Global Particle Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

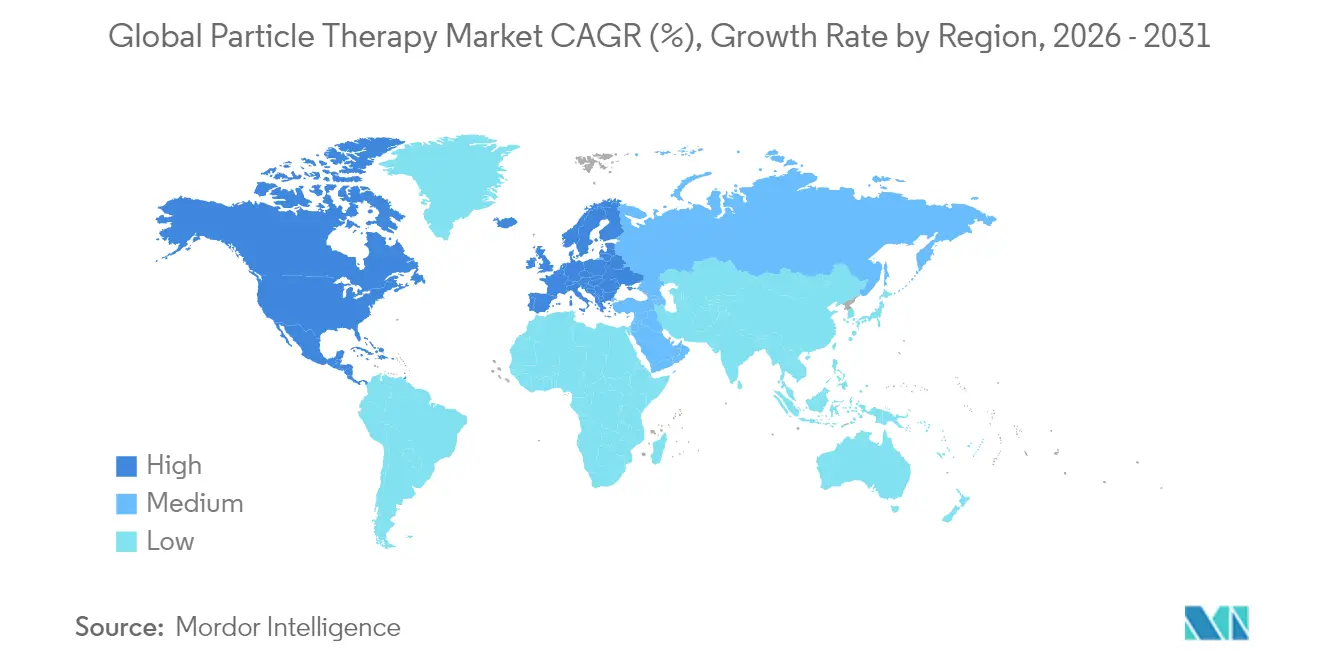

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Particle Therapy Market Analysis by Mordor Intelligence

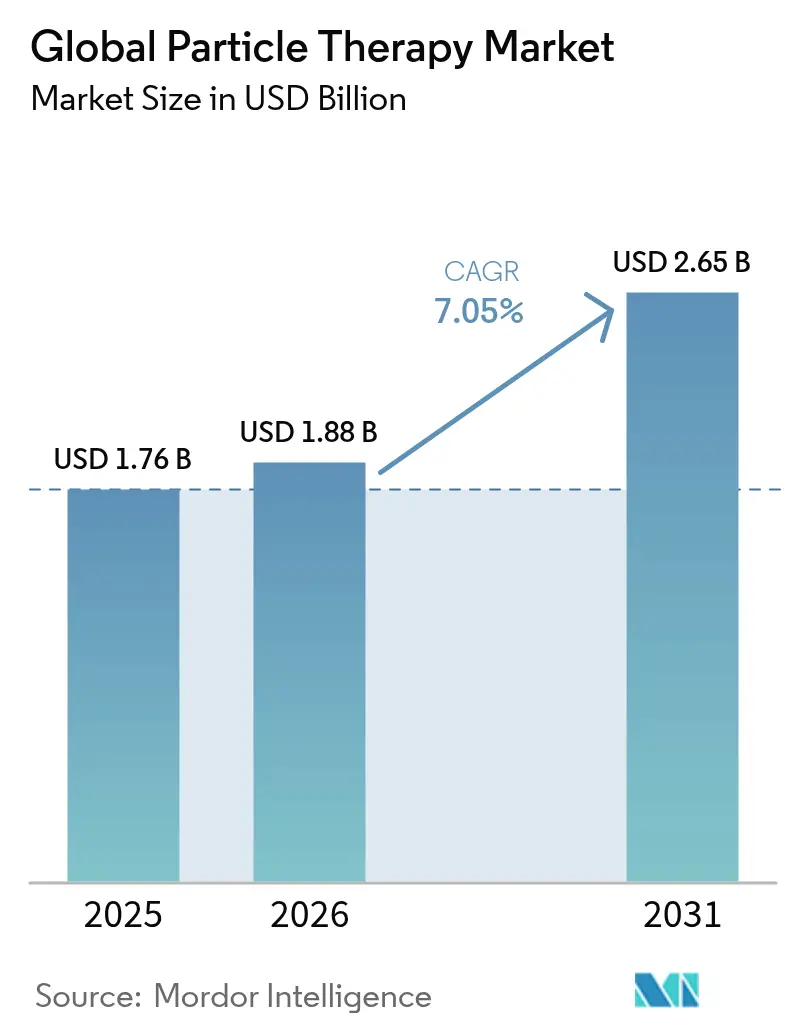

The particle therapy market size is expected to grow from USD 1.76 billion in 2025 to USD 1.88 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at 7.05% CAGR over 2026-2031. The current growth comes from sustained investments in precision oncology equipment, a steady rise in global cancer incidence, and continuous reimbursement improvements that are widening patient eligibility. Vendors are capturing demand through compact single-room systems that trim civil-works budgets by up to 60%, allowing mid-sized hospitals to enter the field without building multi-room bunkers. Clinical momentum behind FLASH-dose delivery is further enlarging the total addressable patient pool, because ultra-high dose rates finish treatment in milliseconds and reduce normal-tissue toxicity, an advantage that resonates with both pediatric and adult cohorts. A supportive policy environment—most notably Medicare’s 2024 local-coverage determinations and Japan’s national insurance listing of carbon-ion therapy—provides near-term revenue certainty, while artificial-intelligence planning tools are easing workflow bottlenecks created by workforce shortages. Collectively, these factors sustain the particle therapy market’s positive outlook and signal that capital formation will stay robust well into the forecast window.

Key Report Takeaways

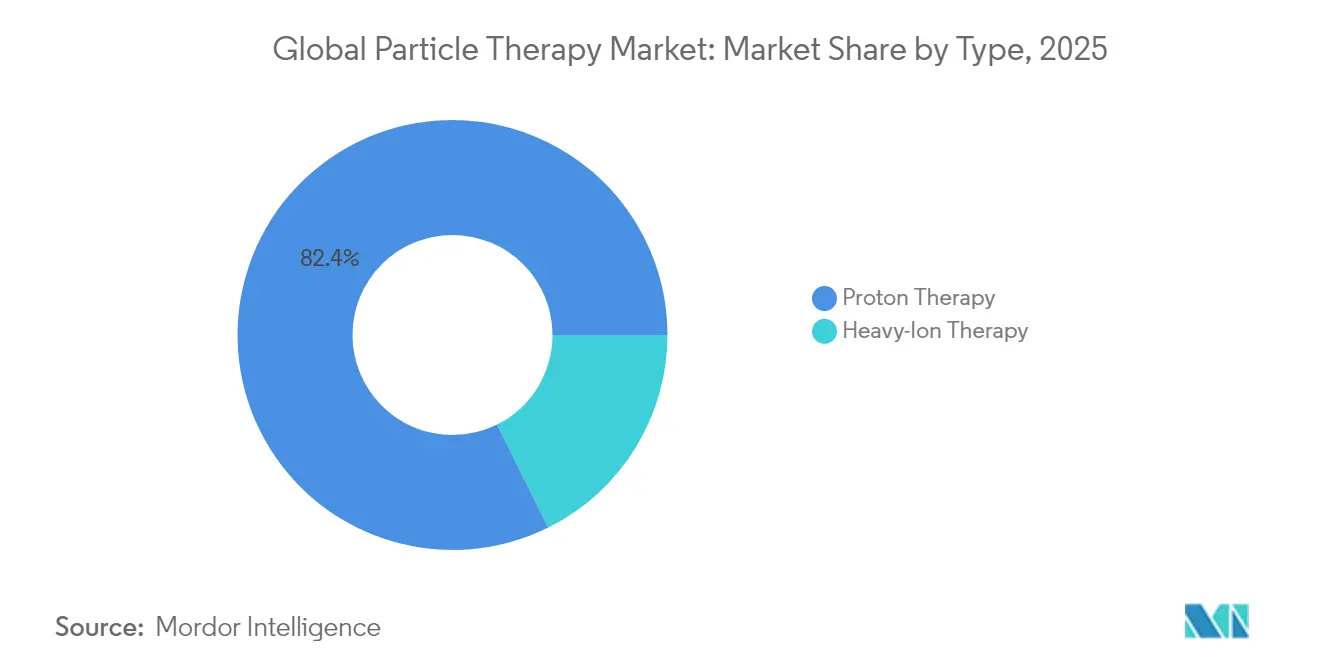

- By type, proton therapy led with 82.35% of particle therapy market share in 2025, whereas heavy-ion therapy is projected to expand at a 7.96% CAGR through 2031.

- By system, multi-room configurations commanded 62.54% share of the particle therapy market size in 2025; single-room systems are advancing at a 7.68% CAGR to 2031.

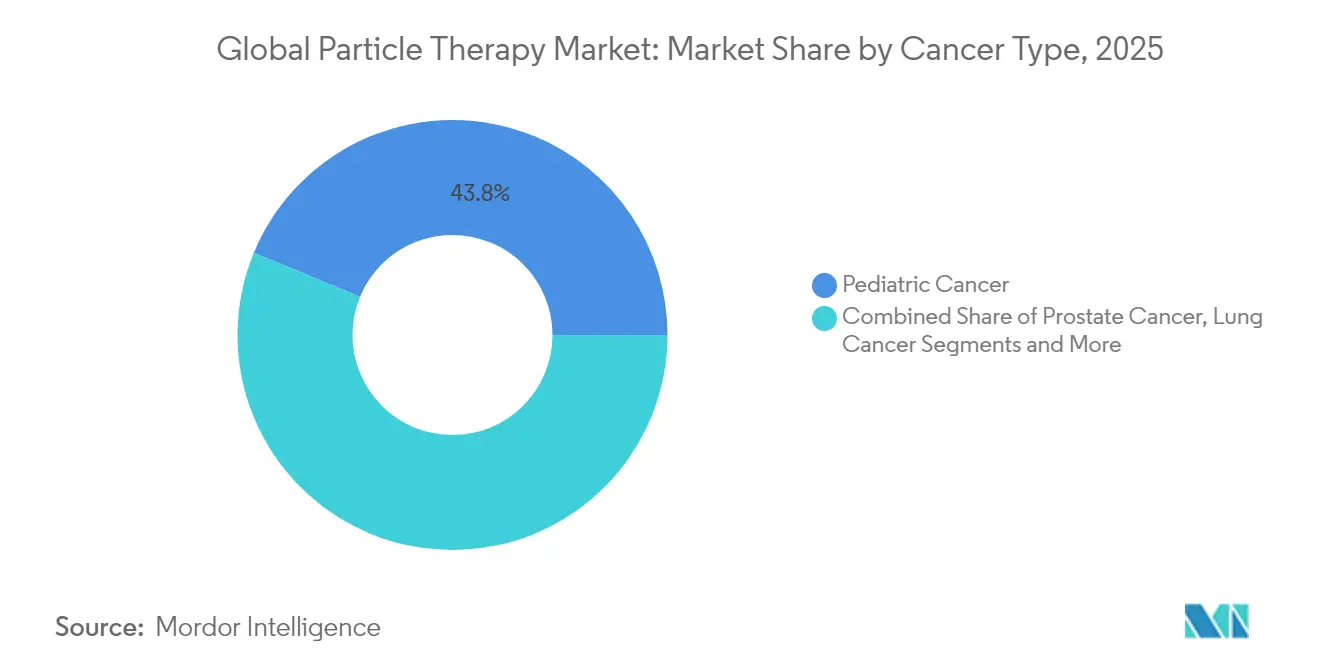

- By cancer type, pediatric indications held 43.75% of the particle therapy market size in 2025; breast cancer applications are set to record an 8.41% CAGR between 2026-2031.

- By geography, North America retained 44.05% particle therapy market share in 2025, while Asia-Pacific is on track for a 9.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Particle Therapy Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in FLASH-dose delivery | +1.2% | Global; early adoption in North America and EU | Medium term (2-4 years) |

| Rising global cancer incidence | +1.8% | Global; pronounced in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Improved reimbursement frameworks (US, JP) | +1.5% | North America and Japan; spill-over into EU | Short term (≤ 2 years) |

| Technological shift to compact systems | +1.0% | Global; faster uptake in cost-sensitive markets | Medium term (2-4 years) |

| AI-based adaptive treatment planning | +0.8% | North America and EU; expanding into Asia-Pacific | Medium term (2-4 years) |

| Public-private proton-center PPP models | +0.7% | Global; highest relevance where capital is constrained | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advances in FLASH-dose Delivery

FLASH radiotherapy delivers dose rates above 40 Gy/s, condensing an entire curative course into a single sub-second exposure that spares surrounding tissue [1]Stanford University Clinical Physics Group, “First-in-Human Proton FLASH Trial Results,” stanford.edu. Pre-clinical and early-phase human studies at Stanford and the University of Pennsylvania report comparable tumor control yet markedly lower fibrosis and dermatitis, supporting broader protocol enrollment. Existing cyclotron lines can integrate FLASH with minimal hardware upgrade, making it a cost-effective differentiator for incumbent hospitals. Regulatory discussions now focus on consensus dose-verification techniques rather than foundational safety, signaling that multi-center trials will soon evolve into guideline-shaping phase III studies. As payers recognize lower toxicity-related complications, value-based reimbursement frameworks are expected to accelerate, reinforcing the driver’s growth contribution.

Rising Global Cancer Incidence

WHO recorded 20 million new cases in 2022 and forecasts 35 million by 2050, a trajectory that intensifies demand for modality portfolios capable of minimizing late-stage side effects. Emerging economies are witnessing faster incidence growth than their healthcare infrastructure can match, magnifying the relevance of portable or retrofittable particle centers. In aging societies like Japan and South Korea, oncologists seek treatments that limit secondary malignancies because survivors often live another two decades. The rise in pediatric cancers, though modest at 0.8% annually in developed regions, carries disproportionately high quality-adjusted life-year (QALY) gains, cementing particle therapy’s value proposition. This epidemiological tide underpins steady patient volume expansion that feeds directly into particle therapy market revenue streams.

Improved Reimbursement Frameworks (US & JP)

CMS broadened proton coverage in 2024, adding select lung, liver and esophageal indications, while preserving medical-necessity safeguards that align payments with peer-reviewed evidence. Japan went a step further by placing carbon-ion therapy on its national insurance schedule, a watershed move that immediately enlarged domestic payer pools. The policy shifts de-risk hospital capital expenditure because revenue per patient becomes more predictable. ASTRO projects a 40–60% jump in eligible U.S. patients within three years, a stretch that effectively lifts capacity-utilization forecasts across newly built systems. Reimbursement certainty shortens payback periods and often serves as the decisive factor for board-level approval of greenfield centers.

Technological Shift to Compact Single-Room Systems

Traditional multi-room vaults cost USD 150–200 million and require massive civil-construction outlays. New single-room platforms, such as Mevion’s S250-FIT and IBA’s Proteus ONE, install inside repurposed linac bays for under USD 50 million and occupy 1/3 the footprint. Engineering advances in superconducting synchro-cyclotrons and dielectric wall accelerators trimmed beamline lengths to less than four meters, allowing gantry rotation without the need for extra-thick concrete. Retrofits, mobile units, and lease-finance contracts now give community hospitals a pathway to offer particle therapy without sinking nine-figure sums. As depreciation schedules shrink and utilization improves, hospital CFOs increasingly secure approval for compact builds, a shift that feeds recurring equipment orders.

AI-based Adaptive Treatment Planning

Deep-learning optimizers generate clinical plans within minutes, rivaling or surpassing human performance while freeing physicists to oversee quality-assurance tasks. GPT-RadPlan, for example, creates proton plans that match human benchmarks on homogeneity while cutting planning time by 90%. Adaptive algorithms that adjust for daily anatomic changes mean fewer margins and more conformal doses, improving organ-at-risk sparing. Vendors bundle AI modules with service contracts, adding high-margin software revenue. In the medium term, AI automation will alleviate staffing bottlenecks and make the particle therapy market more scalable.

Restraints Impact Analysis of Global Particle Therapy Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & OPEX of beamline infrastructure | -2.1% | Global; most acute in price-sensitive regions | Long term (≥ 4 years) |

| Shortage of particle-physics trained staff | -1.4% | Global; shortages pronounced in North America and EU | Medium term (2-4 years) |

| Cyclotron isotope supply bottlenecks | -0.9% | Global; variability across supply-chain resilience zones | Short term (≤ 2 years) |

| Slow regulatory approvals for heavy-ion centers | -0.6% | Primarily emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & OPEX of Beamline Infrastructure

Even after cost reductions, turnkey projects often exceed USD 50 million, dwarfing conventional linac replacement budgets. Shielding, cryogenics, and power-conditioning systems escalate operating costs, with annual service contracts reaching USD 3 million. Hospitals with thin oncology margins struggle to justify these figures unless local payers reimburse at rates that cover both depreciation and service overhead. Because capital grants are finite, a single large particle project can crowd out other equipment purchases, causing institutional inertia. Until vendors unlock sub-USD 20 million systems at scale, capital intensity will remain the most significant drag on the particle therapy market.

Shortage of Particle-Physics Trained Staff

Vacancy rates of 11.3% for medical physicists and 10.7% for radiation therapists illustrate a labor market ill-equipped for rapid center expansion [2]American Society for Radiation Oncology, “Workforce Survey 2024,” astro.org. CAMPEP-accredited residencies graduate fewer candidates than needed to fill retirements, let alone new posts. Workforce scarcity inflates wages by double-digit percentages and slows commissioning timelines because each new vault requires experienced personnel for acceptance, calibration and daily QA. International recruitment compensates but also creates retention risk when visas expire. Automation offers partial relief, yet human oversight remains indispensable, keeping staffing a systemic bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Particle Therapy Market Segment Analysis

By Type:

Proton Therapy Dominance Drives InnovationProton therapy accounted for an 82.35% particle therapy market share in 2025, buoyed by a robust base of phase III evidence, payer familiarity and a pipeline of single-room installations. Heavy-ion therapy is the fastest mover, growing at 7.96% CAGR to 2031 on the back of superior relative biological effectiveness against hypoxic or radioresistant tumors. Early adopters such as Yonsei Cancer Center reported five-year overall survival of 97.5% in localized prostate protocols, results that transcend proton benchmarks. North American acceptance could accelerate once Mayo Clinic’s forthcoming carbon-ion unit enters service, creating spill-over demand for heavy-ion expertise within the particle therapy market. As compact carbon-ion platforms mature, the economic barrier narrows, signaling a more balanced modality mix beyond 2030.

Proton vendors have not remained static. Systems incorporating FLASH capability, intensity-modulated scanning and AI-enabled daily replanning continue to widen the clinical ceiling. Meanwhile, carbon-ion innovators are integrating superconducting gantries to cut magnet mass and facility span. Technology cross-pollination is expected, with proton platforms adopting heavy-ion beam-steering algorithms and heavy-ion systems leveraging proton-era QA automation. The competitive interplay keeps the particle therapy market dynamic and favors suppliers who maintain a multi-modality portfolio.

By System:

Single-Room Configurations Gain MomentumMulti-room centers held 62.54% share of the particle therapy market size in 2025 because legacy hubs treat 1,000+ patients yearly and benefit from economies of scale. However, single-room footprints are climbing 7.68% CAGR as CFOs prioritize modular expansion over mega-projects. Facilities like Atlantic Health’s retrofit of an existing linac vault—notably completed 40% faster than a greenfield build—prove the model’s economic appeal. The newest compact units operate with independent cyclotrons per room, so downtime in one suite no longer halts the entire complex, a historical disadvantage of beam-switching designs.

On the engineering front, magnet miniaturization and improved energy selection systems allow single-room solutions to match the clinical reach of their larger cousins, eliminating trade-off concerns. Vendors market phased build-outs that start with one vault and scale to three or four as case volume rises, giving administrators capital-spend optionality. As leasing and public-private partnerships mature, single-room growth is expected to outstrip multi-room additions, reinforcing the decentralizing trend within the particle therapy market.

By Cancer Type:

Pediatric Applications Lead, Breast Cancer AcceleratesPediatric cases retained 43.75% of the particle therapy market size in 2025 due to the modality’s unrivaled capacity to spare growth plates, ocular structures and developing CNS tissue. Multidisciplinary boards now routinely recommend proton or carbon-ion therapy for medulloblastoma and rhabdomyosarcoma, citing lower risk of neurocognitive decline. Breast cancer is emerging as the fastest grower at 8.41% CAGR, driven by phase II data that show reduced cardiopulmonary dose compared with IMRT. National coverage determinations in the US already list left-sided post-mastectomy proton therapy for women with pre-existing cardiac comorbidities, broadening the addressable cohort.

Prostate cancer, once the marquee indication, is transitioning into a second-line growth driver as competition from advanced photon techniques rebalances referral patterns. Nevertheless, daily CBCT and deformable registration workflows make proton treatment more adaptive, preserving its value in select risk groups. Elsewhere, lung, liver and pancreas studies combining FLASH and image guidance are enhancing tumor-control probabilities, paving the way for indication diversification that stabilizes revenue streams for the particle therapy market.

By Application:

Treatment Dominance, Research ExpansionDirect patient treatment comprised 67.85% of revenue in 2025 as the modality shifted firmly into routine clinical practice for several tumor classes. Research usage, however, is gaining 7.89% CAGR as investigators probe biology-based planning metrics, FLASH fractionation and immuno-radiotherapy synergies. Government-funded consortia, such as Europe’s ARCHADE program, are pooling carbon-ion data sets to fast-track regulatory labeling. Academic centers that anchor multi-room complexes often reserve one suite for protocol enrollment, ensuring bench-to-bedside feedback loops that accelerate innovation. Software-defined accelerators with variable-energy extraction facilitate pre-clinical experiments during off-patient hours, monetizing idle capacity while enlarging the knowledge base that ultimately expands the particle therapy market.

Research emphasis also extends to physics instrumentation. Prompt-gamma detection for real-time range verification and machine-learning beam monitors are closing the loop on intra-fraction uncertainty. Commercial vendors partner with universities to co-develop these add-ons, bundling them into future upgrade packages that raise after-sales revenue.

Geography Analysis

North America Particle Therapy Market

North America controlled 44.05% of the particle therapy market in 2025. Medicare’s broadened coverage stabilized cash flows, and an established pipeline of more than 40 operational centers continues to undertake multi-room expansions. Penn Medicine’s USD 224 million Roberts Proton Therapy Center extension illustrates the region’s willingness to invest in next-generation vaults that include independent cyclotrons for redundancy. Academic ecosystems funnel steady referral streams, while philanthropic campaigns absorb portions of capital costs, mitigating budget risk. The United States also houses most commercial OEM headquarters and third-party service firms, reinforcing supply-chain security. Canada remains an outlier with no domestic center, but provincial task forces in Ontario and Quebec have advanced site-selection studies, a sign that regional demand will soon convert into procurement tenders.

APAC Particle Therapy Market

Asia-Pacific is the fastest-growing region at 9.02% CAGR, fueled by public-sector spending and demographic shifts toward older populations. China hosts an expanding mix of flagship institutions and cost-disruptive entrants. P-Cure’s ultra-compact system in Shandong, priced below USD 30 million, exemplifies a local strategy to bring particle therapy into secondary cities . South Korea commissioned the Yonsei heavy-ion facility in 2024, and preliminary data already support broader case enrollment beyond prostate cancer. Australia’s Bragg Centre, though facing vendor realignment after delays, retains bipartisan commitment, indicating that regulatory approvals are temporary rather than structural obstacles. Regional governments often pair accelerator procurement with domestic-manufacturing mandates, stimulating supply-chain localization that lowers long-term operating expenditures.

EMEA and South America Particle Therapy Market

Europe presents a dual narrative of technological sophistication and incremental capacity growth. Germany’s carbon-ion centers deliver both routine care and multi-site trial leadership, positioning the region as a global hub for heavy-ion expertise. Public-private joint ventures in France and Italy are expanding proton reach, while MRI-guided proton prototypes in Dresden edge toward clinical readiness. Cross-border referral agreements allow smaller nations to send complex cases to neighboring centers, optimizing utilization. Meanwhile, the Middle East, Africa and South America hold early-stage potential. Argentina’s 230-tonne cyclotron installation signals Latin America’s first foray into the particle therapy market, and preliminary feasibility studies are underway in Saudi Arabia and the United Arab Emirates. Collectively, geographic diversification spreads supplier risk and creates multi-tier demand profiles that sustain long-run growth.

Competitive Landscape

The particle therapy market remains moderately concentrated. IBA led revenue with EUR 498.2 million in 2024 and a backlog topping EUR 1.5 billion, anchored by its end-to-end offering of cyclotrons, treatment rooms and radiopharma lines. Siemens Healthineers, following its Varian acquisition, integrates diagnostics, imaging and therapy into an AI-rich platform that targets EUR 300 million in annual synergies by fiscal 2025. Hitachi and Sumitomo Heavy Industries hold regional strongholds across Asia-Pacific, leveraging superconducting beamline patents and turnkey hospital partnerships to defend share.

Mevion Medical Systems differentiates on compactness, with its S250-FIT unit enabling vault retrofits that reduce construction timelines by half. The company’s modular roadmap lets facilities add rooms without downtime, a critical selling point for community hospitals with tight cash-flow constraints. Disruptors such as P-Cure push the cost envelope further, marketing sub-USD 30 million setups that employ patient-seated geometry to shrink gantry weight. Lawrence Livermore’s dielectric wall accelerator is on a path toward regulatory clearance, aiming at sub-USD 20 million price points that could reset the market equilibrium.

Strategic moves center on joint-development agreements, AI software acquisitions and service-level differentiation. Siemens Healthineers added remote QA support using digital twins, cutting downtime by 15%. IBA partnered with RaySearch to embed biological-effect optimization into its TPS suite, fortifying clinical outcomes. Venture funding flows into start-ups that specialize in prompt-gamma imaging or automated plan-verification engines, technologies that incumbent OEMs may eventually acquire to sustain value-chain control. The competitive stakes therefore revolve around breadth of ecosystem rather than single hardware advantages.

Global Particle Therapy Industry Leaders

Hitachi, Ltd.

IBA

Siemens Healthcare GmbH (Varian Medical Systems, Inc.)

Sumitomo Heavy Industries, Ltd.

Mevion Medical Systems.

- *Disclaimer: Major Players sorted in no particular order

Global Particle Therapy Market Companies Covered in this Report

- Abbvie

- Amneal Pharmaceuticals

- Viatris

- Boehringer Ingelheim Intl. GmbH

- GlaxoSmithKline

- Teva Pharmaceutical Industries

- Pfizer

- Novartis

- Roche

- ABL bio

- KISSEI PHARMACEUTICAL

- AstraZeneca

- Prevail Therapeutics

- Newron Pharmaceuticals S.p.A.

- Kyowa Kirin

- ACADIA Pharmaceuticals Inc.

- UCB

- Sunovion Pharmaceuticals

- Neurocrine Biosciences

- Lundbeck A/S

- Voyager Therapeutics, Inc.

- Supernus Pharmaceuticals

Recent Industry Developments in Global Particle Therapy Market

- January 2024: OncoRay launched the world’s first research prototype for full-body MRI-guided proton therapy that offers real-time tumor tracking.

- October 2023: Hitachi delivered a proton therapy system to the National Cancer Centre Singapore, marking the vendor’s entry into Southeast Asia.

- September 2023: Siemens Healthineers (Varian) showcased its latest particle therapy technologies at the ASTRO 2023 annual meeting in San Diego.

Global Particle Therapy Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the particle therapy market as the aggregate annual revenue from proton and heavy-ion beam systems, the accelerators that power them, planning software, treatment accessories, and long-term service contracts booked by hospitals or dedicated oncology centers worldwide. The definition spans both multi-room and compact single-room layouts that deliver clinically approved external-beam treatments for solid tumors.

Scope exclusion: Photon linear accelerators, brachytherapy sources, and research-only FLASH prototypes are left outside this study.

Segments Covered in This Report

- By Mechanism of Action

- Dopamine Agonists

- Anticholinergics

- MAO-B Inhibitors

- Amantadine

- Carbidopa-levodopa

- Adenosine A2A Antagonists

- Other Mechanisms of Action

- By Route of Administration

- Oral

- Transdermal

- Subcutaneous

- Infusion

- Intranasal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed radiation oncologists, medical physicists, hospital procurement leads, and accelerator manufacturers across North America, Europe, and Asia-Pacific. Their guidance verified typical system prices, commissioning timelines, and real-world patient throughput, filling gaps that documents alone cannot close before we triangulate the final estimates.

Desk Research

Our analysts began with authoritative public datasets such as the WHO / IARC GLOBOCAN cancer incidence files, SEER registries, and OECD Health expenditure tables, which anchor patient pools and spending capacity. Supplementary insights were drawn from the Particle Therapy Co-Operative Group facility database, U.S. Medicare fee schedules, and peer-reviewed journals that report dose-outcome evidence for protons and carbon ions. Company filings, investor decks, and procurement tenders located through D&B Hoovers, Dow Jones Factiva, and Global Security then helped price current installations and map fresh orders. The desk work concluded with patent activity mined through Questel to gauge pipeline technology. These sources illustrate, not exhaust, the wide body of material screened for facts and cross-checks.

Market-Sizing & Forecasting

A top-down cancer-incidence build was first prepared, linking site-specific prevalence to the share clinically eligible for particle therapy and to current penetration rates. Results were corroborated with selective bottom-up roll-ups of installed centers, average selling price, and annual capacity utilization. Key inputs include new cancer cases, reimbursement approvals, pipeline center openings, average system ASP shifts, oncology workforce growth, and carbon-ion trial enrollment. Forecasts to 2030 rely on multivariate regression that weights those variables and adjusts for macroeconomic swings flagged by our expert panel. Where bottom-up data were partial, gaps were interpolated using regional benchmark ratios validated during interviews.

Data Validation & Update Cycle

Outputs pass a multi-layer review: automated variance scans, peer checks by a second analyst, and senior oversight before sign-off. The model is refreshed every twelve months, with mid-cycle revisions triggered by material events such as major regulatory approvals or facility launches. Clients therefore receive the latest view, not stale numbers.

How Mordor Intelligence's Global Particle Therapy Market Size Compares to Other Published Estimates

Published figures seldom align because publishers pick different scopes, cost elements, and refresh cadences.

We acknowledge that landscape and show below how scope rigor makes our baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.76 Bn (2025) | Mordor Intelligence | - |

| USD 1.64 Bn (2024) | Regional Consultancy A | Omits service revenues and counts fewer geographies |

| USD 0.70 Bn (2023) | Trade Journal B | Excludes heavy-ion therapy; relies on installed-base tally alone |

| USD 1.01 Bn (2024) | Industry Association C | Uses voluntary site surveys with unverified ASP assumptions |

Differences arise chiefly from what is counted and how often estimates are refreshed. By grounding our model in transparent variables, documented sources, and annual updates, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current Global Particle Therapy Market size?

The particle therapy market size is USD 1.88 billion in 2026, with revenue expected to grow to USD 2.65 billion by 2031 at a 7.05% CAGR.

Who are the key players in Global Particle Therapy Market?

Hitachi, Ltd., IBA, Siemens Healthcare GmbH (Varian Medical Systems, Inc.), Sumitomo Heavy Industries, Ltd. and Mevion Medical Systems. are the major companies operating in the Global Particle Therapy Market.

Which modality holds the largest particle therapy market share?

Proton therapy holds the largest share at 82.35% in 2025, reflecting its established clinical adoption and broad reimbursement coverage.

Which region has the biggest share in Global Particle Therapy Market?

In 2025, the North America accounts for the largest market share in Global Particle Therapy Market.

Page last updated on: