Context Aware Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 78.94 Billion |

| Market Size (2031) | USD 134.62 Billion |

| Growth Rate (2026 - 2031) | 11.30% CAGR |

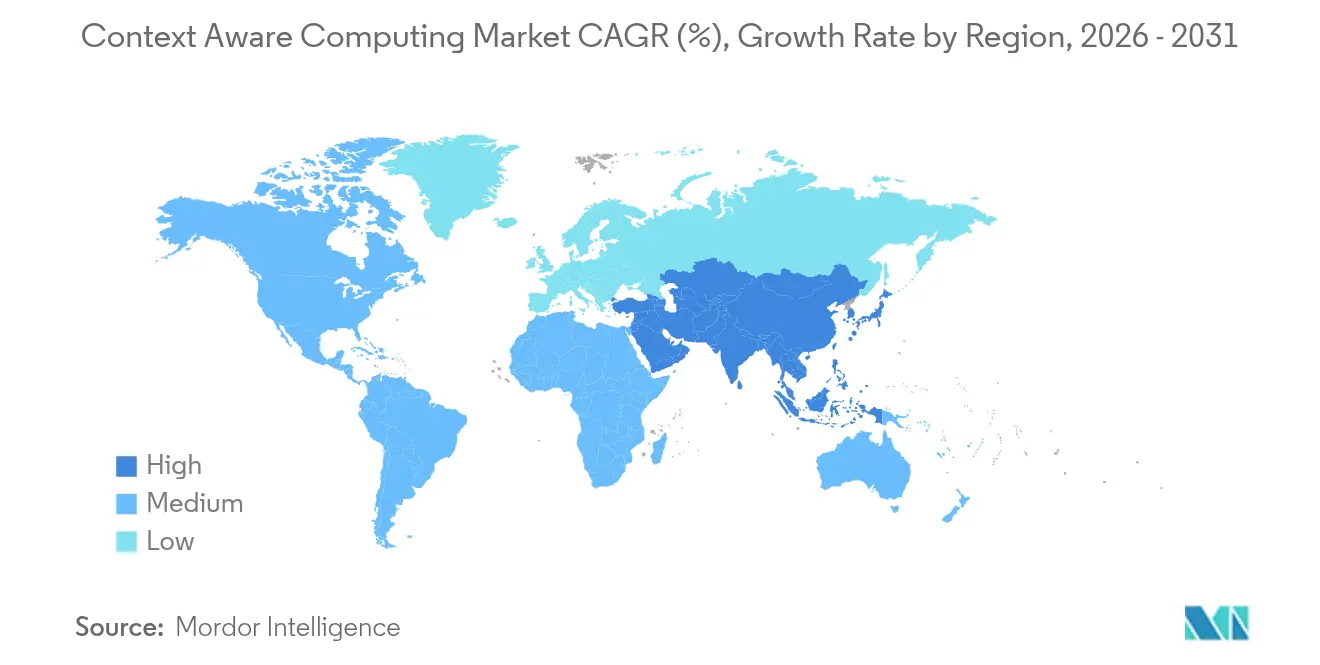

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

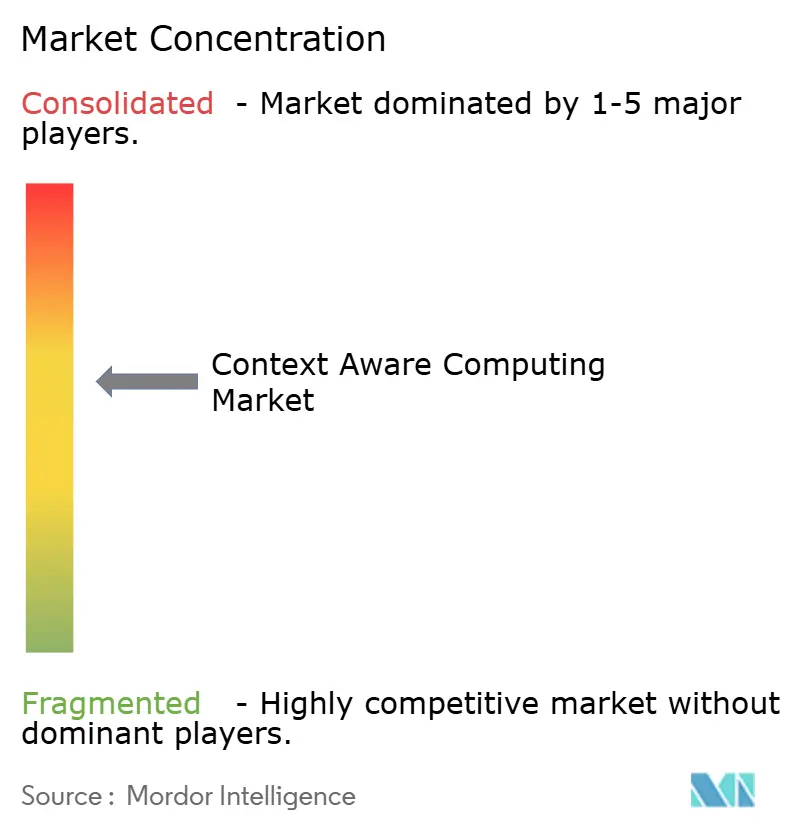

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Context Aware Computing Market Analysis by Mordor Intelligence

The context-aware computing market size is expected to grow from USD 70.94 billion in 2025 to USD 78.94 billion in 2026 and is forecast to reach USD 134.62 billion by 2031 at 11.30% CAGR over 2026-2031. This outlook reflects the structural shift from reactive digital experiences toward predictive, intent-driven services that anticipate a user’s needs before explicit input. Widespread deployment of AI inference engines, falling edge hardware costs, and nationwide 5G coverage now permit real-time contextual analytics on billions of endpoints. Demand intensifies as enterprises seek hyper-personalised engagement, operational efficiency, and privacy-first architectures that keep sensitive data local. Hardware remains the revenue backbone, yet software orchestration layers are becoming the main source of competitive differentiation in the context aware computing market.

Key Report Takeaways

- By component, hardware captured 51.40% of the context aware computing market share in 2025; software is projected to grow at a 12.67% CAGR through 2031.

- By vendor category, device manufacturers held 33.40% revenue share in 2025; online and social platforms are set to advance at a 13.77% CAGR to 2031.

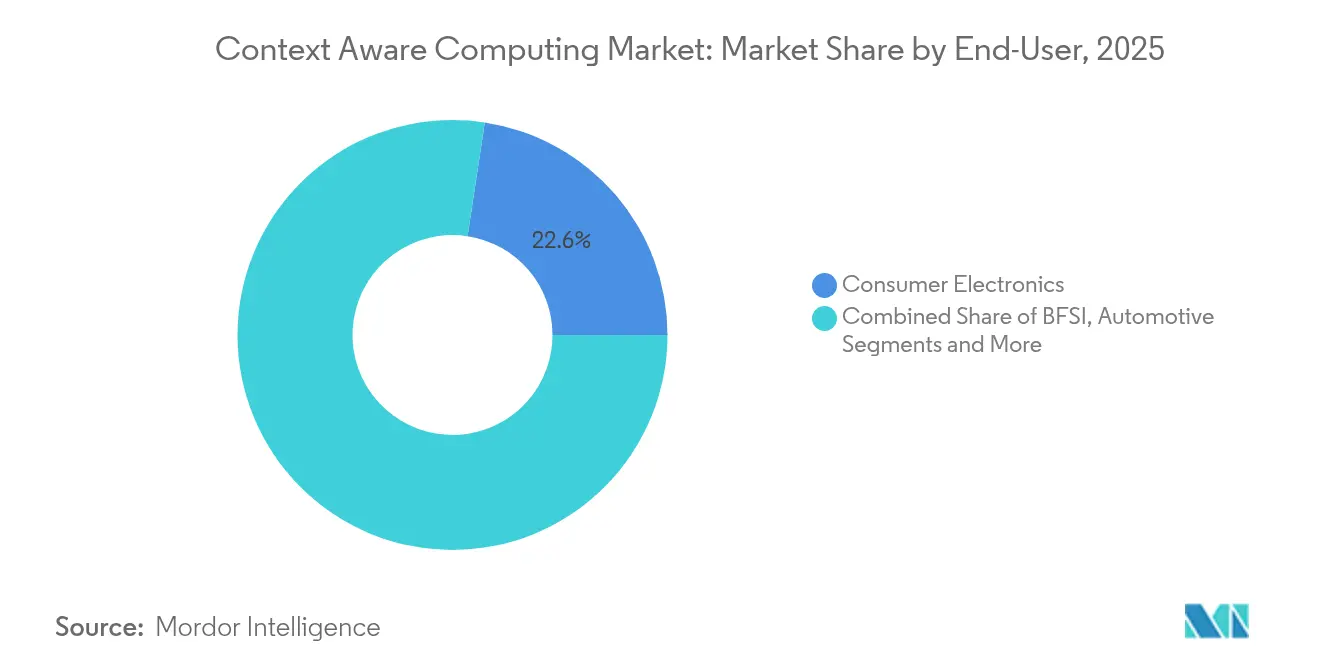

- By end-user sector, consumer electronics accounted for 22.60% of the context aware computing market size in 2025, while healthcare is expanding at a 13.12% CAGR toward 2031.

- By geography, North America dominated with 38.70% of the context aware computing market share in 2025; Asia-Pacific is forecast to rise at a 14.25% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Context Aware Computing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-powered intent prediction boosts UX | +2.4% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Edge-computing cost decline widens adoption | +2.1% | Global, concentrated in Asia-Pacific | Medium term (2-4 years) |

| 5G rollout enables real-time context data | +1.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Surge in IoT endpoints creates data deluge | +2.0% | Global, strongest in Asia-Pacific | Short term (≤ 2 years) |

| In-car infotainment personalisation demand | +0.9% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Context-as-a-Service APIs for SME apps | +1.1% | Global, early uptake in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-powered Intent Prediction Boosts UX

Large language models and machine-learning pipelines embedded in smartphones, vehicles, and retail kiosks now anticipate user goals, suggesting next actions or auto-completing tasks. Apple Intelligence analyses in-device behaviour, ambient conditions, and messaging style to curate prompts and automate workflows.[1]Apple, “Apple Intelligence Preview,” apple.com Organisations deploying comparable models gain higher user retention because experiences feel intuitive and effortless. Value scales rapidly because each interaction refines the model, reinforcing network effects. Capital expenditure on AI infrastructure is rising sharply, evidenced by Oracle’s USD 30 billion partnership with OpenAI focused on high-density GPU clusters. As predictive accuracy improves, consumers increasingly expect proactive services as a baseline capability in the context aware computing market.

Edge-computing Cost Decline Widens Adoption

Advanced 3 nm and 4 nm process nodes have reduced cost per tera-ops and improved performance-per-watt. Qualcomm’s latest Snapdragon platform embeds a dedicated NPU that supports multimodal context analysis on battery-powered devices, eliminating constant cloud calls.[2]Qualcomm, “Qualcomm Reports First Quarter Fiscal 2025 Results,” qualcomm.com Lower total ownership cost unlocks small and medium-enterprise deployment across smart retail shelving, factory automation, and field-service wearables. This broadening addressable base accelerates unit shipments of sensors and gateways, reinforcing demand in the context aware computing industry.

5G Rollout Enables Real-time Context Data

Ultra-reliable low-latency communications reduce round-trip delay to sub-10 milliseconds, making streamed contextual data actionable in real time. GSMA notes that Asia-Pacific operators have commercialised network slicing packages tailored for AR navigation, telemedicine, and industrial robotics.[3]GSMA, “The Mobile Economy Asia Pacific 2024,” gsma.com Enterprises are re-architecting from batch analytics toward streaming inference pipelines that exploit continuous context flows. The performance uplift expands the context aware computing market into scenarios once constrained by latency, including cooperative autonomous vehicles and immersive education services.

Surge in IoT Endpoints Creates Data Deluge

China counted 2.57 billion active IoT terminals by August 2024, a milestone illustrating the sheer scale of contextual signals now flowing from consumer and industrial assets. Hierarchical analytics that start with on-device filtering and escalate only relevant events to the cloud mitigate bandwidth strain. Vendors that deliver efficient sensor-level pre-processing gain traction because they allow customers to capture insight without incurring data-plane cost explosions.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Privacy-first regulations restrict data use | -1.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| High integration complexity with legacy IT | -1.2% | Global, most acute in large enterprises | Long term (≥ 4 years) |

| Model bias risks in context inference | -0.8% | Global | Medium term (2-4 years) |

| Limited battery life on wearable devices | -0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy-first Regulations Restrict Data Use

GDPR-style mandates require explicit consent, data minimisation, and erasure rights that curtail the unfettered data harvesting once common in mobile applications. Firms now pursue federated learning, differential privacy, and on-premises inference to comply, but these techniques often reduce model accuracy and slow roll-outs. Vendors able to deliver privacy-by-design frameworks gain a trust advantage yet must absorb higher engineering costs. The regulatory swing keeps some enterprises cautious, tempering the near-term growth of the context aware computing market.

High Integration Complexity with Legacy IT

Many enterprise resource planning and customer information systems were designed around static data structures and nightly batch processes. Integrating real-time context streams demands middleware, API gateways, and event-driven architectures that can strain budgets and skills. Transition projects progress in phases, delaying full benefit capture. Service providers that offer turnkey integration packages have an opening, but the friction still subtracts from the forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hardware Foundation Enables Software Innovation

Hardware held 51.40% revenue share in 2025 on the strength of sensors, edge gateways, and smart wearables that underpin inference workloads. Sensors for motion, biometrics, and environment represent the largest line-item because every contextual decision starts with precise data capture. Gateways aggregate this input and run first-pass analytics, shortening feedback loops in the context aware computing market. Meanwhile, software outpaces hardware growth at 12.67% CAGR through 2031. Context management middleware harmonises disparate streams, while analytics engines transform raw signals into predictive recommendations. Professional services revenue reflects the steep learning curve enterprises face when tuning data pipelines, security, and compliance. Managed services adoption rises as firms outsource daily operations to focus on business logic.

Software now determines end-user value creation. Middleware vendors bundle schema mapping, identity resolution, and policy enforcement, turning platform choice into a strategic decision. AI inference libraries optimise power draw by splitting workloads across CPU, GPU, and NPU resources. These technical breakthroughs let developers craft granular experiences—such as adaptive in-car infotainment—without rewriting code for every chipset. Resulting demand reinforces upstream sensor and gateway shipments, advancing the context aware computing market size for integrated solutions.

By Vendor: Online Platforms Drive Digital Transformation

Device manufacturers controlled 33.40% of 2025 revenue, leveraging tight coupling between proprietary sensors and companion software to lock in customers. Still, online and social platforms deliver the fastest growth at 13.77% CAGR because they already curate large behavioural datasets that fuel sharper context inference engines. Mobile network operators monetise connectivity by bundling edge computing services, ensuring deterministic performance for latency-sensitive workloads. Independent software vendors occupy niche verticals, offering domain-specific modules such as patient-monitoring dashboards or predictive maintenance toolkits.

Platform players shift toward end-to-end stacks that merge cloud, edge, device, and application layers. Partnerships like IBM’s USD 150 billion US investment—USD 30 billion of which funds advanced RandD—signal escalating entry barriers. Smaller vendors survive by focusing on geography- or domain-specific gaps, but many seek integration deals with larger partners that can carry the compliance and infrastructure burden.

By End-User Industry: Healthcare Leads Digital Health Revolution

Healthcare is set to grow at 13.12% CAGR, fuelled by continuous monitoring wearables, AI diagnostic aides, and telehealth workflows that incorporate patient context acquired from sensors, EHR systems, and ambient data. Early sepsis alerts, fall detection, and medication adherence nudges illustrate high-value outcomes now possible. Consumer electronics kept 22.60% revenue share in 2025 as smartphones, smart speakers, and AR glasses embed always-on context engines that simplify daily routines.

BFSI institutions employ behavioural analytics for fraud detection and hyper-personalised offers. Media firms use adaptive content stitching to raise engagement time. Automotive OEMs roll out occupant mood detection and predictive maintenance alerts that increase safety and brand loyalty. Logistics providers map temperature, location, and traffic context to adjust routes on the fly, optimising cost and service quality. These varied scenarios amplify demand across the context aware computing industry.

Geography Analysis

North America delivered 38.70% of global revenue in 2025, buoyed by robust venture investment, early 5G rollout, and cloud adoption. Enterprises in the United States deploy context-rich customer journeys to lift retention and cross-sell rates. Canada’s public-sector digital strategies add to base demand for privacy-centric deployments.

Asia-Pacific records the highest growth trajectory at 14.25% CAGR through 2031. National 5G coverage, device manufacturing hubs, and sizeable digital-native populations combine to expand the context aware computing market. China’s 2.57 billion IoT endpoints demonstrate the depth of contextual data available to local ecosystem players. Government stimulus for smart city, healthcare, and industrial upgrade projects further accelerates uptake.

Europe advances on differentiated priorities, balancing innovation with strict privacy law compliance. Vendors that integrate consent management and data localisation win enterprise contracts. The Middle East leverages smart-city megaprojects—such as NEOM in Saudi Arabia—to trial large-scale context platforms. Africa shows leapfrog potential because cloud-native mobile services offer practical solutions where legacy infrastructure is thin. South America’s steady smartphone adoption rounds out global demand, with telcos pushing edge computing nodes to support low-latency contextual apps.

Regulatory Landscape

Regulation for context-aware computing is tightening around privacy, transparency, and security controls for AI systems that infer intent from behavioral and ambient data. In the European Union, Regulation (EU) 2024/1689 (AI Act) formalizes risk-based obligations that elevate documentation and governance requirements for higher-risk deployments, reinforcing the shift to privacy-by-design and auditable context pipelines in regulated use cases.

In the United States, standards and procurement-driven requirements are becoming practical compliance anchors for vendors selling into government and critical sectors. NIST advanced this direction with its AI Agent Standards Initiative (February 2026) and related work on software and AI agent identity and authorization, while a June 2026 update process for a GSAR clause on safeguarding government data within LLM systems signals more explicit contractual controls over how contextual data is accessed, processed, and secured. In China, TC260 released Ethics-Safety Guidelines for Artificial Intelligence Applications 1.0 (May 2026), complementing existing cybersecurity and data protection regimes and increasing emphasis on safety and governance for AI-enabled context inference.

Competitive Landscape

The context aware computing market remains moderately fragmented, yet consolidation momentum is building. Tech giants pursue vertical integration to own sensors, silicon, operating systems, and cloud analytics, guaranteeing performance coherence and data control. Oracle’s USD 30 billion investment with OpenAI symbolizes the capital now required to build GPU clusters and foundation models tuned for contextual insight.

Competitive differentiation hinges on AI model accuracy, power efficiency, and security credentials. Companies invest in patented low-power inference architectures, federated learning toolkits, and quantum-safe cryptography to outpace rivals. Mid-tier vendors focus on niche verticals—such as precision agriculture or rail logistics—where domain momentum can offset scale disadvantages. Intellectual-property portfolios, ecosystem partnerships, and compliance frameworks form critical moats. As integrated stacks mature, switching costs rise, nudging buyers toward long-term platform commitments that elevate recurring revenue visibility for leading suppliers.

Context Aware Computing Industry Leaders

IBM Corporation

Microsoft Corporation

Google LLC

Amazon Web Services Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability and secure context delivery for agentic systems are becoming clearer areas of investment, as enterprises shift from single-app copilots to multi-system agents that need standardized access to governed data. Oracle's July 2025 launch of a Model Context Protocol (MCP) server for Oracle Databases points to ongoing demand for enterprise-grade connectors that let context-aware agents query and reason over operational data with controls, supporting opportunities for middleware vendors, database platforms, and systems integrators to package deployable context layers (identity, authorization, audit, and policy enforcement) across legacy IT estates.

Telecom and edge ecosystems also present an opportunity where context-aware policy execution can be embedded closer to users and devices. ETSI work in Experiential Networked Intelligence (ENI) and the ETSI NFV policy information model (including context mapping constructs) supports dynamic network behavior based on real-time context, aligning with 5G network slicing and low-latency use cases in AR navigation, telemedicine, and industrial automation. At the same time, foundational frameworks such as ITU-T Y.3043 and ongoing ISO/IEC JTC 1/SC 41 architecture work for IoT, edge, and cloud interoperability reinforce a standards-backed pathway for multi-vendor deployments, creating room for vendors that productize cross-domain context governance, standardized configuration export/import, and hybrid edge-plus-cloud inference architectures.

Recent Industry Developments

- May 2026: Torq completed its acquisition of Jit to add agentic risk contextualization using a Security Context Graph within its security automation platform. The combination grounds context-aware decisioning for security workflows in continuously updated environment and risk signals.

- February 2026: Snowflake and OpenAI announced a USD 200 million multi-year partnership to bring advanced OpenAI models into Snowflake Cortex AI for enterprise deployments. The partnership tightens integration between governed enterprise data and agentic AI, supporting context-aware applications that depend on controlled data access and centralized policy management.

- November 2024: Apple introduced Apple Intelligence, positioning on-device context processing as a core feature across iOS experiences. This accelerated vendor focus on privacy-first, local inference architectures that reduce continuous cloud calls while still enabling proactive, intent-driven user interactions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from solutions that sense, interpret, and act on real-world context (such as location, activity, time, and device conditions) to personalize or automate digital and physical experiences across consumer and enterprise use cases.

Scope exclusions: We exclude basic connectivity-only services and generic IT outsourcing that do not directly enable context detection, context processing, or context-driven application behavior.

Segmentation Overview

- By Type

- Hardware

- Sensors

- Edge Gateways

- Smart Wearables

- Software

- Context Management Middleware

- Analytics and Inference Engines

- Services

- Professional Services

- Managed Services

- Hardware

- By Vendor

- Device Manufacturers

- Mobile Network Operators

- Online and Social Platforms

- Independent Software Vendors

- By End-User Industry

- BFSI

- Consumer Electronics

- Media and Entertainment

- Automotive

- Healthcare

- Telecommunication

- Logistics and Transportation

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we first mapped the supply and demand signals behind context-aware computing adoption across regions. Public sources were used to anchor the model, such as IT and telecom indicators from the International Telecommunication Union, macro and digital-economy series from the World Bank, and enterprise ICT and security publications from agencies such as NIST. We also reviewed peer-reviewed papers and patents (through a patent database) to understand how fast sensing, edge inference, and context middleware features move into deployable products.

Next, we used company filings, earnings call transcripts, investor presentations, and product documentation to identify monetization patterns (licenses, usage-based software, hardware attach, and services). For cross-checks, we referred to reputable press, standards and developer ecosystem notes, and a paid company financials and intelligence subscription to keep revenue splits directionally consistent. These examples are not exhaustive, and additional public sources were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work tested what is actually being bought and deployed, then tightened desk assumptions that are often simplified in public sources. We spoke with a mix of solution providers, platform and device ecosystem participants, system integrators, and enterprise buyers across major regions, so pricing logic, deployment mix, and near-term demand constraints could be checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 18% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs spend from digital adoption and device intensity signals, then converts that demand pool into context-aware computing revenues using penetration and monetization assumptions by major end-use setting. In practice, we corroborated totals using selective bottom-up approximations, including sampled vendor revenue ranges, channel checks for solution rollouts, and a simple ASP times volume logic for common hardware and software bundles, which helped adjust for over-counting and locate gaps.

Key inputs for this market include smartphone and connected-device penetration, enterprise cloud and edge compute adoption, the share of apps and systems using location and sensor fusion, average software subscription levels for context engines, services attach rates in deployments, and the pace of privacy and consent requirements that can slow rollout timing. Forecasting was run using scenario analysis supported by trend-based smoothing on key drivers, where expert feedback set realistic ranges for pricing progression and adoption speed by region. When bottom-up references were incomplete, we handled gaps by using conservative attach and utilization assumptions, then re-checking them against independent demand indicators.

Data Validation & Update Cycle

Validation is done in several passes so the final number is not driven by one data stream. We compare outputs with independent signals like device shipments, enterprise IT spend direction, and software subscription growth patterns, then investigate large variances before sign-off. If an assumption moves outside an acceptable range, respondents are re-contacted and the model is rerun with the revised constraint.

Reports are refreshed annually, and interim updates are made when material events occur, such as sharp currency movements, major regulation changes, or step-changes in deployment economics. Before delivery, an analyst performs a fresh pass on market inputs and recent announcements so clients receive the latest updated view.

Mordor Intelligence's Context Aware Computing Market Size Compared Against Other Published Estimates

Published market values for context-aware computing can look far apart, even when the label is the same, because boundaries and timing choices differ. The spread usually comes from what gets counted as a context-aware solution versus a broader digital stack, and from how pricing and currency are handled across regions.

A refresh-led gap can be common in this market because subscription pricing, services attach, and regional currency conversion can shift totals quickly from one update cycle to the next. By re-checking ASP progression assumptions and applying consistent currency timing during the annual refresh, then doing targeted re-validation calls on outlier segments, the estimate stays more traceable to what is being deployed. This is the specific approach used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 78.94 B (2026) | |

| Industry Research Outlet A | USD 83.76 B (2025) | Uses a different base year and component split (solutions vs services), which can shift the implied mix and pricing, especially when currency conversion timing is not aligned to a single reference period. |

| Industry Research Outlet B | USD 64.20 B (2024) | Leans on an earlier base year with a faster pricing and adoption ramp, and the 2024 snapshot can understate the latest software and services monetization that expanded in subsequent cycles. |

Looking across the table, most of the difference is explained by base-year selection and how pricing and currency are treated when moving from one year to the next. When scope stays tight to context sensing, processing, and context-driven actions, and the price logic is refreshed and re-checked with practitioners, the result is a practical number that can be repeated and stress-tested as the market evolves.

Key Questions Answered in the Report

What is the current value of the context aware computing market?

The market stands at USD 78.94 billion in 2026 and is projected to grow to USD 134.62 billion by 2031.

Which component segment is growing fastest?

Software is the fastest-growing component, expanding at a 12.67% CAGR to 2031 as middleware and analytics drive differentiation.

Why is Asia-Pacific experiencing the highest growth?

Mass IoT deployments, accelerated 5G coverage, and supportive government programs position the region for a 14.25% CAGR.

How do privacy regulations affect adoption?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Context Aware Computing Market?

GDPR-style laws impose consent and minimisation requirements, compelling vendors to adopt federated learning and local processing, which adds cost and complexity.

What industries will benefit most from context aware computing?

Healthcare leads due to continuous monitoring and predictive analytics, while consumer electronics, BFSI, automotive, and logistics also gain efficiency and personalisation advantages.

Who are the leading players in this space?

Large tech firms such as Oracle, Apple, Qualcomm, IBM, and Cisco are setting the pace by integrating hardware and AI stacks to deliver real-time contextual intelligence

Page last updated on: