End User Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

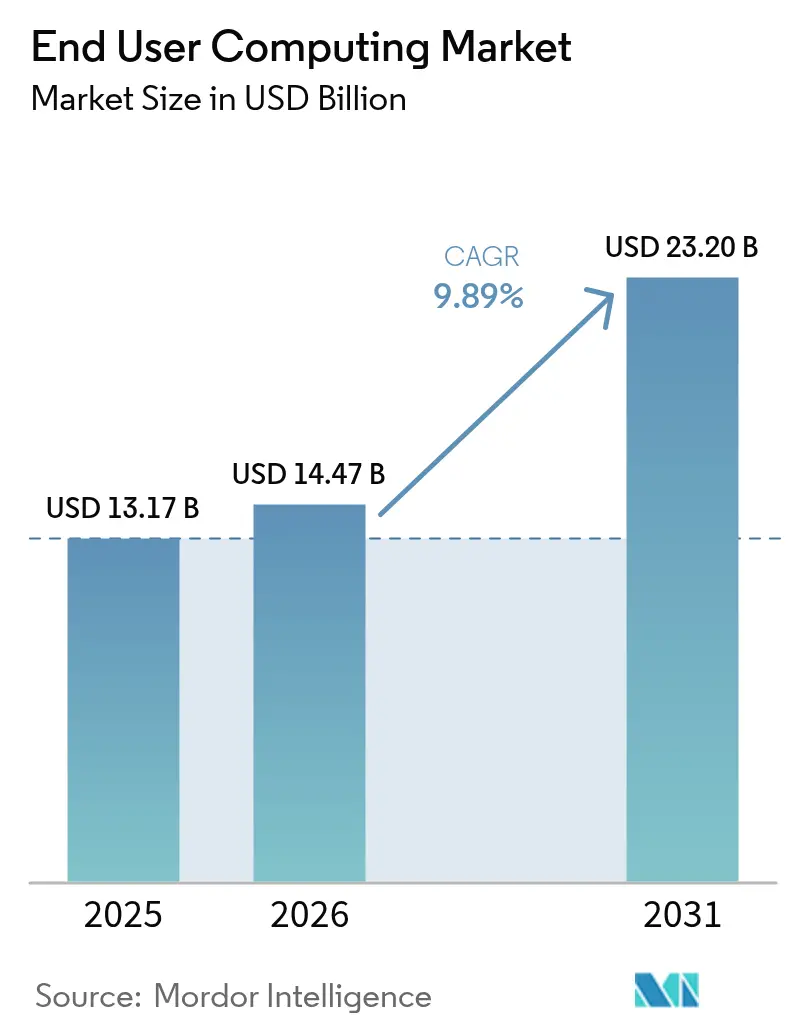

| Market Size (2026) | USD 14.47 Billion |

| Market Size (2031) | USD 23.2 Billion |

| Growth Rate (2026 - 2031) | 9.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

End User Computing Market Analysis by Mordor Intelligence

The End-User Computing market size was valued at USD 13.17 billion in 2025 and estimated to grow from USD 14.47 billion in 2026 to reach USD 23.2 billion by 2031, at a CAGR of 9.89% during the forecast period (2026-2031). This sustained expansion is driven by large-scale digital workplace programs, mandatory hardware refresh cycles ahead of the Windows 10 end-of-support deadline, and a rapid shift toward cloud-hosted virtual desktops that reduce capital expenditures while enhancing flexibility. Demand is further amplified by organizations rolling out AI-capable endpoints that can process generative models locally, as well as the strong adoption of bring-your-own-device (BYOD) policies across 82% of enterprises. Additionally, there is a growing investment in unified endpoint management to protect a diverse range of devices. Competitive intensity remains high as vendors race to bundle endpoint operating systems, virtualization software, cloud services, and AI tooling into a single value proposition, forcing buyers to assess road-map certainty, licensing stability, and data-sovereignty safeguards. The End-User Computing market also benefits from telecom-edge partnerships that push ultra-low-latency augmented-reality and virtual-reality workloads closer to field workers, thereby expanding the addressable use cases.

Key Report Takeaways

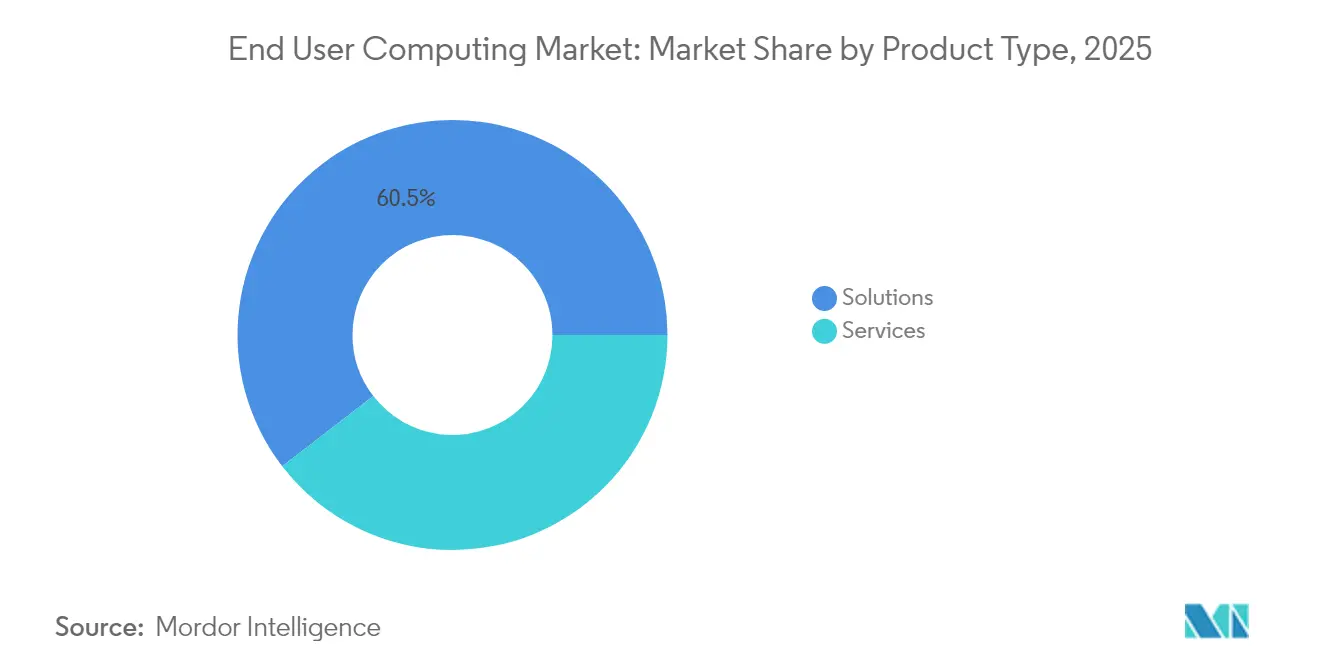

- By product type, Solutions held the largest market share in 2025 at 60.45%, while Managed Services are projected to grow the fastest from 2026 to 2031 with a CAGR of 10.05%.

- By organization size, Large Enterprises dominated in 2025 with a 45.85% share, whereas Small and Medium Enterprises are expected to expand most rapidly, growing at a CAGR of 10.25%.

- By deployment mode, on-premises solutions led with a 28.95% market share in 2025, while Cloud deployments are forecast to grow fastest at a CAGR of 10.38%.

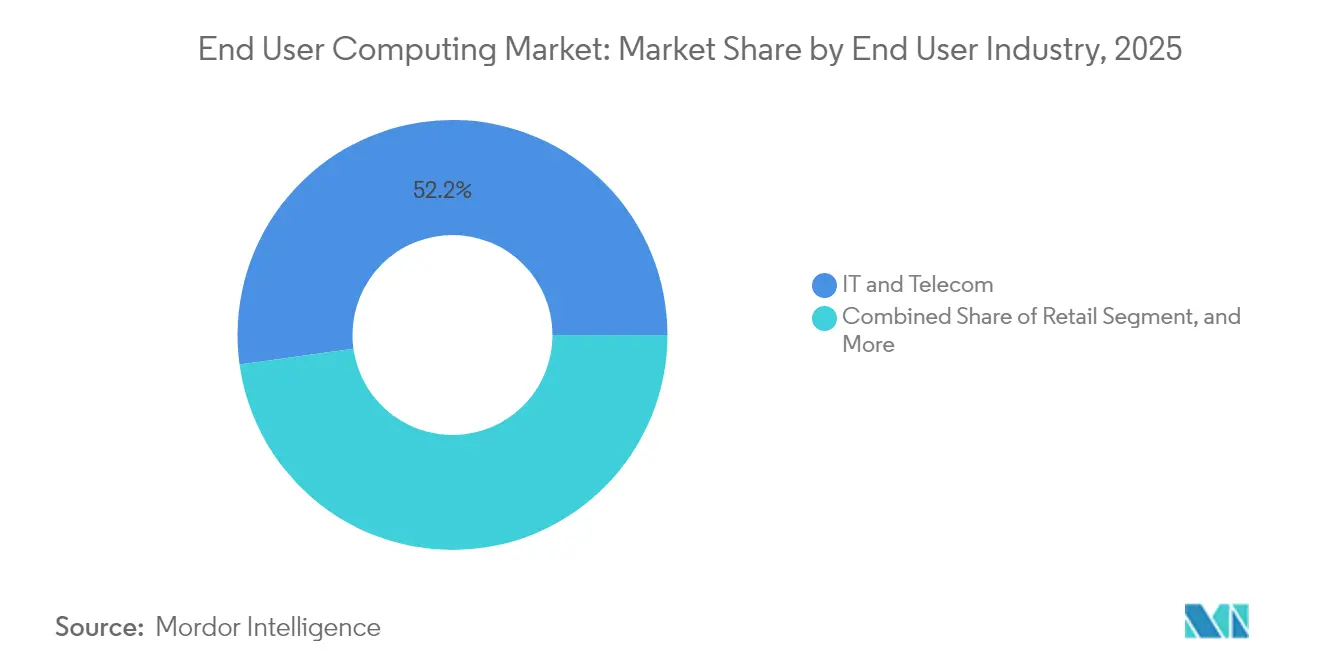

- By end-user industry, IT and Telecom accounted for the largest share in 2025 at 52.20%, while Healthcare is projected to be the fastest-growing sector with a CAGR of 9.97%.

- By delivery model, Virtual Desktop Infrastructure led with a 36.65% share in 2025, while Desktop-as-a-Service is expected to grow at a CAGR of 10.12%.

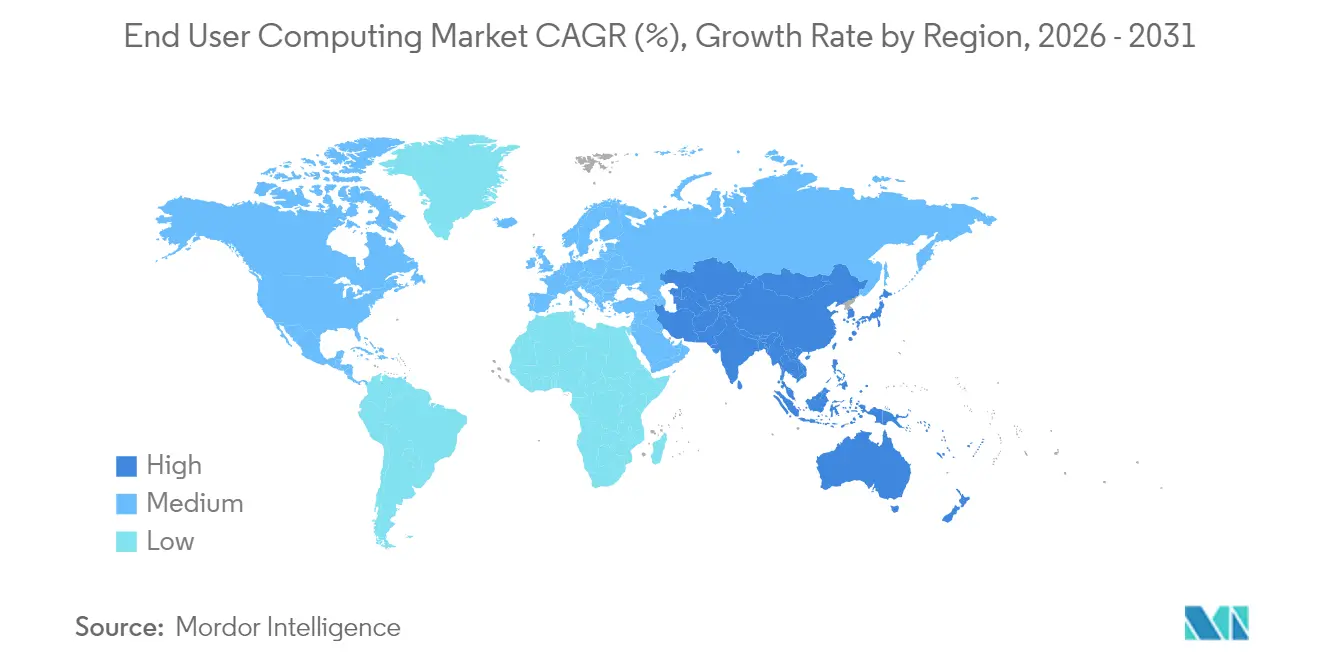

- By geography, the Asia Pacific was the largest regional market in 2025 with a 62.40% share, and it is also forecast to be the fastest-growing region with a CAGR of 10.72%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global End User Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drive to increase employee productivity via digital workspaces | +2.8% | Global (APAC leading) | Medium term (2-4 years) |

| Growing adoption of cloud-based desktop and application virtualization | +2.5% | North America, Europe, fast-scaling APAC | Short term (≤ 2 years) |

| Rising BYOD policies and mobile workforce requiring unified endpoint management | +2.1% | Global | Short term (≤ 2 years) |

| Windows-10 end-of-support triggering enterprise PC refresh cycles | +1.8% | Global | Short term (≤ 2 years) |

| Emergence of AI-capable endpoints enabling on-device GenAI workloads | +1.6% | North America, APAC | Long term (≥ 4 years) |

| Telco edge-cloud partnerships enabling ultra-low-latency EUC for field AR-VR | +0.9% | APAC, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Drive to Increase Employee Productivity via Digital Workspaces

Enterprises are reimagining productivity by combining virtual desktops, collaboration suites, and AI copilots inside a single digital workspace. Organizations that reach advanced workplace maturity levels report a 57.8% boost in positive employee experience metrics, thanks to quicker access to resources, app self-service, and uniform security controls. Microsoft’s early field data shows AI copilots save roughly 10 hours per employee each month, translating into tangible capacity gains. The result is a measurable uplift in innovation, inclusion, and well-being, as seamless device hopping and automated workflows reduce friction and burnout.

Growing Adoption of Cloud-Based Desktop and Application Virtualization

Consumption-based desktop hosting is scaling fast because it eliminates capital expenditure and shortens deployment timelines from months to days. Azure Virtual Desktop production use already spans 26% of surveyed organizations, with 58% planning rollouts within the next two years, driven by policy-based scaling, pay-as-you-go pricing, and native Microsoft 365 integration. Healthcare providers illustrate the upside: browser-delivered desktops logged sub-minute sign-ins, freeing clinicians to spend more time with patients and less on IT wait states.

Rising BYOD Policies and Mobile Workforce Requiring Unified Endpoint Management

The U.S. mobile workforce alone now exceeds 93.5 million workers, forcing IT teams to secure personal devices, such as phones, tablets, and laptops, without hindering user choice.[3]Hypori Inc., “Mobile Workforce Strategies,” hypori.comA mature BYOD program can save USD 341 per employee each year, yet 82% of breaches still involve human error, prompting firms to invest in zero-trust authentication, remote wipe, and containerized workspaces.[1]Ntiva Inc., “What Your BYOD Policy Needs in 2024,” ntiva.com Unified endpoint management brings policy consistency to this sprawl, integrating device telemetry, patch automation, and experience analytics into a single console.

Windows-10 End-of-Support Triggering Enterprise PC Refresh Cycles

Microsoft ends extended support for Windows 10 in October 2025, exposing unpatched PCs to a 74% higher risk of breach. Hardware-eligibility checks reveal that roughly 40% of business PCs lack TPM 2.0 or a compatible CPU, compelling organizations to either swap devices or virtualize the desktop instead. Many buyers view the mandatory refresh as an opportunity to transition to zero-touch deployments using Windows Autopilot and Intune, while standardizing on AI-ready chipsets to future-proof their investments.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity integrating EUC with legacy applications and infrastructure | -1.4% | Global, heavily regulated verticals | Medium term (2-4 years) |

| High upfront transformation costs for VDI and DaaS migrations | -1.1% | SMEs, cost-sensitive regions | Short term (≤ 2 years) |

| Vendor consolidation-driven license uncertainty | -0.8% | Global VMware customer base | Short term (≤ 2 years) |

| Data-sovereignty concerns hindering full cloud adoption | -0.6% | Europe, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complexity Integrating EUC with Legacy Applications and Infrastructure

Banks, hospitals, and government agencies still depend on thick-client applications tied to specific OS versions, hard-coded drive mappings, or serial-port peripherals. Virtual desktops must replicate these dependencies while guaranteeing millisecond response times in mission-critical workflows. Integration projects therefore add middleware, APIs, and parallel test environments, extending timelines and inflating costs. Change-management gaps further undermine ROI; 73% of employees who move to digital workspaces without structured training feel disengaged, risking project rollback. Firms mitigate the drag by phasing workloads, rewriting monoliths into modular services, and introducing user-experience analytics that flag adoption bottlenecks early.

High Upfront Transformation Costs for VDI and DaaS Migrations

Licensing, infrastructure, consulting, and user-training fees produce steep entry barriers, particularly for SMEs. On-premise VDI requires servers, storage, GPUs, and skilled administrators, whereas cloud-hosted DaaS converts the spend into OPEX but can spike as workforces scale unpredictably. Managed DaaS providers promise savings of up to 60% by pooling expertise and automating patching, yet customers must master metering and right-sizing to dodge cost overruns. Investment hurdles often delay adoption until a major event—such as OS end-of-life or office relocation—creates an unavoidable business case.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Solutions Dominate, Services Accelerate

Solutions retained 60.45% End User Computing market share in 2025, underpinned by mature VDI platforms, device-management suites, and software-asset tools that together generated roughly USD 8 billion in annual recurring revenue. Vendors use unified consoles to orchestrate endpoints, apps, and security, which simplifies compliance audits across thousands of assets. Growth now skews toward managed services, with a 10.05% CAGR, as enterprises prefer outcome-based contracts that offload patching, scaling, and experience monitoring to specialists.

Managed service providers embed AI-driven observability and self-healing capabilities, enabling customers to transition from firefighting tickets to proactive optimization. Healthcare customers, for instance, adopt Device-as-a-Service bundles that convert capex to predictable opex and deliver pre-configured clinical workstations on 36-month refresh cycles, reducing help-desk volumes by double-digit percentages.

By Organization Size: Large Enterprise Scale Meets SME Agility

Large enterprises controlled 45.85% of End User Computing market size in 2025 and rely on tailored integrations, zero-trust overlays, and global federated identity to secure tens of thousands of users. Concurrent licensing and in-house talent give them lower per-seat operating costs, yet hardware refresh mandates and AI upgrade cycles force continual reinvestment.

SMEs, conversely, expand at 10.25% CAGR because cloud-native desktops remove the need for data-center space or specialized staff. Browser-launched workspaces deploy in under 48 hours and include automatic scaling, backup, and compliance templates. For many SMEs the Windows 10 sunset is a trigger to jump straight to cloud desktops, avoiding hardware outlays and accessing Windows 11-ready environments instantly.

By Deployment Mode: Cloud Momentum Outpaces On-Premise Control

On-premise estates still hold a 28.95% share in 2025, favored by defense, finance, and healthcare entities that prioritize data residency and deterministic performance. Co-location within corporate LANs also supports latency-sensitive imaging or CAD tasks. The trade-off is heavy capex and reliance on scarce virtualization experts.

Cloud endpoints are the clear growth engine, with a 10.38% CAGR, led by Azure Virtual Desktop and similar offerings that integrate conditional access, autoscaling, and consumption-based billing. Hybrid blueprints dominate enterprise roadmaps: sensitive workloads stay on-site, while burst capacity, disaster recovery, and contractor access shift to cloud regions nearest to users, lowering latency without ceding governance.

By End-User Industry: IT-Telecom Leads, Healthcare Surges

IT and telecom operators generated 52.20% of their revenue in 2025, leveraging virtual desktops to isolate development sandboxes, secure call-center agents, and experiment with 5G edge computing that hosts AR-enabled field diagnostics. The sector’s technically adept staff accelerates adoption cycles and drives early proof-of-concepts.

Healthcare is logging the fastest 9.97% CAGR as hospitals modernize their clinical workspaces. GPU-accelerated virtual desktops render medical images in real-time, keeping patient data within secure data centers that support telehealth consultations, cross-disciplinary collaboration, and mobile ward rounds. Early pilots show doctors reclaim up to 30 minutes daily and nurses up to 50 minutes through single-sign-on roaming.

By Delivery Model: VDI Foundation, DaaS Innovation

VDI accounted for 36.65% End end-user computing market size in 2025 and remains the backbone for organizations that demand full control over hypervisors, storage, and networking. NVIDIA virtual GPUs enable the seamless operation of graphics-intensive applications for architects and radiologists, maintaining performance parity with high-end workstations.

DaaS, growing at a 10.12% CAGR, removes infrastructure burdens altogether. Microsoft, Citrix, and niche providers combine autoscaling, compliance dashboards, and integrated backup, letting customers spin up global workspaces via API. Gartner projects virtual desktops will be cost-effective for 95% of employees by 2027, highlighting DaaS as the mainstream trajectory for knowledge work.

Geography Analysis

The Asia Pacific controlled 62.40% of the End-User Computing market in 2025 and is projected to post a regional 10.72% CAGR from 2026 to 2031. A Zoho survey reveals that APAC organizations have achieved a 66.35% digital workplace maturity score, five points above the global average, with 76% reaching advanced levels. Penetration of AI-enabled tools (54%) and team chat (72%) epitomizes a mobile-first mentality, while steady 5G rollouts create fertile ground for edge-enhanced virtual desktops.

North America exhibits entrenched VDI estates across regulated sectors and leads the early adoption of AI copilots, which save roughly 10 hours per user per month. The Windows 10 cutoff brings an immediate refresh wave that favors modern endpoint management and DaaS. Europe mirrors the pattern but adds stringent GDPR mandates, steering multinationals toward hybrid deployments that balance local data residency with global cloud scale.

Emerging markets in the Middle East, Africa, and Latin America treat cloud desktops as a leapfrog opportunity to bypass legacy infrastructure. Consumption models align with budget constraints, while telco-edge collaborations promise sub-20-millisecond latency for immersive field maintenance or remote-assistance scenarios. Governments increasingly codify data-localization rules, encouraging regional cloud zones and sovereign VDI stacks that can interconnect with global platforms.

Competitive Landscape

Vendor consolidation has reshaped competitive dynamics, yielding a moderately concentrated field where the top five providers hold about 60% share. KKR carved out VMware’s EUC division for USD 4 billion and re-launched it as Omnissa, instantly inheriting USD 1.5 billion in annual recurring revenue and 26,000 customers. Omnissa is now adding AI-powered diagnostics, self-healing, and “Omni” chat-assistants while extending App Volumes from VDI to physical PCs.

Citrix strengthened its control plane by acquiring eLux, an endpoint OS running on 2.5 million devices, enabling secure, lightweight clients that pair with its management stack. HP targeted the experience layer through its purchase of Vyopta, integrating collaboration analytics that surface meeting-room utilization and voice-quality anomalies. Qualcomm entered the arena with an on-premise AI appliance suite, allowing enterprises to run generative models locally, reducing cloud inference costs and preserving data sovereignty.

Differentiation now hinges on end-to-end platform cohesion: device firmware, operating system, virtualization, security policies, and AI workflows are being woven into unified offerings. Buyers weigh roadmap certainty, especially when licensing terms can shift abruptly after acquisitions. Trust in data-sovereignty controls and zero-day patch cadences are emerging as procurement deal-breakers alongside traditional cost and performance metrics.

End User Computing Industry Leaders

Genpact

Citrix Systems, Inc.

Vmware, Inc.

Fujitsu Ltd.

Hitachi

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Citrix acquired Unicon GmbH, integrating the eLux thin-client OS deployed on 2.5 million endpoints.

- June 2025: IGEL bought Stratodesk to deepen its secure endpoint OS expertise

- June 2025: Omnissa expanded App Volumes to support physical PCs, targeting 95% of the global PC installed base.

- March 2025: Omnissa unveiled a three-tier partner program that rewards outcome-based projects over product reselling.

- January 2025: Qualcomm launched an on-premise AI Appliance Solution and Inference Suite for vertical-specific workflows.

Global End User Computing Market Report Scope

End-user computing (EUC) encompasses user access to enterprise applications and data anywhere, anytime, using one or more devices to access virtual desktop infrastructure (VDI) located either at the enterprise's premises or in the public cloud.

The end-user computing market is segmented by type (solution [virtual desktop infrastructure, device management, and other solutions], and services), organization size (large enterprises and small & medium enterprises), deployment mode (on-premise and cloud), end-user industry (IT and telecom, banking, financial services, and insurance), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Solutions | Virtual Desktop Infrastructure |

| Device Management | |

| Unified Communication | |

| Software Asset Management | |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| On-Premise |

| Cloud |

| Hybrid |

| IT and Telecom |

| Banking, Financial Services and Insurance |

| Healthcare |

| Retail |

| Government |

| Education |

| Transportation and Logistics |

| Virtual Desktop Infrastructure |

| Desktop-as-a-Service |

| Cloud Workspaces |

| Enterprise Mobility Management |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| North Africa | |

| Rest of Africa |

| By Product Type | Solutions | Virtual Desktop Infrastructure |

| Device Management | ||

| Unified Communication | ||

| Software Asset Management | ||

| Services | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By End User Industry | IT and Telecom | |

| Banking, Financial Services and Insurance | ||

| Healthcare | ||

| Retail | ||

| Government | ||

| Education | ||

| Transportation and Logistics | ||

| By Delivery Model | Virtual Desktop Infrastructure | |

| Desktop-as-a-Service | ||

| Cloud Workspaces | ||

| Enterprise Mobility Management | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| North Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the End User Computing market in 2026?

The process instrumentation market size is valued at USD 14.47 billion in 2026.

What is driving the shift from VDI to Desktop-as-a-Service?

It stands at USD 14.47 billion and is projected to reach USD 23.2 billion by 2031.

What is driving the shift from VDI to Desktop-as-a-Service?

Organizations seek elastic scaling, lower upfront costs, and provider-managed security, pushing DaaS to a 10.12% CAGR through 2031.

Why is Asia Pacific leading adoption?

APAC firms post the highest digital-workplace maturity scores, aggressive 5G rollouts, and the fastest uptake of AI-enabled tools.

How will Windows 10 end-of-support affect spending?

The October 2025 deadline forces hardware refreshes and accelerates moves to cloud desktops that support Windows 11 without new PCs.

Which industry vertical is growing fastest?

Healthcare, expanding at a 9.97% CAGR as hospitals deploy virtual desktops to secure patient data and boost clinician mobility.

What role does AI play in modern EUC platforms?

AI copilots save around 10 hours per employee monthly, while on-device inference preserves data sovereignty and trims cloud costs.

Page last updated on: