Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

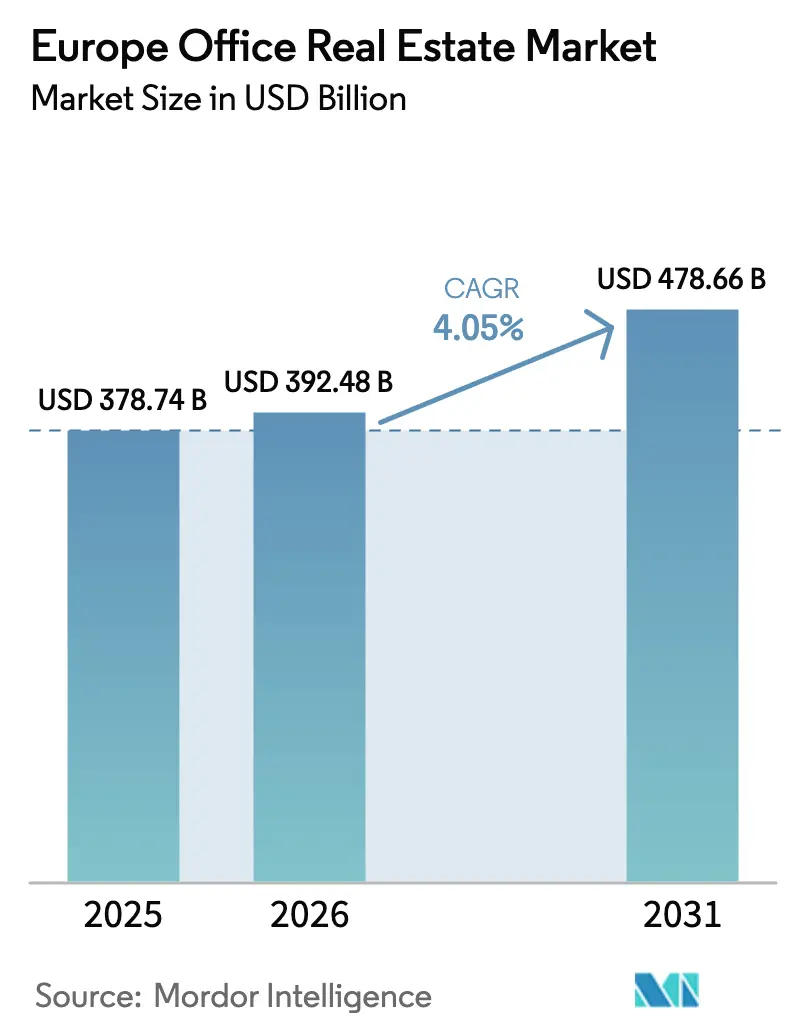

| Base Year Market Size (2025) | USD 378.74 Billion |

| Market Size (2026) | USD 392.48 Billion |

| Market Size (2031) | USD 478.66 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Office Real Estate Market Analysis by Mordor Intelligence

The Europe Office Real Estate Market size is projected to be USD 378.74 billion in 2025, USD 392.48 billion in 2026, and reach USD 478.66 billion by 2031, growing at a CAGR of 4.05% from 2026 to 2031.

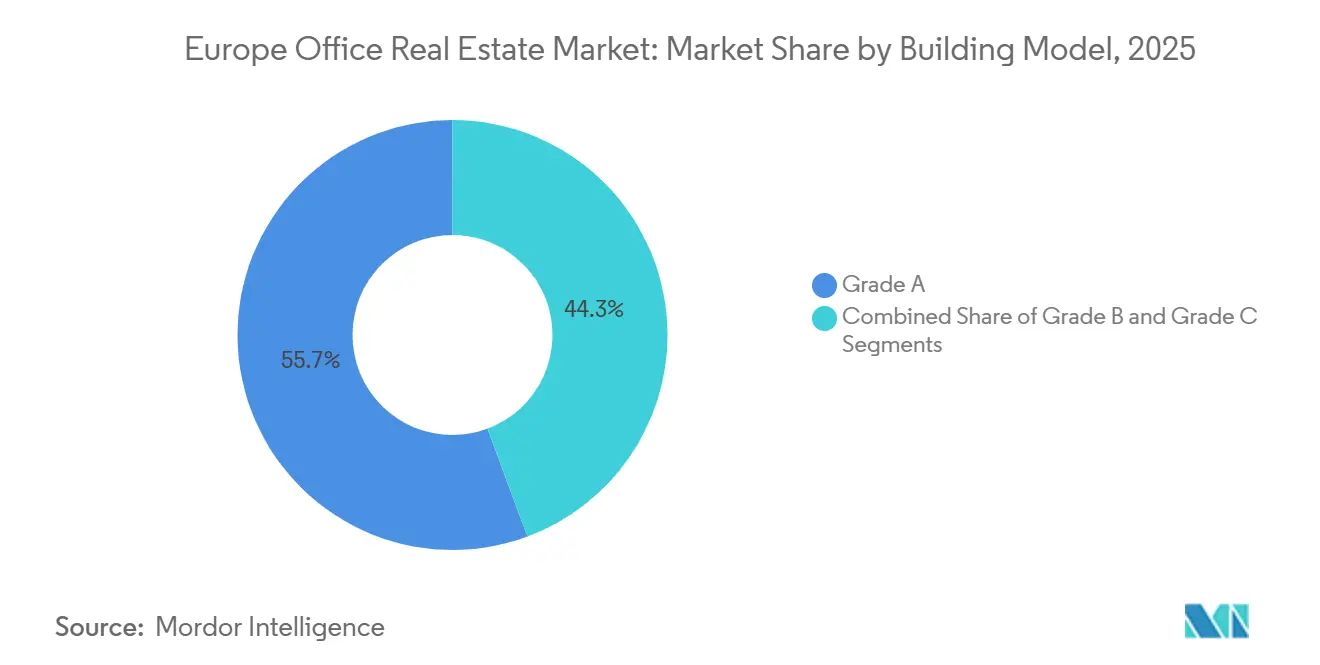

Landlords holding Grade A assets captured 55.68% of the 2025 transaction value, illustrating that investors are concentrating capital into certified, energy-efficient buildings despite continuing hybrid-work uncertainty. Rental transactions dominated with a 74.88% share of deal flow in 2025, yet sales are projected to outpace leasing by advancing 5.15% annually through 2031 as institutional funds seek long-duration cash flows that hedge inflation. Germany anchored 29.58% of activity in 2025, but the Rest of Europe, Central and Eastern hubs, Iberian cities, and Nordic capitals will deliver the fastest 5.52% CAGR as nearshoring and data-center projects redirect tenants toward lower-cost corridors. Headline risks include a persistent sublease overhang, embodied-carbon rules, and 15-minute-city zoning that collectively shrink conventional pipelines, while the EU Energy Performance of Buildings Directive (EPBD) accelerates obsolescence of non-compliant stock and raises prime rent expectations in certified towers.

Key Report Takeaways

- By building grade, Grade A properties held 55.68% of the European office real estate market share in 2025, while the same grade is advancing at a 4.99% CAGR through 2031.

- By transaction type, the rental segment accounted for 74.88% of the European office real estate market size in 2025, and sales are projected to grow at a 5.15% CAGR through 2031.

- By end user, IT & ITES tenants led with 32.08% of the European office real estate market share in 2025, whereas the same cohort is also the fastest-expanding at a 5.37% CAGR to 2031.

- By country, Germany captured 29.58% of the 2025 value, while the Rest of Europe is forecast to post the steepest 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nearshoring by US and Asian tech giants | +0.9% | Germany, UK, Ireland, Netherlands | Medium term (2-4 years) |

| EU EPBD 2026 zero-emission mandate accelerating green upgrades | +0.8% | Germany, France, Netherlands, pan-EU | Short term (≤ 2 years) |

| AI-data-center ecosystem spillover | +0.7% | Frankfurt, London, Amsterdam, Paris, Dublin, Nordics | Medium term (2-4 years) |

| Corporate Science Based Targets net-zero pledges | +0.6% | UK, Germany, France | Medium term (2-4 years) |

| EU Recovery & Resilience Facility funds | +0.5% | Poland, Czech Republic, Romania | Long term (≥ 4 years) |

| Tradable digital building passports | +0.4% | Denmark, Estonia, Netherlands, pilot EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nearshoring Expansion of US and Asian Tech Giants into Tier-1 European Cities Raising Large-Floorplate Absorption

Microsoft, Google, ByteDance, and Tencent expanded their hubs in Germany, Ireland, and the Netherlands during 2025, each signing contiguous blocks exceeding 5,000 m² to co-locate engineering and cloud operations teams. Frankfurt’s Q1 2025 take-up hit 194,600 m², the strongest quarterly absorption since 2019, and lifted prime rents to USD 52 per m² per month. High-spec, edge-compute-adjacent floorplates are leasing before completion, pulling forward revenue recognition for developers but capping upside if market rents accelerate faster than fixed escalators. Secondary cities lacking fiber connectivity or international airports have failed to capture comparable volumes, widening geographic divergence across the region.

EU EPBD 2026 Zero-Emission Mandate Accelerating Pre-Emptive Green Upgrades

The Energy Performance of Buildings Directive requires all new non-residential construction after 2026 to emit zero on-site fossil-fuel emissions and imposes phased retrofits for existing assets by 2030. Landlords in Germany and the Netherlands have front-loaded heat-pump, façade-insulation, and rooftop-solar programs, compressing cap rates on certified assets by as much as 75 basis points compared with non-compliant peers [1]European Commission, “Energy Performance of Buildings Directive,” ENERGY.EC.EUROPA.EU. Retrofit costs averaging USD 165–275 per m² are squeezing small owners but rewarding early movers with 10%-plus rental premiums. Municipal enforcement is already separating a two-tier market in which EPC A stock enjoys valuation resilience while C-rated buildings confront stranded-asset risk. As a result, capital is flowing toward refurbishment pipelines rather than speculative ground-up towers, tightening Grade A supply in core districts.

Corporate Science Based Targets Net-Zero Commitments Fueling Demand for Energy-Positive Flagship Offices

More than 1,000 European corporations have filed Science-Based Targets pledges that embed Scope 1–3 carbon cuts into real-estate briefs, pushing tenants to insist on LEED Platinum, BREEAM Outstanding, or DGNB Gold space [2]Science Based Targets, “Companies Taking Action,” SCIENCEBASEDTARGETS.ORG. Prime CBD rents in certified buildings rose 4% in 2025, even as headline vacancy drifted higher, highlighting a widening quality gap. Finance and professional-services firms have consolidated into fewer headquarters yet upgraded specifications, lifting average deal size beyond 10,000 m². The preference for energy-positive assets also redirects relocation searches to transit-rich nodes able to support micro-mobility plans, reshaping occupier maps inside London, Frankfurt, and Paris.

EU Recovery & Resilience Facility Green-Retrofit Funds Unlocking CapEx for Aging Stock in CEE Markets

The EU Recovery & Resilience Facility earmarked USD 796.18 billion equivalent, with at least 37% for climate projects, allowing Polish, Czech, and Romanian landlords to fund heat-pump conversions and LED retrofits at subsidized rates[3]European Commission, “Recovery and Resilience Facility,” European Commission, commission.europa.eu. Stabilized yields of 7%-8% in CEE gateways compare favorably to 4%-5% in core Western markets, prompting German and U.S. pension funds to allocate fresh capital to Warsaw, Prague, and Bucharest. Execution risk remains from permit delays and labor shortages, yet early disbursements have already narrowed energy-performance gaps and compressed cap-rate spreads.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained high ECB interest rates tightening credit spreads | -0.9% | Southern Europe, CEE, pan-EU | Short term (≤ 2 years) |

| Corporate sublease wave at ≤ 30% desk utilization | -0.7% | UK, Germany, France, Netherlands | Short term (≤ 2 years) |

| 15-minute-city zoning caps curbing CBD supply | -0.4% | Paris, Barcelona, Milan, Brussels | Medium term (2-4 years) |

| Embodied-carbon caps limiting steel-and-glass redevelopments | -0.3% | UK, Netherlands, France, Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained High ECB Interest Rates and Tighter Credit Spreads Suppressing Development Pipelines

The European Central Bank kept its deposit rate at 2.75% in January 2025, pushing total borrowing costs for speculative office projects above 6%. Developers now require stabilized yields of 7%-8% to break even, a hurdle only fully pre-leased Grade A towers can clear. Frankfurt, Munich, and Amsterdam each saw permitting volumes fall 40%-50% versus 2022 peaks, severely restricting post-2027 deliveries. Refinancing risk for loans originated in 2020-21 is triggering opportunistic asset sales at double-digit discounts, yet bid-ask gaps remain wide, freezing many transactions.

Sublease Wave from Corporates Hitting ≤ 30% Utilization, Pressuring Prime Rents

Hybrid-work utilization below 30% has unleashed sublease space equal to 15%-20% of available stock in London, Frankfurt, and Paris. Discounted sublets undermine landlord pricing power and extend lease-up times for new schemes. Canary Wharf and La Défense each carry more than 200,000 m² of surplus, prompting concessions worth USD 550-880 per m² in tenant allowances plus up to 18 months rent-free. Appraisers have widened Grade A cap rates 50-100 bps for buildings facing high sublease exposure, reflecting uncertainty about future cash flows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Quality Polarization Rewrites Tenant Preferences

Grade A assets accounted for 55.68% of Europe office real estate market size in 2025 and are projected to grow at a 4.99% CAGR through 2031. Prime CBD rents for Grade A exceeded USD 57 per m² per month in Munich during 2025, 30% above comparable Grade B space, underscoring tenants’ readiness to pay premiums for wellness amenities, column-free floorplates and ESG credentials. The segment benefits from tight supply because financing for speculative projects is scarce, and embodied-carbon rules steer developers toward refurbishing older stock rather than building fresh towers. Grade B assets occupy roughly one-third of inventory and show a bifurcated outlook: centrally located offices within 500 m of transit nodes are attracting value-add investors who inject USD 110-165 per m² of retrofit capital to meet EPC B thresholds, whereas car-dependent suburban properties face conversion or demolition. Grade C buildings, often built prior to 1990, are exiting the market entirely as conversion rates to residential or life-science uses doubled to 12% of stock in 2024.

Flight-to-quality dynamics are visible in leasing spreads: Frankfurt Grade A rents at USD 52 per m² per month stand USD 17 higher than Grade B comparables and the differential has widened 600 bps since 2019. Occupiers cite employee-engagement goals and Scope 2 carbon targets as key drivers. The divergence is reinforcing investor appetite for refurb-to-core strategies, compressing yields on upgraded Grade B to within 100 bps of Grade A. With the EPBD deadline looming, lenders have begun to reserve preferential loan-to-value ratios for certified assets, tilting the balance further toward high-grade stock and accelerating the write-off of obsolete offices.

By Transaction Type: Sales Outpace Rentals Despite Rental Dominance

Rental agreements captured 74.88% of the European office real estate market share in 2025, a reflection of occupiers' favoring three-to-five-year flexibility clauses amid uncertain headcount forecasts. However, the sales category is forecast to expand 5.15% annually through 2031, eclipsing rental growth as global pension and sovereign-wealth funds allocate capital into long-dated, income-producing stock. Cross-border inflows reached USD 8.8 billion in H1 2025, led by Asian sovereign investors securing German and Dutch assets at 4%-plus net yields. Distressed disposals by highly leveraged owners are widening the investable universe for opportunistic buyers that can underwrite capex. Meanwhile, corporate tenants increasingly request break clauses and green fit-out packages, elongating negotiation cycles and pressuring landlords to fund larger tenant incentives, all of which moderate rental-growth trajectories.

Build-to-suit transactions dominate the modest new construction that is breaking ground because lenders require pre-leases covering at least 60% of net rentable area before releasing funds. The trend channels capex away from speculative projects and into bespoke headquarters anchored by investment-grade tenants. Simultaneously, trophy-asset trades illustrate depth of demand: in November 2024, CBRE Global Investors acquired a LEED Platinum Frankfurt tower fully leased to Deutsche Bank for USD 418 million at a 4.2% yield, the tightest German office pricing post-pandemic. Such deals highlight that liquidity pivots toward core, stabilized products even while secondary assets languish.

By End User: IT & ITES Lead as BFSI Consolidates

Information Technology and IT-enabled services users held the largest 32.08% share of the European office real estate market size in 2025 and are advancing at the fastest 5.37% CAGR. Hyperscalers, SaaS providers, and fintech firms are driving take-up above 25,000 m² per deal in Frankfurt, Dublin, and London to accommodate AI-model training and cloud-operations teams. More than 80% of tech leases executed in 2025 required LEED Gold or higher, setting a de facto sustainability baseline for premium buildings. Banking, Financial Services and Insurance (BFSI) occupiers, the second-largest cohort at roughly 26% of demand, are shrinking total footprints by 10%-15% yet upgrading to smaller numbers of flagship, client-facing floors, a swap that inflates average rent per employee while trimming net area. Professional-services partnerships, occupying close to 20% of space, mirror BFSI behavior by replacing private offices with collaboration zones, cutting per-capita density down to 8-10 m².

Life sciences companies, still a niche at under 5% share, signal a promising conversion path for obsolete offices. Landlords in Cambridge, Basel, and Copenhagen have repositioned pre-1990 buildings into wet lab shells that command double-digit rents. Such transactions underscore adaptive reuse as an emerging competitor to conventional leasing, eroding the low-spec office demand pool while opening a new valuation floor for otherwise stranded stock.

Geography Analysis

Germany retained the largest 29.58% slice of the European office real estate market size in 2025 and is slated to expand at a 4.2% CAGR through 2031. Frankfurt’s Q1 2025 absorption of 194,600 m² was driven by U.S. cloud providers and Asian fintechs, lifting prime rents to USD 52 per m² monthly. Munich’s USD 59 per m² rate reflects automotive-tech and semiconductor demand alongside low vacancy. The country’s fast-tracked office-to-residential permits enabled 20% of obsolete stock to be converted in 2024, culling inefficient inventory, sustaining rent resilience even in a high-rate climate.

The United Kingdom and France together represented roughly 36% of regional value in 2025, yet differ in outlook. London’s Canary Wharf attracted Visa and JP Morgan commitments, but sublease surpluses lifted citywide vacancy to 9.5%, restraining net effective rent growth. Paris, conversely, imposed 15-minute-city zoning that caps CBD permits at 50,000 m² annually. The scarcity underpins 4% rent growth in the 8th arrondissement despite broader economic headwinds. Labour-law rigidity and slow permitting deter speculative projects in both locales, implicitly protecting incumbent landlords’ cash flows.

Italy and Spain, jointly near 13% of the market value, posted vigorous leasing in 2025. Milan recorded 110,000 m² of Q1 take-up; Grade A alone captured 60% and commanded USD 69 per m² per month in prime rents, a national high. Madrid and Barcelona delivered USD 45 and USD 34 per m² monthly, respectively, paired with investment yields 200-300 bps wider than core German assets, attracting U.S. private-equity capital. Local governments accelerate adaptive-reuse permits, further tightening Grade A supply across both countries.

The rest of Europe delivered the fastest 5.52% CAGR projection to 2031 as CEE capitals and Nordic cities capture nearshoring and data-center spillover. Warsaw’s vacancy dipped to 11.2% in Q4 2024 thanks to IT outsourcing demand, while Stockholm and Copenhagen absorbed more than 50,000 m² each, tied to edge-compute facilities. EU Recovery & Resilience funds help finance deep retrofits, squeezing yield spreads versus Western peers and magnetizing institutional capital seeking diversification without sacrificing liquidity.

Competitive Landscape

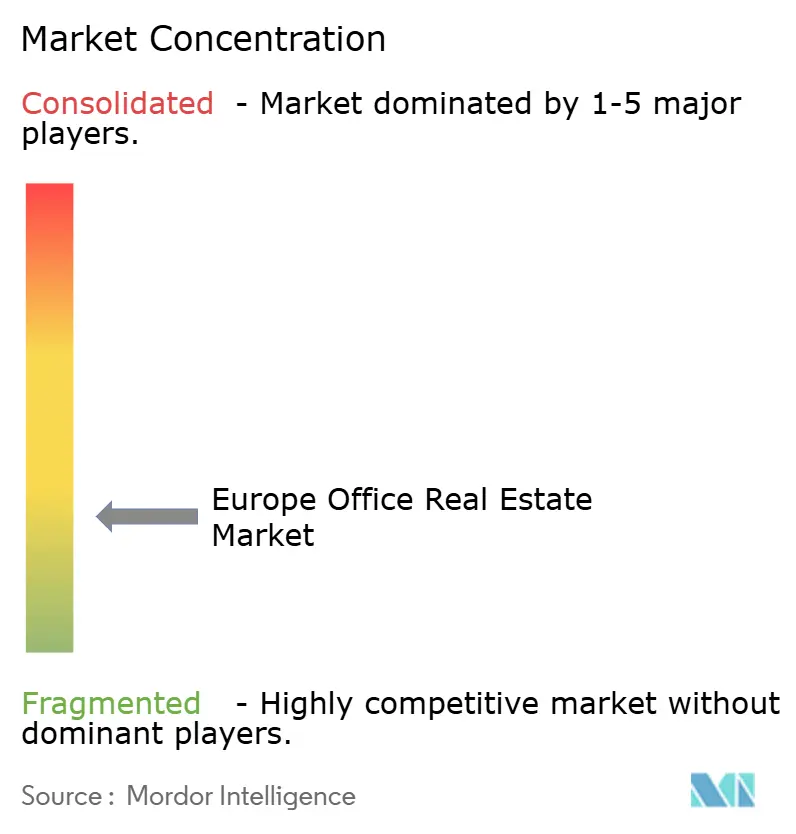

The Europe office real estate market remains fragmented; no single landlord exceeds mid-single-digit share, but scale players Aroundtown, Gecina, and Unibail-Rodamco-Westfield wield negotiating leverage in Paris, Berlin, and Amsterdam. They capitalize on balance-sheet depth to pre-fund retrofit campaigns and access USD-linked green loans such as Unibail-Rodamco-Westfield’s USD 1.32 billion facility priced 25 bps inside conventional debt. Service giants JLL, CBRE, and Cushman & Wakefield dominate occupier advisory, yet fee compression is prompting them to bundle PropTech and sustainability consulting to defend margins.

Competition is most intense in Grade A development, where land scarcity, carbon caps, and permitting delays create natural barriers to entry. Build-to-core institutional funds partner with turnkey contractors to mitigate cost inflation and deliver pre-leased towers. Adaptive reuse has emerged as a high-return niche: landlords converting obsolete offices to labs or housing routinely target 12%-15% unlevered IRRs double new-build office returns, drawing global opportunistic capital. At the same time, PropTech disruptors offer 30%-40% faster delivery via modular construction and integrate IoT analytics that reduce operating expenses by up to 20%.

Smart-building retrofits present another competitive axis. Only 30% of European offices deploy real-time energy monitoring, leaving a wide adoption gap that nimble owners exploit to command 5%-8% rent premiums. Technology is also compressing leasing cycles: AI-powered space-planning and virtual-tour platforms are shortening tenant decision windows from 18 months to about nine, allowing proactive landlords to secure occupancy ahead of slower rivals. As sublease supply weighs on rents, owners that pair ESG upgrades with flexible fit-outs gain a decisive edge in retaining blue-chip tenants.

Europe Office Real Estate Industry Leaders

Jones Lang LaSalle IP, Inc.

CBRE

Cushman & Wakefield

Savills

Colliers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Microsoft confirmed a USD 3.52 billion investment to expand German AI and cloud campuses in Frankfurt and Munich, adding space for 2,500 employees.

- January 2025: Aroundtown divested a USD 495 million bundle of secondary German offices to a Blackstone-led group, illustrating renewed appetite for stabilized income streams.

- December 2024: Unibail-Rodamco-Westfield obtained a USD 1.32 billion green loan linked to 40% verified carbon-intensity cuts across Paris and Amsterdam portfolios.

- November 2024: CBRE Global Investors paid USD 418 million for a LEED Platinum Frankfurt tower fully leased to Deutsche Bank at a 4.2% yield.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European office real estate market as the total capital value of income-producing and owner-occupied office buildings that are transacted for lease or sale across EU-27, the U.K., Norway, Switzerland, and other continental hubs. Stock under construction is counted once a completion certificate is issued, whereas coworking licenses, serviced-office fees, and property-management revenues are excluded.

Scope exclusion: pure land banks, student housing, and mixed-use assets where offices account for under 50% of net lettable area are left outside the model.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End User

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifescience, Energy, Legal)

- By Country

- Germany

- UK

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with leasing brokers, valuation surveyors, lenders, and large occupiers across Germany, France, the Nordics, and CEE test supply pipelines, achievable rents, and retrofit premiums. Online surveys with facilities heads validate vacancy thresholds that trigger relocations, letting us fine-tune absorption assumptions.

Desk Research

Mordor analysts start with authoritative public statistics from Eurostat, national land registries, the ECB's commercial property price index, and customs data on construction materials. These baselines are enriched with industry associations such as EPRA, RICS, and BPF, as well as peer-reviewed journals tracking energy-efficient retrofits. Company 10-Ks, REIT filings, and reputable news feeds through Dow Jones Factiva give transaction color and forward guidance. Paid databases, D&B Hoovers for landlord financials and Questel for refurbishment-related patents, help us benchmark refurbishment cost curves. This list is illustrative; many further references support data capture and cross-checks.

Market-Sizing & Forecasting

A top-down stock-value reconstruction from national accounts is paired once with sampled asset-level roll-ups for Grade A clusters to ground the estimate. Key drivers fed into the model include net absorption, average prime rent, yield compression trajectories, EPC-linked cap-ex, and demolition ratios. Forecasts to 2030 rely on a multivariate regression of GDP growth, office-based employment, and ECB policy rates, refined through scenario analysis where experts diverge. Where city-level bottom-up tallies fall short of national totals, gap shares are apportioned using historical leasing flow weights before final reconciliation.

Data Validation & Update Cycle

Outputs pass three-layer checks: algorithmic variance flags, senior analyst peer review, and a quarterly re-contact of panel experts for material events. Reports refresh annually, and a final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Europe Office Real Estate Baseline Earns Board-Room Trust

Published numbers often disagree because firms mix stock value with annual investment flows or bundle flex workspace fees into real estate revenue. Scope boundaries, currency bases, and refresh cadence amplify gaps.

Key gap drivers include (i) alternate studies treating every standing structure, including half-vacant suburban blocks, as fully valued stock, and (ii) flow-based reports quoting only one-year transaction volumes, thereby missing latent capital value swings when debt costs shift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 377.2 bn (2025) | Mordor Intelligence | - |

| €1.2 tn (2024) | Regional Consultancy A | Counts entire stock irrespective of occupancy and quality; omits country-level retrofit write-downs |

| €93 bn (2022) | Trade Journal B | Measures annual deals only; excludes owner-occupied assets and untapped debt-funded refurbishments |

These contrasts show that Mordor's disciplined scope setting, mixed modelling logic, and yearly refresh deliver a balanced, transparent baseline clients can rely on for capital planning. The present study sizes the 2025 market at USD 377.2 billion. Regional Consultancy A reports roughly €1.2 trillion for 2024. Trade Journal B cites €93 billion of 2022 office transactions.

Key Questions Answered in the Report

How large is the Europe office real estate market in 2026?

The Europe office real estate market size is USD 392.48 billion in 2026.

What is the forecast CAGR for European offices to 2031?

The market is projected to grow at a 4.05% CAGR between 2026 and 2031.

Which tenant group drives the fastest demand growth?

IT & ITES firms are expanding leasable footprints fastest at a 5.37% CAGR through 2031.

Why are Grade A rents rising despite higher vacancy in older stock?

Corporations chasing energy-positive, amenity-rich buildings will pay 25%-30% premiums, widening the grade spread.

How do EU carbon rules affect new office development?

Embodied-carbon caps and the 2026 zero-emission mandate push developers toward refurbishments and timber-hybrid designs, cutting speculative ground-up starts.

Which geography is expected to grow quickest through 2031?

Rest of Europe, including Central-Eastern and Nordic hubs, is expected to post the strongest 5.52% CAGR as nearshoring and data-center projects accelerate demand.

Page last updated on: