Commercial Vehicle Active Power Steering Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

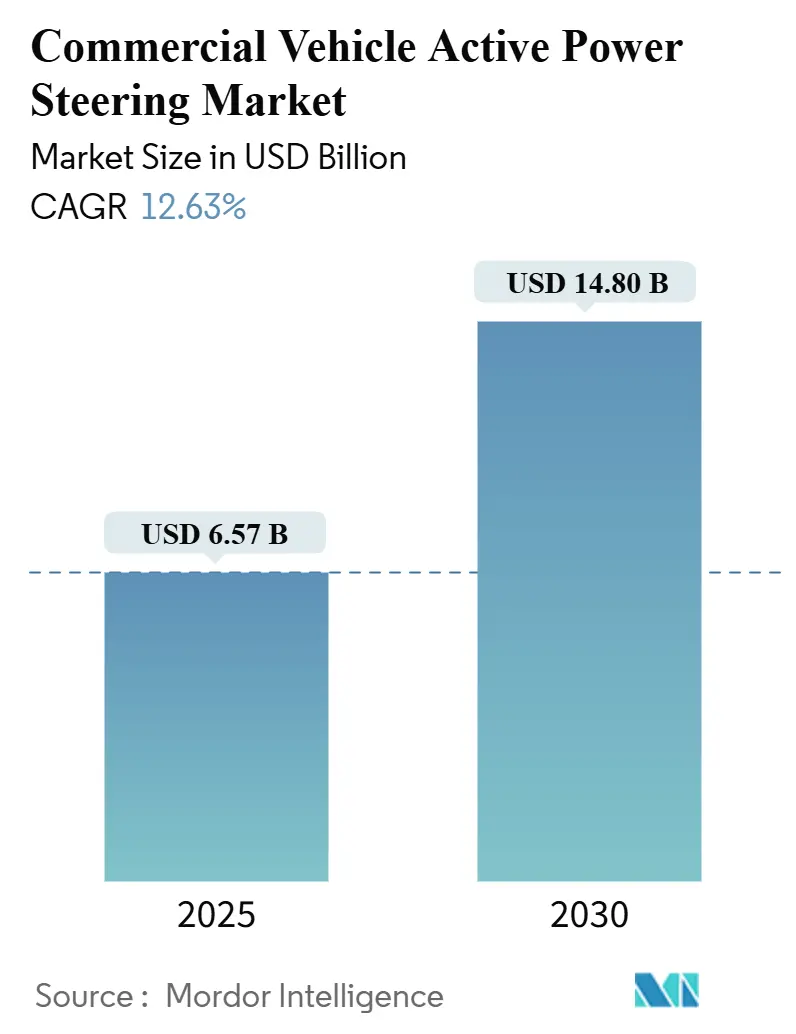

| Market Size (2025) | USD 6.57 Billion |

| Market Size (2030) | USD 14.80 Billion |

| Growth Rate (2025 - 2030) | 12.63% CAGR |

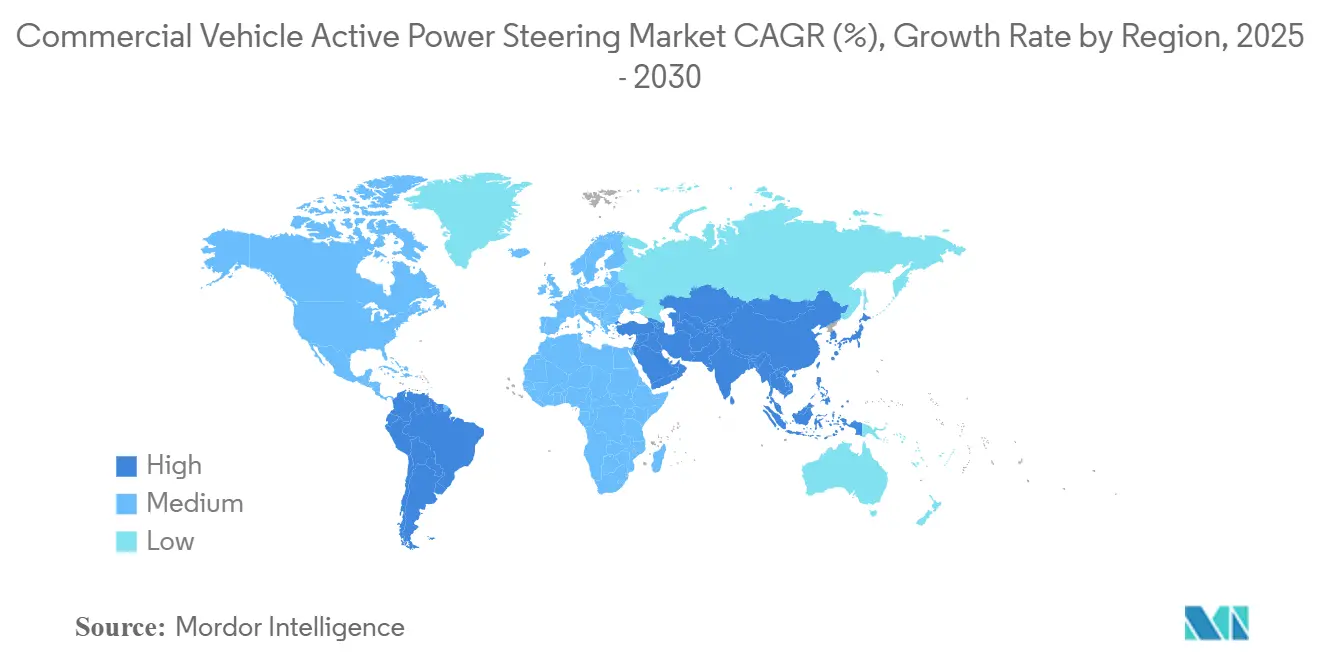

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Vehicle Active Power Steering Market Analysis by Mordor Intelligence

The Commercial Vehicle Active Power Steering market size stands at USD 6.57 billion in 2025 and is projected to reach USD 14.80 billion in 2030, translating to a 12.63% CAGR. Electrification mandates, stringent CO₂ standards, and the need for ADAS-compatible architectures propel rapid technology migration from hydraulic to electric and steer-by-wire solutions. OEMs view electric assistance as an immediate route to fuel-economy gains because it removes the parasitic load of engine-driven pumps. At the same time, fleet operators report measurable reductions in driver fatigue and maintenance downtime. Semiconductor reliability improvements and the arrival of 48 V power domains unlock higher output torque, allowing electric systems to serve heavier trucks that once relied exclusively on hydraulic gear. Competitive intensity rises as tier-1 steering suppliers expand into software-defined steering domains and vertically integrate electronics to buffer supply disruptions.

Key Report Takeaways

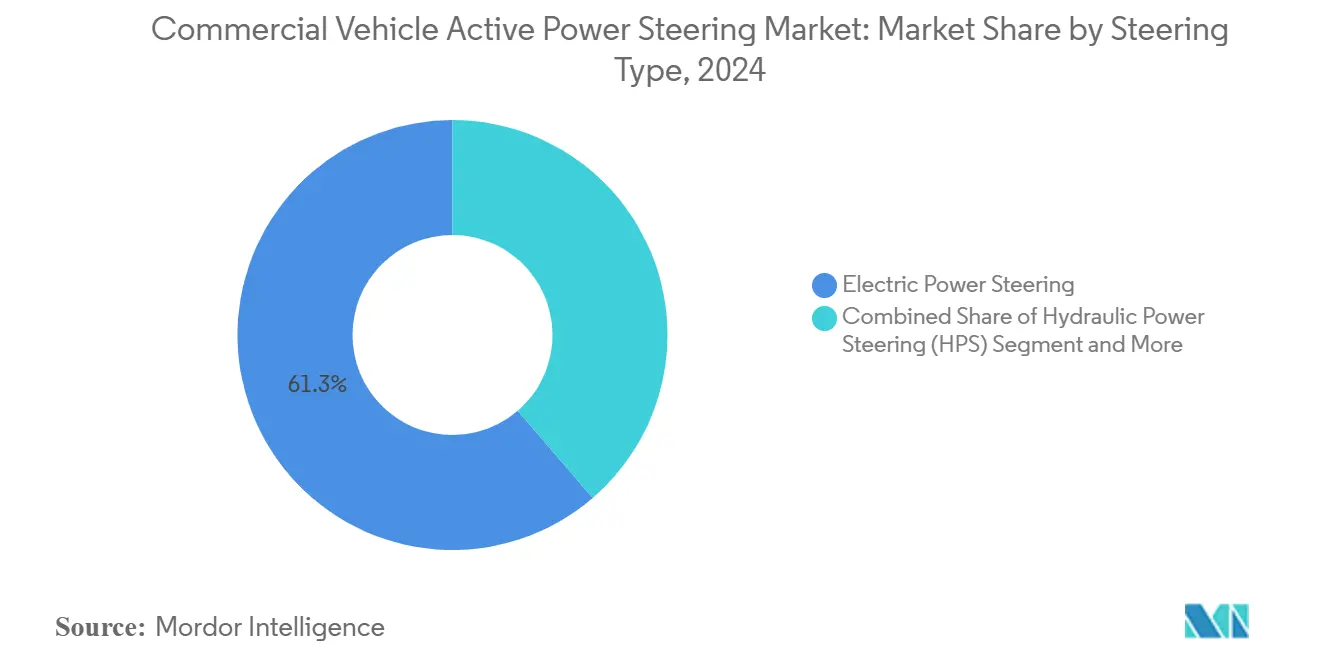

- By steering type, Electric Power Steering led with 61.32% revenue share in 2024; steer-by-wire EPS is forecast to expand at an 18.45% CAGR through 2030.

- By equipment, the Steering Gear held a 34.68% share of the Commercial Vehicle Active Power Steering market in 2024; sensors record the highest projected CAGR at 11.63% to 2030.

- By vehicle type, Passenger Vehicles accounted for 52.03% of the Commercial Vehicle Active Power Steering market share in 2024, while Medium & Heavy Commercial Vehicles are advancing at a 6.81% CAGR.

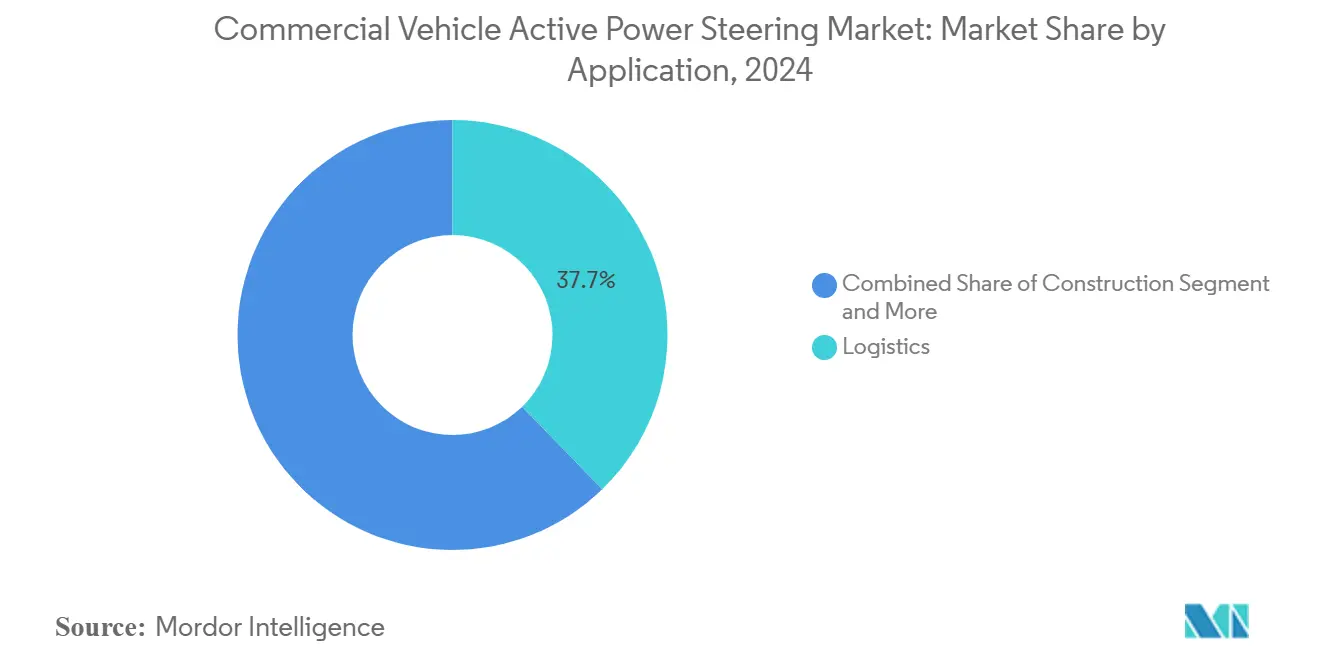

- By application, Logistics commanded a 41.52% share in 2024; Public Transport is poised for the fastest growth at 9.72% CAGR through 2030.

- OEM sales captured 73.04% of 2024 revenue by distribution channel; the Aftermarket segment is forecast to rise at an 8.21% CAGR.

Global Commercial Vehicle Active Power Steering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of ADAS-Ready EPS Architectures | +2.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Stricter Global CO₂/Fuel-Efficiency Rules | +2.1% | Global, led by EPA Phase 3 and EU standards | Short term (≤ 2 years) |

| Fleet Electrification Targets in Logistics | +1.9% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| OEM Shift to 48-V Power Domains | +1.4% | Global, with faster adoption in premium segments | Long term (≥ 4 years) |

| Steering-by-Wire Pilot Programs in HD Trucks | +1.2% | North America and EU, limited Asia-Pacific trials | Long term (≥ 4 years) |

| Regional Retro-Fit Mandates for City Buses | +0.9% | EU (London DVS), select Asia-Pacific cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of ADAS-ready EPS Architectures

Integrating Advanced Driver Assistance Systems with electric power steering represents a fundamental shift in commercial vehicle architecture, enabling features like lane-keeping assistance and collision avoidance that require precise torque overlay capabilities. EU General Safety Regulations mandating Steering Assistance Systems and Emergency Lane Keeping Systems for newly manufactured trucks and buses from July 2024 have accelerated this transition[1]"Mandatory safety systems and new rules for trucks and vans from 7 July," trans.info.. The technical complexity lies in achieving ISO 26262 functional safety compliance while maintaining the robustness required for commercial duty cycles. Nexteer's High Output Column-Assist EPS, launched in April 2025 with torque capability up to 110 Nm, exemplifies this evolution by extending electric assistance into heavier vehicle segments previously dominated by hydraulic systems[2]"Nexteer Expands Portfolio With High Output Column-Assist Electric Power Steering," Manila Times, manilatimes.net.. The convergence of steering and ADAS creates network effects where steering system selection increasingly influences broader vehicle architecture decisions, particularly regarding sensor fusion and fail-safe redundancy.

Stricter Global CO₂/Fuel-Efficiency Rules

Regulatory pressure for emissions reduction is reshaping steering system economics, with electric power steering offering measurable fuel economy benefits that directly address compliance requirements. The EPA's Phase 3 Heavy-Duty Vehicle Standards require CO₂ emissions reductions of up to 50% for certain vehicle categories by 2032, making every efficiency gain critical for OEM compliance strategies[3]"Final Rule: Greenhouse Gas Emissions Standards for Heavy-Duty Vehicles – Phase 3," U.S. Environmental Protection Agency (EPA), epa.gov.. Electric power steering eliminates the continuous parasitic load of engine-driven hydraulic pumps, delivering fuel savings of 2-4% in typical long-haul applications. This efficiency advantage becomes more pronounced in stop-and-go urban delivery cycles where hydraulic systems operate at peak load during frequent maneuvering. The regulatory timeline creates urgency for commercial vehicle manufacturers, as non-compliance penalties can exceed USD 10,000 per vehicle, compelling the business case for EPS adoption despite higher upfront costs.

Fleet Electrification Targets in Logistics

Commercial fleet operators are accelerating electric power steering adoption as part of broader electrification strategies, driven by total cost of ownership advantages and operational efficiency gains. Major logistics operators report that electric steering systems reduce driver fatigue by up to 30% compared to hydraulic alternatives, directly impacting productivity in multi-shift operations. The integration benefits extend beyond individual vehicle performance, as electric steering systems enable fleet management capabilities like remote diagnostics and predictive maintenance that reduce unscheduled downtime. China's aggressive urban electrification mandates for commercial vehicles create a template that other regions are beginning to follow, with several major cities implementing zero-emission delivery zones that effectively require electric powertrains and compatible steering systems. The network effects of fleet adoption create economies of scale that benefit the broader market, as volume commitments from large logistics operators justify supplier investments in next-generation steering technologies.

OEM shift to 48-V power domains

In the Commercial Vehicle Active Power Steering Market, the OEM shift to 48‑V power domains is emerging as a key growth driver. This transition enables more efficient electrical systems, reduces energy consumption, and supports integrating advanced driver-assistance features. By adopting 48‑V architectures, commercial vehicle manufacturers can enhance steering responsiveness, improve fuel efficiency, and meet increasingly stringent emissions regulations, while also providing the electrical headroom necessary for future electrification and hybridization initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and Validation Cost, Reliability Concerns in Harsh Duty-Cycles | -1.6% | Global, with heightened impact in commercial and heavy-duty segments | Medium term (2–4 years) |

| Hydraulic-EPS Cost Parity Still Distant in Emerging Markets | -1.4% | Asia-Pacific, Latin America, and Middle East | Long term (≥ 4 years) |

| Cost of SBW | -1.8% | Global, particularly affecting smaller OEMs | Long term (≥ 4 years) |

| Semiconductor Supply-Chain Volatility | -1.3% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D and Validation Cost of Steer-by-Wire

The development and validation costs for steer-by-wire systems present significant barriers to market expansion, particularly for smaller commercial vehicle manufacturers lacking the resources for extensive testing programs. Functional safety requirements under ISO 26262 demand comprehensive hazard analysis and risk assessment, with validation costs often exceeding USD 50 million for a complete steer-by-wire program across multiple vehicle platforms. The technical complexity of eliminating mechanical backup systems while maintaining fail-safe operation requires dual-redundant electronic architectures and extensive real-world validation across diverse operating conditions. UK Vehicle Certification Agency guidance on steer-by-wire compliance for Individual Vehicle Approval highlights the regulatory complexity, with requirements for comprehensive documentation of failure modes and control system integrity. These barriers create a two-tier market where established suppliers with deep R&D resources can advance steer-by-wire technology while smaller players remain dependent on conventional electric power steering architectures.

Semiconductor Supply-Chain Volatility

Ongoing semiconductor shortages continue to constrain commercial vehicle active power steering production, with lead times for critical control units extending beyond 52 weeks in some cases. Electric power steering systems require multiple semiconductor components, including torque sensors, position encoders, and electronic control units, making them particularly vulnerable to supply chain disruptions. The concentration of semiconductor manufacturing in Asia-Pacific creates geographic risk, as regional disruptions can cascade through global commercial vehicle production networks. Suppliers respond through vertical integration and dual-sourcing strategies, but these adaptations require significant capital investment and longer-term supply agreements that may increase system costs in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Steering Type: Electric Dominance Accelerates Steer-by-Wire Transition

Electric Power Steering commands 61.32% market share in 2024, reflecting the technology's maturation and cost-competitiveness relative to hydraulic alternatives, while Steer-by-Wire EPS emerges as the fastest-growing segment with 18.45% forecast CAGR through 2030. The transition from hydraulic to electric assistance has reached an inflection point where electric systems offer superior total cost of ownership despite higher initial investment, driven by reduced maintenance requirements and energy efficiency gains. Hydraulic Power Steering maintains relevance in heavy-duty applications where extreme torque requirements exceed current electric capabilities, though this segment faces pressure from high-output electric alternatives like Nexteer's 110 Nm column-assist system launched in April 2025.

Electro-Hydraulic Power Steering represents a transitional technology that combines electric control with hydraulic actuation, offering a pathway for manufacturers to adopt electronic steering control while leveraging existing hydraulic infrastructure. ZF's recent production launch of steer-by-wire systems for NIO's commercial vehicle platform in February 2025 demonstrates the technology's commercial readiness, though adoption remains limited by validation requirements and regulatory approval timelines. The steering type segmentation reflects broader industry dynamics where technological advancement creates market fragmentation before eventual consolidation around dominant architectures, with steer-by-wire positioned to capture increasing share as autonomous driving requirements drive demand for fully electronic steering control.

By Equipment: Sensors Drive Intelligence Integration

Steering Gear dominates equipment segmentation with 34.68% market share in 2024, representing the mechanical foundation that translates steering inputs into wheel movement, while Sensors emerge as the fastest-growing segment at 11.63% CAGR, driven by the proliferation of torque sensors, position feedback systems, and redundant safety monitoring required for advanced steering architectures. The sensor growth trajectory reflects the transformation of steering from a purely mechanical system to an intelligent subsystem that provides real-time feedback for vehicle dynamics control and autonomous driving functions. Modern commercial vehicle steering systems integrate multiple sensor types, including non-contact torque sensors, steering angle sensors, and motor position encoders, that enable precise control and diagnostic capabilities.

Steering Columns and Steering Wheels represent mature segments with steady growth aligned with overall vehicle production. However, both categories are experiencing technological evolution as manufacturers integrate driver monitoring systems and haptic feedback capabilities. The equipment segmentation reveals the increasing complexity of modern steering systems, where traditional mechanical components are augmented with electronic intelligence that enables integration with broader vehicle safety and automation systems. This trend toward sensor-rich steering architectures creates opportunities for specialized component suppliers while challenging traditional mechanical suppliers to develop electronic capabilities or risk market share erosion.

By Vehicle Type: Heavy Commercial Vehicles Accelerate Adoption

Passenger Vehicles currently dominate with 52.03% market share in 2024, reflecting the earlier adoption of electric power steering in lighter vehicle segments where power requirements and validation complexity are more manageable, yet Medium & Heavy Commercial Vehicles represent the fastest-growing segment at 6.81% CAGR as operators recognize the operational benefits of active steering in demanding duty cycles. The vehicle type dynamics illustrate a market in transition, where commercial vehicle adoption lags passenger cars by several years but accelerates rapidly once the technology proves reliable in commercial applications. Light Commercial Vehicles serve as a bridge segment, adopting passenger car steering technologies while addressing the unique requirements of commercial duty cycles, including higher mileage, diverse operating conditions, and extended service intervals.

The growth trajectory in heavy commercial vehicles reflects several converging factors including regulatory mandates for advanced safety systems, fleet operator recognition of driver fatigue reduction benefits, and the integration requirements of autonomous driving systems being piloted in commercial applications. Transport for London's Direct Vision Standard requirements, which mandate enhanced safety systems for heavy goods vehicles operating in London, exemplify regulatory drivers that accelerate active steering adoption in commercial segments. The vehicle type segmentation suggests that commercial vehicle active power steering adoption will accelerate as regulatory requirements expand and fleet operators quantify the total cost of ownership benefits including reduced driver turnover and improved safety performance.

By Application: Public Transport Leads Growth Trajectory

Logistics applications command 41.52% market share in 2024, reflecting the segment's size and early adoption of efficiency-enhancing technologies, while Public Transport emerges as the fastest-growing application at 9.72% CAGR driven by urban mobility initiatives and the integration of autonomous shuttle programs in major metropolitan areas. The application segmentation reveals distinct adoption patterns where logistics operators prioritize fuel efficiency and driver comfort benefits, while public transport authorities focus on safety enhancements and passenger experience improvements. Construction applications maintain steady demand driven by the harsh operating conditions that benefit from active steering's ability to reduce operator fatigue and improve precision in confined spaces.

Hübner's Articulated Bus Steering Control system, launched at InnoTrans 2022, demonstrates the technological sophistication emerging in public transport applications, with electronically controlled multi-axle steering that enables 36-meter bi-articulated buses to operate on normal roads without special guidance infrastructure. The application dynamics suggest that public transport will drive innovation in active steering technologies due to the segment's willingness to adopt advanced systems for safety and operational efficiency, creating technology spillover effects that benefit other commercial vehicle applications as costs decline and reliability improves through volume production.

By Distribution Channel: Aftermarket Gains Momentum

OEM channels dominate with 73.04% market share in 2024, reflecting the integration requirements of modern active power steering systems that necessitate factory installation and calibration, while Aftermarket channels represent the fastest-growing segment at 8.21% CAGR, driven by retrofit opportunities in existing commercial vehicle fleets and the emergence of modular steering solutions designed for field installation. The distribution channel dynamics reflect the maturation of active steering technology, where early adoption focused on new vehicle integration, but expanding applications create retrofit opportunities for fleet operators seeking to upgrade existing assets. Regulatory mandates like New York's Divisible Load Notice, requiring steerable lift axle retrofits for certain commercial vehicles, demonstrate how policy changes can create sudden aftermarket demand.

The aftermarket growth trajectory benefits from the development of modular steering systems that simplify installation and reduce integration complexity, enabling fleet operators to upgrade vehicles without extensive factory modifications. This trend toward modularity creates opportunities for specialized aftermarket suppliers while challenging OEM suppliers to develop retrofit-friendly products that capture aftermarket value rather than ceding it to third-party providers. The distribution channel segmentation suggests that successful active steering suppliers will need dual-channel strategies that address both OEM integration requirements and aftermarket accessibility to maximize market penetration.

Geography Analysis

Asia-Pacific dominates the Commercial Vehicle Active Power Steering market with a 48.25% share in 2024. It leads growth projections at 8.91% CAGR through 2030, driven by China's aggressive commercial vehicle electrification mandates and the region's concentration of manufacturing capacity. The region's growth momentum reflects several converging factors, including government policies favoring electric commercial vehicles, the emergence of domestic steering system suppliers, and massive infrastructure investments that create demand for advanced commercial vehicle technologies. ZF's expansion into Chinese commercial vehicle markets, including partnerships for steer-by-wire production with NIO, demonstrates how established suppliers adapt to regional dynamics while local manufacturers develop competitive capabilities. India's development of cost-effective electric power assist steering systems specifically tuned to local road conditions and topography illustrates the region's focus on appropriate technology adaptation rather than direct technology transfer.

North America and Europe represent mature markets with established regulatory frameworks and sophisticated commercial vehicle fleets that drive demand for advanced steering technologies. The EPA's Phase 3 Heavy-Duty Vehicle Standards and EU General Safety Regulations create regulatory pull for active steering adoption, while established suppliers like Bosch, ZF, and Nexteer maintain technological leadership through continuous R&D investment. These regions exhibit different adoption patterns, with North America emphasizing long-haul efficiency benefits while Europe focuses on urban mobility and safety enhancements driven by city-specific regulations like London's Direct Vision Standard. The geographic segmentation reveals a multi-speed market where regulatory maturity and economic development levels influence both adoption timing and technology requirements, creating opportunities for suppliers that can adapt their offerings to regional preferences and regulatory environments.

South America, the Middle East, and Africa represent emerging markets with significant growth potential but face challenges, including cost sensitivity, infrastructure limitations, and regulatory development gaps that slow active steering adoption. These regions typically lag developed markets by 3-5 years in commercial vehicle technology adoption but offer substantial volume opportunities as economic development accelerates and regulatory frameworks mature. The geographic dynamics suggest that successful market penetration requires region-specific strategies that balance technological advancement with cost constraints while anticipating regulatory evolution that will eventually drive active steering adoption across all major commercial vehicle markets.

Competitive Landscape

The Commercial Vehicle Active Power Steering market exhibits moderate concentration, with established tier-1 suppliers maintaining technological leadership while facing pressure from emerging regional players and semiconductor supply chain constraints reshaping competitive dynamics. Market leaders, including Bosch, ZF Friedrichshafen, and Nexteer Automotive, leverage their R&D capabilities and OEM relationships to advance steer-by-wire technologies and high-output electric systems. However, the competitive landscape is evolving as traditional boundaries between steering, electronics, and software blur. Patent analysis reveals intensive innovation activity in steering system intelligence. IEEE documentation shows significant patent filings focused on neural network integration, adaptive control algorithms, and sensor fusion technologies that enable autonomous driving compatibility.

Emerging competitive threats include vertical integration by commercial vehicle OEMs seeking to control critical technologies and the entry of semiconductor companies developing integrated steering control solutions that challenge traditional supplier relationships. The competitive intensity is amplified by regulatory requirements for ISO 26262 functional safety compliance, which creates barriers to entry while enabling established suppliers with validation expertise to maintain market position. Technology convergence creates white-space opportunities in areas like predictive maintenance, fleet management integration, and autonomous vehicle steering systems, where traditional automotive suppliers compete with technology companies and software developers. The competitive landscape suggests that long-term success requires balancing mechanical engineering expertise with electronic and software capabilities, as steering systems evolve from mechanical components to intelligent subsystems that enable broader vehicle automation and connectivity.

Commercial Vehicle Active Power Steering Industry Leaders

-

Robert Bosch GmbH

-

JTEKT Corporation

-

ZF Friedrichshafen AG

-

Nexteer Automotive

-

NSK Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nexteer Automotive launched High Output Column-Assist Electric Power Steering (HO CEPS) with torque capability up to 110 Nm, extending electric steering into heavier commercial vehicle segments previously dominated by hydraulic systems and enabling broader EPS adoption across vehicle platforms.

- February 2025: ZF Friedrichshafen began production of steer-by-wire systems for NIO's commercial vehicle platform, marking a significant milestone in the commercialization of fully electronic steering for heavy-duty applications and demonstrating technology readiness for autonomous driving integration.

Global Commercial Vehicle Active Power Steering Market Report Scope

| Hydraulic Power Steering (HPS) |

| Electric Power Steering (EPS) |

| Electro-Hydraulic Power Steering (EHPS) |

| Steering Racks |

| Steering Columns |

| Steering Wheels |

| Others |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Logistics |

| Construction |

| Public Transport |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Steering Type | Hydraulic Power Steering (HPS) | |

| Electric Power Steering (EPS) | ||

| Electro-Hydraulic Power Steering (EHPS) | ||

| By Equipment | Steering Racks | |

| Steering Columns | ||

| Steering Wheels | ||

| Others | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Application | Logistics | |

| Construction | ||

| Public Transport | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What value does electric power steering add in heavy-duty trucks?

It removes engine-driven pump losses, saving up to 4% fuel while reducing driver effort, which shortens payback to under two years in long-haul fleets.

How will the steer-by-wire roll-out timeline look?

Pilot fleets are on the road in 2025, and OEMs plan volume production after 2027 once ASIL D validation completes.

Which region leads adoption of active power steering?

Asia-Pacific leads with 48.25% 2024 revenue and the fastest 8.91% CAGR due to strong electrification mandates.

Why are sensors the fastest-growing equipment segment?

Steer-by-wire and ADAS integration require torque, angle, and position feedback, driving an 11.63% CAGR for sensor content.

Can existing trucks be upgraded?

Yes, aftermarket kits with modular electric assist units allow retrofit during regular maintenance, and the segment grows at 8.21% CAGR.

What is the main supply-chain risk?

Semiconductor shortages lengthen ECU lead times beyond 50 weeks, prompting suppliers to dual-source or vertically integrate chip production.

Page last updated on: