Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

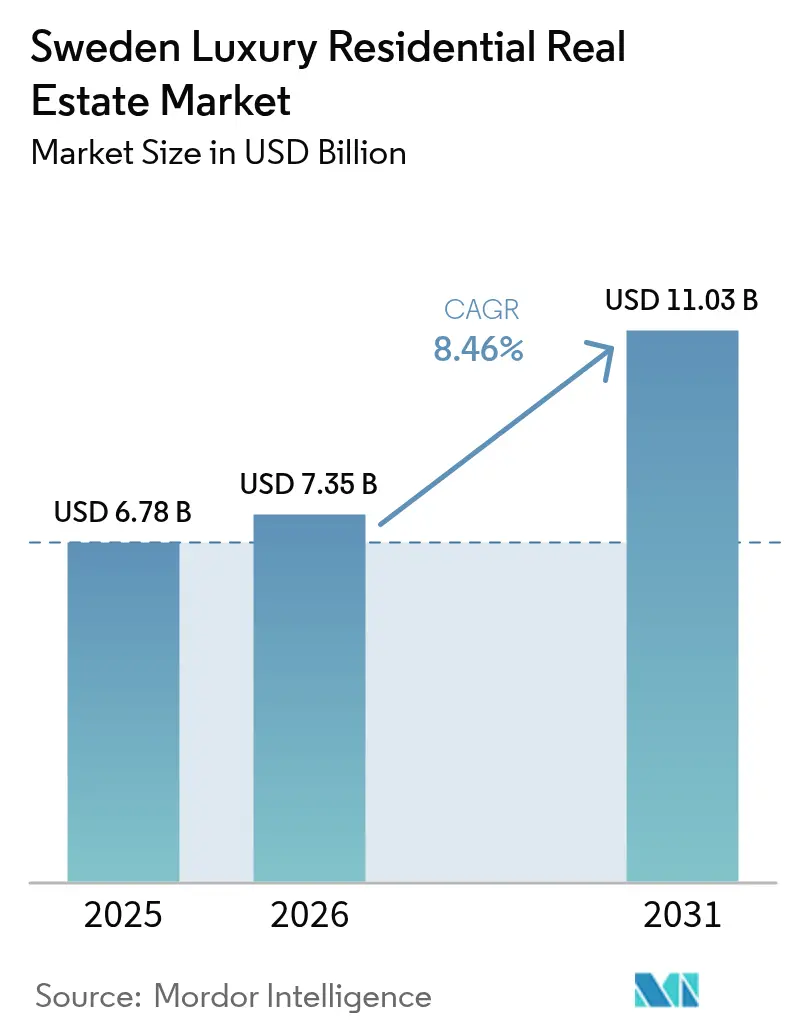

| Base Year Market Size (2025) | USD 6.78 Billion |

| Market Size (2026) | USD 7.35 Billion |

| Market Size (2031) | USD 11.03 Billion |

| Growth Rate (2026 - 2031) | 8.46% CAGR |

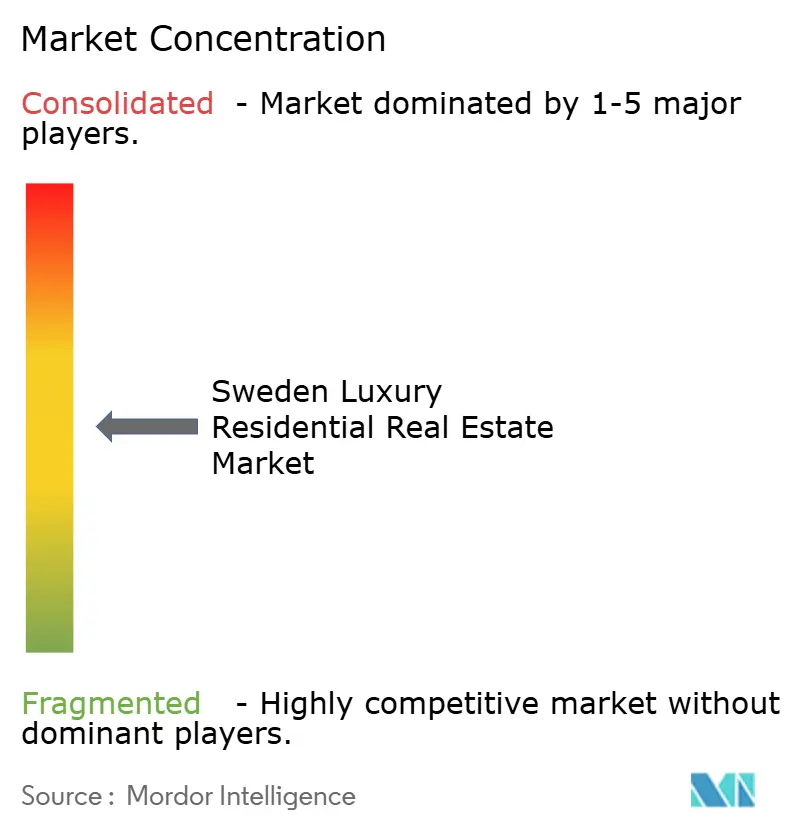

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Sweden luxury residential real estate market size was valued at USD 6.78 billion in 2025 and estimated to grow from USD 7.35 billion in 2026 to reach USD 11.03 billion by 2031, at a CAGR of 8.46% during the forecast period (2026-2031). The upswing mirrors robust inflows from ultra-high-net-worth (UHNW) buyers who view prime Swedish homes as a safe-haven hedge and a krona-discounted store of value. Exchange-rate advantages, accommodative monetary policy, and a transparent legal framework have collectively pushed demand beyond the pace at which new stock can be delivered. Developers continue to face zoning bottlenecks, yet institutional investors deploy fresh capital into income-generating rental formats to capture predictable yields while domestic households preserve wealth through direct ownership. Tight supply, deepening digitalization, and rising wellness expectations provide fertile ground for price appreciation and product innovation in the Sweden luxury residential real estate market

Key Report Takeaways

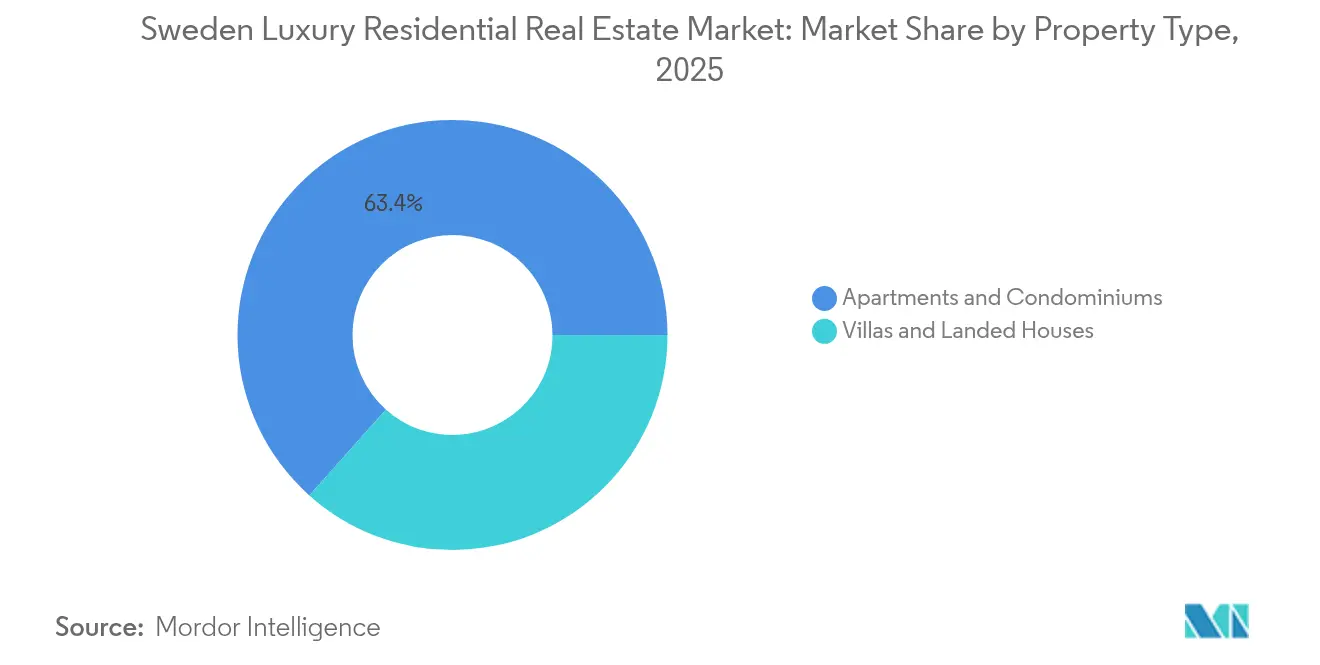

- By property type, apartments and condominiums led with 63.40% of the Sweden luxury residential real estate market revenue share in 2025. The Sweden luxury residential real estate market for villas and landed houses is projected to expand at an 8.72% CAGR between 2026-2031.

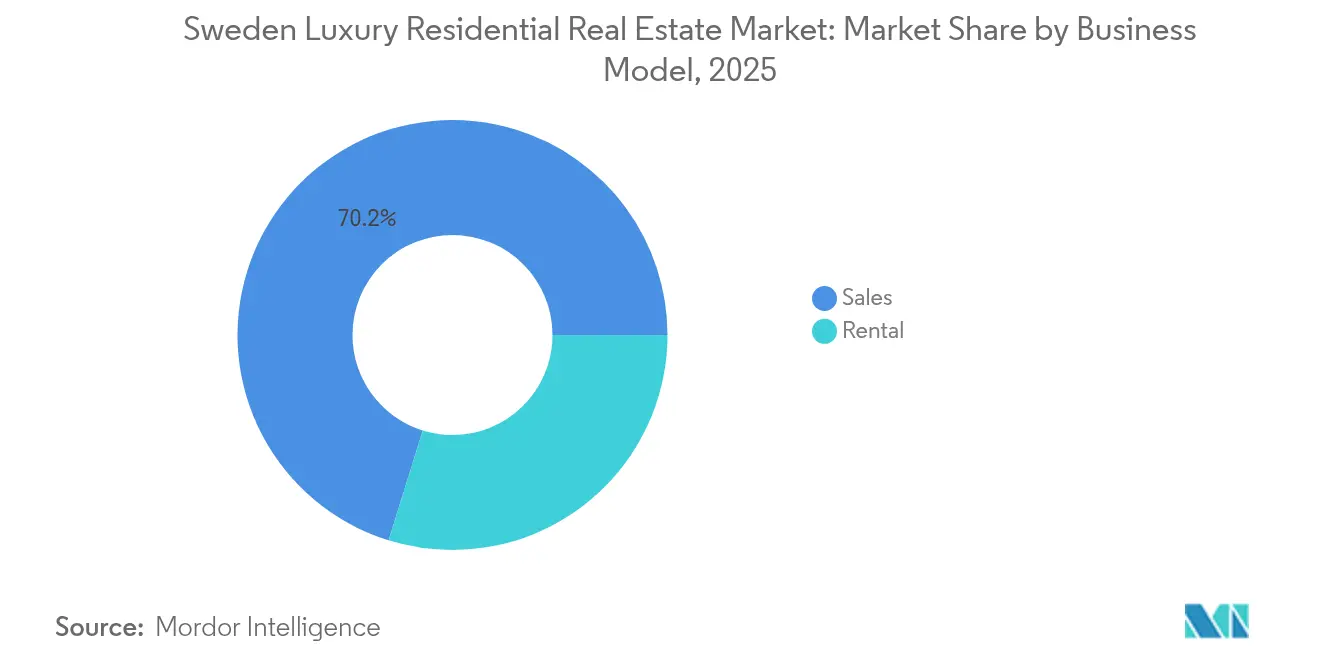

- By business model, sales transactions held 70.20% of the Sweden luxury residential real estate market share in 2025. The Sweden luxury residential real estate market for rentals is advancing at a 9.35% CAGR between 2026-2031.

- By mode of sale, secondary transactions accounted for 58.30% of the Sweden luxury residential real estate market size in 2025. The Sweden luxury residential real estate market for new-build activity is projected to grow at 8.93% CAGR between 2026-2031.

- By geography, Stockholm commanded 45.60% the Sweden luxury residential real estate market's national value in 2025. The Sweden luxury residential real estate market for Malmö is the fastest-growing city at 9.58% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust UHNW inflows & Sweden's safe-haven appeal | +2.1% | Stockholm, Gothenburg | Long term (≥ 4 years) |

| Negative / low real interest rates fueling hard-asset allocation | +1.8% | Nationwide, concentrated in metropolitan areas | Medium term (2-4 years) |

| Second-home demand from EU & UK buyers seeking krona discount | +1.2% | Coastal regions, archipelago, ski resorts | Short term (≤ 2 years) |

| Tokenized property platforms enabling crypto-wealth deployment | +0.9% | Stockholm and Gothenburg tech corridors | Medium term (2-4 years) |

| Wellness-centric “healthy homes” commanding premiums | +0.7% | Urban cores and high-end suburban projects | Long term (≥ 4 years) |

| Stockholm's tech-talent boom boosting prime residential demand | +0.6% | Greater Stockholm | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust UHNW Inflows & Sweden's Safe-Haven Appeal

Sweden’s neutral foreign policy, rock-solid legal institutions, and AAA credit rating keep drawing UHNW families that want to shift capital away from volatile financial assets. Foreign ownership of second homes jumped 6.3% in 2024, and purchases concentrated on Stockholm’s archipelago islands and Gothenburg’s waterfront, where trophy assets trade almost entirely in cash. Low property taxes and no foreign-buyer restrictions make entry frictionless, turning the Sweden luxury residential real estate market into a preferred diversification play. This unlevered capital inflow cushions price cycles, lifts liquidity in the top quartile, and raises the bar for local bidders. The resulting depth of global demand underpins long-run appreciation prospects, even when domestic cycles soften.

Negative/Low Real Interest Rates Fueling Hard-Asset Allocation

The Riksbank trimmed its policy rate from 4.0% to 3.75% and signaled more cuts, keeping real rates negative once house-price inflation is factored in. Affluent Swedes hold financial assets worth SEK 16 trillion (USD 1.5 trillion), and roughly 79% of household borrowing already flows into housing. Cheap leverage allows domestic buyers to scale up, while foreign investors exploit both the rate spread and krona weakness to lock in superior yields. The stance strengthens asset valuations and absorbs supply faster than it can be replenished, thereby nurturing the Sweden luxury residential real estate market’s compound growth.

Second-Home Demand from EU & UK Buyers Seeking Krona Discount

The krona has fallen 13% against the euro since 2022, creating a window for European and British buyers to secure Scandinavian lifestyle assets at an implicit discount. Many cash-rich households dissatisfied with post-Brexit UK housing prospects switched sights to Sweden’s coast and ski territories, where sticker prices remain below historic peaks. Currency-arbitrage purchases also spill into the short-let segment, supplying high-yield inventory to Sweden’s expanding tourism pipeline. This cross-border appetite injects liquidity during periods of subdued domestic turnover and stabilizes high-end prices in the Sweden luxury residential real estate market.

Tokenized Property Platforms Enabling Crypto-Wealth Deployment

Stockholm’s fintech scene incubates blockchain venues that fractionalize luxury homes and settle in cryptocurrency. Early-stage platforms target prime districts where rental yields and liquidity justify tokenized structures, opening segments previously accessible only to institutions. Progressive regulators and cutting-edge digital infrastructure make Sweden one of Europe’s easiest venues for compliant tokenization. As crypto-wealth seeks regulated bricks-and-mortar exposure, token deals are expected to grow in share, add transparency, and accelerate closing times across the Sweden luxury residential real estate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce developable land & tight zoning in core cities | -1.4% | Stockholm, Gothenburg, Malmö urban cores | Long term (≥ 4 years) |

| Stricter energy-efficiency retrofit capex for heritage stock | -0.8% | Historic districts nationwide | Medium term (2-4 years) |

| Climate-risk-driven insurance spikes on coastal assets | -0.6% | Archipelago and other waterfront zones | Long term (≥ 4 years) |

| Supply-side squeeze from construction-sector bankruptcies | -0.5% | Nationwide, acute in major metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Developable Land & Tight Zoning in Core Cities

Geographic constraints and heritage-heavy districts cap the volume of fresh luxury housing that can realistically be built in Sweden’s top three cities. Planning approvals require lengthy consultation, and minimum lot sizes or building-height limits prevent density upgrades. Supply scarcity entrenches resale premiums, yet it also suppresses transaction velocity and sidelines buyers priced out of mature enclaves[1]Karin Wanngård, “Detaljplan Statistics 2025,” Stockholm Municipality, start.stockholm. The net effect is a structural drag on overall absorption and the long-run expansion of the Sweden luxury residential real estate market.

Stricter Energy-Efficiency Retrofit Costs for Heritage Stock

Sweden’s climate strategy obliges owners of pre-2000 buildings to deploy extensive insulation, ventilation, and renewable upgrades, especially in landmark areas. Retrofitting protected façades can add 15-25% to acquisition budgets, deterring some cross-border buyers who prefer turnkey efficiency. Compliance elevates capex and prolongs renovation cycles, leveling down the CAGR trajectory[2]Anders Sjelvgren, “Energy Efficiency Standards for Existing Buildings 2025,” Boverket, boverket.se. Yet assets that successfully combine heritage charm with low operating loads often achieve meaningful price premiums, offsetting part of the initial restraint in the Sweden luxury residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments, Anchor Urban Luxury Demand

Apartments and condominiums captured a 63.40% slice of 2025 turnover as global investors favor maintenance-light, centrally located assets with concierge services. Secondary apartments in Östermalm, Södermalm, and Vasastan trade quickly, supported by liquid resale channels and robust furnished-rental yields. Developers escalate amenity packages to differentiate new inventory, bundling fitness studios, shared rooftop gardens, and EV-ready parking into mid-rise designs. Foreign buyers like the instant usability and straightforward governance of Swedish condominium associations, translating into sustained demand even when credit conditions tighten.Villas and landed homes, while smaller in value terms, chart the fastest growth at 8.72% CAGR as privacy-seeking executives and cash-rich EU buyers pursue coastal and archipelago retreats. Large land plots around Lidingö, Djursholm, and Saltsjöbaden realize above-trend premiums owing to zoning limits that keep new supply muted. The Sweden luxury residential real estate market share for villas could edge toward 39.50% by 2031 if construction capacity recovers. Upsizing families target hybrid working layouts, biophilic design, and garden space, while high-net-worth foreigners treat waterfront estates as long-term capital stores and seasonal leisure bases.

By Business Model: Ownership Prevails but Rentals Accelerate

Sales still dominate with 70.20% of market activity as UHNW buyers lean into direct ownership for wealth preservation and lifestyle certainty. Cash continues to displace leverage at the top tier, aided by krona-linked discounts and thin transaction-cost friction. Brokers report a surge in off-market deals, signaling deeper liquidity and heightened privacy in the Sweden luxury residential real estate market for sales transactions. Developers focus on turnkey finishes to limit buyer-side renovation exposure and accelerate closes within a competitive pipeline.Rental formats, however, post a 9.35% CAGR thanks to institutional capital chasing predictable cash flows. Build-to-rent (BTR) campuses around emerging sub-markets such as Flemingsberg and Hagastaden absorb tech-sector talent and corporate expatriates, offering flex tenures with hotel-grade services. Tokenization and co-living hybrids further expand access for younger professionals who prize mobility over homeownership. Luxury landlords attain premium gross yields in a city with stringent rent control on conventional stock, supporting a solid risk-adjusted return stack in the Sweden luxury residential real estate market.

By Mode of Sale: Secondary Assets Hold the Lead

Resale homes represented 58.30% of 2025 deal flow as historically significant apartments and villas change hands within ultra-affluent circles. These addresses hold irreplicable waterfront or heritage footprints, and scarcity inflates price per square foot. The Sweden luxury residential real estate market share tied to secondary stock should soften marginally yet remain dominant, because zoning and environmental impact assessments limit the pipeline of new projects. High-resolution virtual tours and data-rich reporting have shortened the marketing cycle, enabling global bidders to commit without extensive site visits.Primary, or new-build, inventory is projected to grow at 8.93% CAGR through 2031, lifted by developers who embed wellness technology, ESG credentials, and smart-home platforms from inception. Miljöbyggnad Silver and higher certifications are becoming baseline, and buyers pay a premium for on-site solar, grey-water recycling, and passive-house envelopes. Bankruptcies in the construction sector are slowing the initiation of new projects, causing Sweden's luxury residential real estate market for newly built homes to remain constrained until labor and material constraints are resolved.

Geography Analysis

Stockholm anchors national luxury demand with 45.60% of 2025 value. The city fuses financial services scale with a thriving startup ecosystem that minted five unicorns in 2024 alone, enriching a new cadre of cash-opted buyers. Prime islands such as Djurgården, Skeppsholmen, and Fjäderholmarna fetch record prices as trophy mansions become increasingly rare. On the rental side, executive relocation packages underpin double-digit annual growth for high-spec flats, a trend that stabilizes income for landlords within the Sweden luxury residential real estate market.

Malmö logs the fastest growth at a 9.58% CAGR, propelled by cross-border mobility across the Öresund Bridge that draws Danish and continental European money. Thriving life-science clusters in Medicon Village and the Västra Hamnen eco-district embed ESG DNA into new luxury stock that aligns with EU Taxonomy rules. Waterfront penthouses with geothermal heating systems regularly clear above USD 1,200 per square foot, narrowing the historic price gap with Stockholm. Improved rail connectivity will further weave Malmö into pan-Nordic executive itineraries, extending the catchment for the Sweden luxury residential real estate market beyond domestic demand.

Gothenburg and Uppsala play complementary roles. In Gothenburg, C-suite executives from Volvo Group, Northvolt, and SKF find a unique blend of port-city commerce and archipelago leisure. Submarkets such as Änggården and Hovås enjoy stability, as buyers seek a harmonious balance between city access and nature. Uppsala’s luxury sector leans into cultural charm and academic gravitas anchored by a 500-year-old university. Renovated 19th-century townhouses within walking distance of biotech hubs trade briskly, appealing to professors and global R&D executives. Both cities broaden geographic participation and add diversification pathways within the Sweden luxury residential real estate market.

Competitive Landscape

Fragmentation remains the hallmark of Sweden's luxury residential real estate market competitiveness. International franchises such as Sotheby’s International Realty, Christie’s International Real Estate, and Engel & Völkers devote resources to Stockholm and coastal trophy niches, but none surpass a double-digit national share. Swedish boutiques like Fantastic Frank, ESNY and Bjurfors Premium exploit hyper-local data, Scandinavian design aesthetics and curated digital storytelling to capture clientele that values discretion. Technology serves as the main battlefield: virtual-reality walk-throughs, blockchain escrow, AI-assisted valuation engines, and white-label tokenization solutions differentiate brokers in a crowded field.

Developers integrate vertical services, spinning up in-house brokerage and asset-management arms to retain end-to-end control over brand experience. Institutional investors break into the sales space via branded-residence concepts and long-lease strata, while prop-tech start-ups advertise instantaneous purchase offers or co-investment clubs to younger millionaires. Partnerships escalate; JLL’s cross-border advisory, EQT’s BTR roll-out, and Boverket’s permit streamlining each lower friction in capital deployment or approvals, thereby raising the sophistication ceiling in the Sweden luxury residential real estate market.

Barriers to scale persist. Zoning heterogeneity, linguistic nuance in contracts, and hyper-local buyer cultures impede the network benefits that usually crown a single national champion. Consequently, the top five intermediaries still control well under 35% of transaction value. The situation keeps fee margins healthy for specialized advisers while incentivizing continual innovation in client acquisition and retention. Ecosystem participants who blend Scandinavian authenticity with global reach stand to expand their share fastest in the Sweden luxury residential real estate market.

Sweden Luxury Residential Real Estate Industry Leaders

Sotheby’s International Realty Sweden

Skeppsholmen Sotheby’s

Eklund Stockholm New York (ESNY)

Bjurfors Premium

Svensk Fastighetsförmedling Luxury

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stockholm Municipality rolled out a public-private framework that enabled 1,790 luxury property transactions in one month through fast-track approvals.

- May 2025: Boverket launched a collaboration program with international architects to standardize new building-permit regulations coming into force in December 2025.

- April 2025: JLL forged a strategic alliance with Nordic investors, raising cross-border transaction volume by 30% via shared due-diligence protocols.

- April 2025: EQT Real Estate acquired an 800-unit build-to-rent campus in Flemingsberg, Stockholm, investing EUR 150 million (USD 162 million) with Miljöbyggnad Silver certification targets.

Sweden Luxury Residential Real Estate Market Report Scope

Luxury Residential real estate refers to properties that are exclusively designed for human occupation, which provides charmed and resort life with high end amenities. Sweden Luxury Residential Real Estate Market is segmented by Type (Apartments and Condominiums, Villas and Landed Houses), and by Key Cities (Stockholm, Malmo and Other Cities). The report offers market size and forecasts for the Sweden Luxury Residential Real Estate Market in value (USD Billion) for all above segments.

By Property Type

| Apartments & Condominiums |

| Villas & Landed Houses |

By Business Model

| Sales |

| Rental |

By Mode of Sale

| Primary (New-build) |

| Secondary (Resale) |

By City

| Stockholm |

| Gothenburg |

| Malmö |

| Uppsala |

| Other Cities |

| By Property Type | Apartments & Condominiums |

| Villas & Landed Houses | |

| By Business Model | Sales |

| Rental | |

| By Mode of Sale | Primary (New-build) |

| Secondary (Resale) | |

| By City | Stockholm |

| Gothenburg | |

| Malmö | |

| Uppsala | |

| Other Cities |

Key Questions Answered in the Report

What is the current valuation of the Sweden luxury residential real estate market?

The market is valued at USD 7.35 billion in 2026 and is projected to grow to USD 11.03 billion by 2031 at an 8.46% CAGR.

Which Swedish city has the largest share of luxury residential value?

Stockholm leads with 45.60% of national turnover in 2025, reflecting its role as the country’s financial and tech center.

Are apartments or villas more popular among luxury buyers?

Apartments dominate with a 63.40% share due to urban convenience, while villas see the fastest growth at an 8.72% CAGR driven by lifestyle and privacy needs.

How are interest rates influencing luxury property demand?

Negative real interest rates and expected policy easing reduce financing costs and push both domestic and foreign investors toward hard assets like prime housing.

What role does tokenization play in Sweden’s luxury property scene?

Blockchain-based platforms are fractionalizing high-end homes, enabling cryptocurrency investors to access regulated real estate and adding liquidity to the segment.

Why is Malmö considered a high-growth luxury market?

Strong cross-border connectivity via the Öresund Bridge and sustainable waterfront development have positioned Malmö for a 9.58% CAGR through 2031.

Page last updated on: