Cold Laser Therapy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

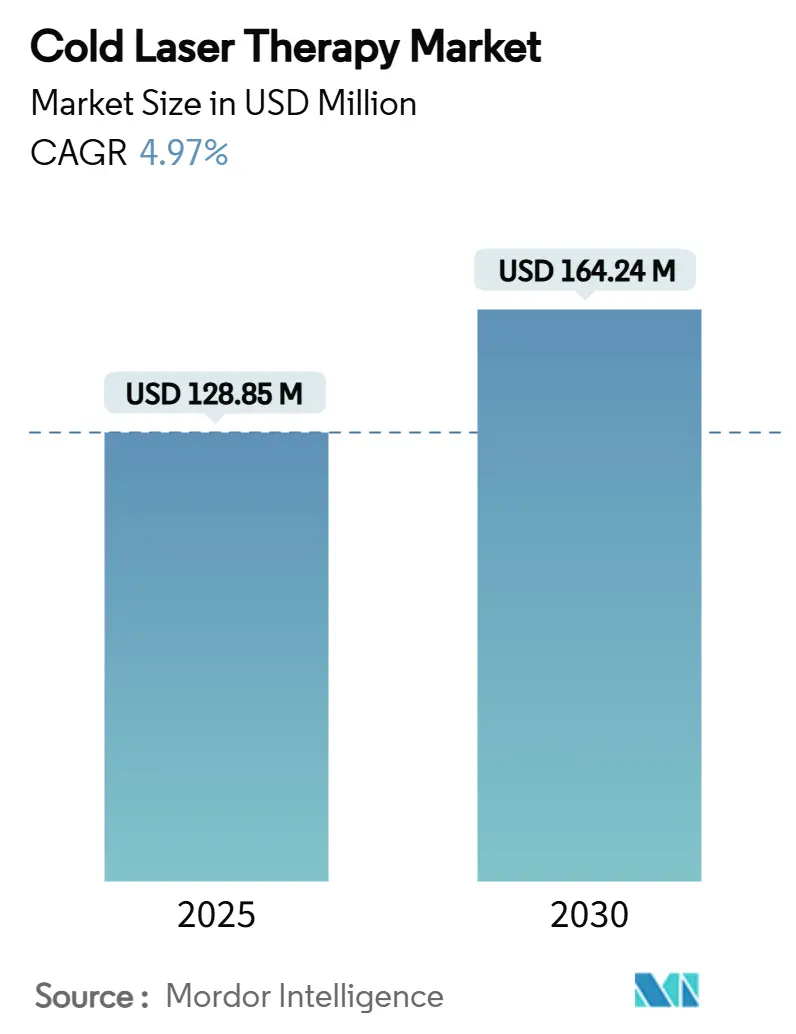

| Market Size (2025) | USD 128.85 Million |

| Market Size (2030) | USD 164.24 Million |

| Growth Rate (2025 - 2030) | 4.97% CAGR |

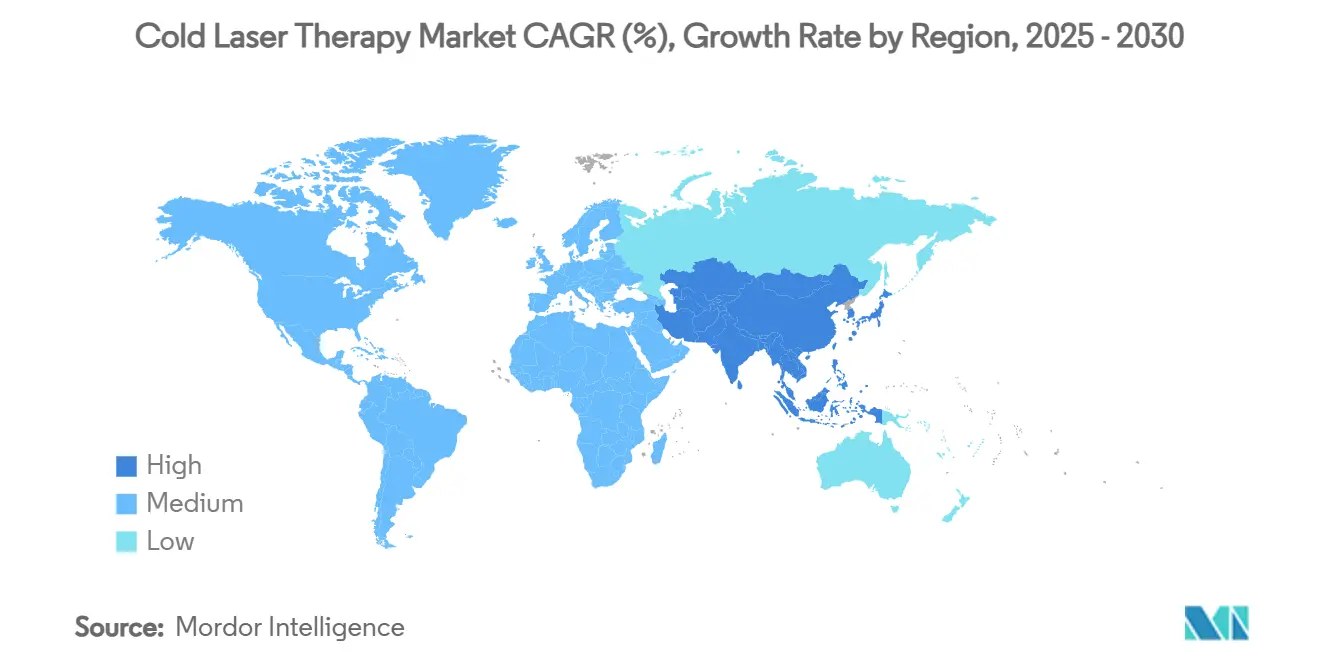

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Laser Therapy Market Analysis by Mordor Intelligence

The cold laser therapy market size stands at USD 128.85 million in 2025 and is projected to reach USD 164.24 million by 2030, advancing at a 4.97% CAGR. This outlook positions the cold laser therapy market as a pivotal pillar within non-invasive care, fuelled by a wider move to reduce pharmaceutical dependency and manage chronic pain. The FDA’s late-2024 clearance of the Valeda Light Delivery System for dry age-related macular degeneration confirms that regulatory acceptance is keeping pace with technology. Class 3B lasers remain the installed workhorse in clinics, yet rising practitioner demand for deeper tissue reach is pushing Class 4 adoption. Hand-held devices now bridge professional and home environments, and a new Current Procedural Terminology (CPT) code approved in August 2024 paves the way for broader payer coverage. Collectively, these shifts keep the cold laser therapy market on a steady, innovation-led trajectory.

Key Report Takeaways

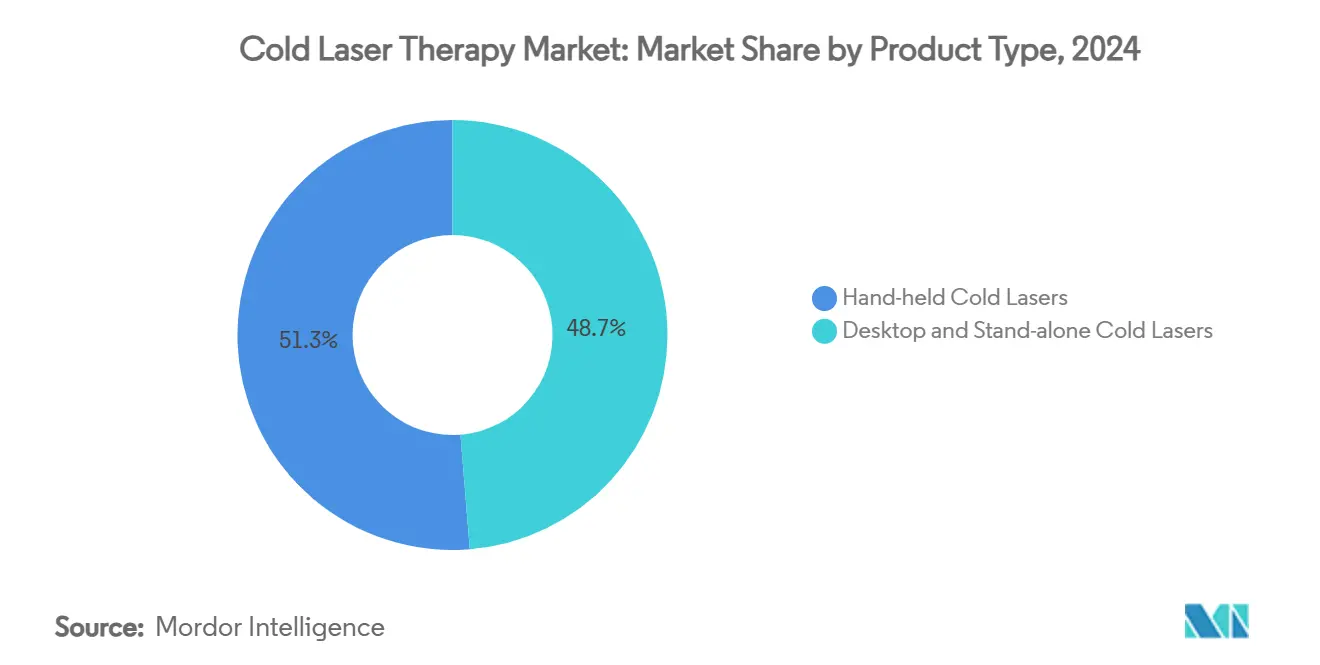

- By product type, hand-held cold lasers captured 51.27% of cold laser therapy market share in 2024 while the same segment is forecast to expand at an 8.42% CAGR through 2030.

- By power class, Class 3B devices led with 62.48% revenue share in 2024; Class 4 systems show the highest projected CAGR at 7.07% to 2030.

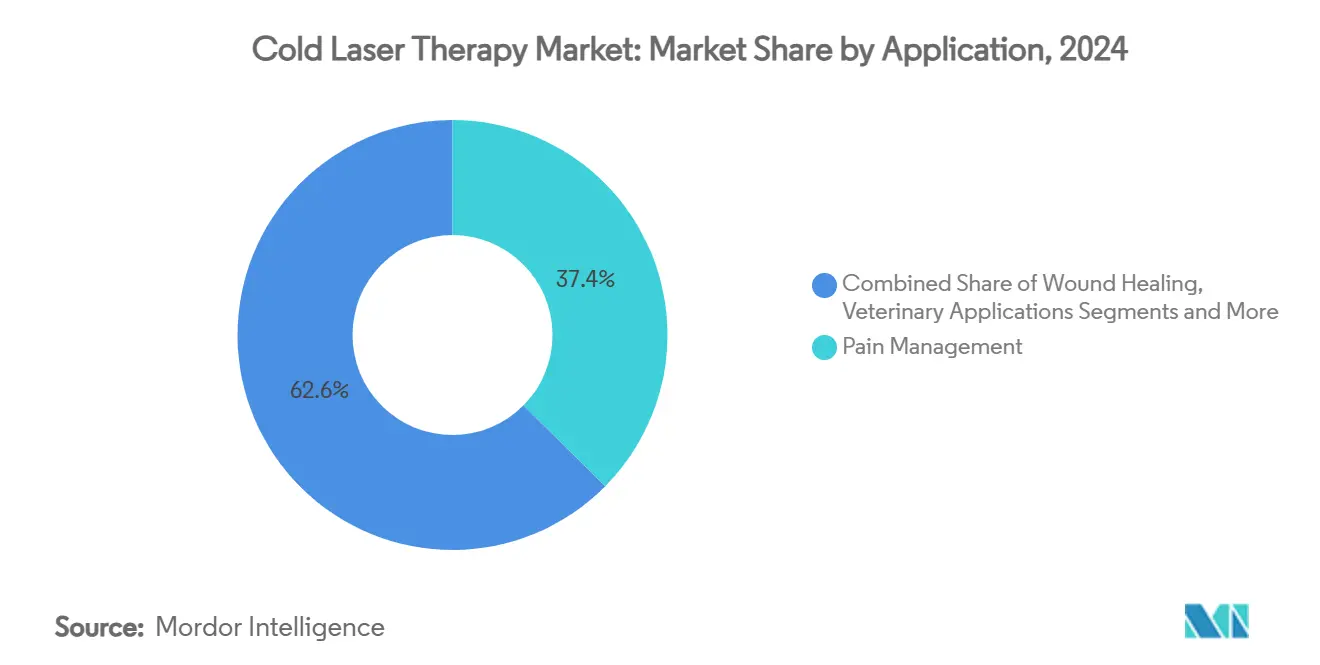

- By application, pain management represented 37.42% of cold laser therapy market size in 2024, yet veterinary applications are set to grow fastest at a 6.68% CAGR.

- By end user, hospitals held 39.66% share of the cold laser therapy market size in 2024, whereas home-care settings are advancing at a 6.14% CAGR.

- By geography, North America accounted for 41.26% of cold laser therapy market share in 2024, while Asia-Pacific is projected to record a 6.99% CAGR through 2030.

Global Cold Laser Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic musculoskeletal pain | +1.2% | North America, Europe, global spill-over | Long term (≥ 4 years) |

| Preference for non-invasive care | +0.9% | Developed markets worldwide | Medium term (2-4 years) |

| Rapidly ageing global population | +0.8% | Asia-Pacific core, North America and Europe | Long term (≥ 4 years) |

| Expanding sports-injury management adoption | +0.6% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Wearable rehabilitation device integration | +0.4% | North America and Europe | Medium term (2-4 years) |

| Moves toward over-the-counter availability | +0.3% | Select markets in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Musculoskeletal Pain

Global pain statistics continue to climb, creating an expanding pool of patients who perceive photobiomodulation as a credible alternative to opioids. The mechanism focuses on mitochondrial recovery, enabling sustained pain relief without addiction risk. A 2024 clinical program using FibroLux reported a 52% tender-point reduction in fibromyalgia cohorts, marking a transition from symptom masking to cellular repair.[1]Corporate Release, “Multi Radiance Medical Therapeutic Laser Receives FDA Clearance for Fibromyalgia Pain Relief,” Multi Radiance Medical, multiradiance.com Provider attitudes echo this shift because repeated laser sessions carry no cumulative tissue damage, dovetailing with value-based reimbursement models. Insurer restrictions on long-term opioid use indirectly accelerate adoption, positioning the cold laser therapy market as a sustained pain-management solution rather than an adjunct modality.

Growing Preference for Non-Invasive Treatments Over Pharmacological Options

Patient aversion to systemic side effects has magnified interest in energy-based care. The opioid crisis reshaped physician habits, heightening demand for therapies that demonstrate quantifiable benefit without addiction concerns. Whole-body photobiomodulation achieved clinically meaningful pain reduction and improved quality of life in a 6-month randomized trial, showing outcomes on par with mainstream interventions.[2]Santiago Navarro-Ledesma et al., “Outcomes of Whole-Body Photobiomodulation on Pain,” Frontiers in Neuroscience, frontiersin.org Immediate applicability, real-time feedback, and lack of drug interactions reinforce patient trust. For multi-morbid seniors, photobiomodulation offers a path to pain management without adding pharmacologic load, a factor that underpins the modest but persistent 4.97% CAGR underpinning the cold laser therapy market.

Rapidly Ageing Global Population

Demographic momentum in Asia-Pacific is steering healthcare toward modalities that address degenerative conditions while keeping systemic safety high. Photobiomodulation delivers localized effects that work for cardiovascular-compromised or renal-impaired seniors. The Valeda system clearance for dry age-related macular degeneration exemplifies how geriatric-oriented approvals will broaden the addressable market. Ageing demographics dovetail with rising demand for home-use devices, reducing mobility-related care barriers and lifting the overall cold laser therapy market outlook.

Expanding Adoption in Sports-Injury Management

Professional sports teams now embed photobiomodulation into pre-exercise warm-ups and post-match recovery. Clinicians cite enhanced mitochondrial ATP production as a reason for quicker return-to-play timelines. Studies published in 2024 chart significant declines in muscle damage biomarkers when lasers are applied both before and after intense activity. Field-side portability broadens use cases, aligning with athlete scrutiny on prohibited substances. Visibility from elite teams resonates with recreational athletes, expanding the cold laser therapy market to retail and wellness spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement coverage | -1.1% | Global, stronger in cost-sensitive markets | Medium term (2-4 years) |

| Scarcity of large-scale randomized evidence | -0.8% | Global | Long term (≥ 4 years) |

| Eye-safety power-limit constraints | -0.5% | Global | Long term (≥ 4 years) |

| Cannibalization from low-cost LED devices | -0.4% | Global, high in price-sensitive regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Coverage Across Major Healthcare Systems

Private payers often label laser therapy investigational, limiting coverage to narrow oncology-related indications. Blue Cross Blue Shield’s 2024 policy defers reimbursement for common musculoskeletal conditions, leaving patients to self-fund courses that can require 12 or more sessions. Although the American Medical Association secured a CPT code in 2024, payer uptake remains patchy. Treatment deferral, therapy substitution, and geographic coverage gaps collectively dampen market velocity. Manufacturers channel resources into payer-education programs, yet premium devices remain a purchase weighed against out-of-pocket appetite.

Scarcity of Large-Scale Randomized Clinical Evidence for Some Indications

Evidence varies widely across applications, complicating meta-analysis and hindering reimbursement wins. Regulatory bodies request multi-center trials, but device developers often lack the working capital to fund studies across diverse disease states. Veterinary photobiomodulation, despite promising signals, still shows mixed outcomes due to inconsistent protocols.[3]Darryl L. Millis and Anna Bergh, “Laser Therapy in Animals,” Animals, mdpi.com Until standardization and stronger datasets are in place, payers and clinical guideline committees hesitate, placing a brake on broad cold laser therapy market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hand-Held Devices Drive Market Evolution

Hand-held lasers held 51.27% share in 2024, the highest among product categories. Clinical professionals appreciate their ability to transition from bedside use to home-based regimens without recalibration. The devices integrate lithium-ion power packs, wavelength multiplexing, and user-friendly interfaces that guide patients through preset protocols. Strong growth at 8.42% CAGR signals that portability has become a decisive buying parameter in the cold laser therapy market. In tertiary hospitals, bedside staff deploy hand-held lasers to manage post-surgical pain before patients discharge, creating continuity when those same units are later rented or sold for home follow-up. Sports teams favor rugged hand-held formats that withstand field environments while complying with anti-doping rules. Elderly users embrace ergonomic skins and low activation force buttons that respect reduced grip strength. Retail pharmacies in Australia and Canada have begun stocking basic hand-held models, testing future OTC potential once broader regulatory clearance materializes.

Desktop and stand-alone lasers remain essential for specialty clinics that require higher power outputs, real-time dosimetry, and integration with electronic medical records. They deliver consistent beam homogeneity across large treatment areas, suiting obesity-related joint disorders or full-back muscle strains. Despite slower growth, desktop systems command premium pricing because advanced cooling extends diode life. Service contracts assure uptime, reinforcing loyalty among orthopaedic and rehabilitation centers. Some vendors bundle classroom training and protocol libraries, cementing clinical best practice and raising switching costs. Thus, while hand-held units expand the addressable customer base, desk-top platforms maintain the therapeutic benchmark, ensuring balanced revenue across the cold laser therapy market.

By Power Class: Class 4 Systems Gain Therapeutic Momentum

Class 3B devices led with 62.48% share in 2024, benefiting from historical ubiquity and straightforward operator training. Their established safety profile simplifies multi-clinic deployment, and many insurers reimburse 3B codes more readily than higher-powered alternatives. Yet practitioner observations highlight limitations when attempting to reach deep bursae or posterior joint capsules. This clinical gap underpins an expected 7.07% CAGR for Class 4 lasers, which can exceed 500 mW continuous-wave output. In controlled protocols, Class 4 energy profiles reduce session count by as much as 40% versus Class 3B, making them attractive even when initial device cost is higher.

Veterinary adoption illustrates how Class 4 traction begins at niche use cases. Large animal practices prefer higher power to treat equine tendon injuries without sedation, a setting where rapid penetration is paramount. Manufacturers are introducing dual-mode units that toggle between 3B and 4 output, offering practitioners flexibility when treating both superficial dermatology and deep musculoskeletal targets. Regulatory clarity continues to evolve, as seen in April 2024 FDA draft guidance on thermal effects for devices, improving submission predictability for innovators. Over the forecast horizon, safety-certified eyewear, interlocked activation triggers, and real-time irradiance monitoring are expected to reduce operator anxiety and foster broader Class 4 uptake, thereby widening the cold laser therapy market footprint.

By Application: Veterinary Segment Emerges as Growth Leader

Pain management has anchored 37.42% of cold laser therapy market size since 2024, cemented by decades of clinician familiarity with laser therapy for tendinopathies and lower-back pain. Protocols have been refined to the point where physical therapists routinely embed laser sessions into multi-modal regimens. However, veterinary applications are poised to outrun legacy segments with a 6.68% CAGR. Elevated pet-care spending in North America and Europe means owners increasingly request advanced modalities once reserved for human medicine. Regulatory landscapes are less stringent, allowing faster commercial roll-outs. Case-series data on canine osteoarthritis show measurable improvements in lameness scores within three weeks of treatment, bolstering practitioner confidence.

Dermatology and aesthetics increasingly deploy lasers for scar remodeling and collagen stimulation. Clinics pair laser sessions with topical platelet-rich plasma, reporting synergistic gains in wound closure time. Wound healing protocols in diabetic ulcers have also gained traction, addressing a rising comorbidity in ageing populations. Emerging neurologic indications, including concussion recovery and mild cognitive impairment, attract R&D spending as researchers probe photobiomodulation’s interaction with brain-derived neurotrophic factor. While early-stage, these investigations set the stage for broader clinical claims that could open fresh revenue corridors for the cold laser therapy market.

By End User: Home-Care Settings Drive Market Transformation

Hospitals generated 39.66% of revenue in 2024 on the back of established procurement cycles and blended reimbursement. They leverage device fleets across inpatient wards, outpatient rehabilitation, and surgical recovery suites. Yet home-care is advancing fastest at 6.14% CAGR as consumer digital literacy climbs and insurers pilot home-based coverage models. Remote patient-monitoring platforms now integrate laser session logs, giving clinicians visibility into adherence. The Mayo Clinic’s ongoing trial evaluating variable frequencies for low-back pain illustrates academic backing for at-home dosing schedules.

Specialty clinics such as sports therapy centers and pain management groups retain steady demand, benefiting from compact device footprints and quick turnover times. Veterinary clinics mirror this dynamic on the animal-health side, frequently purchasing combined laser and ultrasound carts to maximize utilization. Device vendors support veterinary owners through modular subscription models that reduce upfront capital investment. Overall, the expansion of patient-centric care redefines success metrics for suppliers, compelling them to balance clinical-grade robustness with consumer-friendly design without diluting brand credibility in the cold laser therapy market.

Geography Analysis

North America commanded 41.26% cold laser therapy market share in 2024, bolstered by clinician familiarity, CPT coding, and a strong private insurance ecosystem. Growth in the region is now incremental, centering on premium-priced condition-specific devices. Asia-Pacific, by contrast, will progress at a 6.99% CAGR to 2030, reflecting surge demand in Japan, China, South Korea, and India. Demographic ageing, expanding middle-class spending, and public-hospital modernization create fertile conditions for adoption. Manufacturers secure local distribution alliances to navigate country-specific regulatory nuances and language requirements.

Europe remains a steady contributor, aided by universal reimbursement frameworks in Scandinavia and Germany. Sports clubs in Spain and Italy drive visibility in athletic circles, while national health services in the United Kingdom fund pilot laser programs for osteoarthritis. South America lags in absolute size but benefits from inbound medical tourism, particularly in Brazil’s cosmetic surgery clinics. Middle East and Africa show early activity in private orthopedic hospitals catering to expatriate populations, though infrastructural deficits limit swift uptake. Across these regions, incremental payer acceptance, local manufacturing incentives, and culturally specific wellness trends shape the unfolding geography profile of the cold laser therapy market.

Competitive Landscape

A moderately fragmented supplier matrix defines the cold laser therapy industry. No single entity controls a decisive share, yet brand equity remains a differentiator. Erchonia Corporation, THOR Photomedicine, and Enovis collectively anchor the mid-market, each fielding diversified wavelength portfolios to hedge against segment volatility. Multi Radiance Medical carved a niche through its FDA-cleared FibroLux, the first device aimed at fibromyalgia-specific indications, underscoring a shift toward disease-targeted approvals.

Strategic consolidation quickened in 2025. Alcon bought LumiThera to secure the Valeda platform for ophthalmology, signalling that eye-care giants see photobiomodulation as an adjacent growth engine. Enovis acquired LimaCorporate for EUR 800 million, adding orthopedic depth and sales synergies. Boston Scientific’s entry via Bolt Medical laser assets broadens competition beyond traditional pain and rehab into cardiovascular segments.

Technology roadmaps now emphasize quantum hyperlight integration, battery density improvements, and cloud-linked dosage analytics. Suppliers offer software updates that recalibrate pulse widths based on fresh clinical data, prolonging device life cycles and embedding user lock-in. Training ecosystems—including certified practitioner courses—strengthen network effects. Collectively, these strategic plays reinforce a vibrant yet competitive cold laser therapy market where innovation tempo and regulatory agility dictate future leadership.

Cold Laser Therapy Industry Leaders

Erchonia Corporation

THOR Photomedicine Ltd

Enovis

Multi Radiance Medical

Biolase Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Aerolase launched the FDA-cleared Neo Elite skin platform in India with Kaya Clinic, signalling emerging-market expansion.

- April 2025: Acclaro Medical unveiled AuraLux, a cold fiber laser for total skin health at the Medical Spa Show in Las Vegas.

- March 2025: Theralase Technologies reported interim Parkinson’s disease data showing motor and non-motor gains with its TLC-2400 Cool Laser Therapy system.

Global Cold Laser Therapy Market Report Scope

| Hand-held Cold Lasers |

| Desktop & Stand-alone Cold Lasers |

| Class 3B (≤500 mW) |

| Class 4 (>500 mW) |

| Pain Management |

| Wound Healing |

| Dermatology & Aesthetics |

| Veterinary Applications |

| Other Applications |

| Hospitals |

| Specialty Clinics |

| Home-care Settings |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hand-held Cold Lasers | |

| Desktop & Stand-alone Cold Lasers | ||

| By Power Class | Class 3B (≤500 mW) | |

| Class 4 (>500 mW) | ||

| By Application | Pain Management | |

| Wound Healing | ||

| Dermatology & Aesthetics | ||

| Veterinary Applications | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home-care Settings | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current cold laser therapy market size?

The cold laser therapy market size is USD 128.85 million in 2025, with expectations to reach USD 164.24 million by 2030.

Which product category is growing fastest within the cold laser therapy market?

Hand-held devices are advancing at an 8.42% CAGR due to their portability and suitability for home and professional settings.

Why is veterinary application considered a key growth area?

Veterinary laser therapy faces fewer regulatory hurdles, benefits from rising pet-care spending, and shows promising clinical outcomes, resulting in a projected 6.68% CAGR.

How will the new CPT code affect adoption?

The August 2024 CPT code opens a clearer reimbursement pathway, which, once widely implemented, should reduce patient out-of-pocket costs and drive broader clinical uptake.

What regions present the highest future growth potential?

Asia-Pacific is forecast to post a 6.99% CAGR as ageing demographics and healthcare investment converge to accelerate adoption.

Page last updated on: