Scandinavian Commercial Real Estate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

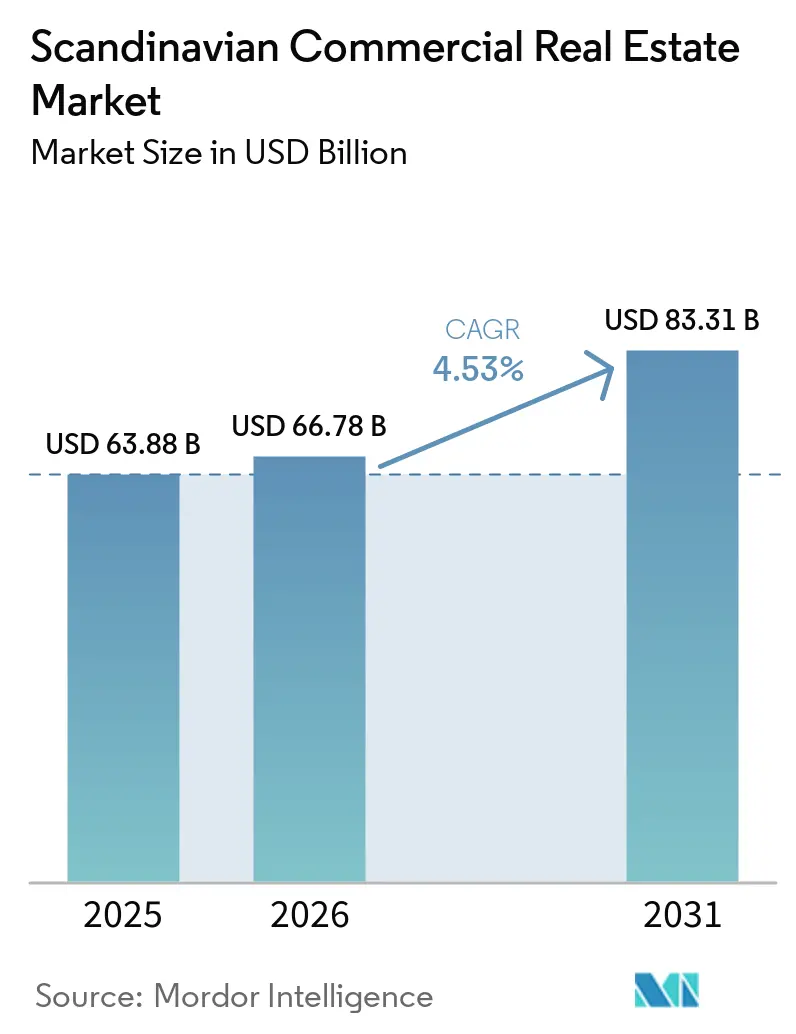

| Base Year Market Size (2025) | USD 63.88 Billion |

| Market Size (2026) | USD 66.78 Billion |

| Market Size (2031) | USD 83.31 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

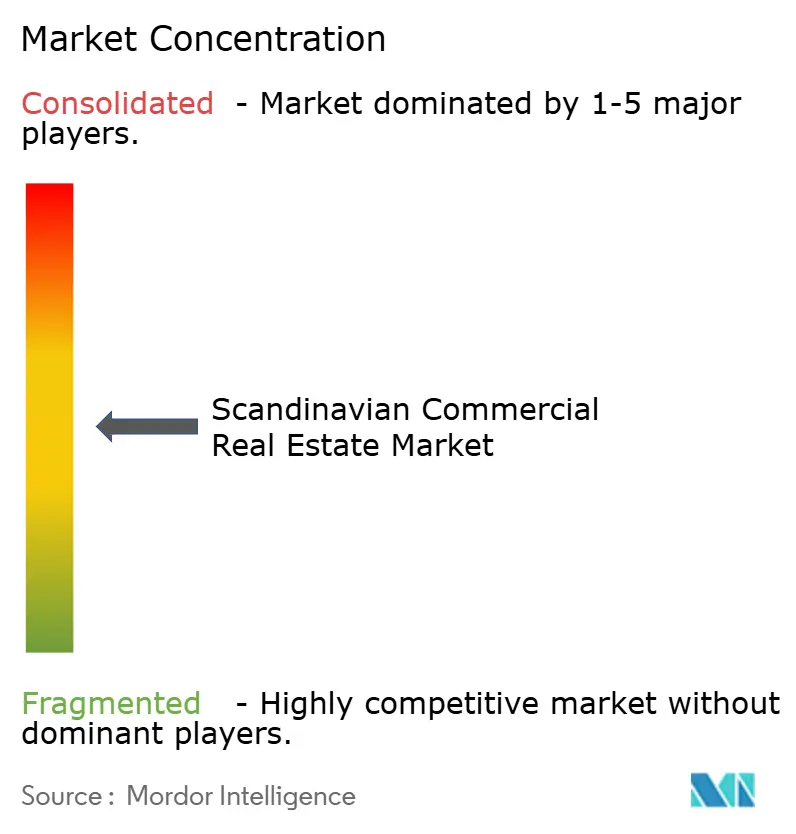

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scandinavian Commercial Real Estate Market Analysis by Mordor Intelligence

The Scandinavian commercial real estate market size is expected to grow from USD 63.88 billion in 2025 to USD 66.78 billion in 2026 and is forecast to reach USD 83.31 billion by 2031 at 4.53% CAGR over 2026-2031. Steady growth reflects a mature environment where institutional investors tilt portfolios toward energy-efficient buildings rather than purely yield-driven assets. Sovereign wealth funds accelerate this tilt, especially after Norway’s Government Pension Fund Global (GPFG) pledged net-zero emissions for its unlisted holdings by 2050. Stable borrowing costs follow the European Central Bank’s 25-basis-point rate cut in 2024, while cross-border capital still grapples with Swedish krona volatility[1]European Central Bank, “Euro Area Bank Interest-Rate Statistics: April 2025,” European Central Bank, ecb.europa.eu. Country demand remains anchored in Sweden’s technology-focused economy, yet Denmark now captures logistics attention as the Fehmarnbelt link nears completion. Office buildings still dominate volume, but logistics warehouses post the fastest absorption on record, vacancy lows around the Oresund corridor.

Key Report Takeaways

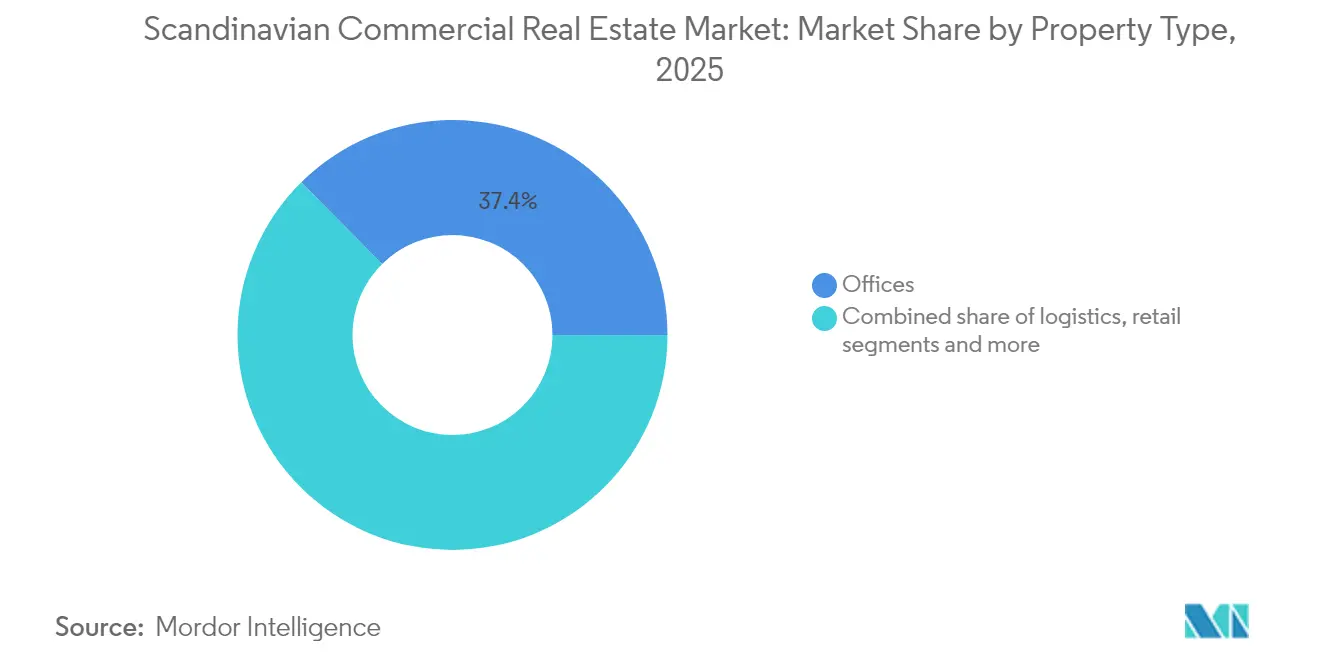

- By property type, offices led with 37.42% of the Nordic commercial real estate market share in 2025, whereas logistics is projected to grow at a 4.73% CAGR through 2031.

- By business model, sales transactions held 70.25% of the Nordic commercial real estate market size in 2025; rental structures advance at a 4.92% CAGR to 2031.

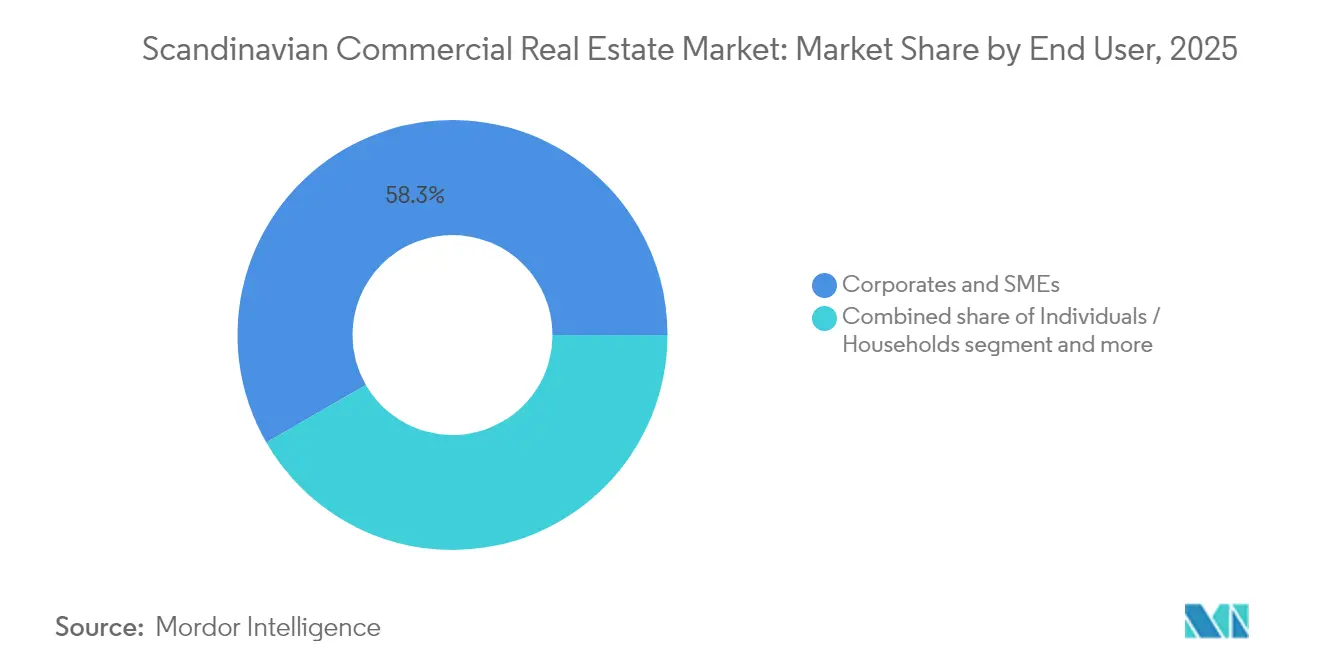

- By end-user, corporates and SMEs commanded a 58.33% share in 2025, and individuals drove the fastest growth at a 4.76% CAGR.

- By geography, Sweden contributed 45.60% of the Nordic commercial real estate market in 2025, while Denmark records the highest forecast CAGR at 4.62% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Scandinavian Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing prime-office stock triggering refurbish-first investment wave | +0.8% | Sweden, Norway | Medium term (2-4 years) |

| Sovereign-wealth-backed green-building mandates | +0.6% | Nordic region | Long term (≥4 years) |

| Retail-to-last-mile conversion subsidies in Sweden | +0.4% | Sweden, Denmark | Short term (≤2 years) |

| Data-centre corridor incentives in Norway | +0.5% | Norway, northern Sweden | Medium term (2-4 years) |

| Record-low logistics vacancy around the Oresund | +0.3% | Denmark, southern Sweden | Short term (≤2 years) |

| Pension-fund reallocations from bonds to Nordic multifamily | +0.7% | Nordic region | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Ageing Prime-Office Stock Triggering Refurbish-First Investment Wave

Large office blocks built in the late 1980s are due for energy retrofits to satisfy tight ESG standards. Sweden’s proposal to raise the safe-harbor limit on interest deductions to USD 2.4 million encourages investors to finance deep renovations beyond routine upkeep. Skanska’s USD 55.1 million Regndroppen project in Malmö illustrates capital flowing to certified, low-carbon refurbishments. Higher-spec space now secures premium rents and longer leases as tenants downsize but upgrade. Non-certified stock risks valuation discounts, reinforcing a two-tier office market.

Sovereign-Wealth-Backed Green-Building Mandates

GPFG targets a 40% carbon-intensity cut by 2030, already aligning 43% of its portfolio with a 1.5 °C pathway. Denmark raises the bar too, capping new-build emissions at 7.1 kg CO₂e/m²/year from mid-2025, roughly 15% tighter than prior rules. Developers who integrate on-site renewables and circular materials unlock a cost-of-capital advantage as lenders price green premiums. Retrofits will still play a role, but new builds designed for Swan Ecolabel thresholds win the clearest investor backing.

Retail-to-Last-Mile Conversion Subsidies in Sweden

State aid worth up to USD 2.2 million per energy-intensive company offsets power-price spikes and makes urban logistics schemes financially viable. REMA 1000’s purchase of 64 ex-ALDI stores, expected to yield USD 15 million yearly, typifies retail footprints transitioning into temperature-controlled hubs. The incentive ends in 2025, which accelerates project pipelines as developers race to secure cheaper electricity contracts.

Data-Centre Corridor Incentives in Norway

Oslo’s green-industry roadmap channels NOK 60 billion (USD 6 billion) in risk guarantees toward renewables that power data centres. Bulk Infrastructure’s recurring revenue jumped 160% during Q3 2024, on track for USD 60 million annually from signed hyperscale deals. Natural cooling and low-carbon hydro power drive opex savings that lure AI workloads from mainland Europe. Yet local grid bottlenecks could push completion of some campuses past 2027.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Denmark's 2025 energy-performance regulation cost inflation | -0.4% | Denmark, Sweden | Short term (≤2 years) |

| Sovereign-wealth fund tightening ESG divestment criteria | -0.3% | Nordic region | Medium term (2-4 years) |

| Swedish krona volatility dampening cross-border capital | -0.5% | Sweden | Medium term (2-4 years) |

| Limited REIT-law harmonisation across the region | -0.2% | Nordic region | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Denmark's 2025 Energy-Performance Regulation Cost Inflation

Stricter BR18 rules demand lower carbon footprints and new fire-safety upgrades, stretching retrofit budgets on legacy stock. Certificates last 10 years, but owners of older assets must retrofit sooner to avoid rental downgrades. International investors must also navigate longer permitting cycles, extending holding periods before cash flow stabilises.

Swedish Krona Volatility Dampening Cross-Border Capital

The krona trades 10-15% below euro fair value, increasing hedging costs and eroding leveraged returns. Domestic buyers, however, benefit from the discount and can acquire assets that global funds overlook, leading to a local-versus-foreign pricing gap[2]Swedish Ministry of Finance, “Changes to Interest-Deduction Limitation Rules,” Government Offices of Sweden, government.se.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices Hold 38% Share While Logistics Grows Fastest

Offices accounted for 37.42% of the Nordic commercial real estate market in 2025, underlining deep headquarters demand across Stockholm, Copenhagen, and Oslo. Prime CBD towers capture occupancy from technology and finance tenants that insist on wellness certifications and renewable energy-sourced power. Occupiers pay premiums for proximity to mass transit and onsite amenities, keeping rental uplifts intact even as hybrid working trims space footprints. High-spec buildings command superior valuations, whereas class-B stock suffers from rising vacancy and retrofit expenses.

Logistics assets expand at a 4.73% CAGR, the fastest among all property types through 2031, as cross-border e-commerce and pharma cold-chain requirements escalate. Record-low vacancy around the Oresund feeds rent inflation and development pre-lets. Nomeco’s USD 75 million pharmaceutical hub in Køge highlights how specialist storage creates defensive income streams. Government backing for rail and ferry upgrades shortens delivery lead times, further lifting take-up. In contrast, retail continues to recalibrate; grocery-anchored centres remain defensive, but discretionary malls repurpose excess space into logistics or healthcare units, supporting a gradual supply-demand re-balance.

By Business Model: Sales Transactions Dominate at 71% but Rental Gains Momentum

Sales deals made up 70.25% of the Nordic commercial real estate market share in 2025, affirming investors’ preference for outright ownership to implement bespoke ESG upgrades. GPFG alone holds USD 315 billion in unlisted real estate, underscoring ample dry powder for core and value-add acquisitions. Domestic pension funds likewise rotate from fixed income toward property to hedge inflation and secure long-term cash flows.

Rental-oriented structures are projected to grow at 4.92% CAGR, outpacing outright purchases as corporates favour asset-light strategies. Sale-leasebacks unlock capital without compromising operational control, while flexible lease clauses accommodate headcount shifts. Technology-heavy buildings, such as data centres, increasingly adopt triple-net terms that pass utility and maintenance risk to tenants, raising landlord certainty. As interest-rate cycles normalise, predictable rental streams look more attractive than volatile exit multiples, bolstering demand for income-focused vehicles such as open-ended core funds and listed REITs.

By End-User: Corporates Represent 59% Demand as Retail Investors Accelerate

Corporates and SMEs generated 58.33% of Nordic commercial real estate market demand in 2025, driven by headquarters consolidation and strategic manufacturing footprints for renewables. Professional-services tenants seek wellness-certified space to attract talent, pressing landlords to exceed local green-building codes. Flexible-office operators also target enterprise clients seeking short, service-heavy contracts.

Individual investors, enabled by digital trading apps and fractional ownership structures, are set to expand at a 4.76% CAGR. Platforms lower the minimum ticket size, bringing supply chain warehouses and neighbourhood supermarkets into retail investor portfolios. Prisma Properties’ planned USD 115 million IPO will float a portfolio focused on discount retail, signalling appetite for listed vehicles that combine stable rent rolls with inflation-linked escalators. High household savings and pension reforms that boost voluntary contributions further enlarge the retail capital pool.

Geography Analysis

Sweden remains the heavyweight, securing 45.60% of the Nordic commercial real estate market in 2025 thanks to Stockholm’s status as a regional financial nucleus and robust technology talent pipeline. The country’s allure intensifies after Brookfield pledged USD 10 billion for a 750-megawatt AI campus in Strängnäs, the region’s largest single data-centre plan. Yet krona weakness complicates foreign bids, making domestic institutions the prime buyers of urban offices and logistics sites. Fiscal incentives for energy-intensive industries, capped at USD 2.2 million per firm, shield warehouse margins from power-price volatility and help accelerate retail-to-last-mile conversions.

Denmark delivers the fastest growth, with the market forecast to expand at a 4.62% CAGR between 2026 and 2031. Completion of the Fehmarnbelt Fixed Link by 2028 will slash travel times to Germany, reinforcing Copenhagen’s role as a 24-hour gateway to 100 million consumers. Recent transactions underscore appetite: the Amager Strand portfolio sold for USD 161 million to Wihlborgs, validating prime coastal office pricing even under stricter energy codes. BR18 upgrades inflate retrofit costs, yet well-capitalised funds exploit the gap by acquiring secondary assets at discounts and repositioning them for green certifications.

Norway leverages sovereign-wealth strength to export ESG standards across the Nordic commercial real estate market. GPFG’s 40% carbon-intensity reduction target by 2030 guides underwriting, favouring assets powered by hydro and offshore-wind electricity. Government risk guarantees of USD 6 billion back a green-industry roadmap that stimulates demand for clean-tech manufacturing plants and high-density data hubs. Currency volatility tied to oil prices prompts foreign buyers to hedge exposure, yet domestic entities accept krone swings and thus secure pipeline projects at sharper yields.

Competitive Landscape

Competition in the market remains moderate, with a growing focus on sustainability. Leading institutional investors, such as GPFG and Alecta, are refining their acquisition strategies to prioritize certified assets while actively funding net-zero developments. A notable example is Brookfield’s USD 10 billion investment in a data center in Sweden, marking the largest single-asset commitment in the Nordic commercial real estate market. This move highlights the increasing preference of cross-border capital for high-density, clean-power infrastructure.

Local developers reposition outdated offices and suburban malls into mixed-use clusters. Skanska’s USD 55 million Malmö scheme combines refurbish-first strategy with green leases that offload operating-expense risk onto occupiers. Wihlborgs expands water-adjacent portfolios, banking on Copenhagen Airport spill-over and e-commerce traffic. At the same time, new entrants such as Bulk Infrastructure post 160% revenue growth on the back of hyperscale contracts, challenging incumbents that lack specialist power-and-fiber expertise.

Currency shifts create a two-speed market. Domestic pensions exploit krona weakness to acquire discounted Swedish towers, while foreign core funds pivot toward Denmark’s euro-pegged environment for currency stability. Digital fund-raising platforms broaden competition by pooling thousands of small tickets into single-asset vehicles, raising execution speeds on sub-USD 50 million deals. Overall, ESG differentiation, access to cheap renewable energy, and capital-market agility separate winners from laggards.

Scandinavian Commercial Real Estate Industry Leaders

Vasakronan AB

Castellum AB

Fabege AB

Balder Fastigheter

NREP (Logicenters)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Brookfield to invest up to USD 10 billion in a 750 MW AI-ready data-centre campus in Strängnäs, Sweden.

- May 2025: Amager Strand Portfolio near Copenhagen Airport sold for USD 161 million to Wihlborgs, reflecting sustained demand for Danish offices.

- March 2025: Norway’s oil fund bought a 25% stake in Covent Garden for USD 741 million, extending its European diversification strategy.

- February 2025: Skanska committed USD 55.1 million to the Regndroppen office redevelopment in Malmö, targeting delivery in 2027.

Scandinavian Commercial Real Estate Market Report Scope

The report provides key insights into the Scandinavia commercial real estate market. It focuses on the market dynamics, technological trends, and government initiatives taken in the residential real estate sector. Also, the report sheds light on the key trends in the market, like factors driving the market, the restraints to market growth, and opportunities in the future. Additionally, the competitive landscape of the commercial real estate market of Scandinavia is depicted through the profiles of key players active.

| Offices |

| Retail |

| Logistics |

| Others (Industrial, Hospitality, etc.) |

| Sales |

| Rental |

| Individuals / Households |

| Corporates & SMEs |

| Others |

| Denmark |

| Norway |

| Sweden |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (Industrial, Hospitality, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Country | Denmark |

| Norway | |

| Sweden |

Key Questions Answered in the Report

What is the current size of the Nordic commercial real estate market?

It stands at USD 66.78 billion in 2026 with a projected value of USD 83.31 billion by 2031.

Which property segment leads the market today?

Office buildings hold 37.42% of market share, driven by corporate headquarters demand in Stockholm, Copenhagen, and Oslo.

Why is Denmark forecast to grow the fastest?

Growth at 4.62% CAGR stems from the Fehmarnbelt Fixed Link, strict green-building codes that spur refurbishments, and strong logistics demand.

How does currency risk affect investors?

A weak Swedish krona increases hedging costs for foreign buyers, discouraging some cross-border deals while giving local funds a pricing edge.

What role do sovereign wealth funds play?

Norway’s Government Pension Fund Global sets stringent carbon targets and directs sizable capital toward low-emission buildings, influencing regional standards.

Which emerging trend should investors watch?

Data-centre expansion powered by renewable energy, highlighted by Brookfield’s USD 10 billion commitment, is poised to reshape industrial sub-markets across the Nordics.

Page last updated on: