Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

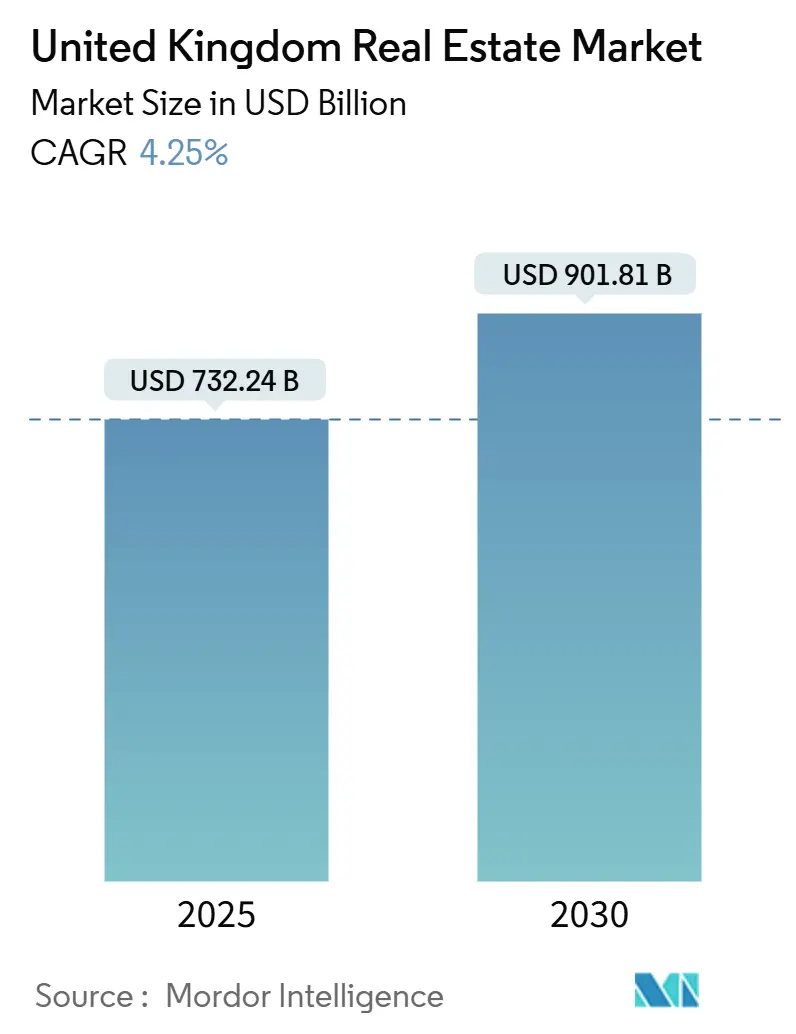

| Market Size (2025) | USD 732.24 Billion |

| Market Size (2030) | USD 901.81 Billion |

| Growth Rate (2025 - 2030) | 4.25% CAGR |

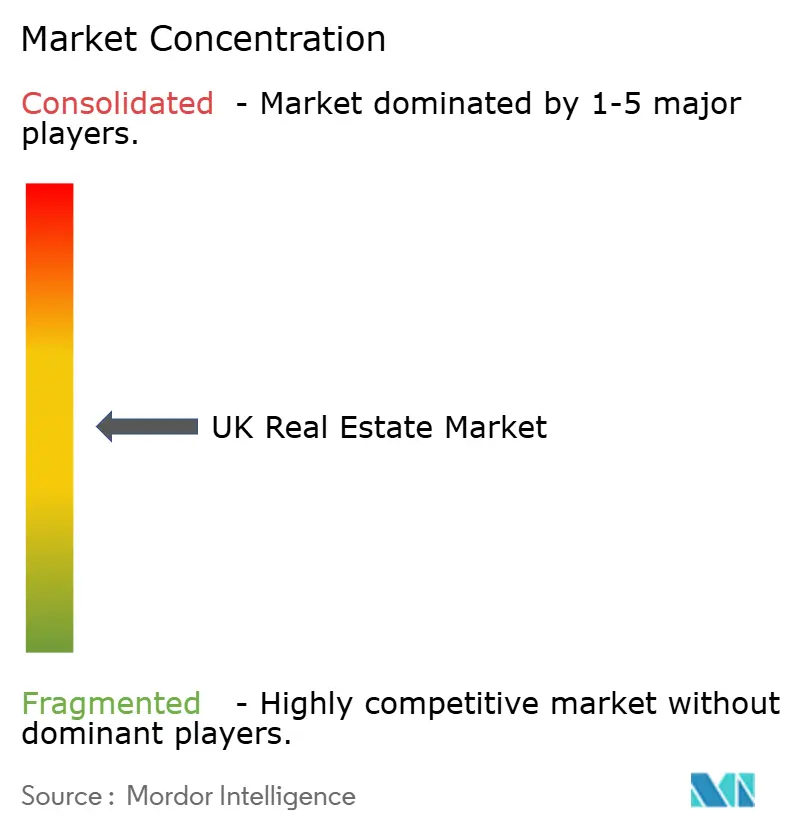

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Real Estate Market Analysis by Mordor Intelligence

The United Kingdom Real Estate Market size is estimated at USD 732.24 billion in 2025 and is expected to reach USD 901.81 billion by 2030, at a CAGR of 4.25% during the forecast period (2025-2030). Accelerated home-building targets, resilient institutional investment, and a stable legal framework sustain this growth even as interest-rate volatility lingers. Institutional inflows continue to favor logistics, build-to-rent, and mixed-use schemes, while e-commerce expansion boosts demand for warehouse space. Government planning reforms and brownfield incentives shorten project timelines, and technology adoption is improving planning efficiency. Tight supply in key regions supports price stability, but elevated construction costs and labor shortages keep margins under pressure[1]Department for Levelling Up, Housing and Communities, “Brownfield Land Release Fund 2,” GOV.UK, gov.uk.

Key Report Takeaways

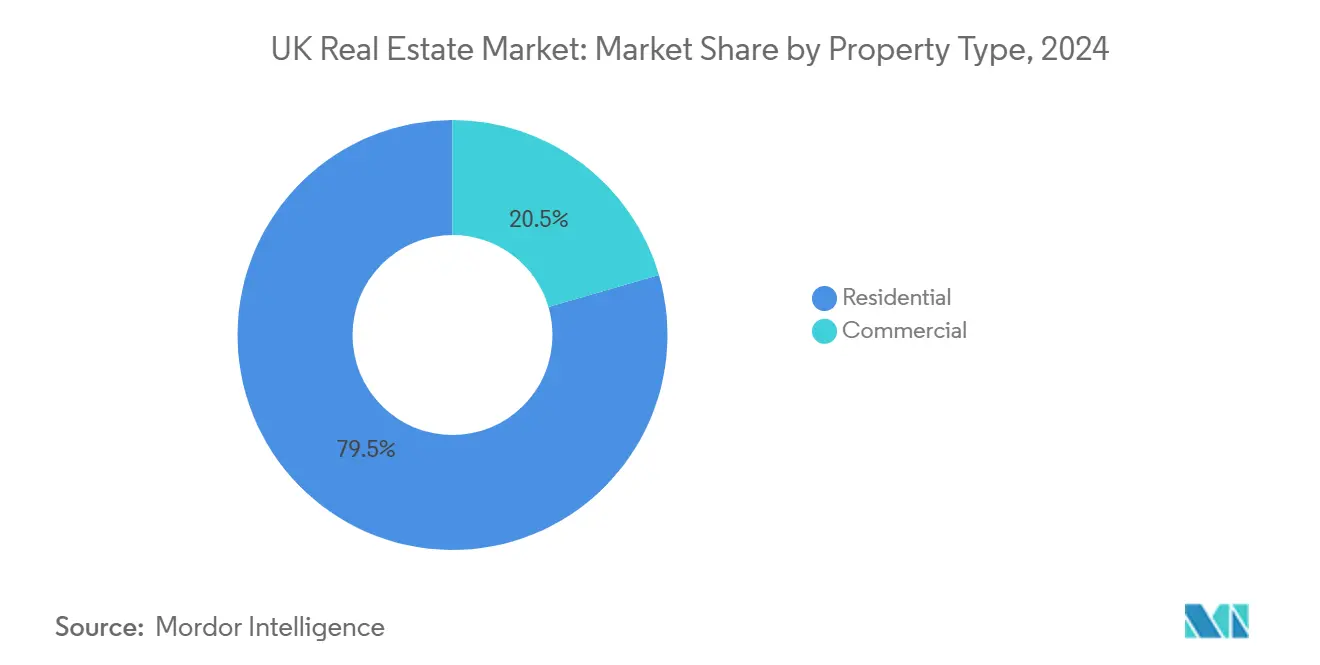

- By property type, residential led with 79.5% revenue share of the United Kingdom real estate market in 2024; logistics is projected to post the fastest 4.81% CAGR through 2030.

- By business model, the sales segment held 65.2% share of the United Kingdom real estate market size in 2024, while rentals are expected to expand at a 4.93% CAGR during 2025-2030.

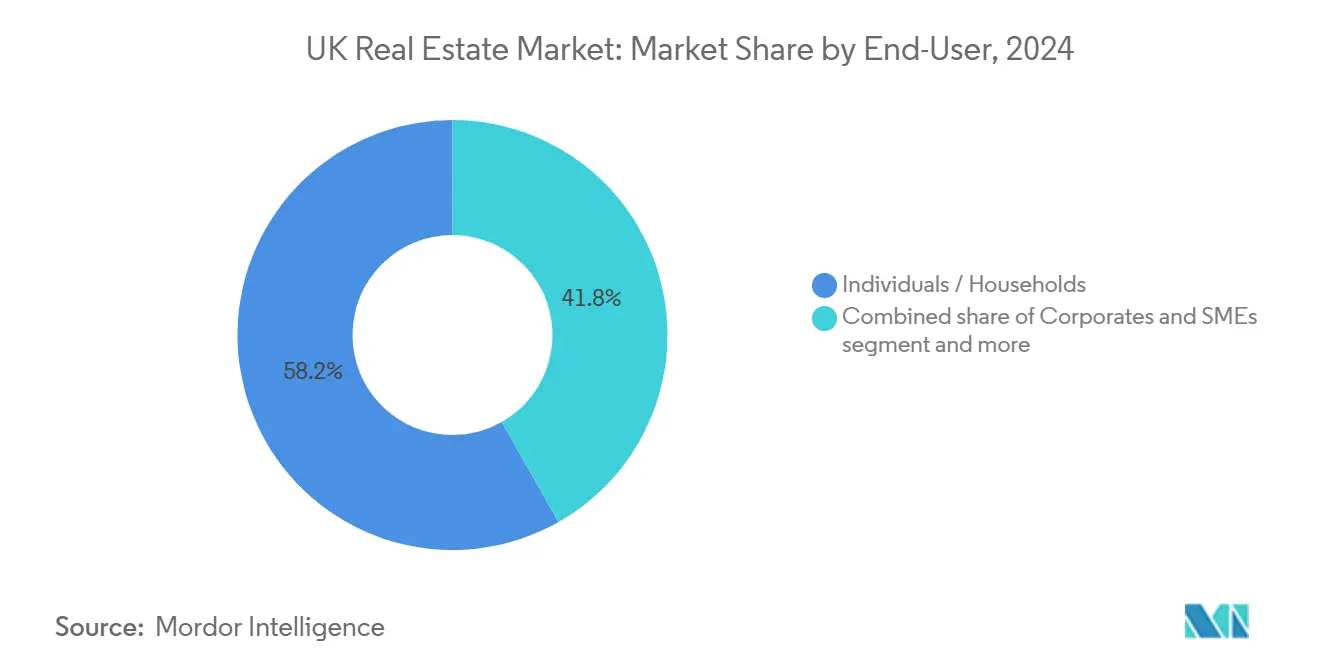

- By end-user, individuals and households accounted for 58.2% of the United Kingdom real estate market share in 2024, and this segment is forecast to grow at the fastest 5.07% CAGR to 2030.

- By geography, England dominated with a 71.2% revenue share in 2024 in the UK Real Estate Market; Scotland is set to record the highest 5.35% CAGR between 2025-2030.

United Kingdom Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong institutional capital inflows into logistics, build-to-rent, and life-science assets | +1.2% | England core, Scotland emerging | Medium term (2-4 years) |

| Government-led housing initiatives and planning reforms | +0.9% | National, high-demand areas | Long term (≥4 years) |

| E-commerce and nearshoring driving industrial and warehouse demand | +0.8% | Logistics hubs | Medium term (2-4 years) |

| Urban regeneration and mixed-use developments | +0.6% | London, Manchester, Birmingham | Long term (≥4 years) |

| Sustainability mandates steering capital toward green assets | +0.5% | National, London focus | Medium term (2-4 years) |

| Stable legal and financial frameworks | +0.4% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Strong Institutional Capital Inflows Transform Build-to-Rent Dynamics

Build-to-rent attracted USD 1.5 billion during Q2 2024, 77% of which targeted single-family housing. Nest, Legal & General, and PGGM committed USD 1.25 billion to net-zero schemes, adding scale to a pipeline of 115,000 completed homes. Median letting times fell to 24 days, signaling undersupply. Blackstone’s USD 925 million partnership with Vistry confirms sustained appetite, especially in the south-east.

Government Planning Reforms Accelerate Housing Delivery Pipeline

The Levelling Up and Regeneration Act 2023 introduced commencement notices and longer enforcement periods, while a brownfield presumption could yield 11,500 London homes annually. More than 100 new-town proposals, each topping 10,000 dwellings, await approval, and National Development Management Policies aim to simplify infrastructure funding. Taylor Wimpey plans up to 10,000 completions in 2024, citing faster approvals.

E-commerce Expansion Drives Logistics Real Estate Demand

Blackstone’s USD 250 million purchase of 18 last-mile assets highlights conviction in logistics. Warehouse rents rose 1.1% in Q1 2025, and 6.3 million sq ft was leased despite lower large-unit take-up. Limited new starts—down 57%—tighten supply, supporting prime rental growth near 4% in 2025. Logistics drew USD 10.25 billion of investment in 2024, eclipsing offices for the first time.

Urban Regeneration Projects Redefine City-Center Value Propositions

Birmingham’s USD 2.38 billion Smithfield scheme will deliver 3,000 homes plus offices and retail over 15 years. Canary Wharf will convert the former HSBC tower at a USD 500 million–1 billion cost to a mixed-use asset. Manchester’s Viadux 2, supported by USD 1.18 billion in housing loans, illustrates growing vertical residential supply.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising interest rates curbing affordability | -0.8% | National, first-time buyers | Short term (≤2 years) |

| Planning delays prolonging development pipelines | -0.6% | England, London acute | Medium term (2-4 years) |

| Construction inflation and material shortages | -0.5% | National | Short term (≤2 years) |

| Post-Brexit policy uncertainty impacting investor confidence | -0.3% | National, EU investors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Interest-Rate Volatility Constrains Mortgage Accessibility

The Bank of England base rate at 4.5% keeps two-year fixed mortgages near 5.0%, still above 2023 peaks. Buy-to-let lending is projected to shrink to USD 11.3 billion in 2025, and first-time buyers form only 27% of private sales. UK Finance, however, expects overall lending to reach USD 325 billion in 2025, signaling a gradual recovery[2]Bank of England, “Monetary Policy Report – February 2025,” Bank of England, bankofengland.co.uk.

Construction Cost Inflation Pressures Development Margins

In 2024, 4,208 construction firms became insolvent, reflecting cash-flow stress and higher input costs. Brexit-related labor gaps and safety-compliance levies add to expense, yet 48% of industry leaders anticipate output growth in 2025. The government’s USD 969 billion infrastructure pipeline and Blackstone’s USD 12.5 billion AI data-center plan underscore continued project flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Residential Dominance Drives Market Expansion

Residential accounted for a 79.5% share of the United Kingdom real estate market in 2024, underpinning overall growth. The segment benefits from a 4.81% forecast CAGR, propelled by a 1.5 million-home pledge and mandatory 370,000-unit annual targets. The United Kingdom real estate market size for residential assets is set to widen as apartments deliver density in urban cores while single-family homes attract families to commuter belts. Build-to-rent stock adds scale and offers investors stable yields.

Logistics leads commercial sub-sectors as e-commerce penetration rises, whereas offices face hybrid-work adjustments with secondary-grade space recording a 34.2% drop in take-up. Retail warehouses outperform high-street units with expected 8.9% returns in 2025, and industrial vacancy remains manageable at 7.6%. Developers such as Berkeley pivot toward rental assets, illustrating a capital pivot within the United Kingdom real estate industry.

By Business Model: Sales Transactions Lead Despite Rental Growth

Sales transactions held 65.2% of the United Kingdom real estate market share in 2024 and carry the highest 4.93% CAGR outlook as mortgage accessibility improves. Barratt’s 36.7% lift in reservation rates after integrating Redrow signals rising consumer confidence. Government incentives for first-time buyers and a cultural bias toward ownership sustain demand.

Rental transactions continue to institutionalize through large-scale build-to-rent vehicles. Regulatory changes, such as the forthcoming Renters’ Rights Bill, favor professional landlords by adding tenant protections. The United Kingdom real estate market size attributed to rentals should expand as global investors form joint ventures exceeding USD 875 million to acquire multi-let industrial and residential assets[3]UK Finance, “Mortgage Market Forecasts 2025,” UK Finance, ukfinance.org.uk.

By End-user: Individual Households Drive Demand Fundamentals

Individuals and households comprised 58.2% of the UK real estate market in 2024 and are forecast to grow at a 5.07% CAGR, the fastest among end-users. Lower fixed-rate mortgages and a 1.3 million-household social-housing waiting list intensify demand. The United Kingdom real estate market continues to draw younger families, reinforcing steady absorption in both for-sale and for-rent segments.

Corporate occupiers temper office demand but boost logistics take-up amid supply-chain re-design. Government and institutional actors shape pipeline direction through planning policies and land disposals. International buyers, including Norway’s sovereign fund, invested USD 0.71 billion for a Covent Garden stake, showing a long-term commitment to prime assets.

Geography Analysis

England generated 71.2% of 2024 revenue, equal to roughly USD 500.1 billion of the United Kingdom's real estate market size. London anchors international capital inflows, yet a sharp supply imbalance—8,450 housing starts against an 80,000-unit target—tightens affordability. Brownfield policies aim to add 11,500 London homes each year, while Birmingham’s USD 2.38 billion Smithfield and Manchester’s tower pipeline reflect growth outside the capital. Retail returns in key English cities outpace offices, which adapt to hybrid occupancy.

Scotland is the fastest-growing geography with a projected 5.35% CAGR to 2030. Positive price expectations returned in early 2025, and rental demand exceeds supply, driving rent inflation. Lower price-to-earnings ratios relative to England appeal to both domestic and foreign investors. Institutional funds target build-to-rent in Glasgow and Edinburgh, leveraging favorable land pricing and supportive planning frameworks[4]Royal Institution of Chartered Surveyors, “UK Residential Market Survey: April 2025,” RICS, rics.org.

Wales and Northern Ireland contribute smaller shares but benefit from regeneration initiatives and unique cross-border dynamics. Proximity to English economic hubs supports Welsh residential builds, while Northern Ireland leverages distinct legal frameworks to attract logistics investors. Both regions stand to gain from national housing targets and infrastructure spending, broadening the footprint of the United Kingdom's real estate market.

Competitive Landscape

The UK real estate market is moderately concentrated. Barratt’s USD 3.13 billion acquisition of Redrow creates capacity for 23,000 annual units and demonstrates scale-seeking behavior. The Competition and Markets Authority examines information-sharing among builders, but current evidence points to intense rivalry rather than dominance. Developers with faster planning expertise and balance-sheet strength capture market share in the United Kingdom real estate market.

Strategic pivots focus on asset-light rental models and technology. Berkeley’s “2035” plan earmarks free cash flow for rental platforms, and Persimmon aligns new-build designs with planning reforms. AI solutions such as JLL’s “Hank” optimize energy use, while the government’s “Extract” tool is set to digitize planning documents by 2026, reducing approval cycles. Data-driven efficiencies create competitive advantage across the United Kingdom real estate industry.

International capital deepens competition. Blackstone added USD 250 million of last-mile warehouses and partners with domestic builders for build-to-rent delivery. Legal & General exited CALA for USD 1.69 billion to refocus on core annuity-backed real-estate strategies, and SEGRO’s USD 0.69 billion bid for Tritax EuroBox strengthens its pan-European logistics network. Players that blend domestic insight with global funding secure a foothold in high-growth niches of the United Kingdom real estate market.

United Kingdom Real Estate Industry Leaders

Barratt Redrow plc

Taylor Wimpey plc.

Persimmon plc.

Berkeley Group

The British Land Company PLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Australia’s Macquarie Group acquired stakes in several UK airports, signaling confidence in transportation-linked real estate.

- June 2025: The government launched the “Extract” AI tool to digitize planning documents, with nationwide rollout by Spring 2026 Prime Minister's Office.

- March 2025: Norway’s sovereign wealth fund invested USD 0.71 billion for a 25% interest in Covent Garden, valuing the asset at USD 3.38 billion.

- March 2025: The Commonhold White Paper positioned commonhold as the default tenure for new flats, with draft legislation expected in 2025 Ministry of Housing, Communities & Local Government.

United Kingdom Real Estate Market Report Scope

By Property Type

| Residential | Apartments & Condominiums |

| Villas & Landed Houses | |

| Commercial | Office |

| Retail | |

| Logistics | |

| Others (industrial real estate, hospitality real estate, etc.)` |

By Business Model

| Sales |

| Rental |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Country

| England | London |

| Rest of England | |

| Scotland | |

| Wales | |

| Northern Ireland |

| By Property Type | Residential | Apartments & Condominiums |

| Villas & Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Logistics | ||

| Others (industrial real estate, hospitality real estate, etc.)` | ||

| By Business Model | Sales | |

| Rental | ||

| By End-user | Individuals / Households | |

| Corporates & SMEs | ||

| Others | ||

| By Country | England | London |

| Rest of England | ||

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the United Kingdom real estate market?

The market is valued at USD 732.24 billion in 2025 and is projected to reach USD 901.81 billion by 2030.

Which property type holds the largest share?

Residential assets account for 79.5% of market revenue in 2024, making them the dominant property type.

Why is Scotland the fastest-growing region?

Scotland offers lower price-to-earnings ratios, improving affordability, and has a forecast 5.35% CAGR through 2030, attracting both domestic and foreign investors.

How are planning reforms impacting supply?

Mandatory commencement notices, brownfield presumption, and new-town initiatives aim to streamline approvals and add significant residential capacity nationwide.

What role does institutional capital play in rentals?

Build-to-rent projects secured USD 1.5 billion in Q2 2024, indicating strong appetite for professionally managed rental housing and stable long-term yields.

How is technology influencing the sector?

AI tools such as the government’s “Extract” solution and JLL’s “Hank” enhance planning efficiency and building energy performance, providing competitive advantages to early adopters.

Page last updated on: