Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

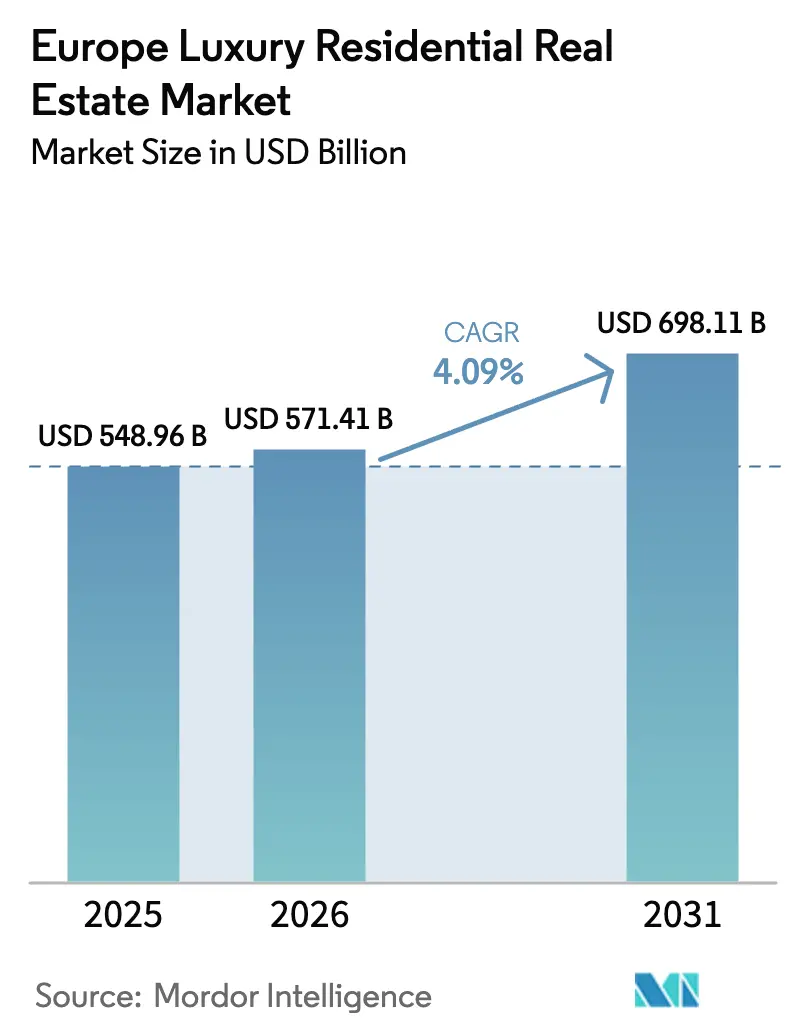

| Base Year Market Size (2025) | USD 548.96 Billion |

| Market Size (2026) | USD 571.41 Billion |

| Market Size (2031) | USD 698.11 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

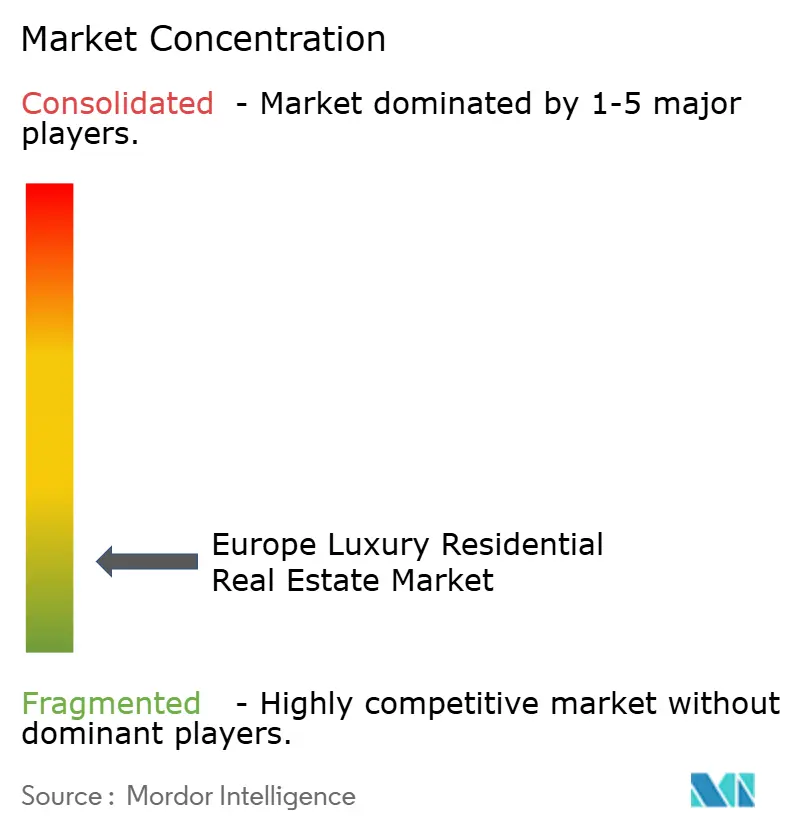

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Europe Luxury Residential Real Estate Market size was valued at USD 548.96 billion in 2025 and is estimated to grow from USD 571.41 billion in 2026 to reach USD 698.11 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

Demand is being reshaped by cross-border wealth migration, historically tight prime-location supply, and a building code overhaul that channels capital toward energy-efficient retrofits. Cash-rich high-net-worth individuals (HNWIs) now dominate the ultra-prime brackets, while higher financing costs have slowed leveraged deals, especially in mid-tier luxury. Scarcity of shovel-ready land inside heritage districts is boosting per-square-foot prices and tilting buyers toward turnkey or refurbished stock that already meets new efficiency thresholds. Large branded-residence pipelines in Spain and Portugal broaden choice but do not fully offset the slowdown in London and Paris new-build starts, so resale valuations keep climbing.

Key Report Takeaways

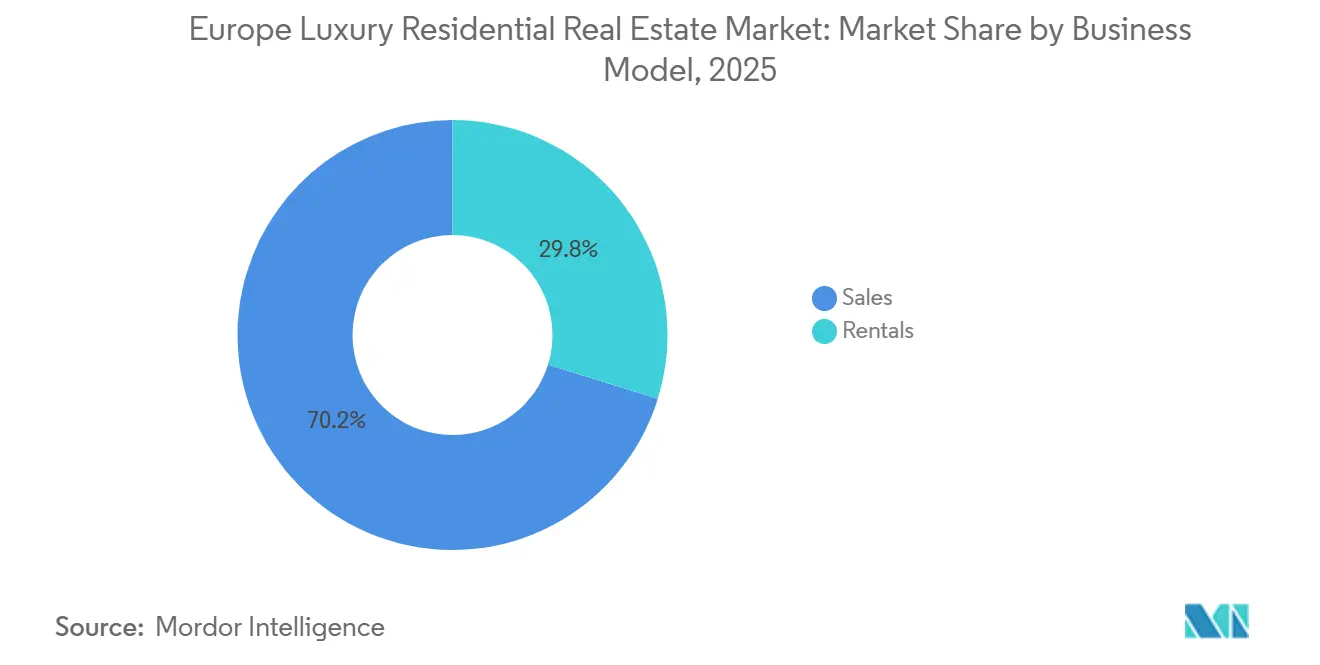

- By business model, the sales channel controlled 70.2% of the Europe luxury residential real estate market share in 2025; rentals, however, are forecast to expand at a 4.68% CAGR to 2031.

- By property type, apartments and condominiums led with 59.1% of the Europe luxury residential real estate market size in 2025, while villas and landed houses are projected to grow the fastest at 4.87% CAGR through 2031.

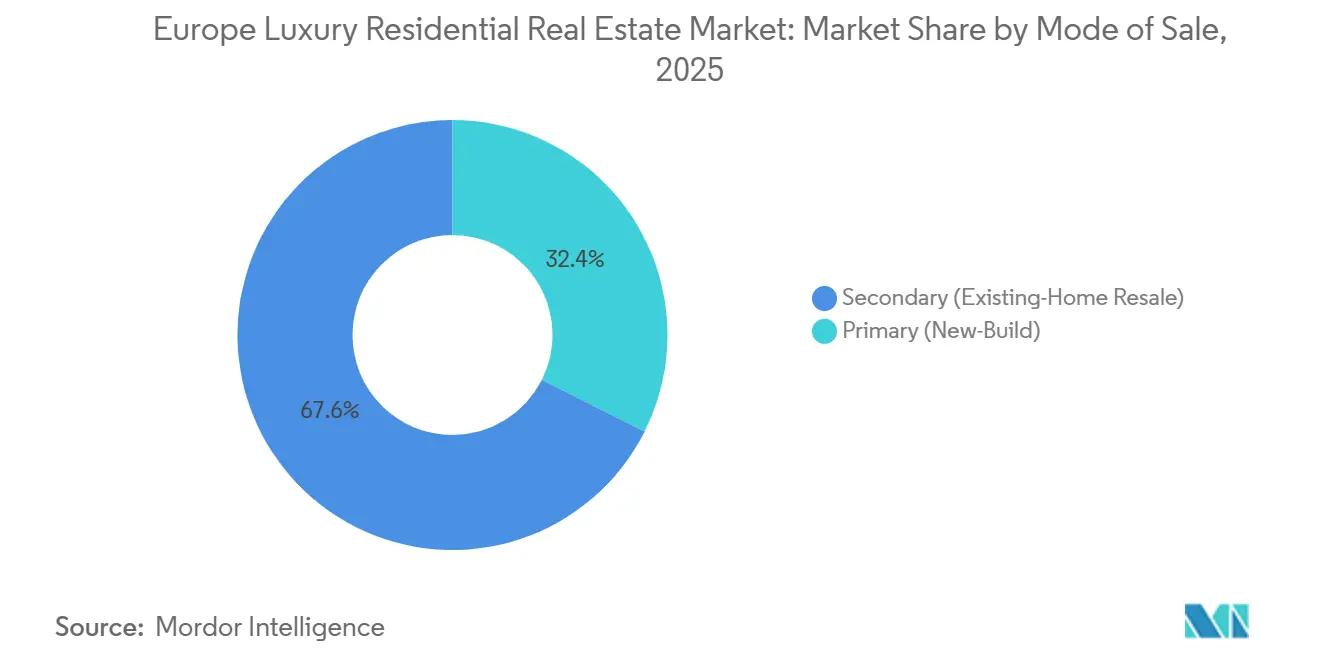

- By mode of sale, resale properties captured 67.6% of transactions in 2025; the new-build segment is expected to register a 4.59% CAGR between 2026 and 2031.

- By country, the United Kingdom accounted for 23.4% of the market in 2025, whereas Spain is anticipated to be the fastest-growing national market at a 5.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wealth migration and second-home demand are supporting prime city and resort residential absorption | +1.2% | Spain, Portugal, Italy, France, Greece | Medium term (2-4 years) |

| Limited prime stock and strict development controls are sustaining scarcity-driven pricing power | +0.9% | United Kingdom, France, Italy | Long term (≥ 4 years) |

| Growth in branded residences and amenity-led projects is expanding high-end development pipelines | +0.8% | Spain, Portugal, France | Medium term (2-4 years) |

| Sustainability upgrades and energy ratings are influencing buyer preference for modernized luxury assets | +0.7% | EU-wide compliance zones | Medium term (2-4 years) |

| Preference for turnkey renovated homes is increasing demand for premium refurbishment services | +0.6% | France, Italy, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Wealth Migration and Second-Home Demand Supporting Prime City and Resort Residential Absorption

Net inflows of millionaires into Portugal, Spain, and Greece are redirecting global capital toward Mediterranean resort corridors. Roughly 45% of prime Spanish transactions in 2025 involved non-resident buyers who paid USD 5 million to USD 50 million for Marbella villas, a range that still looks attractive against London or Monaco price points. Henley & Partners estimated that Portugal welcomed around 1,400 new HNWIs in 2025, confirming the country’s status as a European gateway for Latin American and U.S. families. Greece recorded USD 2.75 billion of non-resident investment in 2024, an annual jump of 28.9%, and more than 85% of these deals targeted island or coastal second-homes. Italy’s flat-tax regime attracted only 5,000 elective-residence applicants since launch, showing that lifestyle infrastructure matters more than headline incentives. Together, these flows underpin resilient absorption in both city pied-à-terre markets and resort villa enclaves[1]Henley & Partners, “Private Wealth Migration Report 2025,” henleyglobal.com .

Limited Prime Stock and Strict Development Controls Sustaining Scarcity-Driven Pricing Power

New-build activity in London fell to just 3,990 housing starts in the 12 months to March 2025 as the Building Safety Act Gateway 2 approval queue lengthened, discouraging developers from high-rise schemes. Paris faces parallel constraints, where heritage protections limit façade alterations, pushing buyers toward existing Haussmann-era apartments despite higher renovation costs. Monaco’s average sales price reached USD 51,967 per m² in 2024 as supply additions stayed negligible and three-quarters of transactions exceeded USD 10 million. In the United Kingdom, a mandatory second-staircase rule for buildings over 18 meters added an estimated USD 1.8 billion in extra construction costs, making many prime projects unviable. These combined bottlenecks lock in scarcity and transfer value to owners of compliant legacy stock[2]Government of the United Kingdom, “Building Safety Act Guidance,” gov.uk .

Growth in Branded Residences and Amenity-Led Projects Expanding High-End Development Pipelines

Spain and Portugal hosted 47 branded residence projects—about 2,400 units—by mid-2025, priced roughly 30% above comparable non-branded stock. Knight Frank predicts global branded schemes to top 1,000 by 2030, with Europe claiming 13% of the total. Amenities ranging from hotel-style concierge to fractional ownership attract UHNWIs who value turnkey management and potential rental income. A EUR 200 million Marbella project announced in January 2026 demonstrates regional momentum and Middle Eastern capital appetite. While such pipelines support primary-market growth, they do not fully offset the London slowdown, so scarcity in core cities persists.

Sustainability Upgrades and Energy Ratings Influencing Buyer Preference for Modernized Luxury Assets

The EU’s revised Energy Performance of Buildings Directive (EPBD) obliges member states to lift the lowest-performing 15% of homes to EPC E by 2030 and to phase out fossil-fuel boilers by 2040. Construction estimates indicate that zero-emission building standards raise project costs 8%-12%, pushing smaller developers out of the market. Italy, where 60% of housing stock predates 1970, faces one of the steepest compliance curves, yet forward-thinking sellers already retrofit villas to EPC A or B and achieve price premiums of up to 20% in Lake Como and Tuscany. France ties mortgage conditions to EPC ratings, incentivizing owners to renovate early to secure lower lending margins. The United Kingdom scrapped its EPC C rental mandate in October 2025, saving landlords money but leaving tenants free to demand lower-utility homes, a mismatch that may bifurcate future rents[3]European Commission, “Energy Performance of Buildings Directive Revision,” europa.eu .

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher financing costs are reducing leveraged buyer activity in prime markets | -0.6% | United Kingdom, Germany, France, Netherlands | Short term (≤ 2 years) |

| Tax, residency, and ownership regulation changes are increasing transaction friction for foreign buyers | -0.5% | United Kingdom, Spain, Portugal | Medium term (2-4 years) |

| Tight planning and heritage constraints are limiting new supply and extending project timelines | -0.4% | United Kingdom, France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Financing Costs Reduce Leveraged Buyer Activity in Prime Markets

The European Central Bank (ECB) cut policy rates eight times during 2025, yet prime mortgage costs remain roughly double 2020 levels, keeping debt-financed buyers on the sidelines. Germany booked USD 4.5 billion of residential trades in H1 2025 versus USD 9 billion in H1 2022, with most investors paying cash to sidestep interest pressure. Italy saw mortgage issuance grow 32.8% in Q1 2025, but 70% of these loans served mid-tier rather than ultra-prime segments, a sign that top-end buyers prefer equity. In London, transactions involving loan-to-value ratios above 50% fell below 20% of 2025 volume, down from 35% in 2019. Elevated debt service, therefore, caps upside for leveraged demand until rate spreads normalize.

Tax, Residency, and Ownership Regulation Changes Increasing Transaction Friction for Foreign Buyers

The United Kingdom abolished its “non-dom” tax status in April 2025, prompting an exodus of an estimated 16,500 millionaires and depressing prime central London inquiries by about one-third. Spain floated a 100% surcharge on non-EU property acquisitions in 2025; although still under debate, the proposal cut new-buyer interest 20%-30% according to broker polls. Portugal’s 2024 Golden Visa overhaul removed property purchases as a qualifying option, slashing program applications by 60% in 2025. Greece froze new building permits on Mykonos through 2030, funneling demand into scarce existing villas and curbing supply pipelines. These policy swings inject uncertainty and extend decision timelines for international buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rentals Scale Faster as Flexibility Trumps Ownership

Sales represented 70.2% of 2025 turnover, underscoring the traditional dominance of deeded ownership in the Europe luxury residential real estate market. In core hubs such as London, weekly rents in prime central neighborhoods average USD 1,300-6,500, while Paris leases luxury apartments for USD 5,300-21,200 each month, attracting corporate executives, international students, and expatriate families. Côte d’Azur summer villa rents can eclipse USD 212,000 per week at peak events, and Swiss Alpine chalets in St. Moritz now command up to USD 159,000 per ski week, reflecting demand for short, experience-rich stays.

The rental segment is forecast to grow at a 4.68% CAGR from 2026 to 2031, faster than the 3.85% CAGR projected for sales, as families adopt multi-residence lifestyles without tying up equity. Corporate relocation packages have pivoted toward flexible leases, and wealth advisers increasingly recommend renting while awaiting tax-residency clarity post-Brexit. As brokerage firms notice higher recurring fees from lettings, many pivot to hybrid models, integrating concierge and property-management arms to enhance margins and lengthen client life-cycles within the Europe luxury residential real estate market.

By Property Type: Villas Outpace Apartments on Privacy Premium

Apartments and condominiums retained 59.1% of 2025 revenue, a testament to dense urban cores in London, Paris, Milan, and Berlin. Yet villas and landed houses are expected to log the quickest expansion at a 4.87% CAGR through 2031 as post-pandemic buyers prize gardens, pools, and gated privacy. In Spain, Golden Mile listings in Marbella run from USD 5 million to USD 50 million, while Cap Ferrat villas on France’s Côte d’Azur frequently break USD 100 million, drawing Middle Eastern family offices and U.S. tech entrepreneurs.

Although vertical living dominates capital cities, branded villa resorts are blurring residential and hospitality lines by layering hotel-style amenities and rental programs on freehold titles. This hybrid gives UHNWIs personal use plus yield potential, and average launch prices stand 30% above non-branded peers, reinforcing the premium direction of the Europe luxury residential real estate market size at segment level.

By Mode of Sale: Resale Dominance Mirrors Bottlenecks in New-Build Supply

Existing-home resales made up 67.6% of 2025 transactions, illustrating how planning delays lock buyers into established stock. London’s new-build launches dropped 77% from their 2015 peak, keeping secondary Mayfair and Kensington apartments in short supply and increasing bidding tension. In Spain, 60%-70% of Marbella deals involved resales because post-COVID buyers preferred proven neighborhoods, while Parisian purchasers value Haussmann architecture that most new towers cannot match.

Primary (new-build) inventory should still post a 4.59% CAGR from 2026-2031, thanks largely to hotel-affiliated branded residences in Spain and Portugal. More than 1,200 such units are due in Spain by 2027, and Knight Frank tallies a global pipeline surpassing 1,000 schemes by 2030. However, elevated construction costs tied to EPC compliance and safety rules mean the bulk of incremental supply remains concentrated in leisure markets rather than heritage city cores, perpetuating the resale premium inside the Europe luxury residential real estate market.

Geography Analysis

The United Kingdom captured 23.4% of the 2025 value, anchored by London districts where resale flats in Knightsbridge or Mayfair trade at USD 2,600-6,500 per ft². Abolishing the non-dom tax status in 2025 pushed an estimated 16,500 millionaires abroad, softening offshore demand, yet new-build starts also plunged—down 77% from 2015—so restricted supply continues to underpin prices. Gateway 2 approvals under the Building Safety Act average 26 months, versus 17 months in 2015, and compliance costs add roughly USD 1.8 billion countrywide, discouraging speculative towers in prime zones.

Germany and France remain dominated by institutional-grade apartment blocks in Berlin, Munich, and Paris. Germany recorded USD 4.5 billion of trades in H1 2025 and expects USD 8.1 billion for the year, while rents on new stock rose about 8% YoY, confirming suppressed supply. France forecasts almost 940,000 transactions in 2026, with Paris prime values near USD 10,150 per m², and ultra-luxury deals above USD 5 million jumped 24% YoY. Lyon, Nice, and Saint-Tropez also post solid activity, aided by domestic second-home buyers and Americans leveraging the strong dollar.

Spain is projected to grow the fastest, at a 5.05% CAGR through 2031, thanks to a surge in Latin American and Northern European buyers chasing Mediterranean lifestyle assets. Madrid prime prices rose 6.4% in the 12 months to June 2025, and foreign purchasers now represent about 45% of luxury deeds. Parallel momentum lifts Portugal, which led the EU in 2025 price growth at 16.3% YoY; Algarve homes averaged USD 3,675 per m², and Lisbon new-build penthouses fetched up to USD 12,720 per m². Greece, Monaco, and emerging Eastern European spots such as Bucharest round out the regional patchwork, each benefiting from niche demand drivers ranging from Golden Visa alternatives to record super-yacht berthing activity.

Competitive Landscape

Sotheby’s International Realty, Knight Frank, Savills, CBRE, Engel & Völkers, Barnes International Realty, John Taylor, and Christie’s International Real Estate headline a field where no single brokerage controls even 10% of Europe’s ultra-prime volume. The Europe luxury residential real estate market, therefore, remains relationship-driven and locally fragmented. Boutique agencies complete as much as 50% of >USD 10 million trades in Côte d’Azur or Tuscany because confidential sourcing and off-market matchmaking trump global advertising reach.

Strategic responses center on digital platforms, branded-residence partnerships, and geographic infill. Sotheby’s rolled out its “Extraordinary Living” portal in October 2025, using artificial-intelligence (AI) match scores and virtual-reality home tours to shorten viewing cycles. Savills bolstered its Lisbon presence through a February 2026 acquisition to capture Portugal’s branded-residence surge, while Knight Frank opened a Dubai hub in 2024 to funnel Gulf capital into Spain and France. Engel & Völkers introduced an AI-based valuation engine in December 2025 that crunches comparables and macro data in seconds, arming its 16,000 advisors with real-time pricing guidance.

Product diversification is also underway. CBRE’s 2024 purchase of 12 Parisian blocks converted them into luxury rentals aimed at global corporations, signaling institutional interest in stable prime-residential income. Coldwell Banker Global Luxury launched a cross-border certification course in September 2025 so agents can handle tax, visa, and heritage-asset due diligence, elevating service quality. Christie’s renewed its art-property tie-up in November 2025, weaving fine-art auctions into home marketing, an alluring combo for collectors who treat residences as lifestyle portfolios.

Europe Luxury Residential Real Estate Industry Leaders

Mansion Global

Propriétés Le Figaro

Sotheby’s International Realty Affiliates LLC

John Taylor

Barnes International Realty

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Savills bought a boutique brokerage in Lisbon, adding Algarve and Comporta specialists to deepen Iberian coverage.

- January 2026: Knight Frank partnered with a Dubai family office to co-develop a USD 212 million branded-residence scheme in Marbella with fractional ownership options.

- October 2025: Sotheby’s International Realty introduced its “Extraordinary Living” AI-enabled digital ecosystem for UHNWI clients.

- August 2025: CBRE acquired 12 prime Paris buildings for USD 150 million, converting them into luxury rentals at targeted 3.5%-4.5% yields.

Europe Luxury Residential Real Estate Market Report Scope

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

What is the projected value of the Europe luxury residential real estate market in 2031?

It is forecast to reach USD 698.11 billion by 2031, reflecting a 4.09% CAGR from 2026.

Which country is expected to grow the fastest through 2031?

Spain is poised for the quickest expansion at a 5.05% CAGR as lifestyle demand and branded residences accelerate.

Why are rentals increasing faster than sales in the luxury segment?

Corporate relocations and UHNWIs maintaining multiple homes prefer flexible leases, driving a 4.68% CAGR for rentals versus 3.85% for sales.

How are energy regulations affecting luxury property values?

Homes upgraded to EPC A or B ratings can command up to 20% premiums, while G-rated stock in Paris sells at 12% discounts.

What strategic moves are brokers making to stay competitive?

Leading firms deploy AI valuation tools, expand into Iberia, and partner on branded-residence projects to secure higher-margin pipelines.

Page last updated on: