TD-LTE Ecosystem Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 162.97 Billion |

| Market Size (2030) | USD 394.83 Billion |

| Growth Rate (2025 - 2030) | 19.36% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

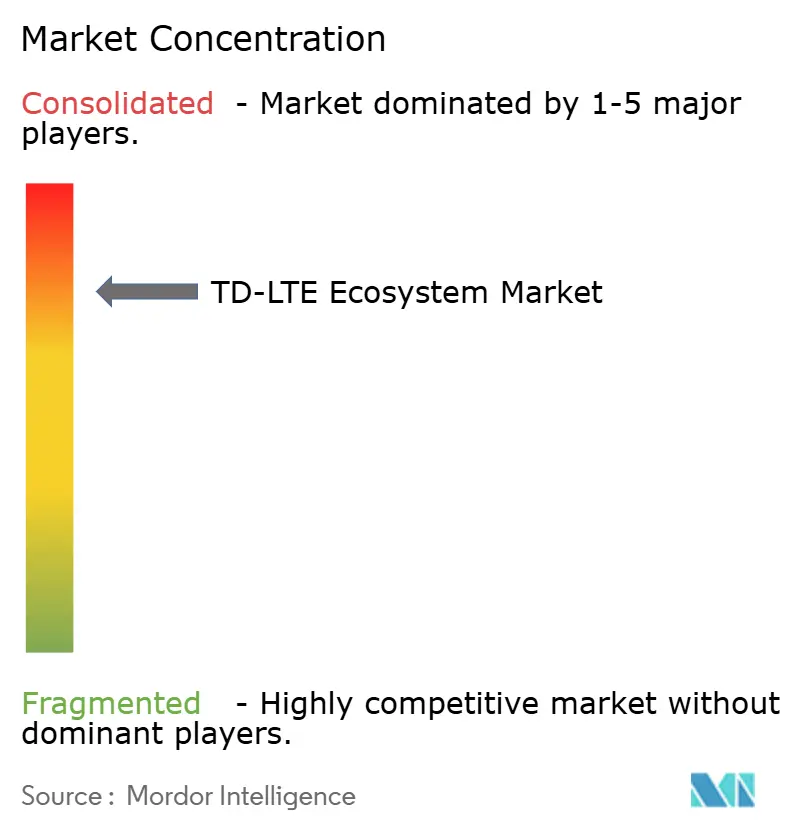

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

TD-LTE Ecosystem Market Analysis by Mordor Intelligence

The TD-LTE ecosystem market size was USD 162.97 billion in 2025 and is projected to reach USD 394.83 billion by 2030, representing a 19.36% CAGR during the period. Operators view the technology as a capital-efficient bridge between legacy 4G and full 5G rollouts, especially in spectrum-constrained settings where time division duplex allows dynamic downlink allocation. Rising industrial digitization, government-funded rural broadband programs, and the lower cost of unpaired spectrum sustain demand. Competitive momentum is now shifting toward software-defined networks, Open RAN architectures, and small cell densification, all of which align with the requirements of edge computing. The TD-LTE ecosystem market continues to benefit from regulatory mandates that equate fixed wireless with fiber for subsidy eligibility, broadening addressable revenue pools.

Key Report Takeaways

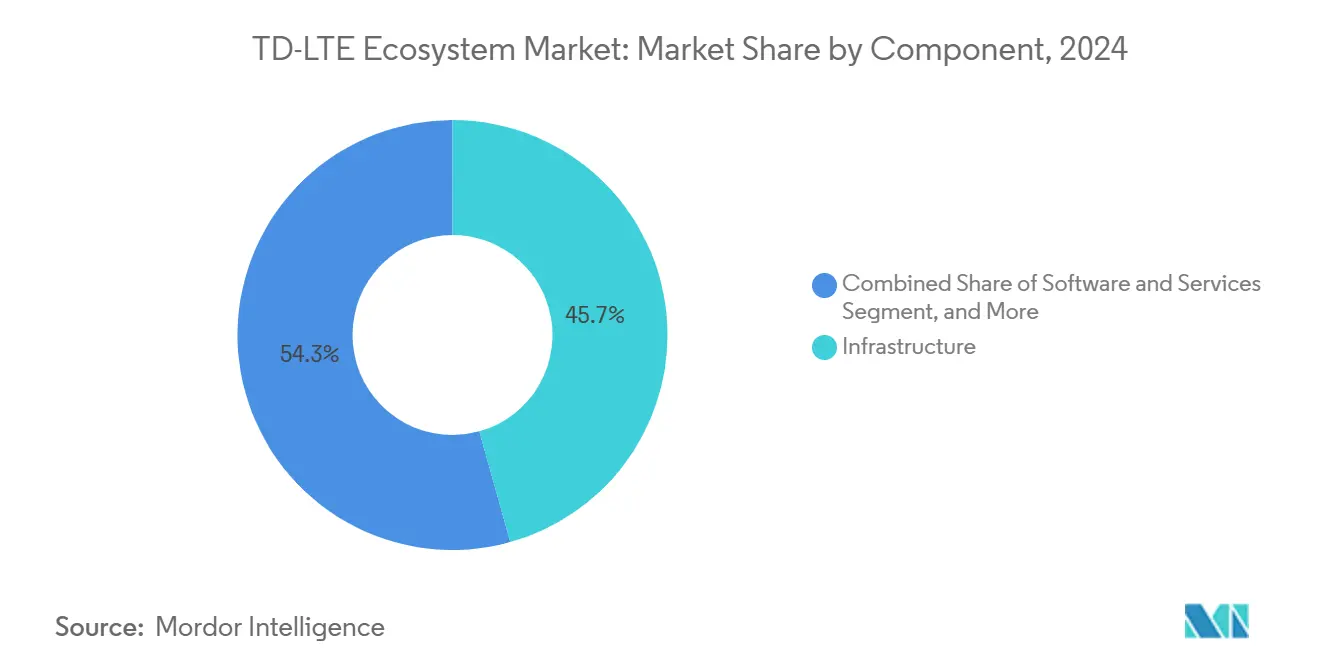

- By component, infrastructure led the TD-LTE ecosystem market with a 45.67% revenue share in 2024, while software and services are projected to advance at a 19.63% CAGR through 2030.

- By device type, smartphones held 51.38% of the TD-LTE ecosystem market share in 2024, and wearables are forecasted to grow at a 20.23% CAGR through 2030.

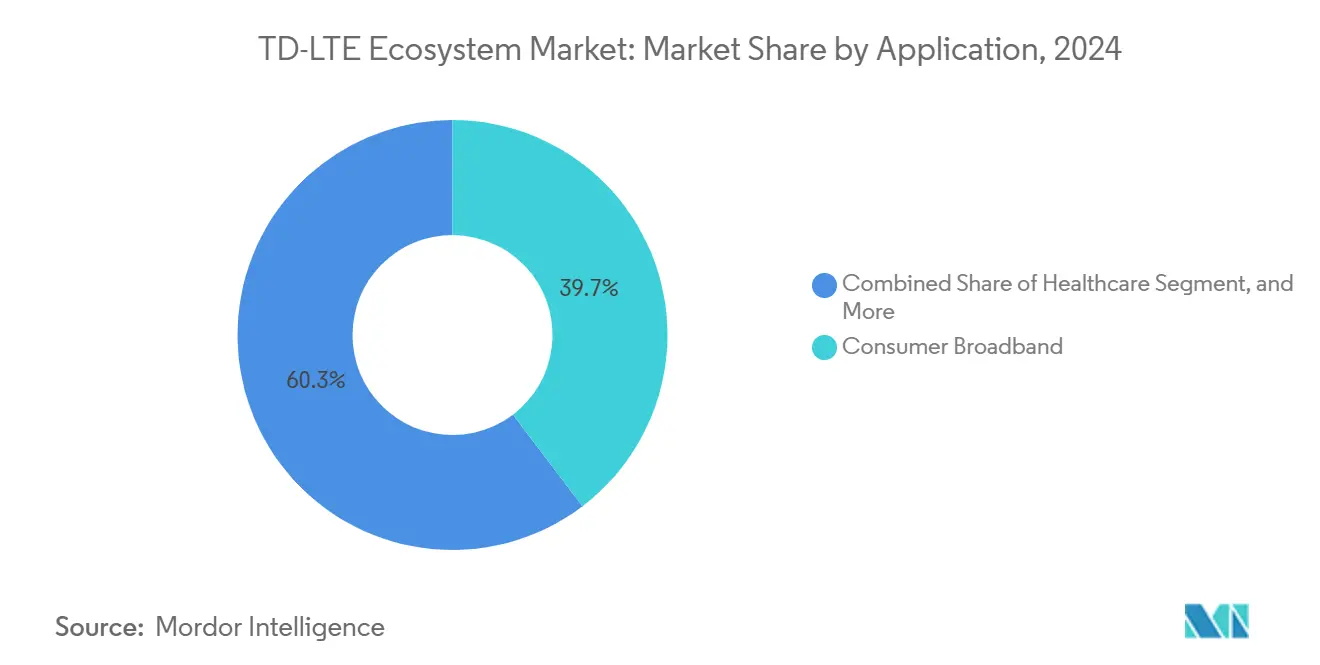

- By application, consumer broadband captured a 39.66% share of the TD-LTE ecosystem market size in 2024, whereas industrial and manufacturing are expected to expand at a 19.89% CAGR over the forecast horizon.

- By deployment environment, macrocell architectures accounted for a 62.37% share of the TD-LTE ecosystem market in 2024; however, small cell installations are set to rise at a 20.14% CAGR to 2030.

- By geography, the Asia Pacific commanded a 42.89% share of the TD-LTE ecosystem market in 2024, while the Middle East is projected to record the fastest growth, with a 19.78% CAGR up to 2030.

Global TD-LTE Ecosystem Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Mobile Data Traffic And Video Streaming | +4.2% | Global, with peak impact in Asia Pacific and North America | Short term (≤ 2 years) |

| Availability Of Unpaired TDD Spectrum At Lower Cost | +3.8% | Asia Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Expansion Of Fixed Wireless Access In Underserved Areas | +3.1% | Global rural markets, concentrated in India, Brazil, and Middle East | Medium term (2-4 years) |

| Industrial Private Networks Demand For Deterministic Wireless | +2.9% | North America and Europe manufacturing hubs | Long term (≥ 4 years) |

| Open RAN Adoption Unlocking New TD-LTE Refresh Cycles | +2.7% | Global, with early adoption in Europe and Asia Pacific | Medium term (2-4 years) |

| AI Driven Self Optimizing Networks Enhancing TDD Spectral Efficiency | +2.9% | Global, led by tier-1 operators in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile Data Traffic and Video Streaming

Video accounts for more than 70% of mobile traffic in developed markets, and the asymmetric downlink orientation of TD-LTE provides greater spectral efficiency than FDD systems.[1]Cisco Systems, “Cisco Annual Internet Report (2018–2023) White Paper,” cisco.com Operators utilize the technology to manage peak-hour congestion without requiring the purchase of additional paired spectrum. Four-k and emerging eight-k streaming intensify downlink demand, making time-division duplex an attractive capacity overlay. Quality-of-service requirements under the European Electronic Communications Code further encourage operators to adopt flexible TD-LTE configurations that can dynamically allocate resources. As a result, the TD-LTE ecosystem market achieves sustainable revenue growth driven by increased traffic.

Availability of Unpaired TDD Spectrum at Lower Cost

Governments typically auction 2.3 GHz and 2.6 GHz unpaired bands at 40-60% lower prices than paired FDD allocations, allowing carriers to secure wide channels for less capital.[2]World Bank, “Connecting for Inclusion: Broadband Access for All,” worldbank.org Chinese standardization around TD-SCDMA has created scale benefits that continue to lower radio costs worldwide. Arbitrage is critical for operators in emerging economies with an average revenue per user below USD 5, where capital budgets remain tight. International Telecommunication Union guidance increasingly favors TDD above 3 GHz, cementing long-term structural cost advantages that funnel more traffic to the TD-LTE ecosystem market.

Expansion of Fixed Wireless Access in Underserved Areas

Rural broadband targets in India, Brazil, and parts of Africa adopt TD-LTE to bypass costly fiber digs, cutting network build times from years to months.[3]GSMA, “Spectrum Pricing Trends,” gsma.com Customer premises equipment eliminates the need for trenching, and subsidy programs now treat fixed wireless on par with fiber, broadening project eligibility. Private equity commitments to rural internet have totaled USD 15 billion since 2024, with the majority earmarked for TD-LTE deployments due to their faster returns. This driver elevates both revenue stability and political support for the TD-LTE ecosystem market.

Industrial Private Networks Demand for Deterministic Wireless

Factories require a latency of less than 10 milliseconds and five-nines reliability for robotics and machine vision. Time-division framing enables precise slot allocation, matching industrial timing needs better than FDD. Lightly licensed spectrum simplifies on-site ownership, and edge analytics thrive on TD-LTE’s low latency. International Electrotechnical Commission standards list the technology among preferred industrial wireless solutions, driving the TD-LTE ecosystem market into manufacturing spending cycles that outpace general telecom growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure For Macrocell Upgrades | -2.8% | Global, with peak impact in developed markets | Short term (≤ 2 years) |

| Rapid Migration To 5G Reducing Standalone TD-LTE Investments | -3.2% | North America and Europe, spreading to Asia Pacific | Medium term (2-4 years) |

| Spectrum Synchronization Conflicts In Mixed TDD-FDD Markets | -1.9% | Europe and North America with mixed spectrum portfolios | Long term (≥ 4 years) |

| Energy Consumption Concerns Among ESG Focused Operators | -1.7% | Global, led by European operators with ESG mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Macrocell Upgrades

Modernizing macro sites costs USD 200,000 to USD 500,000 per location, including radios, baseband units, and backhaul enhancements. In low-margin markets, payback periods lengthen, slowing deployment plans and tempering near-term TD-LTE ecosystem market growth. Integration complexity also forces full radio access network swaps instead of incremental upgrades, further straining capital budgets.

Rapid Migration to 5G Reducing Standalone TD-LTE Investments

Tier-one carriers are pivoting resources toward 5G non-standalone architectures that leverage existing 4G cores. Vendors channel R&D funds into 5G features, and regulators allocate fresh spectrum toward 5G, marginalizing pure TD-LTE plays. The investment diversion tempers long-term confidence in the TD-LTE ecosystem industry roadmap, limiting standalone expansions beyond rural and industrial use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Infrastructure Dominance Amid Software Transformation

Infrastructure accounted for 45.67% of 2024 revenue, underscoring the capital-intensive nature of base stations, core elements, and backhaul. Operators continue to refresh radios to support carrier aggregation and massive MIMO while expanding fiber and microwave backhaul. At the same time, software and services post a 19.63% CAGR, signaling a pivot to cloud-native cores and managed network operations.

Open RAN disaggregation lets carriers mix hardware and software from multiple vendors, reducing lock-in and lowering costs. Spending on AI-driven optimization software rises as carriers automate RF tuning and traffic prediction. As virtualization deepens, the TD-LTE ecosystem market size for software components is set to approach infrastructure outlays in the out-years, rebalancing the value chain toward recurring service revenue.

By Device Type: Smartphone Supremacy with Wearable Acceleration

Smartphones represented 51.38% of 2024 unit sales, driven by replacement programs and subsidy bundles that favor TD-LTE for affordable data connectivity. The segment remains the anchor for high-volume silicon design and economies of scale.

Wearables exhibit the fastest 20.23% CAGR, driven by the demand for health tracking, industrial worker safety, and enterprise augmented reality, which necessitates always-connected form factors. Rugged tablets are gaining market share in logistics and field services, where Wi-Fi connectivity proves unreliable. Customer premises equipment and routers proliferate in fixed wireless deployments, while IoT modules extend the TD-LTE ecosystem market into automotive telematics and smart city sensors. USB dongles are declining but persist in niche industrial applications that require dedicated channels.

By Application: Consumer Broadband Leadership with Industrial Momentum

Consumer broadband accounted for 39.66% of 2024 revenue, as TD-LTE fixed wireless substitutes for fiber where terrain or cost prohibit trenching. Unlimited data plans and government subsidies reinforce adoption.

Industrial and manufacturing exhibit the highest 19.89% CAGR as plants automate assembly lines and adopt predictive maintenance. Banking and financial services deploy TD-LTE for resilient ATM and point-of-sale connectivity, while healthcare leverages it for telemedicine and remote monitoring. Transportation and logistics integrate the network into fleet telematics and traffic management systems. Public safety agencies turn to TD-LTE for mission-critical services during emergencies, adding new addressable layers to the TD-LTE ecosystem market.

By Deployment Environment: Macrocell Foundation with Small Cell Innovation

Macrocells held a 62.37% revenue share in 2024, forming the backbone of coverage across cities and suburbs. Their wide area reach is indispensable for mobility and voice continuity.

Small cells are projected to post a 20.14% CAGR as operators densify their networks for increased capacity and to fill indoor coverage gaps. Edge compute integration at small cell sites supports low-latency applications, such as machine vision and autonomous navigation. Indoor customer premises equipment is popular in enterprises lacking fiber, while outdoor CPE delivers broadband to rural homes. The heterogeneous mix drives the TD-LTE ecosystem market size upward through increased spending on layered architecture.

Geography Analysis

Asia Pacific accounted for 42.89% of 2024 revenue, buoyed by China’s nationwide TD-LTE grids and India’s rural broadband mandates. Domestic equipment supply chains reduce cost, and policy frameworks favor unpaired spectrum allocations. Operators in Japan and South Korea continue to run TD-LTE as a complement to 5G for load balancing during peak video traffic.

The Middle East records the fastest 19.78% CAGR as sovereign wealth funds bankroll national broadband objectives and oil economies diversify into digital infrastructure. Fixed wireless access fills coverage deserts across desert regions where fiber is uneconomical. Government programs bundle TD-LTE routers with affordable data plans to lift household connectivity rates.

North America pursues TD-LTE chiefly for rural fixed wireless and industrial private networks. Federal Communications Commission subsidy rules now treat TD-LTE as fiber-equivalent, channeling funds to operators that upgrade equipment. Europe emphasizes Open RAN and sustainability, pressuring vendors to meet energy efficiency standards. South America and Africa show growing adoption as mobile-first consumers seek affordable broadband, contributing incremental volume to the TD-LTE ecosystem market.

Competitive Landscape

The TD-LTE ecosystem exhibits moderate concentration. Top infrastructure vendors still control the majority of macrocell and core sales, but Open RAN breaks down monolithic solutions, inviting new entrants that focus on software and system integration. Established suppliers are pivoting to managed services, edge computing, and industrial private networks to preserve their margins.

Vendor strategies center on vertical integration and ecosystem alliances. Huawei markets turnkey private networks tailored to factories and mines, while Ericsson enhances TD-LTE through acquisitions that expand enterprise wireless portfolios. Nokia leads in rural fixed wireless deployments under government programs, leveraging its software assets for dynamic spectrum sharing.

Specialist software firms capture value through self-optimizing network platforms that use artificial intelligence to manage traffic and interference. Open RAN pioneers Mavenir and Altiostar supply virtualized baseband functions, challenging incumbent economics. As hardware commoditizes, differentiation increasingly lies in analytics, energy efficiency, and security. These shifts reshape revenue models inside the TD-LTE ecosystem industry.

TD-LTE Ecosystem Industry Leaders

Huawei Technologies Co., Ltd.

ZTE Corporation

Telefonaktiebolaget L. M. Ericsson

Nokia Corporation

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Samsung Electronics completed interoperability testing of its Open RAN-compliant TD-LTE radios with Mavenir’s virtualized baseband, enabling multi-vendor deployments for European carriers preparing spectrum refarming initiatives in the 2.6 GHz band.

- June 2025: Nokia launched its Cloud RAN-ready TD-LTE baseband platform, partnering with Amazon Web Services to offer operators a subscription-based model that bundles virtualized radio functions, orchestration tools, and lifecycle support.

- April 2025: Huawei secured a USD 730 million contract from Saudi Telecom Company to expand TD-LTE fixed wireless access coverage to 1.2 million additional households, including deployment of edge-enabled outdoor CPE units optimized for desert climates.

- February 2025: Ericsson signed a USD 950 million agreement with Telkom Indonesia to modernize 15,000 TD-LTE small cell sites, integrating AI-based self-optimizing network software for traffic management and energy savings across Java and Sumatra.

Global TD-LTE Ecosystem Market Report Scope

| Infrastructure | RAN (Base Stations/eNB) |

| Core Network | |

| Backhaul | |

| Devices | Smartphones |

| Tablets | |

| CPE/Routers | |

| IoT Modules | |

| Software And Services | Network Management |

| Deployment And Integration | |

| Managed Services |

| Smartphones |

| Tablets |

| Laptops |

| Routers And CPE |

| M2M/IoT Modules |

| USB Dongles |

| Wearables |

| Consumer Broadband |

| Healthcare |

| Retail |

| Banking And Financial Services |

| Industrial And Manufacturing |

| Public Safety And Emergency Services |

| Transportation And Logistics |

| Other Application |

| Macrocell |

| Small Cell |

| Indoor CPE |

| Outdoor CPE |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Infrastructure | RAN (Base Stations/eNB) | |

| Core Network | |||

| Backhaul | |||

| Devices | Smartphones | ||

| Tablets | |||

| CPE/Routers | |||

| IoT Modules | |||

| Software And Services | Network Management | ||

| Deployment And Integration | |||

| Managed Services | |||

| By Device Type | Smartphones | ||

| Tablets | |||

| Laptops | |||

| Routers And CPE | |||

| M2M/IoT Modules | |||

| USB Dongles | |||

| Wearables | |||

| By Application | Consumer Broadband | ||

| Healthcare | |||

| Retail | |||

| Banking And Financial Services | |||

| Industrial And Manufacturing | |||

| Public Safety And Emergency Services | |||

| Transportation And Logistics | |||

| Other Application | |||

| By Deployment Environment | Macrocell | ||

| Small Cell | |||

| Indoor CPE | |||

| Outdoor CPE | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the TD-LTE ecosystem market in 2025?

The TD-LTE ecosystem market size reached USD 162.97 billion in 2025.

What is the forecast CAGR for TD-LTE between 2025 and 2030?

The market is projected to grow at a 19.36% CAGR over the forecast period.

Which application segment is expanding the fastest?

Industrial and manufacturing applications are advancing at a 19.89% CAGR through 2030.

Which region leads in revenue contribution today?

Asia Pacific accounts for 42.89% of 2024 revenue, the highest regional share.

Why are small cells important for TD-LTE growth?

Small cell sites deliver dense capacity and low-latency edge computing, driving a 20.14% CAGR in that deployment category.

How does unpaired spectrum pricing influence adoption?

Unpaired TDD bands typically cost 40-60% less than paired FDD, enabling cost-effective network expansion in emerging markets.

Page last updated on: