Scandinavian Residential Real Estate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

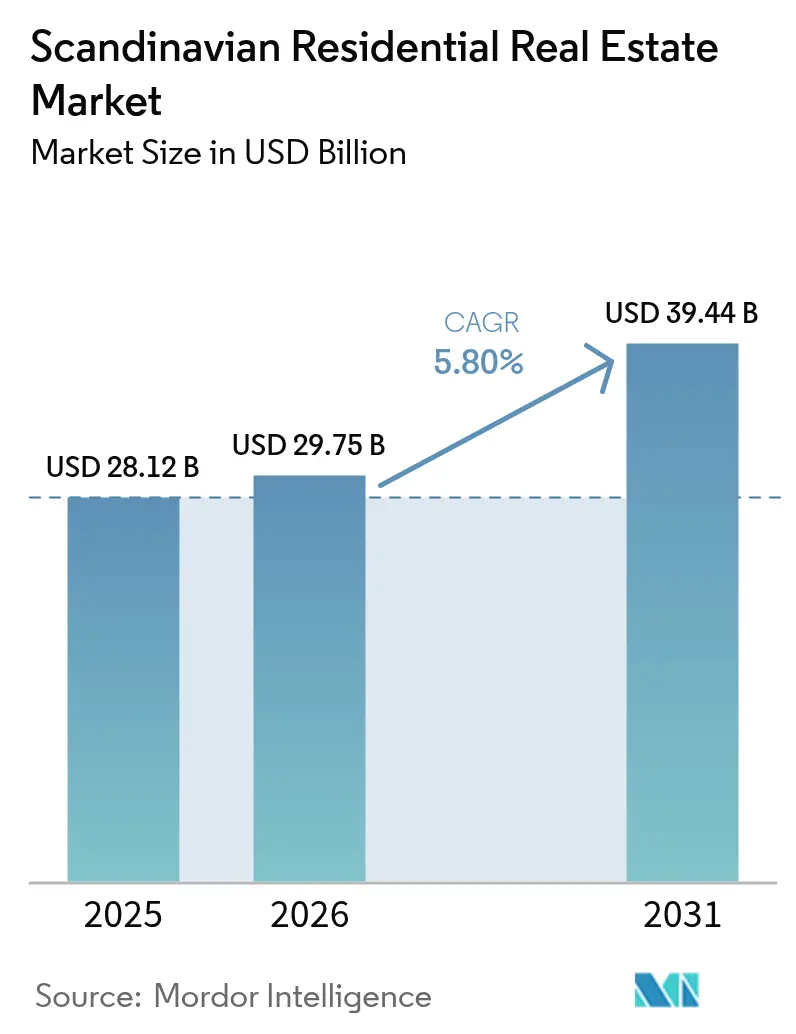

| Base Year Market Size (2025) | USD 28.12 Billion |

| Market Size (2026) | USD 29.75 Billion |

| Market Size (2031) | USD 39.44 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scandinavian Residential Real Estate Market Analysis by Mordor Intelligence

Scandinavian residential real estate market size in 2026 is estimated at USD 29.75 billion, growing from 2025 value of USD 28.12 billion with 2031 projections showing USD 39.44 billion, growing at 5.80% CAGR over 2026-2031. Normalized interest rates, a surge of institutional capital and demographic shifts toward renting underpin this growth trajectory[1]Erik Thedéen, “Monetary Policy Report April 2025,” Sveriges Riksbank, riksbank.se. Sweden’s rapid rate-cut cycle, Denmark’s consistent 4.2% annual price gains through 2026 and Norway’s looser lending terms collectively expand transaction volumes and bolster pricing power[2]Michael Rasmussen, “Nordea Housing Market Outlook 2025,” Nordea, nordea.com. Tight urban land supply intensifies demand for high-density apartments, while EU-aligned green-building rules accelerate new-build activity across the Scandinavian residential real estate market. Institutional investors, lured by predictable rental cash flows and ESG credentials, now treat housing as a core allocation alongside logistics and infrastructure.

Key Report Takeaways

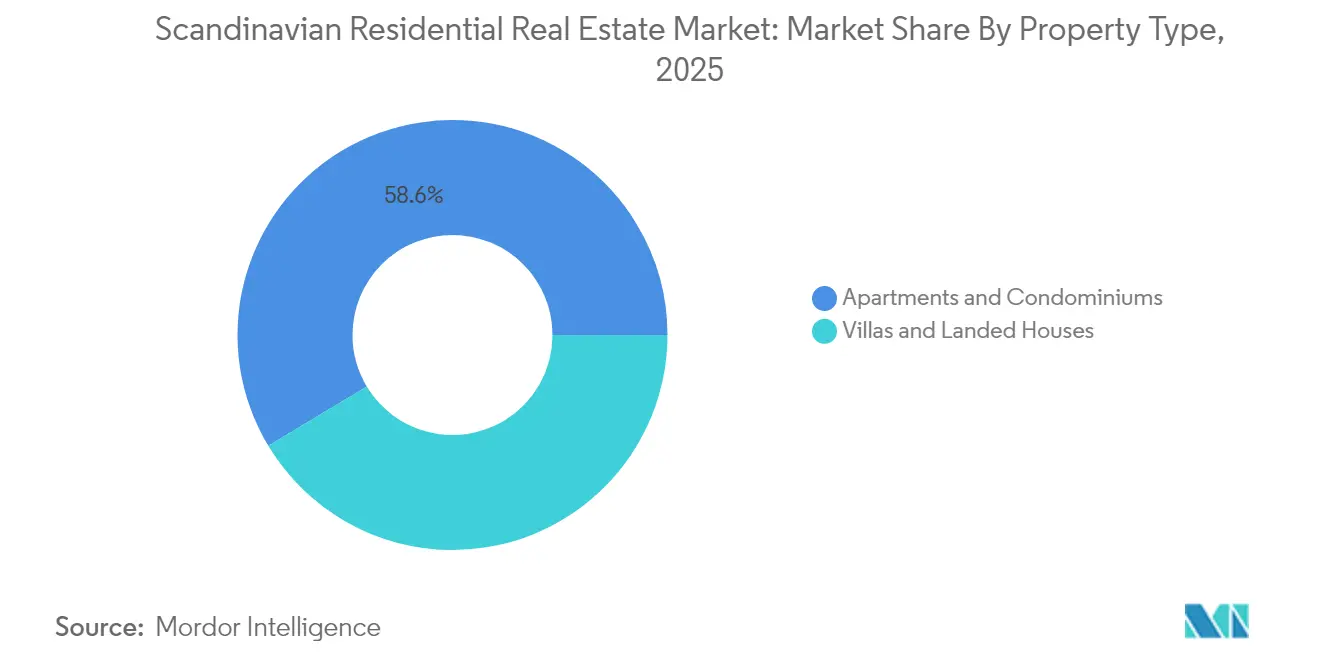

- By property type, apartments and condominiums commanded 58.62% share of the Scandinavian residential real estate market size in 2025 and are projected to grow at a 6.02% CAGR through 2031.

- By price band, the mid-market segment held 45.55% share of the Scandinavian residential real estate market size in 2025; the affordable tier is advancing at a 6.08% CAGR to 2031.

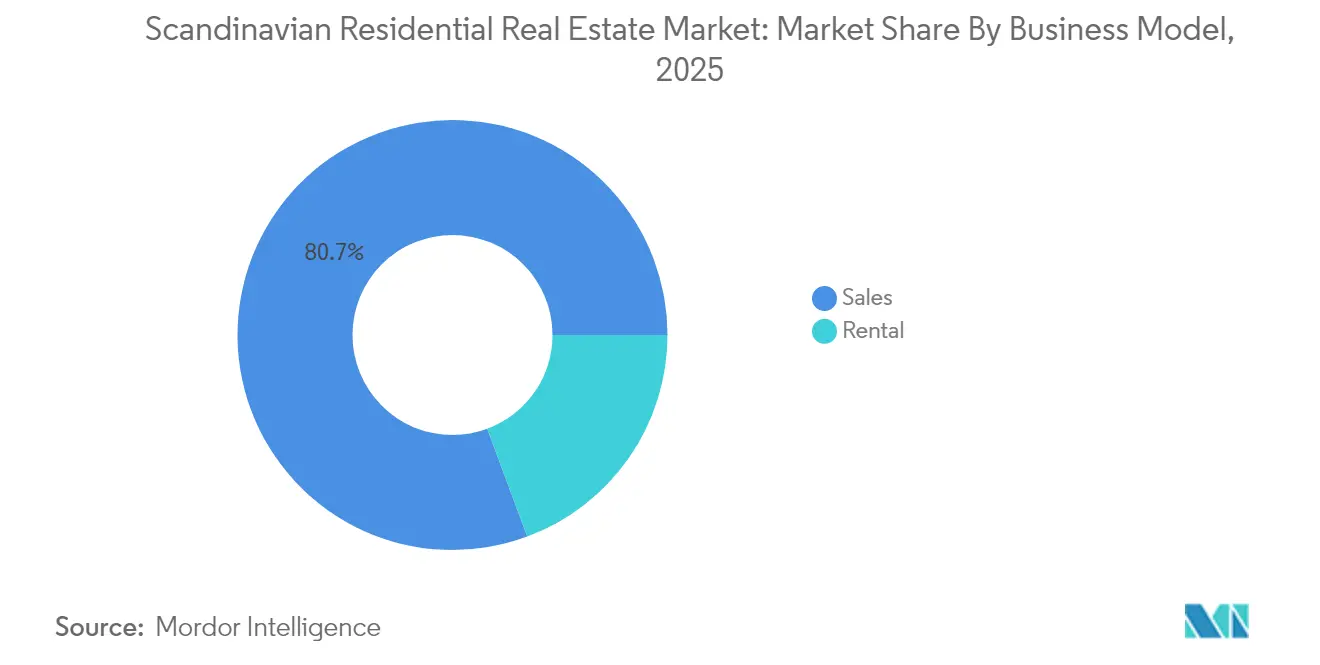

- By business model, rental housing captured 19.35% of Scandinavian residential real estate market share in 2025 and is forecast to expand at 6.74% CAGR through 2031.

- By mode of sale, primary transactions accounted for 37.45% share of the Scandinavian residential real estate market size in 2025 and will grow at 6.79% CAGR between 2026-2031.

- By geography, Sweden led with 47.60% of Scandinavian residential real estate market share in 2025, while Denmark is forecast to expand at 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Scandinavian Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest-rate normalisation & expected cuts | +1.5% | Global, strongest in Sweden and Norway | Short term (≤ 2 years) |

| Rapid urbanisation & shrinking household size | +1.2% | Sweden and Denmark urban centers, spillover to Norway | Medium term (2-4 years) |

| Institutional capital inflow & REIT expansion | +1.1% | Stockholm and Copenhagen | Medium term (2-4 years) |

| Green-housing incentives & EPC regulation | +0.8% | EU-wide, early adoption in Denmark and Sweden | Long term (≥ 4 years) |

| Municipal land-release reforms | +0.7% | National policies, city-specific execution | Long term (≥ 4 years) |

| Cross-border remote-worker inflow | +0.6% | Major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interest-Rate Normalisation & Expected Cuts

The Riksbank’s key rate is set to slide to 2.25% by 2025, while Norges Bank guides toward a 3.25% base rate, lowering mortgage servicing costs and boosting loan approvals. Sweden saw investment volumes rebound 66% year-over-year to SEK 138.5 billion in 2024, with residential assets representing 28% of deal flow. Danish mortgage coupons stabilised near 3.5%, opening regional arbitrage opportunities for cross-border capital. First-time buyers already make up half of new Norwegian home loans after down-payment rules eased, signalling rising proprietorship demand. Cheaper credit also galvanises institutional allocations, a structural boon for the Scandinavian residential real estate market.

Rapid Urbanisation & Shrinking Household Size

Population concentration and smaller household units intensify demand for compact apartments in Stockholm, Copenhagen and Oslo. Average household size is falling, prompting developers to prioritize micro-units, coworking lounges and shared amenities that raise per-square-meter revenue while preserving affordability. Oslo’s central districts posted 6% price growth in 2024, underscoring how urban cores command a premium despite flexible work trends. The Scandinavian residential real estate market therefore pivots toward high-density projects that limit commute times and offer lifestyle convenience. Remote workers still gravitate to lively neighborhoods, reinforcing the value proposition of centrally located apartments.

Institutional Capital Inflow & REIT Expansion

Residential allocations now rank third in global cross-border flows into Europe, jumping 10% to USD 21.63 billion in H2 2024. Foreign investors accounted for 45% of Danish residential trades in the same period, attracted by krona hedging benefits and stable yields. Stockholm REITs achieved liquidity spikes after regulatory tweaks simplified unit issuance, enabling retail investors to piggy-back on institutional underwriting. Scale-seeking pension funds back build-to-rent vehicles that promise predictable income and ESG compliance, deepening capital pools for the Scandinavian residential real estate market. Manager competition now centres on track record and sustainability scores rather than leverage.

Green-Housing Incentives & EPC Regulation

Denmark will cap operational emissions for all new housing at 7.1 kg CO2e/m²/year from July 2025, forcing a shift toward timber, recycled steel and on-site renewables. Stockholm Wood City, a 2,000-unit mass-timber district, exemplifies the cost and branding upside of exceeding minimum environmental thresholds. Nordic lenders offer interest-rate rebates for EPC-rated projects, translating sustainability into cheaper capital. Energy-efficient stock realizes rental premiums and lower vacancy risk, bolstering cash-flow resilience across the Scandinavian residential real estate market. Developers integrating heat-pump systems and smart-metering platforms report faster pre-sales and reduced lifecycle costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High household indebtedness | -0.9% | Norway and Sweden, moderate effect in Denmark | Short term (≤ 2 years) |

| Macro-prudential lending caps (LTV/DSI) | -0.7% | All three countries with varying implementation | Medium term (2-4 years) |

| Skilled-labour shortage in modern timber construction | -0.6% | Sweden and Denmark mass-timber projects, spillover to Norway | Medium term (2-4 years) |

| Climate-adaptation cost for coastal homes | -0.5% | Denmark and Norway coastal zones, limited pockets in Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Household Indebtedness

Norwegian households allocate a significant share of disposable income to mortgages, with 14.5% experiencing acute strain during 2023’s rate spike[3]José Manuel Campa, “ESRB Warning on Vulnerabilities in Residential Real Estate Sectors,” European Systemic Risk Board, esrb.europa.eu. Sweden and Denmark likewise face elevated debt-to-income ratios, prompting warnings from the European Systemic Risk Board about variable-rate exposure. Heavy leverage curbs upgrade activity and dampens speculative demand across the Scandinavian residential real estate market. Younger buyers juggling student loans and rising living costs delay ownership, sustaining rental demand but clipping sales momentum. Banks respond with tougher underwriting, preserving asset-quality ratios at the expense of loan-book growth.

Macro-Prudential Lending Caps (LTV/DSI)

Regulators maintain LTV ceilings and impose debt-service limits to contain systemic risk, thereby capping leverage available to first-time buyers. Norway’s down-payment cut to 10% eases entry but overall borrowing power remains constrained by DSI rules, particularly in Oslo’s pricey districts. Stockholm buyers confront similar affordability walls as banks stress-test loans at interest-rate buffers well above prevailing coupons. While these policies fortify financial stability, they slow turnover and temper price escalation within the Scandinavian residential real estate market. Developers pivot to rental and co-living offerings to monetise demand sidelined by credit caps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments Drive Urban Density

Apartments and condominiums secured 58.62% of Scandinavian residential real estate market share in 2025 and register the fastest 6.02% CAGR through 2031. Villas hold the remaining 41.38%, appealing to families favoring private outdoor space in commuter belts. High land costs, zoning limits and mass-timber modular systems give apartments superior build-economics, supporting sustained outperformance in the Scandinavian residential real estate market.

Stockholm Wood City’s 2,000 units illustrate how embedded coworking, EV charging and neutral-carbon credentials unlock premiums among eco-conscious urbanites. Developers also exploit density bonuses offered by municipalities to integrate public transport nodes and mixed-use podiums. Energy-sharing heat grids cut operating bills, reinforcing occupancy stability for institutional landlords and underpinning the segment’s contribution to Scandinavian residential real estate market size.

By Price Band: Mid-Market Dominance Faces Affordable Pressure

Mid-market homes represented 45.55% of Scandinavian residential real estate market size in 2025, balancing quality and cost for dual-income households. Yet policy-backed affordable stock is expanding at 6.08% CAGR, aided by municipal land-release auctions and favourable VAT waivers.

Danish schemes permitting shared-equity mortgages have widened the buyer base, creating tailwinds for affordable builders and cooperative housing associations. Luxury residences remain niche, battling a smaller demand pool and higher capital-gains taxes. The mid-market must therefore differentiate via smart-home packages and flexible layouts to retain wallet share in the increasingly competitive Scandinavian residential real estate market.

By Business Model: Rental Surge Reshapes Ownership Patterns

Rental housing held 19.35% of Scandinavian residential real estate market share in 2025 but accelerates at a sector-leading 6.74% CAGR, propelled by mobility-minded professionals and strict credit rules. Sales transactions grow more modestly as ownership affordability wanes.

Institutional funds back purpose-built rental platforms offering hotel-grade services, bulk broadband and community apps that lift retention. Copenhagen’s rents climbed 5-7% in 2024 amid undersupply, cushioning investor yields versus bond spreads. The rental boom is therefore reshaping cash-flow expectations and asset-allocation models across the Scandinavian residential real estate market.

By Mode of Sale: Primary Market Leads New Construction

Primary sales captured 37.45% of Scandinavian residential real estate market size in 2025 and are forecast to expand at 6.79% CAGR, buoyed by pent-up demand for energy-efficient inventory. Secondary trades, though larger at 62.55%, contend with ageing stock that often requires costly retrofits to meet EPC thresholds.

Developers leverage modular timber, BIM and on-site PV arrays to cut embodied carbon and shorten delivery cycles, thereby securing green-loan discounts and faster absorption rates. Buyers prize customisable interiors and future-proof wiring, validating premiums that lift gross development margins in the Scandinavian residential real estate market.

Geography Analysis

Sweden commanded 47.60% of Scandinavian residential real estate market value in 2025, powered by Stockholm’s technology-led jobs boom and landmark urban timber schemes such as Stockholm Wood City. Residential investment hit SEK 138.5 billion in 2024, a 66% rebound that signals re-liquefied capital markets and expanding Scandinavian residential real estate market size. Rate cuts and balanced housing policy sustain demand across both ownership and rental sectors, while EPC incentives reward green-forward developers.

Denmark is the fastest-growing slice of the Scandinavian residential real estate market at 6.86% CAGR to 2031, anchored by Copenhagen’s 61% transaction share and 45% foreign-capital penetration. House prices are projected to rise 4.2% in 2025 and 4.0% in 2026 on the back of tight labour markets and wage growth beating inflation. Emissions caps effective July 2025 amplify demand for next-generation, low-carbon housing, reinforcing Denmark’s regulatory leadership and supporting further expansion of Scandinavian residential real estate market size.

Norway retains a meaningful position despite indebtedness headwinds and buildable-land scarcity near fjordside metros. The government’s down-payment relaxation to 10% from January 2025 broadens access, while base-rate reductions ease servicing costs, nudging latent demand into action. Oslo’s prime districts predict 6% price appreciation in 2024, as currency weakness entices overseas buyers and green construction incentives attract institutional partners. The country’s surplus renewable energy underpins highly efficient housing, differentiating Norway within the broader Scandinavian residential real estate market.

Competitive Landscape

The Scandinavian residential real estate market is moderately fragmented. Fastighets AB Balder manages SEK 216.9 billion in assets, maintaining a 50% net-debt-to-assets ceiling to safeguard credit metrics. Heimstaden Bostad controls 71,838 homes with SEK 2.3 billion rental income and >97% occupancy, illustrating the scale institutional landlords now bring to the Scandinavian residential real estate market. Skanska adapts its pipeline, prioritising energy-efficient builds after recording SEK 42.8 billion revenue in Q3 2024 despite softer condo presales.

PropTech challengers multiply. Oslo-based Findable raised EUR 9 million to automate document compliance across 2 million property files, signalling that data-driven OPEX reduction is a new competitive lever. Bane NOR Eiendom teamed with Telescope to embed AI risk-scoring across its portfolio, marrying sustainability reporting with asset-management dashboards. Such partnerships intensify the digital arms race, forcing incumbents in the Scandinavian residential real estate market to integrate sensors, IoT and analytics or risk obsolescence.

Institutional consolidation continues in build-to-rent, where pension and insurance capital seek platform scale to harvest steady cash flows. KLP Eiendom’s acquisition of Ulven Boligutleie extends its Norwegian rental foothold, while Brookfield’s SEK 95 billion commitment to Swedish data-centre infrastructure may spur ancillary housing demand for tech-sector staff. Overall, capability differentiation hinges on balance-sheet strength, ESG credentials and operational tech adoption within the Scandinavian residential real estate market.

Scandinavian Residential Real Estate Industry Leaders

Riksbyggen

Fastighets AB Balder

Danish Homes

Dades AS

Veidekke ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Brookfield Asset Management plans SEK 95 billion investment in Swedish AI infrastructure, potentially lifting regional housing demand.

- March 2025: Scandinavian Astor Group AB issues SEK 125 million of new shares to fund acquisitions after 329% Q4 2024 revenue growth.

- March 2025: Findable secures EUR 9 million Series A to expand its AI property-management platform.

- February 2025: KLP Eiendom acquires Ulven Boligutleie, boosting Norwegian rental exposure.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Scandinavia's residential real estate market as the annual transactional value of newly built and existing housing units, including apartments, condominiums, villas, and landed houses, sold or rented in Denmark, Norway, and Sweden during 2019-2030. The figure captures developer sales, secondary-market conveyances, and formal rental contracts that generate monetary consideration in local currency, converted to U.S. dollars by year-average exchange rates.

Exclusions: Commercial premises, student dorms, cooperative shares issued without a deed, and transactions in Finland or Iceland remain outside scope.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Existing-home Resale)

- By Country

- Norway

- Sweden

- Denmark

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed municipal planners, residential brokers, developer finance leads, and buy-to-let funds across Copenhagen, Oslo, Stockholm, and key second-tier cities. The conversations clarified absorption rates, discounting tactics, preferred unit sizes, and investment appetite, enabling us to fine-tune model coefficients and validate secondary findings.

Desk Research

We began with country housing statistics sourced from national land registries, central banks, and statistics offices, then overlaid macro signals from OECD, Eurostat, and Nordic price indexes. Regulatory texts, land-use plans, and permit dashboards framed supply pipelines, while listed developers' filings, IFC mortgage data, and paid datasets such as D&B Hoovers and Dow Jones Factiva enriched company-level volumes and prevailing pricing. Finally, trade-association notes, construction-cost indices, and reputable press helped sense short-term demand pivots. This list is illustrative, and many additional public and subscription sources were consulted for cross-checks.

Market-Sizing & Forecasting

A top-down build starts with recorded transaction values published by each country's cadastre, which are then adjusted for informal cash deals using broker insights. Results are cross-checked through sampled bottom-up roll-ups of major developers' closings and rental inventory to validate order of magnitude. Key inputs include housing starts, mortgage-rate trends, net immigration, median household income, and urbanization velocity; their interplay is forecast through a multivariate regression complemented by scenario analysis for interest-rate shocks. Where developer disclosures are incomplete, gap factors are imputed from historical absorption ratios verified in primary interviews.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review that flags abnormal swings versus prior years, plots the series against independent indices, and triggers call-backs when deviations exceed preset bands. The dataset refreshes annually, with interim revisions when material policy or rate shifts occur, and a final sense-check is performed before publication.

Why Our Scandinavian Residential Real Estate Baseline Commands Reliability

Published estimates often diverge because firms vary geographic cutoffs, treat asset values differently, and apply inconsistent price-capture methods.

By sticking to transacted residential value only and refreshing models each year, Mordor Intelligence offers a lean yet timely baseline that decision-makers can trace back to concrete records.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.12 B (2025) | Mordor Intelligence | - |

| EUR 500 B (2023) | Regional Consultancy A | Includes commercial assets and Finland, reports total stock value rather than yearly turnover |

| USD 10.12 T (2024) | Global Consultancy B | Uses modeled asset capitalization across all property classes, relies on macro ratios without transaction verification |

In sum, others widen scope or inflate values through asset-stock valuations, whereas our disciplined focus on observable transactions and transparent variables keeps the Scandinavian baseline balanced and repeatable for clients.

Key Questions Answered in the Report

What is the current size of the Scandinavian residential real estate market?

The market is valued at USD 29.75 billion in 2026 and is projected to reach USD 39.44 billion by 2031.

Which country leads in market share?

Sweden holds 47.60% of market value, backed by Stockholm’s technology economy and large-scale timber projects.

How do green-building regulations affect development costs?

Denmark’s 2025 CO₂ cap and broader EPC rules encourage mass-timber and renewable energy use, raising upfront costs but unlocking financing discounts and premium pricing.

Which property type offers the best growth outlook?

Apartments and condominiums post the strongest 6.02% CAGR, driven by urbanisation and efficient land use.

Page last updated on: