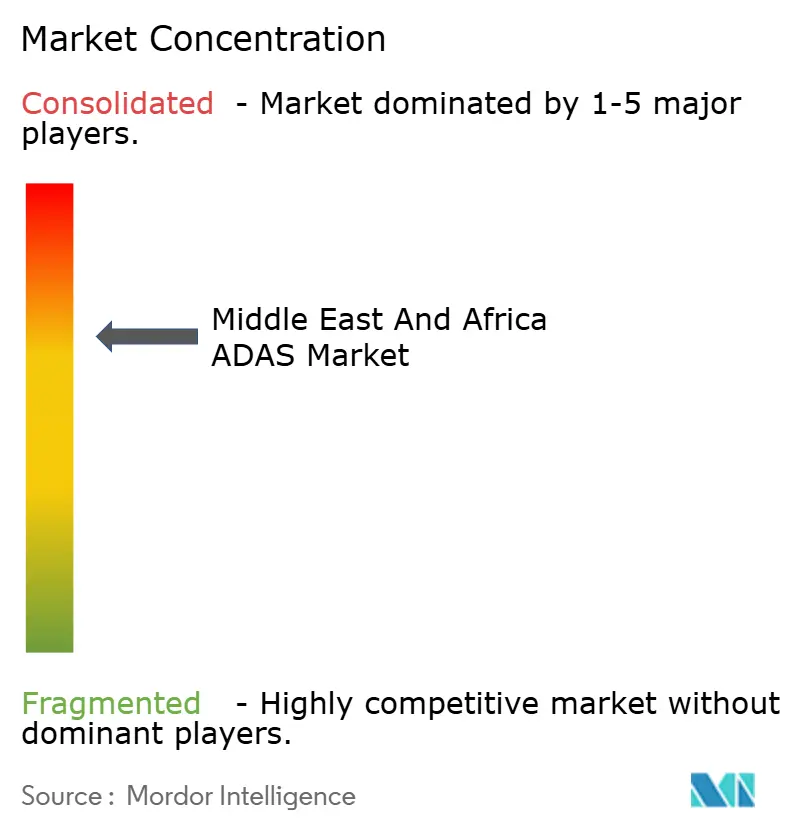

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa ADAS Market Analysis by Mordor Intelligence

The Middle East and Africa Advanced Driver Assistance Systems market size is expected to grow from USD 1.32 billion in 2025 to USD 1.52 billion in 2026 and is forecast to reach USD 3.06 billion by 2031 at 15.02% CAGR over 2026-2031. This sustained expansion underscores how Gulf governments treat ADAS as an essential pillar of their smart-mobility agendas rather than an optional premium feature. Regulatory catalysts such as Dubai’s Law No. 9 of 2023 and Saudi Arabia’s Vision 2030 targets, combined with sovereign-wealth-fund investments into autonomous technology corridors, create a predictable demand pipeline. Sensor innovation that endures high heat and dust, rising premium-vehicle registrations, and expanding 5 G-enabled V2X networks reinforce the region’s commercial logic for rapid ADAS adoption. As a result, the advanced driver assistance systems market is evolving from hardware-centric packages to software-defined platforms optimized for Middle-Eastern operating conditions.

Key Report Takeaways

- By system type, parking-assist systems led with 29.12% revenue share in 2025, while automatic emergency braking is projected to expand at a 18.74% CAGR through 2031.

- By sensor technology, camera solutions captured 42.75% share in 2025; LiDAR units are the fastest-growing at a 18.96% CAGR to 2031.

- By vehicle type, passenger cars accounted for 74.10% share in 2025, whereas medium and heavy commercial vehicles are set to grow at a 16.35% CAGR over the forecast period.

- By level of autonomy, Level 1 driver-assistance held 56.85% share in 2025; Level 2 platforms show the strongest momentum with a 17.22% CAGR through 2031.

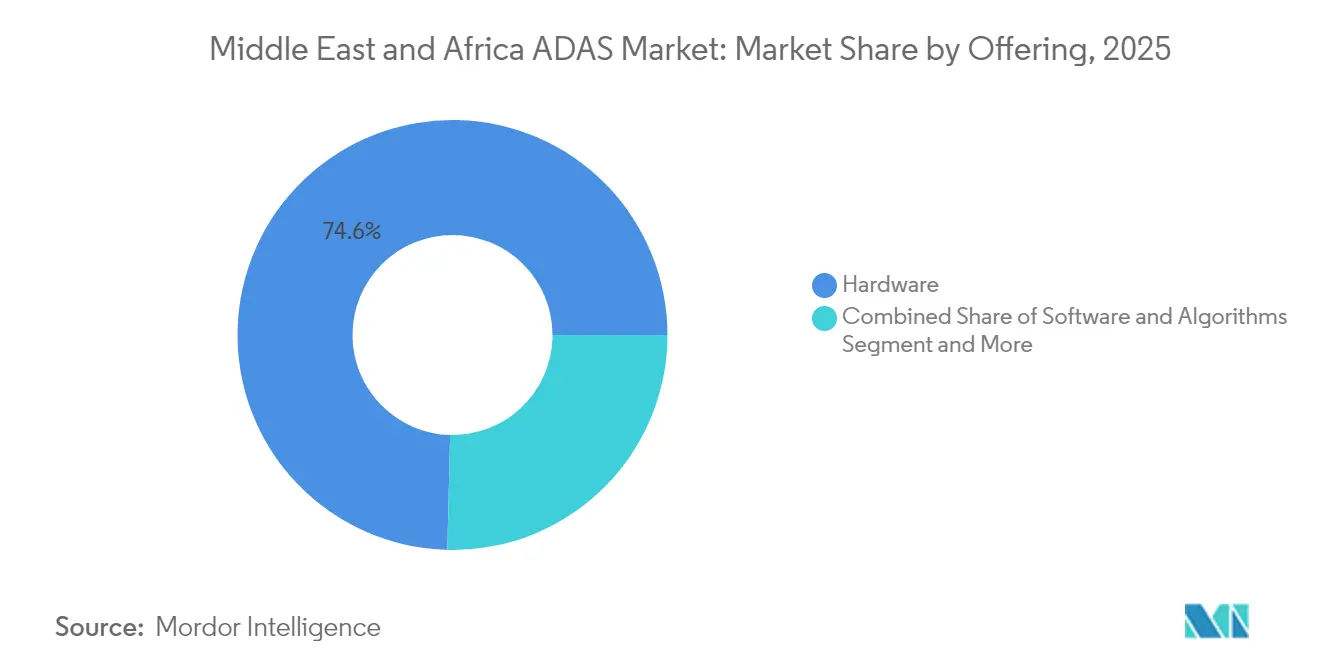

- By offering, hardware components represented 74.62% of 2025 revenue, while software and algorithms are forecast to rise at a 16.44% CAGR.

- By distribution channel, OEM-fit installations dominated with 84.10% share in 2025; the aftermarket segment is advancing at a 16.71% CAGR.

- By geography, Saudi Arabia commanded 28.20% regional share in 2025, and the United Arab Emirates is poised for the highest growth at a 15.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa ADAS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory NCAP-Style Safety Regulations | +3.2% | Gulf states with early adoption in UAE, Saudi Arabia | Medium term (2-4 years) |

| Premium-Vehicle L2+ Feature Penetration | +2.8% | UAE, Saudi Arabia, Qatar with spillover to Egypt, Morocco | Short term (≤ 2 years) |

| Sensor Cost Declines and Local Assembly | +2.1% | Egypt, Morocco manufacturing hubs, regional distribution | Medium term (2-4 years) |

| Smart-City V2X Infrastructure Corridors | +1.9% | Dubai, Riyadh, NEOM smart city projects | Long term (≥ 4 years) |

| Fleet Standardization of Safety Packs | +1.7% | Urban centers across GCC, North Africa | Short term (≤ 2 years) |

| Vision-2030 Mobility Tech Funding | +1.4% | Saudi Arabia with regional spillover effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory NCAP-style Safety Regulations & Fleet-fit Mandates

Regional transport ministries now embed Euro-NCAP-equivalent safety suites into type-approval frameworks. Dubai’s Roads and Transport Authority began requiring telematics in heavy trucks, and UN ECE’s Driver Control Assistance Systems regulation offers a harmonized technical rulebook [1]“Driver Control Assistance Systems Regulation,”, United Nations Economic Commission for Europe, unece.org. Because operating licences increasingly hinge on compliance, fleet operators accelerate ADAS installation schedules, creating a predictable revenue stream for Tier 1 suppliers.

Premium-vehicle Uptake Boosting L2+ Feature Penetration

Affluent Gulf consumers value collision-avoidance and highway-pilot functions as lifestyle statements. Hyundai’s IONIQ range and Chinese brands like Changan now bundle Highway Driving Assist and automated lane-change features as standard on top trims. The demonstration effect shortens diffusion cycles, prompting mid-segment OEMs to offer stripped-down L2 packages at lower price points.

Sensor Cost Declines & Local Assembly Incentives

Governments in Egypt and Morocco tie import-duty relief and land grants to local electronics content. Investments such as Leoni’s EUR 40 million wiring-harness plant and Geely’s CKD facility decrease logistics costs and shorten lead times [2]“Leoni Egypt Wiring Harness Factory,”, MarkLines, marklines.com. Component localization also builds a technician base to perform the intricate calibration of ADAS hardware demands.

Smart-city Corridors Enabling ADAS-ready V2X Infrastructure

Mega-projects, including NEOM and Dubai 5G corridors, integrate adaptive traffic signal networks with roadside units that broadcast real-time data. Partnerships among telecom carriers, Tier 1s, and municipal IT agencies deliver the latency thresholds required for cooperative lane-merge and signal-phase-timing applications. Controlled testbeds reduce supplier validation time, accelerating commercial release cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost Vs Disposable Income | -2.3% | Sub-Saharan Africa, North Africa excluding Gulf states | Medium term (2-4 years) |

| Sparse Calibration and Servicing Networks | -1.8% | Rural areas across MEA, smaller urban centers | Long term (≥ 4 years) |

| Harsh Dust-Heat Environment Degrading Sensors | -1.4% | Desert regions across MEA, particularly Saudi Arabia, UAE, Egypt | Short term (≤ 2 years) |

| Tariff Swings and Supply Chain Disruption | -1.1% | Import-dependent markets, cross-border trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High System Cost Versus Disposable Income in Africa

In Sub-Saharan markets, the price uplift for ADAS can equal 5–10% of a new-vehicle invoice, a hurdle when average car-ownership costs already strain household budgets. Retrofit kits once addressed this gap, but Mobileye’s 2024 exit from aftermarket programs removed a key low-cost channel. Without local credit subsidies or deeper duty breaks, mass adoption lags behind Gulf peers.

Sparse Calibration and Servicing Networks

A shortage of trained technicians and specialized equipment outside tier-one cities slows repairs and raises total-cost-of-ownership fears. Frequent sandstorms and high ambient heat exacerbate sensor misalignment, requiring recalibration cycles that many workshops are unequipped to perform. This reliability concern discourages buyers in secondary markets until service-capacity gaps close.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Emergency Braking Drives Safety Evolution

Automatic emergency braking contributes the highest incremental value, expanding at 18.74% CAGR as regulators add forward-collision mitigation to inspection checklists. While already mainstream, parking-assist technology still holds a 29.12% share because dense urban cores in Dubai and Riyadh heighten low-speed collision anxiety. Tier 1 suppliers bundle these features to encourage higher take-rates, reinforcing the advanced driver assistance systems market’s momentum.

Integrated safety suites increasingly combine blind-spot detection, adaptive front lighting, and driver-monitoring cameras. Tier 1s such as Bosch overlay AI perception algorithms on modular hardware, enabling OEMs to deploy tailored packages without costly redesigns.

By Sensor Technology: Camera Dominance Faces LiDAR Challenge

Cameras remain the economic workhorse, controlling 42.75% of 2025 revenue. Yet Gulf operators contend with glare and dust, catalyzing LiDAR’s 18.96% CAGR as solid-state units drop below USD 500 per channel. Radar upgrades to 4D-imaging configurations add weather-resilient object classification, while ultrasonic rings stay vital for low-speed urban maneuvers.

Software-defined architectures let OEMs refine algorithms over the air, optimizing sensor fusion for regional driving idiosyncrasies. This capability shifts differentiation from hardware cost curves toward update cadence and data-science expertise, a hallmark of the advanced driver assistance systems industry.

By Vehicle Type: Commercial Fleets Lead Transformation

Passenger cars account for 74.10% of the advanced driver assistance systems market size in 2025, but commercial fleets deliver the highest growth logic with CAGR 16.35%. Cargo firms retrofit telematics-linked ADAS to cut insurance premiums and driver downtime. Dubai’s heavy-truck telematics mandate accelerates adoption among logistics operators seeking compliance certificates.

Ride-hailing companies leverage ADAS to elevate passenger-safety branding and reduce collision settlement expenses. Fleet data generated by these platforms feeds machine-learning loops that refine perception stacks, further differentiating service quality and fueling the advanced driver assistance systems market.

By Level of Autonomy: L2 Systems Gain Regulatory Momentum

Level 1 functionalities still dominate with 56.85% share, but multi-function Level 2 packages post a 17.22% CAGR outlook as UN ECE regulations clarify design-validation rules. VW’s collaboration with Valeo and Mobileye targets 360-degree sensor coverage in mid-segment models by 2027 .

Driver-monitoring cameras become compulsory in L2 packages, ensuring that legal liability stays with attentive humans and enabling regulators to permit hands-off cruising lanes

By Offering: Software Growth Signals Industry Evolution

Hardware held the largest slice of 2025 revenue at 74.62% of the advanced driver assistance systems market share, reflecting the cost weight of sensors, electronic control units, and wiring harnesses in every new vehicle platform. This predominance mirrors OEM-design choices that still package safety functionality around physical components certified during type approval.

Though accounting for a smaller base in 2025, software and algorithms post the fastest 2026-2031 trajectory with a 16.44% CAGR. Over-the-air update capability, AI-driven perception stacks, and subscription monetization elevate code to a strategic asset, encouraging Tier 1s such as Aumovio to pivot toward software-defined vehicle roadmaps.

By Distribution Channel: OEM Integration vs. Aftermarket Agility

Factory-installed systems captured 84.10% of 2025 deliveries, showing how in-line calibration, cybersecurity compliance, and tighter quality controls favor OEM-fit installations for the advanced driver assistance systems market size. The integrated approach also supports coordinated warranty coverage and life-cycle data collection that streamlines future feature upgrades.

The aftermarket segment, while representing the minority today, records the quickest advance at a 16.71% CAGR through 2031. Fleet retrofits of medium- and heavy-duty vehicles, extended asset life, and regulatory compliance mandates sustain demand even after Mobileye’s 2024 exit from retrofit programs. Independent service providers that invest in specialized calibration tools are positioned to capture this upswing, especially in commercial-vehicle corridors where downtime costs outweigh retrofit expenses.

Geography Analysis

Saudi Arabia commands 28.20% of 2025 revenue thanks to Vision 2030’s explicit ADAS and autonomous-mobility milestones. NEOM’s USD 100 million joint venture with Pony.ai supplies a testbed for Level 4 robo-taxis. The UAE records a 15.38% CAGR on the back of Dubai’s target to make 25% of trips autonomous by 2030. North-African manufacturing schemes improve affordability but will not close income gaps quickly, delaying mass uptake outside premium tiers.

The United Arab Emirates operates as a regulatory sandbox, fast-tracking approvals for pilot projects by WeRide, Baidu, and Uber. Federal legislation provides a unified compliance ladder, giving suppliers scale benefits across the seven emirates. An expanding 5G and roadside-sensor grid supplies the low-latency backbone needed for cooperative perception applications.

Beyond the Gulf, Egypt and Morocco prioritize supplier-park incentives to integrate ADAS wiring, camera brackets, and ECUs into CKD lines. This localization trims import duties and aligns with continental trade zones, progressively lowering retail pricing for mass-market trims. South Africa’s established export base offers engineering talent, though US tariff risks temper investment velocity.

Competitive Landscape

Market power is shifting from pure-play hardware vendors to vertically integrated platform players. Autoliv, Aumovio, and ZF still dominate restraint technologies, yet Chinese challengers such as WeRide and Pony.ai deploy full-stack solutions financed by Gulf sovereign funds. Consolidation manifests in software-centric alliances—exemplified by Volkswagen-Valeo-Mobileye—where perception algorithms, driver-monitoring logic, and OTA pipelines combine into turnkey Level 2+ suites.

Suppliers that master desert-tuned perception, in-field calibration, and cyber-security certification secure an edge. As shown by DENSO’s equity stake in Onsemi, strategic control of semiconductor supply mitigates chip-shortage volatility. As over-the-air feature licensing matures, recurring software revenue reduces margin dependence on ECU bill-of-materials, supporting sustainable profitability trajectories across the advanced driver assistance systems market.

Middle East And Africa ADAS Industry Leaders

Robert Bosch GmbH

Continental AG

Mobileye

Autoliv AB

Hyundai Mobis Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pony.ai and Uber launched a joint robotaxi pilot in Dubai, aiming for phased removal of safety operators pending final approval

- May 2025: DENSO and Rohm agreed to co-develop power and sensor chips for EVs and ADAS within an integrated supply chain.

- April 2025: Uber and WeRide signed with Dubai RTA to embed autonomous vehicles in the city’s Self-Driving Transport Strategy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we consider the Middle East and Africa ADAS market to consist of every factory-installed or professionally retrofitted driver-assistance hardware module and its embedded control software, radar, camera, ultrasonic, LiDAR, and sensor-fusion ECUs that enable SAE Level 1 and Level 2 functions in on-road passenger cars and commercial vehicles across 18 regional countries.

Scope Exclusions: Purely software-only over-the-air feature upgrades that do not add or replace physical sensing hardware remain outside our sizing scope.

Segmentation Overview

- By System Type

- Parking Assist Systems

- Adaptive Front-lighting

- Night Vision

- Blind-Spot Detection

- Lane Departure Warning

- Automatic Emergency Braking

- Driver Monitoring & Drowsiness Detection

- By Sensor Technology

- Radar (24 / 77 / 79 GHz)

- Camera (Mono, Stereo, Surround)

- LiDAR (Solid-state, Mechanical)

- Ultrasonic & Infra-red

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium & Heavy Commercial Vehicles & Buses

- By Level of Autonomy

- L1 (Driver Assistance)

- L2 (Partial Automation)

- L2+ (Enhanced Partial Automation)

- By Offering

- Hardware (ECU, Sensors)

- Software & Algorithms

- Integration & Calibration Services

- By Distribution Channel

- OEM-fit

- Aftermarket Retrofit

- By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- South Africa

- Egypt

- Morocco

- Nigeria

- Rest of Middle East and Africa

Detailed Research Methodology and Data Validation

Primary Research

We spoke with regional safety regulators, OEM product planners, Tier 1 sensor engineers, and aftermarket installers across the GCC, South Africa, and North Africa. Their insights validated real-world sensor bills of material, country-level take rates, average selling prices, and emerging retrofit channels, letting us resolve desk-research gaps and fine-tune growth assumptions.

Desk Research

Our team first compiles baseline demand signals from open sources such as OICA vehicle production tallies, UN Comtrade component trade codes, Gulf Standards Organization mandates, and road-fatality statistics issued by the WHO. We enrich these with country dashboards published by transport ministries in Saudi Arabia, the UAE, South Africa, and Egypt, which quantify new-vehicle safety-feature fitment rates.

To tighten model inputs, we tap paid databases, D&B Hoovers for supplier revenues and Dow Jones Factiva for contract awards, plus technical literature in IEEE Xplore and WIPO patent families tracking radar and camera innovations. Additional context comes from OEM 10-Ks, tier-one supplier presentations, and regional automotive associations. This list is illustrative; many further sources helped us cross-check figures and clarify definitions.

Market-Sizing & Forecasting

A top-down build starts with 2024 light-vehicle parc and new registrations, applies verified ADAS penetration ratios, and multiplies by consensus ASPs to derive the 2025 value pool. Selective bottom-up checks, supplier revenue roll-ups and sampled dealership price audits, are then used to adjust totals where variance exceeds 5 percent. Key variables driving the model include Gulf NCAP rollout timelines, sensor cost curves, hybrid EV sales share (which correlates with high-spec trims), regulatory lead times for AEB mandates, and 5G V2X infrastructure milestones. A multivariate regression with ARIMA error correction projects each driver through 2030; scenarios are stress tested with interviewees for plausibility.

Data Validation & Update Cycle

Before sign-off, two analysts triangulate outputs against independent indicators such as import duties collected on radar modules and insurance premium discounts tied to ADAS fitment. Anomalies trigger re-checks with sources. Reports refresh every twelve months, with mid-cycle updates when material policy or technology shifts occur.

Why Mordor's Middle East And Africa ADAS Baseline Commands Reliability

Estimates published by different firms often diverge because they adopt dissimilar system lists, miss retrofit flows, or convert currencies at varied dates.

Key gap drivers in this market include whether aftermarket kits are counted, how ASP erosion is modeled, and the depth of country coverage beyond the GCC.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.32 billion (2025) | Mordor Intelligence | - |

| USD 0.72 billion (2024) | Global Consultancy A | Narrower system scope; excludes aftermarket retrofits; fewer vehicle classes |

| USD 2.00 billion (2025) | Industry Research Firm B | Shipment-only forecast without price normalization; covers six countries only |

In sum, Mordor's disciplined variable selection, dual-path validation, and annual refresh cadence provide decision-makers with a transparent, balanced baseline that can be traced back to publicly verifiable metrics and corroborated expert opinion.

Key Questions Answered in the Report

What is the current value of the ADAS market in the Middle East and Africa?

The advanced driver assistance systems market size is USD 1.52 billion in 2026.

How fast will the regional ADAS market grow through 2031?

The ADAS market is forecast to expand at a 15.02% CAGR, reaching USD 3.06 billion by 2031.

What sensor technology is growing the quickest?

LiDAR solutions are advancing at a 18.96% CAGR, driven by resilience to dust and glare.

Why are commercial fleets investing in ADAS?

Fleet operators quantify benefits through lower insurance payouts, improved driver retention, and regulatory compliance incentives.

How does local manufacturing affect ADAS affordability?

New wiring-harness, ECU, and CKD plants in Egypt and Morocco cut import duties and logistics costs, gradually lowering retail prices across North Africa.

Page last updated on: