Ophthalmic Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

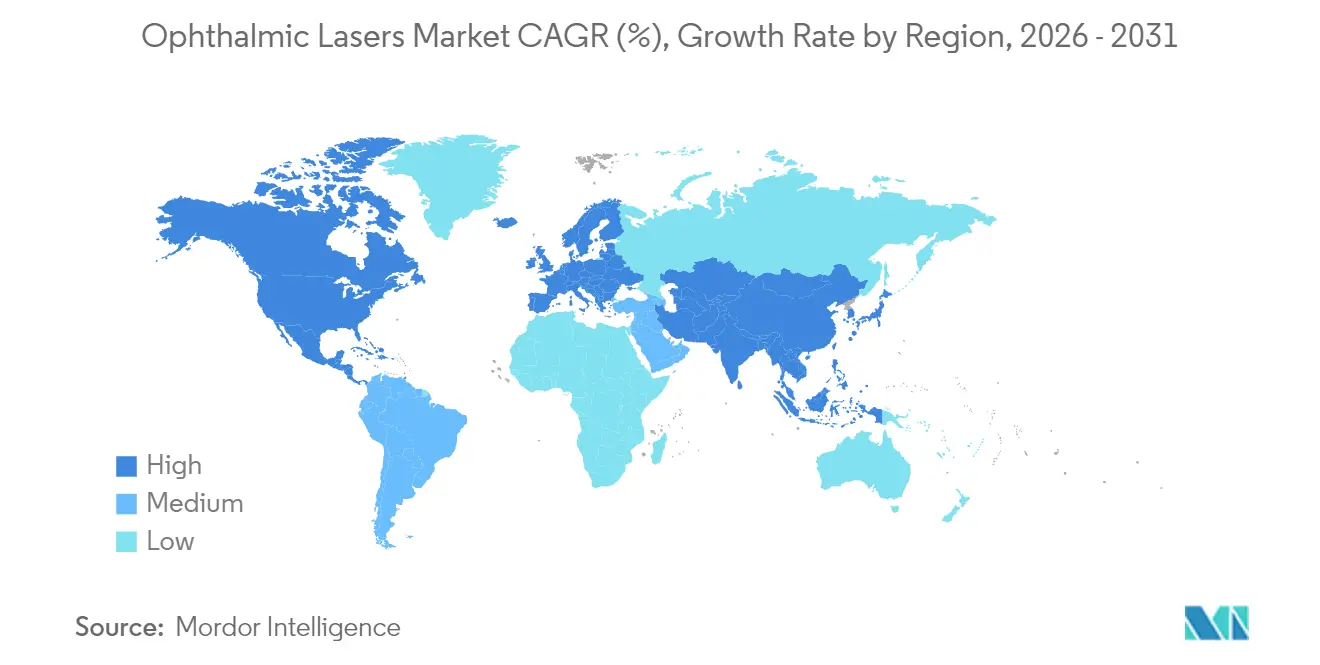

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Lasers Market Analysis by Mordor Intelligence

ophthalmic lasers market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.56 billion with 2031 projections showing USD 2.05 billion, growing at 4.64% CAGR over 2026-2031. Momentum derives more from precision-engineering upgrades than volume expansion, with femtosecond platforms setting new speed benchmarks while retaining tissue accuracy. North America anchors demand through high procedural volumes and early regulatory approvals, yet Asia-Pacific supplies the steepest growth curve as rising myopia and aging demographics converge. The sustained shift toward ambulatory surgery centers (ASCs) and office-based suites is reshaping capital-equipment preferences toward portable, integrated platforms. Competition now pivots on AI-ready systems that compress treatment times, improve outcome predictability, and streamline clinical workflows, allowing premium pricing even under cost-containment pressure.

Key Report Takeaways

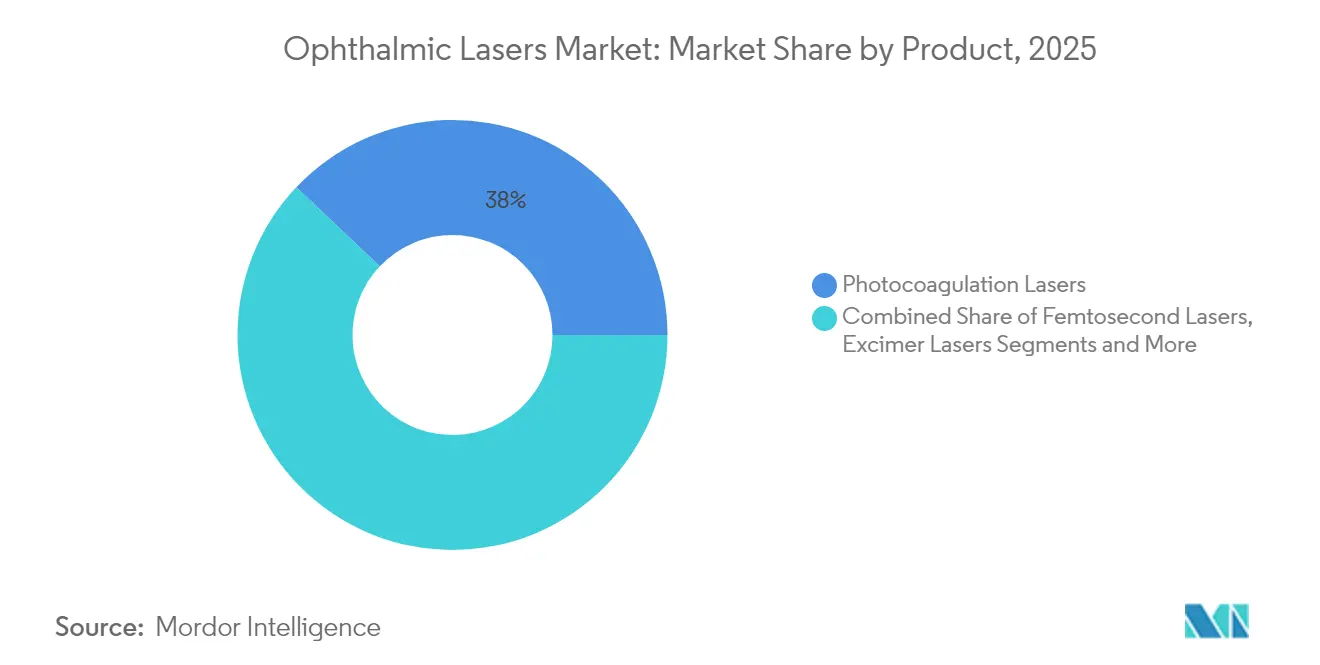

- By product type, photocoagulation lasers held 37.95% of the ophthalmic lasers market share in 2025, while femtosecond lasers are projected to expand at an 8.45% CAGR through 2031.

- By application, cataract surgery devices commanded 33.72% share of the ophthalmic lasers market size in 2025; refractive error corrections are forecast to grow fastest at 9.05% CAGR to 2031.

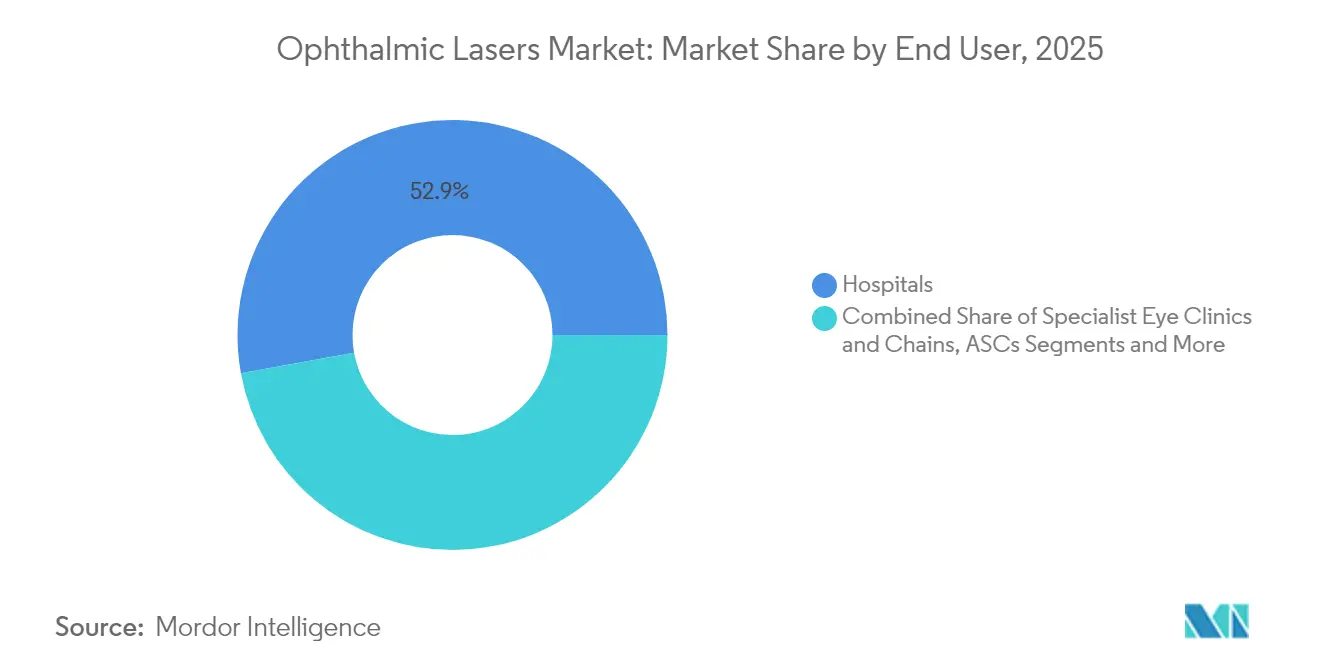

- By end user, hospitals maintained a 52.85% revenue share in 2025, whereas ASCs are advancing at a 6.85% CAGR through 2031.

- By geography, North America led with 36.95% revenue share in 2025, while Asia-Pacific is on track for a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ophthalmic Lasers Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of ophthalmic disorders | +1.20% | Global, APAC focus | Long term (≥ 4 years) |

| Rising regulatory approvals & clearances | +0.80% | North America & EU | Medium term (2-4 years) |

| Continuous femtosecond & excimer upgrades | +1.00% | Global, developed markets | Medium term (2-4 years) |

| Expanding optometrist scope-of-practice laws | +0.40% | North America | Long term (≥ 4 years) |

| Portable low-energy tabletop lasers | +0.60% | Emerging markets | Short term (≤ 2 years) |

| AI-driven personalised ablation profiles | +0.70% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Ophthalmic Disorders

Cataract cases already affect over 20.5 million Americans and continue to climb, guaranteeing a steady patient pool for laser-assisted surgeries. Asia-Pacific adds additional pressure as visual-impairment prevalence rose 17.9% from 1990 to 2015, mainly because of urban myopia and diabetes-linked retinopathy.[1]Asia-Pacific Journal of Ophthalmology Editors, “Visual Impairment Trends 1990-2015,” journals.lww.comThese overlapping pathologies often require multipurpose laser platforms capable of photocoagulation, capsulotomy, and trabeculoplasty in a single session, encouraging providers to purchase broad-spectrum systems. The demographic wave also underpins service-contract revenue, as high device utilization necessitates predictable maintenance. Manufacturers with complete portfolios are therefore better positioned to capture the compounding demand across cataract, refractive, and retinal indications.

Rising Regulatory Approvals & Clearances

Regulators have become more receptive to genuine innovations, shortening time-to-market. The FDA cleared Bausch + Lomb’s Teneo excimer platform in 2024, the first such approval in two decades. LumiThera’s Valeda system secured authorization as the inaugural photobiomodulation therapy for dry AMD, widening therapeutic frontiers. Parallel activity in Europe saw ViaLase win a CE mark for femtosecond glaucoma therapy and Espansione Group gain approval for photobiomodulation devices. Each clearance enlarges the addressable patient pool and sets clinical precedent, easing future submissions and supporting a healthy pipeline of differentiated offerings.

Continuous Femtosecond & Excimer Technology Upgrades

Carl Zeiss Meditec’s VisuMax 800 operates at 2,000 kHz—quadrupling legacy speed—while preserving centration accuracy, shortening procedure times and enhancing patient comfort. Johnson & Johnson’s ELITA platform shows superior refractive precision in early trials, and Bausch + Lomb’s Teneo delivers 500 Hz ablation with 1,740 Hz eye tracking for unmatched on-axis control. These advancements raise the entry bar for rivals and shorten replacement cycles as surgeons demand the newest performance benchmark every five to seven years.

AI-Driven Personalized Ablation Profiles

Artificial intelligence now parses multimodal imaging to refine ablation maps at the micron level, boosting postoperative predictability. The Kane formula and Hill-RBF calculators already outperform conventional nomograms in IOL power determination. Emerging systems apply similar machine-learning logic to intraoperative guidance, dynamically adjusting energy delivery based on real-time corneal response. Vendors able to pair hardware upgrades with proprietary AI engines build defensible product ecosystems that lock in recurring software revenue and drive premium differentiation.

Restraints Impact Analysis of Ophthalmic Lasers Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Purchase & Maintenance Cost | -1.40% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Shortage Of Laser-Trained Ophthalmic Surgeons | -0.90% | Global, severe in rural areas | Long term (≥ 4 years) |

| Reimbursement Uncertainty For FLACS Codes In EMs | -0.60% | Emerging markets focus | Medium term (2-4 years) |

| Competing Premium IOL & Pharma Pipelines Curbing Demand | -0.50% | Developed markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High System Purchase & Maintenance Cost

Advanced laser units range between USD 500,000 and USD 1.5 million, while annual service contracts absorb 8-12% of that figure, stressing smaller practices. Emerging economies face 25-40% import mark-ups and currency-related volatility that prolong payback periods. Although leasing and shared-usage models alleviate cash flow barriers, they often cap monthly shots or procedures, limiting revenue upside. Consequently, group purchasing and multi-site health networks favor vendors that bundle fleet-wide service at predictable rates, nudging the market toward a few scale-efficient suppliers.

Shortage of Laser-Trained Ophthalmic Surgeons

The American Academy of Ophthalmology projects a 30% workforce deficit by 2035, with rural adequacy falling to 29%.[2]American Academy of Ophthalmology Workforce Committee, “Ophthalmologist Supply and Demand 2025-2035,” aao.org Laser proficiency requires extended fellowships, and the 6-12 month learning curve suppresses productivity during training. Urban clustering of qualified surgeons leaves vast regions underserved, dragging procedure volumes despite latent demand. Tele-mentoring and simulation labs are proliferating, yet capacity expansion lags technological progress, tempering uptake in both developed and emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ophthalmic Lasers Market Segment Analysis

By Product:

Femtosecond Innovation Reshapes Precision SurgeryPhotocoagulation systems retained 37.95% of the ophthalmic lasers market share in 2025, a testament to their entrenched role in retinal care. However, femtosecond platforms are on an 8.45% CAGR trajectory through 2031, propelled by ultrafast pulse rates that slash chair time and discomfort. The VisuMax 800’s 2,000 kHz speed not only enhances throughput but also supports SMILE procedures that preserve corneal biomechanics. In contrast, excimer devices rely on incremental gains such as Teneo’s 1,740 Hz eye-tracking, reinforcing their place in surface ablation. Nd:YAG disruptors continue to anchor capsulotomy and vitreolysis, while selective laser trabeculoplasty (SLT) systems broaden glaucoma therapy options. Multipurpose consoles that merge photocoagulation with femtosecond or Nd:YAG modules are increasingly favored for capital efficiency.

The femtosecond surge underscores a transition from thermal to photo-disruptive precision. Vendors integrating AI-driven planning and ergonomic improvements command premium placements. As a result, segment players investing in cross-platform ecosystems are set to outpace niche specialists, especially in high-volume ASCs seeking all-in-one devices. In value terms, the ophthalmic lasers market size for femtosecond equipment is projected to capture USD 0.64 billion by 2031, reflecting sustained replacement demand among early adopters.

By Application:

Refractive Corrections Accelerate Beyond Therapeutic InterventionsCataract-oriented lasers safeguarded a 33.72% stake in 2025, yet refractive error corrections promise the quickest lift at 9.05% CAGR to 2031, fuelled by consumer willingness to finance vision-enhancement electives. Femtosecond-assisted LASIK and SMILE now compete on optical-zone stability and reduced dry-eye incidence, with small-incision lenticule implantation reporting 87% visual-acuity maintenance.

Sub-threshold micropulse modalities advance retinal-disease management by limiting collateral damage, while SLT innovations like Alcon’s Voyager DSLT remove gonio-lens handling, simplifying glaucoma workflows. The ophthalmic lasers market size for refractive applications is forecast to expand from USD 0.5 billion in 2026 to USD 0.77 billion by 2031 as elective procedure volumes climb. Integrated consoles capable of toggling between cataract fragmentation, corneal reshaping, and trabeculoplasty appeal to mixed-case sites, further blurring historical single-indication boundaries.

By End User:

ASCs Capitalize on Surgical Migration TrendsHospitals still account for 52.85% of global revenue, yet ASCs are sprinting ahead at 6.85% CAGR to 2031. U.S. ASC procedure counts are set to rise 21% to 44 million by 2034, with cataracts alone nearing a 19% share. This volume surge tilts purchasing toward compact, maintenance-lite lasers that fit small footprints and enable rapid patient turnover.

Office-based surgical suites, adopted by about 150 U.S. eye practices, augment profit margins through self-pay refractive lens exchange and premium IOL implants. Academic centers, while slower-growing, sustain demand for research-grade versatility and training features. Consequently, manufacturers must segment portfolios: rugged, turnkey units for ASCs and advanced, data-rich systems for teaching hospitals.

By Technology Integration:

Stand-Alone Systems Compete with Workflow IntegrationStandalone lasers offer modular flexibility, letting clinics upgrade optics or software piecemeal, whereas integrated phaco-laser workstations centralize multiple tasks into a single footprint. Alcon’s Unity VCS melds vitreoretinal photocoagulation with cataract and glaucoma modules to fit high-volume theatres.

Large eye-care networks value the harmonized data flows and streamlined training that integrated rigs supply, but smaller sites prefer the capex agility of discrete boxes. Device makers respond by offering dual roadmaps: a hybrid field-upgradable portfolio and a fully integrated flagship line, protecting share across divergent buyer profiles. As interoperability standards mature, cloud-enabled platforms may eventually erase the trade-off, creating an open ecosystem while preserving upgrade optionality.

Geography Analysis

North America Ophthalmic Lasers Market

North America led the ophthalmic lasers market with 36.95% revenue in 2025 and is expected to post mid-single-digit growth through 2031. High equipment penetration, favorable reimbursement, and early FDA clearances keep the region ahead, yet looming surgeon shortages cap upside. Projections show a 30% ophthalmologist deficit by 2035, with rural access dipping lowest. Migration to ASCs and value-based payment rewards lasers that cut complications, but rising capital costs nudge some practices toward leasing consortia and shared-service models.

APAC, EMEA and South America Ophthalmic Lasers Market

Asia-Pacific is the fastest-advancing territory at 6.05% CAGR. Escalating myopia—now exceeding 80% in certain urban young-adult cohorts—combines with aging populations to swell cataract and refractive workloads. Yet uneven surgeon distribution and price-sensitive procurement favor stripped-down, low-maintenance designs. China’s volume-based procurement squeezes margins, pushing manufacturers to offer value-tier SKUs, while India and Southeast Asia reward portable handheld units suited to outreach camps. Robust clinical-training alliances and philanthropic programs will be pivotal in converting underlying disease prevalence into sustainable device adoption. Europe exhibits steady expansion courtesy of CE-mark alignment and universal insurance coverage. CE approvals in 2024 for femtosecond glaucoma and photobiomodulation devices demonstrate regulatory agility. Country-level reimbursement nuances, however, generate market fragmentation, requiring vendors to tailor value-submission dossiers by payer. Western Europe champions clinical-outcome data while Eastern markets lean on affordability, creating bifurcated demand streams within the continent. Middle East & Africa and South America house significant unmet surgical need but grapple with supply-chain gaps and currency risk. Donation programs, mobile surgery caravans, and government co-payment schemes could gradually unlock latent potential, though short-term growth remains modest.

Regulatory Landscape

Ophthalmic laser systems are regulated as medical devices, and market entry is shaped by region-specific pathways such as the US FDA 510(k) process for many Class II ophthalmic laser devices (for example, the Navilas Laser System 577sl received FDA 510(k) clearance on October 29, 2025 under 21 CFR 886.4390). In the US, manufacturers also align product and facility compliance to FDA expectations for device regulation and laser product requirements, including registration/listing and UDI where applicable, which affects launch sequencing and the pace of portfolio refreshes.

International standards continue to anchor safety and performance requirements and support cross-border submissions. ISO 15004-2:2024 updated optical radiation safety requirements for ophthalmic instruments, and the publication of SIST EN IEC 60601-2-22:2020/A11:2026 further aligned laser equipment safety expectations with EU MDR (EU) 2017/745. On the quality side, the FDA Quality Management System Regulation (QMSR) became effective on February 2, 2026, reinforcing quality-system rigor and increasing the value of globally harmonized QMS and traceability for suppliers serving multiple geographies.

Competitive Landscape

Industry consolidation has produced a cohort of diversified leaders such as Alcon, Johnson & Johnson Vision, Bausch + Lomb, and Carl Zeiss Meditec, collectively controlling the majority of global revenue. These firms leverage broad catalogs, regulatory mastery, and global distribution to defend their share. Alcon’s USD 356 million purchase of LENSAR in March 2025 deepens its femtosecond arsenal and dovetails with the Unity VCS integrated suite. Johnson & Johnson complements its TECNIS IOL franchise with AI-enabled laser planning tools, tying pre-op diagnostics to intra-op execution for seamless refractive outcomes.

Carl Zeiss Meditec differentiates on cutting-edge speed and ergonomic advances embodied in VisuMax 800, appealing to high-volume refractive clinics. Bausch + Lomb counters with Teneo’s eye-tracking superiority, aiming at centers that prioritize surface-ablation accuracy. New entrants such as ForSight Robotics, armed with USD 125 million Series B funding, target automation niches, signaling a potential shift toward robot-assisted laser execution.

Price competition intensifies in emerging economies where stripped-down models gain traction. Tier-two vendors compete on portability and service responsiveness rather than raw performance. Strategic alliances that bundle hardware, consumables, software analytics, and extended-service contracts are emerging as the dominant go-to-market template, further raising the barriers for single-product challengers.

Ophthalmic Lasers Industry Leaders

Alcon

Johnson & Johnson Vision

Carl Zeiss Meditec

Bausch + Lomb

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Ophthalmic Lasers Market Companies Covered in this Report

- Alcon

- Johnson & Johnson

- Carl Zeiss

- Bausch + Lomb

- Topcon Corp

- IRIDEX Corp

- Lumenis

- Lumibird Group

- Nidek

- Ellex Medical Laser

- Coherent

- Ziemer Group

- SCHWIND eye-tech-solutions

- LENSAR

- Lightmed

- Quantel Laser USA

- iVIS Technologies

- ViaLase

- ForSight Robotics

- WaveLight GmbH

- HAAG-Streit

Market Opportunities and Future Outlook

Workflow-integrated platforms represent a key opportunity as providers shift procedures into ASCs and office-based suites and prioritize shorter chair time, reduced variability, and fewer handoffs between diagnostics and treatment. Technology roadmaps that integrate imaging and planning into laser delivery (including AI-augmented OCT concepts) are reinforcing this direction, alongside purchasing behavior that favors multipurpose or unified workstations over single-indication consoles when footprint and staffing are constrained. Recent regulatory clearances and approvals also broaden the addressable mix beyond refractive and cataract use cases into glaucoma and retina-adjacent therapeutic frontiers, supporting portfolio bundling at high-volume sites.

Glaucoma and next-generation therapeutic applications add further room for growth where laser approaches can reduce dependency on chronic medications or implants, particularly as optometrist scope-of-practice expansion and surgeon scarcity push demand for more efficient care models. Evidence of market movement includes BVI Medicals FDA 510(k) clearance in April 2025 for Leos (Laser Endoscopy Ophthalmic System) for minimally invasive glaucoma surgery, and the October 2025 FDA 510(k) clearance for the Navilas Laser System 577sl, both of which expand regulated pathways for newer procedural workflows. At the same time, compliance complexity and updated standards, including ISO 15004-2:2024 and IEC 60601-2-22 updates via A11:2026, raise the bar for vendors that can package safety engineering, documentation, and service readiness into scalable regional deployments.

Recent Industry Developments in Ophthalmic Lasers Market

- June 2026: ZEISS Medical Technology signed a strategic agreement with Aier Eye Hospital Group to install 25 VISUMAX 800 femtosecond lasers across Aiers domestic and international networks starting later in 2026. The multi-unit rollout concentrates advanced refractive capacity within a large hospital chain and strengthens ZEISS positioning for standardized, network-level procurement and training.

- March 2026: Bausch + Lomb announced positive 24-month U.S. clinical trial results for the ELIOS System, an implant-free procedure using excimer laser technology for open angle glaucoma. The data package supports broader clinical confidence in laser-based glaucoma options and reinforces competitive differentiation versus device-implant and medication-centered pathways.

- November 2024: LumiTheras Valeda Light Delivery System received FDA clearance as a photobiomodulation therapy for vision loss in dry AMD. The clearance widened the therapeutic scope for light-based systems beyond traditional photocoagulation and refractive indications, encouraging vendors to invest in new clinical categories and supporting evidence-generation activity.

Ophthalmic Lasers Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as revenues from purpose-built ophthalmic laser systems used in human eye care for diagnosis and treatment across refractive, cataract, glaucoma, and retinal procedures, counted at the point of sale to care providers and facilities.

Scope exclusions: Excludes consumables, service and maintenance contracts, refurbished units, veterinary-use lasers, and broader surgical laser systems that are not specifically used for ophthalmic care.

Segments Covered in This Report

- By Product

- Femtosecond Lasers

- Excimer Lasers

- Nd:YAG Photodisruption Lasers

- Photocoagulation/Diode & Argon Lasers

- Selective Laser Trabeculoplasty (SLT) Lasers

- Pattern-Scanning Photocoagulators

- Combined Multipurpose Platforms

- By Application

- Cataract Surgery (FLACS, Capsulotomy)

- Refractive Error Correction (LASIK, SMILE, PRK)

- Glaucoma (SLT, Cylophotocoagulation)

- Diabetic Retinopathy & DME

- Age-Related Macular Degeneration

- Pediatric & Other Retinal Disorders

- By End User

- Hospitals

- Specialist Eye Clinics & Chains

- Ambulatory Surgery Centers (ASC)

- Academic & Research Institutes

- By Technology Integration

- Stand-alone Laser Systems

- Integrated Phaco-Laser Workstations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public health and procedure context, so our assumptions sit on known demand signals and not just vendor messaging. We referenced sources such as the World Health Organization (vision impairment burden), the US CDC and National Eye Institute (disease prevalence and screening guidance), and OECD and World Bank indicators (health spending and access trends) to keep the demand side realistic.

We also reviewed regulatory and product context from sources such as the US FDA device databases and guidance notes, plus technical and clinical evidence in peer-reviewed ophthalmology journals to understand where lasers are standard of care versus optional. Supplier side clues were taken from annual reports, investor presentations, and press releases, and we used paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export checks where relevant. The sources listed here are illustrative, and we relied on additional public references to compile data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary calls and surveys were used to pressure-test procedure mix assumptions and pricing, especially where public statistics do not separate laser-assisted procedures cleanly. We covered demand-side voices from hospitals, ambulatory surgical centers, and specialty eye clinics, and we also spoke with supply-side and channel participants to confirm installation trends and replacement timing across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 46% |

| Mid tier: 59% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 15% | Managers: 44% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where procedure volumes and treated patient pools are reconstructed by geography, and then converted into annual laser system demand using adoption and replacement logic. To keep the totals grounded, results were corroborated with selective bottom-up approximations, such as a roll-up of visible supplier revenue exposure, distributor channel checks, and sampled average selling price (ASP) times unit volume for key laser categories.

Inputs that mattered most included cataract and refractive procedure volumes, glaucoma and diabetic retinopathy treatment rates, installed base and average replacement cycles for laser platforms, ASP ranges by laser type, and facility mix shifts between hospitals, ambulatory surgical centers, and specialty eye clinics. Where a local market had thin disclosure, gaps were handled by using proxy procedure indicators and then adjusting with interview feedback until the implied units and price bands stayed plausible.

For forecasting, scenario analysis was used because near-term demand is sensitive to elective procedure recovery, capital budget cycles, and adoption speed for newer platforms. Each scenario was anchored to expert views on procedure growth and pricing direction, then reconciled back to macro health spending and regulatory signals so the curve did not drift unrealistically.

Data Validation & Update Cycle

Outputs were checked against independent signals such as procedure trend direction, trade flow reasonability for major importing countries, and the implied installed base growth versus replacement needs. If a country total looked too high or low, the assumptions were re-opened, and follow-up outreach was triggered to confirm whether the issue came from adoption rates, ASP bands, or timing of capital purchases.

Before sign-off, the model goes through multi-step analyst reviews, with variance checks across regions and cross-links to related ophthalmology device spending patterns. The report is refreshed annually, and interim updates are done when material events occur, after which a final pre-delivery pass is completed so clients receive the latest consistent view.

Mordor Intelligence's Ophthalmic Lasers Market Size Versus Other Published Estimates

Published numbers for ophthalmic lasers do not always match, and the differences are usually explained by what is included and when it is counted. In this space, a lot of the spread comes from whether service revenue and refurbished systems are included, along with which laser types and care settings are treated as in-scope.

Key gap drivers also show up in how procedure demand is translated into system sales, since adoption rates and replacement cycles can move totals meaningfully. Currency timing, the chosen base year, and how ASP progression is handled can further widen the range, particularly when forecasts lean conservative or assume faster technology upgrades without direct validation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.63 B (2026) | |

| Industry Research Publisher A | USD 1.58 B (2024) | Uses a different base year and reporting window, and the scope language does not clearly separate system sales from adjacent revenue like services, which can shift what gets counted in the total. |

| Market Analytics Firm B | USD 1.30 B (2023) | Starts from an earlier base year and may apply broader average pricing and adoption assumptions, which can understate later-cycle installations when replacement demand and procedure throughput rise. |

Procedure volume direction, installed base replacement signals, and interview-confirmed ASP bands are the checks that keep Mordor Intelligence tied to system-only revenues, which helps explain why its 2026 value sits between earlier base-year counts and estimates built with looser scope boundaries. The comparison shows that aligning the definition to device sales and then validating adoption and pricing assumptions produces a more repeatable number that can be traced back to clear drivers.

Key Questions Answered in the Report

What is the current size of the ophthalmic lasers market in 2026?

The ophthalmic lasers market stands at USD 1.63 billion in 2026 and is forecast to reach USD 2.05 billion by 2031.

Which product segment is growing fastest?

Femtosecond lasers are projected to grow at an 8.45% CAGR through 2031 as speed and precision upgrades encourage rapid adoption.

Why are ambulatory surgery centers important for future sales?

ASCs focus on high-throughput eye procedures, with cataract surgeries alone making up nearly 19% of projected ASC volume, driving demand for compact, efficient lasers.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest trajectory at 6.05% CAGR due to escalating myopia rates and expanding access to cataract care.

How is artificial intelligence changing laser eye surgery?

AI refines ablation profiles and intraoperative adjustments, improving refractive accuracy and creating a premium differentiator for systems embedded with machine-learning engines.

What limits broader adoption of advanced laser systems?

High capital costs and a shortage of trained laser surgeons, particularly in rural and emerging markets, restrain penetration despite strong underlying demand.

Page last updated on: