Content Delivery Network (CDN) Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

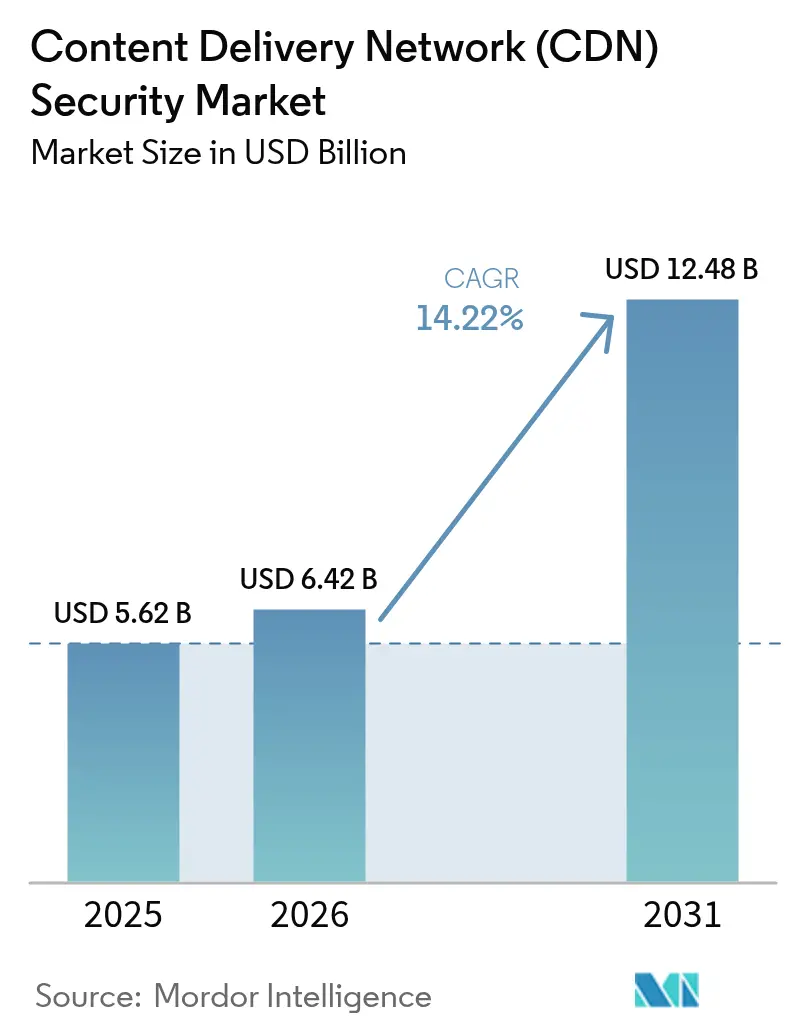

| Market Size (2026) | USD 6.42 Billion |

| Market Size (2031) | USD 12.48 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Delivery Network (CDN) Security Market Analysis by Mordor Intelligence

The CDN Security market size was valued at USD 5.62 billion in 2025 and estimated to grow from USD 6.42 billion in 2026 to reach USD 12.48 billion by 2031, at a CAGR of 14.22% during the forecast period (2026-2031). Escalating attack volumes, aggressive regulatory deadlines, and the migration of workloads to multi-cloud and edge environments are the primary forces behind this expansion. Enterprises now insist on always-on, behavioral-based mitigation after Cloudflare documented a 358% jump in global DDoS events during Q1 2025, equal to 20.5 million blocked attacks. Mandates such as the EU’s Digital Operational Resilience Act (DORA) and PCI DSS v4.0 elevate compliance risk, while OTT traffic growth pushes content owners to embed security deeper into delivery pipelines. A parallel shift toward cloud delivery enables rapid deployment, illustrated by the 65.7% share that cloud implementations already hold. Competitive intensity is rising as incumbents consolidate (Akamai’s USD 450 million acquisition of Noname) while specialists such as Cloudflare expand AI-powered detection to counter evolving bots and scrapers.

Key Report Takeaways

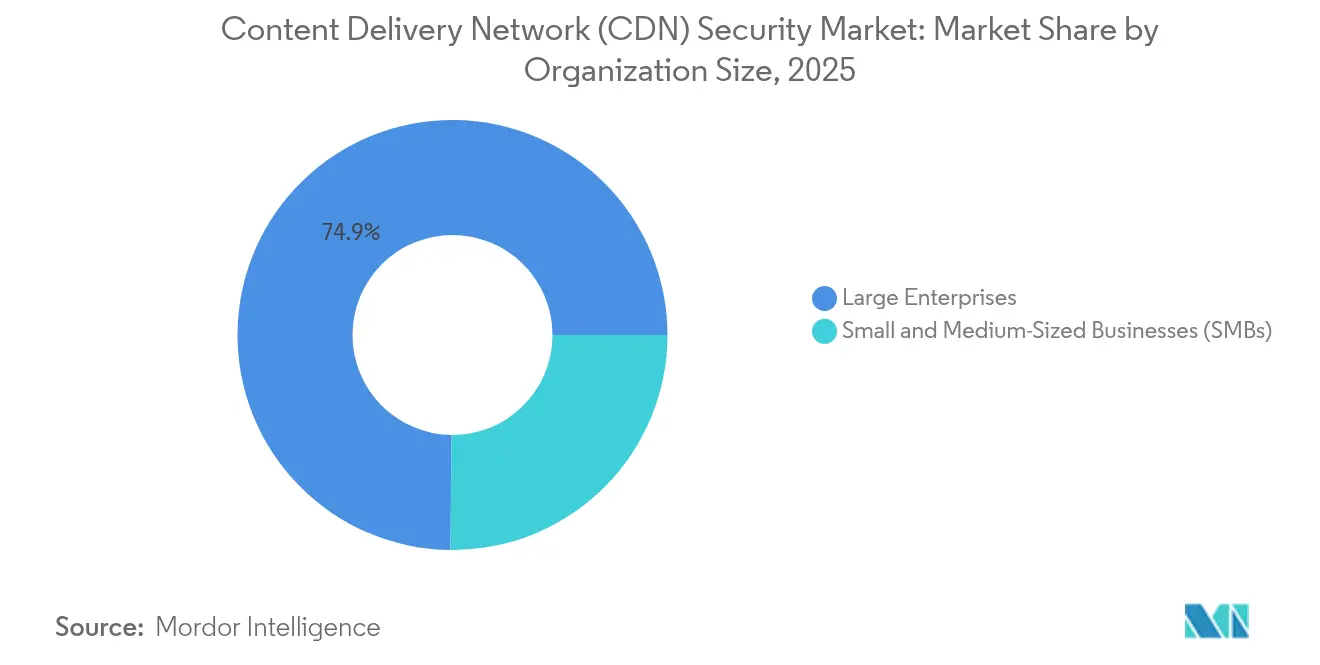

- By organization size, large enterprises held 74.85% of CDN Security market share in 2025; small and medium businesses are projected to post the fastest 14.31% CAGR through 2031.

- By security type, Web Application Firewalls led with 46.65% revenue share in 2025, whereas bot mitigation is forecast to expand at a 15.02% CAGR to 2031.

- By deployment mode, the cloud segment accounted for 65.10% of the CDN Security market size in 2025 and is growing at a 15.75% CAGR between 2026-2031.

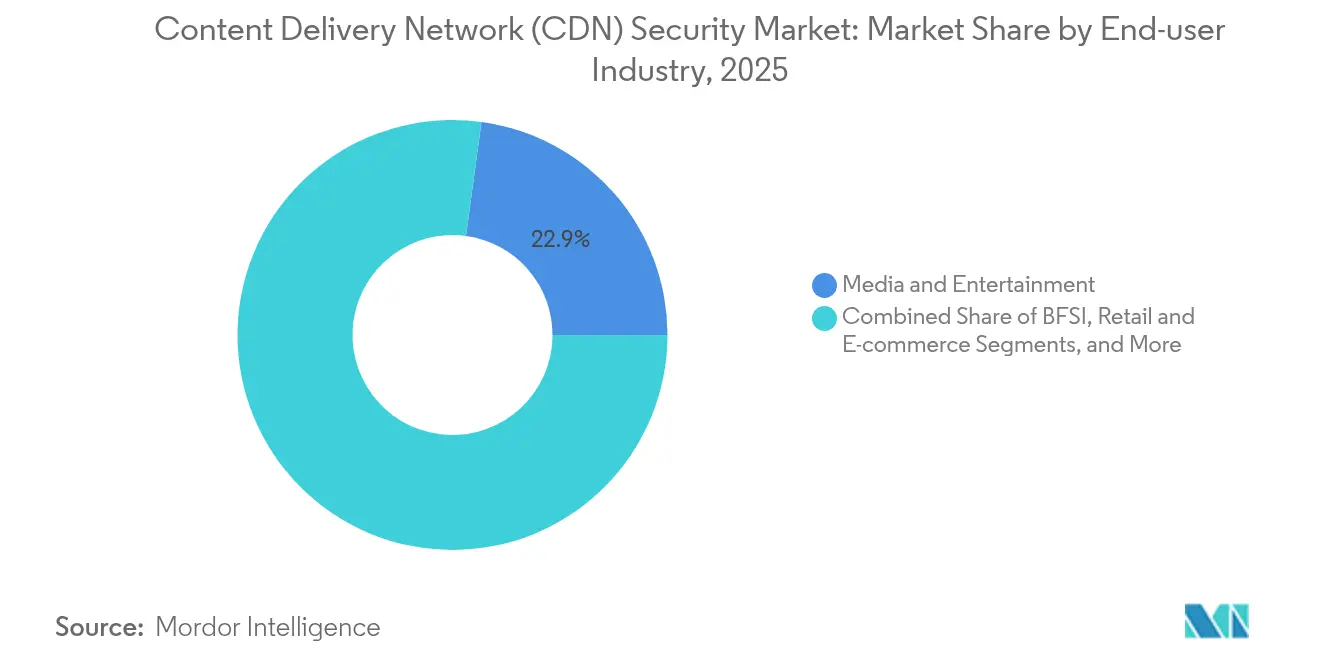

- By end-user, media and entertainment commanded 22.85% share of the CDN Security market size in 2025, while healthcare is advancing at a 14.36% CAGR through 2031.

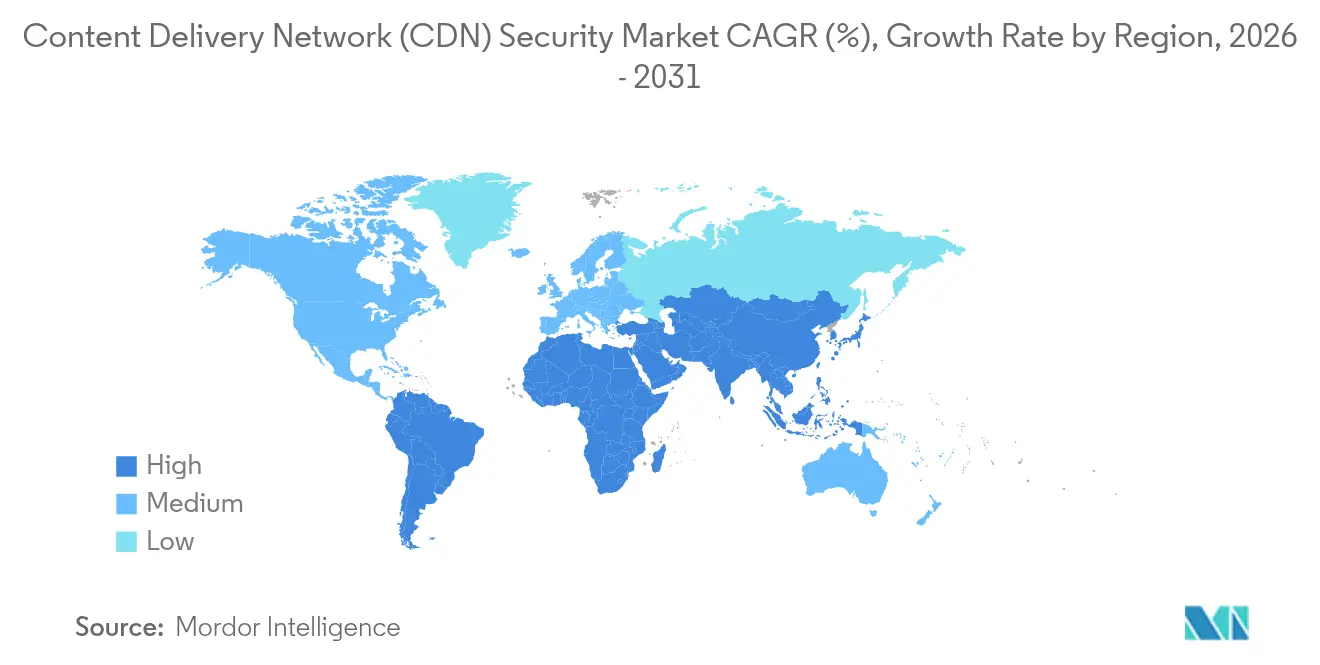

- By geography, North America led with 32.55% market share in 2025; Asia-Pacific is the fastest-growing region at 14.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Delivery Network (CDN) Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency and sophistication of DDoS / L-7 attacks | +3.2% | Global, with highest impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid growth in OTT video and real-time streaming traffic | +2.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Enterprise shift to multi-cloud and edge architectures | +2.5% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Regulatory uptime and data-protection mandates (e.g., DORA, PCI DSS v4) | +2.1% | EU for DORA, Global for PCI DSS v4 | Long term (≥ 4 years) |

| Edge PoP consolidation enabling embedded zero-trust controls | +1.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Algorithmic network-cost steering driving security-integrated CDNs | +1.0% | Global, primarily affecting large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency and Sophistication of DDoS / L-7 Attacks

Cloudflare’s telemetry shows network-layer assaults ballooned 509% year-over-year in Q1 2025, while terabit-scale floods are now routine. Multi-vector campaigns combine SYN floods with Mirai botnets, and reflection methods such as CLDAP and ESP have spiked 3,488% and 2,301% respectively.[1]Field Effect Team, “2025 Global Threat Landscape,” Field Effect, fieldeffect.comCarpet-bombing tactics, 82.78% of all observed attacks in 2024, force organizations to adopt always-on defenses instead of traffic-divert approaches. Financial services remain the primary target as geopolitical tensions spur hacktivism; Akamai logged a 154% rise in sector-focused events in 2023. CDN security vendors now embed ML-driven anomaly scoring at edge PoPs to distinguish legitimate microbursts from malicious floods.

Rapid Growth in OTT Video and Real-Time Streaming Traffic

Subscriber churn correlates directly with stream buffering, prompting platforms to deploy multi-CDN setups plus DRM watermarking. ContentArmor and Limelight upgraded forensic watermarking to curb piracy, integrating directly into delivery layers.[2]Content Armor Staff, “Limelight & ContentArmor Partner for OTT Watermarking,” Content Armor, contentarmor.net Edge-native infrastructure from Qwilt reduces first-frame latency, but its proximity to viewers exposes surface area to credential-stuffing and token theft. Security stacks therefore integrate per-session entropy checks and token binding without inflating latency budgets crucial for live sports.

Enterprise Shift to Multi-Cloud and Edge Architectures

Hybrid workloads erode the traditional perimeter. Akamai highlights that internal API calls now represent 53% of east-west traffic, making visibility essential across VPC hops. The State of Oklahoma consolidated more than 100 agencies through Zscaler Zero Trust, blocking 34,000 encrypted threats and 17.6 million policy violations. Unified policy engines spanning cloud, on-prem and edge PoPs drive demand for platform-agnostic CDN Security market solutions that enforce identity-aware routing and micro-segmentation.

Regulatory Uptime and Data-Protection Mandates

DORA compels EU financial entities to perform resilience testing and third-party risk management or risk heavy fines. PCI DSS v4.0 extends script-monitoring to all website components; requirements 6.4.3 and 11.6.1 formalize tamper detection—a catalyst for advanced WAF rollouts. Shawbrook Bank adopted F5 BIG-IP and Silverline to keep controls uniform across data centers and public cloud, underscoring compliance-driven spending F5. Platforms such as Dynatrace’s newly acquired Runecast automate evidence collection for auditors, shrinking manual compliance overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shortage of skilled cyber-security practitioners | -2.3% | Global, most acute in developing markets | Long term (≥ 4 years) |

| High TCO of always-on mitigation for SMEs | -1.8% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| IPv6 traffic exposing gaps in legacy filtering appliances | -1.2% | Global, with higher impact in regions with rapid IPv6 adoption | Short term (≤ 2 years) |

| Rising energy costs at edge PoPs slowing footprint expansion | -0.9% | Global, with highest impact in regions with expensive energy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Skilled Cyber-Security Practitioners

Forty-six percent of reported breaches hit firms with under 1,000 staff, and 82% of ransomware incidents target the same cohort. Universities average up to 1,580 public-facing domains yet often lack security teams to harden them. Providers now ship point-and-click configuration presets and AI triage, but a persistent talent gap slows CDN Security market adoption among resource-constrained buyers.

High TCO of Always-On Mitigation for SMEs

While algorithmic scrubbing can cut bandwidth bills, SMEs still balk at premium features like behavioral analysis. The OECD notes 72% of small firms embrace basic cyber hygiene but struggle with price and know-how barriers.[3]OECD Analysts, “SME Digitalisation Barriers,” OECD, oecd.org Subscription-based “security-as-a-service” offerings from Cloudflare and Radware spread costs monthly, yet currency fluctuation in emerging economies keeps ROI challenging, tempering overall CDN Security market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Budgets Dominate, SMEs Accelerate

Large enterprises controlled 74.85% of 2025 revenue thanks to complex infrastructures and deep security budgets that span DDoS, WAF, bot and zero-trust layers. NEC rolled out Zscaler for 120,000 global employees to centralize internet and private-app access. Conversely, SMEs show the strongest 14.31% CAGR as managed cloud models democratize tools once reserved for Fortune 500. Cloudflare’s partnership with Rakuten Mobile offers packaged zero-trust services aimed at Japan’s small-business segment. Talent shortages and cost sensitivities persist, yet simplified dashboards and usage-based pricing unlock adoption.

By Security Type: WAF Reigns, Bot Mitigation Surges

Web Application Firewalls held 46.65% share in 2025, bolstered by PCI DSS v4.0 script-monitoring mandates. Fortinet’s FortiAppSec Cloud combines WAF with performance analytics to streamline deployment. Bot mitigation, expanding 15.02% CAGR, addresses AI-driven scraping and credential abuse. Cloudflare’s AI Labyrinth generates decoy pages to trap illegal crawlers, while HUMAN Security claims 99.9% detection accuracy via intelligent fingerprinting. As attackers weaponize machine learning, layered defenses that join WAF, bot and API protection will shape the CDN Security market trajectory.

By End-User Industry: Media Leads, Healthcare Gains Speed

Media and entertainment contributed 22.85% of 2025 spend as OTT platforms battled piracy and high-capacity floods. Multi-CDN plus DRM watermarking remain standard, with Limelight’s joint work with ContentArmor improving traceability of exfiltrated streams. Healthcare is the fastest riser at 14.36% CAGR; Yale New Haven Health’s March 2025 breach of 5.5 million records renewed urgency for layered defenses. Retail also faces silent bot threats—Chain Store Age cites only 5% of luxury brands as fully protected—fuelling demand for adaptive screening.

By Deployment Mode: Cloud Supremacy

Cloud implementations account for 65.10% of CDN Security market share, outpacing on-prem with a 15.75% growth rate. TeN’s migration to Cloudflare cut delivery costs while enabling “security-by-default” with always-on DDoS and WAF. SB Technology launched Cloudflare WAF services to counter Japan’s 53% jump in DDoS activity. Hybrid remains a bridge for regulated sectors; F5’s Distributed Cloud lets FNZ extend unified policy to wealth-management apps.

Geography Analysis

North America generated 32.55% of global revenue in 2025. Mature compliance regimes and high per-capita cyber spend underpin adoption. Oklahoma’s statewide Zscaler roll-out blocked 34,000 encrypted threats and 17.6 million policy violations, proving zero-trust viability at scale.

Asia-Pacific is expanding at a 14.86% CAGR. Akamai logged 51 billion web-app attacks against APAC sites in 2024, a 73% jump, with Australia, India and Singapore worst hit. Rakuten Mobile’s partnership with Cloudflare commercializes managed zero-trust for local SMEs, while Japan’s cyber insurance market is growing nearly 50% a year.

Europe sees steady growth as DORA and GDPR tighten operational and data-protection requirements. Banks retrofit API and WAF controls for resilience testing, and Estonia’s Information System Authority relies on Cloudflare to safeguard sovereign digital services. Latin America and Africa remain nascent; CDNetworks now operates PoPs in 20 LATAM countries to reach 600 million subscribers, laying groundwork for future CDN Security market uptake.

Regulatory Landscape

Regulatory requirements affecting CDN security purchases increasingly combine cyber-risk controls for critical-infrastructure contexts with obligations tied to web, DNS, and API protection. In the EU, Commission Implementing Regulation (EU) 2024/2690 entered into force in November 2024 and sets binding technical and methodological measures (including areas such as access control, cryptography, and supply-chain security), lifting baseline expectations for edge and delivery-layer controls used by digital infrastructure providers.

China issued GB/T 45279.4-2025 in February 2025 (effective June 2025), defining security protection requirements and testing methods for CDN services in IPv4/IPv6 environments. This pushes both providers and buyers toward documented verification of filtering and security behavior. In 2026, updates and guidance tied to operational cyber hygiene continued to extend into CDN-adjacent security domains, including NIST’s March 2026 updates for secure DNS infrastructure (SP 800-81 Rev. 3) and cloud-native API protection guidelines (SP 800-228 update). ENISA also released a May 2026 technical advisory on secure update mechanisms that emphasizes cryptographic verification of updates when delivered via CDNs, reinforcing integrity controls for software and content distribution.

Competitive Landscape

Market concentration is moderate. Akamai, Cloudflare and AWS combine scale, global footprints and security portfolios to hold nearly half of global revenue. Akamai’s USD 450 million Noname buy broadened its API shield, followed by asset purchases from Edgio and a USD 100 million cloud contract with a major tech firm. Cloudflare counters with patented CSRF protection and bot-defense IP. Fastly integrates AI-driven bot management, while hyperscalers bundle content delivery and security under unified SLAs. Niche innovators such as Kasada and Corero target specific pain points from infinite challenge loops to high-precision DDoS filters, keeping competitive pressure high. Patent arsenals, vertical specialization and edge network scale now define differentiation across the CDN Security market.

Content Delivery Network (CDN) Security Industry Leaders

Akamai Technologies, Inc.

Amazon Web Services, Inc.

Cloudflare Inc.

Imperva Inc.

Nexusguard Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are forming around hardening shared edge infrastructure and standardizing security controls that can operate across multi-CDN and multi-cloud deployments. The May 2026 disclosure of Underminr, an architectural weakness affecting shared CDN infrastructure at internet scale (reported as impacting roughly 88 million domains), points to unmet need for stronger tenant isolation, improved abuse detection on shared edge IPs, and more consistent correlation between DNS, TLS, and application telemetry within CDN security stacks.

A second opportunity is converged web, API, and bot protection delivered as unified edge services, influenced by shifts in attacker techniques and by platform consolidation in buyer environments. In June 2026, AWS remediated CVE-2026-13762 in Amazon CloudFront involving an AWS WAF bypass via fragmented HTTP/2 requests, which supports demand for protocol-aware controls and continuous validation of edge enforcement for modern application traffic. Vendors are also responding to the operational impact of bulk automated traffic: in April 2026, Cloudflare formalized work on cache strategies to manage AI crawler loads, enabling differentiated bot policy, traffic filtering, and cache-layer segmentation that can be bundled with bot mitigation and WAAP-style capabilities.

Recent Industry Developments

- July 2026: Cloudflare introduced Precursor, positioned as one-click behavioral defense against modern bots. The launch emphasizes behavioral techniques to counter automation that evades traditional rule-based detection, tying bot mitigation more tightly with edge delivery workflows. It also raises competitive pressure on bot-defense feature depth as buyers look for integrated CDN security controls rather than separate point tools.

- November 2025: AWS introduced support for mutual TLS (mTLS) authentication for Amazon CloudFront to validate client identities at edge locations. This strengthens identity-aware access patterns for APIs and sensitive web applications delivered via CloudFront, complementing WAF and DDoS controls with stronger client authentication. The addition supports tighter zero-trust style policies at the CDN edge for organizations standardizing on AWS delivery and security services.

- November 2024: AWS launched Amazon CloudFront VPC origins to connect CloudFront distributions to private resources in Amazon VPC without exposing them to the public internet. This reduces origin exposure while keeping security enforcement at the edge, improving alignment between delivery, segmentation, and application protection. It also supports architectures where regulated workloads keep origins private while still using CDN acceleration and security controls.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the CDN security market is defined as revenue earned from security capabilities delivered alongside content delivery, where the service is used to protect web apps, APIs, and traffic at the edge.

Scope exclusions: We exclude general enterprise network security that is not tied to CDN delivery paths, and we also exclude pure content delivery services without a security layer.

Segmentation Overview

- By Organization Size

- Small and Medium-Sized Businesses (SMBs)

- Large Enterprises

- By Security Type

- DDoS Protection

- Web Application Firewall (WAF)

- Bot Mitigation and Screen-Scraping Protection

- Data Security and Content Integrity

- Others

- By End-user Industry

- Media and Entertainment

- Retail and E-commerce

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Government and Public Sector

- Education

- Others

- By Deployment Mode

- Cloud

- On-Premise

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping what is being secured and where spending typically shows up, then aligning that to how vendors describe CDN delivered protection. We rely on public sources such as NIST guidance, CISA alerts, and FCC releases on broadband and internet infrastructure, along with OECD digital economy indicators and World Bank data for country level digital adoption signals.

To translate the market into a usable model, we also review company filings, product documentation, and investor materials to understand packaging. This includes items such as WAF, DDoS, bot mitigation, and DNS protection, sold as bundles or as add-ons. A limited set of paid subscriptions for company financials, patent databases, and news and financials is used to confirm timelines, product shifts, and pricing direction. These desk research sources are not exhaustive, and additional public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to stress test the demand story and the pricing logic, especially where public data is thin for edge security attach rates and renewals. We spoke with a mix of security leaders, CDN and edge operations teams, channel partners, and enterprise buyers across APAC, EMEA, and the Americas, so assumptions could be checked and then adjusted where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where edge traffic growth, cloud and web app adoption, and security control penetration are used to reconstruct a realistic demand pool by region. Those totals are then corroborated using selective bottom-up checks, such as sampled price points by security type, customer mix splits by organization size, and channel feedback on typical contract structures.

Key inputs in the model include reported web attack volumes and DDoS intensity trends, enterprise WAF and bot mitigation adoption, the share of traffic protected at the edge versus origin, average contract duration and renewal patterns, and observed price progression as features move from add-ons into standard bundles. Where the bottom-up view has gaps, we use conservative ranges for attach rates and normalize for regional currency timing before finalizing USD totals.

For forecasting, we use scenario analysis anchored to expert consensus on two main drivers: the pace of API protection rollout and the rate of edge workload migration. The scenarios are tied to near-term signals such as regulatory pressure, security budget direction, and web traffic growth, and then rolled into a central case that remains traceable to the same variables each year.

Data Validation & Update Cycle

Outputs are cross checked against independent signals, including cloud and internet usage indicators, reported security incident trends, and directional shifts in edge security product packaging. If a metric changes in a way the model does not explain, we revisit the inputs and trigger a follow-up call to confirm whether the shift is real or driven by data timing.

Before sign-off, the full model goes through variance checks by region and by security type, followed by a multi-step review to ensure assumptions stay consistent across sections. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing changes, regulatory deadlines, or large platform changes. Right before delivery, we run a fresh validation pass so clients receive the most current view supported by the latest signals.

Mordor Intelligence's Cdn Security Market Sizing Compared With Other Published Estimates

Published numbers for CDN security can look far apart because firms do not always count the same revenue streams, and they also pick different base years and growth windows. Differences in what is treated as CDN delivered security versus broader cybersecurity, along with pricing assumptions, usually explains most of the spread.

The benchmark table shows a wide gap that mainly comes from scope and timing choices, then from how bundled security features are valued inside enterprise contracts. In Mordor Intelligence's model, the market is sized around CDN delivered security types like DDoS protection, WAF, bot mitigation and screen scraping protection, data security, and DNS protection, with values stated at USD 6.42 B (2026), which excludes unrelated network security spend that does not sit on the CDN delivery path.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.42 B (2026) | |

| Global Research Publisher A | USD 5.73 B (2025) | Uses a different base year and a longer horizon, and its component split can blend services with solutions in a way that shifts revenue recognition across years, thereby changing the current year market value. |

| Industry Research Publisher B | USD 20.34 B (2024) | Likely applies a broader interpretation that can fold in adjacent cybersecurity spend beyond CDN delivered protections, and it also anchors sizing to an earlier year where currency timing and aggressive adoption assumptions can inflate the total. |

Looking across the table, the practical takeaway is that year selection and what gets counted as CDN specific security explain most of the difference, rather than a disagreement on demand direction. By keeping the scope tied to edge delivered protection categories and then checking results against adoption and pricing signals, the estimate stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is driving the rapid growth of the CDN Security market?

Surging DDoS and bot attacks, tougher regulations such as DORA and PCI DSS v4.0, and enterprises’ migration to multi-cloud and edge architectures collectively push the market toward a 14.22% CAGR through 2031.

Which segment of the CDN Security market is expanding the fastest?

Bot mitigation is projected to grow at 15.02% CAGR as AI-powered scraping and credential abuse outpace traditional defenses.

Why are small and medium enterprises adopting CDN security services?

SMEs face the same threat landscape as large firms but lack in-house expertise; cloud-delivered, subscription-based security solutions lower upfront spending and simplify management, supporting a 14.31% CAGR for the segment.

How does the regulatory environment influence CDN security spending?

Rules like DORA and PCI DSS v4.0 require continuous monitoring, script-level defenses and detailed reporting, compelling financial services and e-commerce firms to invest in advanced WAF, DDoS and compliance dashboards.

Which regions present the greatest growth opportunity?

Asia-Pacific shows the highest 14.86% CAGR, fueled by digital transformation, rising cyber insurance uptake and significant attack volumes reported across Australia, India and Singapore.

Page last updated on: