Automotive Power Steering Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

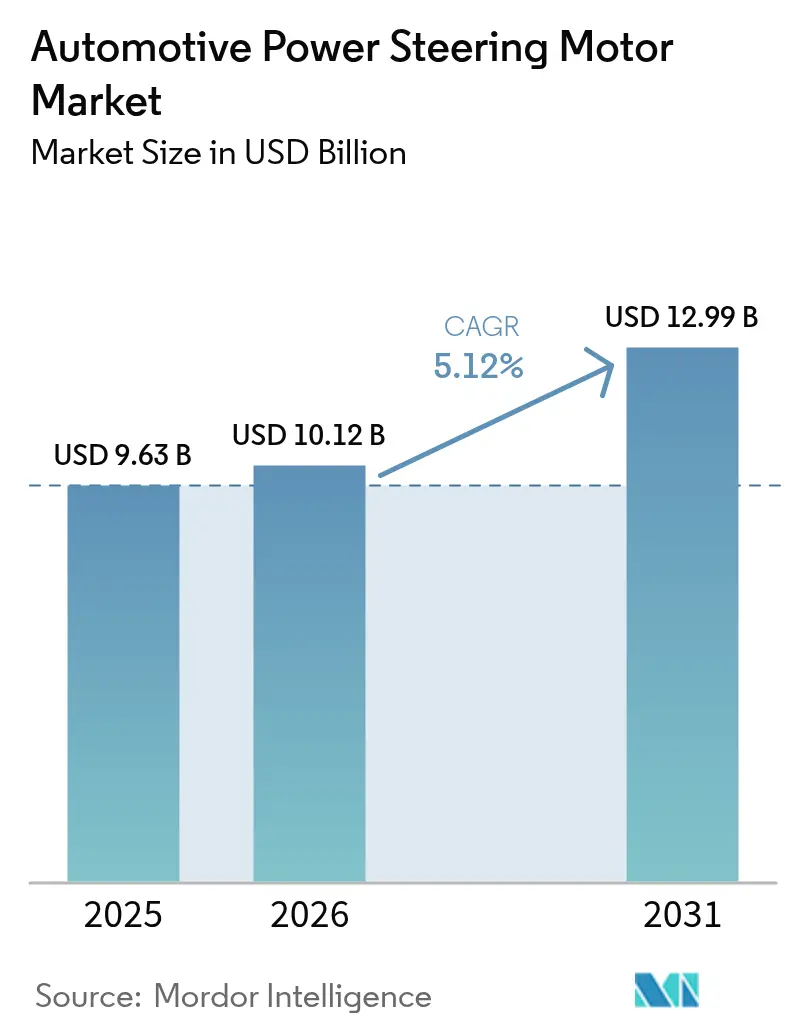

| Market Size (2026) | USD 10.12 Billion |

| Market Size (2031) | USD 12.99 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

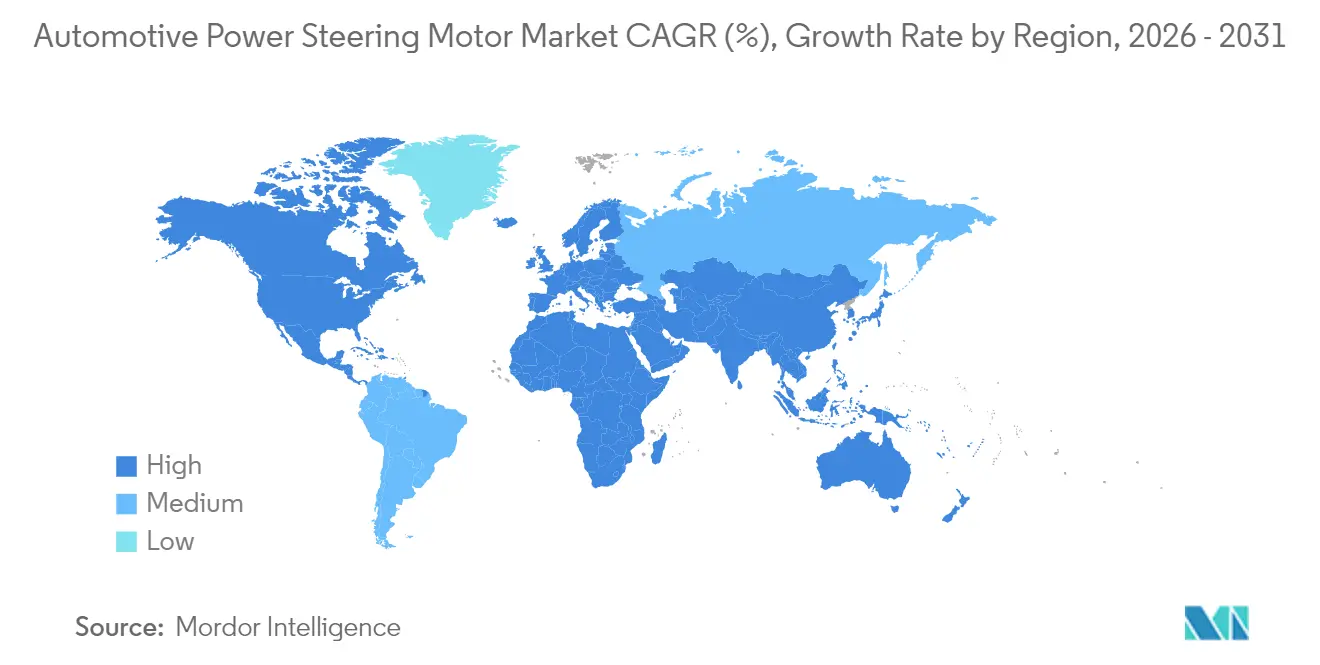

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Power Steering Motor Market Analysis by Mordor Intelligence

automotive power steering motor market size in 2026 is estimated at USD 10.12 billion, growing from 2025 value of USD 9.63 billion with 2031 projections showing USD 12.99 billion, growing at 5.12% CAGR over 2026-2031. Rapid adoption of EPS is propelled by more stringent fuel-economy and CO₂ rules, integration with advanced driver-assistance features, and the shift toward software-defined vehicle platforms. Automakers view steering motors as critical enablers of steer-by-wire architectures that support higher automation levels while lowering lifetime maintenance costs. Asia-Pacific remains the principal manufacturing hub, benefiting from dense electronics supply chains and strong battery-electric vehicle output. In contrast, localization strategies in ASEAN and Mexico are helping cushion rare-earth and semiconductor supply risks. Across all regions, brushless DC motors gain share as silicon-carbide inverters make higher-efficiency power electronics financially viable and compliant with future cybersecurity standards.

Key Report Takeaways

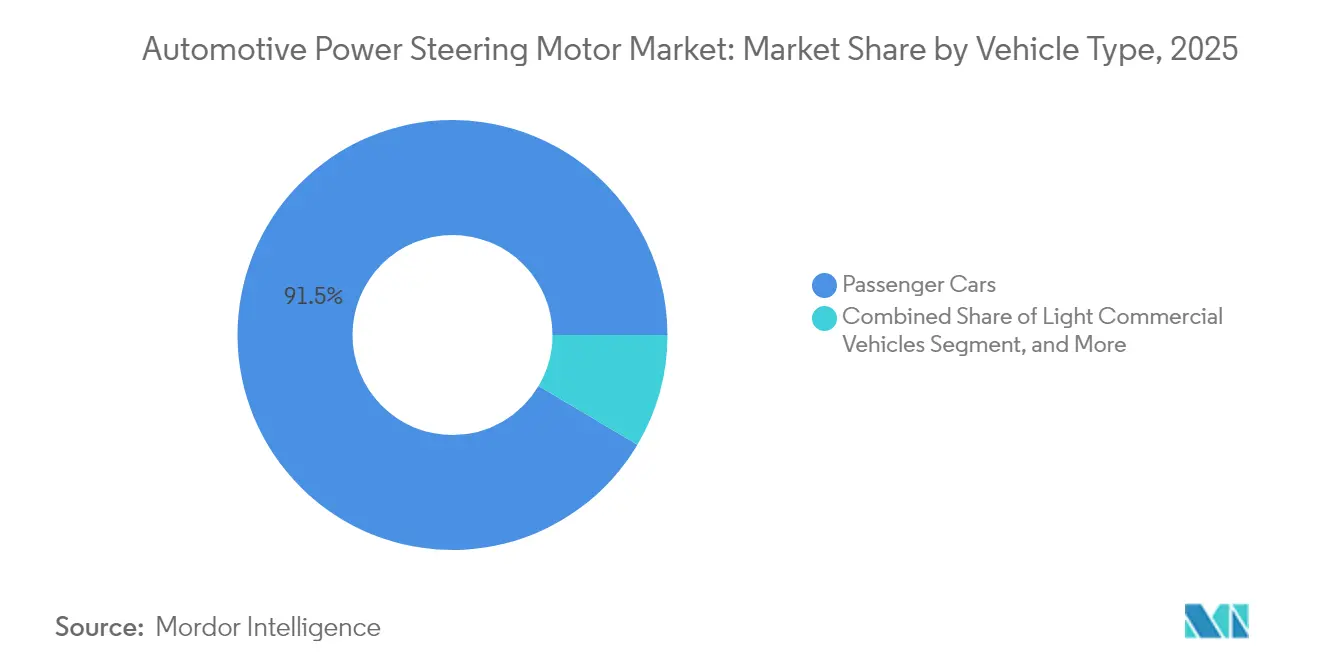

- By vehicle type, passenger cars accounted for 91.48% of the automotive power steering motor market share in 2025, while light commercial vehicles are projected to grow at a 7.12% CAGR through 2031.

- By power-steering type, electric power steering (EPS) dominated with a 70.31% of the automotive power steering motor market share in 2025 and is also expected to register the fastest growth at 8.18% CAGR through 2031.

- By product type, column-assist EPS (CEPS) led with a 41.28% of the automotive power steering motor market share in 2025, while rack-assist EPS (REPS) is forecast to expand at 11.22% CAGR to 2031.

- By motor technology, brushed DC motors comprised 57.45% of the automotive power steering motor market in 2025, whereas brushless DC motors are projected to grow at a 8.72% CAGR through 2031.

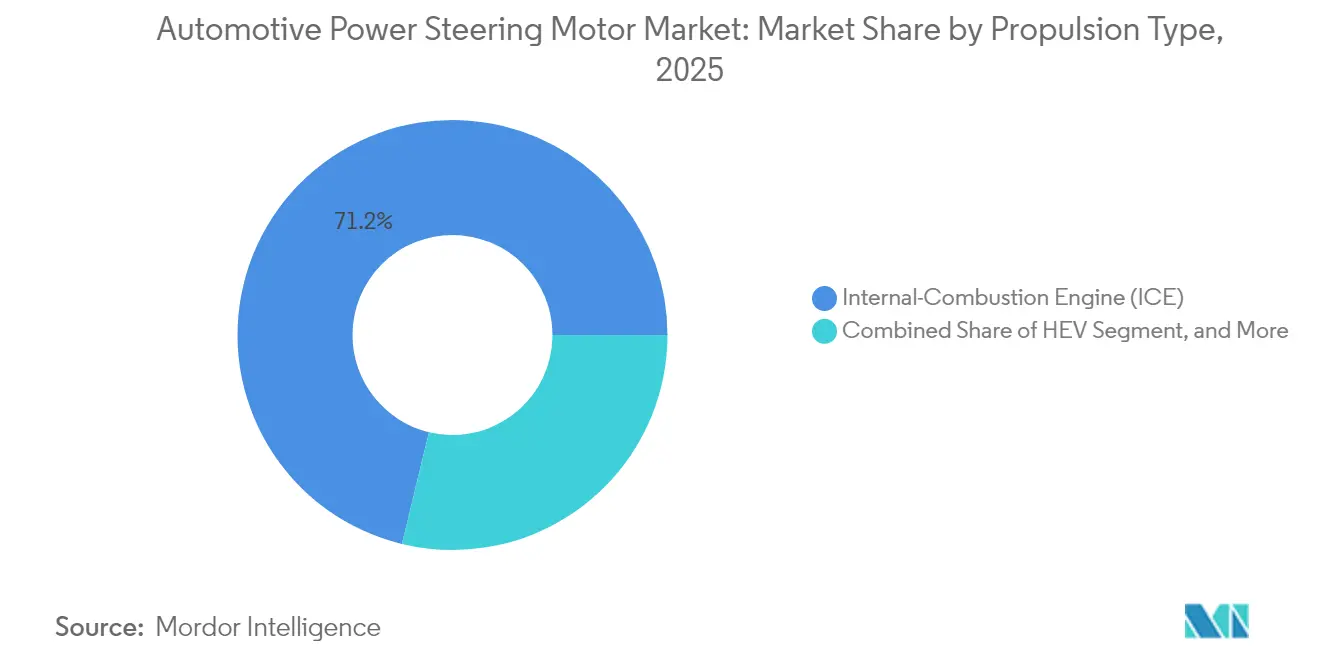

- By propulsion type, internal-combustion engine (ICE) vehicles held a 71.22% of the automotive power steering motor market share in 2025, while battery electric vehicles (BEVs) are set to grow rapidly at a 12.25% CAGR to 2031.

- By sales channel, OEM channels captured 94.35% of the automotive power steering motor market revenue in 2025, while the aftermarket segment is expected to expand at a 8.79% CAGR through 2031.

- By geography, Asia-Pacific led the market with a 54.55% of the automotive power steering motor market in 2025, while the Middle East and Africa is expected to post the fastest growth at 9.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Power Steering Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to EPS for Fuel-Economy and CO₂ Compliance | +1.2% | Global, with EU and China Leading Regulatory Pressure | Medium term (2-4 years) |

| Rapid Electrified-Vehicle Production in China and India | +1.1% | APAC Core, Spill-Over to ASEAN Markets | Short term (≤ 2 years) |

| Integration with ADAS and Steer-by-Wire Roadmaps | +0.9% | North America and EU Premium Segments, Asia-Pacific Following | Long term (≥ 4 years) |

| Tier-1 Vendor Localization in ASEAN and Mexico | +0.7% | ASEAN-5, Mexico, with Supply Chain Benefits to NAFTA | Medium term (2-4 years) |

| Silicon-Carbide Inverter Cost Declines | +0.6% | Global, with Early Adoption in Premium EV Segments | Medium term (2-4 years) |

| OEM Over-the-Air Torque-Map Updates | +0.4% | North America and EU, Expanding to Premium Asia-Pacific Models | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to EPS for Fuel-Economy and CO2 Compliance

Regulatory pressure drives EPS adoption as automakers seek 2-4% fuel economy improvements over hydraulic systems, with the technology eliminating engine-driven hydraulic pumps that consume 2-6 horsepower continuously. European Union's CO2 emission targets of 95g/km by 2025 and China's dual-credit policy create compliance urgency that extends beyond traditional cost-benefit calculations[1]"New vehicle safety systems" Federal Ministry of Transport, bmv.de.. This regulatory momentum accelerates EPS penetration in budget vehicle segments where manufacturers previously avoided the technology due to higher upfront costs. The shift enables automakers to achieve fleet-wide emission reductions without compromising vehicle performance, as EPS systems provide steering assistance only when needed rather than maintaining constant hydraulic pressure. Commercial vehicle manufacturers increasingly adopt EPS to meet stringent emission standards while reducing total cost of ownership through eliminated hydraulic fluid maintenance and improved fuel efficiency.

Rapid Electrified-Vehicle Production in China and India

China's BEV production surge creates concentrated demand for EPS motors, with domestic manufacturers like BYD and emerging players requiring steering systems optimized for electric vehicle architectures rather than ICE retrofits. India's emerging electrification policies compound this demand, as automakers like Tata Motors achieve 80% localization for EV components, including in-house motor production to reduce import dependency. This regional concentration creates supply chain efficiencies for EPS motor manufacturers capable of establishing local production capabilities, while also exposing the market to geopolitical risks around rare-earth material access and technology transfer requirements.

Integration with ADAS and Steer-by-Wire Roadmaps

EPS systems serve as foundational hardware for automated driving features, with steering motors providing the precise torque control required for lane-keeping assist, automated parking, and emergency steering interventions. ZF's recent steer-by-wire deployment in the Nio ET9 demonstrates how eliminating mechanical steering connections enables advanced vehicle dynamics control impossible with traditional systems. This integration creates vendor lock-in effects, as automakers developing autonomous driving capabilities require steering suppliers capable of delivering integrated hardware-software solutions rather than standalone mechanical components. The technology roadmap extends beyond current ADAS applications, with steer-by-wire systems enabling variable steering ratios, customizable driver experiences, and fail-safe redundancy for higher automation levels. Volkswagen's modular steering system development for Premium Platform Electric vehicles illustrates how EPS integration becomes central to software-defined vehicle architectures, requiring continuous over-the-air updates and performance optimization.

Tier-1 Vendor Localization in ASEAN and Mexico

Manufacturing localization accelerates as Tier-1 suppliers establish regional production capabilities to serve growing automotive assembly operations in Thailand, Indonesia, Malaysia, and Mexico. Nexteer's expansion in Mexico with a new technical center creating 350+ jobs by 2026 exemplifies this trend, focusing on electric power steering and steering column innovations with pre-production prototyping capabilities[2]"Nexteer to Expand Mexico Operations", Assembly Magazine, assemblymag.com.. ASEAN region vehicle production projects to reach 6 million units by the mid-2030s, driven by Chinese OEM investments in EV manufacturing and Japanese automaker capacity expansions[3]"ASEAN: Chinese OEMs increase investment through EV production", Automotive Manufacturing Solutions, automotivemanufacturingsolutions.com.. This localization reduces logistics costs and currency exposure while enabling faster response to regional OEM requirements, particularly as Mexico positions itself to become the 5th largest vehicle producer globally by 2025 with a strong focus on electrification components.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Tightness 2025–27 | -1.1% | Global, with Particular Stress in Automotive-Grade Components | Medium term (2-4 years) |

| High EPS Repair Cost for Budget-Car Segments | -0.8% | Global, with Acute Impact in Price-Sensitive Emerging Markets | Short term (≤ 2 years) |

| Rare-Earth Magnet Price Volatility | -0.7% | Global, with Supply Concentration Risk from China Export Policies | Short term (≤ 2 years) |

| Cyber-Security Compliance Cost Burden | -0.5% | North America and EU Regulatory Markets, Expanding Globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Tightness 2025-27

Automotive-grade semiconductor shortages continue affecting EPS motor production, with power management ICs and motor control processors experiencing extended lead times that disrupt manufacturing schedules and increase component costs. The automotive industry's transition to 800V electrical architectures compounds this challenge, requiring specialized silicon carbide semiconductors with limited production capacity and stringent automotive qualification requirements. EPS manufacturers face allocation constraints from semiconductor suppliers prioritizing higher-volume consumer electronics over automotive applications, despite automotive's higher per-unit profitability. This supply tightness forces longer-term supply agreements and inventory buffers that increase working capital requirements while limiting production flexibility to respond to demand fluctuations.

High EPS Repair Cost for Budget-Car Segments

EPS system replacement costs ranging from USD 800-1,500 create affordability barriers in price-sensitive markets where vehicle values may not justify repair expenses, particularly for aging budget vehicles approaching end-of-life decisions. This cost structure drives consumers toward aftermarket alternatives or vehicle replacement rather than OEM repairs, limiting market expansion in regions with extended vehicle lifecycles and lower disposable incomes. The complexity of EPS motor-control unit integration requires specialized diagnostic equipment and technician training that many independent repair facilities lack, concentrating repair capabilities among authorized dealers with higher labor rates. Budget vehicle manufacturers face design trade-offs between initial cost competitiveness and long-term serviceability, as simplified EPS architectures may reduce upfront costs but increase repair complexity when failures occur.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Segments Drive Electrification

Passenger cars maintain market dominance at 91.48% of the automotive power steering motor market share in 2025, driven by regulatory compliance requirements and consumer demand for advanced driver assistance features that require precise electronic steering control. Heavy commercial vehicles adopt EPS systems more gradually due to higher power requirements and durability concerns. However, emerging applications in electric commercial vehicles create new opportunities for high-torque motor designs. Light commercial vehicles exhibit the fastest growth at 7.12% CAGR 2026-2031, outpacing passenger cars despite representing a smaller market share, as fleet operators prioritize total cost of ownership benefits from EPS systems, including reduced maintenance and improved fuel efficiency.

The commercial vehicle transition reflects broader fleet electrification mandates, where operators seek integrated solutions combining steering, braking, and powertrain controls to optimize vehicle efficiency and reduce operational complexity. Fleet management systems increasingly require remote diagnostics and predictive maintenance capabilities that EPS systems enable through integrated sensors and communication protocols. This creates differentiation opportunities for suppliers capable of delivering fleet-optimized solutions with extended service intervals and remote monitoring capabilities that reduce downtime costs.

By Power-Steering Type: EPS Dominance Accelerates

Electric power steering commands 70.31% of the automotive power steering motor market share in 2025 while growing at 8.18% CAGR through 2031, reflecting the technology's evolution from a fuel economy solution to an enabling platform for advanced vehicle features. Hydraulic power steering systems face declining demand as automakers eliminate hydraulic components to reduce complexity and enable electrification, though the technology persists in heavy-duty applications requiring maximum steering force. Electro-hydraulic power steering serves as transitional technology for manufacturers upgrading existing platforms, combining electric motor assistance with hydraulic backup for applications requiring higher power output than pure EPS systems can deliver.

The EPS growth trajectory accelerates beyond traditional adoption curves as the technology becomes a prerequisite for ADAS integration and autonomous driving development. Automakers increasingly specify EPS systems for their software update capabilities and integration with vehicle stability control, creating vendor partnerships that extend beyond component supply to software development and validation services. This shift transforms EPS suppliers from mechanical component providers to integrated technology partners capable of delivering complete steering solutions with embedded intelligence and connectivity features.

By Product Type: Rack-Assist Systems Gain Traction

Column-assist EPS (CEPS) maintains 41.28% of the automotive power steering motor market share in 2025 due to cost advantages and retrofit compatibility with existing vehicle architectures, particularly in compact and mid-size passenger cars, where packaging constraints favor integrated column-mounted solutions. Rack-assist EPS (REPS) accelerates fastest at 11.22% CAGR, driven by superior performance characteristics and integration advantages in electric vehicle platforms where steering systems require higher precision and responsiveness. Pinion-assist EPS (PEPS) serves specialized applications requiring intermediate power levels, while dual-pinion EPS (DPEPS) addresses high-performance vehicles demanding maximum steering precision and fail-safe redundancy.

Emerging parallel-axis EPS (PA-EPS) configurations enable packaging flexibility for electric vehicle designs where traditional steering column layouts conflict with battery placement and interior space optimization. The product evolution reflects automakers' shift toward platform-specific steering solutions rather than universal applications, creating opportunities for suppliers capable of delivering customized motor designs and control algorithms. Advanced motor topologies including axial-flux permanent magnet designs enable higher torque density and reduced axial length, addressing space constraints in modern vehicle architectures.

By Motor Technology: Brushless Motors Advance

Brushed DC motors retain 57.45% of the automotive power steering motor market share in 2025 due to cost advantages and established supply chains. However, brushless DC motors accelerate at 8.72% CAGR through 2031 as efficiency and durability demands favor the technology's superior performance characteristics. Brushless motors eliminate mechanical wear points and enable precise speed control required for advanced driver assistance features, though higher initial costs limit adoption in budget vehicle segments. The technology transition reflects broader automotive electrification trends where motor efficiency directly impacts vehicle range and battery life.

Silicon carbide power electronics enable brushless motor cost reductions through improved inverter efficiency and reduced cooling requirements, with the SiC device market growing at 26% CAGR through 2030 and automotive applications representing 70% of power SiC demand. This cost convergence accelerates brushless motor adoption as the total system cost approaches brushed alternatives while delivering superior performance and reliability. Rare-earth magnet alternatives, including ferrite and recycled NdFeB materials, address supply chain vulnerabilities while maintaining motor performance standards required for automotive applications.

By Propulsion Type: BEV Growth Transforms Requirements

Internal combustion engine vehicles maintain 71.22% of the automotive power steering motor market share in 2025, though battery electric vehicles surge at 12.25% CAGR as electrification mandates and consumer preferences drive adoption across global markets. BEV steering systems require integration with regenerative braking and vehicle stability control systems, creating opportunities for suppliers capable of delivering coordinated chassis solutions rather than standalone steering components. Hybrid electric vehicles serve as transitional technology, requiring steering systems compatible with both electric and combustion powertrains while optimizing efficiency across operating modes.

The propulsion mix evolution creates distinct requirements for steering motor design, with BEVs enabling higher voltage operation and integrated thermal management while ICE vehicles require compatibility with 12V electrical systems and engine vibration isolation. Over 50% of battery electric vehicles are expected to utilize silicon carbide powertrains by 2027, up from 30% currently, enabling higher efficiency steering systems with reduced power consumption. This transition creates technology roadmap challenges for suppliers serving mixed propulsion fleets while developing next-generation solutions for fully electric platforms.

By Sales Channel: Aftermarket Opportunities Emerge

OEM demand dominates at 94.35% of the automotive power steering motor market share in 2025, reflecting the integrated nature of modern EPS systems that require factory installation and calibration with vehicle control systems. Aftermarket demand grows at 8.79% CAGR through 2031, driven by aging vehicle fleets requiring EPS retrofits and replacement components, particularly in regions with extended vehicle lifecycles and growing service infrastructure. The aftermarket expansion faces challenges from system complexity and diagnostic requirements that limit independent repair capabilities, concentrating service opportunities among authorized dealers and specialized service centers.

Aftermarket growth accelerates as EPS systems reach replacement intervals in early-adoption vehicles, creating demand for remanufactured components and upgrade solutions that improve performance over original equipment. The automotive aftermarket projects 5% CAGR growth through 2025, though electric vehicle adoption poses long-term challenges as EVs require fewer maintenance interventions than ICE vehicles. This dynamic creates opportunities for suppliers capable of delivering retrofit solutions that upgrade hydraulic systems to EPS while maintaining compatibility with existing vehicle architectures and control systems.

Geography Analysis

Asia-Pacific retained a 54.55% of the automotive power steering motor market in 2025, thanks to China’s leadership in vehicle output and accelerating battery-electric volumes. Localized motor production benefits from regional semiconductor back-end assembly and a dense magnet supply chain. Japanese and Korean Tier-1s lead in precision algorithm design, while Chinese suppliers push scale advantages into export markets. India amplifies momentum with localization incentives that raise domestic value content on new EV models.

While still small, the Middle East and Africa region is forecast to post the fastest 9.35% CAGR to 2031 as Morocco and Saudi Arabia nurture export-oriented assembly plants. Government-backed industrial zones provide tax holidays and renewable-energy pricing that lower operating costs for steering-motor plants. Regional growth also mitigates Europe’s supply-risk concerns by adding geographical diversity in critical component sourcing.

Europe and North America transition steadily toward electrification and Level 2+ driver assistance, stimulating demand for motors capable of ISO/SAE 21434 cyber-secure updates. EU crash-worthiness and emissions rules cement EPS as a default specification across vehicle classes. At the same time, the United States leverages the USMCA trade pact to draw component production into Mexican industrial corridors. Semiconductor shortages remain a headwind, but multi-sourcing strategies and onshoring grants help cushion supply shocks. Combined, mature regions account for over one-third of the automotive power steering motor market, with future expansion tied mainly to software monetization and autonomous-ready steering modules.

Competitive Landscape

The automotive power steering motor market is moderately concentrated: top global Tier-1s maintain competitive moats via proprietary motor-control IP, integrated inverters, and long-term supply agreements. Bosch, JTEKT, Nexteer, ZF, and Hyundai Mobis collectively supply the majority of EPS racks to volume platforms. Their early investment in brushless algorithms and ADAS interfaces sets high switching barriers for smaller rivals.

Strategic M&A sharpens vertical integration. Schaeffler’s 2024 merger with Vitesco creates a diversified electromechanical giant spanning e-axles, inverters, and steering drives, enabling bundled chassis offerings that reduce BOM complexity for OEMs. Rare-earth-free motor innovations such as ZF’s I2SM unit showcase how market leaders hedge material risk while promising comparable performance, potentially reshaping sourcing models if adoption scales.

Partnerships between steering specialists and software providers intensify. Automakers demand ISO 26262-compliant toolchains and secure update servers, prompting co-development agreements with embedded-software firms. Tier-1s reciprocally sign wafer-capacity deals with power-semiconductor makers to lock in SiC supply. Competitive intensity thus migrates from mechanical output to software quality, cyber-defense, and supply-chain resilience—areas where incumbents still command notable advantages.

Automotive Power Steering Motor Industry Leaders

-

JTEKT Corporation

-

Robert Bosch GmbH

-

Nexteer Automotive Corp.

-

ZF Friedrichshafen AG

-

NSK Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Motor Group commits USD 21 billion to investment in U.S. manufacturing from 2025-2028, including USD 6 billion for automotive component localization and electric vehicle parts production. This will create over 100,000 jobs and strengthen supply chain capabilities for steering systems and other critical components.

- January 2025: ZF, a global leader in automotive technology, has strengthened its position as the world's leading supplier of chassis components by securing a significant agreement with a major global manufacturer. This development highlights the strategic importance of ZF's newly established Chassis Solutions Division, which is delivering value to customers and advancing the Software Defined Vehicle concept through by-wire solutions. Recognized as the preferred supplier for chassis components across all regions, ZF's agreement includes the planned volume production of brake-by-wire technology and advanced steering systems, specifically designed for a single vehicle class.

Global Automotive Power Steering Motor Market Report Scope

An automotive power steering motor is an essential component of a vehicle power steering system. It is an electric motor that assists the driver in turning the steering wheel, making it easier to control the direction of the vehicle, especially at low speeds and during parking maneuvers. The power steering motor is responsible for providing additional force or torque to the steering mechanism, reducing the physical effort required from the driver to turn the wheels.

The automotive power steering motor market is segmented by vehicle type, power steering type, product type, demand category, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By power steering type, the market is segmented into hydraulic power steering (HPS), electric power hydraulic steering (EPHS), and electric power steering (EPS). By product type, the market is segmented into rack assist type (REPS), column assist type (CEPS), and pinion assist type (PEPS). By demand category, the market is segmented into OEM and aftermarket. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the world. The report offers market size in value USD.

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Hydraulic Power Steering (HPS) |

| Electro-hydraulic Power Steering (EHPS) |

| Electric Power Steering (EPS) |

| Rack-Assist EPS (REPS) |

| Column-Assist EPS (CEPS) |

| Pinion-Assist EPS (PEPS) |

| Dual-Pinion EPS (DPEPS) |

| Parallel-Axis EPS (PA-EPS) |

| Brushless DC Motor |

| Brushed DC Motor |

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV/PHEV) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Power-Steering Type | Hydraulic Power Steering (HPS) | |

| Electro-hydraulic Power Steering (EHPS) | ||

| Electric Power Steering (EPS) | ||

| By Product Type | Rack-Assist EPS (REPS) | |

| Column-Assist EPS (CEPS) | ||

| Pinion-Assist EPS (PEPS) | ||

| Dual-Pinion EPS (DPEPS) | ||

| Parallel-Axis EPS (PA-EPS) | ||

| By Motor Technology | Brushless DC Motor | |

| Brushed DC Motor | ||

| By Propulsion Type | Internal-Combustion Engine (ICE) | |

| Hybrid Electric Vehicle (HEV/PHEV) | ||

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive power steering motor market?

The automotive power steering motor market size was USD 10.12 billion in 2026 and is forecast to reach USD 12.99 billion by 2031.

Which steering technology dominates the global landscape?

Electric power steering holds 70.31% market share and continues to expand as hydraulic systems are phased out.

What factor is driving brushless motor adoption?

Declining silicon-carbide inverter costs boost efficiency and durability, supporting a 8.72% CAGR for brushless motors through 2031.

How will steer-by-wire affect future demand?

Steer-by-wire requires precise, fail-safe motor control and removes mechanical columns, which will increase demand for high-torque EPS units integrated with advanced software.

Page last updated on: