Medical Laser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

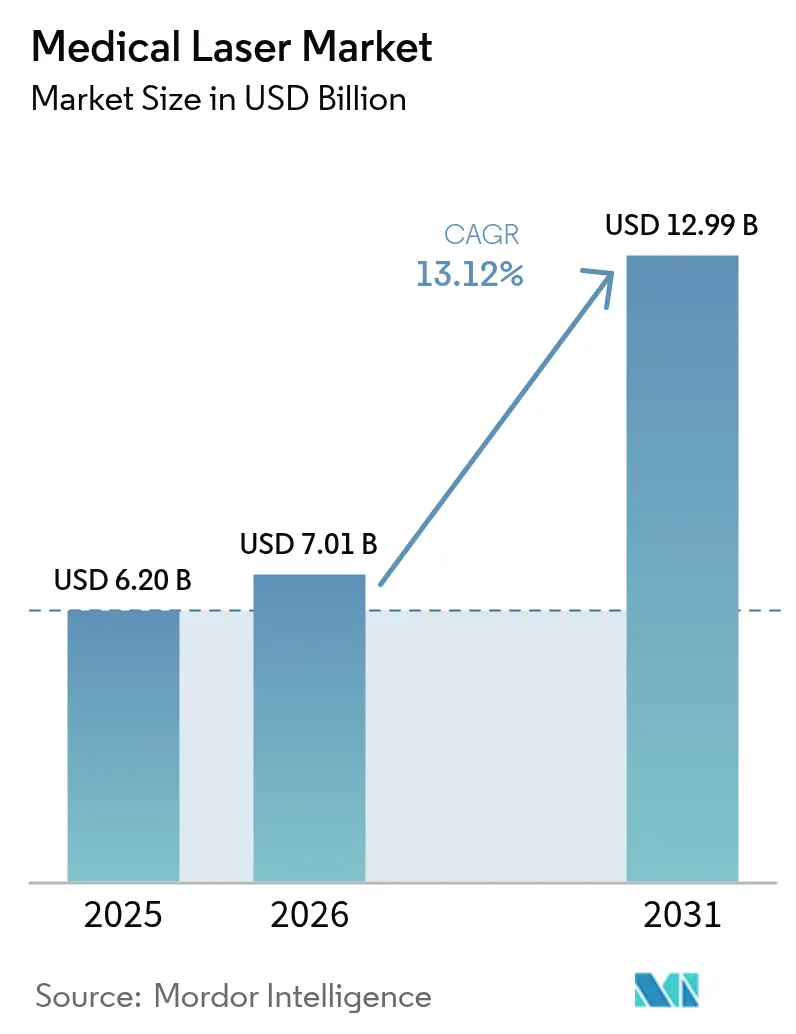

| Market Size (2026) | USD 7.01 Billion |

| Market Size (2031) | USD 12.99 Billion |

| Growth Rate (2026 - 2031) | 13.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

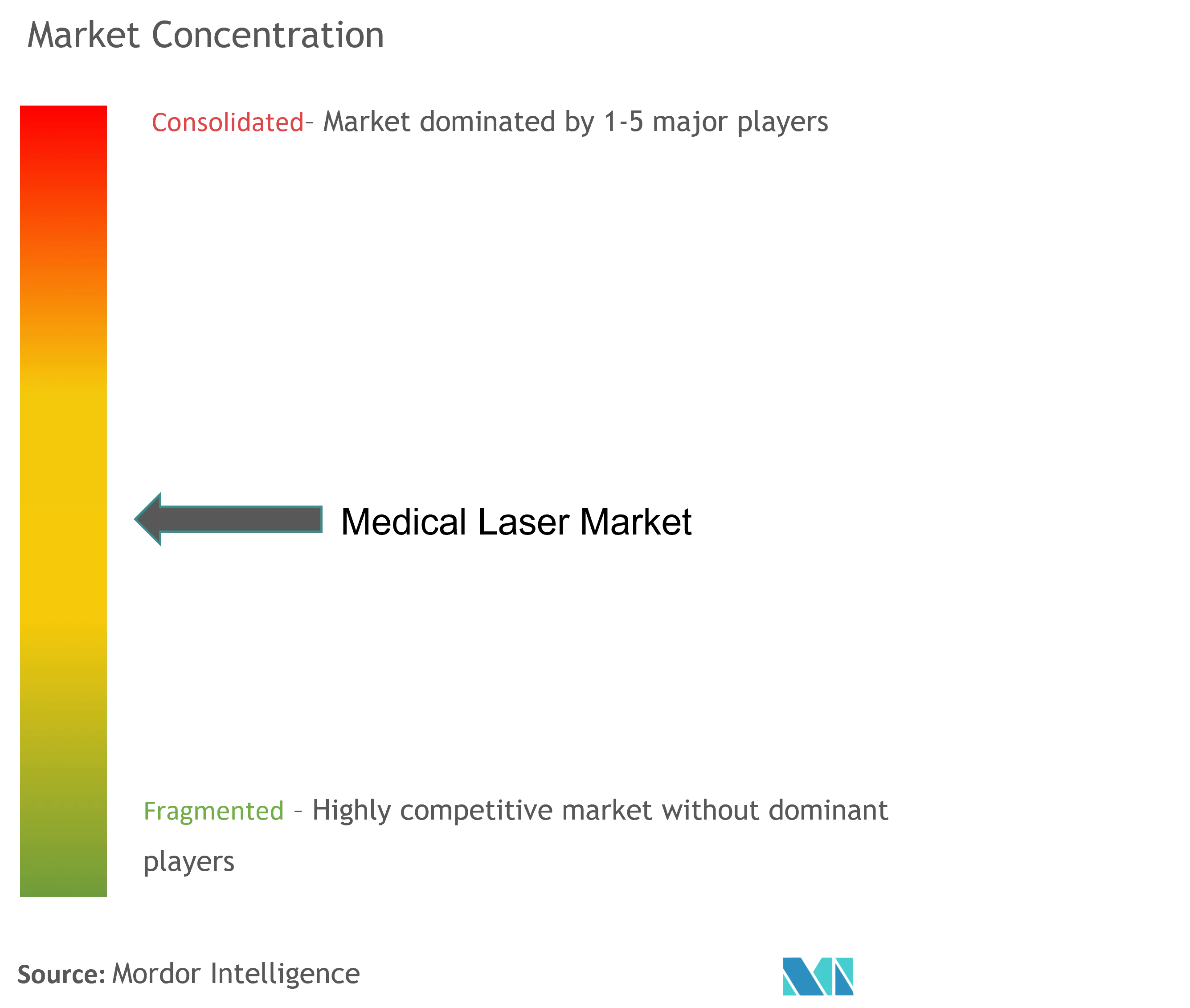

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Laser Market Analysis by Mordor Intelligence

The medical laser market size is expected to grow from USD 6.20 billion in 2025 to USD 7.01 billion in 2026 and is forecast to reach USD 12.99 billion by 2031 at 13.12% CAGR over 2026-2031. This growth rests on aging populations that push ophthalmic and aesthetic procedure volumes, efficiency gains in solid-state and diode platforms, and payers’ preference for outpatient care that relies on laser-based interventions. A steady rise in specialty clinics, technological upgrades in diode efficiency, and regulatory approvals for new indications such as photobiomodulation keep demand strong despite supply-chain risks tied to rare-earth export restrictions. Competitive intensity is moderate but rising as leaders acquire niche players to secure femtosecond, photobiomodulation, and AI-enabled capabilities. Cybersecurity gaps in networked systems and capital cost pressures remain challenges, yet procedure migration to ambulatory surgery centers sustains the medical laser market’s positive outlook.

Key Report Takeaways

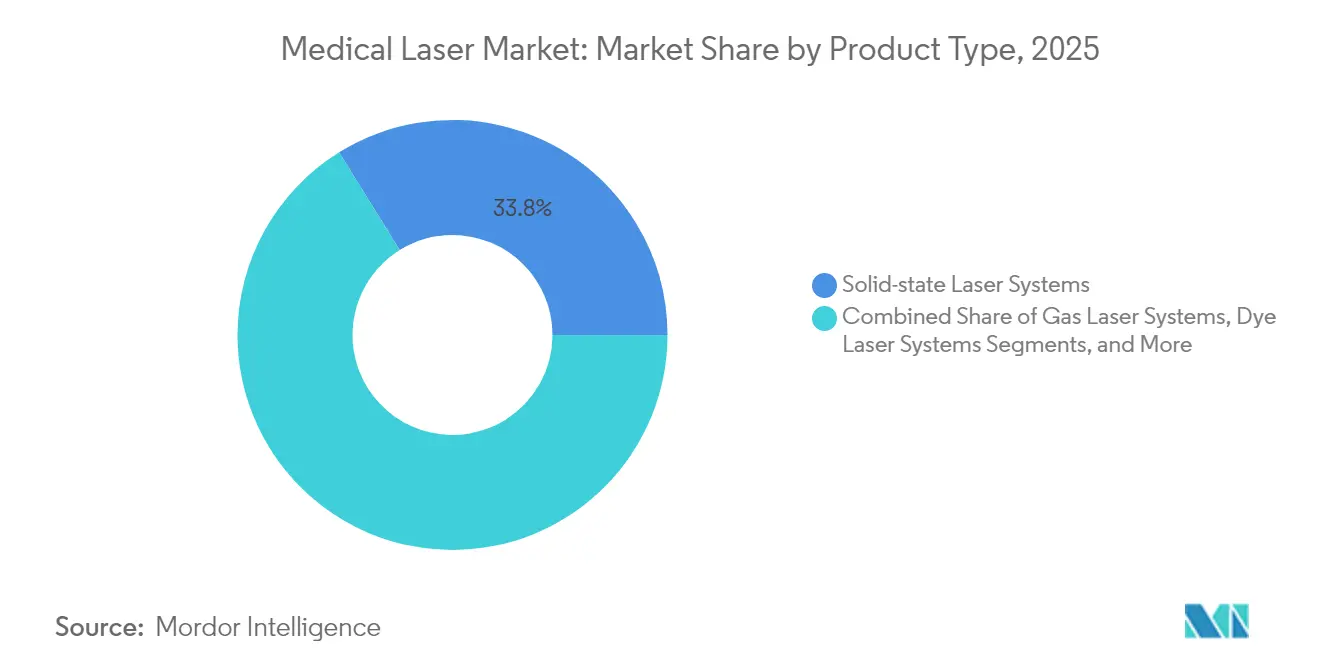

- By product type, solid-state laser systems led with 33.84% revenue share in 2025, while diode semiconductor systems are projected to expand at a 14.03% CAGR through 2031.

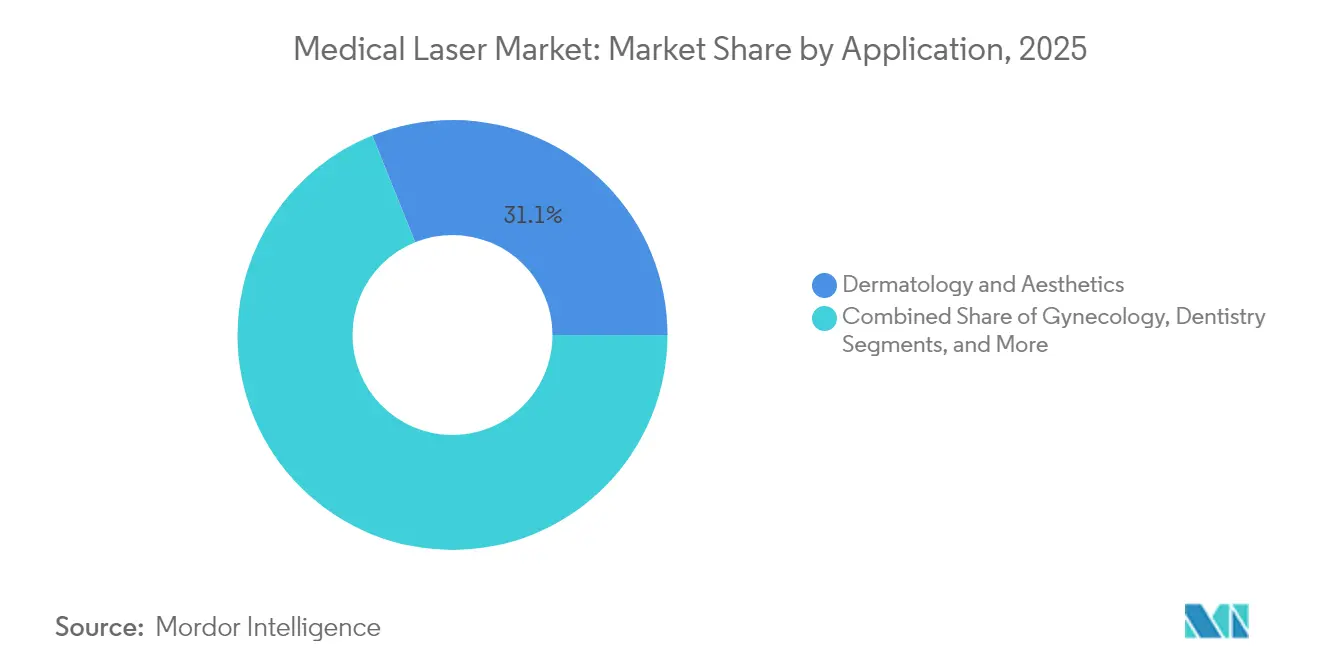

- By application, dermatology and aesthetics held 31.09% of medical laser market share in 2025; ophthalmology is set to grow at a 13.69% CAGR to 2031.

- By end user, hospitals maintained 44.62% share of the medical laser market size in 2025, whereas specialty and aesthetic clinics are advancing at a 13.54% CAGR.

- By geography, North America captured 41.11% of revenue in 2025; Asia-Pacific records the fastest growth at a 14.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Laser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for minimally-invasive procedures | +2.8% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Increasing burden of eye disorders | +2.1% | Global, particularly Asia-Pacific aging populations | Long term (≥ 4 years) |

| Growing demand for aesthetic & cosmetic laser treatments | +1.9% | North America & Europe core, expanding to APAC | Short term (≤ 2 years) |

| Technological advances in solid-state & diode platforms | +1.7% | Global, led by innovation centers in US, Germany, Japan | Medium term (2-4 years) |

| AI-enabled auto-calibration & beam-shaping software adoption | +1.4% | North America & Europe early adopters, APAC following | Long term (≥ 4 years) |

| Expansion of outpatient laser suites in retail-clinic chains | +1.2% | North America primarily, selective European markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Minimally-Invasive Procedures

Ambulatory surgery centers now conduct 72% of all US surgeries, cutting facility costs by 45–60% and accelerating the shift toward laser techniques that shorten recovery times [1]Cameron Cortigiano, “ASC Procedure Volumes Surging,” Becker’s ASC Review, beckersasc.com. Femtosecond systems such as Alcon’s Unity VCS reduce phacoemulsification energy, improving safety and operating-room turnover. High patient-satisfaction scores—92% in outpatient settings—reinforce demand, compelling providers to adopt laser platforms or risk losing volume to more agile competitors. As reimbursement models move toward bundled payments, clinicians favor modalities that lower complications and readmissions, giving the medical laser market sustained momentum. Expansion of retail-clinic chains further democratizes access, allowing routine skin and eye procedures to migrate away from hospitals.

Increasing Burden of Eye Disorders

Glaucoma incidence in the US is projected to climb from 5 million in 2025 to 6.3 million by 2050, raising procedure volumes for trabeculoplasty and cataract surgery. The FDA clearance of LumiThera’s Valeda photobiomodulation platform marked the first approved treatment for dry age-related macular degeneration, with 58% of treated eyes gaining ≥5 letters over 24 months. Asia-Pacific faces parallel pressure from diabetic retinopathy tied to lifestyle shifts, sustaining investment in diode and solid-state ophthalmic lasers. These dynamics keep the medical laser market firmly aligned with precision-medicine priorities despite budget constraints.

Growing Demand for Aesthetic & Cosmetic Laser Treatments

The FDA clearance of Accure’s 1726 nm laser for long-term acne therapy achieved a 70% lesion reduction after four sessions, opening new cash-pay revenue streams. Fractional CO₂ and intradermal systems such as MIRIA’s Focal Point line now treat darker skin with fewer adverse events. Social-media influence fosters preventive aesthetics among younger consumers, diversifying demand beyond traditional middle-age cohorts. Because cosmetic procedures are self-funded, they insulate manufacturers from reimbursement volatility, reinforcing the medical laser market during macroeconomic swings.

Technological Advances in Solid-State & Diode Platforms

Vertical-cavity surface-emitting lasers achieved 74% electro-optical efficiency at room temperature, slashing power consumption for surgical systems. Coherent’s 220 W FACTOR diode pumps expand deep-tissue applications in compact footprints. Novel 445 nm diodes offer superior hemoglobin absorption for precise cutting with minimal thermal spread [2]Zhaoqun Liu, “Technical Characterization of a High-Power Diode Laser at 445 nm for Medical Applications: From Continuous Wave Down to Pulse Durations in the µs-Range,” Applied Sciences, mdpi.com. These innovations heighten competitiveness and drive substitution toward diode platforms, reinforcing the medical laser market’s technology cycle.

AI-Enabled Auto-Calibration & Beam-Shaping Software Adoption

Machine-learning algorithms now adjust pulse parameters in real time, cutting intra-operator variability and enabling consistent outcomes. Flow-cytometry alignment studies report sub-micron accuracy, reducing setup time and operator fatigue. Autonomous beam-shaping extends device life by mitigating component stress, although high software-validation costs restrict near-term deployment to premium systems. As clinicians gain confidence, AI will act as a force multiplier, boosting throughput and underpinning the medical laser market’s value proposition.

Expansion of Outpatient Laser Suites in Retail-Clinic Chains

ASC procedure volumes are forecast to rise 25% between 2025 and 2029, with laser-based interventions a leading contributor. Retail brands invest in diode platforms for hair removal and skin tightening, aiming to capture high-margin services. The model offers same-day care in convenient locations, aligning with consumer expectations of immediacy. However, decentralized sites require standardized safety protocols and tele-supervision to mitigate operator-skill variability, placing operational demands on manufacturers and regulators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | -1.8% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Stringent safety & operator-training regulations | -1.2% | North America & Europe primarily, expanding globally | Long term (≥ 4 years) |

| Rare-earth material shortages for diode pump modules | -0.9% | Global supply chain impact, Asia manufacturing centers | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in networked laser systems | -0.7% | Developed markets with networked infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Costs

Femtosecond cataract platforms carry USD 400,000–500,000 price tags, plus per-use fees of USD 300–400, stretching budgets in smaller practices. Excimer systems range from USD 24,011 to USD 198,000, while annual maintenance averages 3.13% of purchase value, with labor forming two-thirds of expense. Leasing eases cash flow but boosts lifetime cost, limiting uptake in emerging economies and tempering overall medical laser market growth.

Stringent Safety & Operator-Training Regulations

ANSI Z136.3 mandates medical-laser safety officers and periodic recertification, adding indirect expense. FDA 21 CFR 1040.10 requires key switches, interlocks, and visual indicators for Class 3B/4 devices. Europe’s MDR increases technical-documentation requirements; 50% of firms expect to trim product lines to manage compliance costs. Compliance complexity lengthens time-to-market and discourages smaller entrants, affecting medical laser industry competitiveness.

Rare-Earth Material Shortages for Diode Pump Modules

China’s export restrictions on gallium and germanium—key diode materials—have inflated input costs by 75% since 2023. Manufacturers diversify sourcing but face longer lead times and higher inventory requirements, pressuring margins. Some vendors explore alternative semiconductor chemistries, yet qualification cycles are long, leaving the medical laser market exposed to supply shocks over the next two years.

Cyber-Security Vulnerabilities in Networked Laser Systems

Twenty percent of healthcare organizations reported at least one device-related cybersecurity incident in the past year, with connected lasers identified as threat vectors. Ransomware targeting equipment downtime jeopardizes elective surgery schedules and can force costly manual workarounds. Vendors now embed secure boot and network segmentation features, but patch-management lag remains a systemic risk that could erode buyer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diode Systems Drive Innovation Despite Solid-State Dominance

Solid-state platforms controlled 33.84% of revenue in 2025, validating their reliability for high-power cutting and coagulation. Yet diode systems are projected to post a 14.03% CAGR, the fastest within the medical laser market, as 445 nm and 880 nm variants reach performance parity with bulkier designs. The medical laser market size for diode devices is forecast to expand notably as portable handpieces support office-based surgery and aesthetics.

Diodes benefit from lower cooling demands, allowing battery-powered options that fit tele-dermatology and mobile ophthalmology clinics. Gas and dye lasers hold niche positions for ultraviolet treatments and vascular lesions where narrow lines are paramount. Supply-chain constraints in rare-earths may temper diode adoption briefly; however, efficiency gains and factory-scale production give diodes a long-term cost edge in the medical laser market.

By End User: Specialty Clinics Surge as Hospitals Maintain Volume Leadership

Hospitals represented 44.62% of total 2025 placements, reflecting large-case complexity and integrated reimbursement workflows. Conversely, specialty and aesthetic clinics are projected to grow 13.54% annually, accounting for expanding outpatient volumes as patients favor convenience and transparent pricing. In 2024 alone, 72% of US surgeries occurred in non-hospital settings, indicating a durable shift in medical laser market share toward clinics.

Ambulatory centers leverage diodes’ compact footprint to run multiple rooms on single utilities, while hospitals prioritize solid-state platforms for high-acuity care. Academic institutes retain modest demand for trial work but drive innovation pipelines that ultimately feed commercial use, underscoring a virtuous R&D loop within the broader medical laser industry.

By Application: Ophthalmology Acceleration Challenges Dermatology Leadership

Dermatology and aesthetics delivered 31.09% of 2025 revenue, fueled by social-media-driven demand for scar revision and skin resurfacing. Ophthalmology, though smaller, is slated to outpace all other segments with a 13.69% CAGR, enlarging its share of the medical laser market size as dry-AMD and presbyopia therapies reach clinics. Hospitals and vision centers integrate photobiomodulation suites next to existing refractive lasers, boosting procedural cross-selling.

Beyond eyes and skin, urology, gynecology, and dentistry lift unit sales by leveraging diode flexibility in hemoglobin-rich tissue interactions. The adoption of 1940 nm lasers for vein ablation underscores how wavelength tailoring expands indications, illustrating the breadth of clinical opportunity within the medical laser market.

Geography Analysis

North America held 41.11% of the medical laser market in 2025, underpinned by robust reimbursement pathways and a dense ASC network. Alcon’s rapid roll-out of the Voyager DSLT, which delivers 120 pulses without a gonio lens, typifies the region’s first-mover culture. Canada mirrors US trends, albeit with tighter capital cycles that favor lease models.

Europe remains stable, balancing innovation with MDR-driven cost burdens. Carl Zeiss Meditec posted 17.1% revenue growth in EMEA in early 2025, buoyed by refractive-surgery consumables [3]Alcon, “Unity VCS Product Overview,” alcon.com. However, extended certification timelines may constrain smaller vendors, potentially consolidating the medical laser market around established brands.

Asia-Pacific is the fastest-growing arena at a 14.31% CAGR. China’s 10.2% 2024 laser-sector growth reflects public-hospital overhauls and rising aesthetic demand. Japan and South Korea deploy AI-enhanced excimer systems, while India advances through public-private ophthalmology hubs. ASEAN nations, though infrastructure-limited, attract medical tourism, adding volume to regional medical laser market size. Currency volatility and import duties remain hurdles, but demographic momentum signals sustained expansion.

Regulatory Landscape

Medical lasers are handled as both medical devices and radiation-emitting electronic products in major markets. In the United States, manufacturers must meet FDA medical device requirements under the Federal Food, Drug, and Cosmetic Act and also comply with radiological health controls under 21 CFR 1040.10 for laser product performance, including interlocks, indicators, and other safety features for higher-class devices. These dual requirements influence design controls, labeling, and postmarket obligations for Class 3B/4 surgical and therapeutic systems.

In Europe, compliance is increasingly tied to EU MDR (Regulation (EU) 2017/745) and harmonized standards that support presumption of conformity. EN IEC 60601-2-22:2020/A11:2026 sets updated particular requirements for basic safety and essential performance of surgical, cosmetic, therapeutic, and diagnostic laser equipment, and it explicitly links to MDR General Safety and Performance Requirements through Annex mappings. In June 2026, the European Commission published Implementing Decision (EU) 2026/1231 to update the MDR harmonized standards list, reinforcing the need to keep technical documentation and labeling symbol conventions aligned with current standards.

Value Chain Analysis

The medical laser value chain begins with specialized upstream inputs, including high-power laser diodes, laser gain media (for example, Nd:YAG and Ho:YAG crystals), and precision optics and fibers (including materials such as germanium and zinc selenide for certain optical assemblies). These components then move into clean-room module assembly, covering pump modules, resonators, beam delivery, and fiber assemblies, before progressing to system-level integration. At this stage, OEMs combine optics with power electronics, control software, cooling, and mechanical beam-steering assemblies to deliver clinical platforms.

On the downstream side, distribution and adoption depend on service coverage, installation qualification, and user training, given the calibration sensitivity and uptime expectations across ophthalmic, dermatology, and surgical systems. The chain includes vertically integrated players (for example, biolitec Group expanding fiber-related capabilities into laser systems) and specialist suppliers and distributors (including CeramOptec for OEM fiber assemblies and Frankfurt Laser Company for distribution), alongside contract manufacturers that support precision processing. Compliance and testing against IEC 60601-2-22, along with associated FDA-recognized consensus standards, add verification steps and documentation load, making quality traceability and supplier qualification key to lead time and cost control.

Competitive Landscape

North America held 41.54% of the medical laser market in 2024, underpinned by robust reimbursement pathways and a dense ASC network. Alcon’s rapid roll-out of the Voyager DSLT, which delivers 120 pulses without a gonio lens, typifies the region’s first-mover culture. Canada mirrors US trends, albeit with tighter capital cycles that favor lease models.

Europe remains stable, balancing innovation with MDR-driven cost burdens. Carl Zeiss Meditec posted 17.1% revenue growth in EMEA in early 2025, buoyed by refractive-surgery consumables [3]Alcon, “Unity VCS Product Overview,” alcon.com. However, extended certification timelines may constrain smaller vendors, potentially consolidating the medical laser market around established brands.

Asia-Pacific is the fastest-growing arena at a 14.87% CAGR. China’s 10.2% 2024 laser-sector growth reflects public-hospital overhauls and rising aesthetic demand. Japan and South Korea deploy AI-enhanced excimer systems, while India advances through public-private ophthalmology hubs. ASEAN nations, though infrastructure-limited, attract medical tourism, adding volume to regional medical laser market size. Currency volatility and import duties remain hurdles, but demographic momentum signals sustained expansion.

Medical Laser Industry Leaders

Lumenis Ltd

Alcon Laboratories Inc.

Bausch & Lomb Incorporated

Koninklijke Philips NV

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Procedure migration into outpatient and specialty settings is creating space for compact, efficient platforms and standardized safety workflows. In the United States, ambulatory surgery centers account for 72% of surgeries, and the site-of-care shift supports diode and solid-state systems that can operate with smaller footprints, lower cooling demands, and faster room turnover. At the same time, the high capital and per-use economics for premium femtosecond platforms (USD 400,000-500,000 purchase prices plus per-use fees cited in the report context) support leasing, shared-service models, and modular upgrades that expand indications without requiring full system replacement.

Clinical and product development is also opening niches across dermatology, vascular, and urology. In June 2026, a human study reported that a 1940 nm non-ablative fractional laser modulated epigenetic markers linked to skin aging, which supports a differentiated premium dermatology pathway for differentiated cash-pay positioning. On the product side, LASEROPTEK introduced the VASCURA 589 vascular laser in June 2026 using a 589 nm output approach, reinforcing ongoing innovation in wavelength-specific systems that compete with legacy pulse-dye solutions. In urology, a May 2026 multicenter retrospective study on pulsed thulium:YAG in flexible ureterorenoscopy lithotripsy adds evidence depth for high-power solid-state platforms and helps broaden portfolios beyond ophthalmology and aesthetics, where many incumbent OEMs are already concentrated.

Recent Industry Developments

- June 2026: LASEROPTEK launched the VASCURA 589, a high-power solid-state vascular laser that uses a two-stage Raman conversion approach to deliver 589 nm output. The introduction targets vascular dermatology use cases where wavelength selection is used to optimize lesion response and reduce collateral thermal effects. It also signals continued competitive pressure in specialized aesthetic and vascular laser categories as vendors seek differentiation beyond legacy pulse-dye alternatives.

- September 2025: Alcon completed the acquisition of LumiThera, adding the Valeda photobiomodulation device to its ophthalmic portfolio for dry age-related macular degeneration. The deal extends Alcon's presence beyond surgical lasers into light-based therapy workflows that can be deployed in clinics and vision centers. Integrating Valeda into Alcon's broader ecosystem strengthens cross-selling potential alongside existing refractive and glaucoma offerings.

- December 2024: Bausch + Lomb acquired Elios Vision, Inc., bringing the ELIOS procedure, a minimally invasive glaucoma surgery that uses an excimer laser, into its glaucoma treatment capabilities. The acquisition expands Bausch + Lomb's access to laser-enabled MIGS approaches positioned as alternatives to long-term medication dependence. It also increases competitive intensity in ophthalmic lasers as more diversified eye-care companies internalize specialized laser technology rather than relying only on partnerships.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from medical laser systems used in clinical settings for diagnosis or treatment, where the laser is the core energy source delivered through a device platform. Values are captured at the system level and aligned to where the equipment is deployed for patient care.

Scope exclusions: We exclude service contracts, refurbished equipment, and disposables like single-use fiber tips and handpieces, and we also leave out non-laser light devices such as intense pulsed light (IPL).

Segmentation Overview

- By Product Type

- Solid-state Laser Systems

- Diode (Semiconductor) Laser Systems

- Gas Laser Systems

- Dye Laser Systems

- By Application

- Ophthalmology

- Dermatology & Aesthetics

- Gynecology

- Dentistry

- Urology

- Cardiovascular

- Others (ENT, Oncology)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty & Aesthetic Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand backdrop and the regulatory and trade signals that make adoption measurable. We used public sources such as the US FDA device databases, the World Health Organization and World Bank health indicators, OECD health statistics, and government health ministries for procedure and capacity context where available.

We then added triangulation inputs from company annual reports and investor presentations, peer-reviewed clinical journals on laser procedure use, and association publications from dermatology, ophthalmology, dental, and urology groups. For structured cross checks, we also used approved paid subscriptions for company financials and intelligence, patent databases, and an import and export shipment-level database to verify directionally where system shipments and manufacturing activity were moving. These examples are not exhaustive, and many other public and paid sources were also consulted for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how fast hospitals, ambulatory surgical centers, and specialty clinics are refreshing installed systems, and what changes are being seen in average selling prices by laser type. We also checked adoption drivers with surgeons, clinicians, and procurement teams across major regions so that assumptions around procedure mix, utilization, and replacement timing could be corrected when desk indicators were not consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 25% | EMEA: 32% |

| Smaller Players: 20% | Managers: 60% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure volumes, care setting mix, and equipment penetration are reconstructed by application and then translated into annual system demand. Once that demand pool is formed, it is converted into revenue using application-specific replacement cycles and price bands for common laser technologies (such as solid-state, gas, dye, and semiconductor systems).

To keep totals realistic, the model is corroborated with selective bottom-up approximations, including sampled supplier revenue splits, channel checks on unit shipments, and sanity checks using sampled ASP multiplied by implied units for key applications. When direct unit visibility is weak in a country, gaps are handled by using proxy indicators like specialty clinic counts, hospital capex signals, and import patterns, followed by expert review.

Forecasts are generated using scenario analysis supported by short input series, because adoption is influenced by step changes such as new indications, outpatient shift, and reimbursement and regulatory momentum. Variables that are routinely stress-tested include procedure growth in dermatology and ophthalmology, ambulatory center expansion, installed base aging, capex affordability, and expected ASP movement by laser platform as newer systems enter and older ones discount.

Data Validation & Update Cycle

Outputs are checked against independent signals such as reported regional revenue direction, shipment and trade movements, and the implied unit volumes required to support the revenue number. When a region shows unusual swings, the assumptions behind procedure mix, replacement timing, or pricing are reviewed again, and experts are re-contacted to confirm whether a one-time event occurred.

Before sign-off, the model and assumptions go through multi-step analyst reviews, and each major application line is checked for internal consistency so that totals do not rely on one fragile input. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory approvals, technology shifts, or sudden pricing moves. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Medical Laser Market Sizing Compared With Other Published Estimates

Published market sizes for medical lasers often do not match, even when the same years are quoted, because the counted items and the revenue boundary are not uniform across studies. Differences usually come from whether consumables and services are added, how refurbished sales are handled, and how pricing is carried forward from the base year.

Some estimates fold in consumables and broader light-based aesthetic devices into the same total, which expands the numerator quickly when procedure volumes rise. In Mordor Intelligence, only newly manufactured medical laser systems are counted at ex-factory revenues, and items like single-use tips, disposable handpieces, service contracts, and IPL devices are kept out to avoid mixing equipment and recurring lines.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.20 B (2025) | |

| Global Advisory Note A | USD 5.83 B (2025) | Includes consumables alongside laser systems, which can lower the implied system-only ASP and shifts more weight to recurring lines that are not captured in a systems revenue model. |

| Industry Publisher B | USD 6.82 B (2024) | Uses an earlier base year and appears to apply a broader technology and application basket without clearly removing disposables and non-laser light devices, which can raise totals when converted to the next year. |

The spread is mainly explained by what gets counted as part of the market and how the base year is carried forward through pricing and mix assumptions. By keeping the scope tied to system sales and then checking it against procedure-linked demand signals and replacement behavior, our estimate stays easier to audit and repeat across regions.

Key Questions Answered in the Report

What is the current Global Medical Laser Market size?

The Global Medical Laser Market is projected to register a CAGR of 13.12% during the forecast period (2026-2031)

Who are the key players in Global Medical Laser Market?

Lumenis Ltd, Alcon Laboratories Inc., Bausch & Lomb Incorporated, Koninklijke Philips NV and Candela Medical are the major companies operating in the Global Medical Laser Market.

Why is Asia-Pacific considered the most attractive region for future investment?

Aging populations, increasing healthcare spending, and double-digit growth in aesthetics and ophthalmology drive a 14.31% CAGR in Asia-Pacific, the highest regional rate.

Which region has the biggest share in Global Medical Laser Market?

In 2025, the North America accounts for the largest market share in Global Medical Laser Market.

What risks could slow market growth?

High capital outlays, rare-earth material shortages, and cybersecurity vulnerabilities in networked systems pose tangible threats to adoption and profitability.

Page last updated on: