Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

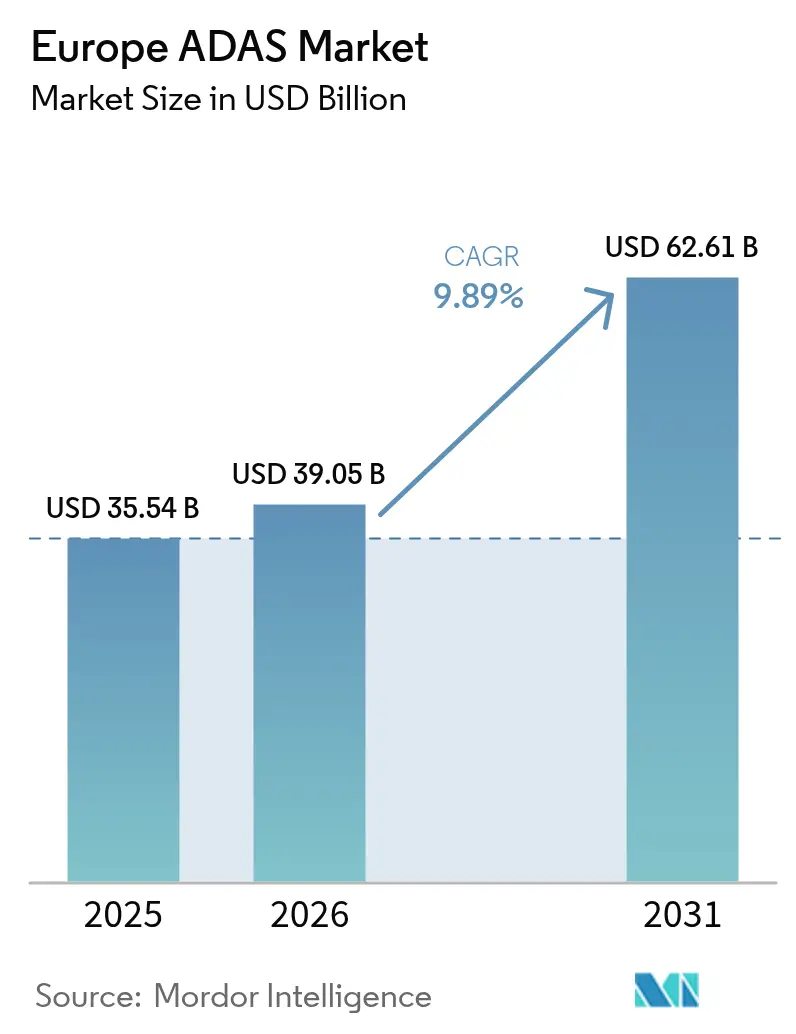

| Base Year Market Size (2025) | USD 35.54 Billion |

| Market Size (2026) | USD 39.05 Billion |

| Market Size (2031) | USD 62.61 Billion |

| Growth Rate (2026 - 2031) | 9.89% CAGR |

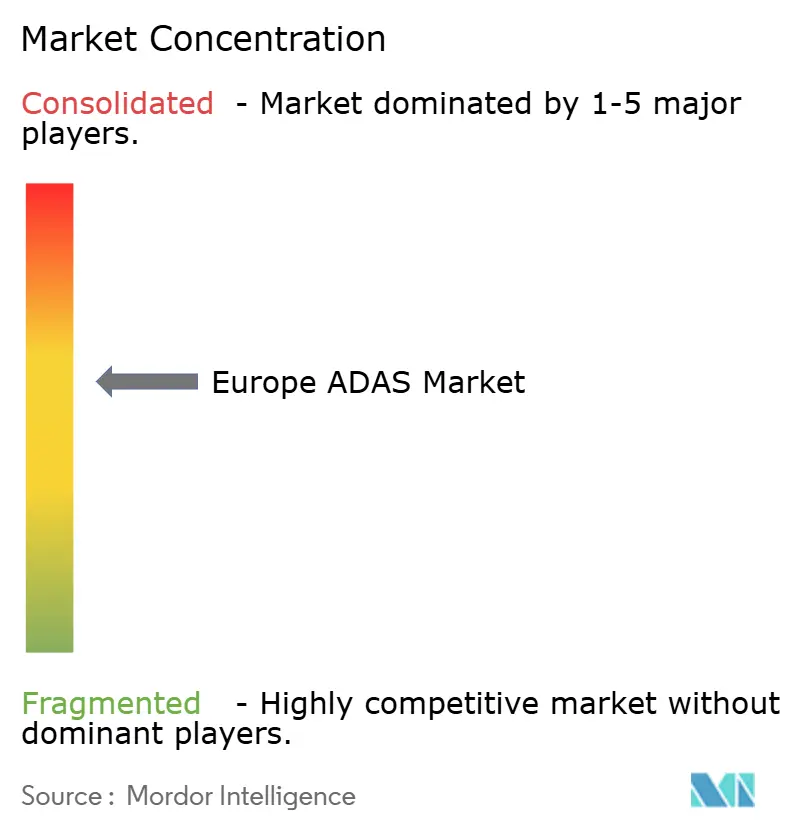

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe ADAS Market Analysis by Mordor Intelligence

The Europe ADAS Market size was valued at USD 35.54 billion in 2025 and estimated to grow from USD 39.05 billion in 2026 to reach USD 62.61 billion by 2031, at a CAGR of 9.89% during the forecast period (2026-2031). Mandatory safety regulations, rapid sensor cost declines, and expanding over-the-air business models collectively reinforce steady demand while creating new profit pools for suppliers of software-defined architectures. Increasing alignment between European Commission mandates and the Euro NCAP 2030 roadmap compresses the traditional “premium-to-mass” trickle-down cycle, making automatic emergency braking, lane-keeping, and driver-monitoring functions standard even on entry-level trims. Competitive intensity rises as semiconductor-centric entrants challenge Tier 1 incumbents with integrated hardware–software platforms that simplify system validation and shorten OEM sourcing cycles. Germany’s early approval of Level 3 highway automation and Spain’s fleet electrification incentives showcase how regulation and industrial policy jointly accelerate penetration across passenger and commercial vehicle classes. Heightened demand for multi-modal sensor fusion that maintains performance in snow, fog, and nighttime conditions supports the shift from single-sensor redundancies to cohesive perception stacks that include radar, camera, and LiDAR in the same enclosure.

Key Report Takeaways

- By system type, automatic emergency braking captured 22.74% of the European ADAS market share in 2025, while night-vision systems are advancing at a 10.04% CAGR to 2031.

- By sensor type, radar retained 37.10% of the European ADAS market share in 2025; LiDAR adoption is projected to climb 10.06% annually through 2031.

- By vehicle type, passenger cars commanded 72.80% of the European ADAS market share in 2025, whereas medium and heavy commercial vehicles are poised for a 10.08% CAGR to 2031.

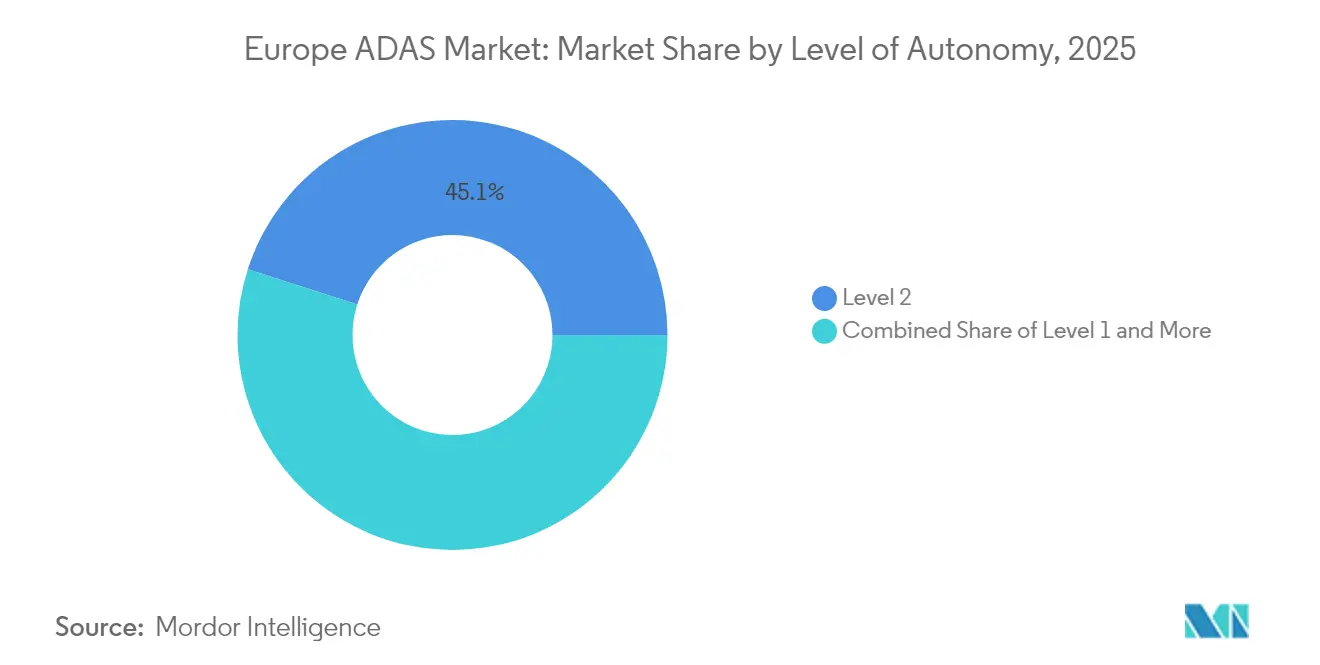

- By level of autonomy, Level 2 systems accounted for 45.05% of the European ADAS market share in 2025, but Level 3 volumes are forecast to grow 10.03% annually due to German and pan-EU approvals.

- By sales channel, OEM factory-fit channels supplied 82.92% of the European ADAS market share in 2025, with aftermarket retrofit solutions tracking a 9.98% CAGR through 2031 as fleet operators modernize legacy assets.

- By geography, Germany accounted for 28.40% of the European ADAS market share in 2025, while Spain registered the highest CAGR of 9.96% till 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe ADAS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU General Safety Regulation 2024 Mandate | +2.8% | EU-wide, with Germany and France leading implementation | Short term (≤ 2 years) |

| EURO NCAP 2030 Vision Roadmap | +2.1% | EU core markets, extending to UK and Switzerland | Medium term (2-4 years) |

| Mass-Market Level 2 Feature Bundling Surge | +1.9% | Germany, France, Italy primary markets | Medium term (2-4 years) |

| 77 GHz Radar Cost Decline | +1.7% | Global, with European OEMs as early adopters | Short term (≤ 2 years) |

| OTA-Based ADAS Feature Monetization Models | +1.2% | Premium markets: Germany, UK, Nordics | Long term (≥ 4 years) |

| Digital-Twin Homologation Frameworks | +0.8% | Germany, Netherlands, Sweden pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU General Safety Regulation 2024 Mandate

The regulation requires automatic emergency braking, lane departure warning, and driver drowsiness detection across every new vehicle category sold in the bloc. Entry-level passenger cars, motorcycles, and agricultural machinery must meet identical baseline safety specifications, forcing OEMs to accelerate procurement schedules that have already filled Tier 1 order books through 2026. Non-compliant models lose type approval, creating a hard stop on regional market access and giving early certified suppliers guaranteed volume visibility [1]“General Safety Regulation,” European Commission, ec. europa.eu .

EURO NCAP 2030 Vision Roadmap Alignment

Euro NCAP’s staged roadmap sets performance thresholds higher than legislative minima, requiring OEMs to demonstrate cyclist, pedestrian, and motorcyclist recognition in complex mixed-traffic conditions. These protocols reward systems that fuse radar, camera, and LiDAR inputs to handle adverse weather, nighttime, and construction zones. Ratings directly influence fleet procurement and insurance pricing, pushing manufacturers toward continuous sensor and software upgrades that favor suppliers with iterative validation capacity[2]“Roadmap 2030,” Euro NCAP, euroncap.com .

Mass-Market Level 2 Feature Bundling Surge

Volume brands such as Renault package adaptive cruise control, lane centering, and emergency braking as default on B-segment hatchbacks, proving that bundling lowers per-sensor cost and widens the revenue base for subscription-driven feature unlocks. BMW’s Personal Pilot illustrates an upsell ladder in which entry functionality ships standard, while premium modules monetize through over-the-air activation throughout the vehicle life cycle[3]“Personal Pilot Announcement,” BMW Group, bmwgroup.com .

77 GHz Radar Cost Decline & Platform Standardization

Switching from 24 GHz to 77 GHz modules improves range and resolution while benefiting from semiconductor process shrinkage that cuts the bill-of-material cost. Continental’s expansion of 77 GHz capacity signals confidence that radar remains the backbone of highway automation even as LiDAR prices fall [4]“77 GHz Radar Expansion,” Continental AG, continental.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incremental Cost | -1.8% | Eastern Europe, Southern Italy, Spain budget segments | Short term (≤ 2 years) |

| Sensor Performance Loss | -1.4% | Nordic countries, Alpine regions, UK | Medium term (2-4 years) |

| GDPR Compliance Cost | -0.9% | EU-wide, particularly Germany and France | Medium term (2-4 years) |

| Gallium Export Controls Hitting Lidar Supply | -0.7% | Global supply chain, European OEM impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Incremental Cost For Entry-Level Vehicles

City-car platforms now face an added cost due to the integration of ADAS hardware and electronics. This development forces OEMs to either absorb the margin pressure or potentially alienate budget-conscious buyers in Eastern Europe and southern markets. Meanwhile, smaller manufacturers, without the advantage of global scale, find it challenging to distribute engineering overheads. As a result, they face an extended affordability gap, awaiting a significant drop in semiconductor prices.

Sensor Performance Loss In Snow/Fog Conditions

Camera detection ranges fall by half in heavy snow, and radar accuracy drops in dense fog, leading to consumer frustration and potential liability. Nordic field tests reveal elevated deactivation rates that undermine trust in assisted-driving promises, spurring investment in thermal imaging and advanced radar while highlighting the cost–benefit tension for mass-market trims.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Emergency Braking Leads Safety Evolution

Automatic emergency braking held 22.74% of the European ADAS market share in 2025, a position cemented when the 2024 General Safety Regulation made the feature mandatory across new registrations. The Europe ADAS market size for night-vision solutions is forecast to grow exponentially by 2031, translating into a 10.04% CAGR as thermal cameras mitigate fog and darkness and help brands differentiate in premium tiers. Forward-collision warning, lane-departure warning, and adaptive cruise control continue to ship in volume bundles, reinforcing pathway migration from reactive to predictive functions that anticipate driver intent.

OEM roadmaps increasingly fuse parking, blind-spot, and drowsiness modules into unified domain controllers that consolidate ECUs and cut wiring complexity. GDPR-compliant drowsiness monitoring expands slowly due to privacy safeguards, yet remains critical for Euro NCAP scoring. Adaptive lighting systems add matrix-LED capabilities that optimize beam patterns without blinding oncoming traffic, positioning illumination control as a safety and energy efficiency play. These converging trends confirm the European ADAS market as a hardware-software ecosystem in which modular safety building blocks become firmware features upgradeable over a vehicle’s lifetime.

By Sensor Type: Radar Dominance Faces LiDAR Challenge

Radar sensors retained 37.10% of the European ADAS market share in 2025, benefiting from USD 32 mid-range module pricing, robust all-weather performance, and regulatory familiarity. The Europe ADAS market size for LiDAR is projected to grow significantly by 2031, riding a 10.06% CAGR once unit pricing falls toward USD 500 and Euro NCAP stresses vulnerable road-user protection. Cameras remain indispensable for lane-line and traffic-sign recognition, yet face snow occlusion issues that elevate the value proposition of thermal and radar fusion.

Continental’s 77 GHz MIMO radar arrays deliver finer resolution while conserving package space, protecting the radar’s core highway role. Simultaneously, Valeo’s solid-state LiDAR price cuts push the sensor into high-volume C-segment crossovers, a milestone that rebalances sensory hierarchies. Integrated perception stacks merge radar velocity, camera semantics, and LiDAR depth into single ECUs, lowering latency and creating redundancy demanded for Level 3 approvals. This integration accelerates supplier consolidation inside the European ADAS market, with OEMs favoring turnkey sensor suites that minimize validation loops.

By Vehicle Type: Commercial Fleets Drive Adoption

Passenger cars delivered 72.80% of the European ADAS market share in 2025. Yet, the European ADAS market size for medium and heavy commercial vehicles is poised to rise at a 10.08% CAGR on safety-driven fleet upgrades. Logistics operators quantify return on investment through lower accident downtime and reduced insurance premiums, allowing faster payback than in retail passenger segments. Two-wheeler adoption picks up as regulators extend safety mandates, though its absolute volume remains small.

ZF’s OnGuardMAX emergency braking illustrates how truck-specific kinematics trigger tailored ADAS calibration distinct from car applications. Fleet purchasing centralizes decision-making, bringing bulk orders that support supplier scale. Passenger-car programs prioritize comfort add-ons such as automated parking, whereas commercial platforms focus squarely on collision avoidance and lane-keeping to protect cargo and drivers. As the driver shortage intensifies, fleets turn to ADAS not only for safety, but also to uplift job satisfaction and retain scarce labor.

By Level of Autonomy: Level 3 Breakthrough Accelerates

Level 2 solutions represented 45.05% of the European ADAS market share in 2025, but Level 3 programs now move from pilot to series production on German Autobahns with a robust CAGR of 10.03% through 2031. The Europe ADAS market share for Level 3 vehicles is expected to rise materially once Mercedes-Benz DRIVE PILOT, approved for 95 km/h operation, expands beyond its initial tranche of S-Class and EQS units. BMW Personal Pilot targets dense traffic up to 60 km/h, underscoring how OEMs segment operational design domains to manage liability and cost.

Level 2+ bridges the gap for brands that cannot yet assume full system liability but still need hands-off capability during monotone highway stretches. Regulatory alignment across France, Italy, and Spain shortens homologation cycles, making Level 3 the new competitive yardstick in premium sales pitches. Even so, cost and functional-safety demands keep Level 4 aspirations confined to geo-fenced pilots, reinforcing that Europe's ADAS market growth remains tethered to incremental autonomy layers.

By Sales Channel: Aftermarket Retrofit Gains Momentum

OEM factory installations captured 82.92% of the European ADAS market share 2025 because sensors, wiring, and domain controllers integrate most efficiently at build. Though smaller, the aftermarket retrofit expands at a 9.98% CAGR as insurers adjust premiums to reflect ADAS presence, prompting fleets to upgrade rather than replace assets. Valeo SafeSide packages radar, camera, and HMI modules in a kit calibrated for vans and rigid trucks, while Continental offers dealer-installed blind-spot detection for older city buses.

Installation complexity remains a hurdle. Workshops require precise alignment rigs and software authorization certificates, spawning a service ecosystem of ADAS-calibration specialists. OTA update support further tightens ties between retrofit suppliers and fleets, unlocking subscription revenue even on legacy vehicles. As compliance deadlines approach, retrofit demand shores up long-tail vehicles, supporting total Europe ADAS market expansion beyond new-car production alone.

Geography Analysis

Germany held 28.40% of the European ADAS market share in 2025, thanks to its dense cluster of premium OEMs, suppliers, and regulatory bodies coordinating early Level 3 approvals. Mercedes-Benz and BMW used these rulings to commercialize conditional automation, compelling domestic suppliers such as Bosch, Continental, and ZF to align roadmaps with higher compute loads, triple redundancy, and cybersecurity-by-design. Government-funded pilot corridors helped validate sensor fusion in real-world mixed traffic, reinforcing Germany’s lead in revenue and influencing EU policy harmonization.

Spain is the fastest-growing geography, posting a 9.96% CAGR through 2031 as its fleet electrification subsidies explicitly require advanced driver-assist kits on commercial vehicles and public buses. Spanish logistics players leverage ADAS to cut operating costs, while municipal tender rules stipulate collision-mitigation systems on new electric refuse trucks and ride-hail vans. EU structural funds further subsidize domestic Tier 2 electronics plants, lowering unit costs and enhancing local sourcing resilience. The country thus moves from technology adopter to partial contributor, adding depth to the broader European ADAS market.

France and Italy retain significant footprints backed by Valeo’s sensor plants and Stellantis’ STLA AutoDrive program, respectively. The United Kingdom sustains Euro NCAP alignment post-Brexit to preserve export continuity, although parallel work on autonomous-vehicle legislation could introduce divergence after 2026. Nordic markets focus on weather-resilient sensors, creating niche demand for thermal imaging and high-performance radar. Eastern Europe, while price-sensitive, benefits from growing component manufacturing that feeds Western OEM plants, reinforcing the continent’s integrated supply web. Collectively, these dynamics ensure that Europe's ADAS market penetration follows a spectrum rather than a single curve, but regulation keeps minimum feature levels rising everywhere.

Competitive Landscape

The competitive field blends traditional Tier 1 dominance with a surge of chip-centric challengers. Bosch, Continental, ZF, and Valeo still control broad portfolios, ranging from radars to domain controllers, preserving share through decades-old OEM ties. They respond to software disruption by forging alliances: Bosch partners with Volkswagen’s CARIAD unit on scalable perception stacks, while ZF integrates NVIDIA Drive for compute power in its ProAI controller, which has been shipping since 2024.

Semiconductor players Mobileye, Qualcomm, and NVIDIA supply turnkey “system-on-module” solutions that bundle SoCs, software, and reference sensors, allowing mid-tier OEMs to cut time-to-market. Their entry intensifies price competition and accelerates platform convergence around centralized compute zones. The strategic twist is revenue migration toward software licensing, data analytics, and over-the-air feature sales, pushing hardware margins downward.

Consolidation is evident as smaller lidar and software startups license IP or accept acquisition offers to navigate Euro NCAP testing costs. Traditional suppliers expand into retrofit and insurance-data services, diversifying income against margin squeeze in original equipment. These moves yield a moderately concentrated Europe ADAS market in which the top five vendors hold about 60% combined share. At the same time, niche specialists survive by focusing on sensors for adverse-weather regions or cybersecurity compliance modules.

Europe ADAS Industry Leaders

Autoliv AB

Continental AG

Delphi Automotive

ZF Friedrichshafen AG

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stellantis launches the STLA AutoDrive platform that bundles adaptive cruise control and lane centering across Peugeot, Opel, and Fiat models, making Level 2+ functionality standard and ready for subscription-based upgrades.

- January 2025: ZF merges Active Safety and Passenger Car Chassis units into the Chassis Solutions Division and secures a North American brake-by-wire order for 5 million vehicles alongside the first steer-by-wire production win on the Nio ET9, confirming by-wire scalability for ADAS integration.

- September 2024: ZF and Farizon sign an IAA Transportation MoU under which ZF supplies ADAS, e-drive, and methanol-hydrogen solutions for Farizon's new-energy trucks, extending European safety technology into Asian commercial-vehicle programs.

Europe ADAS Market Report Scope

ADAS, or advanced driver-assistance system, is a combination of sensors that aid and improve the safety of drivers and passengers on the road. It collects road and driver behavior data and enhances the human-machine interface through audio and visual alerts.

The European advanced driver assistance systems market is segmented by type, technology, vehicle type, and geography. By type, the market is segmented as parking assist systems, adaptive front-lighting, night vision systems, blind spot detection, lane departure warning, and other types. By technology, the market is segmented as radar, Li-DAR, and camera. By vehicle type, the market is segmented as passenger cars and commercial vehicles. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, and the Rest of Europe. The report offers market size and forecasts for the Europe ADAS market in value (USD) for all the above segments.

By System Type

| Parking Assist Systems |

| Adaptive Front-Lighting |

| Night Vision Systems |

| Blind-Spot Detection |

| Automatic Emergency Braking |

| Forward Collision Warning |

| Driver Drowsiness Alert |

| Traffic Sign Recognition |

| Lane Departure Warning |

| Adaptive Cruise Control |

By Sensor Type

| Radar |

| LiDAR |

| Camera |

| Ultrasonic |

| Infra-red |

By Vehicle Type

| Two-Wheelers |

| Passenger Cars |

| Medium & Heavy Commercial Vehicles |

By Level of Autonomy

| Level 1 |

| Level 2 |

| Level 3 |

| Level 4 |

| Level 5 |

By Sales Channel

| OEM-Fitted |

| Aftermarket Retrofit |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By System Type | Parking Assist Systems |

| Adaptive Front-Lighting | |

| Night Vision Systems | |

| Blind-Spot Detection | |

| Automatic Emergency Braking | |

| Forward Collision Warning | |

| Driver Drowsiness Alert | |

| Traffic Sign Recognition | |

| Lane Departure Warning | |

| Adaptive Cruise Control | |

| By Sensor Type | Radar |

| LiDAR | |

| Camera | |

| Ultrasonic | |

| Infra-red | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Medium & Heavy Commercial Vehicles | |

| By Level of Autonomy | Level 1 |

| Level 2 | |

| Level 3 | |

| Level 4 | |

| Level 5 | |

| By Sales Channel | OEM-Fitted |

| Aftermarket Retrofit | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the European ADAS market by 2031?

The market is forecast to reach USD 62.61 billion by 2031 based on a 9.89% CAGR.

Which ADAS system leads current adoption across Europe?

Automatic emergency braking leads with 22.74% share of 2025 installations.

Why is Spain showing the fastest growth in ADAS adoption?

Aggressive fleet electrification policies and mandatory safety requirements push Spain toward a 9.96% CAGR through 2031.

How quickly are Level 3 systems expected to scale?

Level 3 volumes are projected to rise 10.03% annually as regulatory approvals spread and OEM programs mature.

Which sensor technology is poised for the highest growth rate?

LiDAR is on track for a 10.06% CAGR once unit pricing approaches mainstream affordability.

What is driving aftermarket ADAS retrofit demand?

Insurance premium reductions and impending regulatory deadlines motivate fleets to upgrade legacy vehicles at a 9.98% CAGR.

Page last updated on: