Global Surgical Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

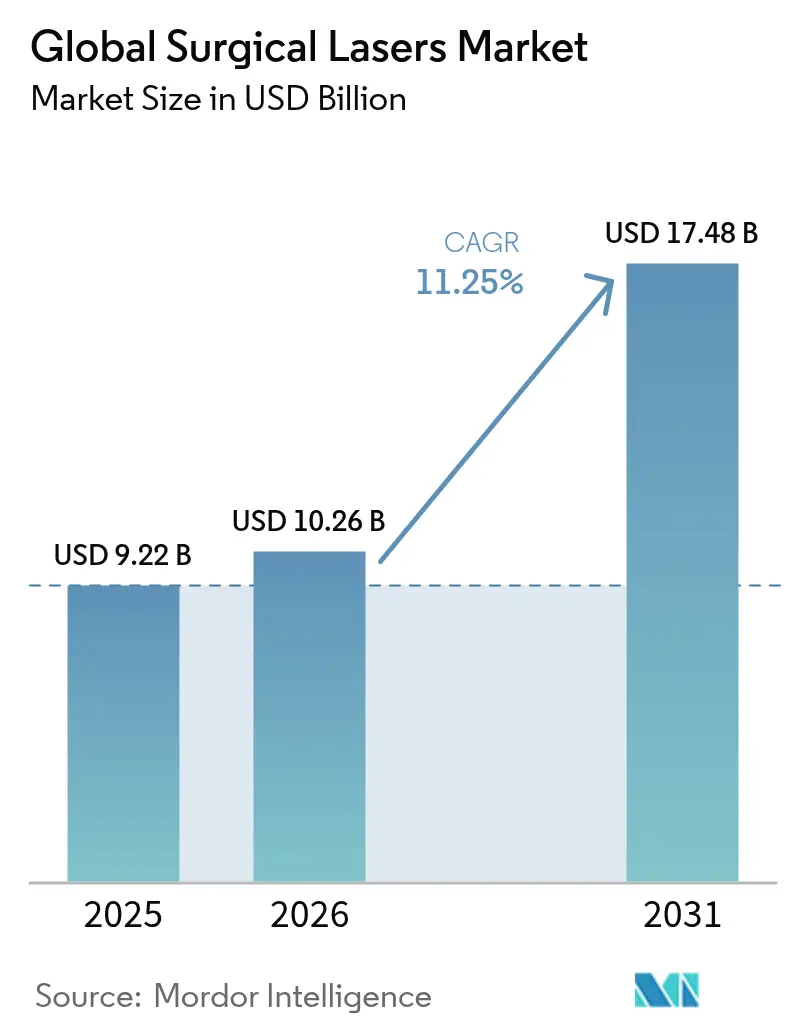

| Market Size (2026) | USD 10.26 Billion |

| Market Size (2031) | USD 17.48 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Surgical Lasers Market Analysis by Mordor Intelligence

The surgical laser market size is expected to grow from USD 9.22 billion in 2025 to USD 10.26 billion in 2026 and is forecast to reach USD 17.48 billion by 2031 at 11.25% CAGR over 2026-2031. Robust growth is underpinned by faster adoption of AI-assisted beam-shaping optics, rising outpatient procedure volumes and regulatory alignment with IEC safety norms. Hospitals and large ambulatory surgical centers are refreshing equipment to meet stricter plume-safety rules, while vendors compete on workflow software that matches laser energy to tissue type in real time. North American reimbursement stability, alongside Asia-Pacific infrastructure upgrades, keeps demand broad-based. Technology convergence with robotic platforms is widening the surgical laser market addressable base, particularly in complex urology and ophthalmology cases.

Key Report Takeaways

- By laser type, carbon dioxide units led with 34.18% surgical laser market share in 2025; diode lasers are forecast to expand at a 12.18% CAGR to 2031.

- By procedure, open surgery retained 32.30% of the surgical laser market size in 2025, while robot-assisted surgery is advancing at a 12.36% CAGR through 2031.

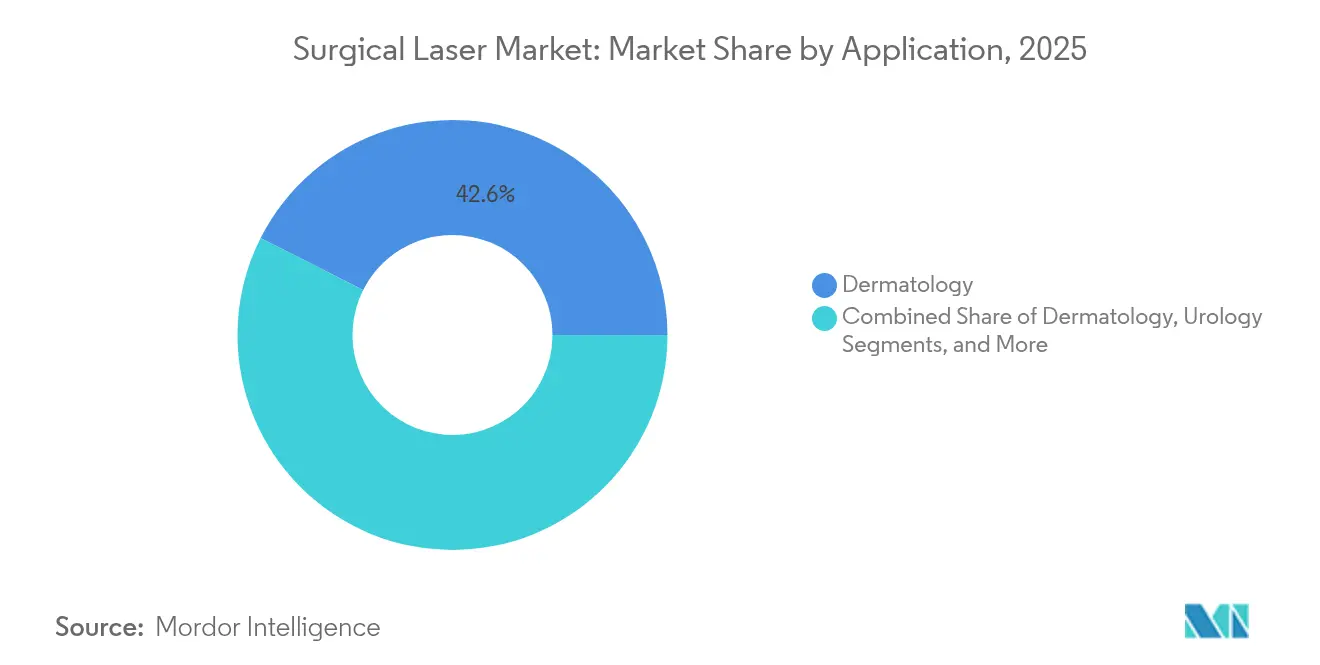

- By application, dermatology captured 42.55% revenue in 2025 and dentistry is the fastest mover at 11.92% CAGR to 2031.

- By end user, hospitals commanded 57.95% of the surgical laser market size in 2025; ambulatory surgical centers are growing at a 12.08% CAGR.

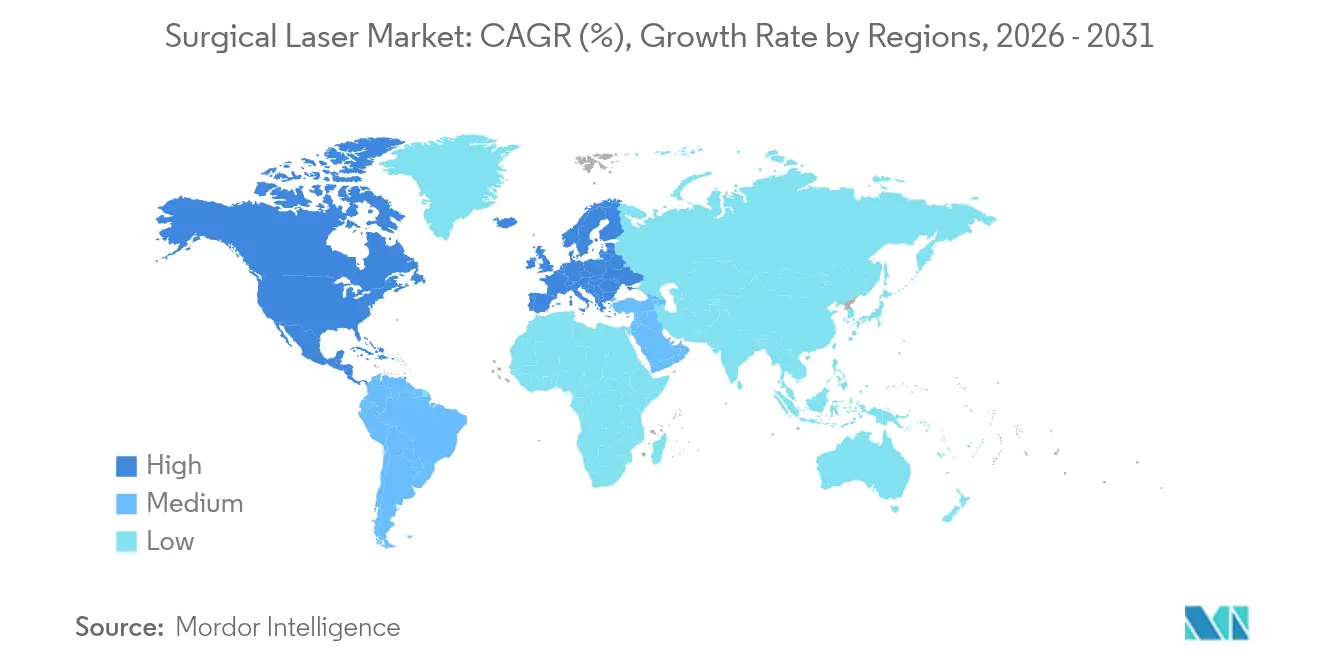

- By geography, North America accounted for 44.72% revenue in 2025, whereas Asia-Pacific is set to grow at 12.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surgical Lasers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in beam-shaping optics | +2.1% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Preference for minimally-invasive & day-care surgeries | +2.8% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Rising incidence of ophthalmic & urologic disorders | +1.9% | Global, accelerated in aging populations (North America, EU, Japan) | Long term (≥ 4 years) |

| Regulatory approvals expanding clinical indications | +1.7% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Rapid adoption of outpatient laser suites (ASC model) | +2.3% | North America dominant, emerging in EU & APAC | Short term (≤ 2 years) |

| AI-driven real-time laser dosimetry & workflow gains | +1.6% | Global, with technology hubs leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Beam-Shaping Optics

Liquid-lens modules now correct focal drift inside flexible fibers, enabling steady ablation at depths past 700 µm—more than triple previous limits [1]Chunqi Zhang, “Liquid Lens Compensation in Fiber-Delivered Surgery,” Applied Optics, opg.optica.org. Fiber shapers developed at MIT tailor beam patterns that cut scattering by half and preserve native tissue architecture, which is crucial for intra-operative imaging. When paired with optical coherence tomography, surgeons receive real-time cross-sections that guide submillimeter resections. Efficiency gains also reduce average pulse energy, lowering thermal damage margins. Collectively, these advances enhance patient safety and shrink operative time, giving the surgical laser market a measurable quality edge that hospitals can monetize through faster case turnover.

Preference for Minimally-Invasive & Day-Care Surgeries

Ambulatory facilities now perform a majority of cataract and gall-bladder cases under local anesthesia, encouraged by a 2025 CMS rule that raises ASC payments by 2.6%. Patients benefit from same-day discharge and 20% shorter wait lists, while payers save up to 45% on facility fees, reinforcing a volume shift into the surgical laser market. Laser platforms with plume-capture and quick-swap fiber handpieces fit ASC workflows and minimize room turnaround time. As outpatient centers invest in robotic carts that combine endoscopy and laser cutting, procedure complexity gradually rises without eroding cost efficiency.

Rising Incidence of Ophthalmic & Urologic Disorders

The prevalence of cataract is set to double in the United States within three decades, boosting demand for femtosecond and excimer lasers that deliver sub-5 µm capsulotomies [2]Robin G. Abell, “Economic Considerations in Laser Cataract Surgery,” American Academy of Ophthalmology, aao.org. In urology, thulium-fiber sources achieve faster stone “dusting” at 50% lower power than holmium systems, cutting retropulsion and scope wear. FDA clearance of the VISUMAX 800 platform brings small-incision lenticule extraction to high-volume centers and demonstrates agency confidence in next-generation optics. Together, aging demographics and superior clinical outcomes continue to widen the surgical laser market.

Regulatory Approvals Expanding Clinical Indications

In March 2025, FDA Laser Notice No. 56 took effect, synchronizing U.S. rules with IEC 60825-1 and IEC 60601-2-22 and obligating manufacturers to file revised product reports. A spate of 2024-2025 clearances—including the da Vinci 5 robot and TENEO excimer platform—has validated multipurpose lasers for ENT, spine and gynecology use. Updated ANSI Z136.3 guidelines supply hospitals with unified hazard controls, simplifying credentialing for staff and accelerating purchasing decisions. Greater clinical breadth moves lasers from niche to standard toolkits, fortifying long-term surgical laser market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & procedural costs | -1.8% | Global, sharper in emerging regions | Long term (≥ 4 years) |

| Reimbursement gaps in developing markets | -1.4% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Global helium shortage | -0.9% | Worldwide CO₂ laser supply chain | Short term (≤ 2 years) |

| Stricter plume-safety mandates | -0.7% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Procedural Costs

State-of-the-art femtosecond workstations can exceed USD 500,000, a hurdle for smaller clinics whose reimbursements remain technique-agnostic. Cost-utility studies confirm visual gains but note payback periods beyond five years in low-volume settings. Mandatory laser safety officer training and ventilation upgrades add overhead. Where humanitarian cataract missions operate at USD 276 per eye, capital intensity underscores adoption gaps [3]Zhaoqun Liu, “Clinical Utility of 445 nm Diode Systems,” Applied Sciences, appliedsciences.mdpi.com. Price sensitivity in emerging economies dampens unit sales and tempers the global surgical laser market trajectory.

Reimbursement Gaps in Emerging Economies

Out-of-pocket payment remains common for laser prostate or refractive surgery in large parts of Asia, limiting rural diffusion despite urban flagship programs. India hosts more than 170 robotic surgery systems, yet installations cluster in metro hospitals where private insurers reimburse advanced procedures. China’s 12% annual expansion in robotic platforms shows that when public insurance widens coverage, laser volumes follow. Absent unified reimbursement codes, many facilities defer acquisition, softening surgical laser market growth in price-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: CO₂ Stability Meets Diode Momentum

Carbon dioxide systems held 34.18% of 2025 revenue, owing to their reliability in ENT and gynecology. At USD 10.26 billion, the surgical laser market size continues to rely on CO₂ for precise vaporization with minimal bleeding. Yet diode units, projected to expand at 12.18% CAGR, are eroding entry-level CO₂ share as 445 nm wavelengths cut soft tissue efficiently while consuming less power. Manufacturers emphasize portable chassis and lower consumable costs, aligning with ASC budgets. As photonic-crystal fibers mature, diode beam quality improves, allowing ENT surgeons to achieve 1 mm cut depths with limited collateral heat. The trend suggests incremental but persistent diversification, safeguarding supply chains from helium scarcity that threatens glass-tube CO₂ capacity.

Carbon dioxide suppliers counter with hybrid systems that embed mid-infrared modules to expand dermatology and oncology use cases. Excimer platforms remain irreplaceable for corneal reshaping and now incorporate active-eye tracking to compensate for micro-saccades, boosting outcome predictability. Fiber and Er:YAG designs pair with robots for spine decompression, reflecting a strategy to widen the surgical laser market by tying hardware to procedure-specific software.

By Procedure: Robots Re-engineer Workflows

Open surgery retained 32.30% of 2025 procedures as legacy protocols and surgeon familiarity persist. Nonetheless, robot-assisted cases are climbing at 12.36% CAGR and already represent a quarter of prostatectomies in leading U.S. centers. Force-feedback sensors integrated into laser end-effectors trim tissue damage by 43%, supporting surgeon confidence. As software updates roll out remotely, installed robots gain new laser modalities without hardware swaps, pushing the surgical laser market toward service-based revenue.

Laparoscopic laser adoption grows steadily, bolstered by high-resolution imaging and plume suction filters that preserve visibility. Percutaneous lithotripsy benefits from thulium-fiber efficiency, shortening operative times and lowering anesthesia exposure. Together, these shifts point to a surgical suite where lasers, robots and imaging platforms operate as a single digital ecosystem, raising entry barriers for newcomers.

By Application: Dermatology Commands, Dentistry Accelerates

Dermatology captured 42.55% of 2025 demand as fractional resurfacing, scar revision and pigment correction remain high-volume indications. AI-driven parameter presets now adjust pulse density to skin phototype in seconds, reducing trial shots and consumable spend. Dentistry, advancing at a 11.92% CAGR, gains from diode and erbium devices that debulk soft tissue with minimal anesthesia, enlarging chairside productivity. With AI guidance, operators cut operative time for crown lengthening by 30%, a strong hook for fee-for-service practices.

Ophthalmology holds share through femtosecond cataract systems whose sub-micron precision lowers posterior capsule rupture rates. Urology benefits from faster lithotripsy, while cardiology explores pulsed-field ablation for arrhythmia management after Boston Scientific’s recent regulatory wins. As each clinical silo matures, cross-specialty laser adoption deepens, diversifying the surgical laser market.

By End User: Hospitals Lead, ASCs Surge

Hospitals retained 57.95% of the 2025 surgical laser market size thanks to capital budgets and 24/7 support teams. Yet ambulatory surgical centers are set to grow 12.08% annually as payers steer low-risk cases to lower-cost sites. Federal reimbursement of USD 7.4 billion for ASCs in 2025 underscores a structural shift. Lasers that combine plume evacuation, small footprints and quick sterilization cycles resonate with ASC throughput goals.

Specialty clinics leverage direct-pay cosmetic and dental procedures to bypass insurance friction. Academic centers stay pivotal in training and clinical trials, accelerating evidence that mainstreams laser indications. State-level smoke-evacuation statutes raise compliance spending, driving smaller ASCs to affiliate with chains that can amortize upgrades, thus concentrating demand among large buyers within the broader surgical laser market.

Geography Analysis

North America generated 44.72% of 2025 revenue on the back of early technology adoption, favorable payer policies and a dense ASC network. FDA approvals of the da Vinci 5 robot and TENEO excimer laser set clinical precedents and underpin replacement cycles. Large device firms report double-digit U.S. revenue gains as hospitals refresh fleets to comply with Laser Notice No. 56. Persistent helium cost inflation, however, nudges providers toward fiber-based alternatives, illustrating a regional pivot that influences global supply strategies.

Asia-Pacific is poised for 12.89% CAGR through 2031. Public insurance expansion in China has spurred double-digit growth in robotic-laser procedures, and Japan’s 97.3% success rate in office-based vitreoretinal work validates outpatient complex surgery. India’s urban hospital chains invest in multi-specialty lasers even as reimbursement lag restrains rural penetration. Government-funded cancer centers in South Korea and Singapore are installing dual-wavelength suites, signaling sustained investment momentum within the surgical laser market.

Europe shows balanced progress. Harmonization with IEC standards simplifies cross-border trade, and energy-efficient fiber lasers align with the region’s sustainability regulations, consuming roughly one-third of the electricity of legacy CO₂ models. Eastern European nations leverage EU structural funds to modernize ORs, though reimbursement ceilings temper high-end adoption. The Middle East and South America represent emerging corridors, where medical tourism and private hospital groups drive premium equipment purchases, yet currency volatility and spot helium shortages present operational hurdles.

Competitive Landscape

The surgical laser market tilts moderately concentrated, with multinationals deepening technology moats through acquisitions and R&D intensity. Cynosure’s merger with Lutronic fuses U.S. distribution with Korean engineering, offering dual platform roll-outs that shorten product cycles. Alcon’s planned Lensar buy strengthens its cataract franchise and secures femtosecond IP crucial for premium intraocular lens alignment. Boston Scientific’s deal for Bolt Medical injects laser-atherectomy tech into its cardiovascular suite, positioning the firm to cross-sell disposables to existing cath-lab customers.

Technology leadership remains a key differentiator. Intuitive Surgical embeds haptic feedback and ten-fold data throughput, translating to gentler tissue manipulation and predictive instrument wear monitoring. IPG Photonics pushes >50% wall-plug efficiency in mid-IR fiber engines, trimming OR energy bills and carbon footprints. Smaller innovators focus on AI-driven treatment planning; AVAVA’s MIRIA platform, for example, integrates dermal imaging with algorithmic fluence maps to personalize aesthetics. Regulatory convergence raises compliance hurdles, favoring incumbents that can amortize testing and documentation costs across broad portfolios, thereby reinforcing competitive positioning within the surgical laser market.

Global Surgical Lasers Industry Leaders

Cynosure

Lumenis

IPG Photonics Corporation

biolitec AG

Alma Lasers Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon signed a definitive agreement to acquire Lensar, augmenting its femtosecond capabilities and expanding its ophthalmic surgery lineup.

- June 2024: Lumenis introduced Folix, the first FDA-cleared fractional laser for hair-loss therapy, leveraging proprietary fractional energy delivery to stimulate follicles.

- March 2024: Intuitive Surgical secured FDA clearance for the da Vinci 5 system, featuring force-feedback and boosted processing power that enhances robotic laser precision.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We define the surgical lasers market as all photonic systems that cut, ablate, or coagulate human tissue during minimally invasive or open procedures across dermatology, ophthalmology, urology, dentistry, gynecology, cardiology, gastroenterology, and oncology. Platforms include CO2, Nd:YAG, diode, holmium, fiber, excimer, and emerging hybrid sources.

Scope exclusion: veterinary laser devices lie outside this analysis.

Segmentation Overview

- By Laser Type

- Carbon Dioxide (CO₂) Lasers

- Nd:YAG Lasers

- Diode Lasers

- Holmium:YAG Lasers

- Fiber & Er:YAG Lasers

- Excimer Lasers

- Other Lasers

- By Procedure

- Open Surgery

- Laparoscopic Surgery

- Percutaneous Surgery

- Robot-assisted Surgery

- By Application

- Dermatology

- Ophthalmology

- Urology

- Dentistry

- Gynecology

- Cardiology

- Gastroenterology

- Oncology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty & Aesthetic Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team surveyed operating room surgeons, biomedical engineers, ASC managers, and laser service providers across multiple countries, which helped us verify replacement cycles, average selling prices, and procedure mix shifts. Follow-up calls with regional distributors allowed us to refine emerging market penetration assumptions.

Desk Research

We started by extracting console import volumes, HS-code unit values, and adoption trends from UN Comtrade, Eurostat, and US International Trade Commission dashboards. We then mapped global procedure counts using WHO Hospital Activity statistics and OECD Health Data. Clinical efficacy and safety insights were pulled from PubMed and FDA 510(k)/MAUDE files, while cost curves and installed base details were validated through American Society for Laser Medicine and Surgery digests and D&B Hoovers filings. According to Mordor analysts, Factiva and Questel searches filled competitive and patent gaps. These examples are illustrative; many other reputable sources were also mined for triangulation.

Market-Sizing & Forecasting

A top-down reconstruct was built from annual laser-assisted procedure volumes multiplied by weighted ASPs, which are then corroborated with selective bottom-up supplier roll-ups and channel checks. Key variables like elective surgery rebound index, outpatient share of laser cases, console replacement interval, rare-earth material pricing, and average diode power per system feed a multivariate regression that drives 2025-2030 projections. Gap pockets in bottom-up inputs, such as unreported clinic purchases, are bridged by calibrated uptake factors agreed upon during primary interviews.

Data Validation & Update Cycle

Model outputs pass anomaly screens against independent import values, hospital capex ratios, and peer-reviewed prevalence benchmarks before senior review. Reports refresh each year; material events, for example, major platform recalls, trigger interim updates, and a last-minute sweep is completed prior to client delivery.

Why Mordor's Surgical Lasers Baseline Commands Reliability

Published estimates often diverge because firms mix different laser types, revenue points, and refresh cadences. We acknowledge this spread and show where numbers shift.

Key gap drivers include narrower ophthalmic coverage in some studies, single-scenario currency locks, or omission of ASC channel revenues. Mordor's disciplined scope, annual refresh, and dual-path (top-down and bottom-up) validation remove such biases, yielding a balanced figure clients can replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.22 B (2025) | Mordor Intelligence | - |

| USD 8.28 B (2024) | Global Consultancy A | Limited laser types and one-off refresh year |

| USD 8.48 B (2024) | Industry Database B | Factory-gate revenues only; fixed 2022 FX; excludes ASC sales |

These comparisons show that, while external values cluster close, variations stem from scope and currency choices rather than fundamental demand. Mordor's transparent variables and repeatable steps therefore provide the most dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current Global Surgical Lasers Market size?

The surgical laser market size was USD 10.26 billion in 2026 and is forecast to reach USD 17.48 billion by 2031, translating to an 11.25% CAGR

Who are the key players in Global Surgical Lasers Market?

Cynosure, Lumenis, IPG Photonics Corporation, biolitec AG and Alma Lasers Ltd are the major companies operating in the Global Surgical Lasers Market.

Why are ambulatory surgical centers important for growth?

ASCs offer lower facility fees and faster scheduling; they also integrate compact, plume-controlled lasers, driving a 12.08% CAGR for the end-user segment through 2031.

Which region has the biggest share in Global Surgical Lasers Market?

In 2025, the North America accounts for the largest market share in Global Surgical Lasers Market.

What technological trend will shape future product design?

AI-assisted beam-shaping and real-time dosimetry are set to become standard, enabling personalized energy delivery that enhances outcomes and reduces collateral tissue damage.

Page last updated on: