Colombia Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

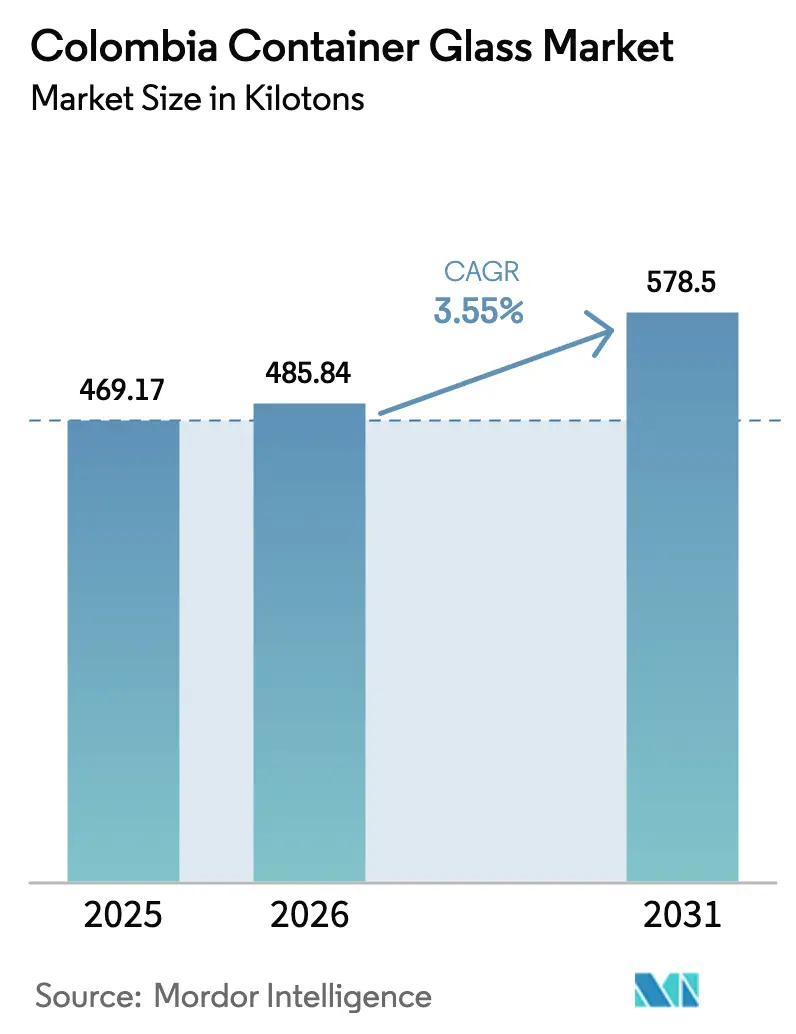

| Base Year Market Size (2025) | 469.17 kilotons |

| Market Volume (2026) | 485.84 kilotons |

| Market Volume (2031) | 578.5 kilotons |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

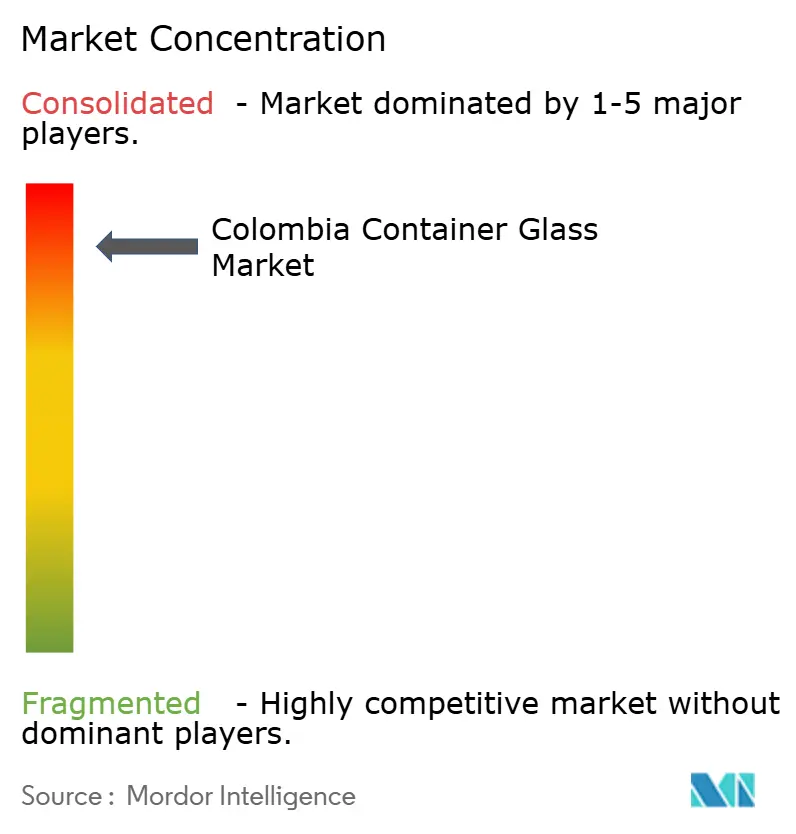

| Market Concentration | High |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Container Glass Market Analysis by Mordor Intelligence

The Colombia container glass market size in 2026 is estimated at 485.84 kilotons, growing from 2025 value of 469.17 kilotons with 2031 projections showing 578.5 kilotons, growing at 3.55% CAGR over 2026-2031. Steady volume gains stem from mandatory extended producer responsibility (EPR) rules, rising consumer demand for sustainable packaging, and large-scale furnace upgrades that improve local supply economics. Brand owners are pivoting toward higher recycled-content bottles to meet Resolution 1407 recovery targets, while premiumization in beer and craft spirits supports value-added flint and amber offerings. The country’s mountainous geography makes imported glass less competitive, enabling incumbents to protect margins even as PET and aluminum challenge entry-level segments. O-I Glass’s USD 120 million Zipaquirá renovation reduces per-ton energy use by up to 15%, giving the company a cost advantage and catalyzing broader technology adoption.

Key Report Takeaways

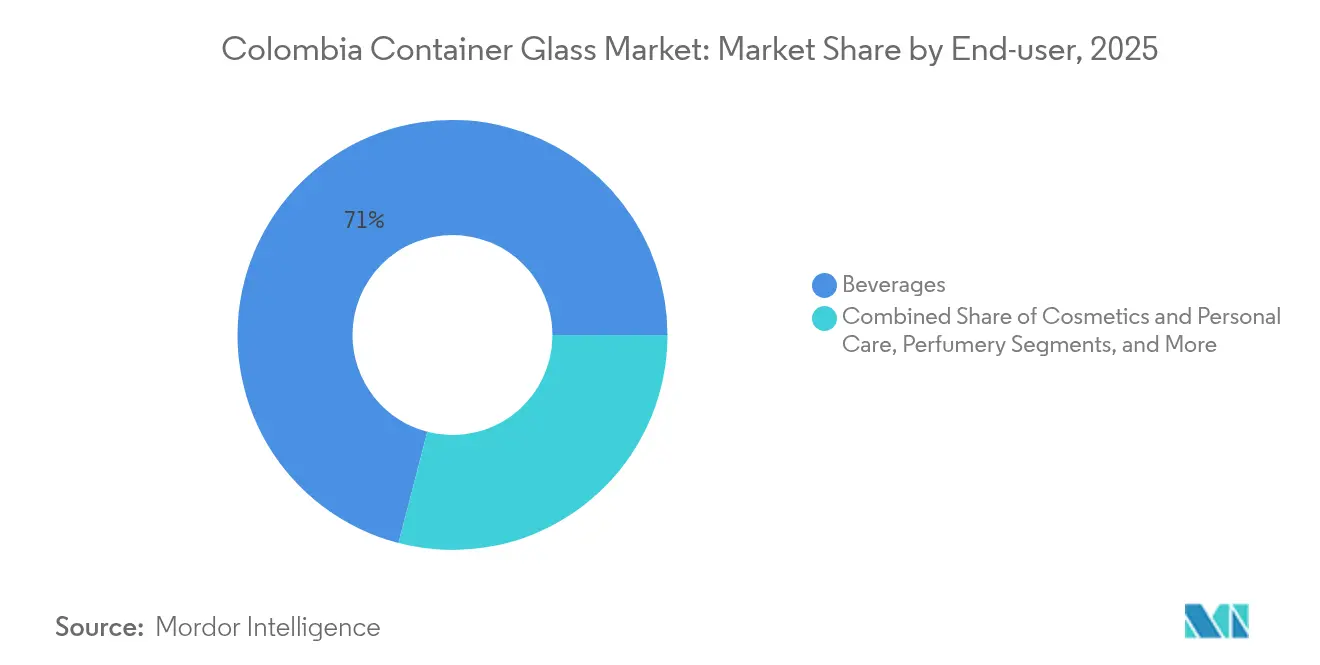

- By end-user, beverages captured 70.96% of the Colombia container glass market share in 2025.

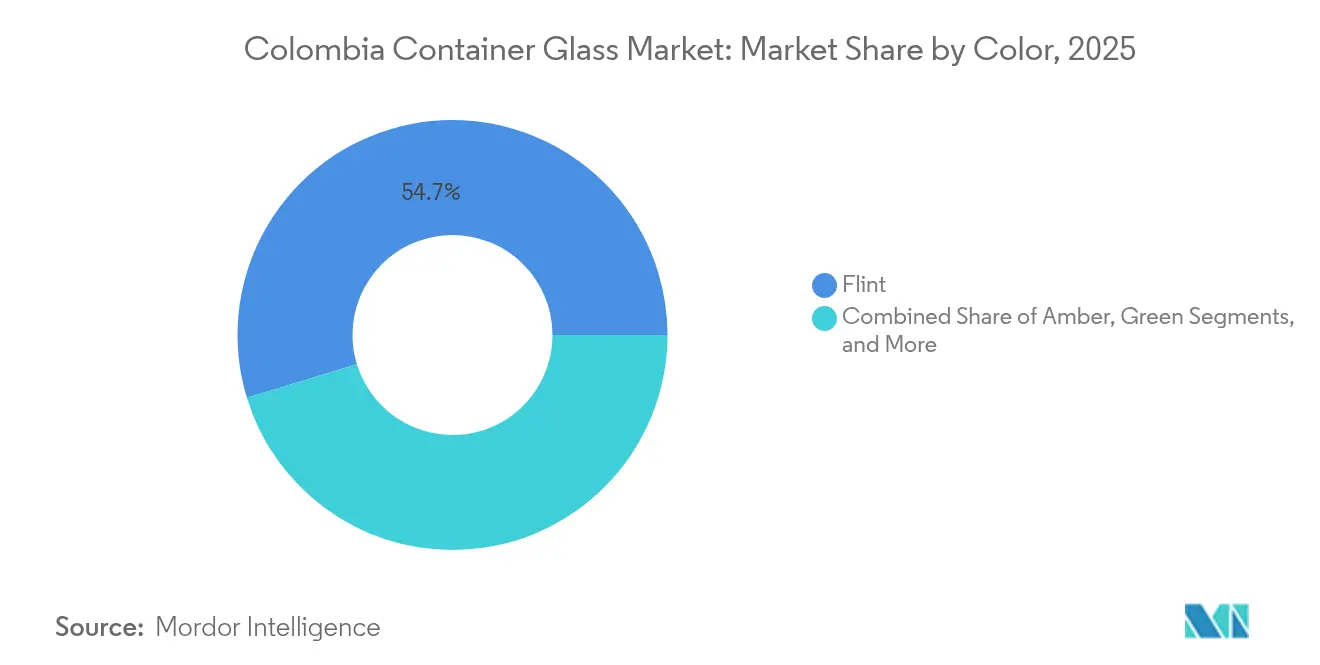

- By color, the Colombia container glass market for amber glass is projected to grow at an 5.46% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High consumer preference for sustainable packaging | +1.2% | National, strongest in Bogotá and Medellín | Medium term (2-4 years) |

| Rapid growth of domestic beer and RTD spirits segments | +0.8% | Antioquia and Cundinamarca | Short term (≤ 2 years) |

| Mandatory EPR and recycled-content rules (Resolution 1407) | +0.6% | National, expanding 2023-2028 | Long term (≥ 4 years) |

| O-I Zipaquirá furnace expansion unlocking local supply | +0.4% | Central corridor | Short term (≤ 2 years) |

| Craft-spirits premiumization driving bespoke bottles | +0.3% | Bogotá, Medellín, Cali | Medium term (2-4 years) |

| Retail-recycler tie-ups boosting cullet availability | +0.2% | Major metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Consumer Preference for Sustainable Packaging

Sustainability scorecards introduced by leading retailers are increasingly rewarding circular materials, propelling the adoption of glass ahead of single-use plastic alternatives. Postobón sourced 31.4% of its packaging from recycled materials in 2019 and aims to achieve a 50% recycled glass content by 2024, thereby reinforcing demand for cullet capacity.[1]Mundo Expo Pack, “Postobón y sus tres pilares para la consolidación de la economía circular,” mundoexpopack.com Resolution 1407 further tilts the playing field by establishing mandatory take-back quotas and expanding geographic coverage to include the San Andrés archipelago and additional cities through 2028. As consumer eco-labels transition from niche to mainstream, beverage and cosmetic brands increasingly rely on premium glass to communicate their environmental credentials and justify retail price premiums.

Rapid Growth of Domestic Beer and RTD Spirits Segments

Beer consumption expanded 7% in 2025, with Águila and Póker together holding more than half of the market value, concentrating bottle demand with a few high-volume fillers. Ready-to-drink spirits mirror this trajectory as millennials seek convenient, bar-quality cocktails at home. In January 2025, beverage manufacturing rose 2.7% even while broader industrial output contracted, underscoring the segment’s defensive qualities. Amber bottles benefit disproportionately because craft distillers and RTD lines require UV protection and distinctive shelf appeal.

Mandatory EPR and Recycled-Content Rules (Resolution 1407)

Resolution 1407 requires producers to register their waste volumes, submit environmental management plans, and meet escalating recovery quotas, thereby formalizing the cullet value chain. Firms that cannot secure recycled feedstock risk non-compliance penalties, creating a premium for integrated collection networks. O-I’s Colombian cullet hub, opened in 2021, positions the company to monetize internal glass scrap and third-party flows while supplying its Zipaquirá furnaces. The regulation’s multicriteria scoring incentivizes collective programs but raises barriers for small entrants lacking audit capabilities.

O-I Zipaquirá Furnace Expansion Unlocking Local Supply

The USD 120 million modernization introduced oxy-fuel combustion and waste-heat-recovery systems, which reduced specific gas use and carbon emissions by approximately 15% per ton, creating 100 new jobs and enhancing output flexibility. Shorter color changeovers allow the plant to service emerging craft-beverage SKUs without sacrificing efficiency. The timing aligns with rising EPR demand, providing domestic fillers with a secure source of high-recycled-content containers and mitigating import exposure amid volatile freight costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and aluminum substitution in value segments | -0.7% | Rural price-sensitive markets | Short term (≤ 2 years) |

| Energy-price volatility for gas-fired furnaces | -0.5% | All manufacturing sites | Short term (≤ 2 years) |

| Mountainous logistics inflating transport costs | -0.3% | Andean corridor | Long term (≥ 4 years) |

| Scarcity of skilled furnace technicians | -0.2% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET and Aluminum Substitution in Value Segments

Amcor’s launch of Colombia’s first 100% recycled-content PET cooking-oil bottle illustrates how polymer containers can erode cost-sensitive glass volumes. Aluminum cans offer lighter freight economics and higher recycling rates, particularly in rural distribution, where transportation accounts for a larger share of the landed cost. While premium beverages still prefer glass for perceived quality, value SKUs increasingly trial alternative formats, capping upside in entry-level niches.

Energy-Price Volatility for Gas-Fired Furnaces

Industrial gas in Bogotá consistently trades above USD 12.5 per Mbtu, compared to USD 3.6 per Mbtu in the United States, eroding margins for energy-intensive melt shops. Colombia’s supply prioritization rules allocate scarce volumes to the residential and power generation sectors during peak periods, forcing glass plants to absorb the risk of load shedding. Smaller manufacturers without efficiency retrofits struggle to compete with O-I’s oxy-fuel platform, accelerating market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Premium Glass Adoption

Beverages maintained a dominant 70.96% share of the Colombia container glass market in 2025 as large brewers and craft distillers continued to favor glass for product differentiation, safety, and shelf stability. The segment’s resilience was highlighted when beverage output grew 2.7% in January 2025 while total manufacturing contracted, reinforcing glass’s defensive characteristics. Bavaria’s high-volume franchises enable economies of scale for standard bottles, whereas emerging craft brands demand bespoke molds that carry higher margins. The cosmetics and personal-care vertical posted a 5.32% CAGR, aided by regulatory preferences for inert packaging and by Colombia’s expanding beauty retail footprint in Bogotá, Medellín, and Cali. Food staples, such as sauces and condiments, continue to stabilize baseline tonnage because artisanal producers promote glass as a premium packaging medium. Pharmaceutical applications leverage glass’s barrier properties, and perfumery remains a niche but lucrative channel where decorative finishes lift average selling prices.

As beverage fillers pledge higher recycled-content thresholds, cullet availability becomes a competitive lever for suppliers. O-I’s dedicated hub secures internal demand while opening third-party revenue streams from competing fillers seeking EPR compliance. Cosmetics brands rely on glass to convey luxury, offsetting the heavier shipping weight through smaller unit volumes and higher price points. The Colombian container glass market size for beverages is projected to advance in tandem with premium SKUs, although some low-end beer lines are experimenting with refillable PET to manage costs.

By Color: Flint Dominance with Amber Acceleration

Flint accounted for 54.72% of Colombia's container glass market share in 2025, driven by widespread acceptance across beverages, food, and personal care uses, where product visibility is crucial. Amber, by contrast, accelerates at a 5.46% CAGR, buoyed by craft spirits that require UV protection and by pharmaceuticals keen to safeguard light-sensitive formulations. O-I’s flexible Zipaquirá line can switch colors quickly, enabling smaller batch economics and stimulating adoption among micro-distilleries and indie brewers. Green glass remains confined to select wine and specialty beverage niches, while decorative blues and blacks cater to high-margin cosmetics and perfumery.

The availability of recycled brown cullet supports Resolution 1407's recovery metrics because amber can accept greater impurity levels without impairing its aesthetics. The Colombia container glass market share for amber is therefore on a gradual upward trajectory as regulatory quotas rise. Flint still towers in absolute tonnage, but its growth moderates toward the 3.55% market CAGR as baseline penetration approaches saturation in mainstream soft-drink and food jars.

Geography Analysis

Production clusters around Bogotá, Medellín, and Cali align furnace capacity with the country’s principal beverage filling corridors, ensuring timely bottle deliveries at competitive freight rates. O-I’s consolidation of Envigado into its expanded Zipaquirá site concentrates more than 70% of national melt in central Colombia, simplifying supply chain orchestration while leveraging scale economies. Antioquia and Cundinamarca households consume beer at rates 78% above the national mean, underscoring bottle demand density and justifying furnace expansion in proximity to these hotspots.

Resolution 1407’s mandate to extend EPR coverage to the San Andrés archipelago in 2022 and to additional municipalities by 2028 pushes recyclers to invest in cullet collection in historically underserved zones. Although mountainous topography around the Andean corridor inflates trucking costs, it simultaneously shields local producers from cheaper imports by raising landed prices for overseas suppliers. Coastal ports in Barranquilla and Cartagena serve as conduits for specialty bottles and raw materials; Distribuidora Córdoba alone handled USD 26.69 million in glass imports and USD 4.42 million in exports during the period 2021-2025, illustrating active trans-Andean trade flows.

Looking forward, infrastructure upgrades tied to Colombia’s 5G toll highway projects are expected to compress haulage times between coastal terminals and interior consumption nodes, potentially moderating logistics overhead for both domestic and imported glass. However, local furnaces retain a natural hedge because freight savings often offset higher energy costs, preserving glass’s competitiveness even under modest tariff regimes. Regional governments also incentivize on-shore cullet processing to meet rising EPR quotas, fostering circular supply ecosystems that favor proximate melt shops.

Competitive Landscape

The Colombia container glass market is highly concentrated, with O-I Glass operating the nation’s only multi-furnace complex following the shutdown of its Envigado plant and the USD 120 million retrofitting of Zipaquirá in 2024. This site now ranks among the company’s three largest Latin American assets, giving it unparalleled scale and technological sophistication. Smaller manufacturers, such as New High Glass Colombia S.A.S., compete in cosmetics, perfumery, and short-run custom bottles, where agility trumps furnace tonnage. Import-export intermediaries, such as Distribuidora Córdoba, supplement domestic supply by sourcing niche containers from Mexico and Europe for artisanal clients.

O-I’s oxy-fuel burners and waste-heat recovery systems reduce per-ton gas intensity and CO₂ emissions, resulting in lower variable costs and a smoother path to decarbonization targets. The 2021 cullet hub further tightens the loop between collection and melt, enabling the plant to offer higher recycled-content bottles that help beverage fillers clear Resolution 1407 check marks. Secondary players lack comparable capital budgets, which constrains domestic rivalry to niche formats rather than volume battlegrounds.

Strategic partnerships also shape the competitive terrain. Tecnoglass, known primarily for architectural flat glass, refinanced a USD 500 million revolving facility in September 2025, signaling potential diversification funds that could spill into container ventures.[3]LexLatin, “Tecnoglass alcanza refinanciamiento de línea de crédito sindicada,” lexlatin.com Meanwhile, Amcor Rigid Packaging’s 100% PCR PET launch portrays cross-material rivalry rather than direct head-to-head competition with glass. Despite external threats, high replacement costs, and stringent EPR compliance act as strong entry barriers, the Colombia container glass market is firmly anchored around O-I and a small cluster of specialty outfits.

Colombia Container Glass Industry Leaders

O-I Glass, Inc.

Distribuidora Cordoba SAS

CFC CAFARCOL SAS

New High Glass

Feemio Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tecnoglass refinanced and upsized its syndicated revolving credit facility to USD 500 million, extending maturity to 2030.

- May 2025: Global Packaging Solutions unveiled Bag-in-Box systems for liquids in Colombia with a monthly capacity of 350,000 units, targeting exports to neighboring markets.

- November 2024: SIG partnered with Celema to introduce aseptic carton filling technology, specifically designed for flavored milk and plant-based beverages.

- April 2024: O-I Glass completed a USD 120 million sustainable transformation and expansion of its Zipaquirá plant, cutting CO₂ by up to 15% per ton and adding roughly 100 jobs.

Colombia Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Colombia container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors) and by country (Germany, Italy, France, Poland, United Kingdom, Spain, Russia and Rest of Europe). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the projected volume for Colombia’s container glass producers by 2031?

The Colombia container glass market is forecast to reach 578.5 kilotons by 2031, reflecting a 3.55% CAGR from 2026.

How significant is the beverage’s role in container demand?

Beverages account for 70.96% of national glass volume in 2025, and their growth underpins most capacity expansions.

Why is amber glass gaining share?

Craft spirits and pharmaceutical fillers prefer amber for UV protection, driving a 5.46% CAGR in this color segment.

How does Resolution 1407 influence sourcing strategies?

The rule mandates rising recovery targets, prompting fillers to secure recycled cullet supplies and favor integrated glassmakers.

Which regions drive the highest consumption of glass bottles?

Antioquia and Cundinamarca lead demand due to their outsized beer consumption and concentration of bottling lines.

What technology upgrades improve furnace economics?

O-I’s oxy-fuel combustion and waste-heat recovery cut gas use and CO₂ emissions by about 15% per ton of glass melted.

Page last updated on: