Traction Inverter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 11.12 Billion |

| Market Size (2030) | USD 24.74 Billion |

| Growth Rate (2025 - 2030) | 17.34% CAGR |

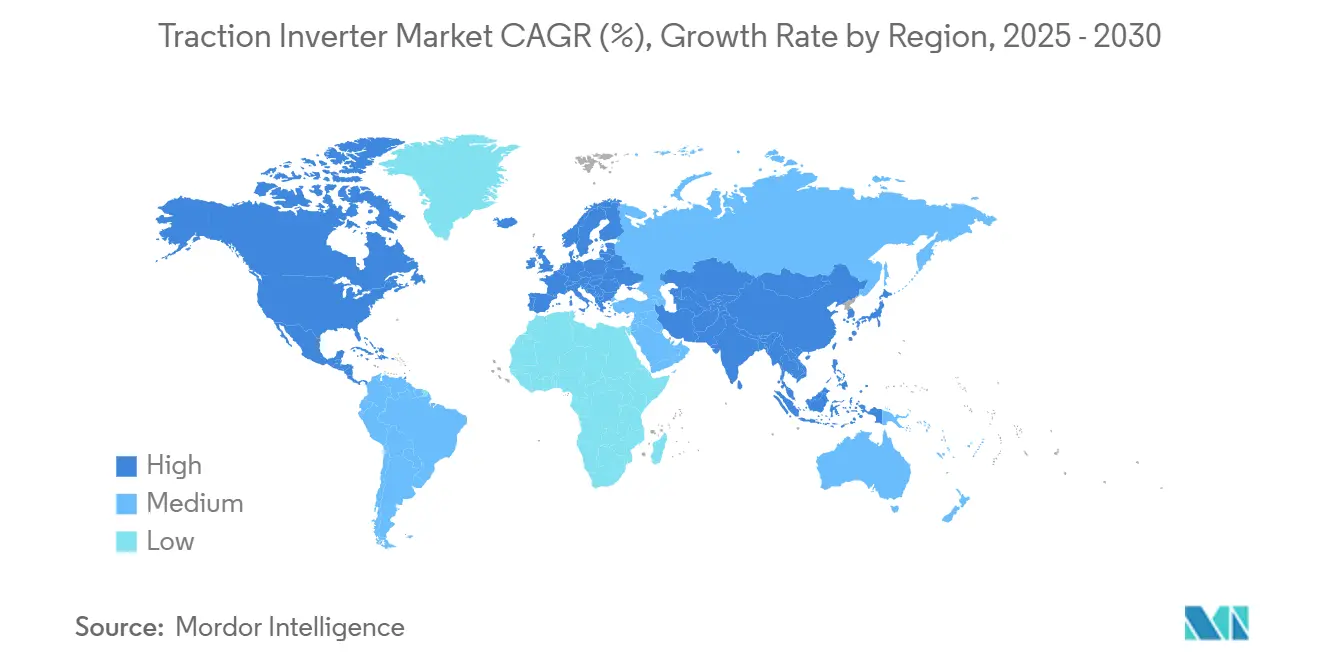

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

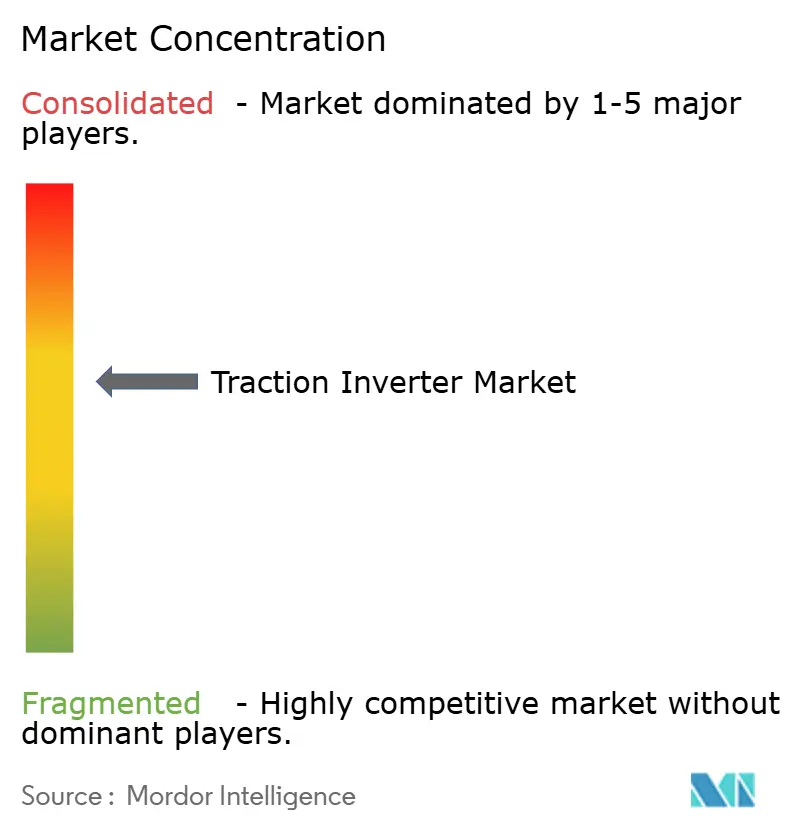

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Traction Inverter Market Analysis by Mordor Intelligence

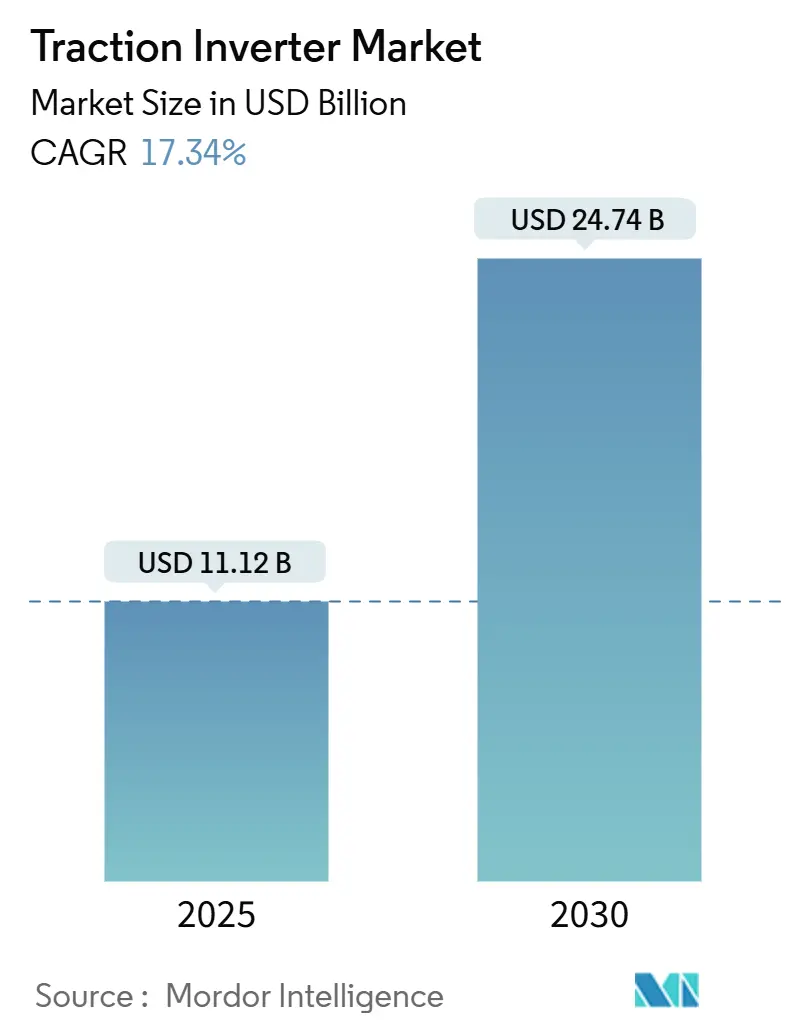

The global traction inverter market size is valued at USD 11.12 billion in 2025 and is forecast to expand to USD 24.74 billion by 2030, advancing at a 17.34% CAGR during the forecast period (2025-2030). Rising zero-emission mandates, rapid silicon-carbide (SiC) penetration, and a migration toward integrated e-axle architectures are shaping demand and product design. Battery Electric Vehicles (BEVs) hold dominant volumes, SiC modules steadily erode insulated-gate bipolar transistor (IGBT) leadership, and 800 V-plus platforms are scaling beyond premium portfolios. Geographic momentum remains anchored in Asia-Pacific. Middle East and Africa’s early-stage programs post the fastest growth, while government incentives in North America and Europe sustain policy-driven volume visibility. Competition intensifies as incumbent automotive suppliers, pure-play power-electronics firms, and emerging Chinese manufacturers race to deliver smaller, lighter, and more efficient assemblies that comply with functional-safety and cybersecurity mandates.

Key Report Takeaways

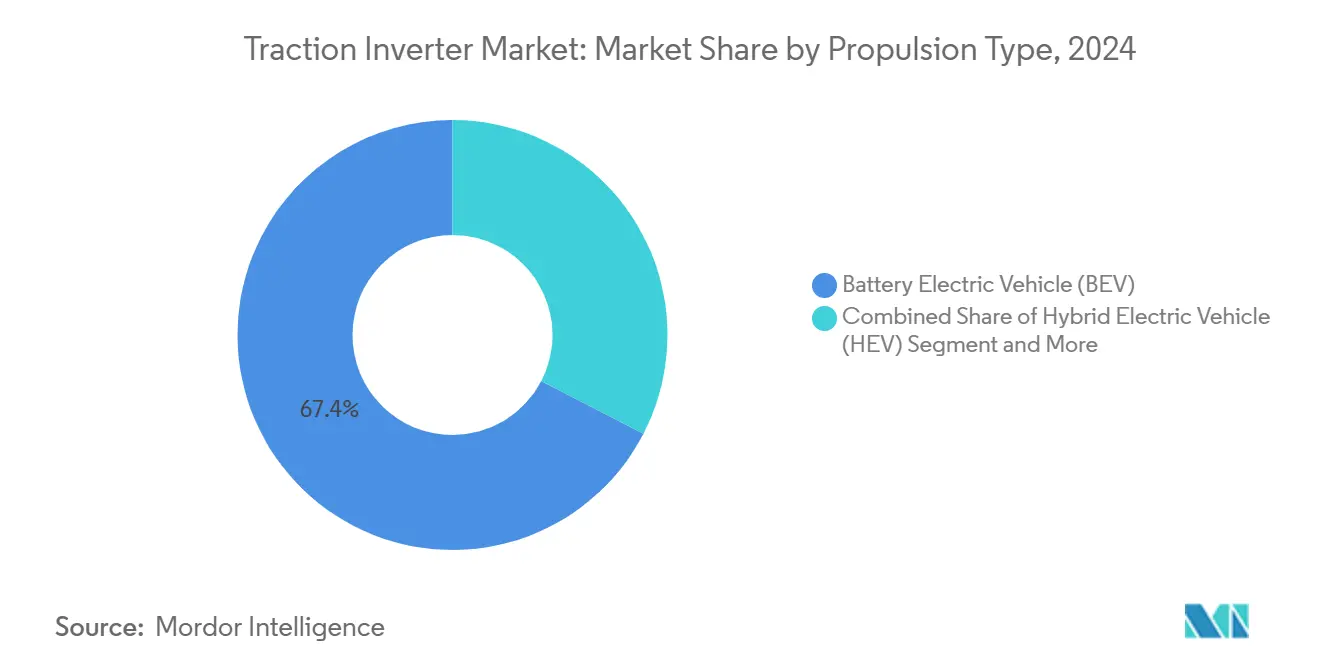

- By propulsion type, Battery Electric Vehicles captured a 67.44% share of the traction inverter market in 2024. In contrast, Fuel Cell Electric Vehicles are projected to expand at a 20.15% CAGR during the forecast period (2025-2030).

- By voltage range, 201 V—900 V systems accounted for 55.03% share of the traction inverter market in 2024; platforms operating above 900 V are forecasted to advance at a 19.05% CAGR during the forecast period (2025-2030).

- By technology, IGBT modules led the traction inverter market with a 56.18% share in 2024, while SiC modules are expected to be poised with a 17.85% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars held a 63.05% share of the traction inverter market in 2024, and low-speed vehicles are expected to rise at an 18.65% CAGR during the forecast period (2025-2030).

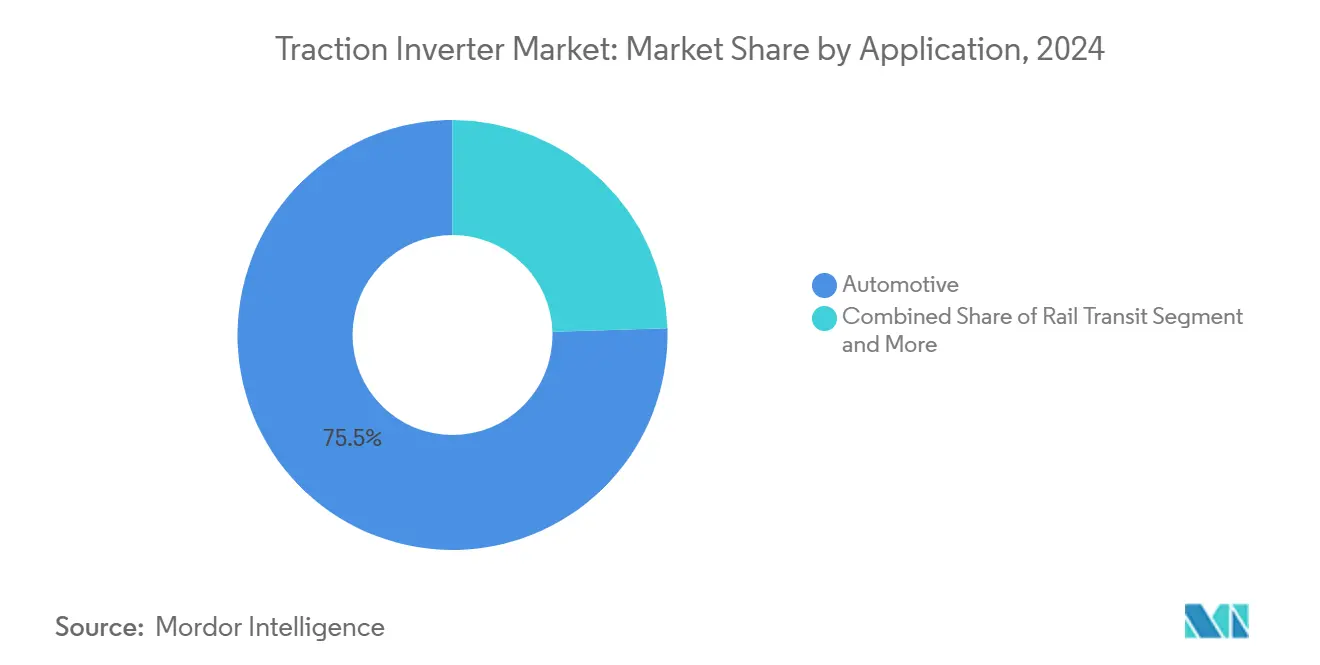

- By application, automotive accounted for a 75.48% share of the traction inverter market in 2024; industrial mobility is expected to register the highest CAGR at 18.33% during the forecast period (2025-2030).

- By distribution channel, OEM routes dominated at 90.25% share of the traction inverter market in 2024, whereas the aftermarket is expected to climb at a 19.25% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific led with 46.13% oshare of the traction inverter market in 2024, and the Middle East & Africa is expected to post an 18.04% CAGR during the forecast period (2025-2030).

Global Traction Inverter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Zero-Emission Mandates and Incentives | +3.2% | EU, China, California, expanding globally | Medium term (2-4 years) |

| Declining SiC Power Module Costs | +2.8% | Asia-Pacific hubs, spreading worldwide | Long term (≥ 4 years) |

| OEM Shift to E-Axle Architecture | +2.5% | Global with early uptake in premium segments | Medium term (2-4 years) |

| Rail Electrification and Metro Projects | +2.1% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Demand for Bidirectional V2G Functionality | +1.8% | North America and EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Growth in Low-Voltage Micro-Mobility | +1.4% | Asia-Pacific and Europe, urban centers worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives and Zero-Emission Mandates

Regulatory packages such as the European Union’s Fit for 55 framework and China’s New Energy Vehicle quota system are locking in future electric-vehicle volumes, thereby guaranteeing multi-year demand for traction inverters. California’s Advanced Clean Cars II extends requirements to heavy-duty fleets, widening inverter use cases into high-power commercial platforms [1]“Advanced Clean Cars II,” California Air Resources Board, Ca.gov. These policies synchronize infrastructure and vehicle rollouts, accelerating time-to-scale while forcing suppliers to boost capacity in advance of market pull. Functional-safety certification under ISO 26262 further fortifies incumbent positions, creating high entry barriers for new players.

Declining Cost and Higher Efficiency of SiC Power Modules

SiC devices now approach cost parity with legacy silicon solutions as wafer production ramps and planar designs migrate to trench architectures that raise cell density. Infineon’s SiC modules in Xiaomi’s SU7 sedan demonstrate range gains of around 5% versus equivalent IGBT designs, validating a clear efficiency premium [2]“Infineon SiC Power Modules Extend EV Driving Range,” Infineon Technologies AG, Infineon.com. China-based wafer producers have trimmed SiC substrate cost shares and are projected to reduce further, widening applicability to mid-segment vehicles. The ability to operate at junction temperatures approaching 600 °C reduces cooling mass and unlocks tighter packaging, factors now prized by OEMs chasing higher energy density.

OEM Shift Toward Integrated E-Axle Architectures

Global automakers are collapsing discrete motor, gearbox, and inverter components into sealed e-axle assemblies, shrinking weight and bill-of-material counts. Dana’s TM4-Spicer solution showcased at Bauma 2025 underscores supply-side migration toward one-box propulsion units. Close proximity of power electronics and motor windings demands improved thermal coupling and electromagnetic shielding, elevating design complexity and favoring tier-ones with multidisciplinary expertise.

Investments in Rail Electrification and Metro Projects

India’s rail electrification milestone and metro build-outs from Kuala Lumpur to Boston propel megawatt-class inverter demand that commands higher price points than passenger-car units. Infineon’s 3.3 kV SiC module, tailored for rolling stock, cuts energy use over incumbent silicon variants and lowers acoustic noise for commuter comfort. Rail contracts typically run 30 years, embedding long-term spares revenue while requiring superior reliability profiles compared with automotive duty cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Bottlenecks | –2.1% | Global, most acute in Europe and North America | Short term (≤ 2 years) |

| High R&D for Small OEMs | –1.8% | Global, particularly emerging-market participants | Medium term (2-4 years) |

| EMI Compliance in E-Axles | –1.2% | Global, stricter in the EU and North America | Medium term (2-4 years) |

| Inverter Firmware Cyber-Security Uncertainty | –0.9% | Global, varying standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Substrate Supply-Chain Bottlenecks

Demand for devices continues to outpace the capacity of SiC substrates, creating a significant and persistent supply-demand gap. The transition to 6 to 8 inch wafers faces challenges due to lower yields, which not only increase production costs but also complicate efforts to scale manufacturing processes effectively. Additionally, automotive qualifications introduce a delay of 18-24 months between wafer fab announcements and the commencement of production. This extended timeline exacerbates planning risks for inverter manufacturers, who are often locked into multi-year supply agreements. These manufacturers must carefully manage uncertainties in supply chain dynamics, production schedules, and cost structures to mitigate potential disruptions.

High R&D and Validation Costs for Small OEMs

Multi-million-dollar test matrices, largely fixed irrespective of volume, are driven by regulations like ISO 26262, CISPR 25, and UNECE's cybersecurity mandates. These regulations require extensive testing to ensure compliance, significantly increasing operational costs. New entrants grapple with prohibitive capital outlays, leading to industry consolidation as larger players spread costs across multiple platforms. This dynamic creates a competitive advantage for established companies, enabling them to leverage economies of scale, maintain market dominance, and invest further in innovation and compliance capabilities. Additionally, the stringent regulatory environment acts as a barrier to entry, discouraging smaller firms from entering the market and fostering a landscape where only well-capitalized players can thrive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEVs Drive Volume Growth

BEVs owned a 67.44% share of the traction inverter market in 2024, as falling battery costs aligned with expanding charge infrastructure. Fuel Cell Electric Vehicles log the fastest 20.15% CAGR during the forecast period (2025-2030), led by heavy trucks that value hydrogen’s gravimetric energy density. Hybrid and plug-in hybrid alternatives continue where grid access remains hindered. The traction inverter market benefits as BEV architectures standardize around 3-in-1 e-axle units, simplifying assembly and trimming system weight. Infineon’s long-term SiC supply contract with Stellantis underscores large-scale OEM alignment toward all-electric drivetrains.

Adoption scatter follows policy intensity; China pushes BEV exclusivity, Europe favors transitional PHEVs until charging penetration rises, and North America hosts a mosaic of BEV and hybrid demand responsive to regional incentives. FCEV duty cycles command higher power ratings that lift average selling prices for inverters compared with passenger BEVs, creating a value pool for specialist suppliers versed in combined fuel-cell and traction control strategies.

By Voltage Range: 800 V Systems Gain Momentum

The 201 V-900 V tranche commanded a 55.03% share of the traction inverter market in 2024. Platforms exceeding 900 V are expected to post a 19.05% CAGR during the forecast period (2025-2030), reflecting OEM pursuits of sub-20-minute fast charge. Elevated voltage halves current for equal power, shrinking copper cross-section requirements and boosting efficiency. Higher voltage also magnifies transient immunity needs, sparking demand for 1,200 V SiC MOSFETs such as those adopted by Forvia Hella.

Premium automakers pioneered the jump to 800 V, yet cost-down roadmaps funnel the architecture into mid-segment crossovers. Conversely, low-voltage ranges under 200 V retain relevance for micro-mobility fleets and auxiliary drives, though their monetary share steadily slips as automobiles dominate the shipment mix.

By Technology: SiC Modules Disrupt IGBT Dominance

IGBTs retained a 56.18% share of the traction inverter market in 2024, fortified by mature supply chains and proven reliability. SiC modules, however, notch a 17.85% CAGR during the forecast period (2025-2030), eroding silicon’s edge as wafer prices retreat. BorgWarner’s SiC agreement with onsemi exemplifies the volume turning point [3]“BorgWarner Signs Billion-Euro SiC Deal,” onsemi, Onsemi.com. Thermal tolerance up to 600 °C reduces cooling mass, while triple-the-frequency capability allows smaller magnetics, cutting inverter size.

MOSFET-based solutions persist in low-power or ultrafast-switch genres where SiC cost remains premium and IGBT speed is insufficient. Over the forecast window, desktop simulation suites and AI-driven design tools accelerate concurrent hardware-software optimization, lifting entry requirements for latecomers.

By Vehicle Type: Commercial Segments Show Promise

Passenger cars contributed a 63.05% share of the traction inverter market in 2024, and low-speed vehicles are expected to emerge at an 18.65% CAGR during the forecast period (2025-2030), propelled by e-scooters and compact delivery platforms that suit congested megacities. Commercial truck and off-highway equipment adoption accelerates as total cost-of-ownership math swings in favor of electrification, aided by depot-based charging ecosystems.

Passenger-car scale pushes down per-kilowatt pricing, triggering spill-over cost benefits for vocational segments that often require bespoke thermal or environmental ruggedization. Rail traction maintains steady replacement cycles yet commands premium invoices owing to stringent 30-year service life and megawatt power levels.

By Application: Industrial Mobility Emerges

Automotive captured a 75.48% share of the traction inverter market in 2024, mirroring the light-vehicle production base. Industrial mobility, covering forklifts, construction, and agricultural machinery, is expected to lead growth at an 18.33% CAGR during the forecast period (2025-2030), as emission stipulations sharpen in urban zones and Tier IV diesel norms tighten. Operators value electrified drivetrains for quiet operation, lower maintenance, and regenerative braking benefits during repetitive cycles.

Rail transit inverters contribute selectively but at higher ASPs, reflecting distinctive safety and redundancy requirements. Off-highway electrification leverages modular packs and inverter configurations adapted from passenger cars yet up-engineered for dust, vibration, and thermal extremes.

By Distribution Channel: Aftermarket Gains Traction

OEM procurement streams held a 90.25% share of the traction inverter market in 2024, because traction inverters ship pre-calibrated for specific vehicle control strategies. As cumulative EV fleets age, the aftermarket segment is expected to rise with a 19.25% CAGR during the forecast period (2025-2030), particularly for commercial vehicles with usage-intensive duty cycles. OE-authorized parts dominate near-term replacement, but independent remanufacturers are beginning to reverse-engineer legacy models, a trend that could diversify channel mix post-2030.

Warranty considerations and cybersecurity lockdowns currently restrict third-party servicing; nonetheless, open-diagnostic standards may loosen barriers, echoing historical patterns in internal-combustion powertrain support.

Geography Analysis

Asia-Pacific holds a 46.13% share of the traction inverter market in 2024. The contribution reflects China’s manufacturing scale, predictable domestic demand under a mandated 40% electrified-sales target for 2030, and ready access to SiC wafers that compress cost baselines. Japan and South Korea inject design leadership, notably in high-frequency motor control and functional-safety firmware. India’s indigenous rail-electrification drive and expanding two-wheeler market underpin incremental inverter shipments that favor ruggedized, low-voltage topologies. Policy packages offering purchase subsidies, import-duty waivers, and production-linked incentives foster assembly and component localization, anchoring long-term regional dominance.

Europe upholds stringent CISPR 25 electromagnetic standards and ISO 26262 protocols that elevate technical entry thresholds. Germany’s luxury OEM cohort specifies 800 V SiC architectures to secure rapid-charge parity with internal combustion refuel times, elevating average inverter content per vehicle. Supply security themes encourage dual sourcing between European fabs and Asian foundries, evidenced by Infineon’s multi-billion-euro Kulim expansion and collaboration with Japanese substrate makers. North America harnesses federal tax credits and state-level zero-emission mandates to spur electrification. U.S. SiC wafer startups and onshore packaging plants receive CHIPS Act incentives, aiming to shorten lead times and dilute Asia-centric supply risk. Canada’s battery-materials corridor and Mexico’s cost-efficient final assembly converge to form an integrated continental supply chain.

Middle East and Africa grows from a low installed base yet posts 18.04% CAGR during the forecast period (2025-2030), as rail and bus fleets electrify in Gulf Cooperation Council metros and North African urban centers. Infrastructure investment programs, exemplified by Saudi Arabia’s public-transport blueprint, carve out future inverter demand. South American clusters, led by Brazil’s low-carbon mobility plan, inch forward, albeit with currency fluctuations and import-tariff considerations that can affect short-term order cadence.

Competitive Landscape

Traction inverter competition remains moderately concentrated; the top five players hold a notable share, while numerous specialists address emerging niches. Bosch, Continental, and DENSO exploit platform longevity, broad thermal-management portfolios, and global logistics to sustain OEM preference. Infineon, onsemi, and Wolfspeed drive upstream power-device leadership that cascades into module-level design wins downstream. Chinese challengers—including BYD Electronics and CRRC Electric—leverage cost-advantaged supply chains and local policy backing to penetrate export markets, often via joint ventures with regional assemblers.

Strategic M&A clarifies a pivot toward full-system capabilities. Hitachi Rail’s purchase of Thales Ground Transportation Systems in 2024 enlarged its traction electronics reach to signaling and cybersecurity, illustrating synergy premiums. Vertical moves also appear: semiconductor producers now directly package inverter subassemblies, shortening supply paths and retaining margin. Integrated e-axle orders incentivize co-development agreements tying inverter, motor, and gearbox suppliers into long-term exclusivity, locking out single-component vendors lacking scale.

Technology roadmaps show steep SiC adoption curves. Continental’s 1200 V SiC inverter for premium SUVs is lighter than its 2020 silicon predecessor and offers 99% peak efficiency, evidencing rapid generational turnover. Software-defined control stacks underpin remote calibration, torque-vectoring features, and cybersecurity patching, strengthening aftermarket service revenues.

Traction Inverter Industry Leaders

Mitsubishi Electric Corporation

Robert Bosch GmbH

Hitachi Astemo Ltd.

Continental AG

BYD Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: onsemi broadened its partnership with Schaeffler, supplying next-generation EliteSiC MOSFETs for an all-new plug-in hybrid platform designed for a global automaker. The SiC-based traction inverter boosts energy efficiency and packaging flexibility.

- May 2025: Arrow Electronics and eInfochips, in collaboration with Vishay eMobility, introduced a low-voltage traction inverter reference design targeting light electric vehicles, including e-bikes, e-scooters, and light commercial vehicles.

- January 2025: Infineon expanded its EiceDRIVER family with ISO 26262-compliant isolated gate drivers optimized for IGBT and SiC modules in xEV traction inverters.

- June 2024: NXP Semiconductors partnered with ZF Friedrichshafen to co-develop SiC-based traction inverter solutions featuring NXP’s GD316x gate drivers that support 800 V platforms.

Global Traction Inverter Market Report Scope

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Low Voltage (24 V - 144 V) up to 200 V |

| 201 V - 900 V |

| Above 900 V |

| IGBT Modules |

| MOSFET Modules |

| SiC Modules |

| Passenger Cars |

| Commercial Vehicles |

| Low-Speed Vehicles |

| Locomotives |

| Metro and Light Rail |

| EMUs and DMUs |

| Automotive |

| Rail Transit |

| Industrial Mobility |

| Off-Highway Equipment |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Voltage Range | Low Voltage (24 V - 144 V) up to 200 V | |

| 201 V - 900 V | ||

| Above 900 V | ||

| By Technology | IGBT Modules | |

| MOSFET Modules | ||

| SiC Modules | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| Low-Speed Vehicles | ||

| Locomotives | ||

| Metro and Light Rail | ||

| EMUs and DMUs | ||

| By Application | Automotive | |

| Rail Transit | ||

| Industrial Mobility | ||

| Off-Highway Equipment | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2025 value of the traction inverter market?

The traction inverter market size reaches USD 11.12 billion in 2025.

Which propulsion type leads volume demand?

Battery Electric Vehicles hold 67.44% share of worldwide shipments in 2024.

How fast are SiC-based traction inverters growing?

SiC modules post a 17.85% CAGR between 2025 – 2030 as cost parity improves.

Which region grows the quickest through 2030?

Middle East & Africa records the highest 18.04% CAGR due to new metro and bus projects.

Page last updated on: