Automotive Electro-Hydraulic Power Steering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

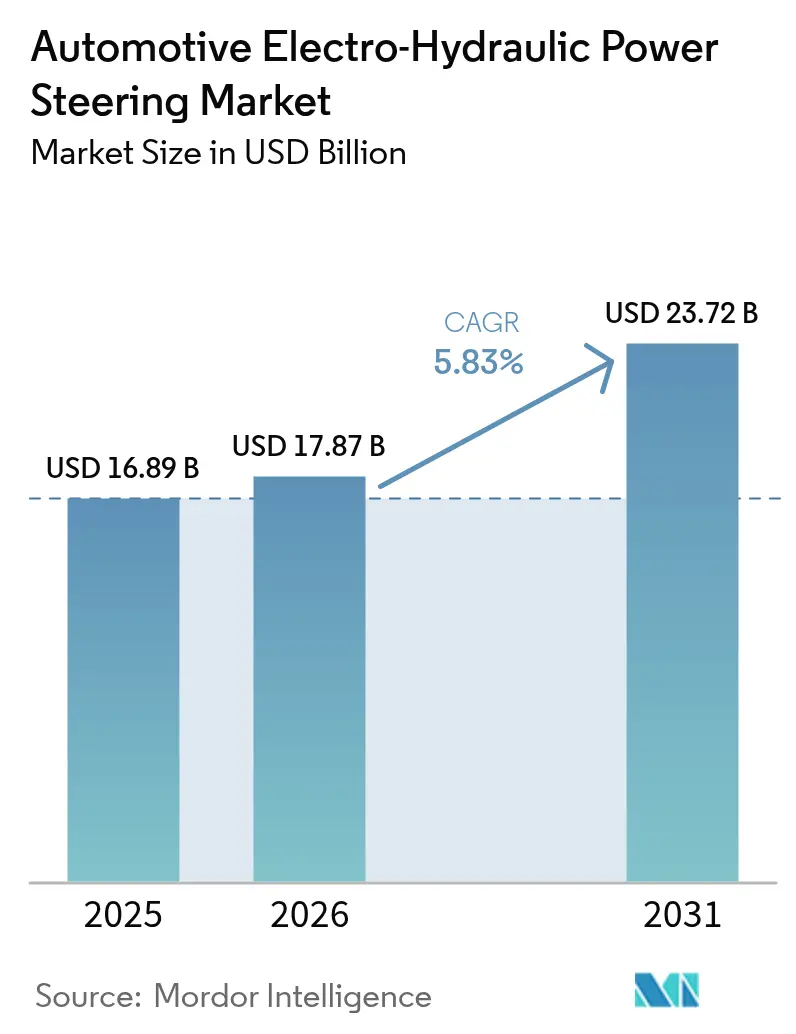

| Market Size (2026) | USD 17.87 Billion |

| Market Size (2031) | USD 23.72 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electro-Hydraulic Power Steering Market Analysis by Mordor Intelligence

The automotive electro-hydraulic power steering market size was valued at USD 16.89 billion in 2025 and estimated to grow from USD 17.87 billion in 2026 to reach USD 23.72 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). This outlook stems from rising electric vehicle production, stricter global emissions rules, and growing requirements for steer-by-wire readiness that demand higher steering energy efficiency. Passenger car and light commercial vehicle electrification is lifting auxiliary 12 V loads, which improves the relative energy profile of on-demand EHPS pumps compared with belt-driven hydraulic systems. Autonomous driving programs call for fail-operational steering architectures, further reinforcing EHPS adoption. Rare-earth material constraints represent the main supply risk, while full electric power steering creates competitive pressure in smaller vehicle segments. Yet EHPS remains the bridge technology that pairs hydraulic force capability with electronic control flexibility, positioning suppliers to benefit across internal combustion, hybrid, and battery-electric platforms.

Key Report Takeaways

- By vehicle type, passenger cars led with 63.86% of the automotive electro-hydraulic power steering market share in 2025, while light commercial vehicles are set to expand at a 7.18% CAGR through 2031.

- By component type, steering motors captured 36.23% share of the automotive electro-hydraulic power steering market size in 2025, whereas sensors and torque modules will accelerate at a 7.61% CAGR to 2031.

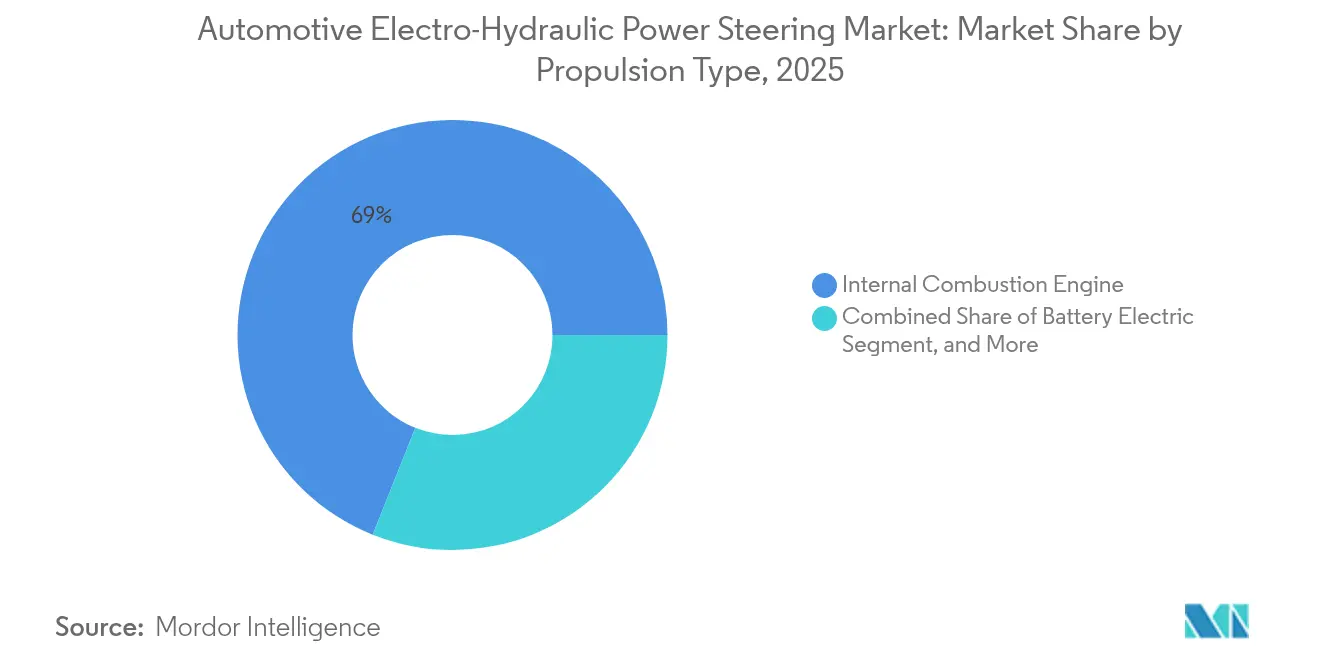

- By propulsion type, internal combustion vehicles held 68.95% of the automotive electro-hydraulic power steering market share in 2025; battery electric vehicles present the fastest growth at 9.08% CAGR over the forecast window.

- By sales channel, the OEM channel commanded 88.95% share of the automotive electro-hydraulic power steering market size in 2025, while the aftermarket is forecast to expand at an 8.42% CAGR to 2031.

- By geography, Asia-Pacific dominated with 47.12% of the automotive electro-hydraulic power steering market share in 2025 and is set to grow at an 8.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Electro-Hydraulic Power Steering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EV production and higher auxiliary 12 V loads | +1.2% | China, Europe, North America | Medium term (2-4 years) |

| OEM demand for steering redundancy for L3+ ADAS | +1.5% | Global premium segments | Medium term (2-4 years) |

| Rapid electrification of light commercial vehicles | +0.9% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Tightening CO₂ and CAFÉ regulations | +0.8% | North America, European Union, expanding Asia-Pacific | Long term (≥ 4 years) |

| Integration of steer-by-wire modules with EHPS pumps | +0.7% | Early adoption in China and Germany | Long term (≥ 4 years) |

| Local sourcing incentives in China and India | +0.6% | China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing EV Production and Higher Auxiliary-12 V Loads

Escalating battery electric and plug-in hybrid volumes raise auxiliary loads for climate, infotainment, and safety functions, which amplifies the efficiency gap between on-demand EHPS pumps and continuously driven hydraulic pumps. Global EV sales reached 14 million units in 2024, with battery electric vehicles taking 73% of deliveries, creating a sizeable addressable base for EHPS systems[1] “Global EV Outlook 2025,” International Energy Agency, iea.org. Commercial segments follow a similar path as electric buses logged 30% shipment growth in 2024, encouraging the adoption of energy-saving steering solutions. The engineering priority now focuses on pump control algorithms coordinating with vehicle energy management to minimize current draw during steady-state cruising.

OEM Demand for Steering Redundancy for L3+ ADAS

Level 3 and above automated driving creates fail-operational steering requirements under ISO 26262, stipulating ASIL-D integrity for steering control[2] “ISO 26262-1:2018 Road Vehicles Functional Safety,” International Organization for Standardization, iso.org. EHPS architecture, with its dual electric motor and hydraulic assist paths, delivers the redundancy and fault tolerance needed to maintain steerability during power interruptions or actuator faults. Recent production launches such as the steer-by-wire solution in NIO’s ET9 highlight how EHPS modules pair with electronic actuation to achieve variable steering ratios and emergency intervention. Suppliers, therefore, align R&D toward diagnostics, sensor fusion, and fallback strategies that satisfy functional safety audits

Rapid Electrification of Light Commercial Vehicles

Light commercial vehicle registrations for zero-emission drivetrains doubled in 2024 across China, Europe, and the United States, reflecting urban delivery electrification and local access restrictions. Fleet operators favor EHPS because demand-based pumps cut parasitic losses during extended idle cycles, which is common in parcel and grocery delivery duty profiles. Lower maintenance needs relative to belt-driven hydraulics further strengthen the business case, so component suppliers customize pump algorithms for high stop-start usage.

Integration of Steer-By-Wire Modules With EHPS Pumps

Steer-by-wire systems eliminate mechanical links to the road wheels, yet many programs retain an EHPS pump as the secondary actuation path to meet functional safety fallback. Early adopters in China and Germany are procuring integrated modules that package the pump, motor, ECU, and pressure accumulator into a single unit. This consolidation eases packaging constraints and supports software-defined chassis control strategies coming to market in premium electric platforms[3]“ZF Steer-by-Wire Series Production Starts for NIO,” ZF Friedrichshafen AG, zf.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Volatility Of Rare-Earth PM Motors | -1.1% | Global, with highest impact in Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Competition From Full-Electric Power Steering (EPS) In B-/C-Segment Cars | -0.8% | Global, particularly acute in volume passenger car segments | Medium term (2-4 years) |

| Up-Front Cost Premium Vs. Conventional HPS | -0.9% | Global, particularly acute in price-sensitive segments | Short term (≤ 2 years) |

| Reliability Concerns In High-Temperature Duty Cycles | -0.7% | Global, with highest impact in hot climate regions and heavy-duty applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility of Rare-Earth Permanent Magnet Motors

Neodymium, dysprosium, and terbium supply remains concentrated in small mines, with China accounting for more than 60% of refined output[4] “Circular on Strengthening Export License Management for Rare-Earth Products,” Ministry of Commerce People’s Republic of China, mofcom.gov.cn. Export licensing changes in 2024 raised spot prices and strained inventory, prompting automakers to review magnet-free synchronous reluctance motors and to dual-source pump assemblies. Steering suppliers are lengthening safety stocks and entering direct offtake agreements with miners to stabilize lead times.

Up-Front Cost Premium vs Conventional HPS

Electronic pumps, sensors, and ECUs add 15%–20% to the steering bill of materials in low-margin B and C segment vehicles. Consumers in emerging markets remain price sensitive, and OEMs face tight cost targets. Automation and higher production volumes are helping close the gap. Industry cost models show parity between EHPS and hydraulic pumps will be attainable once global electric vehicle output passes 20 million units annually, which many forecasts expect by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Lead Despite Commercial Growth

Passenger cars commanded 63.86% of the electric hydraulic power steering market in 2025 on the strength of widespread adoption across compact, mid-size, and luxury platforms. Carmakers integrate EHPS to unlock stop-start compatibility, mild hybrid gains, and growing ADAS content. Electric hydraulic power steering market size for light commercial vehicles is projected to expand at a 7.18% CAGR because parcel fleets favor energy savings during urban duty cycles.

The passenger car share reflects efficient scale, model refresh cadence, and high configuration volumes that absorb the added cost of electronic pumps. Commercial vehicle programs show faster unit growth as final mile delivery regulations tighten in China, Europe, and several United States states. Heavy trucks and buses trail but represent future upside once battery pack economics and high voltage steering actuation converge.

By Component Type: Motors Dominate While Sensors Accelerate

Steering motors held 36.23% electric hydraulic power steering market share in 2025. Their high material value and critical performance role anchor the component mix. Sensors and torque modules will record a 7.61% CAGR through 2031, driven by ISO 26262 redundancy targets that double the number of position and torque sensing channels per system.

Permanent magnet brushless motors remain the industry standard because they deliver high power density and rapid response. Suppliers are investing in ferrite-based or reluctance designs to sidestep rare-earth exposure. Control ECUs migrate toward higher bandwidth microcontrollers as steer-by-wire software layers expand, while sealed pump housings incorporate integrated cooling jackets to extend duty cycles.

By Propulsion Type: ICE Leads Despite BEV Acceleration

Internal combustion vehicles represented 68.95% share in 2025, yet battery electric platforms will advance at a 9.08% CAGR, reflecting global electrification mandates. The electric hydraulic power steering market size for BEVs will reach USD 7.74 billion by 2031, supported by auxiliary power synergies and the elimination of engine-driven pumps.

ICE models still dominate worldwide unit production, and EHPS brings incremental fuel economy gains by removing belt loading. Hybrid architectures use EHPS for seamless engine-on-off transitions, while fuel cell trucks require electronic pumps to manage low-temperature start capability. The propulsion mix, therefore, underlines EHPS flexibility across drivetrain types.

By Sales Channel: OEM Dominance With Aftermarket Potential

The OEM channel accounted for 88.95% of the electric hydraulic power steering market size in 2025, reflecting safety homologation needs that favor factory installation. Aftermarket demand is forecast at an 8.42% CAGR through 2031 as the global EHPS park ages and service networks develop specialized calibration skills.

Vehicle manufacturers tightly integrate steering software with chassis controllers, so replacement parts require VIN-matched coding. Independent parts distributors see opportunity in commercial fleets that retrofit EHPS for energy savings. Component makers are expanding remanufactured pump programs and diagnostic tooling to capture post-warranty revenue.

Geography Analysis

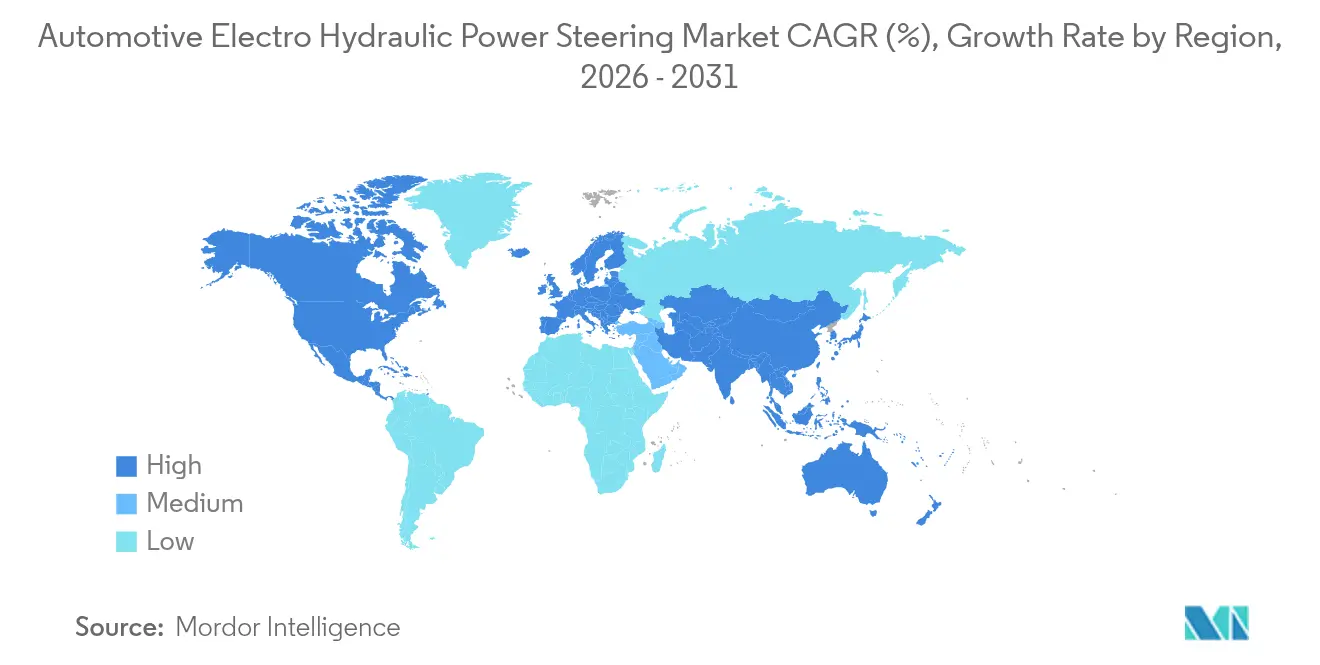

Asia-Pacific remains the clear demand center. The region accounted for 47.12% electric hydraulic power steering market share in 2025 and is projected to expand at an 8.63% CAGR through 2031, making it the largest and fastest-growing territory. China’s battery-electric and plug-in hybrid production scale drives high pump volumes. India’s FAME-II and PLI schemes channel local sourcing toward domestic steer-by-wire and pump facilities. Japan contributes high-reliability sensors and motor controls that meet ISO 26262 targets for export models. Regional suppliers benefit from government incentives that lower landed costs and shorten supply chains for OEM plants clustered in Shanghai, Guangzhou, Chennai, and Nagoya.

North America follows with steady expansion as emissions rules tighten. The EPA’s Multi-Pollutant Standards and California’s Advanced Clean Cars II program compel automakers to electrify auxiliaries, including steering, to meet fleet targets. Battery-electric delivery van adoption has doubled since 2024, pulling EHPS content into parcel and grocery fleets. Domestic automakers also hedge rare-earth risk by funding ferrite and reluctance motor research, which supports regional electric hydraulic power steering market size resilience against supply shocks. Canada’s clean-transport credits mirror United States policy and reinforce cross-border production synergies.

Europe anchors premium vehicle innovation. German, Swedish, and French brands are rolling out steer-by-wire platforms that integrate EHPS pumps as safety-redundant actuators, and ZF began series production for a Chinese luxury marque in early 2025. The European Union target of a 55% fleet-wide CO₂ cut by 2030 keeps pressure on suppliers to deliver efficiency gains at component level. As luxury and performance segments migrate to 800 V architectures, EHPS modules with smart energy-recovery algorithms complement brake-by-wire and active suspension systems. Eastern Europe and the Middle East provide emerging assembly bases, but infrastructure gaps and price sensitivity temper near-term penetration, positioning Asia-Pacific as the principal growth engine through the decade.

Regulatory Landscape

Regulation affecting electro-hydraulic power steering (EHPS) is increasingly tied to electronic steering control, automated driving, and functional safety. ISO 26262 is used as a baseline for functional safety programs in OEM sourcing, while ISO 19725:2026 adds steer-by-wire system safety guidance for passenger cars and light commercial vehicles. That framework informs how EHPS is engineered as a redundant actuation path in fail-operational architectures.

On the type-approval side, UNECE WP.29 work under GRVA continues refining UN Regulation No. 79 (steering equipment) to cover requirements for advanced steering functions and steer-by-wire concepts. In the United States, Section 232 trade measures on automobiles and auto parts affect sourcing strategies for steering motors, ECUs, and pump assemblies. The process for adding parts to the Section 232 scope is managed through a recurring quarterly inclusions window (January, April, July, and October), and tariff offset mechanisms link duty relief to vehicles assembled domestically.

Value Chain Analysis

The EHPS value chain begins with upstream materials and electronics, including rare-earth permanent magnets (used in many steering motors), copper windings, power semiconductors, sensors, and synthetic hydraulic fluids. These inputs move into Tier-2 and Tier-3 manufacturing for motors, pump elements, valves, and PCB assemblies, before Tier-1 integration combines the motor, hydraulic pump, reservoir, ECU/controller, and sensor/torque modules into an application-specific EHPS unit.

Downstream, direct OEM procurement remains the primary route to market because vehicle-level safety validation, software integration, and end-of-line calibration are required. The aftermarket is smaller and more service-intensive, with diagnostic tooling and VIN-matched coding needed when steering control ties into chassis controllers. Bottlenecks tend to concentrate around precision motor capacity and rare-earth exposure, while modularization of the pump-motor-ECU assembly supports reuse across passenger cars and light commercial vehicles with different voltage and duty-cycle requirements.

Competitive Landscape

Automtotive electro-hydraulic power steering market is dominated by several key players such as JTEKT, Bosch, and ZF combine deep steering domain expertise with global manufacturing footprints that support large platform awards. Nexteer and NSK expand portfolios into actuation software, while Continental and Schaeffler invest in electronics and mechatronics to participate in software-defined chassis programs.

Strategic moves target technology differentiation. In February 2025, ZF began series production of steer-by-wire units for NIO and secured a global chassis contract that bundles electromechanical braking with electric recirculating ball steering. Bosch exhibited an electric brake system at CES 2025 that coordinates motor and hydraulic circuits and enables enhanced accessibility for disabled drivers. These examples illustrate the shift toward integrated motion control architectures.

New entrants focus on rare-earth-free motors, over-the-air update capability, and cyber-secure domain controllers. Established suppliers respond with joint ventures, longer raw material contracts, and higher software staffing. Pricing power remains balanced because OEMs want dual sourcing yet depend on proven safety performance.

Automotive Electro-Hydraulic Power Steering Industry Leaders

JTEKT Corporation

Robert Bosch GmbH

Mando Corporation

ZF Friedrichshafen AG

Nexteer Automotive Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Steer-by-wire industrialization is creating a clear area for EHPS, particularly as a safety-redundant actuator path in linkless steering architectures. The key focus for these programs is showing high-integrity behavior under ECE R79-type steering requirements alongside ASIL-D functional safety targets. This demand is supported by supplier activity already underway, including Nexteer bringing a steer-by-wire system into mass production for a Chinese new energy vehicle manufacturer (announced in April 2026) and reporting ASIL D functional safety certification obtained in late 2025. As steer-by-wire scales, integrated EHPS modules that package pump, motor, ECU, sensing, and accumulators can help simplify vehicle packaging and validation.

A second opportunity is in electrified light commercial vehicles and other high-duty steering applications where hydraulic assist capability and on-demand energy use continue to matter. OEMs are also adding more electronic content to support redundancy, diagnostics, and software-defined chassis control. Rare-earth permanent magnet supply risk keeps demand active for alternate motor topologies and multi-sourcing of pump assemblies, which supports suppliers that can qualify magnet-lean or rare-earth-free designs without compromising thermal performance or functional safety compliance.

Recent Industry Developments

- April 2026: Nexteer Automotive announced its steer-by-wire system has entered mass production for a Chinese new energy vehicle manufacturer. The move scales linkless steering beyond pilots and increases demand for redundant steering architectures where EHPS can serve as a hydraulic fallback or secondary actuation path within safety cases.

- February 2025: ZF began series production of steer-by-wire systems for NIOs ET9, marking a high-visibility production milestone for electronically controlled steering. This series launch strengthens the supplier ecosystem for fail-operational steering functions and accelerates integration work across steering, braking, and software-defined chassis domains.

- November 2024: Volkswagen and Ansys announced a collaboration on model-based development for steer-by-wire controllers designed to meet ASIL-D requirements. The partnership highlights the rising importance of simulation-led verification and validation, raising the bar for steering ECU, sensor redundancy, and diagnostic strategies used alongside EHPS modules in advanced vehicle platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers electro-hydraulic power steering (EHPS) systems used in road vehicles, where an electric motor drives a hydraulic pump to provide steering assist, and revenues are measured in USD across OEM and replacement demand.

Scope exclusions: This sizing does not count pure hydraulic steering without an electric pump, and it also excludes fully electric power steering units that do not use a hydraulic circuit.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Buses and Coaches

- Off-highway and Specialty Vehicles

- By Component Type

- Steering Motors

- Hydraulic Pumps

- Sensors and Torque Modules

- ECU / Controllers

- Reservoirs, Hoses and Others

- By Propulsion Type

- Internal-Combustion Engine (ICE)

- Hybrid Electric Vehicle (HEV)

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicles

- Fuel-Cell Electric Vehicle (FCEV)

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Vietnam

- Philippines

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting demand picture and the rules for what gets counted as EHPS revenue. We relied on public series such as vehicle production and registrations from sources like OICA, national transport agencies, and customs statistics for steering-related imports and exports, which helped us see where volumes were moving by region.

To keep the model aligned with real product and cost structure, we reviewed sources such as NHTSA and UNECE regulatory and safety materials, patent filings, peer-reviewed automotive engineering literature, and association publications that discuss steering architectures and pump-motor integration. We complemented this with company filings, investor presentations, and trusted automotive press to understand adoption signals and timing. In a few places, subscription databases were used for company financial intelligence, patent analytics, and shipment-level trade checks. The sources listed here are illustrative, and many other public references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating EHPS fitment patterns and price logic across passenger cars and commercial vehicles, then stress-testing the assumptions with engineering, procurement, and channel viewpoints. We spoke with respondents tied to OEM supply chains, component makers, and aftermarket distributors across APAC, EMEA, and the Americas. Their input was used to close gaps in adoption rates, average selling prices, and the split between OEM and replacement demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 46% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 35% |

| Smaller Players: 16% | Managers: 54% | Americas: 19% |

Market-Sizing & Forecasting

The sizing starts with a top-down demand pool build that reconstructs EHPS consumption from vehicle output and technology penetration by region, and then converts units into value using modeled system pricing. Where the market is less transparent, selective bottom-up approximations were used to keep totals realistic, including sampled system ASP times fitted volumes for key vehicle classes, plus channel checks on replacement activity.

Key model inputs included global vehicle production by type, EHPS fitment rates by propulsion where relevant, OEM versus aftermarket mix, typical replacement cycles for hydraulic components, and ASP progression linked to motor-pump integration and sensor content. Because steering choices can shift with platform launches, we also tracked regulatory and efficiency pushes that influence OEM design decisions, and then we applied scenario analysis to reflect different adoption speeds across regions. Gaps in the bottom-up checks were handled by using conservative ranges from interviews, and then narrowing them once the implied value per vehicle aligned with observed pricing bands.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as vehicle build trends, component demand indicators, and trade movements for steering and hydraulic sub-assemblies, followed by variance checks at region and vehicle-type level. When an outlier appeared, assumptions were revisited and, if needed, respondents were re-contacted to confirm whether the change reflected a true market shift or was a modeling artifact.

Before sign-off, the model and the write-up go through step-by-step analyst reviews so calculations, scope rules, and trend stories match. Reports are refreshed annually, and interim updates are triggered by material events such as major production swings, regulatory changes, or pricing shocks. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Electro Hydraulic Power Steering Market Estimate Compared With Other Published Estimates

Published market sizes for EHPS can look far apart because the scope line is not always drawn the same way, and because the pricing logic behind a system can be treated differently across studies. Differences also come from the forecast window chosen, the year used as the anchor, and whether OEM demand is mixed with longer-horizon technology narratives.

Vehicle production signals, OEM fitment patterns by region, and the OEM versus aftermarket split are the checks that keep the Mordor Intelligence number tied to EHPS-installed demand, and they also prevent EPS and conventional HPS value from being blended into the same total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.87 B (2026) | |

| Trade Publisher A | USD 15.10 B (2025) | Uses a different base year and a longer horizon that can blend near-term OEM fitment reality with more gradual technology adoption, which shifts the implied ramp and starting value. |

| Industry Aggregator B | USD 11.74 B (2025) | Narrower component accounting and conservative pricing assumptions can lower the system value per vehicle, especially if ECU, sensors, or integrated modules are treated as out-of-scope. |

The comparison shows that the spread is mainly explained by year selection and what each source counts inside an EHPS system bill of materials. By keeping scope rules explicit, pressure-testing fitment and pricing through interviews, and then reconciling totals back to vehicle-driven demand, the estimate stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the current size of the electric hydraulic power steering market?

The electric hydraulic power steering market size stood at USD 17.87 billion in 2026 and is forecast to expand to USD 23.72 billion by 2031.

Which region leads the electric hydraulic power steering market?

Asia-Pacific leads with 47.12% market share in 2025 and is also the fastest growing region with an 8.63% CAGR through 2031.

How do emissions regulations influence EHPS adoption?

Tighter CO₂ and CAFÉ rules push automakers to electrify auxiliary systems; EHPS replaces belt-driven pumps, yielding measurable efficiency gains that support regulatory compliance.

What is driving aftermarket growth for EHPS components?

An expanding global vehicle park equipped with EHPS, coupled with rising expertise in electronic steering diagnostics, is generating an 8.42% CAGR for the aftermarket channel.

How vulnerable is the EHPS supply chain to rare-earth shortages?

The sector faces short term risk because neodymium and dysprosium supplies are highly concentrated. Suppliers are pursuing magnet-free motor designs and diversified sourcing to mitigate this exposure.

Page last updated on: