Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

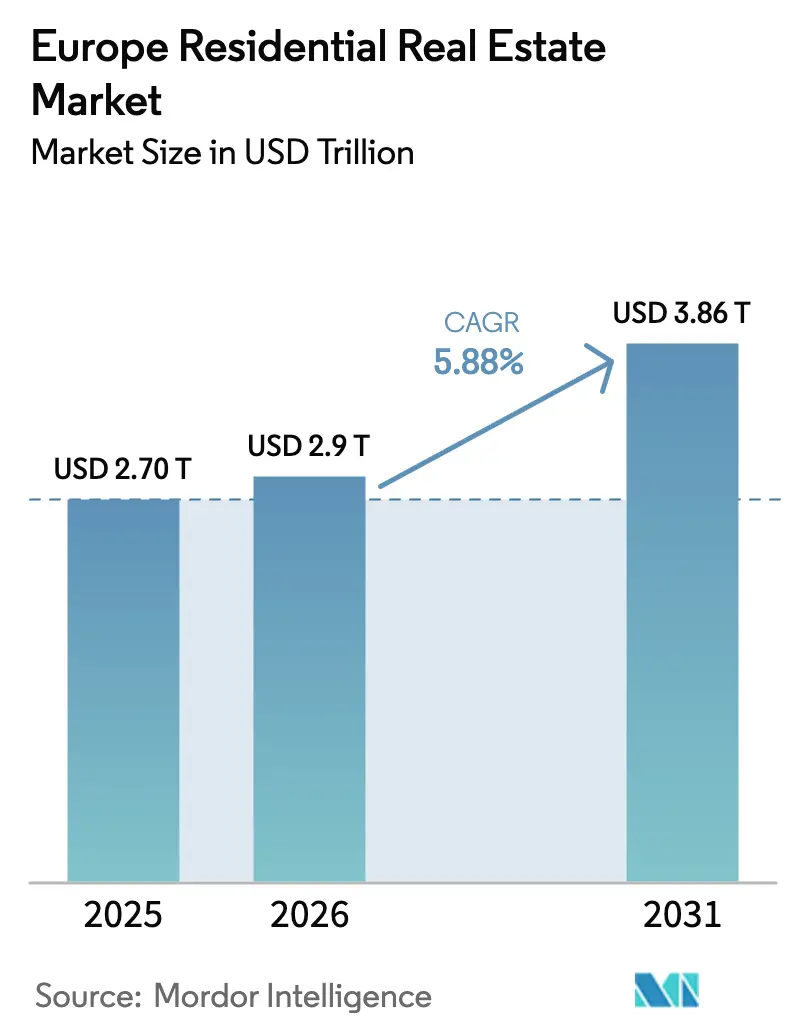

| Base Year Market Size (2025) | USD 2.70 Trillion |

| Market Size (2026) | USD 2.9 Trillion |

| Market Size (2031) | USD 3.86 Trillion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Residential Real Estate Market Analysis by Mordor Intelligence

The Europe residential real estate market size is USD 2.9 trillion in 2026, and it is projected to reach USD 3.86 trillion by 2031 at a 5.88% CAGR. The demand backdrop reflects structural undersupply, lagging permits, and delayed new starts that continue to tighten vacancy in large cities. Energy-compliance mandates under Directive (EU) 2024/1275 and national transpositions are shaping both capital allocation and asset strategies, especially in urban multifamily. Investors continue to rotate into the living sectors as rental growth outpaces inflation in core metro areas, supporting income visibility. Office-to-residential conversions are scaling to address carbon and supply constraints, while cross-border capital keeps liquidity resilient.[1]https://www.europarl.europa.eu/portal/en

Key Report Takeaways

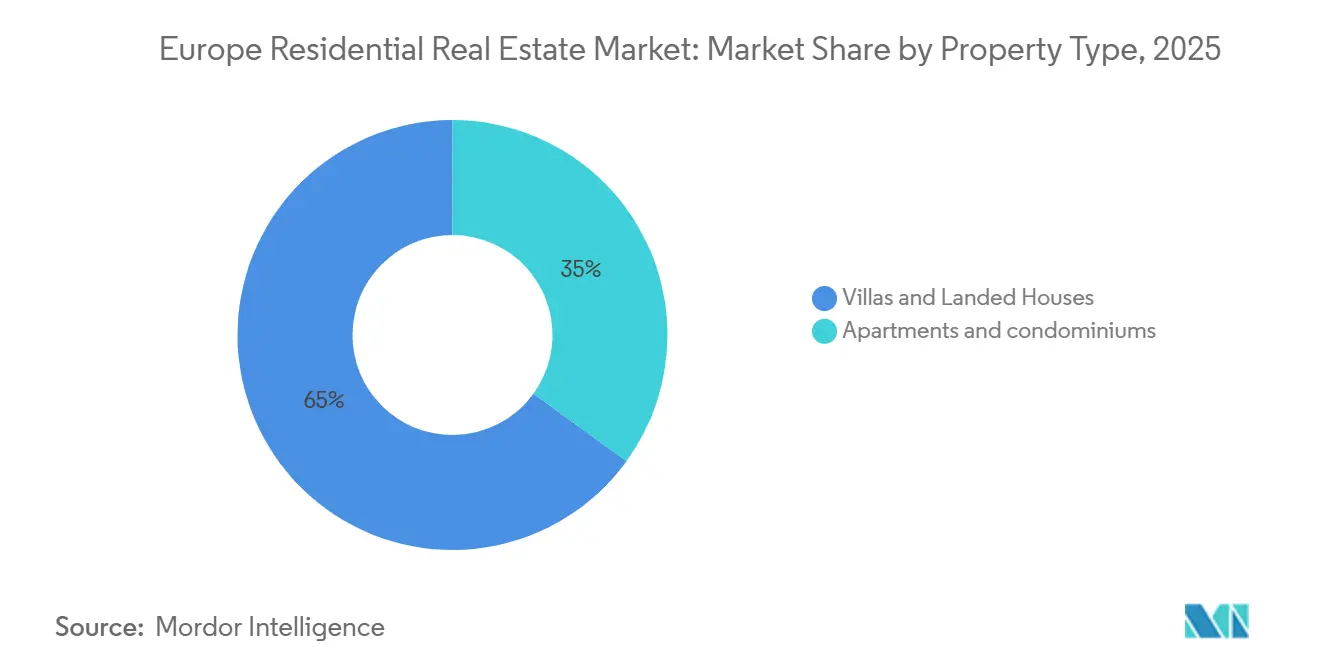

- By property type, villas and landed houses led with 65.00% revenue share in 2025, while apartments and condominiums are forecast to expand at a 6.14% CAGR to 2031.

- By price band, the mid-market tier held 46.00% share in 2025, and the affordable segment is set to grow at a 6.07% CAGR through 2031.

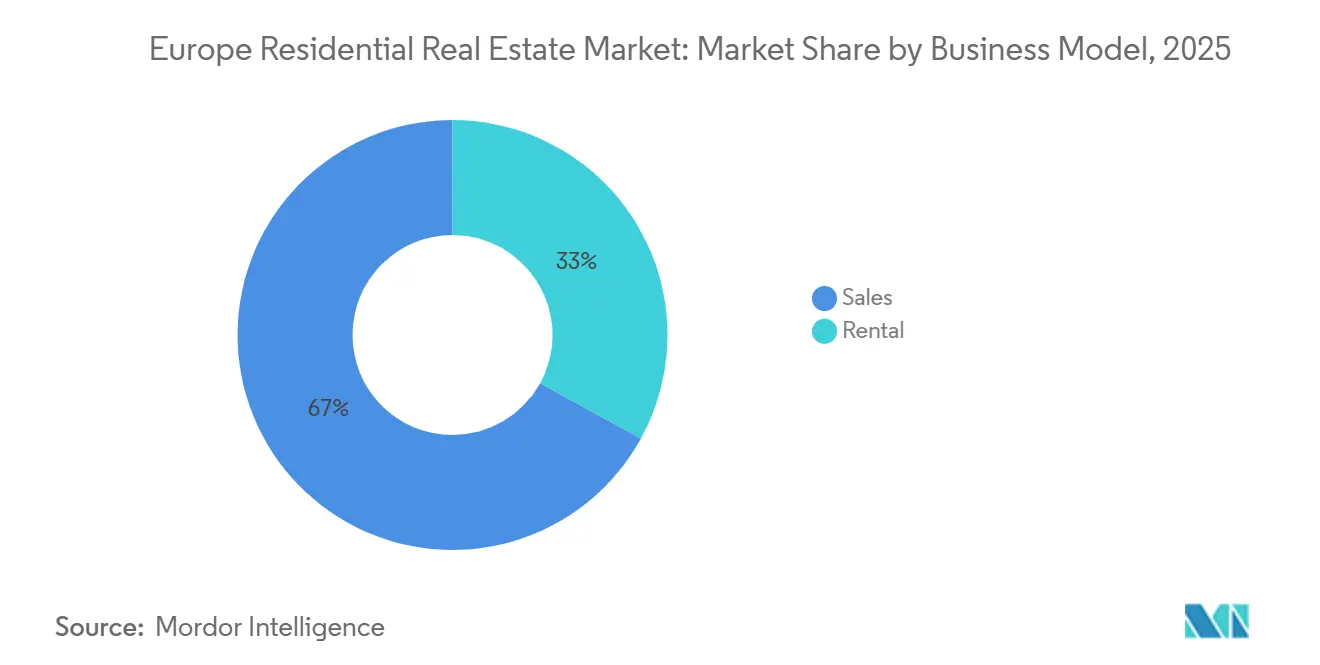

- By business model, sales transactions accounted for 67.00% in 2025, while rental platforms are poised for a 6.24% CAGR through 2031.

- By mode of sale, secondary transactions captured 90.00% of 2025 volume, as primary new-build sales are projected to grow at a 6.19% CAGR through 2031.

- By geography, Germany held a 22.00% share of regional volume in 2025, and the Netherlands is the fastest-growing country with a 6.32% CAGR projected for 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal incentives accelerating deep-retrofit demand across housing stock | +1.4% | EU-wide implementation; concentrated in Germany, France, Netherlands, Belgium | Long term (≥ 4 years) |

| Surge in cross-border private-equity inflows targeting European build-to-rent portfolios | +1.2% | UK, Germany, Netherlands, Southern Europe (Spain, Italy, Portugal) | Medium term (2-4 years) |

| Institutional capital pivot toward purpose-built rental communities | +1.1% | Pan-European; UK, Germany | Medium term (2-4 years) |

| Rise in single-person households fuelling multi-family apartment uptake in urban cores | +0.9% | Netherlands Randstad, France, Île-de-France, Spain Madrid/Barcelona, Belgium Brussels; metros with <3% vacancy | Medium term (2-4 years) |

| Ageing population expanding senior- and assisted-living developments in Germany & Nordics | +0.7% | Germany, Sweden, Finland, Norway, Denmark | Long term (≥ 4 years) |

| Digital-nomad visa adoption boosting Southern-Europe second-home purchases | +0.6% | Spain (Costa del Sol, Balearics, Valencia), Portugal (Algarve, Lisbon), Greece (Athens, islands), Italy (Sicily, Tuscany) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green Deal Incentives Accelerating Deep-Retrofit Demand Across Housing Stock

Directive (EU) 2024/1275 requires Member States to reduce the average primary energy use of residential buildings by 16% by 2030 and 20% to 22% by 2035 versus 2020 baselines, with at least 55% of the reduction from the worst-performing 43% of stock. National policies are converging as transposition deadlines hit in May 2026, with France’s decency decree phase-out of low EPC classes and grant support through MaPrimeRénov’. The Netherlands is consulting on minimum energy label D for all rental homes by 2029, backed by subsidies up to EUR 15,000 per unit (USD 16,200) and a EUR 126 million budget through 2030 (USD 136.1 million). Germany is mandating 65% renewable heat in larger cities from June 2026, and Spain’s National Building Renovation Plan targets steeper energy cuts than the EU baseline with NextGenerationEU funding. Platform operators report regulated rent uplift potential and tenant utility savings after upgrades, which can also lift new lease levels.[2]https://www.bpie.eu/

Surge in Cross-Border Private-Equity Inflows Targeting European Build-to-Rent Portfolios

Cross-border investors represented 45% of European residential deals in 2025, supported by British, French, and Swedish buyers, alongside growing allocations from Asia-Pacific and Middle Eastern sovereign vehicles. Capital is concentrating on build-to-rent platforms that offer scale, geographic diversification, and compliance-ready assets aligned with the Energy Performance of Buildings Directive. Partners Group acquired Empira in January 2025, adding a USD 17 billion gross development value portfolio concentrated in German multifamily and designed to execute retrofits at scale. The move favors vertically integrated platforms that can limit net operating income leakage through standardized operations. Germany’s multifamily financing and the UK’s build-to-rent development flows reinforce a shift toward income-focused rental strategies as lenders offer the highest LTVs to multifamily.[3]https://www.cbre.de/

Institutional Capital Pivot Toward Purpose-Built Rental Communities

European Operational Real Estate investors plan to deploy EUR 51 billion over three years into living assets (USD 55.1 billion), as PBSA surpassed multifamily as the most favored segment for the first time in early 2025. Through the first three quarters of 2025, care homes grew 182% year over year, PBSA rose 71% with a record 6% share of total European real estate investment, and multifamily climbed 10.2%. UK build-to-rent scaled from under 1,000 units in 2004 to nearly 90,000 units two decades later as integrated design and operations advanced delivery. Lenders continue to prioritize multifamily with prime senior LTVs of 60% to 65%, while UK legislation supports professional operators under evolving tenancy rules. The June 2025 merger of Aedifica and Cofinimmo created the largest European real estate trust focused on healthcare and senior housing, showing the premium for pan-European scale.

Rise in Single-Person Households Fuelling Multi-Family Apartment Uptake in Urban Cores

Private rented tenure is expanding across continental Europe as net household formation outpaces net housing additions in key cities, drawing the highest planned three-year capital allocation into multifamily among living sub-sectors. Germany’s Top Seven cities recorded year-over-year rental escalation in the first half of 2025, led by Leipzig and supported by rising median asking rents in Berlin, as household composition trends extend rental demand in central locations close to jobs and transit. The Netherlands is set for 4.8% rental inflation in 2026 after 8.8% in 2025, while a housing shortage and ex-rental transactions at lower average prices bring first-time buyers into the resale mix. Tight rental markets in major French cities reflect low vacancy and a construction deficit that sustains demand for compact urban formats. Operators are professionalizing management to reduce vacancy days and expand net operating income via services, as seen in the OnPlace portfolio in Italy.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ECB rate hikes widening the mortgage affordability gap | -1.3% | Eurozone-wide, the Netherlands' 40% income share, Germany's purchase-price-to-rent compression, and Spain elevated first-time buyer barriers | Medium term (2-4 years) |

| Stricter EPC rules inflating landlord cap-ex | -0.8% | EU-wide EPBD 2024/1275 compliance; acute in France (G-class ban 2025, F by 2028), Netherlands (D-label 2029), Germany (E-class by 2033) | Long term (≥ 4 years) |

| Southern Europe wage stagnation constraining first-time-buyer affordability | -0.6% | Spain (250k household formation vs 132k visas), Italy, Greece, Portugal; wage growth lagging price escalation by 3-5 percentage points | Medium term (2-4 years) |

| Urban growth boundaries limiting green-field land supply in core cities | -0.4% | Amsterdam, Munich, Frankfurt, Paris, Stockholm, Copenhagen; nitrogen protocols (Netherlands), heritage protection, zoning restrictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ECB Rate Hikes Widening Mortgage Affordability Gap

The European Central Bank’s tightening lifted policy rates to a 4.0% peak before easing, but mortgage rates remain above the 2020 to 2021 period and weigh on first-time buyer access. In the Netherlands, third-quarter 2025 originations rose 21.8% to EUR 44.70 billion (USD 48.3 billion), yet housing costs surpassed 40% of net income for new buyers despite a small drop in the ten-year mortgage rate to 3.76%. Spain saw more than 500,000 mortgages in 2025 and expects sales to rise further, but nine EU countries now exceed 40% of income for the typical mortgage service. Across Europe, household loan growth trails nominal GDP as families rebuild buffers after inflation eroded financial asset ratios since 2020. The result is a bifurcation in the Europe residential real estate market where institutional rental platforms capture households priced out of ownership while high-net-worth buyers rely on equity or family transfers.

Stricter EPC Rules Inflating Landlord Capex

EU rules require a 16% cut in primary energy use by 2030 and 20% to 22% by 2035 relative to 2020, with at least 55% of the gain from the worst-performing homes, which accelerates retrofit needs and capital outlays. France has phased bans on the rental of low-rated dwellings, while the Netherlands is advancing minimum label D for all rentals by 2029 with per-unit subsidies up to EUR 15,000 (USD 16,200) and an allocation of EUR 126 million through 2030 (USD 136.1 million). Spain allows tax deductions up to 60% capped at EUR 9,000, for building-level efficiency works, which often fall short of costs that can exceed EUR 20,000 to EUR 40,000 per apartment in urban buildings. The European Heat Pump Association highlights that upfront costs of EUR 12,000 to EUR 20,000 per installation in multifamily stock remain a barrier for small landlords as electricity-to-gas price ratios differ by country. These rules shift stock from fragmented owners to institutional platforms that can secure financing, negotiate bulk procurement, and access EU programs to improve energy performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Condominiums Capture Institutional Flows Despite Villa Dominance

Villas and landed houses held 65.00% of the 2025 mix, the largest share within the Europe residential real estate market. Apartments and condominiums are projected to expand at a 6.14% CAGR through 2031 as investors rotate to scalable urban multifamily that aligns with EPBD compliance. Rent dynamics in major hubs underscore the appeal, with Berlin’s median asking rent at EUR 19.23 per square meter (USD value in brackets if applied), and key city yields that support stable income performance through the cycle. Lenders favor multifamily with comparatively higher acceptable LTV ranges for prime senior facilities, which supports financing for large platforms. These conditions reinforce the attractiveness of professionally managed multifamily within the Europe residential real estate market.

Detached and semi-detached formats continue to benefit from space-led preferences and suburban demand, but energy labels and retrofit costs are shaping valuations and liquidity. Premiums for efficient classes in Germany and the Netherlands highlight how operating cost savings, rent regulation, and energy subsidies influence pricing. As the Europe residential real estate industry aligns with zero-emission building rules for 2030 new builds, more capital is expected to target assets that can meet future standards with moderate capex. Germany’s transaction flow and lender preference for multifamily, together with rising operational capability in continental portfolios, support the segment’s growth outlook.

By Price Band: Affordable Tier Accelerates on Policy Tailwinds Despite Mid-Market Grip

The mid-market price tier accounted for 46.00% share in 2025, and it remains the largest pool of transactable homes in the Europe residential real estate market. The affordable segment is set to grow at a 6.07% CAGR as governments and institutional partners pursue workforce housing with targeted policies and platform strategies. Policy shifts in the Netherlands expand regulation to mid-segment rentals and influence pricing, while subsidies for energy upgrades help preserve affordability within regulated frameworks. Capital allocators continue to see affordable housing as a way to support long-term economic outcomes and resilience across cycles.

The Netherlands provides a clear example of how regulation and incentives shape the mid-segment, from label requirements to rent-setting formulas. In France, expanded interest-free loans and lower mortgage rates are supporting first-time buyers in mainstream brackets, which helps stabilize demand. Germany’s simplified building standards pilots are meant to compress costs for affordable output, while Spain’s protected rent programs add constrained-price inventory to balance stressed zones. These policy trends favor operators with scale and sustainability expertise in the Europe residential real estate industry.

By Business Model: Rental Platforms Outrun Sales Amid Generation Rent and Regulation

Sales-model transactions accounted for 67.00% of the 2025 split, the dominant share of the Europe residential real estate market. Rental platforms are projected to grow at a 6.24% CAGR to 2031 as Generation Rent expands and institutional mandates emphasize predictable income and diversification. Build-to-Rent features in 32% of living-sector mandates among institutional investors, and investors expect strong unlevered returns from multifamily over the medium term. Leading operators are also digitizing management, which raises efficiency and supports NOI growth through better leasing and energy monitoring.

Sales volume remains strong in markets with improved affordability windows and supportive rate trends, as seen in Spain and France into 2026. UK Build-to-Rent development funding stayed active in 2025 even as starts lagged, supported by a large pipeline of consented homes awaiting unlock. Across the Europe residential real estate industry, rental and sales strategies now co-exist in the same platforms as developers balance risk and absorption.

By Mode of Sale: Primary Gains Traction on Compliance Mandates Despite Secondary Lock

Secondary resales represented 90.0% of 2025 transactions, reflecting the weight of existing stock and the prevalence of suboptimal energy performance in legacy homes across Europe. Primary new-build transactions are projected to grow at a 6.19% CAGR into 2031, helped by streamlined approvals and clear zero-emission standards for new homes from 2030. France’s new-home sales cycle remains slower after shifts in investor tax regimes, while Spain expects higher starts as financing conditions improve.

Existing-home pricing dynamics in Germany and the Netherlands show how retrofit potential and discount-to-new premiums sustain liquidity on the secondary side. National rules that expand mortgage headroom for energy upgrades are nudging buyers toward either compliance-ready new builds or clear value-add retrofits in older homes. As permitting remains slower than desired, primary supply will rise gradually, and the Europe residential real estate market will continue to rely on secondary stock for most transactions.

Geography Analysis

Germany held 22.00% of regional volume in 2025, the largest national share within the Europe residential real estate market, supported by persistent undersupply and tight urban renting conditions. Rent growth in the Top Seven cities ran ahead of inflation in early 2025, while construction costs per square meter remained elevated, which constrained new delivery. Investor interest in multifamily stayed firm, and lender surveys showed favorable LTVs for prime residential, which sustained deal flow into 2025. Germany’s implementation following EPBD, including sustainable heating rules and CO2 cost allocation, is reshaping landlord capex plans and tenancy cost-sharing. Large platforms like Vonovia reported steady rent growth and continued construction starts even as the equity market valued the portfolio at a discount to NAV.

Price growth is forecast to moderate in 2026 after a strong 2025, with re-acceleration expected as the structural shortage persists and borrowing capacity rises alongside wage growth. Permits fell in 2025 due to ecological and grid constraints, and completions in 2024 remained below the 100,000 target, which tightens the outlook and sustains rental growth. Regulatory changes lowered the transfer tax for investment properties from 2026, raised the first-time buyer exemption, and expanded the mortgage guarantee ceiling to support demand. Subsidies for rental-home energy upgrades add further momentum to retrofit capital deployment that will influence the Europe residential real estate market in this decade.

Spain posted double-digit price growth into late 2025, with transactions above 700,000 and forecasts for 2026 pointing to elevated sales and stable mortgage origination. A large accumulated deficit and limited approvals relative to estimated needs are keeping pressure on prices and rents in main metro areas. Gross yields increased compared to late 2024, and 2026 rents are expected to rise further while national and local controls try to moderate stress in tension zones. France is stabilizing after a prolonged price correction, helped by lower mortgage rates and an expanded interest-free loan scheme for first-time buyers. UK policy changes in 2025–2026 are transforming private renting while exempting PBSA and BTR from some constraints, which supports professional platform growth as new rules take effect.

Regulatory Landscape

Directive (EU) 2024/1275 (recast EPBD) is a central EU-wide regulatory anchor for residential assets, linking capital allocation and renovation sequencing to mandatory energy-performance trajectories. The directive requires Member States to set national trajectories for progressive renovation of the residential building stock by 29 May 2026, with the market impact concentrated in older, low-rated urban multifamily where compliance planning, capex timing, and leasing strategy increasingly move together.

Policy focus has also broadened from energy to housing availability and platform behavior. In December 2025, the European Commission introduced a European Affordable Housing Plan and advanced work toward an Affordable Housing Act to be presented in 2026, while short-term rental oversight tightened as the EU short-term rentals data-sharing framework became applicable in May 2026, increasing reporting and compliance needs for platform-mediated rentals. On the financing side, European Banking Authority guidelines on ADC exposures to residential property entered into force on 04 November 2025. They affect how banks assess and risk-weight residential construction lending under Article 126a, reinforcing the premium for clear presales, robust collateral, and compliant building specifications.

Value Chain Analysis

Europe residential real estate value creation runs from land and planning (zoning, permitting, and utilities capacity) through development (design, financing, general contracting, and specialist trades), then to transaction and operation (brokerage, conveyance, valuation, property management, and resident services). The chain remains fragmented, with delivery dependent on local permitting throughput and craft-based subcontracting, which raises schedule risk and keeps labor availability and contractor health material to both new-build and refurbishment programs.

Retrofit and compliance workflows are taking a larger share of activity alongside new supply, pulling in energy auditors, EPC assessors, MEP contractors, heat-pump installers, and building-envelope suppliers, along with digital tools for coordination. Execution activity continues, including Veidekke securing a contract in April 2026 to build 62 apartments at Poulssons Kvarter in Baerum, Norway, and Skanska commencing phase 3 of the NU residential project in Warsaw in June 2026 (156 apartments). Supply-side frictions also persist, including labor constraints and episodic material availability stress, with Germanys reported material supply constraints rising to 9.2% of construction companies in April 2026. This continues to support industrialized approaches such as BIM-enabled coordination and off-site or standardized renovation packages to reduce rework, compress lead times, and improve cost control.

Competitive Landscape

The European residential real estate market is moderately competitive. The Europe residential real estate market features large integrated platforms alongside a wide base of private landlords, which results in moderate concentration and varied operating models across regions. Digitalization is now core to operating efficiency, as seen in platforms that centralize leasing, maintenance, and energy management to boost NOI. Sustainability plans and zero-emission alignment are key to future-proofing portfolios, and leading landlords are allocating multiyear capex to accelerate the transition. Cross-border capital represented a sizable share of activity, and pan-European operators gained valuation advantages through scale and consistent ESG protocols.

Strategic M&A and platform building continued in 2025–2026. Partners Group acquired Empira Group in January 2025, adding a large development pipeline and deep retrofit capability focused on Germany. Aedifica and Cofinimmo agreed to merge in June 2025, creating a leading European REIT specialized in healthcare and senior housing. A UK pension-led consortium acquired PRS REIT later in 2025, signaling institutional interest in scaled single-family rental exposure.

Specialized living segments saw continued capital formation and development. UK BTR investment held steady through the first three quarters of 2025, with development-forward capital dominating flows. Scotland carved out exemptions for BTR and PBSA from rent control areas in 2025, which is expected to lift starts in 2026. Several markets inked policies to support conversions and expedite approvals, and Germany flagged a conversion program for 2026 using subsidized finance without rent caps, with the goal of delivering homes faster in constrained segments.

Europe Residential Real Estate Industry Leaders

-

Vonovia SE

-

LEG Immobilien AG

-

Heimstaden Bostad AB

-

TAG Immobilien AG

-

Grand City Properties S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The largest near-term whitespace sits in scaling energy-renovation delivery models that meet EPBD obligations while keeping projects financeable for fragmented owners and manageable for tenants. The EPBD recast requires national renovation trajectories by 29 May 2026 and formalizes a pathway to progressive decarbonization of residential stock by 2050, which creates demand for repeatable solutions (envelope, heat, controls) and for service aggregation that lowers customer-acquisition and project-management costs. The European Commission's March 2026 recommendation and guidance for building-renovation One-Stop Shops supports this opportunity by standardizing how advisory, technical assistance, and financing navigation can be packaged for households and landlords.

A second opportunity is the industrialization and digitization of the renovation and development pipeline to counter permit delays and supply-chain fragmentation. Horizon Europe demonstrations, including projects such as DTERBIM, INPERSO, and DigiFab, are advancing BIM, digital twins, AI-enabled design, and advanced fabrication methods aimed at cutting renovation timelines and improving cost predictability. In parallel, EU workstreams evaluating digitalization of permitting procedures from December 2025 to October 2026 are intended to support faster throughput where adopted. With residential permits reported down in 2025 (BNP Paribas Real Estate) and house prices still rising year on year in early 2026 (Eurostat), platforms that can combine compliant capex execution with standardized operations can capture both retrofit-led value creation in legacy stock and professionally managed rental demand in supply-constrained metro areas.

Recent Industry Developments

- July 2026: TAG Immobilien AG received an S&P Global long-term rating upgrade to BBB, following a Moody's upgrade to Baa2 in May 2026. The higher ratings improve access to longer-tenor funding and support balance-sheet flexibility for development, modernization capex, and portfolio rotation across TAGs core markets.

- June 2026: Heimstaden Bostad AB issued SEK 650 million in green senior unsecured floating rate notes with a 3.5-year maturity. The transaction supports liquidity while aligning funding with energy-efficiency upgrades and sustainability-linked capex programs that are becoming more central under EU building-performance rules.

- January 2025: Partners Group acquired Empira Group, adding a vertically integrated German residential platform with a large development and retrofit pipeline. The deal strengthened Partners Groups ability to execute energy retrofits and scale build-to-rent operations in Germany, where compliance-driven capex and housing undersupply are reshaping portfolio strategies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the total value of residential property activity across Europe, including sales and rental income for homes such as apartments, condominiums, villas, and landed houses, with values expressed in USD.

Scope exclusions: We exclude student dormitories, tourist accommodation, senior-only care homes, and timeshares.

Segmentation Overview

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to set the market boundary and to build consistent input series across countries before we size totals. We typically refer to public housing and construction releases, land registry and transaction statistics, and central bank policy notes because these sources explain how prices and affordability moved during the base period.

We also use official and non-paywalled sources such as Eurostat, national statistical offices, central banks, public land registry agencies where available, and publications from groups such as the European Mortgage Federation, which help validate home price indices, mortgage rates, and lending volumes. Company annual reports, investor presentations, and credible press were reviewed to cross-check rental trends and development pipelines, and then a paid subscription for company financials and news was used selectively to standardize coverage across markets. These desk research sources are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were run with a mix of developers, broker networks, institutional owners, lenders, and service providers to confirm how transaction momentum, rental demand, and pricing actually played out by country. We also spoke with practitioners across the region so our assumptions on buyer mix, build to rent penetration, and supply constraints could be adjusted where desk signals were incomplete.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 57% | Functional/Unit leaders: 34% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where country level housing stock, transaction counts, and rental occupied units are translated into value pools using observed price and rent benchmarks, and then rolled up to the Europe total. To keep the result grounded, we corroborate the totals with selective bottom-up checks, such as sampled price per square meter ranges applied to typical unit sizes, and channel checks on primary versus secondary sales splits, before adjusting outliers.

Key inputs used in the model include home price indices and their lag to policy rates, mortgage rates and approval volumes, household formation and migration signals, residential completions and permits, and rent growth versus wage growth (all used as direction and sanity checks, not as a full causal system). Forecasting is done using scenario analysis supported by trend smoothing, where rate paths and affordability are varied and then aligned to what interviewees expect in terms of transaction recovery timing and rental resilience. Where country data series have gaps, proxy indicators from closely comparable markets are used and then scaled back using housing stock and income levels so the final curve does not overstate smaller markets.

Data Validation & Update Cycle

Outputs are checked against independent signals such as transaction volumes, price index movement, mortgage activity, and new supply indicators to confirm the implied story makes sense. When a country shows unusual variance, the assumptions are re-visited and interview follow-ups are triggered so the model does not carry forward a one-time spike or a reporting artifact.

Before sign-off, the work goes through a multi-step analyst review where calculations, currency conversions, and growth logic are rechecked and any large residuals are explained in plain notes. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Europe Residential Real Estate Market Size Versus Other Published Estimates

Published market values for Europe residential real estate can look far apart because teams often count different transaction types, mix price levels differently across countries, and pick different base years during volatile rate cycles. Differences also show up when rental income is treated as part of the market by one model and excluded by another.

By tracking transaction activity, rent benchmarks, and country coverage rules, Mordor Intelligence keeps the scope consistent across EU-27, the UK, EFTA, and key micro-states, while excluding student dormitories, tourist accommodation, senior-only care homes, and timeshares.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.90 T (2026) | |

| Regional Consultancy A | USD 0.95 T (2024) | This figure appears anchored to an earlier base year and a narrower value pool, and it can undercount when rental value and cross-country price dispersion are not consistently carried through the roll-up. |

| Industry Publisher B | USD 3.97 T (2025) | This figure likely reflects a broader inclusion set and a higher revenue interpretation of residential activity, which can lift totals when definitions of rent, sales value, or adjacent residential formats are treated as in-scope. |

The spread in the table is mainly explained by what is counted as residential activity, which year anchors currency conversion, and how consistently countries are rolled up using the same demand and pricing signals. With clear inclusions and repeatable checks, the final number is easier to trace and update as rates, rents, and transactions shift.

Key Questions Answered in the Report

What is driving capital flows into the Europe residential real estate market in 2026?

Cross-border buyers held 45% of transactions in 2025 and are prioritizing build-to-rent and multifamily platforms that meet energy standards and offer scale.

How are EU retrofit rules affecting the Europe residential real estate market?

Directive (EU) 2024/1275 requires significant energy cuts by 2030 and 2035, accelerating retrofit programs, enabling rent uplifts under certain rules, and favoring institutional owners who can manage large capex.

Which living segments are growing fastest within the Europe residential real estate market?

PBSA rose 71% year over year through Q3 2025 to reach 6% of total European real estate investment, while multifamily retained the deepest liquidity.

Which country leads Europe in multifamily transactions today?

Germany led first-half 2025 with EUR 4 billion in multifamily deals and a 27% share, supported by lenders’ top preference and prime LTVs of 60% to 65%.

How are mortgage costs influencing tenure choices in the Europe residential real estate market?

Elevated mortgage burdens and high price-to-income ratios are steering more households to rentals, which supports platform growth and build-to-rent development.

What policy shifts are shaping build-to-rent in the UK and Scotland?

UK tenancy reforms and Scotland’s 2025 exemption of build-to-rent from Rent Control Areas are intended to support professional operators and restart development pipelines.

Page last updated on: