Active Power Steering Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 11.31 Billion |

| Market Size (2030) | USD 18.36 Billion |

| Growth Rate (2025 - 2030) | 10.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Power Steering Market Analysis by Mordor Intelligence

The active power steering market size stands at USD 11.31 billion in 2025 and is projected to reach USD 18.36 billion by 2030, translating into a 10.17% CAGR through the forecast period. This sustained expansion is rooted in the automotive sector’s rapid electrification, stricter safety mandates, and steady progress toward hands-off autonomous functions, all requiring precise, electronically controlled steering. Electric Power Steering (EPS) remains the anchor technology thanks to lower energy draw and more straightforward software calibration. At the same time, steer-by-wire platforms gain momentum as premium and electric vehicle (EV) programs migrate to complete electronic control. Automakers now treat steering software as a revenue stream, selling downloadable performance modes and comfort presets that refresh the vehicle over its lifetime. Meanwhile, Tier-1 suppliers combine steering, braking, and chassis control within centralized domain architectures, allowing faster integration of over-the-air (OTA) updates and tighter cybersecurity oversight.

Key Report Takeaways

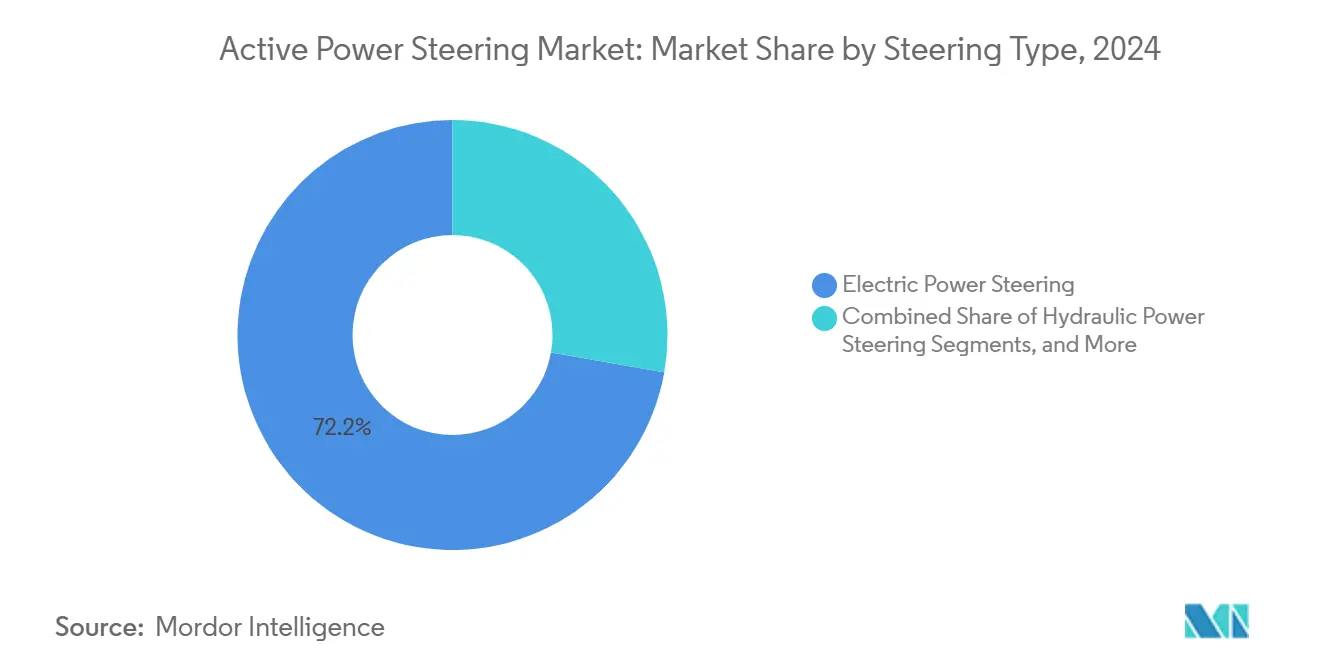

- By steering type, EPS led with 72.22% of the active power steering market share in 2024, while steer-by-wire recorded the highest projected CAGR at 12.32% through 2030.

- By vehicle type, passenger cars held 63.81% of the active power steering market size in 2024, advancing at an 11.98% CAGR to 2030.

- By propulsion type, ICE platforms accounted for 77.87% of the active power steering market share in 2024, whereas BEVs are forecast to expand at a 12.83% CAGR through 2030.

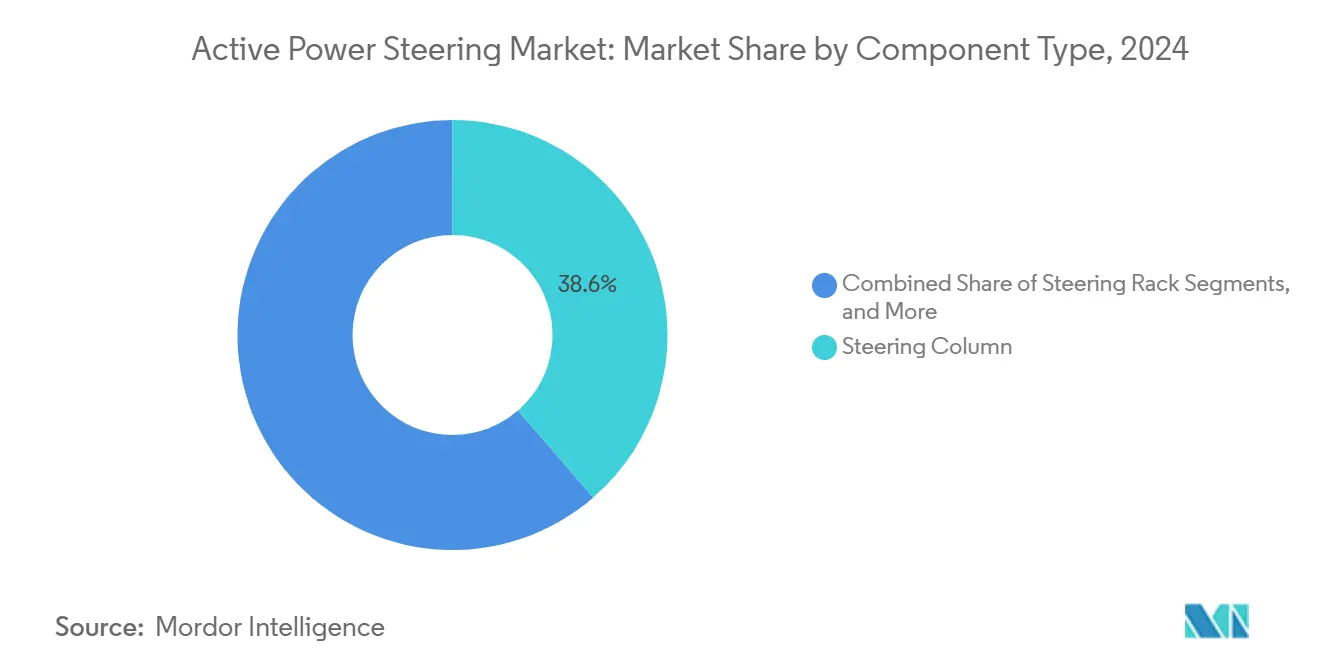

- By component, steering columns captured 38.63% of the active power steering market share in 2024, while sensors represent the fastest-growing component with an 11.74% CAGR through 2030.

- By distribution channel, OEM installations dominated the active power steering market, accounting for 83.77% of the size in 2024, whereas the aftermarket segment is poised for a 10.84% CAGR through 2030.

- By geography, Asia-Pacific commanded 46.31% of the active power steering market share in 2024 and posts the fastest regional growth at a 10.34% CAGR to 2030.

Global Active Power Steering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Push Raising EPS Penetration | +2.1% | Global, led by China and Europe | Medium term (2-4 years) |

| Government Safety Mandates for ADAS-Ready Steering | +1.8% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| OEM Shift to Modular Steering Platforms | +1.5% | Global, concentrated in premium segments | Long term (≥ 4 years) |

| Cost Downs in High-Torque Electric Motors | +1.3% | Global manufacturing hubs | Medium term (2-4 years) |

| Over-The-Air Steering Software Upgrades | +1.2% | North America and Europe early adoption | Long term (≥ 4 years) |

| Tier-1s Bundling Steer-By-Wire with Domain Controllers | +0.9% | Global Tier-1 supplier networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Push Raising EPS Penetration

Electric Power Steering has become a standard feature in nearly all modern battery-electric vehicles, improving energy efficiency and driving comfort. KAYABA’s innovative steering system offers significant energy savings in urban and highway conditions compared to traditional hydraulic systems, helping extend driving range and reduce concerns about battery limitations[1]“KEEPS Electric Power Steering Efficiency Study,”, KAYABA Corporation, kayaba.co.jp. Eliminating belt-driven pumps also frees under-hood space for high-voltage components and simplifies thermal routing around the battery pack. Chinese manufacturers leverage vertically integrated motor production to reduce system cost and accelerate rollout across high-volume compact EVs [2]“EV Components Cost Analysis,”, China Association of Automobile Manufacturers, caam.org.cn. European OEMs link EPS to regenerative braking strategies that recapture urban driving energy, translating into real-world range gains on dense city routes[3]“Regenerative Steering Integration,”, European Automobile Manufacturers’ Association, acea.be. Continuous software calibration lets the same hardware span basic manual steering through Level 3 autonomy, turning EPS into a flexible gateway for future functions.

Government Safety Mandates For ADAS-Ready Steering

Regulators increasingly bake steering redundancy into new-vehicle approval. The UNECE WP.29 automated-steering rule sets technical targets that global suppliers must meet by 2025. NHTSA now requires dual-motor EPS or equivalent fail-safe mechanisms for Level 3 and higher automation, pushing OEMs to over-spec sensors and controllers [4]“Level 3 Vehicle Guidance,”, National Highway Traffic Safety Administration, nhtsa.gov. Europe’s General Safety Regulation obliges new platforms launched after July 2024 to include Emergency Lane Keeping, which only active units can execute with millisecond precision. ISO 26262 compels manufacturers to reach ASIL-D integrity, forcing redundant encoders, dual power rails, and independent firmware checks. These mandates disqualify cost-driven hydraulic racks and electrically assisted steering as a compliance path for global nameplates.

Over-The-Air Steering Software Upgrades

Steering calibration joins infotainment and ADAS as an update-over-the-air candidate. Harman’s update stack enables periodic tweaks that counter tire wear or new regulatory limits without dealership visits. NXP’s secure gateway ensures cryptographic authentication, so only signed steering binaries are executed, satisfying the ISO 21434 requirement. Hitachi Astemo aggregates fleet data to refine control loops, trimming warranty claims linked to steering feel drift by double-digit percentages. Excelfore’s eSync marketplace hints at subscription steering modes—eco, comfort, track—opening recurring revenue for OEMs. OTA capability also future-proofs vehicles against emerging cybersecurity threats by allowing timely patch deployment.

Tier-1s Bundling Steer-By-Wire With Domain Controllers

ZF’s cubiX merges steering control with braking and chassis management, slicing ECU counts and simplifying vehicle harness design. Continental’s SCCU places steer-by-wire and ADAS processing on one microprocessor, executing lane-keeping torque commands in microseconds. NVIDIA’s DRIVE pairing with steering suppliers pushes AI-assisted force feedback that learns driver behavior over time, tailoring effort curves for comfort or sportiness. Centralization also streamlines functional-safety audits because a single domain controller manages redundancy across multiple actuators rather than separate certification paths. As these bundles mature, smaller component makers risk marginalization unless they partner on full-stack offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost Vs. Traditional Hydraulic Units | -1.9% | Global, acute in price-sensitive segments | Medium term (2-4 years) |

| Reliability Concerns in Full Steer-By-Wire Architectures | -1.4% | Europe and North America regulatory focus | Short term (≤ 2 years) |

| Tight Semiconductor Supply for Torque Sensors | -1.1% | Global supply-chain constraints | Short term (≤ 2 years) |

| Cyber-Security Certification Bottlenecks | -0.8% | Developed markets with strict regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High System Cost vs. Traditional Hydraulic Units

Steer-by-wire assemblies command three to four times the bill-of-materials cost of a basic rack-and-pinion setup because they must duplicate sensors, motors, and controllers to satisfy fail-operational rules. Emerging-market buyers often balk at the premium, forcing OEMs to reserve full electronic steering for higher-margin trims. Chinese brands such as BYD pursue vertical integration, cutting off installed cost by fabricating motors and ECUs in-house. Still, software validation, cybersecurity audits, and extensive electromagnetic compatibility tests add expense regardless of where the hardware is built. Until volumes lift further, cost will remain a gating factor outside the premium and electric segments.

Cyber-Security Certification Bottlenecks

ISO/SAE 21434 drives rigorous threat modeling and penetration tests for any networked steering ECU. Distinct national pathways—NHTSA in the United States, ENISA across Europe—add parallel documentation and audit layers that soak up engineering bandwidth and extend launch schedules. OTA update pipelines must pass recurring security reviews, meaning certification is no longer a one-off milestone but an ongoing duty cycle. The scarcity of accredited testing labs creates scheduling conflicts when multiple OEMs converge on similar launch windows. While centralized domain controllers help by housing fewer targets, the security bar will continue rising alongside broader connected-vehicle regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Steering Type: EPS Dominance Drives Steer-By-Wire Innovation

EPS contributed 72.22% share of the active power steering market in 2024, reinforcing its role as the default choice for efficiency and ADAS readiness. Steer-by-wire rides a 12.32% CAGR to 2030 that reflects premium EV launches aiming for cockpit flexibility and autonomous credentials. As component costs fall, EPS platforms increasingly embed software hooks—variable ratio, lane-keep corrections—that mimic steer-by-wire advantages while retaining a physical backup column. Hydraulic racks hang on in heavy trucks where extreme steering loads and long service cycles trump energy savings, but their share contracts as electrified heavy-duty frames materialize. Electro-hydraulic hybrids bridge the gap in buses and vocational trucks, coupling familiar hydraulics with digital valves to enable driver-assist functions without complete electrical conversion. The market is thus bifurcating: EPS handles volume and cost sensitivity, while pure electronic racks stake out future-proof real estate for Level 3+ automation.

Second-tier suppliers seize white-space by offering retrofit steer-by-wire kits for low-speed robotaxis or agricultural platforms where mechanical redundancy is less critical. Meanwhile, leading Tier-1s integrate EPS and steer-by-wire into a single product roadmap, ensuring a seamless migration path for OEMs as regulations tighten. Software commonality lets automakers tune steering feel across base and premium trims using the same motor/gearset package, trimming part proliferation. Over time, this strategy positions steer-by-wire as a logical step once verification, supply stability, and consumer trust converge. Consequently, the market will likely exhibit overlapping generations of technology rather than a clean replacement cycle.

By Vehicle Type: Passenger Cars Lead Adoption Across Segments

Passenger cars delivered a 63.81% share of the active power steering market in 2024, reflecting strong consumer pull for parking assist, lane centering, and energy savings. Fleet electrification in ride-hailing and corporate pools further lifts volumes because everyday users value reduced steering effort and safety assistance that lowers collision risk. The segment’s 11.98% CAGR signals broadening adoption beyond luxury nameplates into compact hatchbacks and midsize SUVs. Light commercial vans trail in volume yet mirror car trends as e-commerce pushes operators to reduce driver fatigue during dense urban routes. Medium and heavy commercial vehicles rely on active power steering for lane-keeping and cross-wind damping, which are critical for highway safety and cargo integrity.

Buses integrate variable-assist columns to ease repetitive low-speed maneuvers while maintaining stability at express-lane velocities. Steer-by-wire offers cockpit layout freedom that could unlock autonomous shuttle interiors, encouraging transit agencies to pilot premium features. Across categories, the market gains additional momentum whenever insurance providers tie lower premiums to ADAS packages validated by active power steering hardware. As residual values for vehicles with electronic steering improve, buyers interpreting the total cost of ownership tilt the adoption curve in favor of active units.

By Propulsion Type: ICE Legacy Meets BEV Innovation

ICE platforms contributed a 77.87% share of the active power steering market in 2024, owing to their vast installed base and the relative ease of swapping hydraulic pumps for EPS. That said, BEVs demonstrate stronger proportional growth, adding product launches and higher attach rates; their 12.83% CAGR through 2030 foreshadows eventual leadership if current electrification policies persist. Hybrids and plug-in hybrids sit in the middle, leveraging EPS to cap fuel burn during frequent engine-off operation. Though niche today, fuel-cell programs almost universally specify steer-by-wire because designers wish to exploit flat-floor architectures incompatible with bulky columns.

The propulsion split highlights an interim period where two architectures coexist. OEMs optimize cost on legacy platforms to retrofit EPS with minimal chassis disruption. In contrast, clean-sheet EV frames integrate steer-by-wire from day one to unlock frunk storage and reconfigurable interiors. Market forecasts, therefore, display steep adoption ramps for electronic racks inside BEVs, while ICE adoption plateaus as incremental gains become harder to justify compared with drivetrain upgrades or connectivity features.

By Component: Sensors Drive Next-Generation Functionality

Traditional steering columns held a 38.63% share of the active power steering market in 2024, underscoring their residual dominance across mixed technology generations. Yet sensors clock the briskest 11.74% CAGR through 2030, thanks to twin trends: higher redundancy levels and richer road-feel emulation. Each steer-by-wire rack may host twin torque sensors, dual angle encoders, and position trackers on two separate shafts. Growth also stems from embedding inertial measurement units inside control assemblies to support lane centering and hands-free highway assist. Steering racks evolve from passive mechanical housings into smart actuators incorporating high-ratio planetary gears and compact cooling loops around in-board motors.

Control modules emerge as the platform braintrust, aggregating up to 16 separate input channels before issuing torque commands. Meanwhile, ancillary components—haptic feedback actuators, redundant power supplies, and secure gateway chips—expand the bill of materials. The component mix, therefore, tilts from iron and aluminum toward silicon and software, underlining why advanced electronics now dictate capability ceilings in the active power steering market.

By Distribution Channel: OEM Integration Dominates Market Access

OEM yielded an 83.77% share of the active power steering market size in 2024 because steering affects homologation and warranty metrics from day one. Automakers embed calibration in chassis development, making later retrofits complex and costly. Nevertheless, the aftermarket posts a healthy 10.84% CAGR through 2030, as heavy-duty fleets and specialty upfitters retrofit lane-keep EPS kits to curb accident exposure. Retrofit kits usually target Class 8 trucks and city buses, where long daily hours magnify fatigue relief benefits.

Regulatory ceilings restrain informal installations; only parts certified to original manufacturing standards can interface with safety systems. Authorized service centers, therefore, capture most retrofit business, giving Tier-1 suppliers an incentive to license designs rather than sell gray-market components. Government incentives for older-fleet safety upgrades in emerging markets may expand addressable volume, particularly if insurers concur on premium discounts tied to verified active power steering installations.

Geography Analysis

Asia-Pacific holds a 46.31% share of the active power steering market in 2024 and sustains the highest 10.34% CAGR through 2030, as China’s EV subsidies, local content rules, and start-up agility translate into aggressive steering of innovation. Domestic OEMs such as NIO install steer-by-wire on flagship sedans to differentiate user experience and claim early autonomy readiness. Japan contributes technological depth, with JTEKT and NSK exporting EPS modules worldwide and funneling learning from kei-car efficiency targets into larger platforms. South Korean system houses leverage electronics expertise to integrate steering updates over 5G links, resonating with the nation’s connected-car strategy.

North America ranks second in volume, stimulated by NHTSA mandates and consumer preference for high-assistance pickup trucks. Tesla’s steer-by-wire implementation inside the Cybertruck is a high-visibility proof point likely to cascade across broader model lines. Fleet adoption in long-haul trucking further fuels regional demand as operators embrace lane-centering to fight driver shortages. Europe’s stringent CO₂ limits and General Safety Regulation keep adoption rates elevated; emergency lane-keep functions require precise electronic racks.

South America, the Middle East & Africa contribute modest shares but feature accelerating curves as CKD assembly plants pick up globally designed EVs already fitted with active power steering. Import tariffs on hydraulic pumps, compared with rising local motor production, help tip cost parity in favor of EPS. Regional free-trade zones encourage multinational Tier-1s to set up local machining cells for racks, enabling quicker supply and qualification cycles. As a result, the active power steering market displays a classic cascade, with mature regions refining technology and manufacturing scale before diffusion pulls prices in line for developing economies.

Competitive Landscape

The active power steering market is moderately concentrated, and legacy Tier-1s hold entrenched contracts yet face nimble challengers focused on software. Bosch, ZF Friedrichshafen, JTEKT, NSK, Nexteer, and Continental collectively control a significant slice of OEM awards thanks to decades of functional-safety credibility and global manufacturing footprints. Their capital strength funds continue R&D in magnetic materials, sensor fusion, and cyber-hardened firmware.

New-wave specialists such as Schaeffler, Hyundai Mobis, and AutonomouStuff differentiate through steer-by-wire kits paired with proprietary software layers that can be re-skinned per brand. Software-defined steering reshapes competitive dynamics: revenue grows with hardware units and post-sale feature unlocks delivered through subscription. Tier-1s respond by bundling steer-by-wire with domain controllers, as evidenced by ZF’s cubiX and Continental’s SCCU product lines, thereby raising switching costs for OEMs already integrating chassis and ADAS on single boards.

The intellectual-property race erects defensive moats yet also triggers cross-licensing; several top-three suppliers entered confidential patent-pool negotiations in early 2025 to avoid litigation that could stall program launches. As pricing convergence approaches, service-level agreements—update cadence, predictive maintenance dashboards, cybersecurity response—become as decisive in award decisions as pure hardware cost. The active power steering market, therefore, evolves into a hybrid product-plus-service arena where continuous support and data analytics shape long-term revenue.

Active Power Steering Industry Leaders

Robert Bosch GmbH

ZF Friedrichshafen AG

JTEKT Corporation

NSK Ltd

Nexteer Automotive Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ZF announced that it will supply Mercedes-Benz with steer-by-wire technology beginning in 2026. This marks ZF's first introduction of the technology to the European market through Mercedes-Benz. The two companies collaborated to develop a Mercedes-Benz-specific steer-by-wire system, leveraging ZF's extensive system expertise and experience.

- February 2025: NIO, a manufacturer of premium smart electric vehicles, and the German technology group ZF reached a milestone in their strategic partnership. Integrating ZF's steer-by-wire technology into the "SkyRide" chassis of NIO's ET9 executive flagship vehicle marks the beginning of serial production for this precision steering system. The ET9 is the first model built on NIO's NT 3.0 platform.

Global Active Power Steering Market Report Scope

| Hydraulic Power Steering (HPS) |

| Electric Power Steering (EPS) |

| Electro-Hydraulic Steering (EHPS) |

| Steer-by-Wire |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (MHCV) |

| Buses & Coaches |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Steering Column |

| Steering Rack |

| Sensors |

| Control Modules |

| Others |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Steering Type | Hydraulic Power Steering (HPS) | |

| Electric Power Steering (EPS) | ||

| Electro-Hydraulic Steering (EHPS) | ||

| Steer-by-Wire | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Medium and Heavy Commercial Vehicles (MHCV) | ||

| Buses & Coaches | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Component | Steering Column | |

| Steering Rack | ||

| Sensors | ||

| Control Modules | ||

| Others | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the active power steering market?

The active power steering market size is USD 11.31 billion in 2025 and is forecast to reach USD 18.36 billion by 2030.

Which steering technology holds the largest share today?

Electric Power Steering dominates with 72.22% active steering market share in 2024.

Which vehicle category is adopting active steering the fastest?

Passenger cars hold 63.81% share and are expanding at an 11.98% CAGR through 2030.

How quickly is steer-by-wire growing?

The steer-by-wire segment is registering a 12.32% CAGR, the fastest pace among steering types.

What restrains wider adoption of steer-by-wire?

High system cost, reliability perception, semiconductor supply limits, and lengthy cybersecurity certification each temper near-term growth.

Page last updated on: