Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

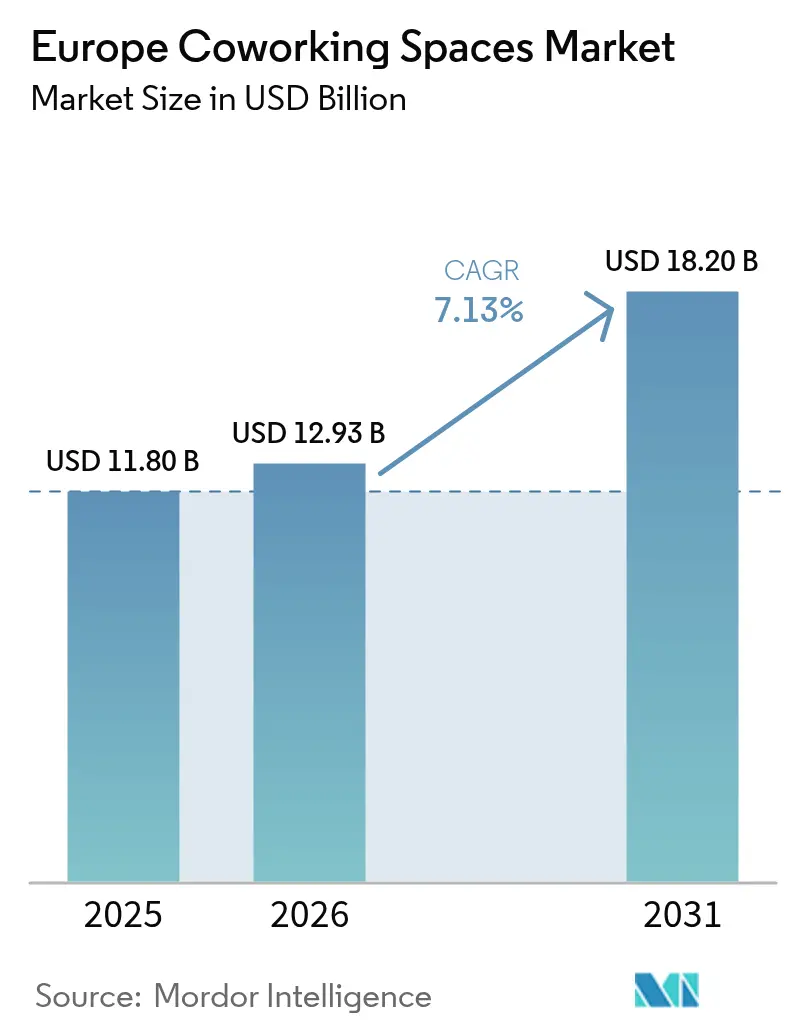

| Base Year Market Size (2025) | USD 11.80 Billion |

| Market Size (2026) | USD 12.93 Billion |

| Market Size (2031) | USD 18.20 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

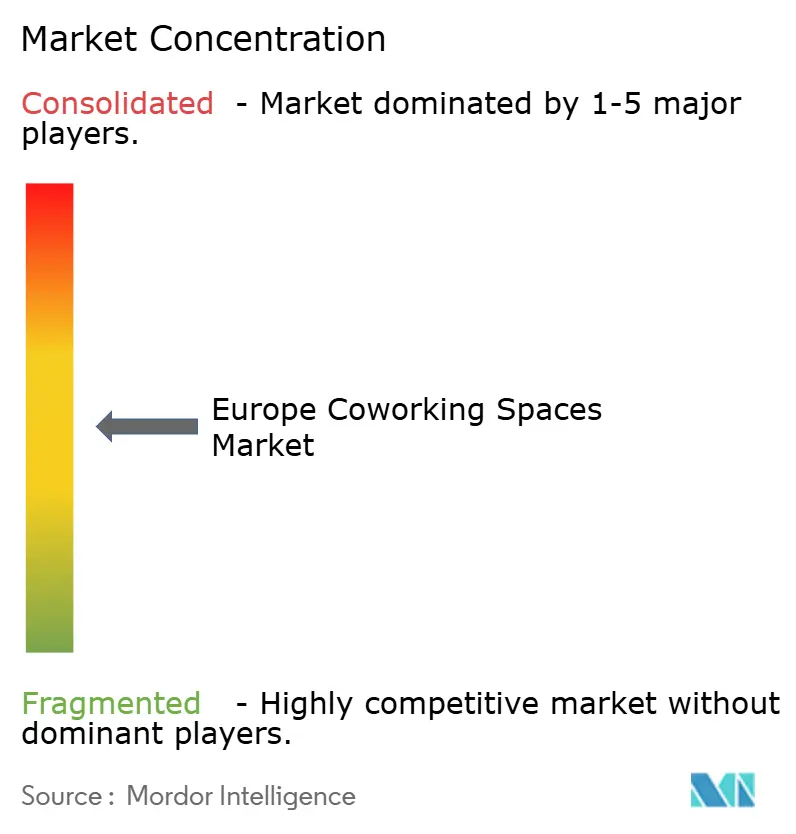

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Coworking Spaces Market Analysis by Mordor Intelligence

The Europe coworking spaces market size is projected to be USD 11.8 billion in 2025, USD 12.93 billion in 2026, and reach USD 18.2 billion by 2031, growing at a CAGR of 7.13% from 2026 to 2031. The Europe coworking spaces market is expanding because corporates are turning long leases into asset-light management agreements, startups are chasing flexible costs, and governments are steering Central Business District (CBD) revitalization subsidies toward operators that re-purpose Grade-B space. Desk-rate resilience in Tier-1 cities is fortified by AI-driven space-utilization analytics that compress vacancy and allow dynamic pricing. At the same time, hybrid-work clauses embedded in the 2025 EU labor codes have seeded structural demand for guaranteed desks within commuting distance of employees’ homes. Germany, the United Kingdom, and France collectively anchor more than half of current revenue, but Spain, Portugal, and Poland are growing faster as new digital-nomad visa schemes expand the addressable member pool.

Key Report Takeaways

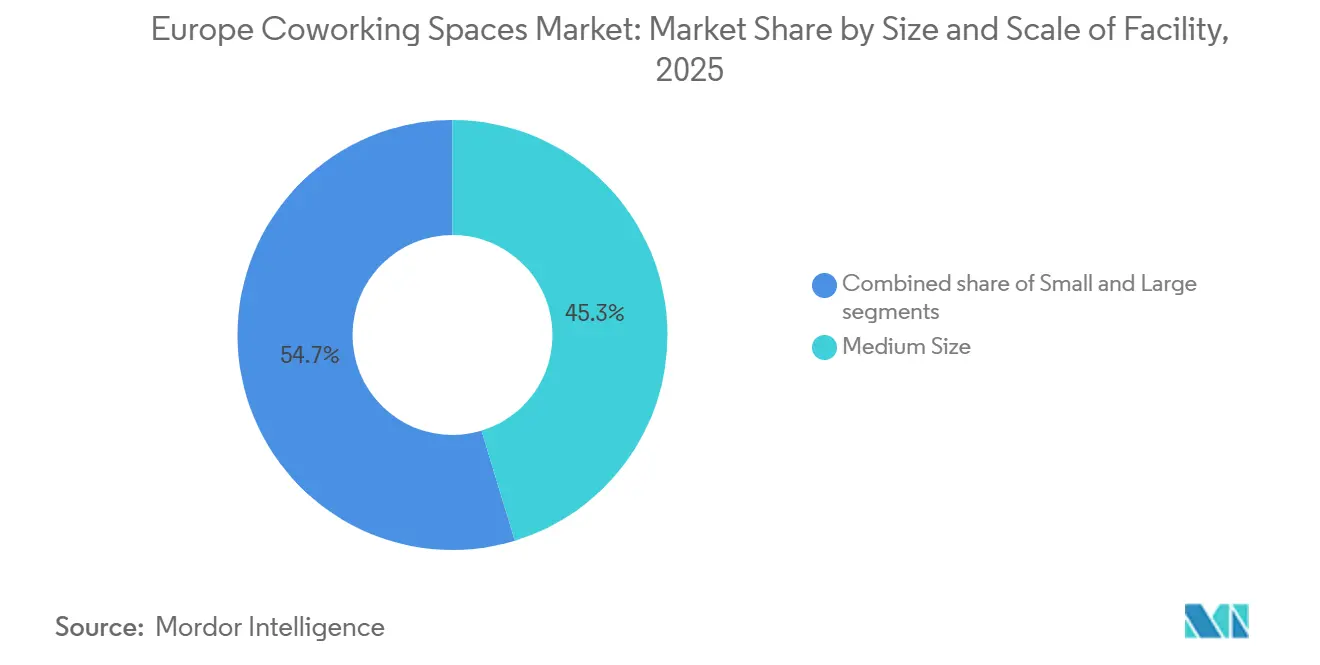

- By size & scale of facility, medium-sized hubs commanded 45.30% of the Europe coworking spaces market share in 2025, while small formats are forecast to expand at an 8.55% CAGR to 2031.

- By sector, the IT & IT-enabled services segment led with 39.10% revenue share in 2025; lifesciences coworking is projected to grow at a 9.01% CAGR through 2031.

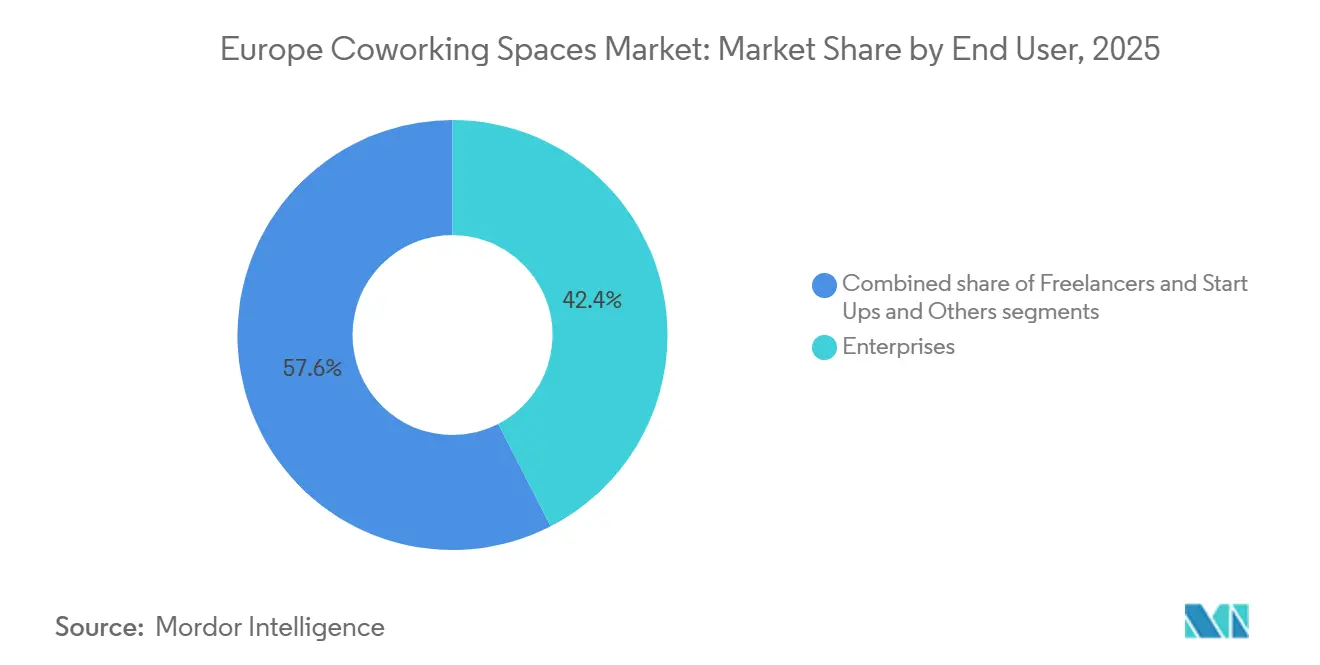

- By end user, enterprises accounted for 42.44% of the Europe coworking spaces market size in 2025, whereas start-ups and other emerging ventures are advancing at an 8.32% CAGR to 2031.

- By geography, Germany held 25.33% of 2025 revenue, and Spain is on track for an 8.77% CAGR that positions it as the fastest-growing national market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Coworking Spaces Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate real-estate portfolio optimisation via flex space | +1.8% | UK, Germany, France | Short term (≤ 2 years) |

| Acceleration of hybrid-work provisions in EU labour codes | +1.5% | EU-27 | Long term (≥ 4 years) |

| Booming startup ecosystem seeking cost-efficient, flexible leases | +1.2% | Germany, France, Spain, Netherlands | Medium term (2–4 years) |

| National & municipal incentives to revitalise post-pandemic CBDs | +0.9% | Italy, Spain, Portugal, Poland | Medium term (2–4 years) |

| AI-enabled space-utilisation analytics lifting operator margins | +0.7% | UK, Germany, Netherlands | Short term (≤ 2 years) |

| EU Digital Nomad Village funds catalysing rural cowork hubs | +0.5% | Spain, Portugal, Italy, Greece | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Real-Estate Portfolio Optimization via Flex Space

Corporates are unwinding decade-long leases in favor of revenue-share management agreements that push real-estate risk back to landlords. IWG disclosed that these agreements now dominate its pipeline, trimming lease liabilities by more than USD 1.27 billion since 2020[1]IWG plc, “Investor Relations,” iwgplc.com. In the United Kingdom, 53% of 2025 flexible-workspace deals were struck under management-agreement structures, a steep climb from 38% in 2019. As per the reports, in 2025 pan-European occupier survey shows 42% of enterprises plan to raise flex-space usage in the next 24 months, citing balance-sheet agility. The model is most attractive to banking and insurance firms that face capital adequacy ratios, and to consulting groups that need rapid city-to-city deployment. As a result, the European coworking spaces market is benefiting from an enterprise demand pipeline that locks in multi-suite commitments without bloating operator liabilities.

Acceleration of Hybrid-Work Provisions in EU Labour Codes

The right-to-disconnect and work-life balance directives enacted in 2025 compel firms to honor hybrid work requests, fueling demand for distributed offices[2]European Parliament, “Right to Disconnect Directive,” europarl.europa.eu. Germany requires employers with more than 50 staff to review such requests in four weeks, creating a predictable compliance timeline. LinkedIn’s 2025 workforce poll found that 68% of European professionals would turn down jobs that lack flexible options. Coworking operators now bake compliance guarantees, desks within 30 minutes of home, and auditable access logs into contracts, turning regulation into a competitive tool. Broader sector uptake in manufacturing back offices and hospital administration signals incremental volume that extends beyond white-collar technology users.

AI-Enabled Space-Utilisation Analytics Lifting Operator Margins

PropTech platforms such as VergeSense and Density feed live sensor data into algorithms that re-allocate desks by the hour, raising utilization by an average of 18% in pilot European deployments[3]VergeSense, “Platform Case Studies,” vergesense.com. Dynamic pricing tied to those heatmaps pushed weekend occupancy up 22% in London and Amsterdam trials. IWG applies the insights to decide which centers to expand or shutter, preventing capital misallocation. In the fiercely competitive European coworking spaces market, data-driven capacity planning is becoming table stakes, granting early adopters a structural margin edge that rivals without PropTech struggle to match.

Booming Startup Ecosystem Seeking Cost-Efficient, Flexible Leases

Startups are forecast to grow their footprint in the European coworking spaces market at an 8.32% CAGR to 2031. The European Investment Bank’s 2025 relocation survey ranked flexible workspace supply as the third-most-critical factor in site selection. Amsterdam’s Norrsken House already hosts 400 impact-tech ventures on monthly passes ranging from USD 273 to USD 1,308, bundling investor introductions with office access. Spanish operator Monday secured USD 15.3 million in 2025 to roll out 12 additional centers focused on early-stage companies. Venture capital funds increasingly sweeten term sheets with coworking credits, effectively subsidizing early occupancy and locking startups into operator ecosystems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ESG retrofit costs for ageing office stock | -1.1% | EU-27, acute in Italy & Spain | Medium term (2–4 years) |

| Surplus grey-lease inventory depressing Tier-1 desk rates | -0.8% | UK, France, Germany | Short term (≤ 2 years) |

| Interest-rate volatility constraining REIT finance windows | -0.6% | UK, Germany, Netherlands | Short term (≤ 2 years) |

| Cross-border VAT & invoicing friction for pan-EU cowork passes | -0.3% | EU-27 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ESG Retrofit Costs for Ageing Office Stock

EU directives require non-residential buildings to achieve minimum energy ratings by 2030, forcing operators of pre-1990 sites to invest USD 164-327 per m² in insulation, HVAC, and renewables. Operators bound to long leases without landlord cost-sharing face a margin squeeze because member churn risk limits their ability to pass costs through. The burden is sharpest in Italy and Spain, where 60-70% of inventory predates 1980. Premium brands such as The Office Group can amortize upgrades across higher desk rates, but budget operators risk obsolescence, muting growth in the European coworking spaces market until retrofit financing gaps close.

Surplus Grey-Lease Inventory Depressing Tier-1 Desk Rates

Corporate downsizing has pushed 1.8 million ft² of sub-lease space into London’s City and West End alone, listing 15-25% below headline rents. Fully furnished grey space offers immediate move-in, eroding price competitiveness for coworking centers that charge USD 900-1,100 per desk. Operators respond by emphasizing community programming and bundled services, yet average revenue per available room in IWG’s UK portfolio slipped 3% in H1 2025. The glut is most acute in top business districts, exerting short-term drag on the European coworking spaces market until sub-lease absorption normalizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Mid-Sized Hubs Anchor Revenue, Small Formats Capture Growth

Medium-sized hubs with 50-200 desks accounted for 45.30% of revenue in 2025, reflecting their versatility in serving both project teams and freelancers. These centers support the European coworking space market by balancing income streams, combining enterprise suites with day passes to buoy occupancy during downturns. Franchise roll-outs by IWG added hundreds of sub-200-desk locations in 2024, lowering capital requirements and accelerating suburban coverage. They also benefit from economies of scale in staffing, IT, and event space, enabling 15-20% EBITDA margins even when desk rates soften.

Small-format facilities with fewer than 50 desks are on track for an 8.55% CAGR through 2031, the fastest among size classes as neighborhood-centric operators target freelancers and micro-enterprises seeking walkable, community-oriented spaces. Brands like Second Home integrate cafés and childcare to reduce friction from commuting. Micro-format kiosks in transit hubs illustrate further downsizing of the European coworking space market, opening hourly-revenue opportunities beyond standard memberships. Landlords appreciate the low cap-ex and short lease terms, accelerating approvals in secondary towns.

By Sector: IT Dominance Meets Lifesciences Disruption

IT & IT-enabled services accounted for 39.10% of 2025 revenue, having pioneered cloud-first, distributed teams that shaped early demand. However, life sciences coworking, currently a niche with fewer than 50 dedicated facilities, will outrun every other vertical at a 9.01% CAGR to 2031. Europe's coworking space market share gains here hinge on bridges like Switzerland Innovation Park Basel’s 115,000 m² wet-lab campus, which bundles seed capital with desks. Catalonia’s Cosymbio network follows a similar shared-equipment model to cut biotech startup burn rates. Pharmaceutical corporates also use flex labs to spin out R&D skunkworks without owning real estate, deepening the sector’s pipeline.

Banking, finance, and insurance remain the second-largest coworking vertical as regulatory capital regimes reward light-footprint leases. Professional services firms tap premium centers for branded client suites across multiple jurisdictions. Cross-vertical synergies emerge when IT startups graduate into enterprise accounts or life science projects evolve from single benches to full floors, illustrating the European coworking spaces market’s ability to retain clients through growth stages.

By End User: Enterprises Lead Share, Start-Ups Drive Velocity

Enterprises accounted for 42.44% of the European coworking market in 2025, driven by hybrid policies that require consistent quality across cities. Suites customized under service-level agreements (SLAs) and ISO 27001 frameworks attract banks, insurers, and global consultancies. Operators such as Regus tier their brands, Regus for corporate suites, Spaces for creative firms, to match divergent décor expectations while maintaining back-office standardization.

Start-ups and emerging ventures, though smaller in absolute share, will lift demand at an 8.32% CAGR through 2031. Venture funds increasingly bundle workspace credits into seed rounds, anchoring fledgling teams within operator ecosystems. Scale-ups often keep a distributed footprint post-IPO, sustaining lifetime value for providers. Freelancers, while churn-prone, feed daily-pass revenue and populate community events that enhance retention for higher-value cohorts. On-demand aggregators like Deskpass commoditize this segment but also funnel incremental traffic, widening the funnel for the E coworking spaces market.

Geography Analysis

Germany captured 25.33% of Europe's coworking revenue in 2025, underpinned by 1.04 million m² of flexible stock across its seven largest metros and 570 centers run by 239 brands. Berlin alone hosts 182 centers, reflecting its status as a startup magnet and comparatively modest rents. The February 2026 acquisition of Design Offices by IWG signals accelerating consolidation as large chains snap up premium German assets to scale quickly. Germany’s 2025 labor-code revisions obligate large employers to evaluate flex-work requests within 4 weeks, turning regulatory compliance into demand for turnkey suites.

Spain stands out as the fastest-growing national market, forecast to post an 8.77% CAGR through 2031. Madrid and Barcelona have already amassed 640,000 m² of flex inventory; JLL forecasts that flexible offices could jump from 3% to 8% of total office stock by 2030. National digital-nomad visas and regional tax credits spur both coastal and inland expansion. IWG plans to scale to 500 Spanish locations using capital-light franchises, while local chain Networkia is adding 4,000 m² in Madrid during 2026.

France, Italy, and the United Kingdom each display distinct demand drivers. France hosts 26 WeWork private offices across nine Parisian buildings alongside Mitwit’s 40-center network, reflecting a two-tiered landscape of global chains and regional specialists. Italy’s Copernico leads with 13 heritage-building conversions totaling 78,000 m² and 6,000 members; WAO Milan will triple its footprint to 22,300 m² by 2026 on a revenue target of USD 5.56 million. The UK maintains 86% occupancy at USD 1,060 average monthly desk rates, but is contending with grey-lease competition that trims pricing power. Beyond the big five, Poland, the Czech Republic, Portugal, and the Netherlands leverage public subsidies, logistics-adjacent flex hubs, and rural digital-nomad programs to inject fresh supply, expanding the geographic footprint of the Europe coworking spaces market.

Competitive Landscape

The competitive landscape remains highly fragmented, with several major international operators, including IWG (Regus, Spaces), WeWork, Mindspace, The Office Group, and Industrious, coexisting alongside numerous regional and local providers. This fragmentation creates significant room for regional specialists and niche operators to expand their presence. IWG has strengthened its position through a franchise and management agreement model, enabling the company to add a large number of locations globally in 2024 without substantially increasing lease liabilities. This approach contrasts with WeWork’s traditional operator-led model, which historically involved higher lease exposure. Additionally, IWG’s acquisition of Germany-based Design Offices in February 2026, combined with the bond financing raised in 2024, highlights the company’s capacity to pursue consolidation and expand its footprint in the flexible workspace market.

Mindspace, The Office Group, and other boutique brands weaponize high-design aesthetics and member-only events to justify desk premiums 20-30% above market norms. Technology is a battleground: operators deploying VergeSense sensors and Density’s people-counting cameras report 15-20% higher occupancy, a margin gap that smaller rivals struggle to close. Cross-border VAT compliance remains a structural hurdle; even well-capitalized networks must navigate fragmented tax codes that shave up to 150 basis points off margins.

White-space opportunities abound in life sciences coworking, rural digital-nomad villages, and micro-format kiosks. Emerging disruptors, Norrsken House in Amsterdam, Cosymbio in Catalonia embed sector accelerators inside their models, trading square footage for ecosystem value that cultivates sticky memberships. As the Europe coworking spaces market matures, scale players will likely pursue bolt-on acquisitions in these niches to diversify portfolios and capture higher-growth verticals.

Europe Coworking Spaces Industry Leaders

IWG (Regus & Spaces)

WeWork

The Office Group (TOG)

Mindspace

Industrious

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: IWG acquired Design Offices, gaining premium German assets in Munich, Hamburg, and Frankfurt.

- December 2025: Norrsken Foundation opened Norrsken House Amsterdam, a 400-startup impact-tech hub with memberships from USD 273 to USD 1,308.

- March 2025: Monday raised USD 15.3 million to double its Spanish network by 12 sites, offering bundled legal, accounting, and HR services.

- January 2025: CTP’s Clubco brand added 4,000 m² in the Czech Republic and Slovakia, embedding flex offices next to logistics parks.

Europe Coworking Spaces Market Report Scope

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| IT & ITES |

| BFSI |

| Business Consulting & Professional Services |

| Other Services (Retail, Lifesciences, Energy, Legal) |

By End User

| Freelancers |

| Enterprises |

| Start-ups & Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | IT & ITES |

| BFSI | |

| Business Consulting & Professional Services | |

| Other Services (Retail, Lifesciences, Energy, Legal) | |

| By End User | Freelancers |

| Enterprises | |

| Start-ups & Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will flexible offices become within Europe by 2031?

The Europe coworking spaces market is forecast to reach USD 18.2 billion by 2031, expanding at a 7.13% CAGR from 2026.

Which country is growing fastest for coworking adoption?

Spain is projected to post an 8.77% CAGR through 2031 as Madrid and Barcelona expand flex offices to 8% of total stock.

What drives enterprise demand for flex space?

Corporates prefer management-agreement models that keep real-estate off balance sheets and support hybrid-work compliance under 2025 EU labor codes.

How are operators protecting margins?

AI-powered occupancy analytics from platforms like VergeSense and Density lift utilization by about 18%, enabling dynamic pricing and stronger EBITDA.

What threatens desk-rate stability in Tier-1 cities?

A surge in grey-lease sub-leases priced 15-25% below headline rents is pressuring coworking rates in London, Paris, and Frankfurt.

Page last updated on: