Cloud VPN Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

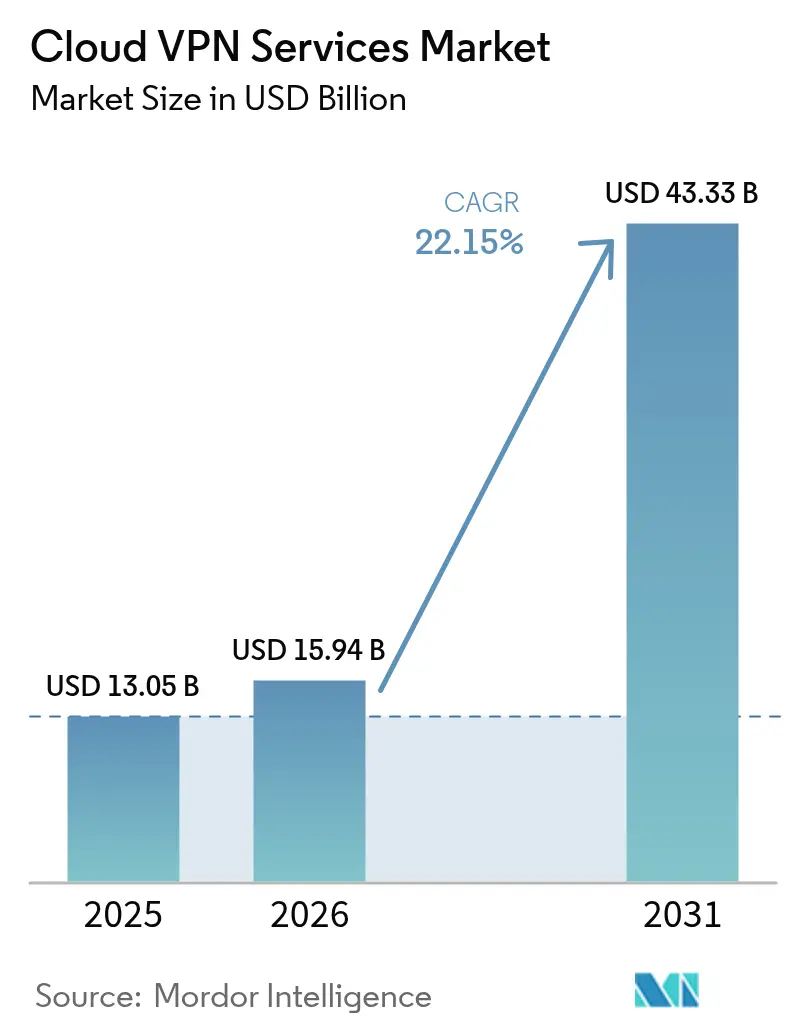

| Market Size (2026) | USD 15.94 Billion |

| Market Size (2031) | USD 43.33 Billion |

| Growth Rate (2026 - 2031) | 22.15% CAGR |

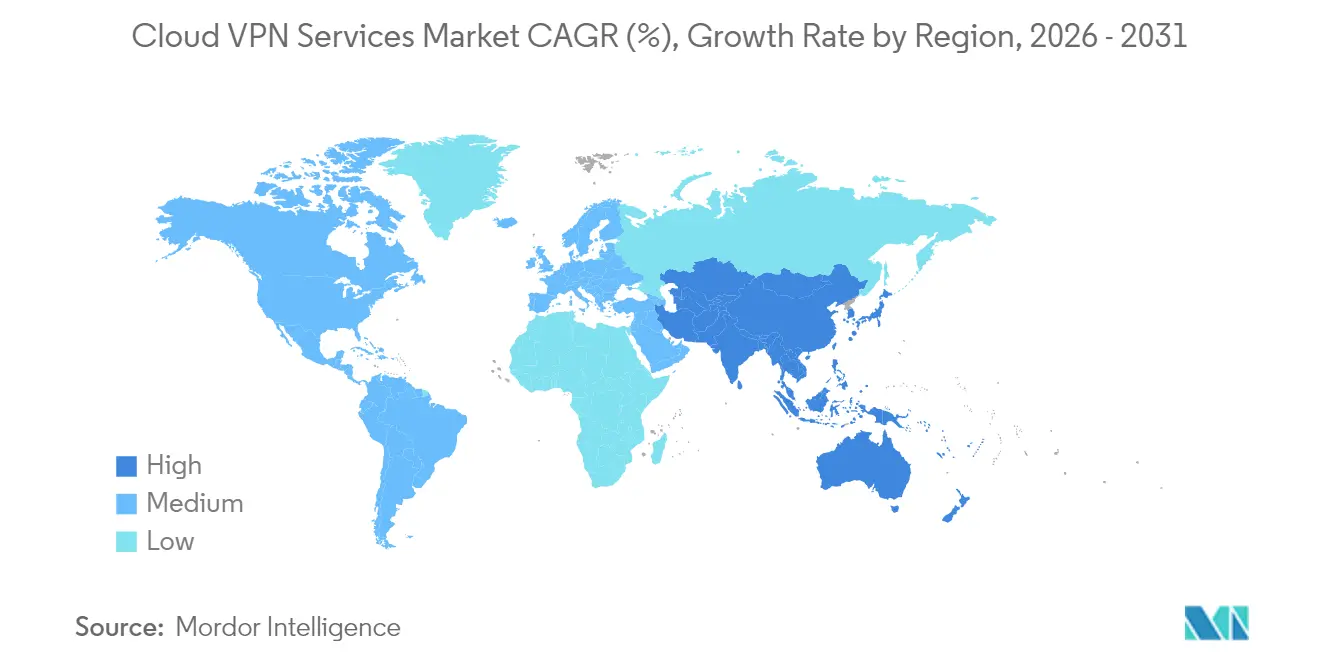

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

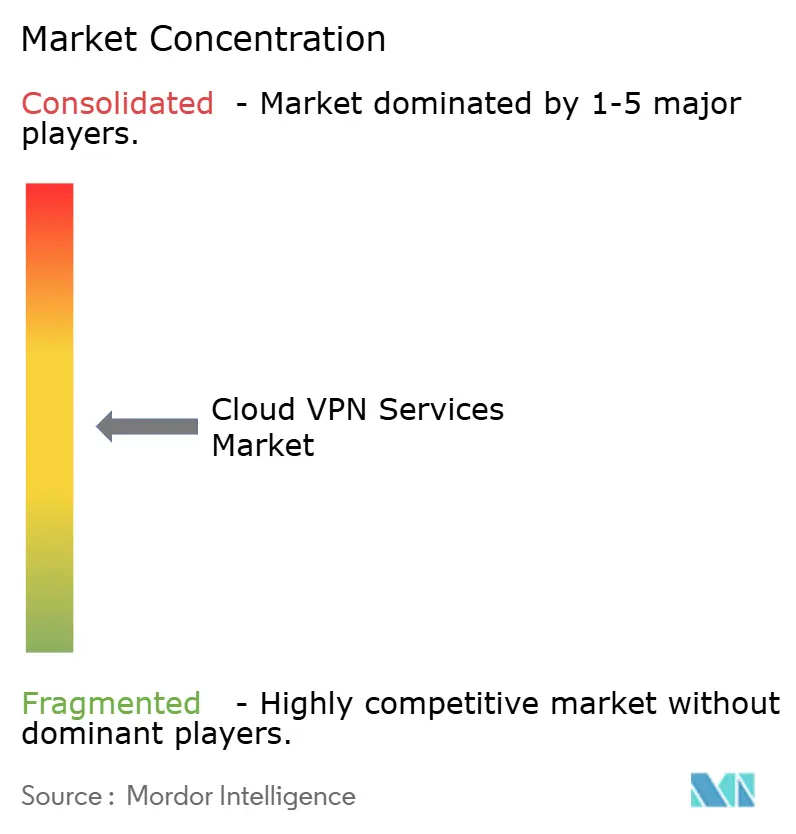

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud VPN Services Market Analysis by Mordor Intelligence

The Cloud VPN Services Market size was valued at USD 13.05 billion in 2025 and estimated to grow from USD 15.94 billion in 2026 to reach USD 43.33 billion by 2031, at a CAGR of 22.15% during the forecast period (2026-2031). The 179% growth trajectory reflects enterprise migration from perimeter-bound security to cloud-native architectures, escalating multi-cloud connectivity needs, and permanent hybrid work patterns. Demand also benefits from the rapid rollout of Secure Access Service Edge (SASE) platforms, 5G private networks for industrial IoT, and vendor bundling of VPN with unified security suites. Competitive intensity rises as legacy network vendors converge with cloud-first security specialists, while persistent skills shortages in cloud-security engineering reinforce the shift toward managed offerings. Country-level data-sovereignty mandates introduce deployment complexity yet encourage regionalized platforms that can meet compliance obligations.

Key Report Takeaways

- By component, software accounted for 62.05% revenue share in 2025, while services are projected to expand at a 24.6% CAGR through 2031.

- By deployment mode, public cloud held 44.75% of the cloud VPN services market share in 2025, whereas hybrid cloud is forecast to grow at a 23.7% CAGR to 2031.

- By enterprise size, large enterprises commanded 59.62% of the cloud VPN services market share in 2025; small and medium enterprises are advancing at a 24.1% CAGR through 2031.

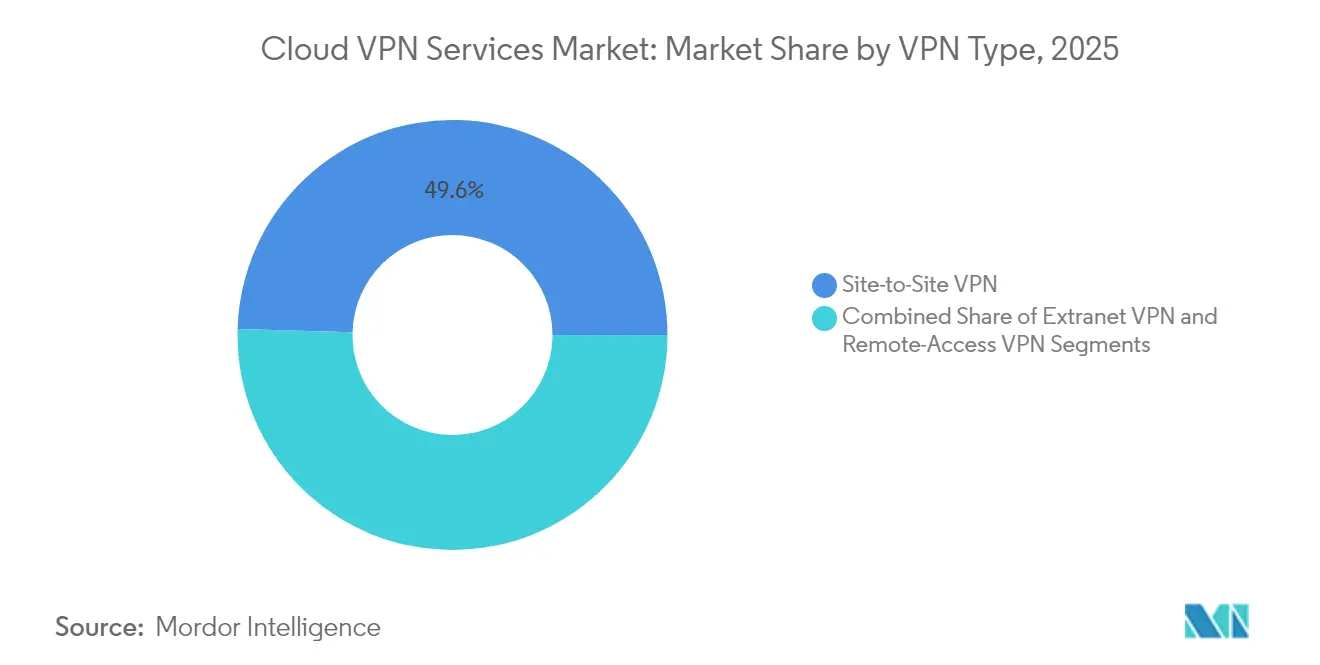

- By VPN type, site-to-site connections captured 49.55% of the cloud VPN services market size in 2025, while remote-access VPN is set to rise at a 24.9% CAGR over 2026-2031.

- By end-user industry, IT and telecommunications led with 28.35% revenue share in 2025; healthcare is the fastest-growing segment at a 23.9% CAGR through 2031.

- By geography, North America secured 34.15% revenue share in 2025, and Asia-Pacific is the fastest-growing region at a 24.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud VPN Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in multi-cloud adoption | +4.2% | North America and Europe concentrated, global spread | Medium term (2-4 years) |

| Expansion of SASE and zero-trust architectures | +5.8% | Global, early in North America, rising in APAC | Short term (≤ 2 years) |

| Work-from-anywhere labour model persists | +3.1% | North America and Europe, global relevance | Long term (≥ 4 years) |

| 5G private networks for industrial IoT | +2.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Vendor bundling of VPN with unified security suites | +1.9% | Global | Short term (≤ 2 years) |

| AI-driven dynamic routing for latency-sensitive apps | +1.5% | North America and Europe, global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Multi-Cloud Adoption

Enterprise multi-cloud strategies reshape VPN requirements as organizations look for unified connectivity across disparate clouds. Cisco reported 117% security revenue growth in Q2 FY 2025, largely tied to multi-cloud connectivity demands. Traditional site-to-site architectures struggle with dynamic cloud workloads, fueling the uptake of cloud-native solutions that spin up tunnels on demand. Salesforce gained 500% bandwidth without extra cost after adopting Prisma SD-WAN across 70 offices. [1]Palo Alto Networks, “Palo Alto Networks Reports Fiscal Second Quarter 2025 Financial Results,” investors.paloaltonetworks.com Unified SASE platforms that abstract provider differences reduce operational friction and lower vendor-lock-in risk, a priority for global enterprises that want future cloud strategy flexibility.

Expansion of SASE and Zero-Trust Architectures

Identity-centric security is displacing network-centric VPN in many enterprises. T-Mobile replaced legacy VPN with Zscaler’s Zero Trust Exchange, enabling direct application access and lower latency. [2]Zscaler, “Zscaler ThreatLabz 2025 VPN Risk Report: Over Half of Organizations Say Security and Compliance Risks Make VPNs Obsolete,” ir.zscaler.com SASE eliminates back-hauling through data centers, improves user experience, and supports least-privilege policies. CISA highlighted 22 VPN vulnerabilities in 2024, accelerating migration. [3]Cybersecurity & Infrastructure Security Agency, “Modern Approaches to Network Access Security,” ic3.gov Converged networking and security within SASE delivers operational efficiency that offsets higher per-user spend compared to appliance-based VPN.

Work-from-Anywhere Labour Model Persists

Hybrid work remains permanent, sustaining high-volume remote access demand. ManpowerGroup’s 30,000 remote staff exceeded VPN capacity, prompting a move to zero-trust alternatives. Organizations select a cloud-delivered VPN that scales elastically rather than over-provisioning on-prem hardware. Providers with global points of presence and dynamic traffic optimization gain an advantage because performance must remain stable across diverse networks and regulatory regions.

5G Private Networks for Industrial IoT

5G private networks bring ultra-low-latency connectivity to meet needs beyond conventional internet-based VPN. Vodafone’s Mobile Private Networks deliver secure dedicated channels for industrial workloads. Advantech’s private 5G solution supports smart factories with isolated secure slices. The integration of VPN inside 5G network slicing permits sector-specific isolation, particularly benefiting manufacturing and logistics, where operational technology requires both speed and security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for clientless ZTNA over VPN | -3.4% | North America and Europe lead, global adoption | Short term (≤ 2 years) |

| Country-level data-sovereignty compliance hurdles | -2.1% | APAC core, Europe and MEA follow | Medium term (2-4 years) |

| Persistent skills shortage in cloud-security engineering | -1.8% | Global shortages, acute in North America | Long term (≥ 4 years) |

| Pricing pressure from open-source alternatives | -1.2% | Global, stronger in price-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Clientless ZTNA over VPN

Zscaler’s 2025 VPN Risk Report found 92% of organizations are concerned about ransomware exposure via VPN, and 65% intend to replace VPN within a year. Clientless ZTNA provides application-specific access without network-wide exposure, reducing attack surface and device management overhead. Telit Cinterion realized a threefold ROI by migrating from Pulse Secure VPN to Prisma Access. Traditional VPN vendors must pivot to zero-trust or risk displacement.

Country-Level Data-Sovereignty Compliance Hurdles

APAC’s sovereign cloud surge compels organizations to keep data inside national borders, complicating centralized VPN architectures. Japanese regulators issued detailed guidance on cross-border sensitive data handling in 2024. Firms must deploy region-specific gateways, raising cost and operational burden while slowing rollouts in regulated sectors such as healthcare and financial services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Software Dominance

Software still underpins 62.05% of 2025 revenue as large enterprises keep granular control over policy management. Managed services, however, deliver the strongest upside at a 24.6% CAGR to 2031 as organizations contend with hiring gaps and operational complexity. The cloud VPN services market size for services is projected to widen sharply, buoyed by subscription models that bundle 24/7 monitoring, incident response, and compliance reporting. Providers showcase rapid deployment; Watercare enabled Zscaler Private Access for 800 users across 1,300 sites in half a day. The segment’s growth also links to multi-cloud sprawl, where specialized skills are necessary to optimize performance across diverse platforms.

Managed-service adoption spreads across verticals. Healthcare providers seek turnkey options due to stringent data privacy mandates, while mid-sized manufacturers rely on MSPs to secure distributed plants. Vendors invest in automation and AI-powered analytics to scale support without proportionally expanding headcount. As economies of scale strengthen, service pricing narrows relative to self-managed software licensing, improving total-cost-of-ownership for resource-constrained buyers. The services boom contributes repeatedly to overall cloud VPN services market momentum during the forecast horizon.

By Deployment Mode: Hybrid Cloud Emerges as Growth Leader

Public cloud maintains 44.75% 2025 revenue share, yet hybrid deployments grow at 23.7% CAGR because enterprises balance on-prem control with cloud scalability. The cloud VPN services market recognizes hybrid as the architectural sweet spot, enabling phased migration of legacy applications. Cisco’s private 5G overview shows how hybrid models achieve five-nines availability while keeping sensitive data on-site. Hybrid adoption is strongest in regulated industries that must maintain data residency yet require ubiquitous application access.

Unified policy orchestration across hybrid footprints is a central customer requirement. Vendors integrate centralized control planes capable of translating intent into device-neutral configurations, reducing manual errors. Hybrid strategies also assist in cost optimization, allowing workload placement based on latency, data gravity, and regulatory needs. Over time, as cloud activity outweighs on-prem workloads, hybrid may transition toward predominately public cloud, but demand for adaptive, location-agnostic VPN persists, driving continued cloud VPN services market expansion.

By Enterprise Size: SME Adoption Accelerates Despite Large Enterprise Dominance

Large enterprises captured 59.62% of 2025 revenue, underpinned by complex infrastructures and sizeable security budgets. Nonetheless, SMEs expand at a 24.1% CAGR, narrowing the penetration gap. The cloud VPN services market size in the SME brackets gains from subscription pricing and simplified onboarding that eliminates prior capex hurdles. Tailscale’s USD 160 million Series C funding underscores investor belief in zero-configuration solutions that resonate with small IT teams.

Threat escalation pushes SMEs away from basic or open-source tools toward enterprise-grade protection. Bundled suites reduce vendor management overhead, letting lean teams adopt VPN, SWG, and ZTNA in a single console. Channels such as MSPs and telcos amplify reach by embedding VPN-as-a-Service in broadband or 5G business packages. As low-touch sales models mature, SMEs’ cumulative contribution to the overall cloud VPN services market revenue will keep rising.

By VPN Type: Remote-Access Growth Challenges Site-to-Site Leadership

Site-to-site VPN remained the largest at 49.55% in 2025 for inter-office traffic, but grows modestly versus remote-access VPN’s 24.9% CAGR surge. Remote-access adoption aligns with enduring hybrid work. The cloud VPN services market size for remote-access solutions escalates as organizations roll out device-agnostic apps. WireGuard’s performance advantage over legacy protocols plays a role in upgrade cycles.

Extranet VPN retains steady demand for supplier portals and B2B exchanges, particularly in manufacturing. Future product roadmaps embed granular partner segmentation and zero-trust principles to mitigate over-privileged access. Remote-access services with dynamic split tunneling and endpoint posture checks appeal to security teams seeking tighter control without user friction. Continuous protocol innovation sustains competitive differentiation, stimulating overall cloud VPN services market innovation.

By End-user Industry: Healthcare Digitization Drives Fastest Growth

IT and Telecommunications represented 28.35% of 2025 revenue due to its cloud readiness and security investments. Healthcare grows fastest at 23.9% CAGR, propelled by telehealth expansion, electronic health record access, and strict data regulations. Zscaler Private Access showcases reduced complexity in securing clinical applications. Financial services maintain heavy usage for customer data protection, while manufacturing’s industrial IoT initiatives deepen reliance on secure connectivity.

Retail relies on VPN for distributed stores and seasonal remote staff, favoring cloud-delivered models that spin up quickly. Energy and Utilities prioritize securing operational technology networks against cyber-physical risks, driving complex segmentation demand. Government initiatives to modernize citizen services adopt a compliant VPN and zero-trust access to safeguard sensitive records. Variation across industries generates tailored requirements that vendors leverage for differentiation, reinforcing long-term cloud VPN services market diversification.

Geography Analysis

North America led with 34.15% revenue share in 2025 as early adopters invested heavily in cloud-native security. Federal zero-trust mandates and CISA guidance steer organizations toward modern access models. Large enterprises allocate significant budgets; Palo Alto Networks posted 37% Next-Generation Security ARR growth with strong regional contribution. Canada follows similar modernization paths, and cross-border trade with Mexico boosts multinational connectivity projects.

The Middle East and Africa show emerging potential. The United Arab Emirates and Saudi Arabia allocate sizable budgets for smart-city and e-government initiatives, seeking carrier-grade SASE and VPN solutions. South Africa and Nigeria experience uptake as cloud adoption spreads among enterprises. Telcos bundle VPN with fiber and 5G for SMEs, lifting penetration rates. Although current revenue contribution is modest, high growth rates translate into notable incremental demand, complementing the broader cloud VPN market expansion.lerates across the region, further enlarging overall cloud VPN services market revenue.

Europe records steady growth anchored by GDPR and cyber-resilience directives. Germany emphasizes OT security for Industry 4.0, while the United Kingdom targets financial services compliance. France advances digital-sovereignty measures that favor European cloud providers with integrated VPN offerings. Russia’s data-localization rules encourage domestic gateways but hinder global providers. Overall, regulatory complexity incentivizes flexible, policy-driven VPN designs.

The Middle East and Africa show emerging potential. The United Arab Emirates and Saudi Arabia allocate sizable budgets for smart-city and e-government initiatives, seeking carrier-grade SASE and VPN solutions. South Africa and Nigeria experience uptake as cloud adoption spreads among enterprises. Telcos bundle VPN with fiber and 5G for SMEs, lifting penetration rates. Although current revenue contribution is modest, high growth rates translate into notable incremental demand, complementing the broader cloud VPN services market expansion.

Regulatory Landscape

Cloud VPN services sit at the intersection of cybersecurity controls, cryptographic requirements, and sectoral compliance programs that increasingly specify how remote access and site connectivity are protected. In the United States, NIST SP 800-77 Revision 1 continues to anchor federal guidance for IPsec VPN security and aligns deployments with approved cryptographic algorithms as legacy algorithms are phased out under NIST cryptographic policy (for example, per the direction of NIST SP 800-131A). Separately, Defense Information Systems Agency (DISA) VPN Security Requirements Guide (STIG) V2R6 tightens operational requirements for gateways supporting DoD environments, including Always On connectivity expectations, multifactor authentication, and certificate-based controls using DoD-approved PKI.

In Europe, cybersecurity risk management obligations for digital infrastructure operators are becoming more prescriptive, shaping how cloud-delivered VPN and adjacent access services are architected and audited. ENISA technical implementation guidance for NIS2 references widely used frameworks such as ISO/IEC 27002:2022 and NIST Cybersecurity Framework 2.0, reinforcing standardized control mapping and evidence collection across member states. The European Commission also published a Cybersecurity Act review proposal on 20 January 2026, advancing debate around more consolidated EU cybersecurity certification approaches for areas such as cloud services and 5G, which can influence vendor assurance requirements for cloud connectivity stacks used in regulated industries.

Value Chain Analysis

The cloud VPN services value chain begins with foundational infrastructure and standards, then moves through software control planes and security stacks into delivery, integration, and ongoing operations. Upstream inputs include hyperscaler networking primitives (for example, AWS, Microsoft Azure, and Google Cloud native VPN constructs), global compute and bandwidth capacity for points of presence, and protocol and crypto implementations for IPsec and OpenVPN/WireGuard-based overlays. Midstream, established networking and security vendors (such as Cisco, Fortinet, and Palo Alto Networks) and cloud-native security specialists (such as Zscaler and Cloudflare) package gateway functions, policy orchestration, identity integration, logging, and performance optimization into SaaS-delivered services that are increasingly positioned alongside SASE and zero-trust access capabilities.

Downstream, distribution and monetization run through direct enterprise sales, channel-led managed services (MSPs and telcos), and cloud marketplaces where procurement, billing, and deployment are streamlined. Integration partners and enterprise networking teams connect cloud VPN to SD-WAN, identity providers, endpoint posture tooling, and SOC workflows, with managed offerings gaining traction where cloud-security engineering skills are constrained. Common bottlenecks concentrate around multicloud routing scale, configuration drift, and service resilience, where single-point-of-failure designs and limited visibility into third-party operational practices can translate into outages or compliance gaps. This raises the value of standardized reference architectures, automated policy validation, and auditable operational processes across regions and clouds.

Competitive Landscape

The landscape balances established networking giants and pure-play cloud security innovators. Cisco, Fortinet, and Palo Alto Networks embed VPN within broader SASE portfolios, leveraging extensive distribution and R&D depth. Fortinet’s Unified SASE ARR reached USD 1.12 billion with 26% growth, proving a successful migration from appliance sales to cloud subscriptions. Zscaler and Cloudflare emphasize zero-trust functionality, winning accounts that bypass traditional VPN altogether.

Emerging disruptors focus on ease of use and developer-friendly tooling. Tailscale attracts SMEs with peer-to-peer mesh networking and zero-configuration, validated by its USD 160 million funding. Open-source projects like WireGuard impose price discipline, pushing vendors to add value via analytics, compliance, and performance SLAs. Patent filings around anomaly alerting and TLS termination reveal ongoing innovation.

Strategic moves include telco partnerships: T-Mobile and Palo Alto Networks launched a managed SASE service integrating 5G slicing, aiming at enterprises and government agencies. Broadcom’s VeloSky converges fiber, cellular, and satellite links with integrated security, targeting service providers. Vendors also form sector-specific alliances, for example, healthcare-focused zero-trust bundles that address HIPAA compliance. As clients prioritize platform consolidation, the ability to provide end-to-end networking and security in a single SLA becomes a decisive factor within the cloud VPN services market.

Cloud VPN Services Industry Leaders

Cisco Systems Inc.

Microsoft Corporation

Amazon Web Services Inc.

Google LLC

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Migration from standalone VPN to cloud-delivered secure connectivity creates whitespace for providers that deliver VPN as part of consolidated SASE and security service edge offers, while keeping compatibility with entrenched enterprise tunneling patterns. A clear catalyst is the rollout of integrated platforms, including Cisco making Cisco SASE with Meraki generally available in June 2026 to unify SD-WAN sites with cloud-delivered security controls, using a packaging model aimed at buyers pursuing platform consolidation without abandoning VPN-based site connectivity immediately.

On the cloud platform side, Microsofts May 2026 public preview of summarized gateway prefixes for Azure Virtual Networks targets a known scale constraint in large hub-and-spoke environments that use Azure VPN Gateway and ExpressRoute. It creates opportunity for cloud VPN providers and managed services teams to modernize hybrid network designs with fewer route advertisements and simpler change control. Security-driven modernization also supports product and services demand around crypto agility, identity hardening, and auditability as standards bodies and regulators tighten expectations. ETSI is progressing a harmonized standard for virtual private networks (draft state in 2026), encouraging vendors to align implementations and documentation to clearer baseline requirements. In parallel, post-quantum transition work is moving from theory into deployable options: Cloudflare announced general availability of hybrid ML-KEM for IPsec tunnels in April 2026 (with noted interoperability references to Cisco IOS XR and FortiOS versions). These shifts favor providers that can deliver managed upgrades, validated configurations, and compliance-ready reporting across public, private, and hybrid deployments in regulated sectors and data-sovereignty constrained geographies.

Recent Industry Developments

- June 2026: Cisco announced the general availability of Cisco SASE with Meraki, integrating Meraki SD-WAN sites with Cisco Safe Access to apply unified cloud-delivered security policies. The release strengthens bundled secure connectivity offers that can displace standalone VPN stacks by combining networking and security controls under a single management experience.

- May 2026: Microsoft introduced a public preview of summarized gateway prefixes for Azure Virtual Networks, enabling aggregated prefix advertisement for Azure ExpressRoute and VPN Gateway connections. This targets routing scale and operational overhead in large hub-and-spoke hybrid designs where cloud VPN connectivity is constrained by route table size and change complexity.

- October 2024: Zscaler expanded its platform with Business Continuity Clouds and Private Service Edges to sustain secure access during disruptive events. The update supports enterprises that require resilient remote and site connectivity patterns with tighter control over where security inspection and private access enforcement occur.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from cloud-delivered VPN services that create encrypted connections between users, branch sites, and cloud workloads, along with the core management functions that run these VPNs in public, private, or hybrid cloud.

Scope exclusions: We exclude hardware-only VPN appliances and standalone zero-trust access tools when they are sold without a cloud VPN service component.

Segmentation Overview

- By Component

- Software

- Services

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By VPN Type

- Remote-Access VPN

- Site-to-Site VPN

- Extranet VPN

- By End-User Industry

- Government and Public Sector

- IT and Telecommunications

- BFSI

- Healthcare

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to frame the demand drivers and set realistic bounds for adoption across industries that rely on remote access. We used public sources such as NIST cybersecurity guidance, CISA advisories, FCC broadband indicators, OECD digital economy statistics, and ITU connectivity datasets to understand security requirements and connectivity readiness.

On the supply side, we reviewed product documentation, public pricing pages, press releases, and security white papers to map what is counted as cloud VPN versus nearby security categories. We also used company filings and investor presentations to anchor revenue mix statements, and we selectively referenced paid subscriptions for company financials and news to confirm timelines and major contract wins. These sources are illustrative rather than exhaustive, since we also checked other public materials for data collection, cross-verification, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what buyers actually purchase under cloud VPN services, and how pricing changes with scale and feature bundles. We spoke with a mix of cloud networking providers, managed service partners, and enterprise network and security teams across APAC, EMEA, and the Americas. The inputs helped us test adoption rates, typical seat and tunnel volumes, and the pace of migrations from legacy VPN setups.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 42% |

| Mid tier: 54% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 16% | Managers: 54% | Americas: 22% |

Market-Sizing & Forecasting

For sizing, the model starts with a top-down build that reconstructs the addressable demand pool from enterprise cloud adoption and remote access usage, and then narrows it using cloud VPN attach rates and typical service penetration by industry. The totals are corroborated using selective bottom-up checks, such as sampled price points and user counts, channel feedback on deal sizes, and roll-ups from a limited set of visible supplier revenue disclosures, which helps us correct obvious overstatements.

Inputs used in the model include remote and hybrid workforce intensity, cloud workload migration activity, VPN user and site-to-site tunnel volumes, average subscription pricing by bandwidth or seat tiers, and security-driven refresh cycles tied to compliance and breach response. Where bottom-up signals are missing for smaller geographies, the gap is handled by applying validated penetration ratios to the local enterprise base and then re-checking the outcome against regional IT spending direction.

Forecasting is built using scenario analysis, where the baseline is guided by expert consensus on cloud adoption pace and security prioritization, and then stress-tested with slower and faster migration assumptions. This approach keeps the forecast practical, since each scenario can be traced back to a small set of observable variables and interview-validated ranges.

Data Validation & Update Cycle

Model outputs are checked against independent signals like enterprise cloud spending direction, reported security budget trends, and observable shifts in remote access tooling preferences, and then the largest variances are investigated. When an anomaly shows up, assumptions are revisited and, where needed, respondents are re-contacted to confirm whether it is driven by pricing, bundling, or a boundary issue in what is being counted.

Before sign-off, the work goes through multiple analyst reviews where calculations, unit conversions, and year-over-year movements are re-checked to avoid hidden compounding errors. The report is refreshed annually, and interim updates are made when major events materially change demand, such as large-scale security incidents or step changes in cloud networking adoption. Right before delivery, a final pass is completed so clients receive the most up-to-date view available.

Mordor Intelligence's Cloud Vpn Services Market Sizing Compared With Other Published Estimates

Published market sizes for cloud VPN services can look far apart, even when the topic sounds identical at first glance. The differences usually come from how each study draws the product boundary, what it counts as a cloud-delivered service versus adjacent security tools, and how pricing and usage volumes are projected over time.

By tracking service revenue tied to cloud-managed VPN control and delivery (and refreshing price tier assumptions each year), Mordor Intelligence keeps the total aligned to paid cloud VPN services rather than blended secure access categories or hardware-led VPN spending, which is where many gaps tend to start.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.94 B (2026) | |

| Global Consultancy A | USD 17.54 B (2026) | Often uses a broader revenue lens that can fold in monitoring, analytics, and adjacent managed connectivity services, which can inflate totals when bundles are counted beyond pure cloud VPN delivery. |

| Regional Consultancy B | USD 3.02 B (2025) | Typically applies a narrower definition closer to cloud VPN as a standalone product line, which can exclude hybrid cloud-managed VPN services sold as part of enterprise networking packages and undercount larger deployments. |

The spread across the table is mainly explained by where each publisher draws the line between cloud VPN services and nearby security or connectivity spend, plus how quickly subscription prices are assumed to expand with added features. In our work, each key assumption is tied back to clear demand signals like user volumes, tunnel usage, and paid service packaging, which makes the final number easier to replicate and update.

Key Questions Answered in the Report

What is the current value of the cloud VPN services market?

The cloud VPN services market is valued at USD 15.94 billion in 2026 and is forecast to reach USD 43.33 billion by 2031.

Which segment is growing fastest within the cloud VPN services market?

Services exhibit the highest growth, registering a 24.6% CAGR as organizations rely on managed offerings to cope with talent shortages and operational complexity.

Why is Asia-Pacific the fastest-growing region?

Regulatory pushes for data sovereignty, rapid cloud adoption, and large-scale 5G industrial projects drive a 24.4% CAGR for Asia-Pacific through 2031.

How does zero-trust network access impact cloud VPN adoption?

Clientless ZTNA reduces reliance on traditional VPN tunnels, offering application-specific access and shrinking attack surfaces, which shifts spending toward zero-trust-enabled platforms.

What role do 5G private networks play in the cloud VPN services market?

5G private networks require secure, low-latency connectivity for industrial IoT; integrating VPN within 5G slices opens new opportunities for vendors targeting manufacturing and logistics sectors.

How severe is the cybersecurity talent shortage affecting VPN deployments?

The National Science Foundation projects a shortfall of 274,000 cybersecurity professionals by 2032, pushing many enterprises to adopt managed VPN services to compensate.

Page last updated on: