Aesthetic Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

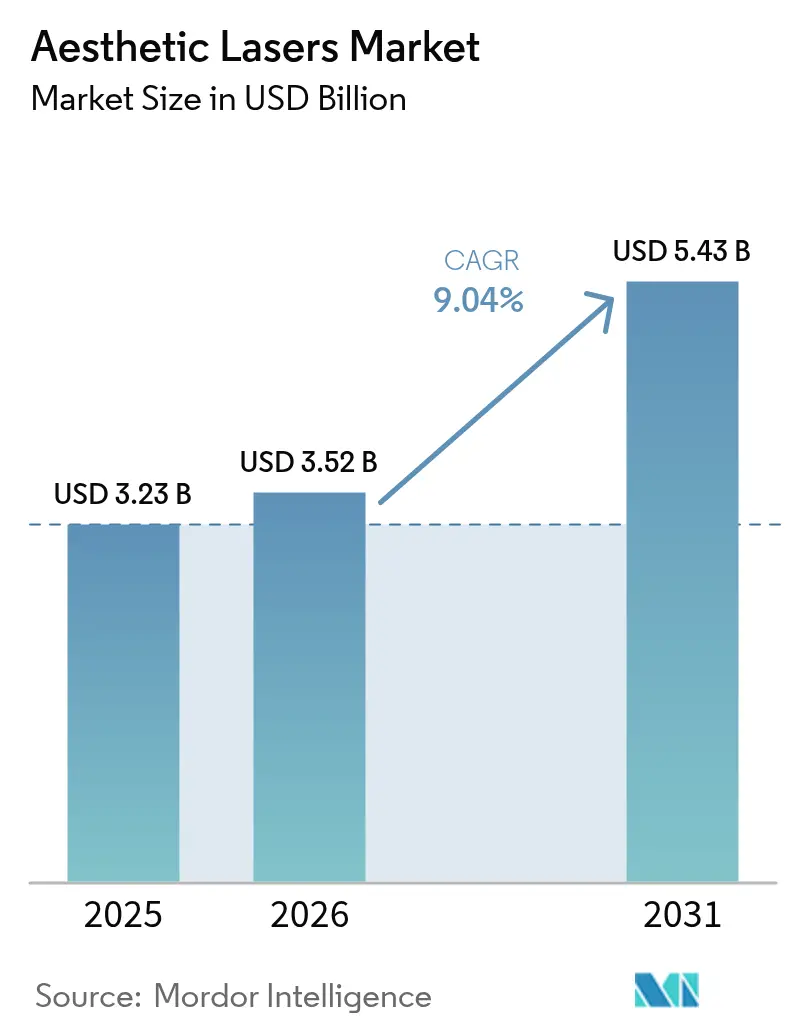

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 9.04% CAGR |

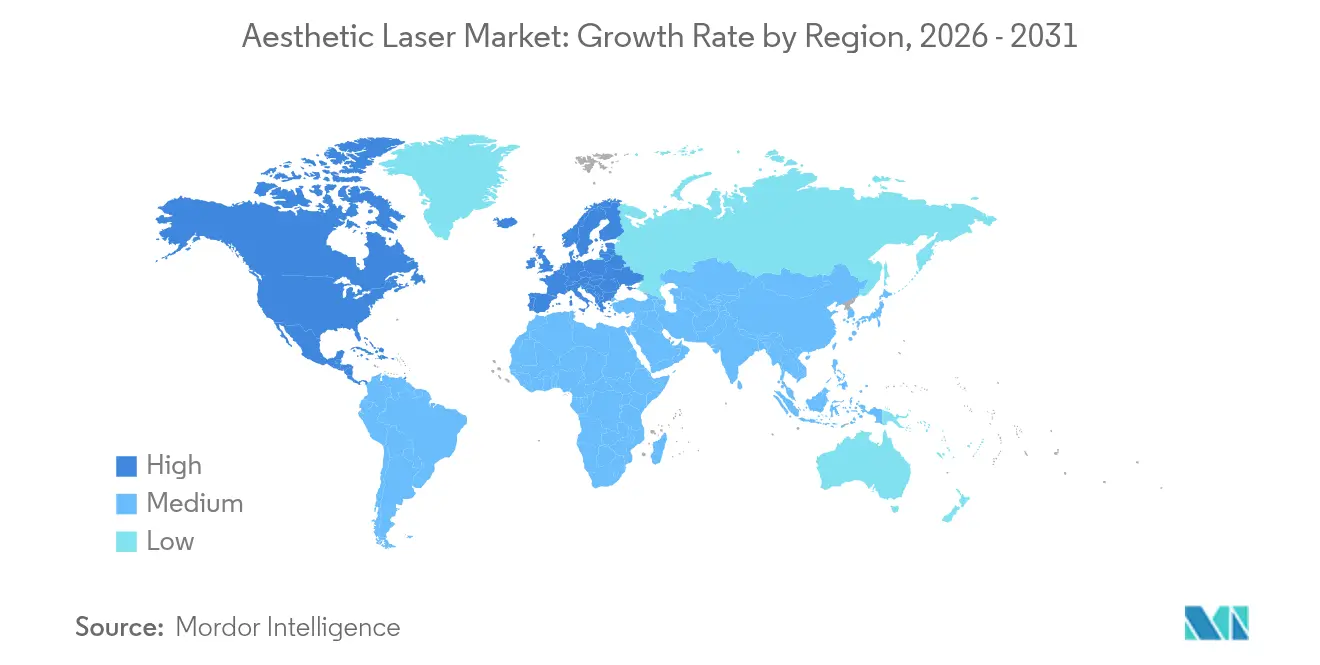

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

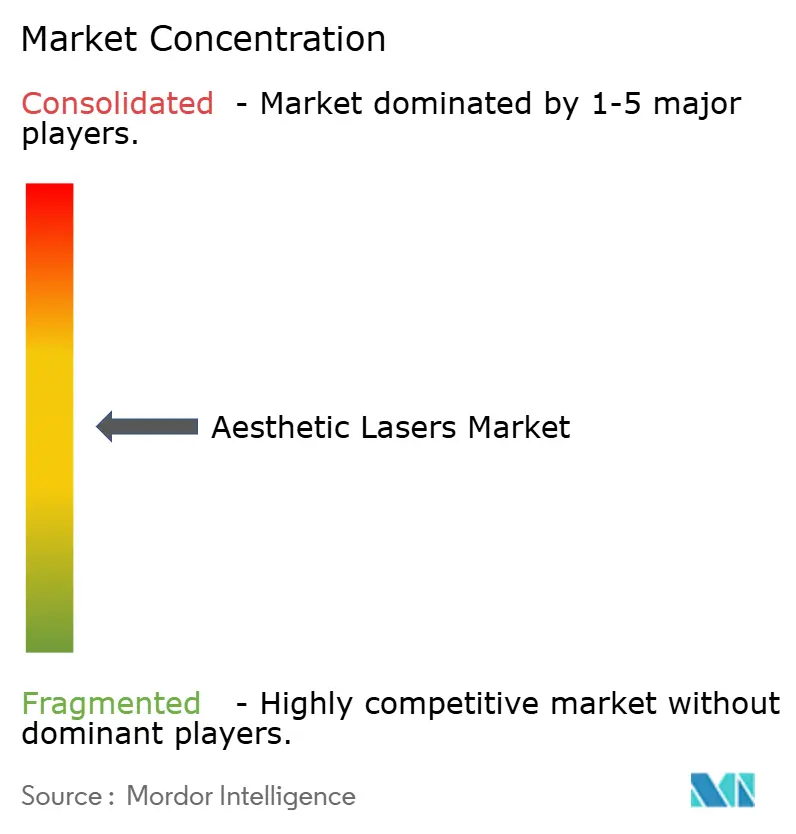

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aesthetic Lasers Market Analysis by Mordor Intelligence

The Aesthetic Lasers Market size was valued at USD 3.23 billion in 2025 and estimated to grow from USD 3.52 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 9.04% during the forecast period (2026-2031). Rising consumer demand for minimally invasive cosmetic interventions that deliver visible results with limited downtime continues to redefine capital-equipment purchase criteria among dermatology practices. An additional implication, derived from the same growth dynamic, is that equipment vendors able to shorten practitioner learning curves may now command pricing premiums that were previously associated only with clinical efficacy.

Key Report Takeaways

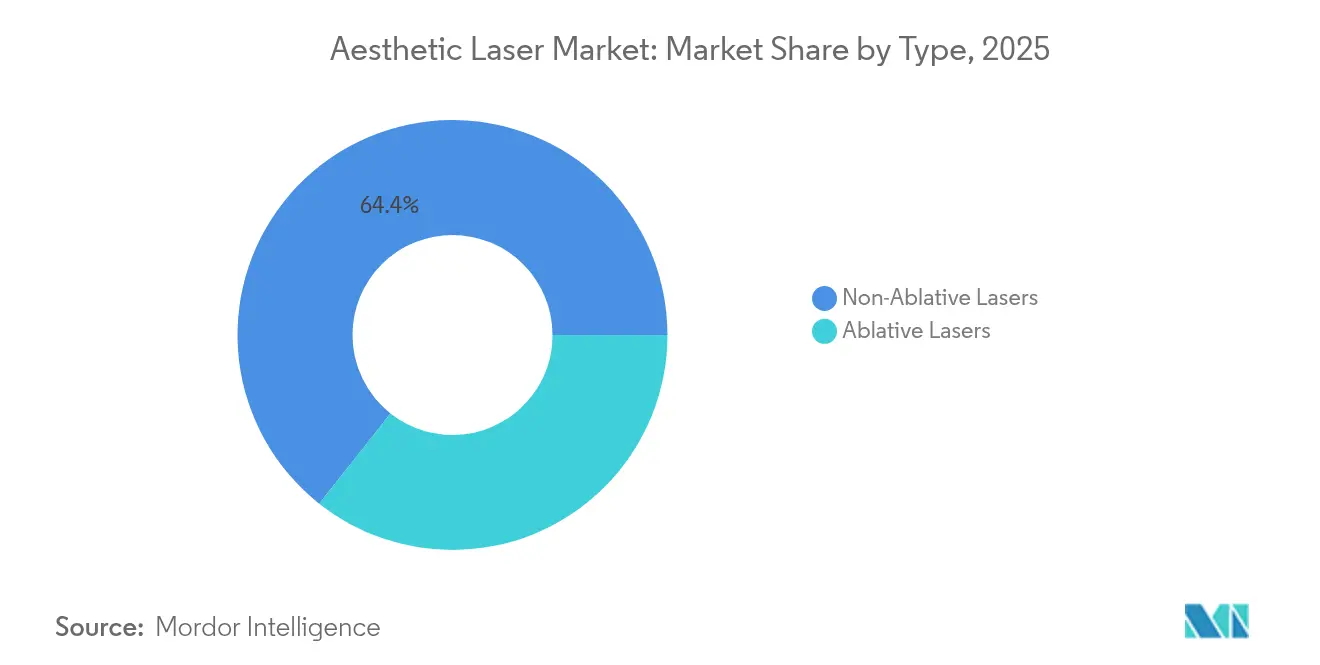

- Non-ablative systems continue to dominate with 64.35 % market share in 2025, buoyed by fractional delivery that balances efficacy and downtime. Ablative lasers are expected to grow with 9.85% CAGR

- Asia-Pacific is the fastest-growing region, registering a 11.75 % CAGR and capturing demand for pigment correction and scar revision. North America held 39.60% share in the global market in 2025.

- Standalone Laser Systems held 71.20% in 2025 whereas Multiplatform hybrids are rising at a 12.90 % CAGR, converting laser consoles into software-upgradable assets and redefining depreciation schedules.

- By portability, non-portable held 79.30% share in the market, while non-portable is expetced to grow with 11.40% CAGR.

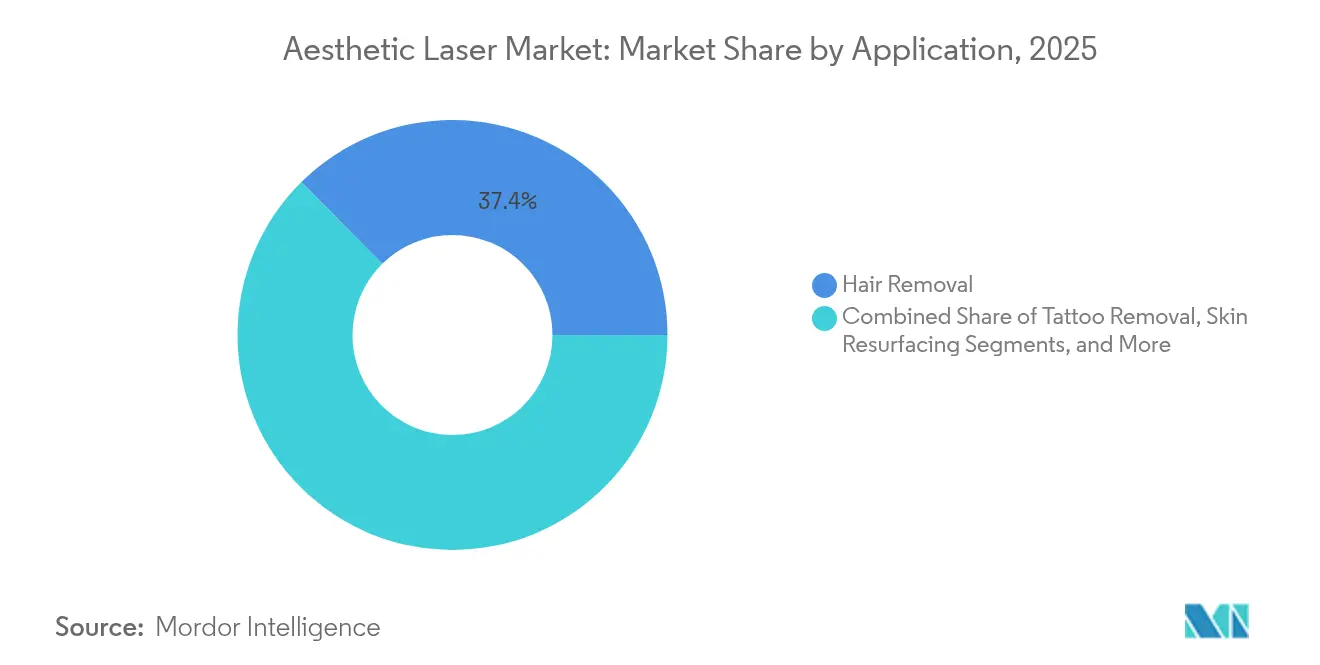

- By application, hair removal have 37.40% share in the market in 2025 whereas body sculpting and skin tightening are growing with 12.85% CAGR.

- Dermatology and aesthetic clinics captured 44.40% market share in 2025, yet medical spas are the fastest-growing channel at 13.60% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aesthetic Lasers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Forecast Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing technological advancements | +1.2 % | Global | Medium term (2-4 years) |

| AI-enabled laser parameter optimization reducing adverse events | +0.6 % | North America, Asia-Pacific | Short term (≤ 2 years) |

| Uptake of picosecond lasers for pigmented lesions among millennials | +0.8 % | Asia-Pacific, North America | Medium term (2-4 years) |

| Medical-tourism-led boom in laser hair removal | +0.7 % | Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Changing lifestyle and growing disposable income | +0.5 % | Emerging markets worldwide | Long term (≥ 4 years) |

| Aging population & rise in skin-laxity-driven laser tightening | +1.4 % | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Demographics Driving Precision-Targeted Treatments

A rapidly expanding 65-plus cohort now prioritizes skin laxity correction through laser tightening, substituting surgical facelifts with outpatient regimens. Because geriatric dermis heals more slowly, device makers are integrating finer energy-increment settings and closed-loop temperature feedback to mitigate overtreatment risk [1]Michael Roh, “Adjusting Laser Parameters for Geriatric Skin,” Journal of Dermatological Research, ncbi.nlm.nih.gov. Clinics that position these protocols as “maintenance of vitality” rather than vanity appeal find higher acceptance among older patients intimately concerned with mobility and recovery time.

Technological Convergence Accelerates Innovation Cycles

Makers are stacking multiple wavelengths and radiofrequency channels into single chassis, effectively collapsing four or five standalone devices into one. The direct result is shorter replacement cycles as single-modality workhorses appear under-spec’d, but the secondary effect is that software upgradability becomes the real lock-in mechanism, not the hardware shell. Alma Hybrid’s CO₂ + 1570 nm pairing illustrates how future competitive advantage may pivot from light sources to treatment algorithms controlled by firmware updates.

Picosecond Technology Transforms Millennial Aesthetic Priorities

Millennial patients equate flawless complexion with social currency, fueling picosecond platform uptake for rapid pigment clearance. Ultra-short pulses deliver a stronger photoacoustic effect while minimizing thermal diffusion, thereby reducing post-inflammatory hyperpigmentation on darker skin types. Clinics that combine these lasers with mobile-app appointment systems quietly capture recurring revenue via bundled maintenance packages, shifting revenue models toward subscription-style skin management.

Medical Tourism Reshapes Global Treatment Distribution

Price-sensitive consumers increasingly fly to India, Thailand, and South Korea where Western-grade technology meets lower procedure costs. Device manufacturers now operate two-track portfolios: flagship consoles for internationally accredited hospitals and leaner variants tailored to domestic mid-tier clinics. This gap indirectly pressures after-sales service divisions to build multilingual technical-support hubs, an investment that may prove more strategic than incremental R&D in sustaining share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR | Forecast Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement in public healthcare systems | –0.9 % | Europe, North America | Medium term (2-4 years) |

| Stringent laser safety regulations delaying product launches | –0.7 % | North America, EU | Short term (≤ 2 years) |

| Social stigma associated with cosmetic treatments | –0.4 % | Middle East, conservative markets | Long term (≥ 4 years) |

| Shortage of trained laser technicians in emerging nations | –0.6 % | Africa, South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Creates Market Stratification

Laser treatment for rosacea and acne remains widely classified as elective, with UnitedHealthcare’s medical policy deeming it “not medically necessary” [2]UnitedHealthcare, “Laser Treatment Medical Policy,” unitedhealthcare.com. Consequently, high-income urban dwellers propel premium clinic revenues, while mid-market providers rely on creative financing or pay-per-session plans to broaden access. The stratification opens a niche for low-cost portable units targeting emerging-market entrepreneurs who lack capital for flagship systems.

Regulatory Complexity Delays Innovation Commercialization

In the United States, all aesthetic laser products fall under Class II, triggering the 510(k) pathway and demanding conformance to IEC 60601-2-22 safety standards [3]U.S. Food & Drug Administration, “Laser Products and Instruments,” fda.gov. Approval timelines stretching 12-18 months erode first-mover advantage, nudging start-ups toward licensing their IP to multinational partners. An unintended outcome is that these multinationals shape the innovation funnel, determining which niche technologies reach global scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Type: Non-Ablative Lasers Dominate Treatment Landscape

Non-ablative systems held 64.35 % market share of the aesthetic lasers market size in 2025, propelled by consumer insistence on treatments that do not interfere with daily routines. Evidence showing that fractional thulium fiber lasers improve epidermal thickness in Asian photodamage cases underscores their cross-ethnic applicability. This dominance also implies that clinics may allocate a disproportionate share of marketing budgets to highlight downtime-free outcomes, subtly shifting competitive discourse away from single-session efficacy toward cumulative skin-quality upgrades.

Modality: Multiplatform Systems Gain Market Momentum

Standalone lasers retained 71.20 % share in 2025, yet multiplatform hybrids are posting a 12.90 % CAGR. The embedded inference is that financing companies could soon recalibrate depreciation schedules, treating multiplatform units more like software-upgradable assets than conventional capital equipment. Longer economic life increases the appeal of leasing models, creating recurring-revenue streams for both lessors and manufacturers.

Portability: Compact Systems Expand Treatment Settings

While non-portable rigs still command 79.30% share, portable devices are forecast to expand at 11.40% CAGR. The surge of high-net-worth patients willing to pay premium fees for home-based sessions suggests that portability may evolve from convenience feature to strategic revenue channel. As device footprints shrink, ancillary products such as single-use safety goggles and sterilization sleeves could experience parallel demand spikes, reinforcing the ecosystem nature of profits in this space.

Application: Body Sculpting Disrupts Traditional Hierarchy

Hair removal retains 37.40% share today, but body sculpting and skin tightening are rising at 12.85 % CAGR between 2026-2031. Because body contouring often stimulates multi-session packages, average revenue per user can exceed that of hair removal by a meaningful margin, incentivizing clinics to reallocate floor space toward larger-form-factor sculpting units. An associated insight is that suppliers of consumables—such as disposable applicator tips—may capture a growing slice of lifetime project economics.

End User: Medical Spas Disrupt Traditional Delivery Models

Dermatology and aesthetic clinics captured 44.40% market share in 2025, yet medical spas are the fastest-growing channel at 13.60% CAGR. Their non-clinical ambience lowers psychological entry barriers for first-time consumers, which in turn enlarges the total addressable market. This shift pressures training organizations to standardize competency frameworks, because inconsistent operator skill levels could adversely affect brand reputation across franchised spa networks.

Geography Analysis

North America controlled 39.60% of global market share in 2025, supported by robust provider networks and early technology adoption. The market size of U.S. minimally invasive “tweakment” procedures reinforces the importance practitioners place on incremental corrections rather than dramatic makeovers. A parallel observation is that patient expectations in major metropolitan areas increasingly revolve around synergistic protocols combining injectables with sub-ablative lasers, suggesting cross-selling opportunities for integrated practices.

Asia-Pacific is forecast to register 11.75% CAGR through 2031, the fastest pace of any region. Countries emphasizing even skin tone as a cultural ideal drive above-average adoption of picosecond and nano-second pigment lasers. Clinics that stock devices capable of addressing both melasma and vascular redness stand to capture share, because dual-indication versatility defrays capital investment more quickly in markets where procedure pricing is tightly competitive.

Europe remains a mature yet expanding market, where preference for natural-appearing outcomes encourages protocols that blend low-energy passes over multiple sessions. An indirect implication is that patient retention may supersede new-patient acquisition as the primary revenue lever for many clinics, particularly in Germany, France, and the UK where word-of-mouth referrals carry considerable weight.

Competitive Landscape

The five largest suppliers collectively account for roughly 40% of revenue, while a long tail of niche specialists drives category innovation. Larger firms prioritize platform extensibility—for instance, Alma Lasers offers modular handpieces that incrementally expand clinical indications—thereby embedding switching costs that lock in customers over multi-year horizons. Emerging competitors, conversely, often stake out narrow applications such as tattoo removal or women’s health, leveraging scientific depth to command premium pricing within those silos.

Hybrid systems combining laser with radiofrequency or ultrasound are further blurring boundaries. The strategy suggests that future competition may pivot around total treatment ecosystem control, spanning consumables, software, and even patient lead-generation platforms.

Aesthetic Lasers Industry Leaders

Candela Medical

Lumenis

Cynosure (Hologic)

Alma Lasers (Sisram)

Cutera

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lumenis launched SPLENDOR X+, coupling Nd:YAG and Alexandrite wavelengths with synchronized delivery for hair removal across all Fitzpatrick skin types.

- April 2025: AVAVA secured FDA clearance for acne scar treatment leveraging Focal Point Technology to deliver high energy in all skin types.

- November 2024: AVAVA’s MIRIA intradermal laser obtained U.S. clearance for precise 1.5 mm dermal targeting while sparing the epidermis.

- July 2024: Crescita Therapeutics signed an exclusive Canadian distribution pact with NanoPass Technologies for MicronJetTM600 intradermal delivery devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the aesthetic lasers market as all professionally operated ablative and non-ablative laser systems, stand-alone or hybrid, sold for cosmetic skin resurfacing, hair removal, tattoo or pigment clearance, vascular treatments, body sculpting, and related dermatologic indications. Equipment rentals, consumables, and non-laser energy devices (IPL, RF, ultrasound) fall outside this value pool.

Home-use beauty gadgets and consumable handpieces are not included in the revenue base.

Segmentation Overview

- By Type

- Ablative Lasers

- Carbon Dioxide (CO₂) Laser

- Erbium Laser

- Non-Ablative Lasers

- Pulsed-Dye Laser (PDL)

- Nd:YAG Laser

- Alexandrite Laser|

- Diode Laser

- Ablative Lasers

- By Modality

- Standalone Laser Systems

- Multiplatform / Hybrid Systems

- By Portability

- Non-Portable

- Portable

- By Application

- Skin Resurfacing & Rejuvenation

- Hair Removal

- Acne & Scar Management

- Tattoo Removal

- Body Sculpting & Skin Tightening

- Vascular & Pigmented Lesion Treatmen

- By End User

- Hospitals

- Dermatology & Aesthetic Clinics

- Medical Spas & Beauty Centres

- Ambulatory Surgical Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- GCC

- South Africa

- Rest of Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview dermatologists, medical-spa directors, device distributors, and regulatory consultants across North America, Europe, Asia-Pacific, and the Gulf. These conversations clarify real-world average selling prices, replacement cycles, patient mix shifts, and regional reimbursement wrinkles, allowing us to cross-check secondary findings and fine-tune assumptions.

Desk Research

Mordor analysts first map the demand universe with open datasets from bodies such as the American Society of Plastic Surgeons, the International Society of Aesthetic Plastic Surgery, Eurostat procedure registries, and the US FDA 510(k) database that tracks laser approvals. Trade association shipment logs, import-export ledgers from Volza, and patent pulse checks on Questel help us benchmark installed base growth and technology refresh. Financial filings gathered through D&B Hoovers and news flows screened on Dow Jones Factiva round out competitive signals, pricing trends, and capacity moves.

Additional context is drawn from peer-reviewed dermatology journals, national health expenditure dashboards, and customs codes for HS 9018 instruments, ensuring that baseline volumes tie back to verifiable public records. The sources cited above are illustrative; many more feeds underpin desk validation.

Market-Sizing & Forecasting

A top-down model begins with documented procedure counts and average laser utilization hours per site, which are then married to typical system lifespans to gauge annual unit demand. Select bottom-up checks, supplier invoice samples and channel margin probes, validate totals before adjustments. Key variables include: 1) annual laser hair-removal sessions, 2) global medical-spa footprint, 3) device ASP progression, 4) regulatory approval momentum, and 5) clinic replacement cadence. A multivariate regression links these drivers to historic revenue, while scenario analysis cushions for macro shocks and currency swings. Gaps in bottom-up granularity are bridged by expert-agreed load factors and regional mix weights.

Data Validation & Update Cycle

Outputs face a three-layer review: statistical outlier scans, senior analyst sign-off, and a pre-publication refresh. We revisit models annually and trigger mid-cycle updates whenever major recalls, reimbursement shifts, or blockbuster platform launches meaningfully move the market.

Why Mordor's Aesthetic Lasers Baseline Stands Reliable

Published numbers vary because publishers slice the device set differently, pick unlike ASP bases, and refresh at dissimilar cadences. By anchoring scope strictly to laser hardware sales and by reconciling clinic-level procedure data with trade flows, Mordor delivers a balanced midpoint buyers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.23 billion (2025) | Mordor Intelligence | - |

| USD 1.60 billion (2024) | Global Consultancy A | Excludes ablative platforms and applies aggressive price erosion assumptions |

| USD 2.38 billion (2024) | Industry Association B | Adds consumable handpieces and keeps 2023 FX rates without discount adjustments |

| USD 5.98 billion (2024) | Market Watcher C | Combines lasers with non-laser energy devices, inflating base year |

The comparison shows that scope creep, price baselines, and refresh timing explain most divergences. Mordor's disciplined definitions, cross-checked variables, and annual recalibration produce a transparent, repeatable baseline for confident decision-making.

Key Questions Answered in the Report

How big is the Aesthetic Lasers Market?

The Aesthetic Lasers Market size is expected to reach USD 3.52 billion in 2026 and grow at a CAGR of 9.04% to reach USD 5.43 billion by 2031.

Which is the fastest growing region in Aesthetic Lasers Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Aesthetic Lasers Market?

In 2025, the North America accounts for the largest market share in Aesthetic Lasers Market.

Why are multiplatform hybrid systems gaining popularity?

They enable clinics to treat multiple indications with a single console, improving return on investment and reducing floor-space requirements.

Page last updated on: